Abstract

Corporate social responsibility (CSR) is a popular research topic, but there have not been comprehensive discussions on CSR evaluation in the banking sector. The purpose of this study is to propose a two-stage analysis combining the modified Delphi method (MDM) and Analytic Network Process (ANP) in order to construct a model for evaluating banks’ CSR. First, we use MDM to select and determine the interdependence of the criteria and then employ ANP to obtain their weights and to rank the alternatives. The results show that 5 criteria and 18 sub-criteria need to be considered in CSR evaluation. The most important criterion and sub-criterion are bank governance and regulatory compliance, respectively. The evaluation model constructed herein can be taken as a decision-making guide for evaluating banking organizations’ CSR and to help promote CSR development in China’s financial industry.

Introduction

Corporate social responsibility (CSR) has become a source of competitive advantage for many corporations, including banks [1, 2]. Apart from its functionality, CSR is an important aspect of banks’ contribution to society. The global economy was severely hit, and financial risks increased due to the COVID-19 epidemic [3]. Therefore, CSR in banks is an important issue for corporate and academic research [4–6].

The term CSR provides a general framework for describing the responsible behavior and social engagement of corporations. However, it is still a problem to find a recognized definition of CSR, let alone CSR assessment. Nevertheless, its assessment is important not only for researchers to examine the relationship between different organizational variables and CSR, but also for stakeholders to use social responsibility information in their decision-making process [7].

The fulfillment of CSR has had a late start in China [8]. Despite the fact that China’s banking CSR has developed to a certain extent, its realization is ineffective. For example, there is no standardized basis for the compilation of banks’ social responsibility reports, any comparability of the reports is relatively poor, the disclosure of report contents varies in terms of the level of detail, and there is a certain degree of subjectivity and one-sidedness [9–11] to the report. Thus, stakeholders have no way to refer to them for a proper and in-depth understanding of banking CSR in China.

In studies on CSR fulfillment in the banking sector [12–14], economic, social, environmental, and management dimensions have been used to measure the social responsibility of banks respectively [15–19]. However, apart from a few attempts, there has not been a comprehensive discussion on CSR fulfillment in the banking sector. Nevertheless, all stakeholders may be interested in knowing the extent of CSR performance in different banks. Therefore, CSR evaluation for the banking sector is needed to address this issue and fill the gap in the literature.

Evaluating banks’ CSR is a complex multi-criteria decision-making (MCDM) problem [20]. Moreover, the requirements for fulfilling CSR are driven by internal and external environments of the enterprise [21], and there are conflicting and interdependent or feedback relationships between different evaluation criteria and sub-criteria [22]. In this regard, the problems may be oversimplified if the assumption of independence is used, thus leading to deviations in evaluation results that may affect decision-making quality.

The modified Delphi method (MDM) is a structured strategy for obtaining feedback from a large number of experts or stakeholders. It seeks to achieve consensus or convergence of views by iteratively collecting and refining expert evaluations. MDM is very useful at improving the fairness and comprehensiveness of the decision-making process in the context of MCDM [23]. Analytic Network Process (ANP) is a decision-making technique that extends the analysis of hierarchy process (AHP). Although AHP has become a popular application for evaluation models, each individual criterion is assumed to be independent. ANP is a method that can calculate the weights of evaluation criteria when they have dependency and feedback relationships and is a method widely used in solving MCDM problems [24]. Therefore, the goal of this study is to provide a robust and comprehensive decision-making framework using MDM-ANP, which is a hybrid MCDM concept that takes into account the complex standard relationships and expert opinions.

To the best of the authors’ knowledge, this is the first study to evaluate CSR in the banking sector by combining MDM and ANP techniques in order to achieve the following research objectives. Construct a system for evaluating CSR in the banking industry based on the fact that MDM can be used to pool expert opinions and reach a consensus. Integrate experts’ consensus and use ANP to analyze the weights of CSR dimensions and indicators in the banking sector. Apply ANP to evaluate and rank the banking industry’s CSR. Fill in the gaps in the research of CSR in the banking industry, so as to provide relevant decision-making suggestions for CSR in this industry.

The rest of the paper runs as follows. Section 2 provides a literature review. Section 3 introduces the methodology used in this study, including the construction of MDM, ANP, and bank CSR evaluation models. Section 4 empirically analyzes the construction of the CSR model for banks and the give sensitivity analysis. Section 5 presents research findings and a discussion. Lastly, the paper offers a conclusion and suggestions.

Literature review

Corporate social responsibility (CSR)

With changes in the economy, society, and environment, the concept of CSR evolving as well closely relates to sustainability and environmental, social, and governance (ESG) [25–27]. In other words, CSR is a multidimensional concept that is conducive to the realization of sustainable development. Specifically, CSR refers to the fact that enterprises, while generating profits and assuming legal responsibilities to shareholders and employees, should also pay attention to their responsibilities to consumers, communities, and the environment, emphasizing their concern for human values in the production process and their contributions to the environment, consumers, and society [15, 29]. Therefore, it is not enough for a company to just pursue profitability and assume legal responsibility for its shareholders and employees. CSR practices also require it to assume responsibility for consumers, communities, and the environment.

Compared with other industries, banking is a typical profit-oriented capitalist activity [30]. As the most important financial institutions, banks shoulder the important social responsibility of serving the real economy and maintaining financial stability [4]. Therefore, every bank must safeguard its stakeholders, social structure, and natural environment [31]. The number of scientific journals and publications interested in CSR evaluation in the banking sector has grown over the past five or six years [32]. CSR has since become an important issue in the banking sector. Moreover, the scale of CSR activities in banks is increasing, and how to measure and evaluate CSR in banks has become particularly important.

Evaluation criteria for CSR practices in banking

CSR research in the banking industry is very extensive, with many scholars focusing on the factors that affect it in banks. For example, Yeung points out that understanding the complexity of financial services and risk management, strengthening ethical practices in banking, implementing strategies to cope with financial crises, protecting customers’ rights, and establishing channels for customer complaints are all key elements of CSR in the banking industry [33]. Board size and CEO duality positively influence CSR in banks [34–36], However, an increase in the number of independent directors on the board will result in a lower level of CSR development [37]. A bank is committed to creating greater social contributions in the areas of corporate governance and philanthropy [38]. In addition, green finance has a positive impact on its CSR [39]. Employee experience, job position, and the number of CSR training programs all affect how bank employees perceive the aspects of CSR that the bank should focus on, which in turn impact its CSR performance [40].

Although there are many studies on the factors affecting CSR in banks, relatively few have been conducted to evaluate CSR in banks. From the literature, we find that scholars mainly measure bank CSR from the stakeholder perspective – i.e., shareholders, customers, employees, environment, and society. For example, Wang et al. measure bank CSR in terms of employees, customers, society and community, shareholders, and ethical and legal compliance. Using PLS-SEM, they confirm that green finance has a facilitating effect on the improvement of CSR in banks [39].

Zafar and Sulaiman construct a model for evaluating Islamic banks’ CSR using shariah governance, employee, community, customer, and environment as the evaluation criteria and apply AHP to find the weights of said criteria [41]. Based on stakeholder theory, Fatma et al. obtain scale items through qualitative research and literature review, establishing a measure of CSR activities in the India banking sector for customer, employee, shareholder, environment, and society [12]. Kilic measures the social responsibility of Turkish banks using four criteria: environment and energy, human resources, products and customers, and community involvement [13]. Esteban-Sanchez et al. assess the social responsibility of banks in terms of corporate governance, relationship with employees, relationship with the community, and products [14].

Aside from stakeholders, there are scholars who use the “Triple Bottom Line Concept” as a theoretical basis to measure banks’ CSR in terms of economic, environmental, social, legal, ethical, and philanthropic responsibilities. For example, Aggarwal and Saxena measure Indian banks’ CSR in terms of economic, ethical, environmental, and philanthropic responsibilities [15]. Franzoni and Allali calculate Islamic financial institutions’ CSR in terms of economic responsibility, discretional responsibility, ethical responsibility, legal responsibility, and religious responsibility [18]. Paulík et al. measure CSR in terms of economic, social responsibility, and environmental dimensions and analyze the relationship between CSR and financial performance of commercial banks [17].

Deng proposes three main CSR criteria in the commercial banking context: the economy, society, and environment. She then uses AHP to determine weights and to establish a relevant evaluation index system [16]. Wu and Yuan construct a CSR model for use in Chinese commercial banks based on the four standards of management responsibility, economic responsibility, social responsibility, and environmental responsibility. They then apply AHP to assign weights to the evaluation indicators [19].

Summarizing the literature, there are many factors affecting CSR in banks, but studies on its evaluation in the banking sector have not focused on all “Triple Bottom Line Concepts”. Many authors limit their discussion to only a few assessment factors and do not consider the full range of assessment factors. Therefore, through the literature this study initially compiles 6 criteria and 25 sub-criteria for assessing CSR in banks, including bank governance, economic responsibility, green development, social responsibility, responsibility management, and public welfare actions. Table 1 lists the operational definitions of the criteria and sub-criteria.

Operational definitions of criteria and sub-criteria

Operational definitions of criteria and sub-criteria

The models constructed by other scholars not only fail to consider that there is interdependence or feedback between different evaluation criteria and between evaluation sub-criteria, but also fail to assess and rank CSR performance of the banking sector. Therefore, this study adopts a two-stage analytical approach that combines MDM and ANP to construct a model for evaluating banks’ CSR.

There are four major shortcomings in CSR studies. First, they focus on the factors that affect CSR in banks. Second, many authors limit their discussion to a few assessment factors without considering the full range of them. Third, they do not consider the interdependence of different assessment criteria. Lastly, they do not assess and rank the CSR performance of the banking sector.

To the best of the authors’ knowledge, this is the first time that a two-stage analysis combining MDM and ANP is used to construct a model for evaluating banks’ CSR. First, through the literature this study initially compiles 6 criteria and 25 sub-criteria for assessing banks’ CSR. Second, using MDM, experts’ opinions can be pooled and a consensus could be reached in order to calculate a CSR evaluation system for the banking sector. By integrating the experts’ consensus, ANP can be used to analyze the weights of the CSR dimensions and indicators of the banking industry. Finally, ANP is applied to evaluate and rank the banking sector’s CSR and to conduct sensitivity analysis of the three alternatives. The methodology of this study is described in Section 3.

Methodology

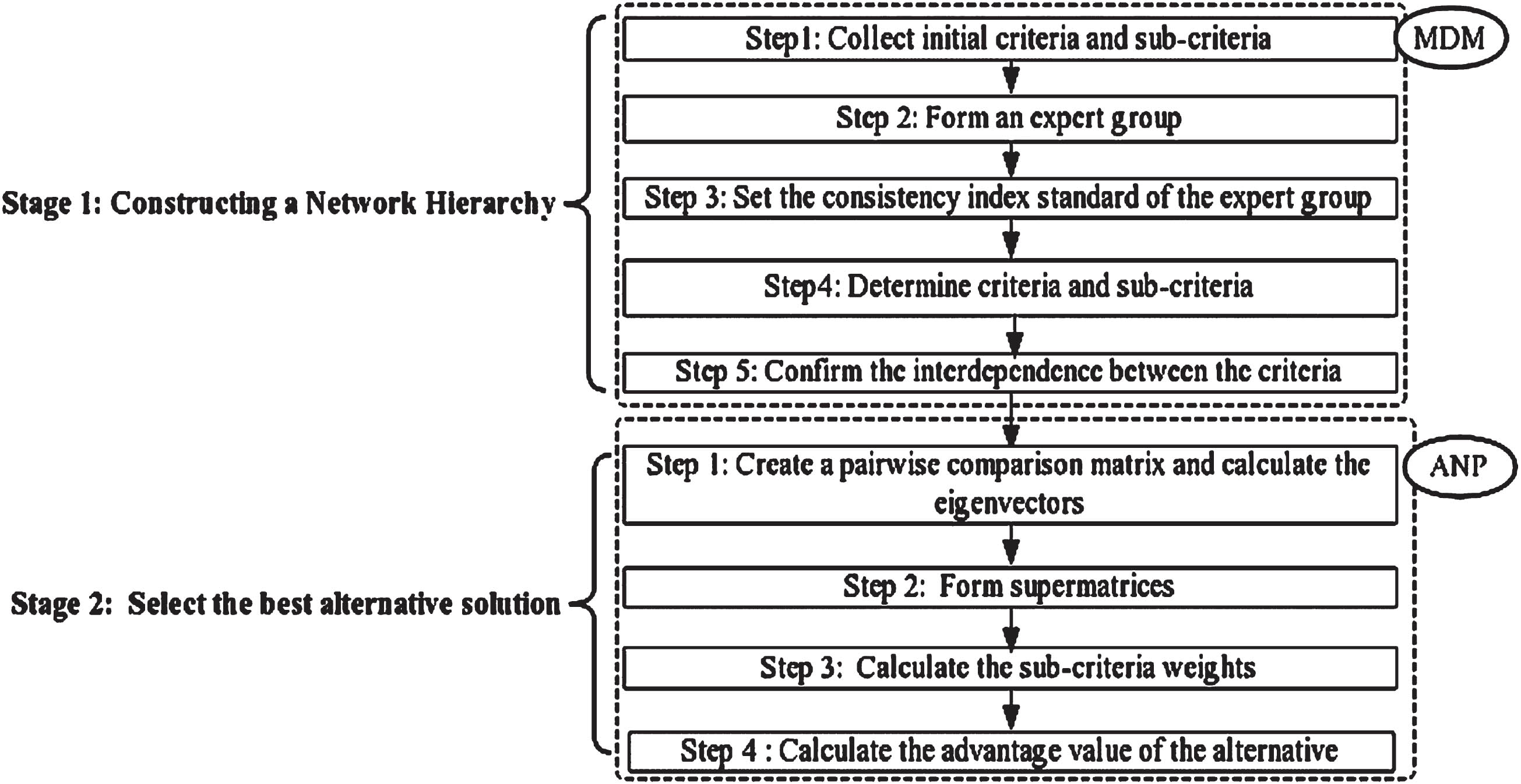

This study employs a two-stage analysis method in which both MDM and ANP are used to construct a CSR evaluation model for banks. In the first stage, the network hierarchical structure is formed, followed by the use of MDM to determine the CSR evaluation criteria and sub-criteria and then to determine the state of interdependence between these criteria. In the second stage, the ANP method helps select the best alternatives.

Figure 1 illustrates the structure of the evaluation model. Although the combined MDM and ANP approach has been applied in different research areas to solve MCDM problems in different domains (see Table 2), such a combination has not been previously used to construct a CSR evaluation system for the banking industry, thus filling the gap in the literature. The two approaches are described separately below.

Two-stage evaluation model of banks’ corporate social responsibility.

Research that combines MDM and ANP

Originally proposed by American RAND Corporation, MDM is designed to address the shortcomings of face-to-face communication and discussions in expert meetings. Since the traditional Delphi method is time consuming and difficult to control, expert opinions are prone to inconsistencies in the implementation process. MDM replaces the practice of taking measurements with open questionnaires in favor of structured questionnaires based on the relevant literature. Researchers can therefore save considerable time and focus on research topics [23].

The advantages of MDM such as simplicity, speed, and no need for multiple rounds of expert discussion mean that all experts’ opinions can be included in one survey, enabling them to reach a consensus and improving questionnaire recall [58]. Thus, MDM has been utilized in many research areas (see Table 2). The method can be used to construct a network hierarchy for assessing social responsibility in banks.

The steps to construct the network hierarchy using the modified form of the MDM are as follows. 1) Organize the starting criteria and sub-criteria through a literature review and form a decision-making group with more than 10 experts. 2) Questionnaires and surveys are designed to set the criteria for expert agreement and to determine the criteria and sub-criteria. 3) The dependence of the criteria on each other is determined.

Analytic network process (ANP)

The ANP method proposed by Saaty is an extension of the AHP method and is for calculating the weights of evaluation criteria when the criteria have dependency and feedback relationships [62]. ANP is one of the most widely-used MCDM methods to solve various problems in the real world, especially in the field of business and financial management, and has been applied to many other fields [24, 63]. ANP as a methodology not only provides a hierarchical structure, but also takes into account the relationships between the criteria, leading to more reliable results [64]. Previously constructed models of CSR in banks mostly use the AHP approach and do not take into account the interdependence between criteria and sub-criteria. According to the results of the first-round questionnaires from experts, there is dependency between the criteria and sub-criteria for assessing CSR in banks. Therefore, ANP is suitable for determining the weights of bank CSR assessment criteria and the choice of alternative options. The ANP method consists of the four following steps.

Step 1: Establish a pairwise comparison matrix and calculate the eigenvector.

According to the network hierarchy and with the help of questionnaire surveys, experts in the decision-making group judged the relative importance of the elements according to the hierarchical structure and Saaty’s nine scales [65]. After integrating their judgment preferences, we obtain a paired comparison matrix A with the largest eigenvalue of A performing the consistency test. If the consistency ratio satisfies 0≤CR≤0.1, then the experts’ judgments are consistent. The calculation formula is:

Here, A is the pairwise comparison matrix, W is the eigenvector, and λmax is the maximum eigenvalue of A.

Step 2: Form the supermatrix.

The calculation process of ANP includes an unweighted supermatrix, weighted supermatrix, and extreme supermatrix. The unweighted supermatrix contains the weights obtained from the original paired comparison matrix. However, the values in the matrix may not conform to the column-stochastic principle. The relevant community weight factors multiply the weights of the same criterion in the unweighted supermatrix to obtain the weighted supermatrix. Multiplying the weighted supermatrix to convergence brings about a limitingsupermatrix.

We take the example of a supermatrix composed of a three-level hierarchy. If there is dependency between the evaluation criteria, then the unweighted supermatrix is W, as shown in formula (2) [62].

Here, W21 represents the eigenvector weight value of the criterion under the decision objective. W32 represents the eigenvector weight value that the paired comparison matrix forms between the third-level elements under the evaluation criterion of the second-level elements. W22 and W33 represent the corresponding weight values of the dependency relationships between the criteria.

The unweighted supermatrix W is normalized, such that the sum of the weights of each column equals one so as to conform to the mathematical inference logic. The supermatrix is the weighted supermatrix W’, as shown by:

Step 3: Select the best alternative.

The weighted supermatrix W′ is multiplied by the power of 2K + 1, K⟶ ∞, to obtain the limiting supermatrix WANP, as shown below.

Step 4: Calculate the advantage value of the alternative.

Under different sub-criteria, after obtaining the advantage value of alternative schemes and combined with formula (4), the comprehensive evaluation value of each alternative scheme can be obtained. The result is taken as the basis for ranking each alternative scheme.

Using MDM to construct the network hierarchical structure

This study adopts MDM to conduct expert consultations aimed at vetting 6 criteria and 25 sub-criteria that are deemed to influence CSR, as summarized in the literature. This process is specifically aimed at identifying key factors that affect CSR evaluations in Chinese banks. As Parente and Anderson suggest, there is no upper limit to the number of experts needed for MDM, but at least 10 should be included [66]. This study recruited a group of 35 experts with affiliations in the banking industry, government, and academia. Their working locations include banks, universities, the China Banking Regulatory Commission, and People’s Bank of China, with an average of 21.8 years of relevant working experience. Table 3 provides their specific background information.

Statistics regarding the experts

Statistics regarding the experts

For the convenience of the participants, the survey was conducted by sending out questionnaires through WeChat and e-mails as well as by interviews. The first-round survey focused on the importance of the evaluation criteria and sub-criteria on a scale of 1 to 5 (1 meaning unimportant, 5 meaning very important) and entailed the use of Faherty’s quartile [67]. Standards for consistency when soliciting and evaluating expert opinions should be set. If the interquartile range of the expert group’s opinion on a given item is less than or equal to 0.50 and Likert’s assessment of importance is less than 4.00, then the opinion is deemed unanimous, and the item is deleted. We vet the results from the first-round questionnaires by deleting criteria that did not reach consistency, thus obtaining 5 main criteria and 18 sub-criteria (Table 4).

Statistics regarding consensus among the expert panel

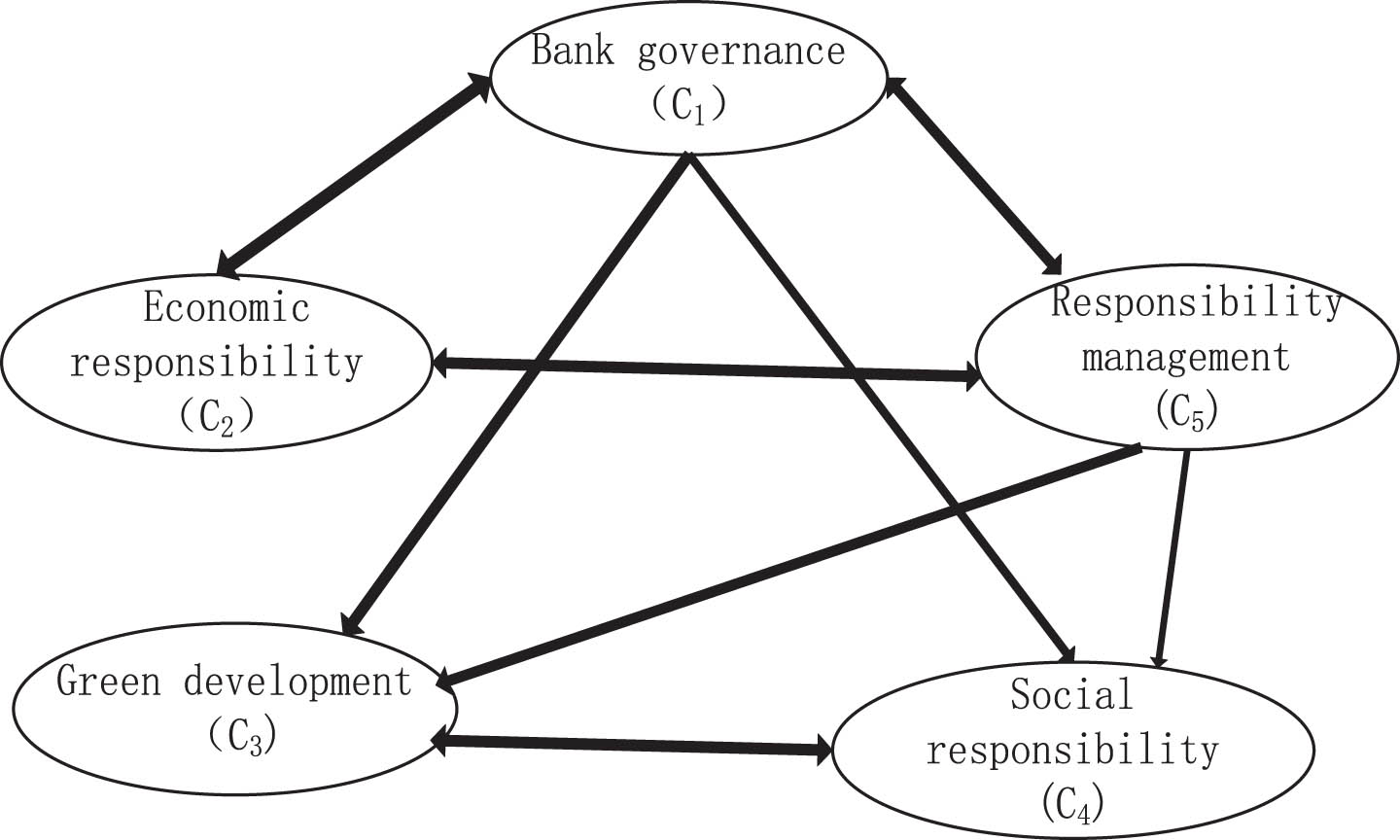

Based on feedback from the expert group, the charitable activities’ sub-criteria are adjusted to the social responsibility criteria to determine the key factors affecting CSR for banks. In the second-round survey, we use a Likert scale to evaluate interdependence between the criteria, with scores ranging from 0 to 4 (0 means no influence, 4 means very strong influence). After assessing the results, a hierarchical structure diagram of the inter-criteria interdependence and banks’ CSR assessment is constructed, as shown in Fig. 2.

Interdependence among the criteria for evaluating bank CSR.

Because large state-owned commercial banks have wide and diversified business coverage, represent the strongest capital and strength in China’s financial sector, and have published social responsibility reports for more than 10 consecutive years, we select three of them as alternatives. The three banks selected are all wholly state-owned commercial banks that are significantly more profitable than policy banks. Second, these three banks are characterized by huge capital, wide business coverage, a large number of branches, and the largest customer base. They have been ranked in the top 20 of the world’s top 100 banks for at least two out of the last three years. Third, there has been no comparison of CSR of these three banks in the past. In sum, the network-level structure diagram ultimately consists of 5 main criteria and 18 sub-criteria, as shown in Fig. 3.

ANP infrastructure for construction and application of the CSR evaluation model in banks. indicates interdependence between criteria.

According to the network hierarchy structure diagram constructed in the first stage, the criteria and sub-criteria are compared in pairs. Thus, a pairwise comparison matrix is established. Following this, the third-round survey was conducted. Calculations return the maximum eigenvalue and corresponding eigenvector of the sub-matrix W21 pairwise comparison matrix from formula (1) and Super Decision (λmax=5.024 and eigenvector = 0.341, 0.253, 0.135, 0.134, 0.137, respectively). Moreover, CI = 0.006 and CR = 0.005 both satisfy the consistency test. Similarly, sub-matrices W22, W32, and W33 are obtained. All satisfy the consistency test. We obtain the unweighted supermatrix W by integrating the sub-matrices W21, W22, W32, and W33 via formula (2). In this study, 0.5 weights are given to sub-matrices W22 and W32, thus producing weighted supermatrix W′.

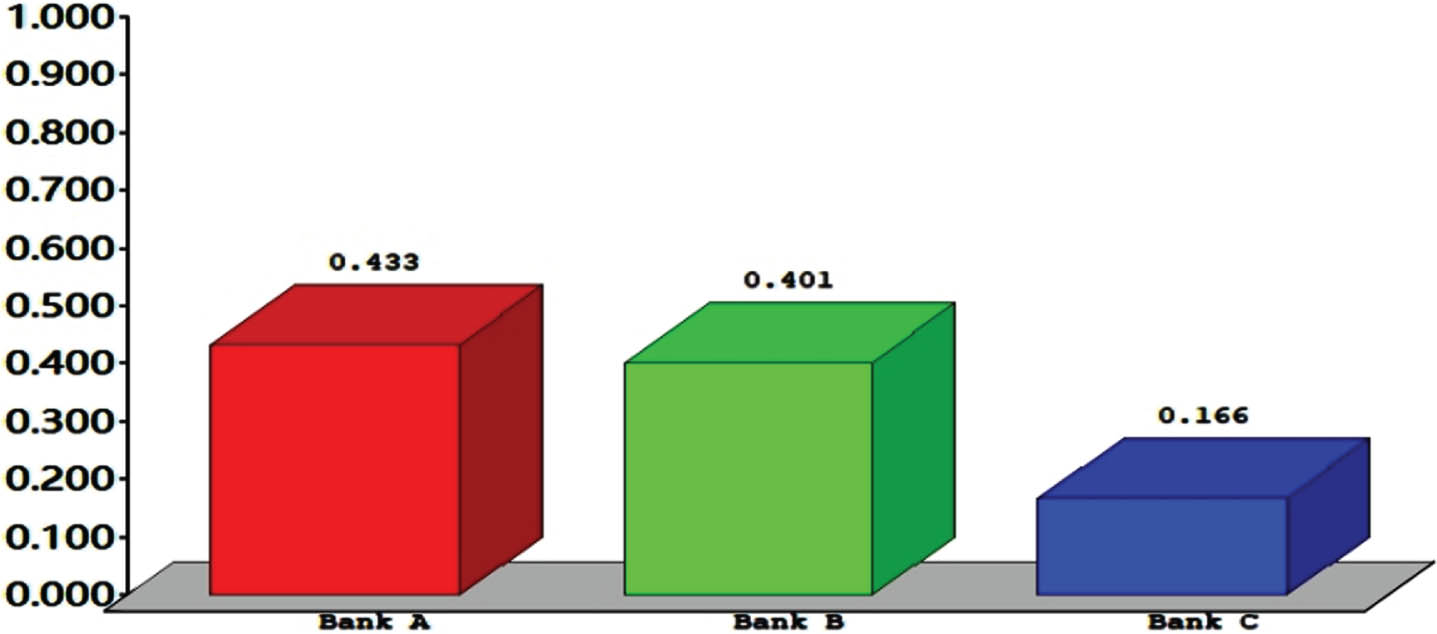

According to formula (4), the supermatrix W′ is also subjected to the limit process to obtain the limit supermatrix WANP. The overall weight of each evaluation criterion is then obtained. Finally, under different sub-criteria, the advantage values of the three alternative schemes are calculated, as shown in Table 5.

Results from experts

Results from experts

As mentioned earlier, this study selects three large state-owned commercial banks in China as case studies. The respective advantage vectors appear in Table 9. The CSR values are: Bank A (0.433), Bank B (0.401), and Bank C (0.166). In other words, Bank A has better CSR than Bank B, which has better CSR than Bank C.

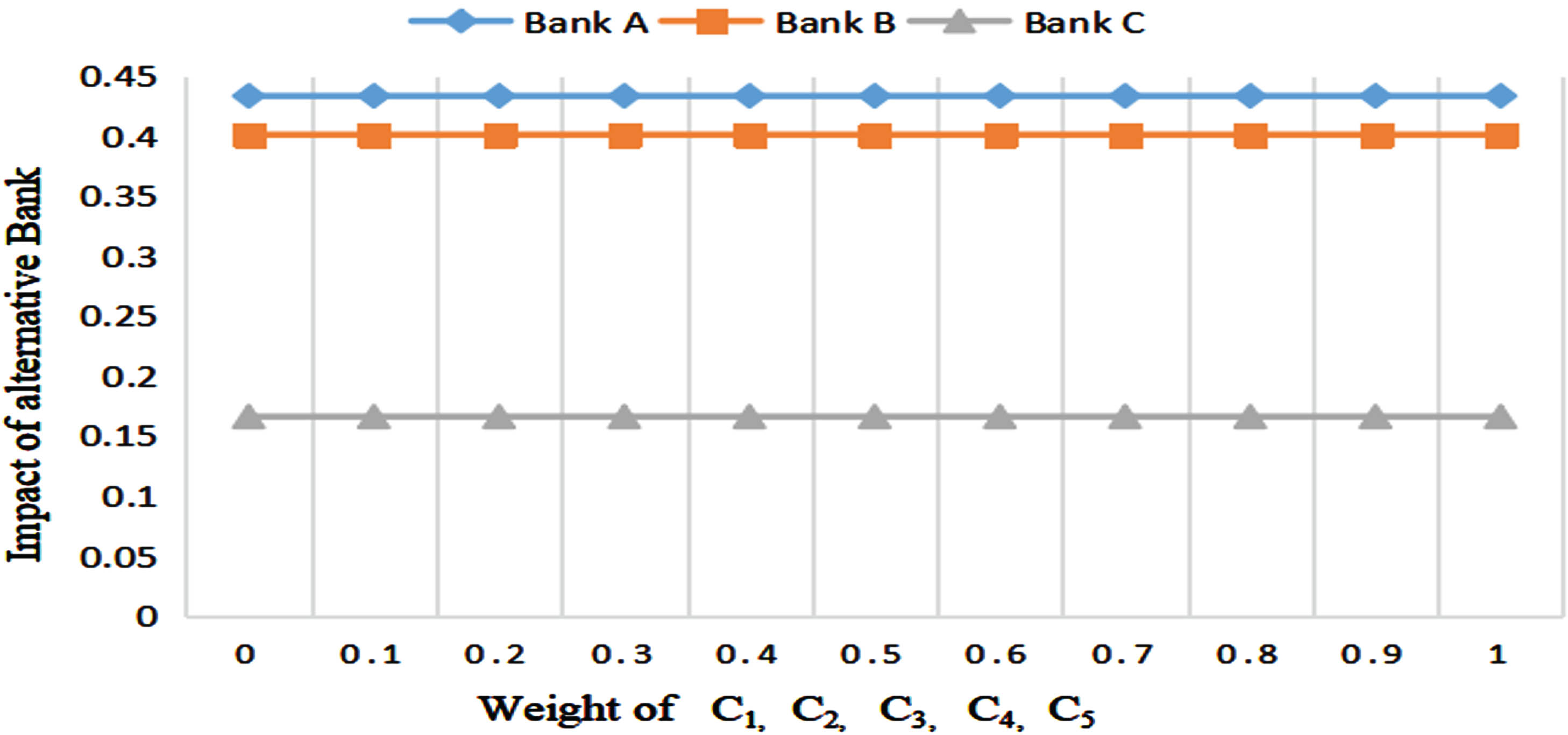

To verify the stability of the CSR evaluation model constructed herein, an overall sensitivity analysis is conducted on the three investigated banks. Regardless of the weights of the 5 evaluation criteria of bank governance, economic responsibility, green development, social responsibility, and management responsibility, the alternative plan does not vary under changes in their parameters. This verifies that the constructed model is very stable, as shown in Fig. 4.

Sensitivity tests of criteria.

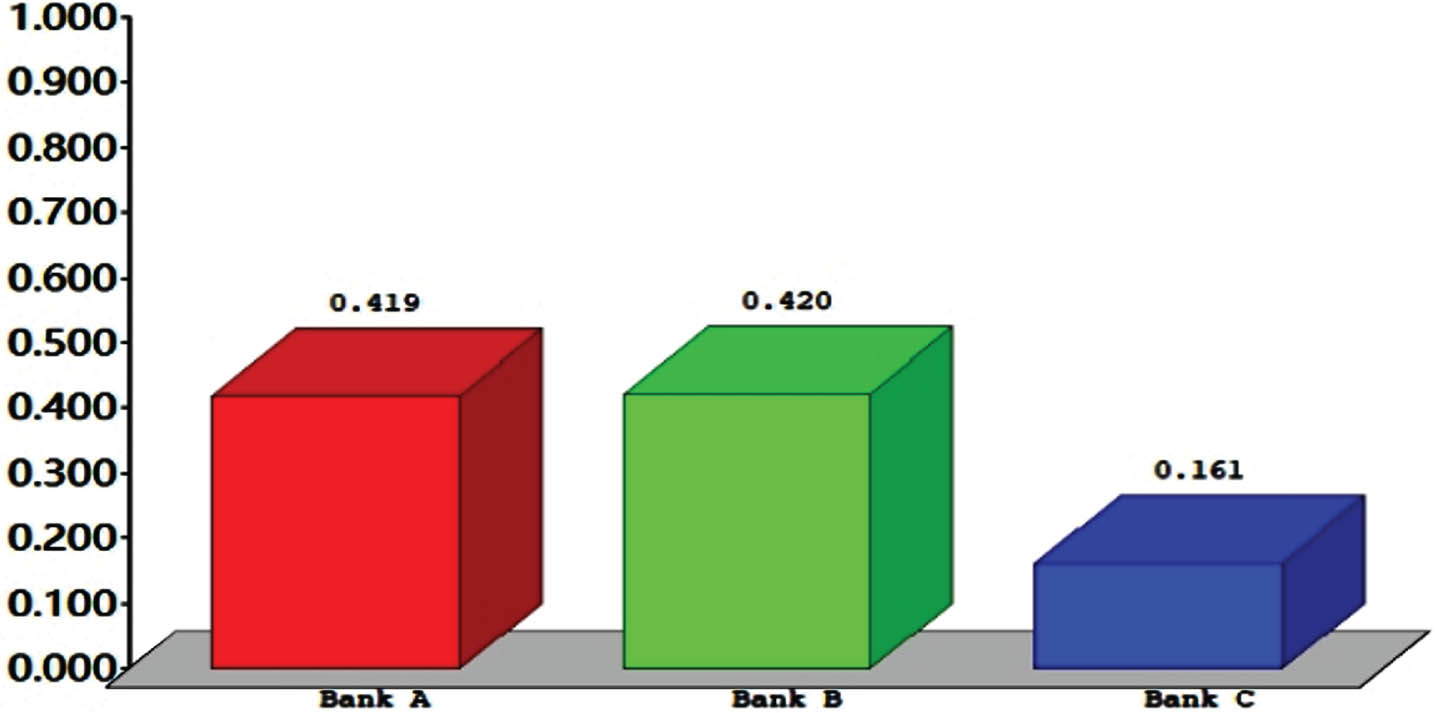

Figure 5 shows the comprehensive evaluation values for CSR in all three banks under the original evaluation framework. Their rankings are: Bank A (0.433), Bank B (0.401), and Bank C (0.166). After adjusting Bank B’s weight parameter from 0.509 to 0.510, the comprehensive evaluation values shown in Fig. 6 are: Bank B (0.420), Bank A (0.419), and Bank C (0.161). The order of alternatives has changed. This means that the model ensures flexible decision-making when a supervisory department evaluates CSR.

Ranking of three alternative solutions within the original bank CSR framework.

Ranking of three alternative solutions when the weight of Bank B is adjusted 0.509 to 0.510.

This study constructs a new CSR evaluation model for use in the banking industry. As detailed earlier, MDM determines the main evaluation criteria, sub-criteria, and hierarchical structure (see Figs. 2 and 3), identifying 5 criteria and 18 sub-criteria (see Table 1). There is a dependency relationship between them, echoing other studies that state banks’ CSR is a complex issue, and that there is interdependency between the different evaluation criteria and evaluation sub-criteria, forming interdependent or feedback relationships [21, 69]. In addition to the three criteria of economic, social, and management, two additional criteria of bank governance and green development are added. The model constructed is more in line with the evaluation of banks’ CSR. CSR in banks is a MCDM issue, and bank managers should fully consider the importance of each criterion and how interdependent they are when making relevant decisions to ensure that their banks can better fulfill social responsibility.

Based on the third-round survey, we use super decision software to obtain the weights of the main evaluation criteria and sub-criteria. In descending order of importance, the main criteria are bank governance (0.341), economic responsibility (0.253), responsibility management (0.137), green development (0.135), and social responsibility (0.134). Of the 18 critical evaluation sub-criteria, the 5 most important include regulatory compliance (0.095), risk control (0.076), responsible governance (0.070), executives’ compensation and characteristics (0.065), and customers (0.063). In other words, bank governance (C1) is the most important main criterion, and banks should continuously improve their corporate governance structure to provide assurance that they fulfill their social responsibility. This echoes Hu et al.’s study that corporate governance is the most important factor affecting CSR [42].

A high-level corporate governance structure provides the means for CSR and helps to safeguard shareholders’ interests and to ensure the fulfillment of social responsibilities [70]. When banks are more active in corporate governance, they tend to incur higher CSR expenditures, which in turn create greater social value [38]. Therefore, banks should continue to improve their corporate governance structure to provide assurance that they are fulfilling their social responsibilities.

Regulatory compliance (C51) is the most important sub-criterion. This is consistent with the development model used for banks with Chinese characteristics, in which China’s banking industry attaches importance to strict supervision based on legal mandates [71]. Legitimacy has become one of the most critical issues for businesses [31], advocating for more compliance of banks with corporate laws and regulations and contributing greatly to CSR, which in turn increases stakeholder loyalty and improves bank efficiency [72]. The current external environment is complex and volatile, and the environment in which the banking industry operates has undergone profound changes. Therefore, banks should strictly comply with regulatory requirements to operate various businesses, continuously improve their risk control capabilities, and ensure the stable development of various businesses.

This study employs two-stage analysis to construct a new CSR evaluation model for use in the banking industry. Based on subsequent analysis involving three state-owned commercial banks in China, the model can effectively evaluate how well CSR is implemented. In this regard, Bank A exhibits better CSR than Bank B, which has better CSR than Bank C (Table 5). Bank A performs best overall, especially in the economic contribution criterion, but needs further improvement in the areas of executive characteristics and compensation, green development, and innovation.

Banks A and B both perform poorly in the financial inclusion criterion compared to other criteria, suggesting that both banks need to further increase financial inclusion. Bank C is clearly inferior to Banks A and B, which means that Bank C is not in a good position to fulfill its social responsibility in the whole industry, especially in terms of risk control, economic condition, and economic contribution under the financial responsibility standard, and there is still much room for improvement. Bank C needs to actively promote the integration of social responsibility management into its development strategy, learn from the good practices of other banks, and continuously improve the level of social responsibility management to help the sustainable development of economy, society, and environment.

Sensitivity analysis shows that none of the alternatives would vary with changes in the parameters of the 5 evaluation criteria, thus verifying high stability (Fig. 4). After considering sensitivity analysis of the three banks, the ranking of alternatives changes (Figs. 5 and 6). Supervisory authorities can employ these to ensure flexible decision-making practices when assessing CSR in the banking context.

Conclusion and suggestions

CSR is one of the most important issues for financial enterprises. How banks fulfill their CSR is of great significance to the sustainable development of China’s economy and the maintenance of social stability.

To facilitate this process, this study employs a two-stage analysis method to construct a new CSR evaluation model, thus providing a set of criteria for measuring and evaluating relevant practices in China’s banking industry. Such an evaluation also provides a way to compare practices between peer institutions, thereby identifying any gaps. In turn, banks can continuously optimize their CSR activities that contribute to sustainable overall development. The main contributions and limitations of this study are discussed in the following subsections.

In terms of academic contributions, this study combines MDM and ANP to construct a new CSR evaluation model for use in China’s banking industry, thus addressing a clear gap in the literature and providing a practical tool for optimizing relevant systems. The model includes 5 main evaluation criteria and 18 sub-criteria, which are more complete and more comprehensive than the criteria used by other scholars to measure bank CSR in China. The model composed of 5 assessment criteria is very stable and more feasible than before. It provides a certain theoretical basis for the supervisory authority to evaluate the social responsibility of banks and enriches the theory of CSR. The results offer future directions for academic study.

In terms of practical contributions, this study constructs a new CSR evaluation model for banks, which enables their operators to clarify the evaluation criteria and sub-criteria of bank CSR and their importance. Therefore, bank operators should respond to the importance of assessment criteria and sub-criteria and continuously optimize their social responsibility activities in order to enhance the evaluation of bank CSR, highlight the image and uniqueness of banks’ CSR, and help improve their competitiveness. The study finds that bank governance and regulatory compliance are the most important evaluation criterion and sub-criterion, respectively. It is recommended that banks should improve their internal governance and strengthen CSR, such as diversify their shareholdings, establish a sound incentive and restraint mechanism for executive compensation, and optimize their management structure, in order to actively fulfill their social responsibility.

Banks should also pay attention to regulatory compliance. If they cannot fulfill their statutory obligations, then they cannot fulfill their social responsibility. It is recommended that banks adhere to the red line and bottom line of compliance, strictly implement regulatory requirements, and take up social responsibility to promote their sustainable and healthy development.

This study also verifies practicability and stability of the new model through sensitivity analysis, thus establishing that it provides flexible decision-making for the supervisory authority when assessing CSR practices. Government departments should therefore use the model to facilitate their formulation of relevant policies. Furthermore, the evaluation criteria can be used to standardize CSR reports issued by Chinese banks, particularly when aiming for full disclosure. The supervisory authority can also assign weights to different evaluation criteria based on specific social and economic development needs.

The expert group recruited for MDM comprises industry, government, and academic experts exclusively from China. This limits generalizability, as banks in other countries may have different business objectives, cultures, and characteristics. It is recommended that future studies expand the sample size to make the constructed assessment framework more generalizable. Methods such as DANP and Fuzzy ANP can also be applied to compare studies in the literature.