Abstract

The adoption of online banking is a big challenge as well as an emergent paradigm which is evolving quickly. The study develops a new exploration model that is used to determine significant constructs of the UTAUT theory that influence the adoption of online-banking. A study was conducted through an online survey of online banking users. Three methods were used; firstly, PLS-SEM was used to determine which of the constructs have a significant impact on behavioral intention to use e-banking, secondly, an incorporated neural network model was used to classify the relative impact of significant variables obtained from PLS-SEM, and finally a hybrid procedure is incorporated from PLS-SEM to initialize the Fuzzy TOPSIS. The findings of the research paper constitute the ranked results and a comparison between them. The results of PLS-SEM and ANN analysis showed the same ranking for the constructs, while the decision making method Fuzzy TOPSIS introduced some changes in the ranking. This study presents valuable insights for the banking system to bring effective projects that increase the possibilities of using online banking.

Introduction

The rapid expansion of the accessibility of the Internet has conduct the increasing use of online banking [1]. It has changed the banking system [2]. The latter has moved rapidly from traditional financial services towards self-service delivery channels [3]. Has appeared as one of the great electronic commerce applications [4].

Online banking is a banking channel that allows customers to accomplish financial transactions wherever the Internet is accessible anytime, anywhere [5]. It offers services such as balance enquiries, balance transfer, opening accounts, payment of bills [2] and other details connected to accounts [6].

Online banking helps the improvement of the efficiency and effectiveness of services [7] which in turn improves banks’ competitive positions [8] in advanced and dynamic banking system. There are many studies that explain the factors that influence the acceptance and use of online banking based on the perspectives of various adoption theories [9–12]. In general, empirical studies are based on multiple regression model [13, 14], partial least square structural equation modelling (PLS-SEM) [15, 16]. These methods are conventional and guided by the approach of the influence of independent variables on dependent variables, excluding non-linear relationships between variables.

This paper proposes a multi-analytical conceptual model to predict customers’ behavior and to determine the main constructs that impact the decision to use online-banking. This model does not only include the factors of UTAUT, but also integrates two new constructs, which are CS and PS, bringing strength, significance and predictability of the results [17].

So the contribution of this study is that it projects an integrated model which incorporates the UTAUT model and the customer service and perceived security constructs.

This study addresses some challenges related with the development of an innovative and hybrid framework that combines PLS-SEM with Fuzzy TOPSIS a Fuzzy Technique for Order Preference by Similarity to Ideal Solution (F-TOPSIS) and also ANN analysis to better estimate the adoption of online banking.

The results obtained from PLS-SEM show the importance that the constructs of UTAUT have regarding behavioral intention to use the online banking. In order to have an efficient decision-making result [18, 19], has been integrated a hybrid model which uses these results as initiators of the fuzzy TOPSIS method with triangular fuzzy numbers [20]. These method belong to the group of multi criteria decision making methods (MCDM) [21, 22].

The fuzzy TOPSIS starts with the construction of the decision matrix according to the structured problem and output from PLS-SEM method. Exactly the results of PLS-SEM orient better a decision maker in the construction of this matrix. The practical model of this hybridization has been effective even for the online learning [20, 23]. From the methodological side, this paper presents a multi-method research plan integrating Partial Least Square Structural Equation Modelling, ANN analysis and Fuzzy TOPSIS.

PLS-SEM shows significant variables from the supported relationships. The significant variables are used as inputs for the neural network structure to decide the relative importance of significant constructs. The ANN technique also serves as a complementary method to the PLS-SEM method because it takes into account the non-linear connections of the model.

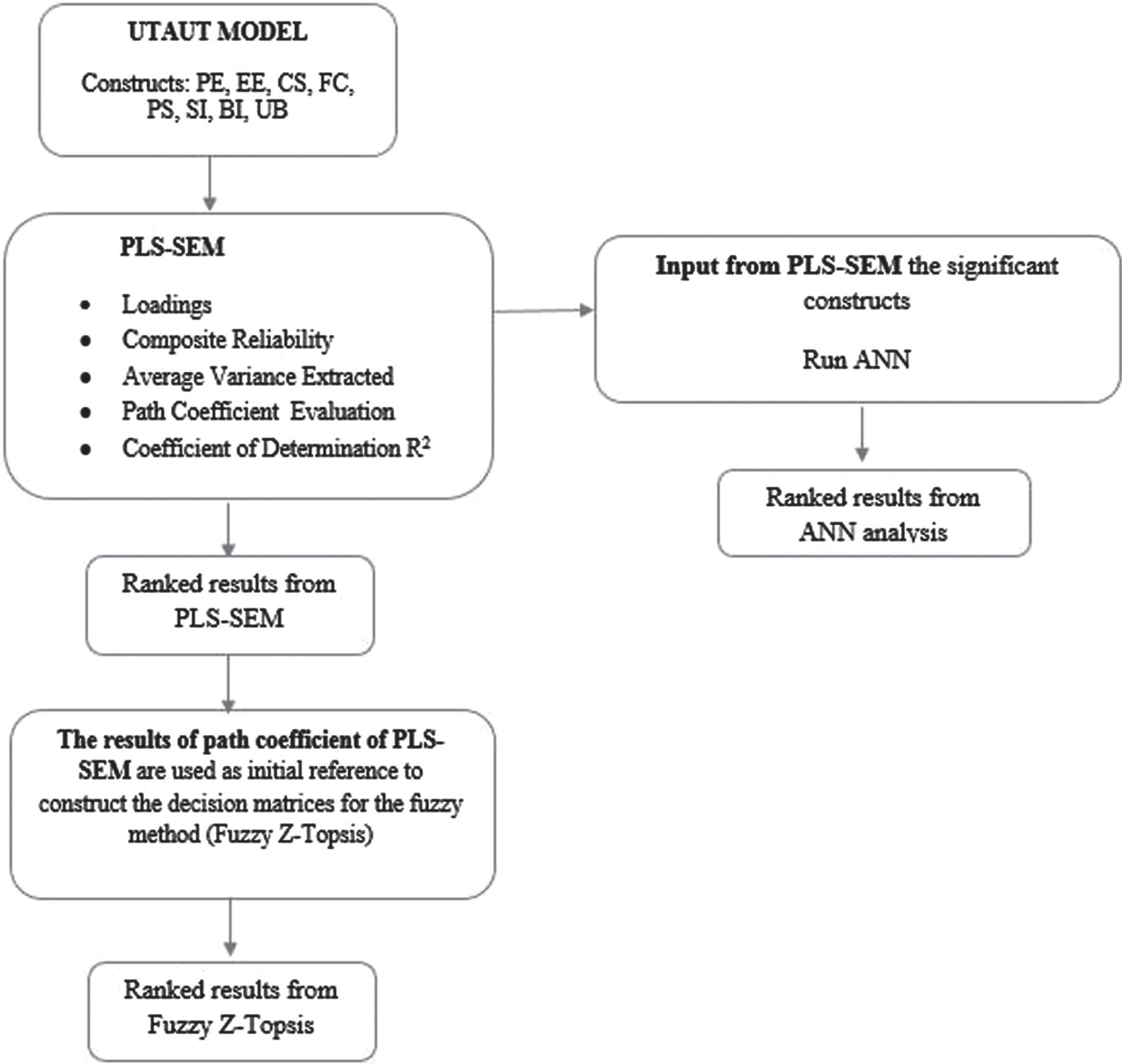

The outcomes of PLS-SEM guide the initializing of the Fuzzy TOPSIS procedure to rank the constructs of the proposed model in relation to behavioral intention to use online banking [20]. The use of multi-method predictive, which is based on the hybridization of 3 methods, ensures a holistic approach to online banking and brings a methodological contribution from the statistical aspect. (See the framework, Fig. 1).

The framework of the research study.

In information systems studies, frameworks with different constructs have been developed to explain individual’s acceptance and use of new technology, such as Theory of Reasoned Action (TRA) [24], Theory of Planned Behavior (TPB) [25], and the Technology Acceptance Model (TAM) [26], UTAUT [27]. Many studies in various contexts of technologies have evolved based on these models or have expanded them with new factors, making them more comprehensive. In the UTAUT model, all the constructs of the above models are integrated, improving the model’s explanatory power to behavioral intentions to use new technology [28]. UTAUT is robust and powerful model to explore determinants of behavioral intention to use a new technology [28].

Research model and hypotheses development

The UTAUT model will also serve as a ground to determine the factors that influence user acceptance of online banking. The UTAUT model includes the constructs: performance expectancy (PE), effort expectancy (EE), social influence (SI) and facilitating condition (FC). To improve the model’s explanatory power and for a holistic understanding of behavioral intention to use online banking, the model has been extended by incorporating the constructs customer service CS and perceived security (PS). The research model is presented in Fig. 1.

Performance expectancy denotes the degree to which a customer perceives that online banking induce greater performance, productivity in the realization of banking tasks [29]. The impact of performance expectancy on behavioral intention to use online banking has been widely provided in previous studies [17, 30]. Based on previous literature, we suggest the following hypothesis:

H1: Performance expectancy positively affects the behavioral intention to use online banking.

Effort expectancy is the degree of ease associated with using the online banking [28]. When the use of online banking by the customer is easy, then the possibility of adoption increases [31]. Multiple studies confirm that effort expectancy have a significant effect on behavioral intention (BI) to use online banking [32–36]. In addressing this issue is investigated effort expectancy and compared it with other constructs of model. Accordingly, the following hypothesis is proposed:

H2: Effort expectancy positively affects the behavioral intention to use online banking.

Social influence is social pressure that customers have from family members, and friends in order to use a particular technology [37]. In the online banking context, it has been found that social influence is an important construct of acceptance of online banking [29, 37–39]. Consistent with these findings, we suggest the following hypothesis:

H3: Social influence positively affects the behavioral intention to use online banking.

Facilitating conditions are the degree to which a user considers that he has the required infrastructure to implement a new technology [40]. If users do not have the necessary tools such as computer, smartphone, internet and necessary operational skills they would have lower possibility to adopt a specific technology [41]. The studies show that facilitating condition is one of the factors that positively affects customers’ intention to use online banking [34, 42]. Consistent with prior literatures, we propose the following hypothesis:

H4: Facilitating condition positively affects the behavioral intention to use online banking.

Perceived security denotes the degree of confidence in online banking to transmit sensitive data [43]. This is the reason why perceived security is considered as essential element in the adoption of online banking [41]. Perceived security is an important factor on the intention to adopt online banking [17, 44]. In this context, we suggest the following hypothesis:

H5: Perceived security positively affects the behavioral intention to use online banking.

Customer service is the expectation that customers have that through online banking transactions will be finalized correctly, the product will be delivered on time, their emails will be answered quickly, receive personalized attention [45]. The adoption of internet banking is strongly impacted by customer service, as evidenced by various studies [45–47]. Moreover, customer service influenced users’ perceptions of effort expectancy in utilizing internet banking, as highlighted by research conducted by [48–50]. Extensive research performed by [50] and [34] demonstrates that customer service has a positive impact performance expectancy. Based on the above arguments, we suggest the following hypotheses:

H6: Customer service positively affects the behavioral intention to use online banking.

H7: Customer service positively affects the user performance expectancy of online banking.

H8: Customer service positively affects the user effort expectancy of online banking.

Research methodology

In this paper a hybridized methodology is employed by the integration of Partial Least Squares Structural Equation Modelling (PLS-SEM), artificial intelligence method named as Artificial Neural Network (ANN), and Fuzzy TOPSIS. The analysis is carried out in three stages. The first stage is connected with PLS-SEM which includes measurement model validation and structural model hypotheses testing.

In the second phase, the hypotheses accepted by the structural model are evaluated by ANN to show the relative impact of significant variables. In the third phase, the significant variables of the structural model according path coefficients are ranked by Fuzzy TOPSIS.

A self-administered questionnaire was established in Albania in 2022. The data accumulating procedure was conducted online through Gmail, Facebook platforms. The study was conducted with a case of 440 customers that had used online banking services of different commercial banks in Albania.

Questionnaire is prepared based on a 5-likert scale in order to collect the responses: (1) Strongly Disagree, (2) Disagree, (3) Neutral, (4) Agree and (5) Strongly Agree. PLS-SEM technique of multivariate statistics was applied to test the hypothesis of existing theories or to evolve theory. The notions of the model are unobservable and measured indirectly by multiple items which are called latent variables or constructs. The PLS-SEM method concentrates on explaining the variance of the dependent variable [51].

Measurement model

In the models of information systems, the concepts have been operationalized by a reflective measurement model [52]. The evaluation of the measurement model includes statistics: item loading, composite reliability (CR), average variance extracted (AVE), discriminant validity.

Item loading presents correlations of items with their corresponding latent variables and it is recommended that this statistic have values greater than 0.7 [53]. Composite reliability values must be greater than 0.7. An indicator that confirms convergent validity is average variance extracted (AVE). The lower limit of AVE values is 0.5 [54].

Structural model

After the statistics of the measurement model have been evaluated and all are within the acceptable limits, we continue with the analysis of the structural model. The latter involves testing the statistical significance of the hypotheses proposed for the research framework, the values of R2, predictive relevance is calculated via Stone-Geisser’s Q2 (predictive relevance). This indicator must have values greater than 0 for a dependent variable to present strong predictive relevance.

ANN evaluation

Artificial Neural Network (ANN) is a parallel distributed processing model which is formed of processing elements that are called neurons, and are connected between them with weighted links [55]. The ANN consists of neurons that are grouped into layers.

The most typical form of neural networks consists of input layer, hidden layers and output layer. In studies related to technology adoption, multi-layer perceptron (MLP) is usually used. The activation function is usually a non-linear function and the most common activation function that is used is sigmoid function because it has easily differentiable properties [56].

ANNs is an artificial intelligence method that is powerful, highly efficient in modelling complex relationships among input layers and output layers [57]. Based on the previous literature [58–61], regarding technology adoption studies where neural networks are based on MLP are commonly used one or two hidden layers. The study data are divided into training set and testing set, where respectively 90% of the data are included in the training set and 10% for testing set [62].

Sensitivity analysis performance is calculated taking into consideration (ANN1, ANN2,...,ANN10) and the average of normalized importance for each ANN construct is calculated, which is called average relative importance [63]. Then the normalized importance of each independent variable is calculated as a ratio of its relative importance with the highest relative importance of all independent variables [64].

Fuzzy TOPSIS

The Technique for Order of Preference by Similarity to Ideal Solution (TOPSIS) is part of multi criteria decision making analysis methods (MCDM), which was originally developed by Ching-Lai Hwang and Yoon in 1981 [65]. The criteria weights in TOPSIS method are calculated using Ordinal Priority Approach or Analytic Hierarchy Process (AHP) [21].

An assumption of TOPSIS is to find the ideal solution via the shortest geometric distance from the positive ideal solution (PIS) and the longest distance from the negative ideal solution (NIS) [66]. Some of the criteria can be addressed as benefit criteria and cost criteria where the scope is to maximize the benefit and to minimize the cost. Using fuzzy numbers usually triangular fuzzy numbers Saaty scale [18] in TOPSIS for criteria estimation leads to Fuzzy TOPSIS method.

The optimal criteria is it that is nearest to the PIS solution. A complex decision problem is based on alternatives A1, A2, ... ,An and criteria C1, C2, ... ,Cm. The group of decision makers judge the construction of the decision matrix of the problem D (x ij ), where x ij is the comparison of the alternative Ai toward criteria Cj.

Fuzzy TOPSIS steps:

Step 1: Define the fuzzy ratings of the k-th decision maker

Step 2: The evaluation of the aggregated fuzzy ratings x

ij

and the aggregated fuzzy weights ω

j

.

Step 3: Compute the normalized fuzzy decision matrix

Step 4: The weighted normalized fuzzy decision matrix

Step 5: Compute the fuzzy positive ideal solution (FPIS) and the fuzzy negative ideal solution (FNIS).

Step 6: Calculate the Euclidian distance from FPIS and FNIS

Step 7: Compute the closeness coefficient CC

i

as follows:

Results

Evaluation of the measurement model

The item loadings shown in Table 1 varied from 0.759 to 0.924, so it’s confirmed that they are greater than the “minimum requirement, which is 0.7.

Measurement model assessment

Measurement model assessment

Moreover, the internal consistency reliability was assessed by observing that the Composite Reliability (CR) values reached 0.8, surpassing the minimum threshold of 0.7, as described in Table 1.

The values of the AVE statistic are greater than 0.5, so they reflect satisfactory convergent validity achieved by the constructs.

The structural model is evaluated based on the significance of path coefficients and the variance of the dependent construct, represented by R square.

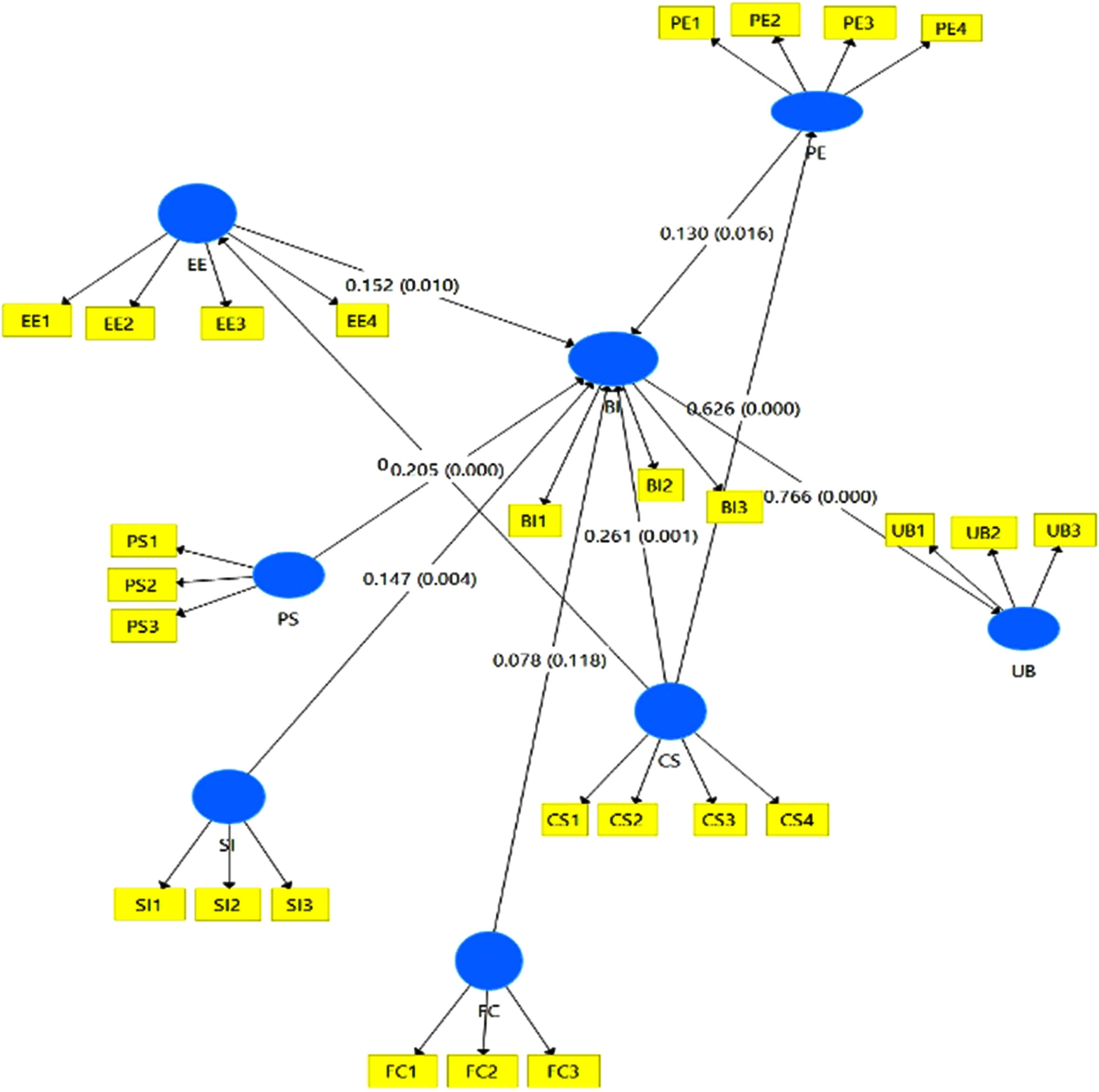

The significance of the path coefficients was evaluated through a T-test conducted using the bootstrapping technique, with a significance level set at 5%. The results of Fig. 2 and Table 2 present the path coefficients of the structural model and the testing of the hypotheses taken into consideration. Table 2 shows the path coefficients.

Path coefficients of structural model.

Path coefficients

The path coefficient for the Performance expectancy influence on behavioral intention to use online banking (β= 013, p = 0.05) indicated the significant positive influence of Performance expectancy on behavioral intention to use online banking. The path coefficient for influence of effort expectancy on behavioral intention to use online banking (β= 0.152, p = 0.05) revealed its significant positive impact on behavioral intention to use online banking.

The path coefficient for the influence of customer service on behavioral intention to use online banking (β= 0.261, p < 0.05) revealed its significant and positive impact.

Additionally, the path coefficient for the influence of perceived security on behavioral intention to use online banking (β= 0.205, p < 0.05) revealed its significant and positive influence, the path coefficient for the influence of social inclusion on behavioral intention to use online banking (β= 0.147, p < 0.05) revealed its significant and positive influence.

Whereas facilitating condition has no significant impact on behavioral intention to use online banking.

The path coefficients for the effects of customer service on effort expectancy (β= 0.713, p < 0.05), and on performance expectancy (β= 0.626, p < 0.05), indicated their respective significant and positive effects.

Table 3 shows that the research model achieved 66.5% of the behavioral intention variation towards online banking. The R2 values are also presented for EE (50.8%), PE (39.1%), UB (60.4%).

Variance explained from constructs

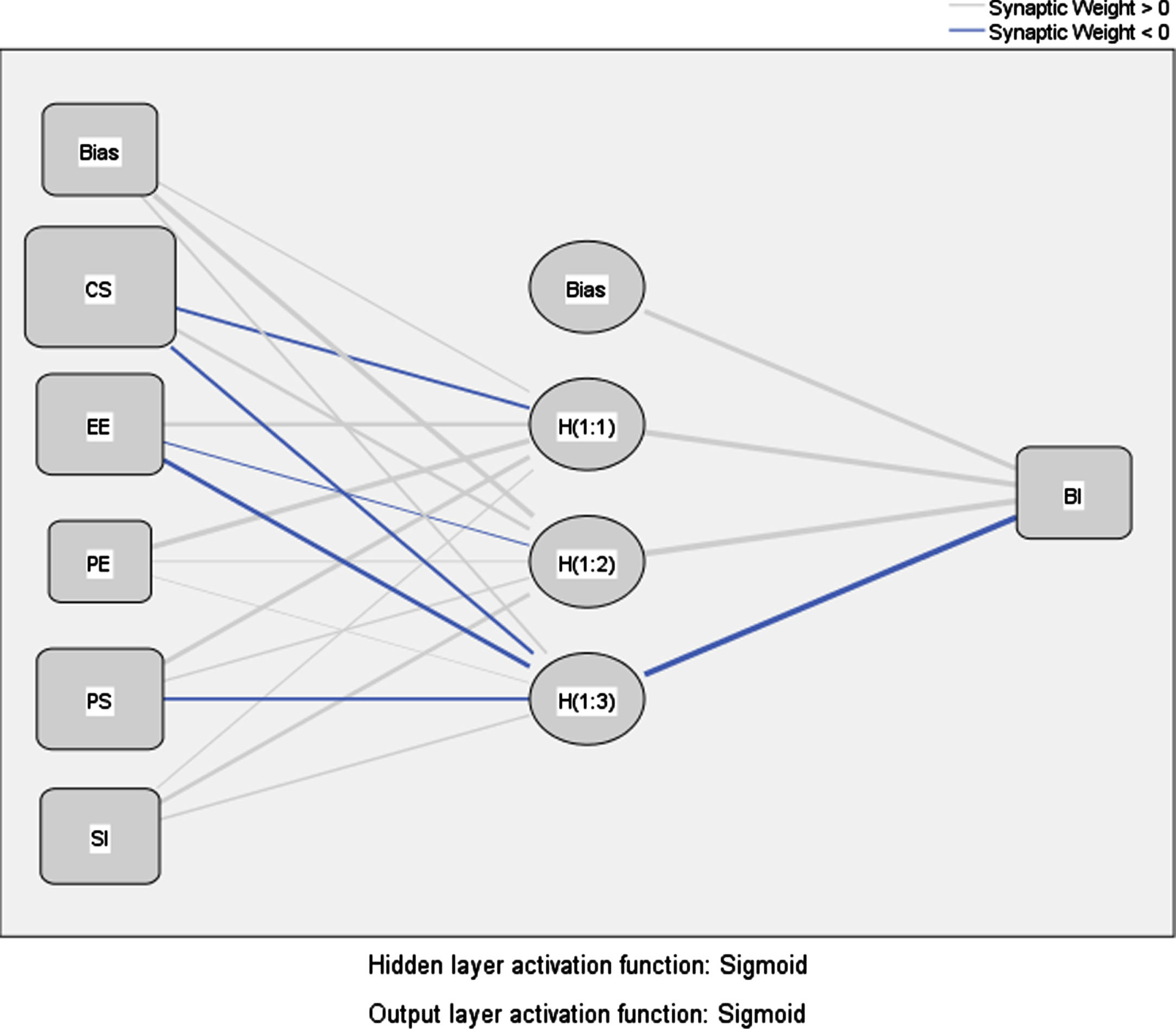

In our research framework, we used SPSS v22 to model the MLP-ANN. The model that has a dependent variable behavioral intention was taken into consideration.

The significant constructs determined by PLS-SEM are used as inputs to the model.

The model has 5 important constructs. The recommendations provided by Leong [64] entail the automatic generation of hidden neurons (nodes) and the utilization of the Sigmoid function as the activation function for both the hidden and output layers.

ANN model.

The results in Table 4 show that in relation to the normalized relative importance indicator, the customer service construct is the most important determinant of behavioral intention, which is followed by perceived security, effort expectancy and social inclusion.

The normalized relative importance

Performance expectancy has the weakest influence on behavioral intention compared to other constructs.

The importance of the significant constructs derived from PLS-SEM analysis (see Table 2) orients better the initialization of the fuzzy TOPSIS method in order to construct the decision matrices.

Three decision makers have evaluated the importance of each of the constructs toward the behavioral intention to use online banking. Each of the decision matrices (DM1, DM2, DM3) must be consistent according Saaty inconsistence (IC) less than 0.1.

Therefore, an integration of the two approaches PLS-SEM and TOPSIS was realized to initially evaluate the proposed model.

Table 6 shows the results for the decision matrices related to decision maker 1 (DM1), decision maker 2 (DM2), and decision maker 3 (DM3). According path coefficients the construct FC (facilitating conditions) is not taken as an important one because the p-value is greater than 0.05. Table 5 shows the initial decisions.

Initial decisions of fuzzy TOPSIS

Initial decisions of fuzzy TOPSIS

Applying equations of step 1 to step 5 is obtained the weighted normalized fuzzy decision matrix. Table 6 shows the weighted normalized fuzzy decision matrix. After calculating FPIS and FNIS is computed the closeness coefficient CC i . Table 7 shows the ranked results.

Weighted normalized fuzzy decision matrix

The ranked results

Table 8 shows a comparison of the results according the classification of the constructs with the ANN method and with PLS-SEM. It is showed that the constructs are ranked the same as with the PLS-SEM method and with the ANN method.

Results comparison PLS-SEM, ANN and fuzzy TOPSIS

This research extends the new technology adoption based on ANN that has traditionally been developed by the PLS-SEM method, as well as fuzzy TOPSIS that initiates from PLS-SEM. The impact of each predictor construct in relation to the predicted construct behavioral intention to use online banking is ranked using ANN sensitivity analysis and Fuzzy TOPSIS. The findings of the ANN paradigm confirm the results obtained from PLS-SEM, while fuzzy TOPSIS confirms the first 2 rankings while the last three change order. The combined approach of three stages PLS-SEM, ANN and Fuzzy TOPSIS method yielded more comprehensive findings concerning the relative significance of the predictor constructs. This valuable information sheds light on the adoption of the new technology. The PLS-SEM analysis shows that customer service has the strongest positive impact on behavioral intention to use online banking and ANN evaluation confirms this result by ranking customer service (CS) firstly. The integrated model showed that customer service is the most important variable among all other variables including fuzzy TOPSIS. This indicates that online banking users are more concerned about quality of customer service. Users are likely more interested in having a satisfactory customer experience, quick and helpful responses from customer support, and efficient problem resolution, which influences their overall satisfaction to the online banking platform. Perceived security was found to be the second most important construct that impacts users’ intention to adopt online banking. So customers place a high level of significance on feeling secure and safe when considering using online banking services. The differ ranks of effort expectancy, perceived expectancy and social inclusion depends from the decision matrices of the decision makers point of evaluation. The results of the study help bank managers with the necessary knowledge about the constructs of UTAUT that have an impact on behavior intention regarding the use of online banking. This study is limited because it was conducted only for the whole Albania country. The subsequent study will include in a broader geographical context and new constructs will be integrated.