Abstract

Offshore grids, with multiple interacting transmission and generation units connecting to the shores of several countries, are expected to have an important role in the cost-effective energy transition. Such massive new infrastructure expanding into a new physical space will require new offshore energy market designs. Decisions on these designs today will influence the overall value potential of offshore grids in the future. This paper investigates different possible market configurations and their impacts on operational costs and required congestion management, as well as prices and emissions. We use advanced integrated energy system optimisation, applied to a study case on the North Sea region towards 2050. Our analysis confirms the well-known concept of nodal pricing as the most preferable market configuration. Nodal pricing minimises costs (0.2–1.6 b€/year lower) and CO2 emissions (0.6–5.6 Mton/year lower) with respect to alternative market designs investigated. The performance of the different market designs is highly influenced by the overall architecture of the offshore grid, and the rest of the energy system. E.g., flexibility options help reducing the spread between the designs. But the results are robust: nodal pricing in offshore grids emerges as the preferable market configuration for a cost-effective energy transition to carbon neutrality.

1. Introduction

1.1 Background

To achieve climate goals and to mitigate the consequences of climate change, energy systems need to reduce emissions to sustainable levels (IPCC, 2022). To decarbonise the energy systems, variable renewable energy (VRE) generation, as well as adequate market design (Newbery, 2018), are likely to be of high value. Solar photovoltaic (PV) and wind energy are becoming more and more competitive with respect to technologies burning fossil fuels (IRENA, 2019). Particularly in Europe, offshore wind generation in the North Sea is likely to play a significant role in achieving the climate goals, and that is why the European Commission is promoting its development (The European Commission, 2020b).

Previous studies have found that it is cost-effective to develop some of the offshore wind development in advanced offshore grid configurations (Gea-Bermúdez et al., 2020; Konstantelos et al., 2017; Koivisto et al., 2019; Gea-Bermúdez et al., 2022) owing to savings in capital expenditure due to economies of scale and increased flexibility of the transmission lines that are part of offshore grids. On the other hand, the potential value that offshore grids can bring to the energy system has been found to be highly dependent on the level of sector coupling between the electricity, heat, and transport sector (Gea-Bermúdez et al., 2022). Offshore grids can both be used to generate and transport electricity, but also to generate other fuels, like hydrogen (H2). As an example, Denmark is considering generating green H2 on the energy island they are planning to develop (DW, 2021).

Considering the vast potential of offshore wind in the North Sea, it is important to investigate the influence that offshore grids can have on the energy markets (not only the electricity one), and how different market designs influence such impact. The market design of offshore grids can play a significant role in the overall value of offshore grids, since it can influence, among other things, investment incentives and congestion management costs. Inspired by the North Sea Wind Power Hub project (North Sea Power Hub, 2020), Tosatto et al. (2021) investigated the influence of an energy island on the European power system by 2030 showing how exporting countries are affected by the lower electricity prices. A similar study has been performed by Jansen et al. (2022). Both Jansen et al. (2022) and Tosatto et al. (2021) assumed nodal pricing in their papers, which according to Commission et al. (2020) would be the one ideal in Europe, since it perfectly reflects all costs of supplying electricity at given nodes and, manages congestion at the same time. However, nodal pricing is not free from problems, since its implementation might cause some market flaws.

The main shortcoming of nodal pricing is—according to one strain of the literature—missing market liquidity and the possibility for suppliers to exercise market power in the grid nodes, which have a few or a single electricity generator. Although some studies find evidence that combining nodes to a large market zone might even exacerbate market power and increase the profits of the dominant company (see Harvey and Hogan, 2000), another part of the literature argues for reduced market power when going from nodal to zonal pricing or potentially increased market power when separating a market zone into more and smaller ones (e.g., Frank A.Wolak, Chairman, 1999; Henney, 1998). Hence, a higher liquidity and, therefore, a more competitive outcome can be achieved by combining several grid nodes in one market zone and thus increasing the number of market players on the generation side and also on the demand side within the zone. With such a configuration, each bidding zone is assumed to contain no significant intra-zonal grid constraints, while the borders between the different zones constitute structural grid constraints. However, if the ignored intra-zonal grid constraints are large, it can potentially lead to high congestion management (Bertsch et al., 2017), the so-called redispatch, and high related costs (Holmberg and Lazarczyk, 2015). The magnitude of this influence in offshore grids is something that has not been investigated yet. Given the fact that offshore grids in the North Sea will mostly connect producers rather than consumption (apart from some offshore H2 generators who will act as consumers of offshore electricity on site) and that there will be several wind parks connected to one offshore grid node, it is likely that the possibility of exercising market power will be reduced. However, we acknowledge that this is the case under the assumption that all offshore generation is constrained off at the same price. As mentioned above, the nodal as well as zonal designs may still enable the exercise of market power in case of dominant players remain in this configuration. This empirical question needs to be tested, depending on the control of wind generation within constrained regions of the offshore zones.

However, given the fact that nodal pricing theoretically serves as the most efficient benchmark for an electricity market configuration, it is worth investigating and comparing nodal versus several zonal approaches to gain insights into the benefits and costs of different market configurations in the immensely growing offshore electricity sector.

1.2 Contribution to the literature of this paper

The main goal of this study is to investigate and quantify the influence of different offshore electricity market designs on the operation of day-ahead markets in integrated energy systems towards 2050, as well as their impact on the required congestion management. The influence of the overall development of the offshore grids on these previous aspects is also analysed, which can be of high value considering the uncertain development of offshore grids. We use as study case the North Sea region. The model includes energy demands for the electricity, heat and transport sectors. We do this through an advanced optimisation process using the open-source energy system model Balmorel. The main contributions of this paper are listed below.

To our knowledge, this paper is the first one analyzing the influence of different offshore market designs on the operation of day-ahead markets towards 2050.

To our knowledge, this paper is the first one analyzing the influence of different day-ahead electricity market offshore grid designs on the required congestion management of the system towards 2050.

To our knowledge, this paper is the first one analyzing the influence of different offshore grid development on the two previous points.

The model used is an integrated energy system, including demand for electricity, heat, and transport sector. This means that the investigated impact quantifies the impact on the entire energy system and not just the electricity one.

The quantification of the difference for scenarios that seek decarbonisation towards 2050 in integrated energy system will inform policy makers and regulators in important decisions about future system architecture. Implementing nodal markets might be more challenging than implementing a zonal one, so there are likely to be practical trade-offs. As a consequence, obtaining insight into comparative differences between different offshore electricity market designs can be of high value.

The structure of the remainder of the paper is as it follows: Section 2 includes the methodology, data and a description of the scenarios and optimisation approach used. Section 3 presents the results, and provides a critical reflection of them. Finally, Section 4 presents the overall conclusions.

2. Methodology

The energy model Balmorel is used for the analysis based on the combination of the model versions employed in Gea-Bermúdez et al. (2023) and Gea-Bermúdez et al. (2022). The Balmorel model has been extended for this paper to be able to simulate congestion management operation. The Balmorel model and data used are open source (Balmorel community, 2021b,a) 1 In the following, we give an overview of the main elements of Balmorel and focus then on scenario development, which includes the optimisation approach used to derive the scenarios.

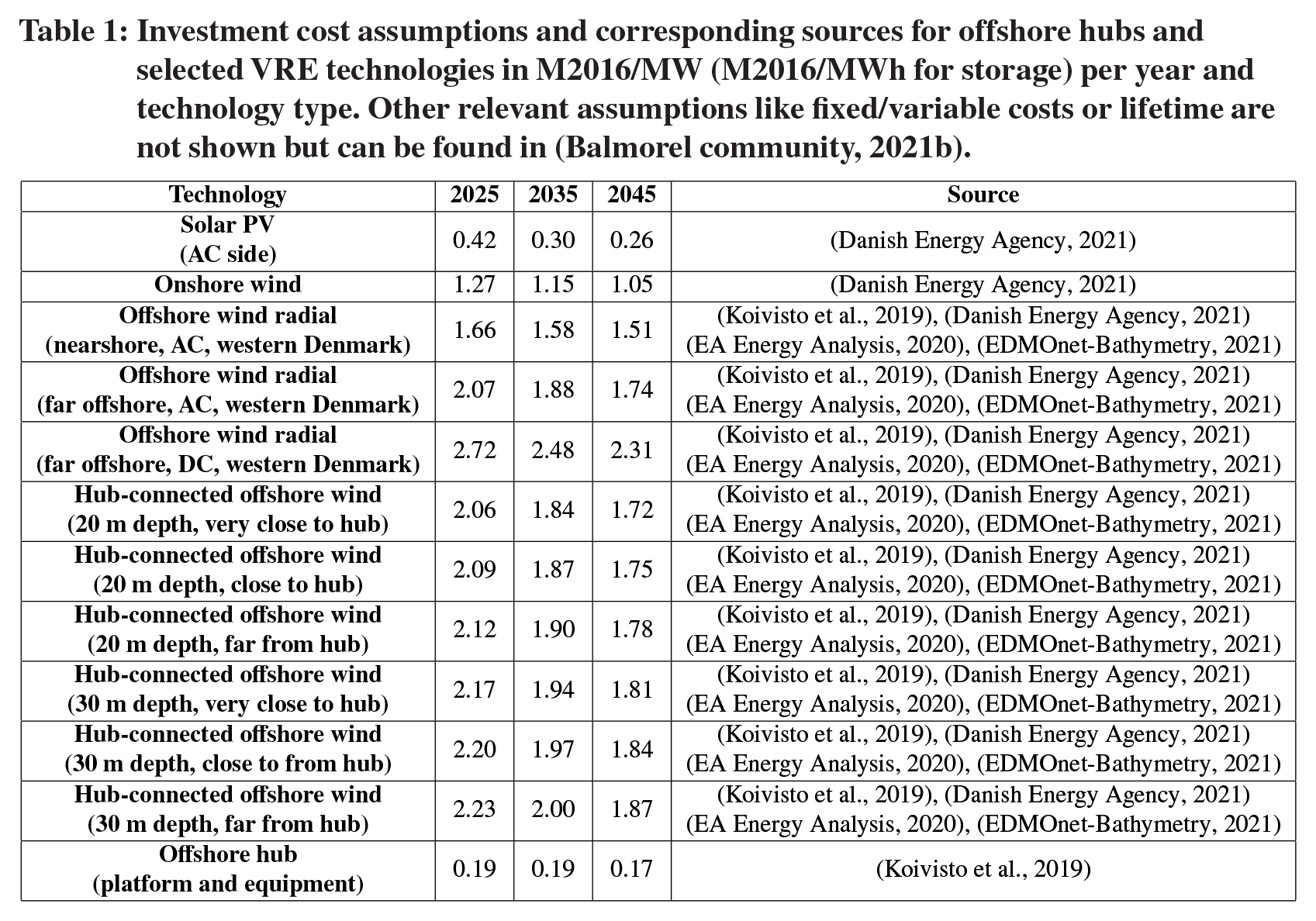

Investment cost assumptions and corresponding sources for offshore hubs and selected VRE technologies in M2016/MW (M2016/MWh for storage) per year and technology type. Other relevant assumptions like fixed/variable costs or lifetime are not shown but can be found in (Balmorel community, 2021b).

2.1 Balmorel

2.1.1 Generic model description

The energy system model Balmorel (Wiese et al., 2018) is open source (Balmorel community, 2021a), has a flexible structure, is deterministic, and has a bottom-up approach. Over the past years, the model has been developed considerably with the goal of including more energy sectors (Gea-Bermúdez et al., 2021), more detailed electrofuels and H2 modelling (Bramstoft et al., 2020; Lester et al., 2020; Jensen et al., 2020), and to have a more advanced system operation modelling (Gea-Bermúdez et al., 2021).

Several configurations of the Balmorel model have been applied in this paper to be able to perform capacity development optimisations, day-ahead optimisations, and congestion management optimisations. The possibility to perform congestion management optimisations is a new feature of the model that has been developed to write this paper.

The temporal resolution in Balmorel is composed of years, and each year contains seasons, which contain terms. The simulated years correspond to 2025, 2035, and 2045, which are meant to represent an average of the time periods 2020–2030, 2030–2040, and 2040–2050, respectively. The meaning of seasons and terms is flexible in Balmorel and it is defined by the user. For example, seasons can be used to represent days, weeks, months, etc., while terms can be used to represent hours, minutes, seconds, etc.

The geographical scope applied in this paper covers 10 countries: United Kingdom, Sweden, Belgium, Denmark, France, Netherlands, Finland, Norway, Germany and Poland. Countries are split into regions in the model based on existing bidding zones. The exception is Germany, that is split into four bidding zones in the model to capture existing intra-country bottlenecks. In total we model 37 biding zones (21 onshore + 16 offshore hubs). Within the same bidding zone, transmission constraints are ignored, while between different zones the transmission is limited mainly by the interconnector capacities.

While considering different market zones, we have considered the inter-zonal bottlenecks and existing market configurations in most countries. At the same time, by splitting Germany into four model regions, we believe in having captured the intra-zonal network bottlenecks in one of the countries with the largest and growing congestion management needs (Kunz, 2013; Bundesnetzagentur, 2021). The growing congestion stems from the fact that Germany is still organized as one market zone in electricity trading. However, since we model Germany in four zones, our model probably captures a large share of the congestion issues that a model with more zones would capture. This can be seen as a proxy and modelling simplification for the flow-based market coupling that takes place in reality, mainly in the Central-Western European (CWE) market area.

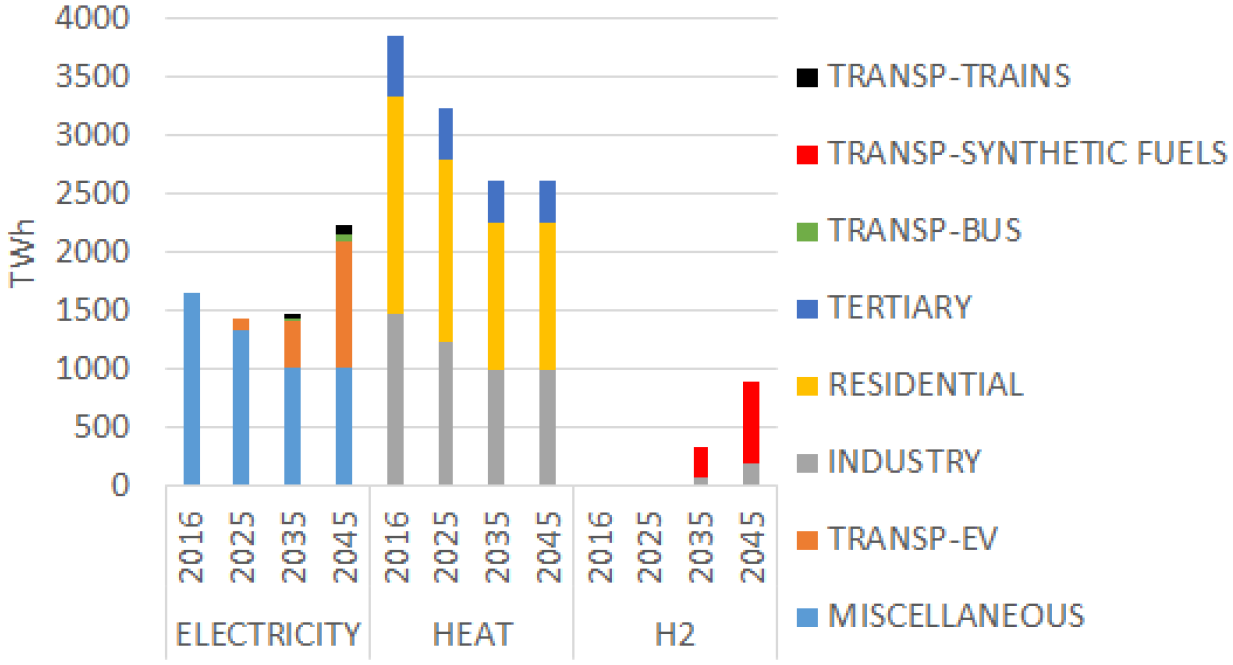

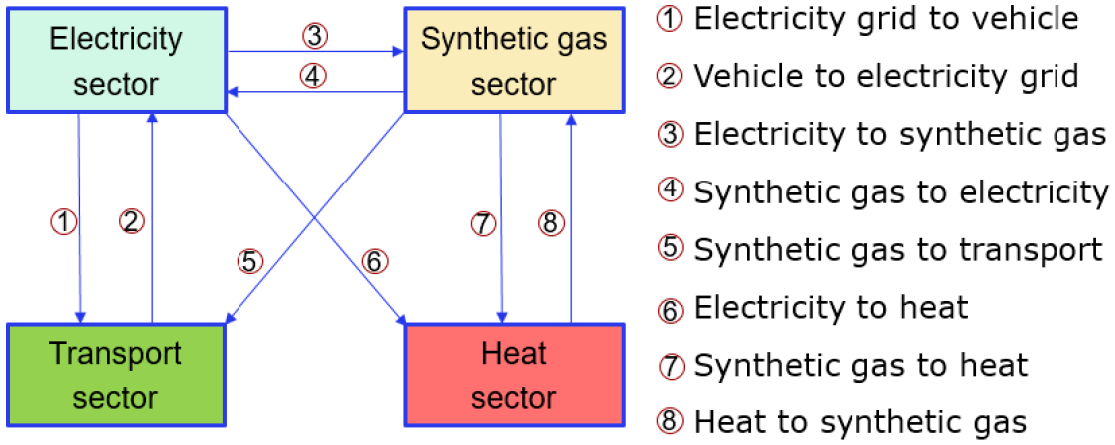

The energy system modelling includes energy demands of the electricity, heat, and transport sectors. The energy demands of these sectors are modelled as electricity, heat, and H2 demand (Figure 1). European or national decarbonisation goals towards 2050 of the transport sector are applied in the paper. Figure 2 illustrates the potential synergies that are captured in the model.

Total exogenous demand assumed in the studied countries per commodity, year, and sector (TWh). The year 2016 is considered as the base year of the model and is not included in the optimisations. H2 stands for hydrogen. Figure obtained from GeaBermúdez et al. (2022).

Possible synergies between all the sectors included in the model. Figure obtained from Gea-Bermúdez (2021).

The generic objective of the optimisation model is to minimise discounted system costs (Equation 1) while satisfying the energy needs of the consumers. In the absence of market power (as it is assumed in this paper), modelling market clearing as an optimisation problem is equivalent to modelling it as an equilibrium problem since they share the same Karush–Kuhn–Tucker conditions. Part of the annual demand for the different commodities is assumed to be exogenous (Figure 1), although additional demand can take place due to sector coupling and/or storage/transmission losses. The different costs of each of the years (y) studied are grouped in fixed costs

The overall decision variables in the model are investment capacities in different technologies (generation/storage units, H2 pipelines, electricity transmission, district heating expansion), and technology operation per term (energy generation, storage content, storage loading, energy trade, and electric vehicle (EV) operation). The storage content of hydro reservoirs without pumping is modelled per season though, meaning that the energy content per term is not modelled. Another variable which is optimised in the model is generation and storage unit mothballing. Mothballing means that units can be not available for operation during one year, to avoid paying the annual fixed costs, and then become operative again in future years. At the end of their technical lifetime, the units are forced to be decommissioned. Decommissioning costs of exogenous units are not part of the model.

Future years are discounted to reflect the socio-economic value of time using an annual discount rate of 4% (Danish Energy Agency, 2021), which is used to calculate the resulting discount factor (DFy) of each modelled year. If only one year is optimised at a time, then the discounting is not relevant.

Other key equations in the model are commodity balances (electricity balance, heat balance, etc.), technology-specific operational constraints, storage balance, and resource potentials, e.g., maximum installed onshore wind capacity.

Additional special equations, variables, and costs, e.g., unit commitment-related ones (on/ off status, ramping limits, minimum up-time, etc.), are also part of the model. However, they are by default not activated, unless the user finds it relevant. The complexity of the model can increase significantly when activating these special parts of the model.

2.1.2 Modelling energy system components

SNG can be generated through methanation-direct air capture units, which consume heat, H2 and electricity. SNG can be used as a perfect replacement of natural gas and its CO2 emissions are not penalised in the objective function as it is assumed to be carbon neutral. The costs, losses and constraints of natural gas networks, in which SNG is assumed to flow, are not included in the model. This means that SNG generated in each of the regions of the model can be freely distributed around the modelled regions.

The H2 balance is defined for each region in the model. The modelling includes generation of H2 with alkaline water electrolysis units, transport of H2 between regions with H2 pipelines that assume linear bi-directional flow, and network losses. The data related to the transport of H2 is based on Danish Energy Agency (2021). Inflexible H2 demand from industry is included and based on European Commission (2018). H2 demand of the transport sector is modelled as relatively flexible and is explained later in this section. More details can also be found in Gea-Bermúdez et al. (2023).

Inflexible EV annual demand include the electrification of rail transport and buses that are not currently electrified. This annual demand data is taken from Transport and Environment (2018) and is broken down using exogenous time series in each region, with the demand pattern assumed constant for trains, and time dependent for buses. The time dependent patterns for buses is based on Philip Swisher (2020).

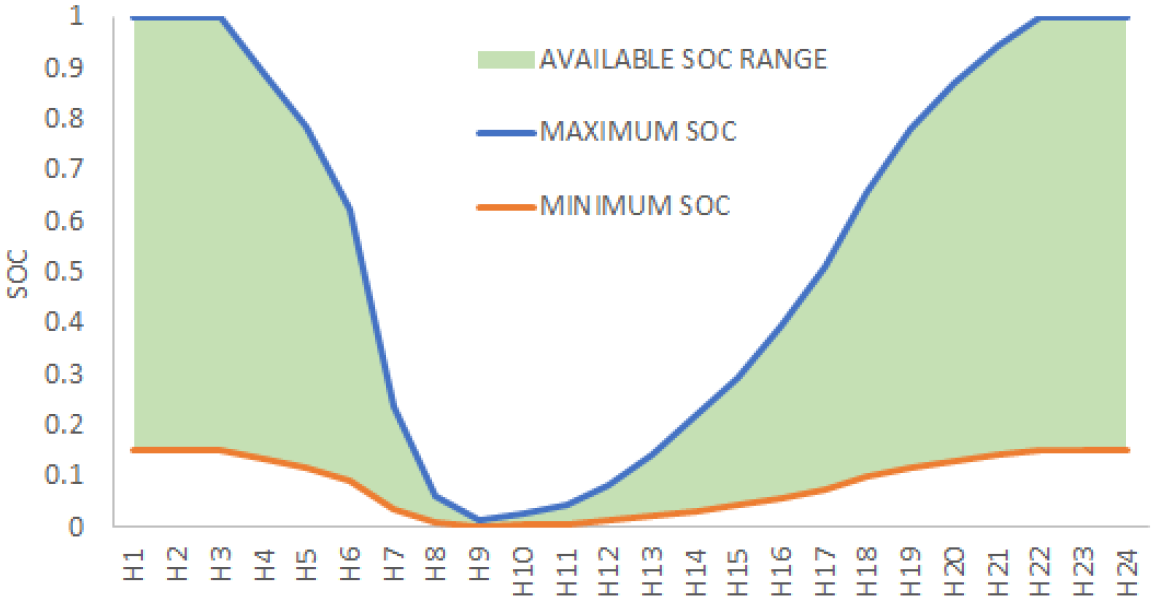

Road transport (excluding buses) is modelled as flexible EVs, which are represented as a virtual storage for each model region based on the work of Gunkel et al. (2020). The modelling includes limits to charging and discharging related to usage patterns, the electricity consumed for charging, and a representation of the battery storage in the EV fleet. The main equation of EVs is the hourly virtual storage balance. The balance is defined assuming seasonal cycles, i.e. the level of the storage at the start of each modelled season must equal the level at the end of that season. The model optimizes discharging and charging as well as the virtual storage content of the aggregated EV fleet. The number of EVs towards 2050, which is used as input to derive the time series of EVs, is based on (Philip Swisher, 2020). EVs are divided into battery EVs and plug-in hybrid EVs. Plug-in hybrid EVs are not allowed to be used for vehicle-to-grid purposes, and therefore, can only provide smart charging. Bottom-up modelling of driving patterns is used to generate the time-dependent input parameters used in the model. Vehicle trips are assumed to start when vehicles leave from home and to finish when they return, disregarding the performed activity. It is assumed that most EVs are not connected to the grid during most working hours. Trip consumption is calculated using the distance travelled by vehicles and average drive-train efficiencies. Therefore, different driving behaviours are disregarded. Inflexible charging restricts minimum charging, whereas the charger capacity restricts maximum charging. Furthermore, upper and lower limits for the state of charge are time-dependent and are based on assumptions related to when EVs are at charging stations (see Figure 3). EV charging is penalised with a charging loss and distribution grid losses. Operational and capital costs of EVs are not included. In short, in the model, flexible EVs can provide flexibility via smart charging (since only part of their demand is assumed to be inflexible) and by providing vehicle-to-grid services.

Illustration of the available state of charge (SOC) range during the day of electric vehicles. Figure obtained from Gea-Bermúdez et al. (2022).

The annual synthetic fuel demand required to decarbonise the shipping and aviation transport sectors of the studied countries is included in the scenarios and is based on Transport and Environment (2018). Such demand is modelled as an increasing annual H2 demand towards 2050 that needs to be satisfied in each onshore region along the year. H2 can be generated anywhere, but it needs to be sent ultimately to the onshore regions to be consumed. The hourly distribution of this H2 demand is optimized, although the peak-to-average ratio of such distribution is limited with an upper bound of 1.5 in each region to consider limited flexibility of the technologies that consume such H2. More information regarding the modelling of this H2 demand can be found in Gea-Bermúdez et al. (2022).

Investments in biomass units are not allowed in the optimisations, since the generation of synthetic fuels for the transport sector is likely to use a large share of the available biomass resources (Sims et al., 2010). The costs and challenges related to the transport of the biomass resources are not included.

The national onshore wind potential for the scenarios (419 GW in total for the investigated countries) is taken from Nordic Energy Research and International Energy Agency (2016). This limit is relatively low, and tries to model low onshore wind social acceptance. Potentials for radially-connected OWPP are based on Koivisto et al. (2019) and Nordic Energy Research and International Energy Agency (2016), whereas large-scale solar PV national potentials are taken from Ruiz et al. (2019). More information regarding the VRE modelling can be found in Gea-Bermúdez et al. (2021).

Introducing the possibility to build an offshore grid allows for multiple configurations of offshore infrastructure. The offshore grid technologies considered for investments in this paper are hub-to-hub and hub-to-shore electricity/H2 transmission lines/pipes, hub platforms, and hub-connected offshore wind farms, electrolysers, fuel cells, and steel tank H2 storage. A total of 16 locations in the North Sea to deploy offshore grid technologies are included in the model.

Offshore regions, which are modelled by default as individual regions (bidding zones), can then be used to generate and transport electricity and/or H2. Along this paper, offshore regions are also interchangeably called hubs. Modelling offshore grids as individual bidding zones allows to capture possible congestion issues of the pipes and electrical interconnectors connected to the hubs. In some of the runs made in this paper, the market configuration of offshore grids is modified (see Section 2.2).

The size of the offshore hub platform located in a particular offshore region is defined with its nameplate electrical capacity

Wake losses and transmission losses are modelled linked to the size of hub-connected wind farms. The larger the installed capacity of hub-connected wind farms are, the larger the resulting wake losses and transmission losses will be. Detailed information about the modelling of these losses can be found in Gea-Bermúdez et al. (2023).

2.2 Scenarios and optimisation approach

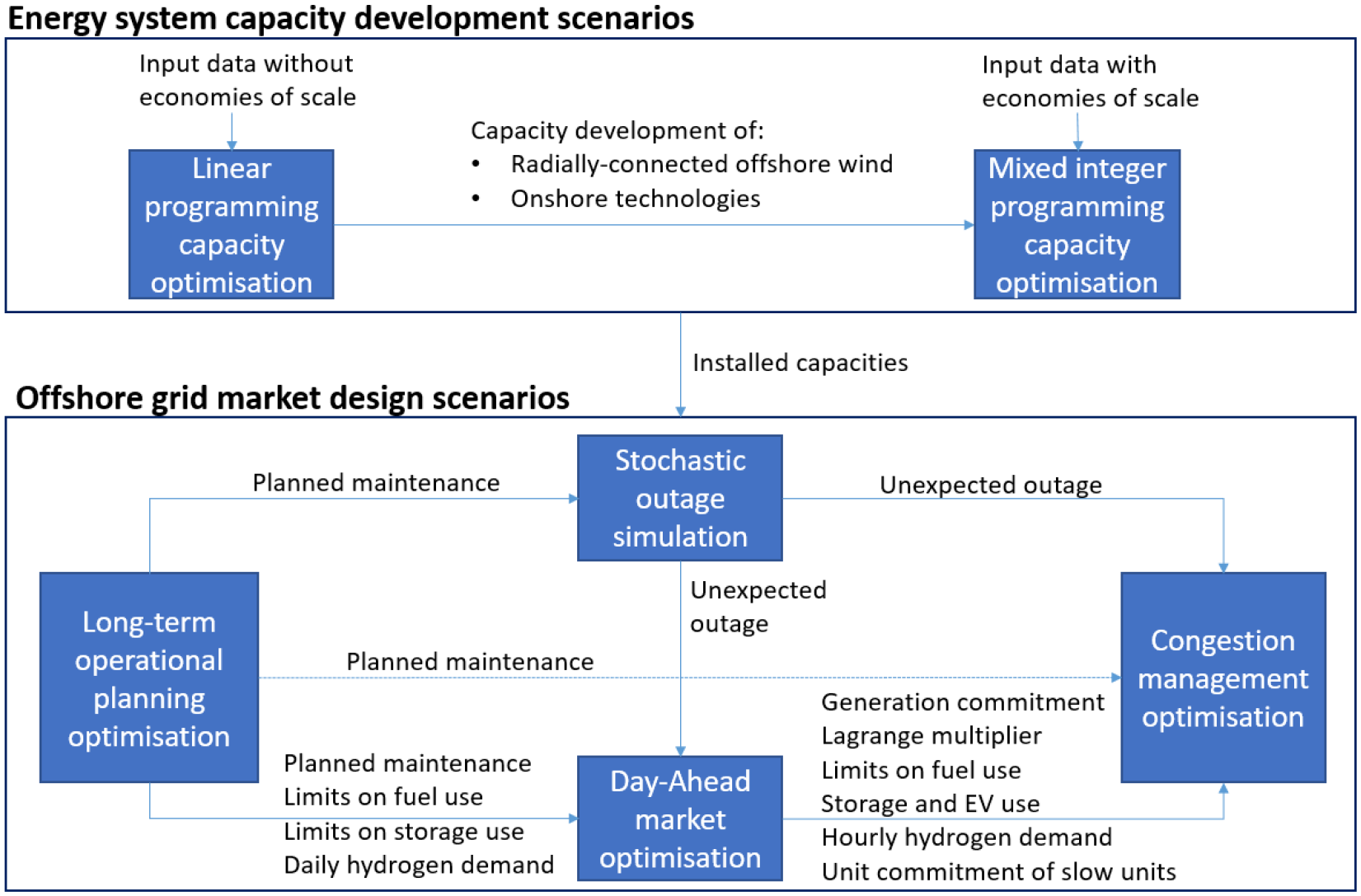

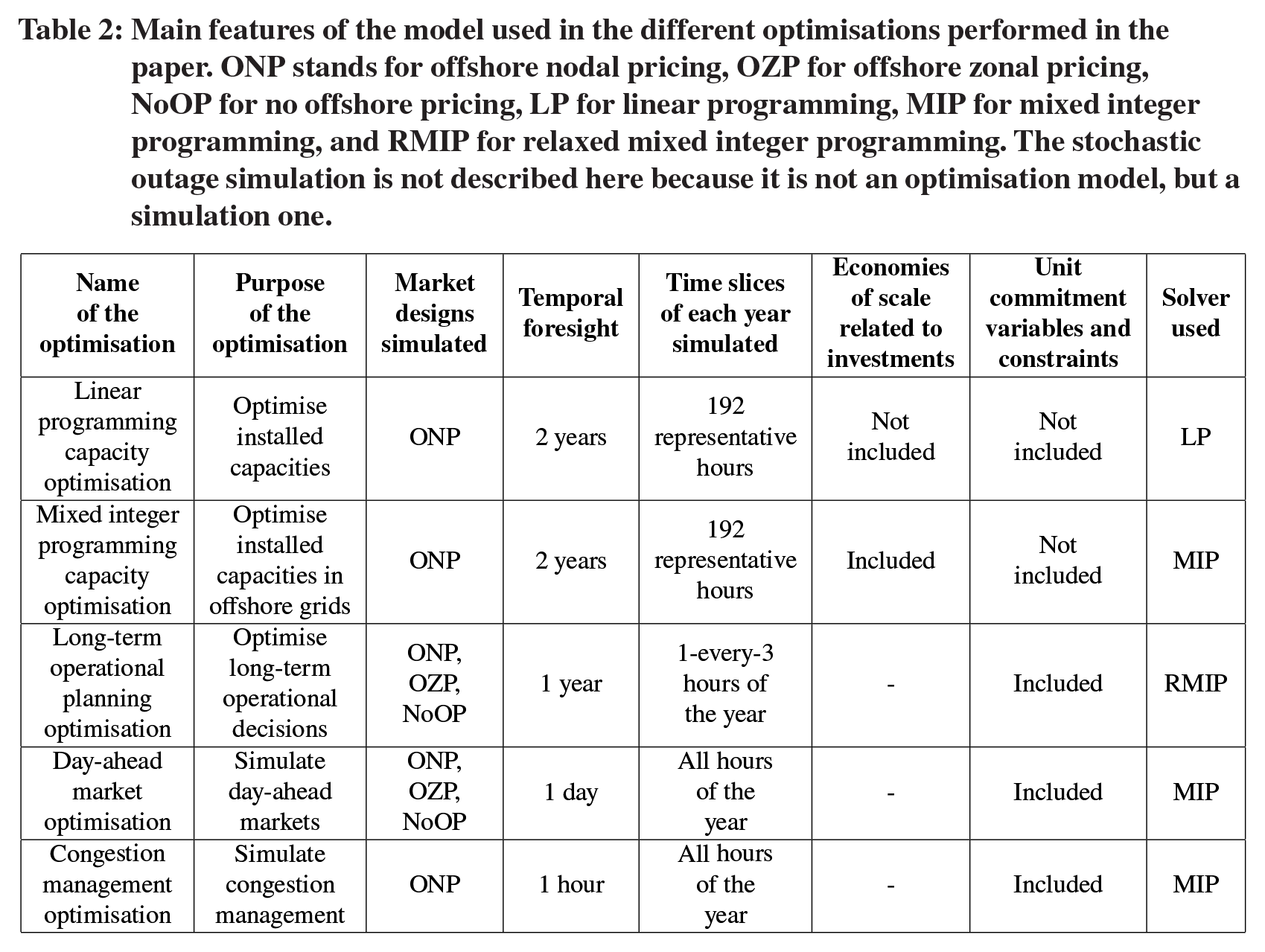

The purpose of this paper is to investigate the impact that different offshore electricity market designs have on integrated energy systems towards 2050, as well as their influence on the required congestion management of the system. To achieve this objective a sequence of optimisations and simulations, illustrated in Figure 4, are performed. Each optimization applies a different configuration of the Balmorel model. The main features of the model used in the different optimisations are presented in Table 2.

Optimisation sequence and input/output flow applied to derive the scenarios of this paper. The optimisation sequence used for the capacity development scenarios is described in Section 2.2.1, and the one used for the market design scenarios is described in Section 2.2.2. EV stands for electric vehicles.

Main features of the model used in the different optimisations performed in the paper. ONP stands for offshore nodal pricing, OZP for offshore zonal pricing, NoOP for no offshore pricing, LP for linear programming, MIP for mixed integer programming, and RMIP for relaxed mixed integer programming. The stochastic outage simulation is not described here because it is not an optimisation model, but a simulation one.

First, we derive energy system capacity development scenarios towards 2050, where off-

shore grid development can take place. For this purpose, two main scenarios are created:

The

Compared to

These two scenarios can lead to very different configurations, use and purpose of the offshore grids, and therefore, can influence the impact of different offshore market configurations. Details about how the optimisations for these capacity development scenarios are performed can be found in Section 2.2.1.

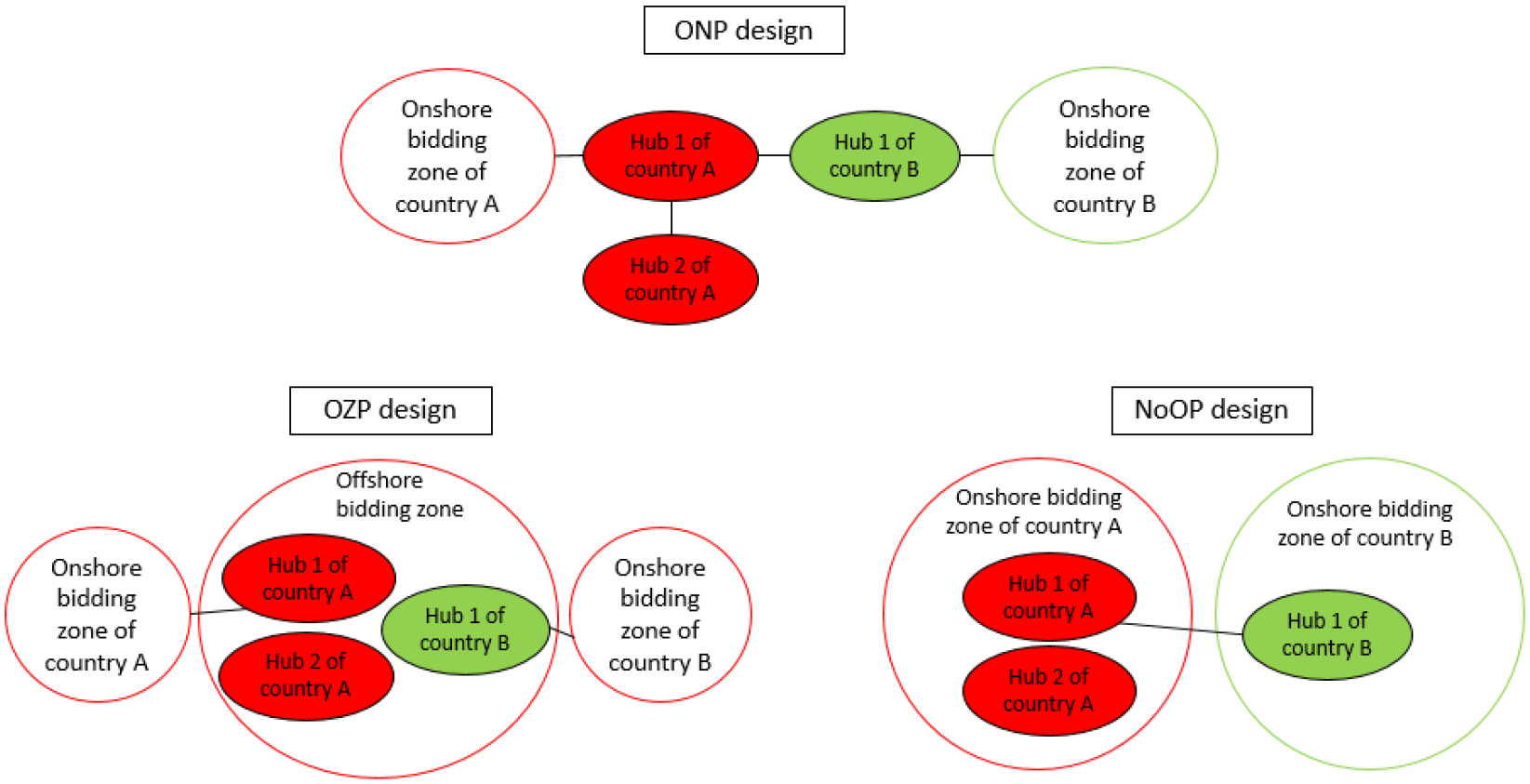

After having derived the capacity development scenarios, we simulate the impact of implementing different day-ahead offshore electricity market designs in each of them. Three offshore electricity market design options are modelled (see Figure 5 for an illustration):

Offshore market designs investigated in the paper. Black lines correspond to the electric interconnectors that are not ignored when using the different market configurations. ONP stands for offshore nodal pricing, OZP for offshore zonal pricing, and NoOP for no offshore pricing.

OZP (offshore zonal pricing): In this market design, all hubs are assumed to form a unique offshore bidding zone. To model this design, we ignore hub-to-hub electricity transmission capacity constraints and losses.

NoOP (no offshore pricing): In this market design, hubs are assumed to be part of one onshore bidding zone of the country they belong to. The corresponding onshore region is the closest one that belongs to the same country, except for Germany, for which the western region (DE-W) is used for simplicity. To model this design, electricity transmission capacity constraints and losses of hub-to-hub electricity interconnectors of hubs that belong to the same corresponding onshore bidding zone, and of hub-to-corresponding onshore bidding zone, are ignored.

Zonal market design is used for onshore regions in all the runs.

After simulating day-ahead markets with different offshore electricity market designs, we then simulate the required congestion management that transmission system operators perform to make sure a feasible dispatch of the units takes place in real time, which is a consequence of having ignored some of the offshore grid electricity transmission lines in the zonal market configurations.

Details about how these market scenarios are created can be found in Section 2.2.2.

2.2.1 Generation capacity development scenarios

Each capacity development scenario is obtained by performing two consecutive optimisations. The first optimisation uses linear programming (LP) and the second optimisation uses mixed integer programming (MIP). The objective of the LP optimisation is to analyse the competition of all the technologies included in the model (including the development of offshore grids), whereas the objective of the MIP optimisation is to model economies of scale of offshore grids to avoid unrealistically small investments in offshore grids. The approach is based on Gea-Bermúdez et al. (2020). In the MIP optimisation, investments, decommissioning, and/or mothballing of almost all technologies are forced from the LP optimisation to reduce calculation time and make the problem solution feasible. The exceptions are: hub-connected units (electrolysers, H2 storage, OWPP, and fuel cells), hub platforms, and offshore H2 pipes and offshore transmission lines in the North Sea. Economies of scale are modelled in offshore electricity transmission lines, offshore H2 pipes and offshore hubs. Because of including all the potential offshore electricity interconnectors in the optimisations, the offshore configuration used in these runs is therefore equivalent to using a

Both MIP and LP optimisations are obtained using limited inter-temporal foresight with a two-year rolling horizon approach similar to Gea-Bermúdez et al. (2023). Since in this paper we run the years 2025, 2035, and 2045, the approach considered translates into optimising 2025 with perfect foresight of 2035, save investment decisions of the year 2025, and then optimise 2035 with perfect foresight of 2045. Therefore, each investment runs includes two subruns: 2025–2035, and 2035–2045. In these runs, the meaning of seasons and terms are weeks and hours of the week, respectively.

Due to the complexity of the MIP and LP runs, only a limited amount of time steps are used in these runs. The time steps are selected with the approach described in Gea-Bermúdez et al. (2020). In the LP and MIP runs, we use 8 weeks that are spread over the year, the days of the week Thursday, Friday, Saturday, and 1 every 3 hours of each of those days, resulting in 192 time slices per year. Using the methodology described in Gea-Bermúdez et al. (2020), the time series are scaled using probability integral transformations to maintain the annual statistical properties of the original hourly time series. Weather data from several years (40 years for wind and solar PV) is used in the scaling of the time series to improve VRE representation in the reduced amount of time steps used. EV profiles and seasonal hydro inflow are scaled in a different way though for simplicity due to their modelling being different to the rest of the time series: EV profiles correspond to the average of three-consecutive-hour time steps, and seasonal hydro inflow is linearly scaled with respect to average annual inflow.

Annual average availability of the generation and storage units, as well as all type of energy

transmission in the model (electricity, H2, and district heating) is assumed for all the time steps used.

Unit commitment constraints, and related variables and costs are not considered in these runs to simplify the problem and make the MIP computational feasible. The impact of this simplification on results should not be high considering the high number of flexibility options that are included in the model (Poncelet et al., 2020).

The key output from this set of optimisations is investments, mothballing, decommissioning, and peak regional H2 demand to generate synthetic fuels for the transport sector towards 2050.

These results are then used as input in the offshore grid market design scenarios.

2.2.2 Scenarios for offshore grid market design

To derive the impact of having different offshore market designs in each of the energy system capacity development scenarios, we perform the following consecutive optimisations/simulations: long-term operational planning optimisation, stochastic outage simulation, day-ahead market optimisation, and congestion management optimisation. The method is inspired (and expanded) from the one used in the scenarios of Gea-Bermúdez et al. (2021).

A large amount of back-up expensive-to-operate fast units (gas turbines for the electricity sector) are added to the scenarios to avoid unmet load due to lack of generation capacity in the system. The lack of generation capacity can be a consequence of having used a reduced amount of time steps when performing the capacity development optimisations. As shown by Gea-Bermúdez et al. (2023), the importance of this back-up capacity is likely to be very small in terms of total generation, and non-negligible in terms of capacity. The investment costs and fixed costs of these back-up units are not reported in the results of the paper based on the assumption that the optimal installed capacity of these units would not be highly affected by the actual market design, and that would mainly be driven by security of supply standards.

The objective function of these runs is to minimise the variable operational costs of each analysed year. The years are optimised in parallel to speed up the runs.

Generation units are assumed to have full availability, whereas all type of energy transmission in the model (electricity, H2, and district heating) are assumed to have annual average availability in each time step. Unit commitment constraints (minimum fuel generation, minimum time on/ off, and ramping limitations), and related variables and costs are considered in this runs. However, to reduce the complexity of the optimisation, the commitments of the units in the different seasons are not linked (i.e. the on/off status of one season disregards what happened in previous seasons). To help computational speed, we relax integer variables. Relaxing the integer variables is likely not to have a significant impact on the key output from these runs (Gea-Bermúdez et al., 2021).

In these runs, offshore grids are modelled using the three different market designs for each capacity development scenario to reflect that optimal long-term operational decisions are likely to be affected by the actual day-ahead offshore electricity market design.

The objective function of these runs is to minimise the variable operational costs (fuel

costs, CO2 tax, etc.) of each day, starting with the optimisation of the first day of the year and ending with the last one. The years are optimised in parallel to speed up the runs.

Unit commitment constraints (minimum fuel generation, minimum time on/off, and ramping limitations) and related variables and costs are considered in this run. The commitment of the units in the different seasons are linked, which means that the on/off status in one season is limited by the on/off status in previous seasons.

From the corresponding stochastic outage simulation, this run uses as input the hourly stochastic outages.

Based on the results of the corresponding long-term operational optimisation, the dayahead optimisation run sets limits to the seasonal use of fuels with annual restrictions, forces the energy content of storage units at the beginning of each day and the planned maintenance during the year, and forces the total daily H2 demand to generate synthetic fuels for the transport sector, although its distribution along the day is optimised.

In these congestion management runs, we use the

To simulate the behaviour of congestion management markets, the optimisations are performed using a seasonal rolling horizon approach of one hour of foresight, assuming this market takes place one hour before delivery.

A penalty (additional cost) is added to the objective function to reflect the payment that transmission system operators would need to make to the units that have been asked to generate less energy than the commitments made in the day-ahead market, i.e. the constrained off payment. The value of such penalty for each year y, technology t, output commodity (electricity, heat, H2, or SNG) c, and hour h is the Lagrange multiplier

The resulting objective function in the model for the congestion management runs is Equation 3, which minimises, in each hour h, the total variable operating and maintenance costs of the system

The total penalty is calculated using the non-negative variable

Unit commitment constraints (minimum fuel generation, minimum time on/off, and ramping limitations), and related variables and costs are considered in this run. The commitment of the units in the different seasons are linked, which means that the on/off status in one season is limited by the on/off status in previous seasons. The on/off commitment of the units whose technical characteristics are assumed to prevent them from being able to generate from 0 to full capacity in 1 hour is forced to be the same as the one from the corresponding day-ahead market optimisation. The rest of the units are allowed to deviate if found optimal.

The use of all sort of units with storage (including EVs) is forced from the corresponding day-ahead market optimisation. The hourly H2 demand for synthetic fuel generation for the transport sector is also forced to be the same as the one from the corresponding day-ahead market optimisation. Additionally, the use of fuels with annual restrictions is also limited in each season from the corresponding day-ahead market optimisation.

This run uses as input the stochastic outage from the corresponding stochastic outage simulation, and forces the planned maintenance during the year from the corresponding long-term operational planning optimisation.

In summary, this run represents an energy system where the system operator aims to minimise costs, has one-hour foresight, has control of all the units in the system, and can modify the generation of the units (and the on/off status of relatively fast units) as long as it compensates them so their final profit is not lower than the one expected from the actions on the day-ahead markets.

3. Results

This section summarises and discusses the results obtained from the different optimisations. It focuses first on the two capacity expansion scenarios and continues with the answers to the research question, i.e. the impact of different offshore zonal market configurations on prices and system costs. The section also includes a critical reflection on key modelling assumptions. All monetary values are provided in €2016.

3.1 Energy system capacity development scenarios

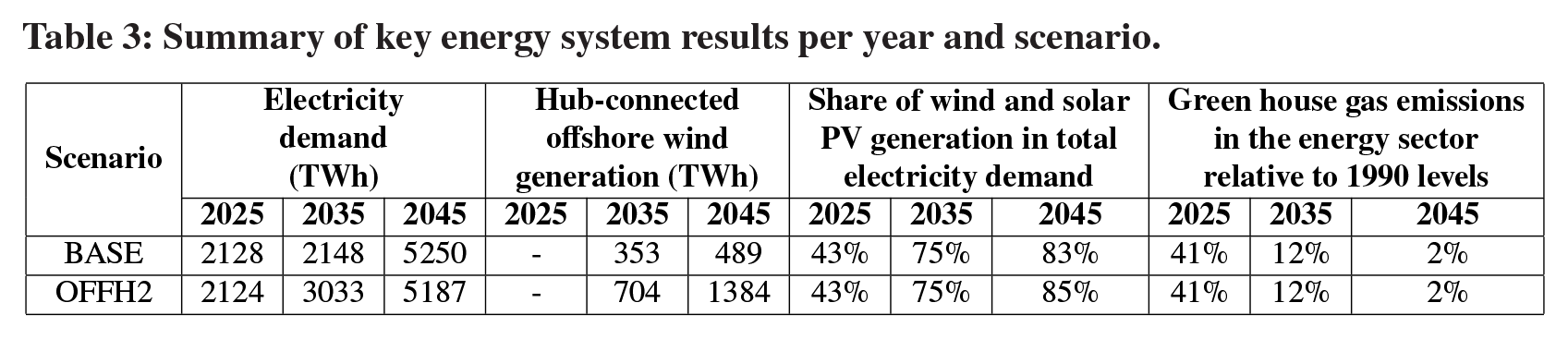

The energy system of both scenarios (

Summary of key energy system results per year and scenario.

The scenarios are therefore very similar in terms of annual electricity demand, annual emissions, and annual wind plus solar PV generation.

Part of the offshore wind development in the scenarios takes place in offshore grids. However, investments in hub-connected offshore wind only take place from 2035 onwards. This result is likely to be related to offshore wind being more expensive than other competitors like solar PV or onshore wind.

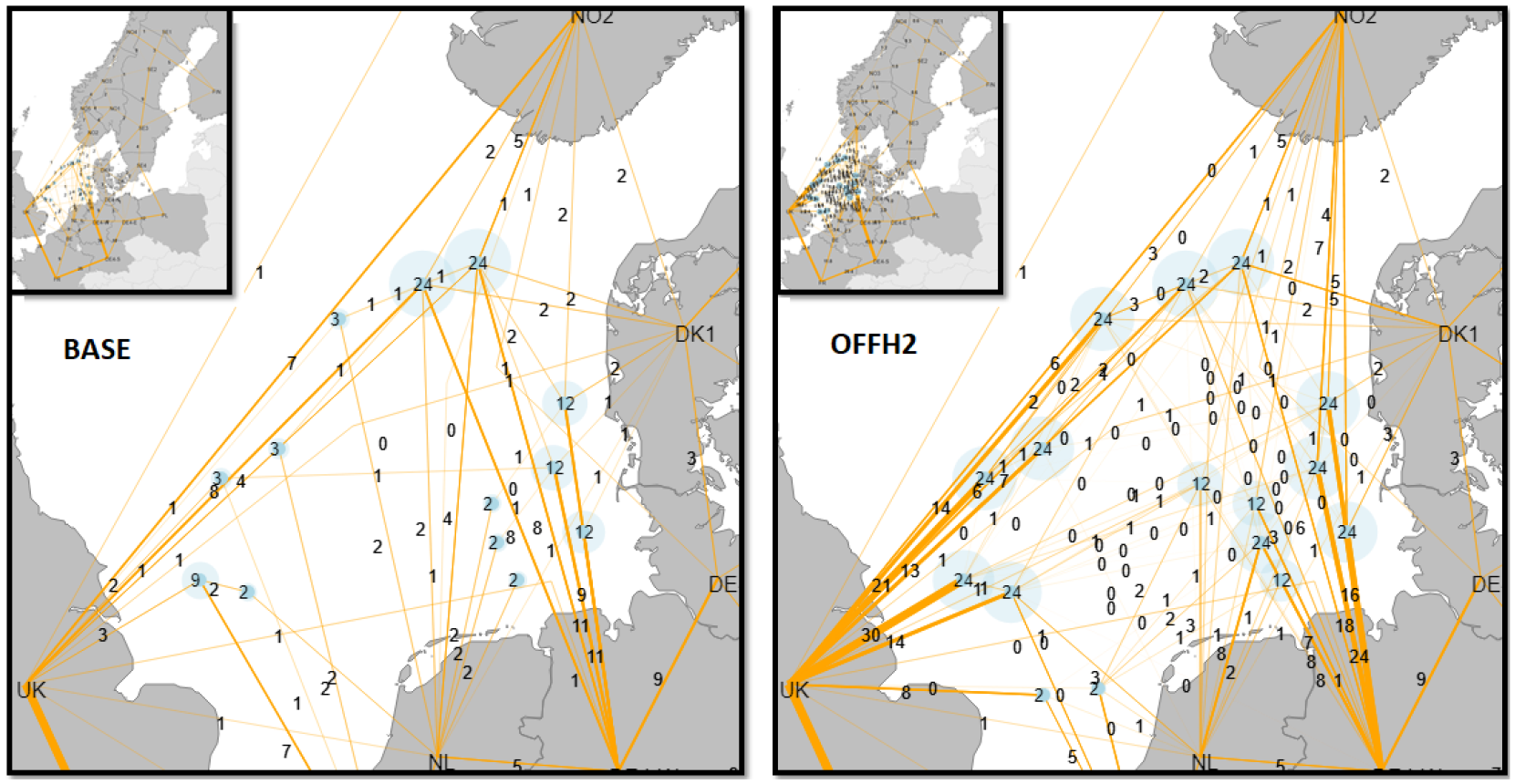

The development of the offshore grid is considerably different in the two studied scenarios (Figure 6 and Figure 7). In the

Transmission map of the studied North Sea region for each scenario in 2045. The space that hub-connected wind farms would require are depicted in the light blue circles, whereas the total hub-connected wind farm capacity is shown as numbers in the middle of such circles, which represents the location of the hub. Transmission lines, (i.e. interconnectors) are depicted in orange. The unit for all the numbers is GW. All numbers have been rounded to the unit. The entire energy system modelled is shown in the upper left corner of each figure.

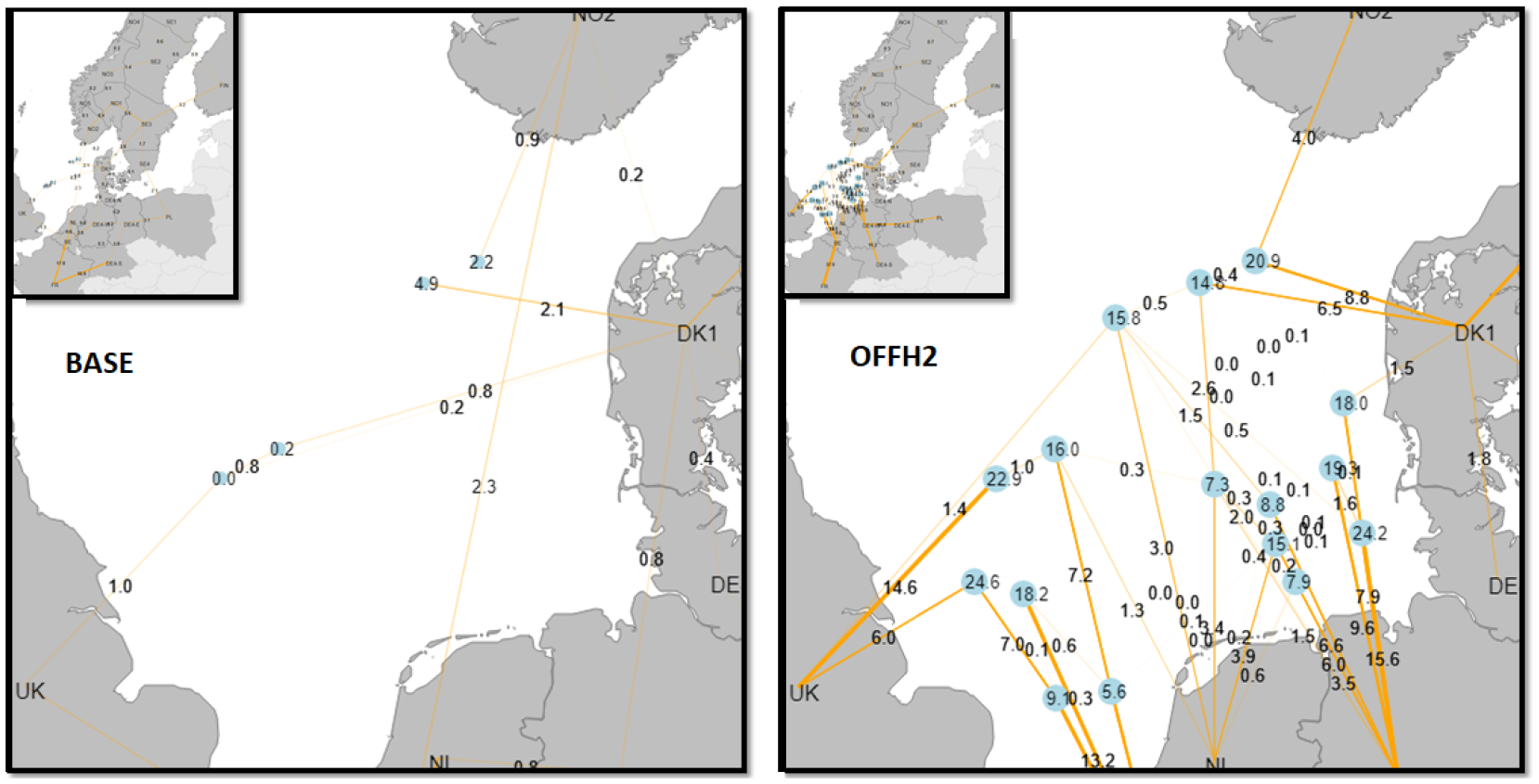

Hydrogen grid by 2045 and scenario. Hubs with electrolyser capacity are depicted as blue dots and hydrogen pipes as yellow lines. The hubs without electrolyser capacity are not shown. The total electrolyser capacity in each hub is the number that is in the middle of the blue dots, whereas the numbers that are on top of the orange lines correspond to the hydrogen pipe capacity. The unit for all the numbers is GW. The numbers have been rounded to the first decimal. The entire energy system modelled is shown in the upper left corner of each figure.

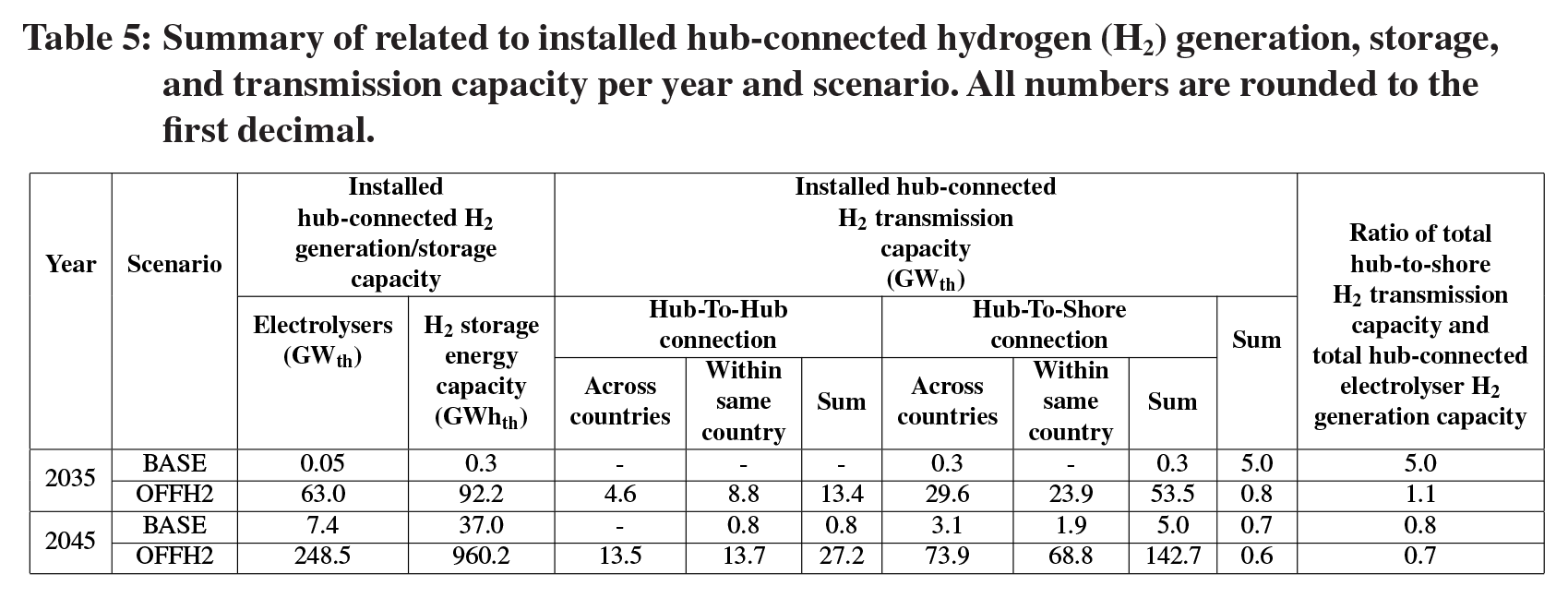

The level of H2 generation taking place in the hubs is very different between the two scenarios. In the

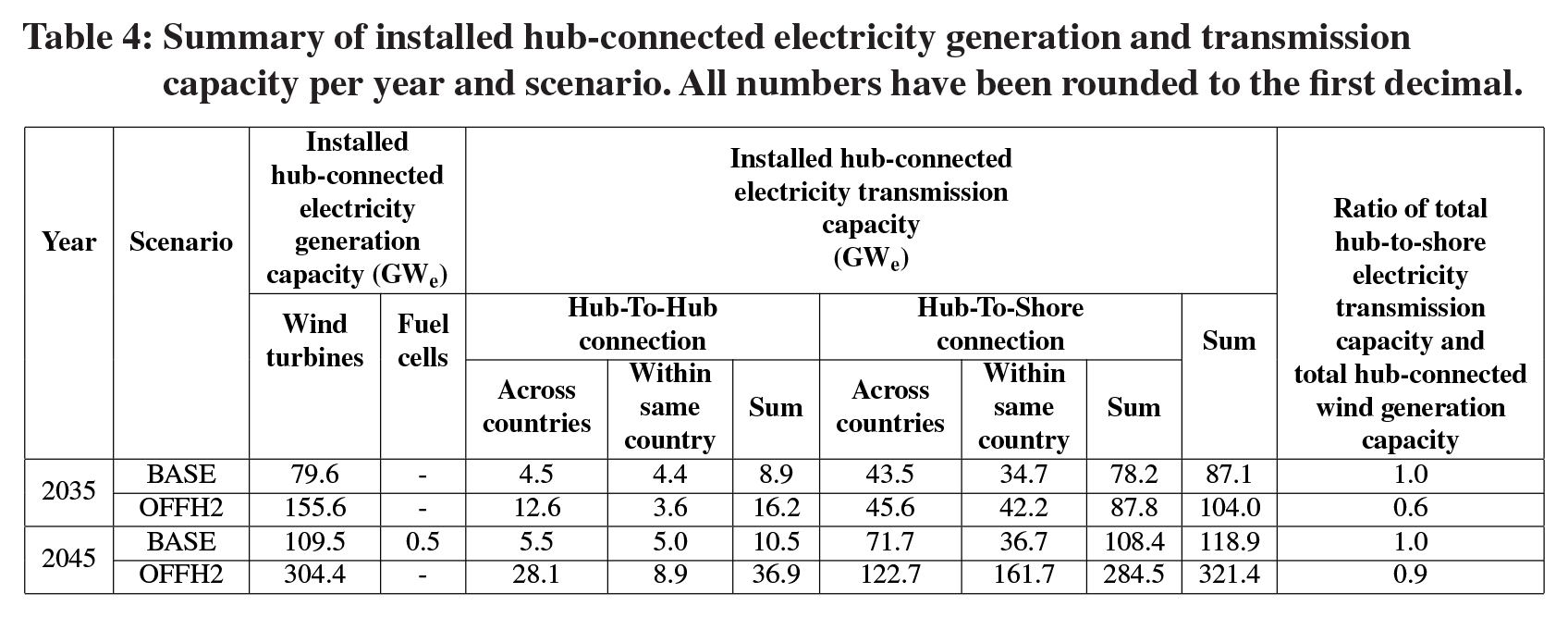

The different role that offshore H2 generation plays in the scenarios has a strong influence on the design of the electricity infrastructure of offshore grids. For instance, the ratio of hub-connected electricity transmission capacity and hub-connected wind capacity is around 1 in the

Summary of installed hub-connected electricity generation and transmission capacity per year and scenario. All numbers have been rounded to the first decimal.

Summary of related to installed hub-connected hydrogen (H2) generation, storage, and transmission capacity per year and scenario. All numbers are rounded to the first decimal.

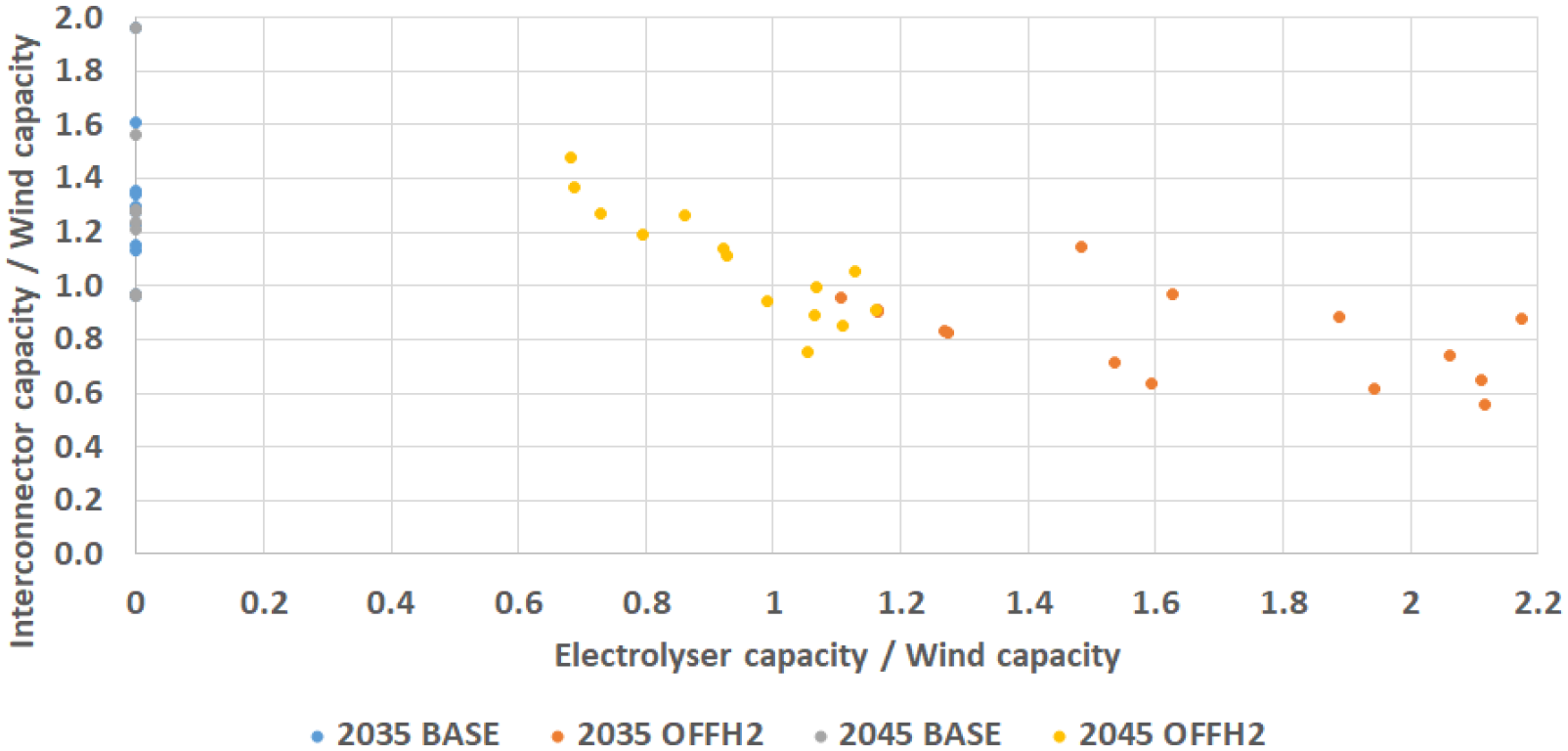

In scenario

Ratio of aggregated electricity interconnector capacity and installed wind capacity in each hub versus ratio of installed electrolyser electricity input capacity and wind capacity in each hub per scenario and year. Each dot corresponds to an offshore hub. The aggregated electricity interconnector capacity of each hub is calculated by adding all the electricity interconnectors connected to that hub. The y axis has been limited to 2, and the x axis to 2.2 to show the most representative values.

The two scenarios, therefore, show different offshore grid configurations that are likely to be relevant when investigating the impact of the electricity offshore market design towards 2050.

3.2 Impact of offshore grid electricity market design

The results show that different offshore market designs have a significant influence on the energy system towards 2050. 4 The impact on day-ahead markets, and on congestion management is presented below. For the sake of space limitations, we focus the analysis on the electricity side.

3.2.1 Impact on day-ahead markets

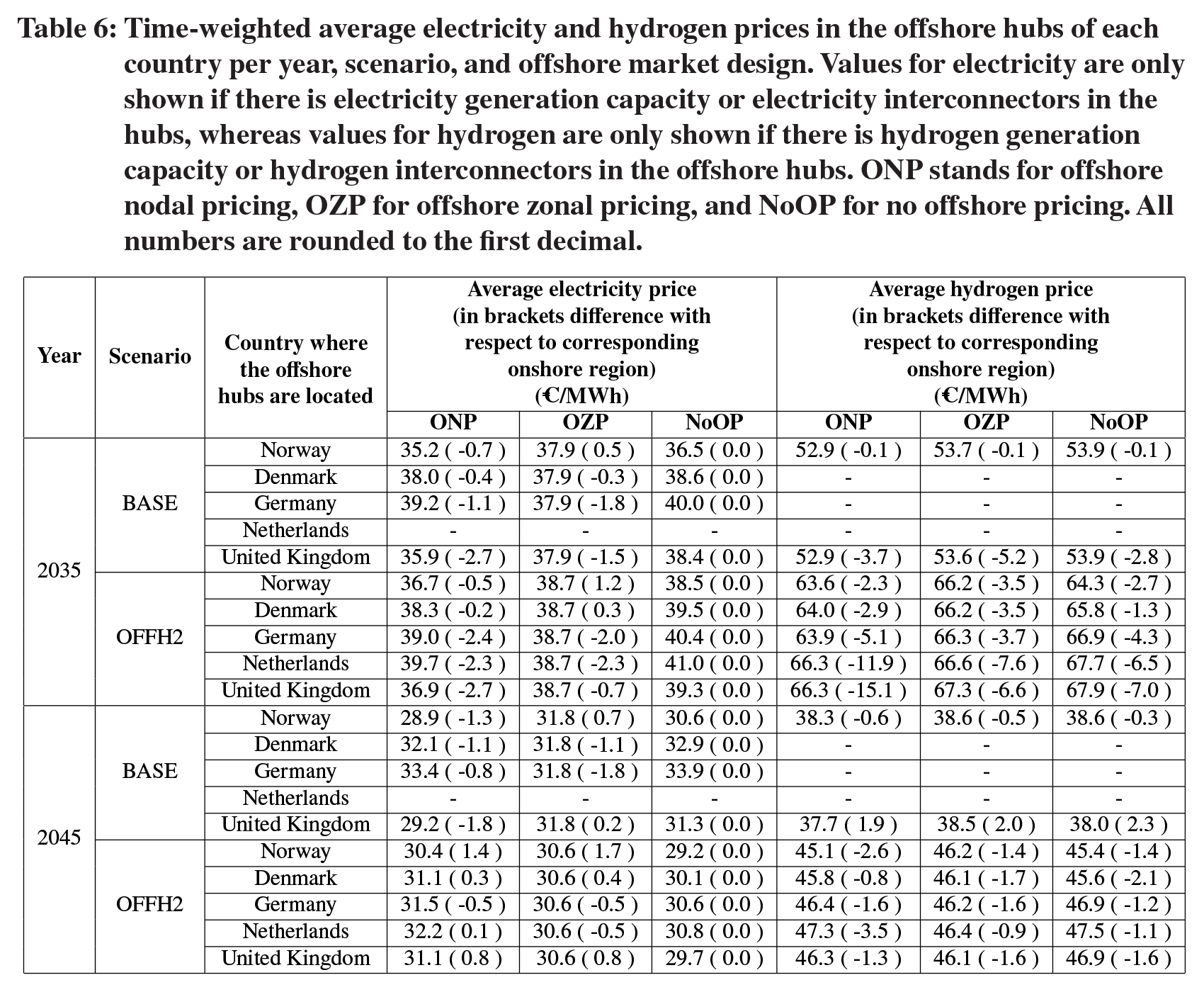

The impact of the offshore grid electricity market design on the average day-ahead electricity prices and on the average day-ahead H2 prices (Table 6) is highly dependent on the year, region and capacity development scenario. In the studied years of the

Time-weighted average electricity and hydrogen prices in the offshore hubs of each country per year, scenario, and offshore market design. Values for electricity are only shown if there is electricity generation capacity or electricity interconnectors in the hubs, whereas values for hydrogen are only shown if there is hydrogen generation capacity or hydrogen interconnectors in the offshore hubs. ONP stands for offshore nodal pricing, OZP for offshore zonal pricing, and NoOP for no offshore pricing. All numbers are rounded to the first decimal.

The average price difference of offshore hubs with their corresponding onshore region (Table 6) is highly dependent on the scenario and market design. Overall, average prices in the offshore hubs are lower than in their corresponding onshore regions, which is an expected result considering the higher likelihood of curtailment in the offshore hubs due to electricity line congestion. However, in a few cases the average prices in the offshore regions are higher than in their corresponding onshore region. The difference in electricity prices is overall limited, ranging from –2.7 to 1.7 €/MWh in the different scenarios and years, and considerably higher for H2 prices, ranging from −15.1 to 2.3 €/MWh.

H2 prices are likely to be highly linked to electricity prices, but may have been affected by H2 pipeline congestion and H2 storage. At the same time, electricity prices in the hubs may have been affected by H2-related technologies, specially in scenario

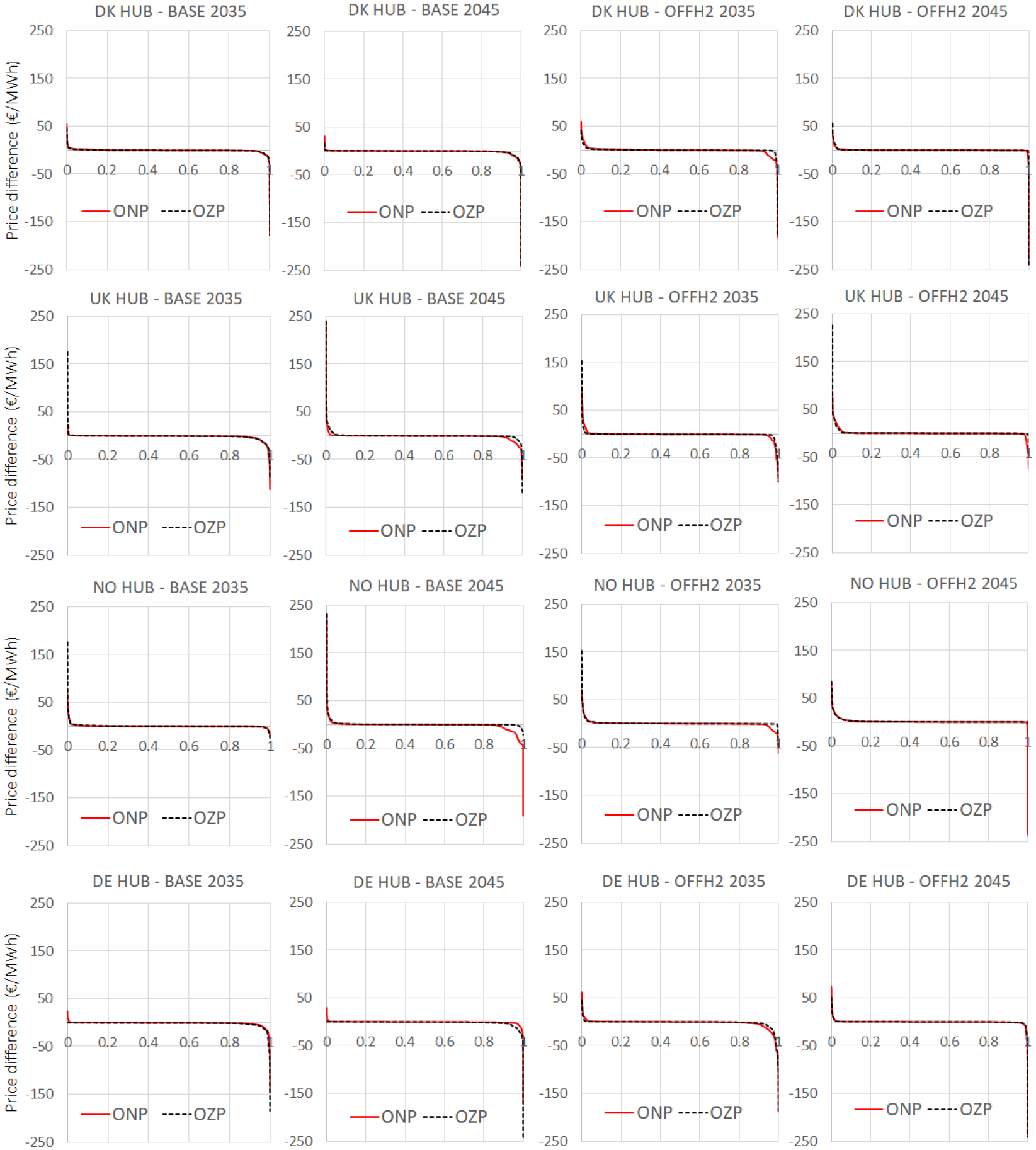

The analysis of the hourly distribution of the difference in electricity price of the offshore hubs with their corresponding onshore region shows that in most of the hours the difference is very small, which explains the limited average difference. This suggests that offshore prices are set by onshore prices in most of the hours (Figure 9). The analysis also shows that there is a higher number of hours with lower electricity price in the hubs than in their corresponding onshore region, which explains that the difference in average prices is generally negative. This result is most likely linked to curtailment taking place in the hubs due to electricity line congestion. Figure 9 also shows that, overall, when using market design

Ranked difference between electricity price in selected offshore hubs and the price in their corresponding onshore region per scenario, market design, and year. The difference when using market design NoOP (no offshore pricing) is 0, and hence, not shown. Only 4 out of 16 hubs are shown for illustrative purposes. ONP stands for offshore nodal pricing, OZP for offshore zonal pricing, DK for “Denmark, “UK” for the United Kingdom, NO for Norway, and “DE” for Germany.

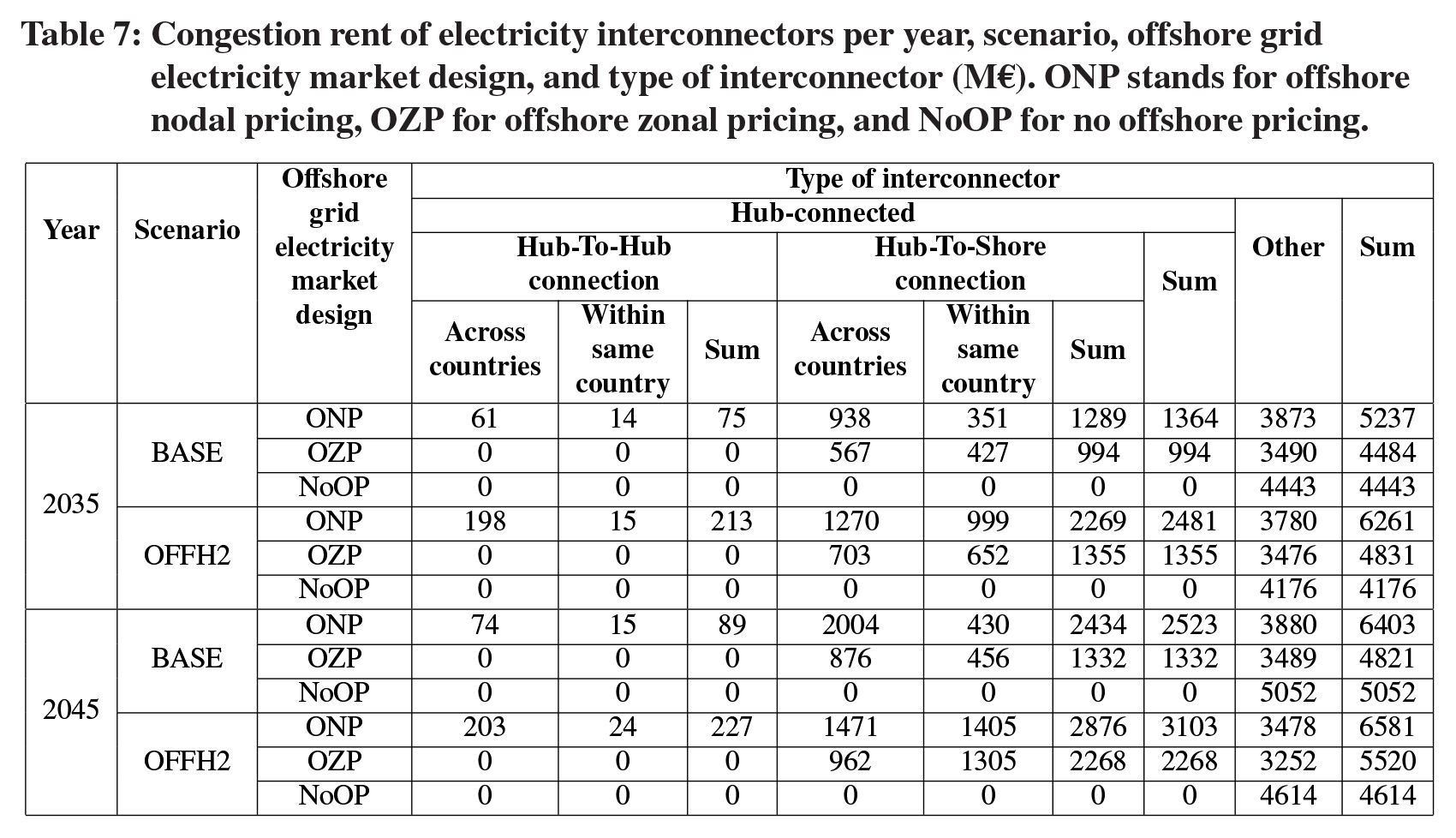

The offshore grid electricity market design has a significant impact on the congestion rent of electricity interconnectors (Table 7). In all the scenarios, the market design

Congestion rent of electricity interconnectors per year, scenario, offshore grid electricity market design, and type of interconnector (M€). ONP stands for offshore nodal pricing, OZP for offshore zonal pricing, and NoOP for no offshore pricing.

In day-ahead markets alternative market designs to

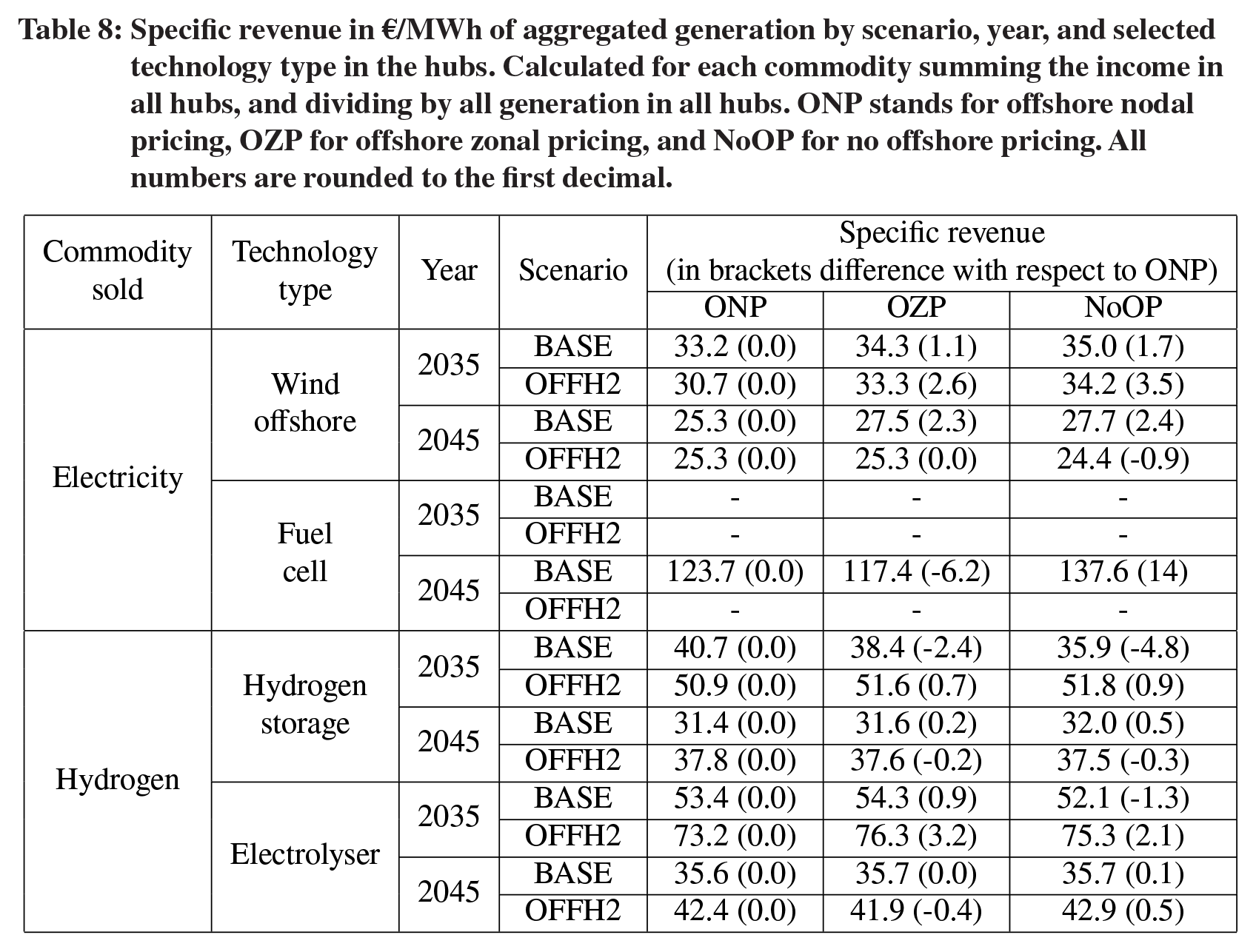

Specific revenues (also known as capture prices) of hub-connected technologies in dayahead markets are highly dependent on the technology studied, the capacity development scenario, the year, and the offshore market zone configuration (Table 8). The results for the different technologies are likely to be affected by the already discussed factors that influence average prices. Particularly, the difference in specific revenue of hub-connected offshore wind farms using alternative market design to

Specific revenue in €/MWh of aggregated generation by scenario, year, and selected technology type in the hubs. Calculated for each commodity summing the income in all hubs, and dividing by all generation in all hubs. ONP stands for offshore nodal pricing, OZP for offshore zonal pricing, and NoOP for no offshore pricing. All numbers are rounded to the first decimal.

The total electricity demand in day-ahead markets is also affected by the market configura-

tion. The price-responsive electricity demand, part of it linked to sector coupling (EVs’ net charging, power to electricity, power to hydrogen, and power to synthetic natural gas) is highest when not using

These results suggest that the overall energy system development and the flexibility in it can have a large impact on the influence that offshore electricity market design has on congestion rents, the specific revenue of the hub-connected units as well as on the prices.

3.2.2 Impact on congestion management

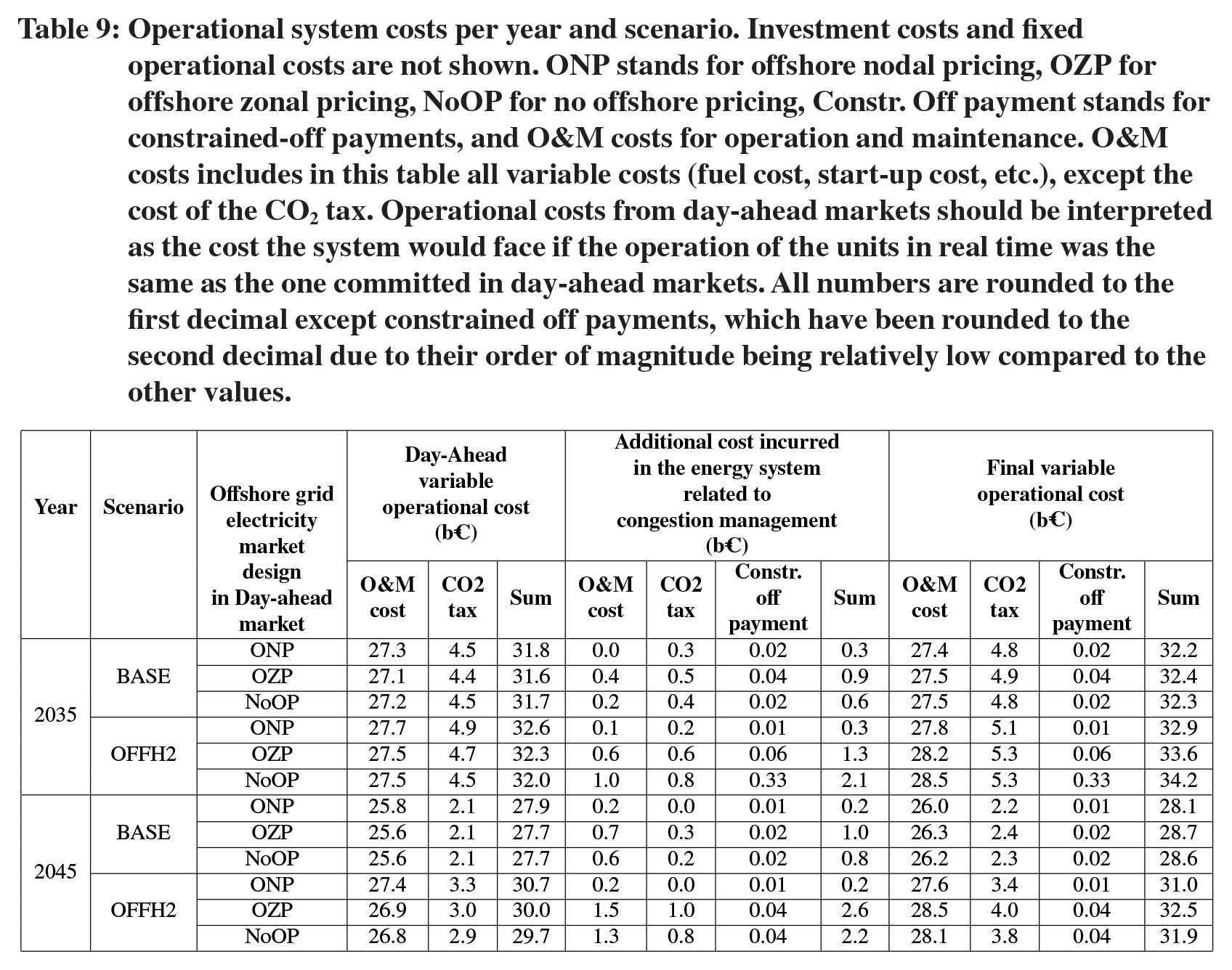

In terms of variable operational system costs (Table 9) the results show that the offshore electricity market design that leads to the lowest final energy system costs is the

Operational system costs per year and scenario. Investment costs and fixed operational costs are not shown. ONP stands for offshore nodal pricing, OZP for offshore zonal pricing, NoOP for no offshore pricing, Constr. Off payment stands for constrained-off payments, and O&M costs for operation and maintenance. O&M costs includes in this table all variable costs (fuel cost, start-up cost, etc.), except the cost of the CO2 tax. Operational costs from day-ahead markets should be interpreted as the cost the system would face if the operation of the units in real time was the same as the one committed in day-ahead markets. All numbers are rounded to the first decimal except constrained off payments, which have been rounded to the second decimal due to their order of magnitude being relatively low compared to the other values.

In day-ahead markets, the

The lower costs in day-ahead markets for

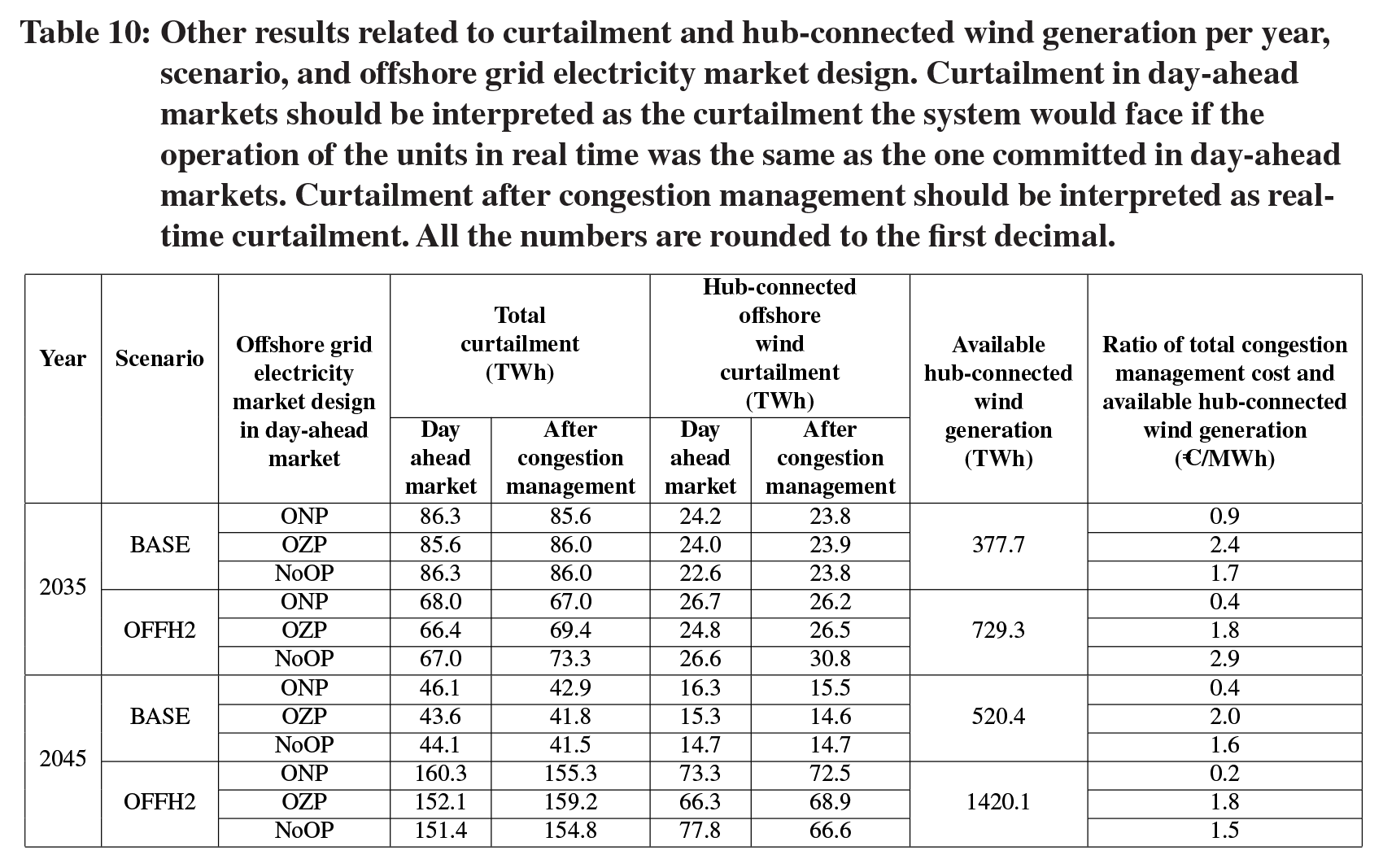

Other results related to curtailment and hub-connected wind generation per year, scenario, and offshore grid electricity market design. Curtailment in day-ahead markets should be interpreted as the curtailment the system would face if the operation of the units in real time was the same as the one committed in day-ahead markets. Curtailment after congestion management should be interpreted as realtime curtailment. All the numbers are rounded to the first decimal.

In terms of final variable operational costs, the worst market design for the

The congestion management costs are in absolute numbers higher in the scenario

When calculating the ratio between congestion management cost and the total available hub-connected wind generation (Table 10), the results show relatively similar order of magnitude for both scenarios when not using

The curtailment after congestion management has taken place (Table 10), i.e. curtailment in real time, is also highly dependent on the scenario, market design, and year. These results are highly influenced by the constrained-off payment of the different VRE technologies when using different market designs (which is linked to day-ahead prices), and the congestion of the lines after congestion management is applied. For instance, if in a particular hour day-ahead prices seen in the hubs are high, the penalty for constraining-off the generation of hub-connected wind generators will also be high, and therefore, from a cost-minimisation perspective, curtailment after congestion management is likely to take place only if there is line congestion. It is particularly interesting the case of scenario

Overall, the results obtained are likely to be linked to the magnitude and overall use of the ignored hub-to-hub and hub-to-shore electricity transmission lines in the day-ahead market in the different scenarios, as well as the overall composition of the energy system and the flexibility in it (partly linked to sector coupling). However, it is not straight forward to derive which factor is the main responsible for the results obtained due to the high complexity of the overall studied energy system.

For example, by 2045 in the

The same analysis done by 2045 for the

These results suggest that total ignored offshore transmission line capacity is not the only factor affecting congestion management costs, and therefore, when designing offshore markets, it is likely to be key to identify critical offshore hub-connected transmission lines, i.e. lines that due to the configuration of the integrated energy system are likely to experience high congestion, so they are accounted for in day-ahead markets.

Overall, these results highlight that the impact of the offshore grid market design is highly influenced by the overall configuration of the offshore grid, as well as the rest of the energy system.

3.2.3 Critical reflection

The assumptions of economic rationality and perfect markets are some of the main limitations of the model. Considering that in reality heat markets, electricity markets, and gas market take place with different time schedules during the day could have affected the results of this paper.

In this paper, we have focused on the impact of market design on the operation of the energy system. The modelling of investments has assumed offshore nodal pricing (

This paper has used a single weather year in the scenarios. Considering the uncertainties related to the variation of wind generation along the years could have influenced the design of offshore grids, and hence, the impact of the results of this paper. Future research should take this into account.

The uncertainties related to VRE generation in day-ahead markets have not been considered in this paper. Not considering potential forecast errors could have underestimated the impact of the offshore grid electricity market design. This could be of special important when VRE technologies provide most of the electricity of the system. This aspect should also be considered in future research.

The use of the different storage technologies included in the model for congestion management purposes has not been considered in this paper. Strategic bidding in different markets could potentially reduce congestion management costs, at the expense of increasing costs in day-ahead markets. This could be analysed in future research.

The role that sector coupling has played in providing flexibility to reduce congestion management costs has not been analysed in the paper due to space limitations. Most likely, without flexible electricity load, the congestion management costs of the system would have been higher. This is a topic worth investigating in future research.

The reinforcement of distribution grids has not been considered in this study. Considering the large increase of electricity demand towards 2050 that is part of the scenarios of this paper, it is likely that there will be need for such reinforcement. Without reinforcing distribution grids, it is likely that there will be more wind curtailment, as suggested by Tosatto et al. (2021).

The simplified approach to model energy flows used in the paper, which is based on linear flows using net transfer capacity, is done for the sake of computational complexity. It could have led to too optimistic trading volumes, and hence, underestimated the costs of the energy system. More advanced modelling of electricity, H2, and/or heat flows could further improve the results of the model.

Due to modelling limitations the congestion management cost is not 0 in the

Finally, in this study we assume perfect competition for all market design runs and ignore possible market power execution (discussed in Section 1.1) and strategic bidding of generators that can lead to additional costs for the energy system. And these costs at the end can also vary between different zonal configurations and market designs. However, as the scope of this paper is to derive findings related to a well-regulated market and optimal design, we neglect market power issues and can still hold our main conclusions related to a theoretically and practically optimal market configuration for offshore energy hubs.

4. Conclusions

This paper has investigated the impact of different electricity market offshore designs on the operation of day-ahead markets, as well as the impact on the required congestion management on integrated energy systems towards 2050. We have done this through an advanced optimisation process using the open-source energy system model Balmorel.

Our analysis confirms the well-known concept of nodal pricing as cost-effective market configuration. We show for an advanced and integrated offshore electricity market that offshore nodal pricing (

Price results and congestion rents are highly dependent on the offshore grid and market configuration, and differ between the investigated years. The impact is not uniform across countries. Offshore wind generation volumes are not found to have a significant influence on the congestion management cost per MWh of hub-connected offshore wind.

The impact of different market designs is highly dependent on the overall configuration of the offshore grid, as well as the availability of H2 generation. Higher flexibility in offshore grids and in the rest of the system might reduce the spread between the designs and thus help mitigate implications of suboptimisation.

Our results confirm that nodal pricing in offshore grids is preferable over price zones or no offshore pricing at all. Choosing this market configuration can thus contribute to pave the way for a cost-effective energy transition to carbon neutrality in Europe in 2050.

Supplemental Material

sj-pdf-1-enj-10.5547_01956574.45.4.jgea – Supplemental material for Offshore Market Design in Integrated Energy systems: A Case Study on the North Sea Region towards 2050

Supplemental material, sj-pdf-1-enj-10.5547_01956574.45.4.jgea for Offshore Market Design in Integrated Energy systems: A Case Study on the North Sea Region towards 2050 by Juan Gea-Bermúdez, Lena Kitzing and Dogan Keles in The Energy Journal

Footnotes

Acknowledgements

The authors would like to acknowledge Maksym Pavlyuk’s data support for this paper.

1.

The branch used for the data and code used in this paper is called “H2_Transport_update_2021_JGB” (last access 1st September 2021)

2.

The energy system capacity development scenario for the

3.

The CO2 emissions corresponding to the transport sector that is not part of the model, i.e. the use of traditional fossil fuels for transport, are derived based on [European Environment Agency, 2020]. Additional GHG emissions that are part of the energy sectors covered by the model are estimated assuming that the CO2 emissions are 96.85% of the total GHG emissions of the studied system using data from [European Environment Agency, 2020]

4.

Since there is no offshore grid development in 2025 in the scenarios, the impact of the market design has been run only for the years 2035 and 2045.

5.

Results from day-ahead markets should be interpreted as the costs, generation, curtailment, etc., the system would face if the operation of the units in real time was the same as the one committed in day-ahead markets

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.