Abstract

We estimate the effects of export dynamics on energy consumption using a balanced panel of 95 economies and three subsamples, i.e., low- and lower-middle-income (LMEs), upper-middle-income (UMEs), and high-income (HIEs) from 1997 to 2013. We show the non-linear linkages between export diversification (ED) and energy use. More specifically, we show the inverted-U shape ED effects on energy use per output unit. This result implies the increases in energy inefficiency in the progress of diversification improvement in exports until a threshold level from which ED would help to enhance energy efficiency. Our analysis of the three subsamples shows consistent findings regarding the effects of ED across income levels. The inverted-U shape effects of ED are consistent in LMEs and UMEs, while it is ambiguous in HIEs. The results suggest that low and middle economies should diversify exports as much as possible to pass the threshold, where diversification can improve energy efficiency.

Introduction

Against the backdrop of climate change and global warming, reducing energy consumption is one of the most urgent policy actions (UN, 2020). One feasible option to support this process is to improve energy efficiency, which enhances energy security and economic growth (Le & Nguyen, 2019). Several studies (Nguyen et al., 2018; Phuc Nguyen et al., 2019; Tiba & Frikha, 2018) examine the impacts of economic integration, i.e. trade openness, on CO2 emissions or energy consumption. More recently, Bashir et al. (2020) examined the impacts of export product diversification on energy intensity in a sample of 29 OECD countries from 1990—2015. They find that export diversification (ED) can contribute to decreasing energy and carbon intensity. However, there is no current study on the impacts of ED1 on the efficiency of energy consumption globally. We use energy efficiency instead of intensity in our analysis to better understand the relationship, as efficiency can affect energy intensity, and efficiency improvements in processes and other factors can contribute to changes in energy intensity.2 Since most OECD countries are advanced economies with high development status, they are in the stage of high technological development and energy consumption efficiency. In contrast, developing countries may not be in good condition of technologies or economic development (Canh, Schinckus, et al., 2019; Phuc Nguyen et al., 2019) and thus the effect of ED on energy intensity may not be as found in advanced countries. Moreover, recent studies, e.g., Le et al. (2020) and Canh and Dinh Thanh (2020), emphasize that the export diversification process brings both pros and cons with benefits and costs. Therefore, the ED appears to have non-linear effects on economic factors such as income inequality (Le et al., 2020) and shadow economy (Canh & Dinh Thanh, 2020).

The Export Diversification measures the export product diversification (see https://www.imf.org/external/np/res/dfidimfydiversification.htm)

Energy intensity measures the quantity of energy required per unit of output or activity. In contrast, energy efficiency represents the changes in the amounts of energy inputs or services for a given amount of energy input.

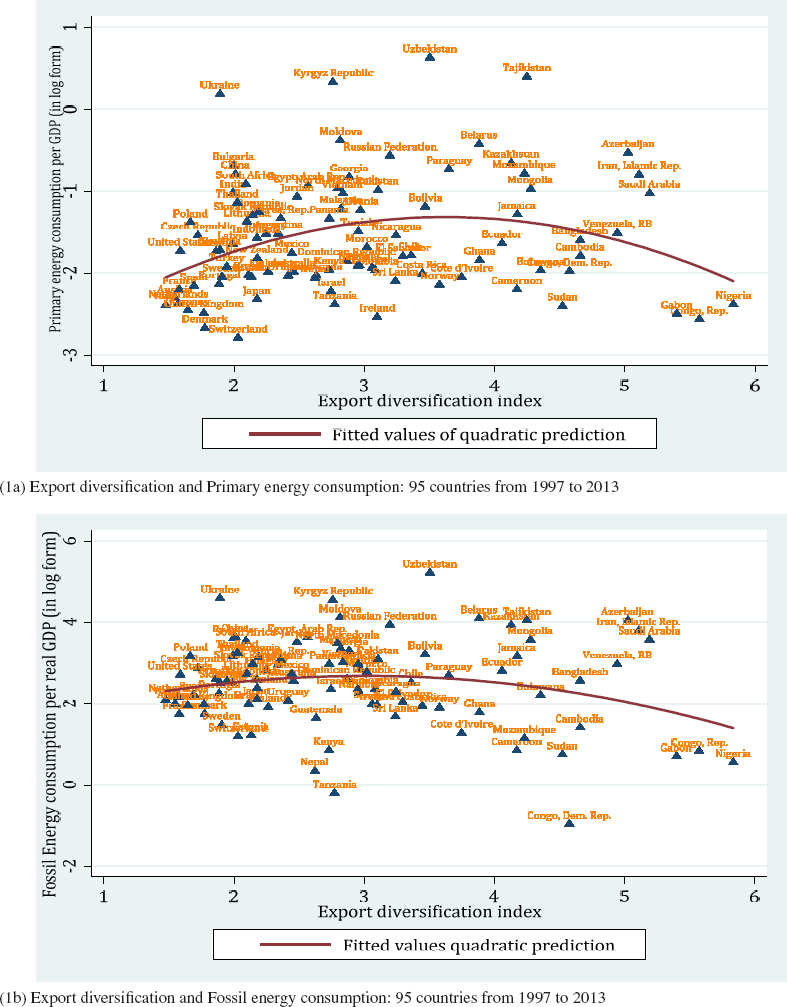

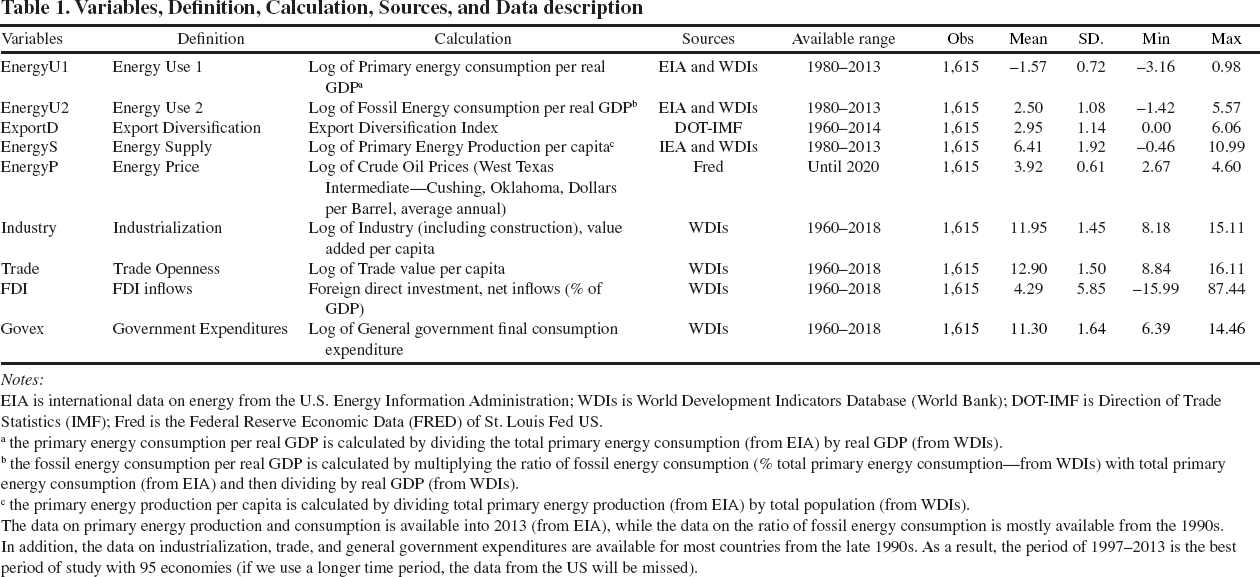

To shed further light on the relationship between export diversification and energy consumption, this paper estimates the effects of export dynamics on energy consumption using a balanced panel of 95 economies and three subsamples, i.e., low- and lower-middle-income (LMEs), upper-middle-income (UMEs), and high income (HIEs) from 1997 to 2013. To motivate our paper, we first present Figure 1, which shows the non-linear (inverted-U shaped) relationships between the export diversification index from IMF and the primary energy consumption per real GDP (Figure la) and fossil energy consumption per real GDP (Figure lb). As defined by the IMF, higher values for the ED index indicate lower diversification.

There are numerous economic reasons that could lead to a non-linear relationship between ED and energy use. For example, although Shahbaz et al. (2019) show that ED increases energy demand in the long run for the US, Le and Nguyen (2019) show that ED might be both beneficial and costly for domestic economic activities. For example, ED might benefit employment (Egger & Etzel, 2012), productivity (Njikam, 2017), poverty reduction (Le et al., 2020), and economic reform (Schrank, 2005). Thus, increases in ED may result in line with investment in technological advancement (Xuefeng & Yaşar, 2016), which enhances energy efficiency as the structural changes in production technology. However, ED is also linked with high initial costs for new production or new market entry (Aw & Lee, 2017; Hoffman et al., 2016), resulting in low technology investment for cost savings. This high cost of the diversification process may lead to the wisdom of "growth first, clean later," as proposed in the Environmental Kuznets Curve hypothesis (EKC). As a result, ED could lead to higher energy inefficiency and, hence, lower energy demand. Consequently, the (non)-linear empirical effects of ED (as measured by the ED index) on energy efficiency depend on various factors one utilizes to analyse the research objectives.

This study differs from previous studies (e.g. Shahbaz et al. (2019) while contributing to the current study on the impacts of ED on energy intensity (see Bashir et al. (2020) by extending the impacts of ED on the efficiency of energy consumption in a global sample. Moreover, we use a global sample and three subsamples, including low- and lower-middle-income (LMEs), upper-middle-income (UMEs), and high-income (HIEs), which broadens the literature on global evidence. The paper adapts a recent study by Canh et al. (2020) in calculating two proxies of energy efficiency, i.e., the efficiency of energy use in production and energy efficiency use in consumption, separately. Notably, we base our empirical approach on a new line of literature on the impacts of ED on economic factors (e.g., Le et al. (2020) and Canh and Dinh Thanh (2020)) to investigate the non-linear impacts of ED on the efficiency of energy use. Empirically, we estimate ED's effects on primary energy use per output unit and fossil energy use per output unit. We control for the effects of energy supply, energy prices, and other factors such as industrialization, FDI inflows, government expenditures, and trade openness. We use 97 countries from 1997 to 2013 as an empirical sample. Due to the availability of energy consumption data, our sample ended in 20133. The panel-corrected standard errors (PCSE) model is applied as the primary estimator to deal with cross-sectional dependence. Moreover, we use the feasible general least squares (FGLS) and two-step GMM models as robustness checks to address heteroscedasticity and endogeneity issues.

This is best period of data from the World Development Indicators database of World Bank (version 2020).

Export Diversification and Energy use: 95 countries from 1997 to 2013

Our main empirical results are as follows. We first document that there are mutual causalities between ED and both variables of energy use. Second, our panel estimation shows the in-verted-U shape effects of ED on energy use per output unit and fossil energy use per output unit, respectively. Consequently, our results indicate that the increases in export diversification may lead to higher energy use (or lower energy efficiency) until a threshold level, from which the increases in export features would enhance the energy efficiency. Third, the estimations for three subsam-ples show consistent inverted-U shape impacts of ED on energy use in LMEs and UMEs, which is unclear in HIEs. The results have two important implications. Firstly, the export diversification strategy should be supported by governments, especially in LMEs and UMEs, as much as possible to overcome the threshold to improve energy efficiency. Secondly, the diversification of exports at the initial stage is one of the causes of environmental degradation due to higher energy consumption: It must be backed by suitable policies for firms to transform their production technology as soon as possible.

The paper is structured as follows. The next section is the literature review. In Section 3, we discussed methodology and data. Results are presented and discussed in Section 4. The final section 5 comes with the conclusion.

The urgency in reducing energy intensity (Sadorsky, 2013) and raising energy consumption efficiency (Bye et al., 2018) are paid more attention to in the literature on energy—and environmental economics than in sustainable development. That is, the understanding of energy use's drivers is paid more attention to energy and environmental economics (Adom & Adams, 2018; Bye et al., 2018; Chen & Lei, 2018). The IPAT model (the Influence, Population, Affluence, and Technology) is first proposed by Ehrlich and Holdren (1971), and then the STIRPAT model (the Stochastic Impacts by Regression on Population, Affluence, and Technology) by Dietz and Rosa (1997), as an extension of IPAT, who have linked the human activities, especially economic activities to environmental degradation. In this line of literature, the impacts of economic activities on energy consumption, which cause CO2 emissions and then global warming and climate change, are paid huge interest, but the conclusions are still mixed (Chen, 2018; Hanif, 2018; Saidi et al., 2017). On the other hand, the Environmental Kuznets Curve hypothesis (EKC) indicates that the relationship between economic development and environmental quality is an inverted-U shape (Rashid Gill et al., 2018; Sun, 1999). The EKC theory explains that energy consumption, such as coal, fuel, and gas, is increased much more in the economic development process of poor economies by the wisdom of "grow first, clean up later" (Rock & Angel, 2007). Environment quality is paid more attention in high-income economies when the country attains a certain threshold of economic development, from which the citizens demand regulatory institutions and actions to protect the environment (Azadi et al., 2011). In addition to the STIRPAT model or EKC hypothesis, other factors, i.e., urbanization (Kasman & Duman, 2015; Zang et al., 2017), industrialization (Jiang & Lin, 2012), economic integration (Phuc Nguyen et al., 2019), shadow economy (Canh, Thanh, et al., 2019) are suggested as drivers of CO2 emissions or energy consumption in general. Recently, Shahbaz et al. (2019) showed that export diversification is linked with higher energy demand in the long run in the case of the US over the period 1975-2016. The features of export activities, i.e., export diversification and export quality, have been an interesting topic in recent years from both international organizations such as the IMF and research attention (Osakwe et al., 2018).

On the one hand, ED positively affects domestic economic diversification (Albassam, 2015), which is linked with new economic activities through entrepreneurship (Schrank, 2005). Contractor and Kundu (2004) indicate that export-led strategies are better at stimulating economic growth than inward-looking ones. ED is also argued as a positive factor in employment (Egger & Etzel, 2012), domestic firm productivity (Njikam, 2017), and economic reform (Schrank, 2005). A higher ED may lead to more economic activities, which might be invested in technological advancement (Xuefeng & Yaşar, 2016). As a result, ED may lead to higher energy efficiency due to structural changes in production. However, ED also has its cons. The literature shows that diversification to a new market or new products is faced with high initial entry costs (Aw & Lee, 2017; Hoffman et al., 2016).

For instance, Fillat et al. (2015) notice that multinational activities come with diversification benefits and fixed—and sunk costs of entry into new markets or products. These costs are primarily exogenous and vary across markets and products; thus, the export-diversification strategy may face more vulnerability. In this vein, Vannoorenberghe et al. (2016) document higher volatility faced by small Chinese firms in expanding the scope of their export partners. Xuefeng and Yaşar (2016) show that a higher cost in the initial stage of export diversification is due to firms' lack of knowledge and experience. Furthermore, ED is also linked with higher international competition from international producers and systematic international risk (Jones et al., 2011). Jones et al. (2011) argue that higher export diversification would imply more significant exposures toward systematic international risks, which could pose local economic agencies in a more challenging and riskier ecosystem by investing in economic activities in low technology to save costs. In the constraints of initial costs and international risk exposures, the new economic activities or the economic transformation of domestic firms may follow the wisdom of "growth first, clean later" as proposed in the Environmental Kuznets Curve hypothesis (EKC).

In contrast, economic activities are executed in high energy inefficiency following export diversification, especially in the initial process. In summary, ED can be hypothesized to cause higher energy use until a threshold, which helps reduce energy use as the higher benefits of ED through the scale of economics. There may be an inverted-U shape relationship between ED and energy use. Therefore, we hypothesize that ED has a non-linear impact on energy use. Furthermore, the increases in ED at the initial stage are linked with high initial costs of entry and competition, while economic agents may follow the EKC hypothesis; thus, they would expand economic activities into high energy-intensive sectors. Therefore, an additional hypothesis can be formed as ED has inverted-U impacts on energy use.

There are already some studies on the non-linear relationship between ED and economic factors, i.e., firm productivity (Xuefeng & Yaşar, 2016) and income inequality (Le & Nguyen, 2019). Nevertheless, there is no study on the non-linear impacts of ED on energy use. The following section presents the methodology and data to investigate the impacts of ED on energy use.

Methodology and Data

In this study, we investigate the non-linear impacts of ED (ExportD) on energy use (Energy U) on energy use with a focus on energy efficiency in producing an output unit by building the function of energy use as follows. First, the energy consumption function has two main control variables: energy supply (EnergyS) (Azam et al., 2015) and energy price (EnergyP) (Omri & Nguyen, 2014). In fact, supply and price are two common drivers of any consumption function of any product.

Our explanatory variables differ from the Stochastic Impacts by Regression on Population, Affluence, and Technology (STIRPAT) model that has been often used in the environmental economics literature. Since our analysis focuses on the energy efficiency in production (energy use per output unit), unlike the STIRPAT, we find that industrialization would be more critical (Lin & Zhu, 2017) than urbanization. Moreover, we normalize our variables per capita, and hence, we also do not include the total population as one of our variables. However, we include Trade openness (Trade), FDI inflows (FDI), and government expenditures (Govex) as control variables for sensitivity check the proxies of economic integration and government role (Phuc Nguyen et al., 2019). More importantly, we include ED and the squared term of ED to examine the non-linear impacts of ED on energy use. The empirical investigation of energy intensity is formed by panel estimation of country level:

in which: i, t denote for country i at year t. α and β are estimated coefficients. γi and ∂ are country and year effects, respectively; ∊it is residual terms.

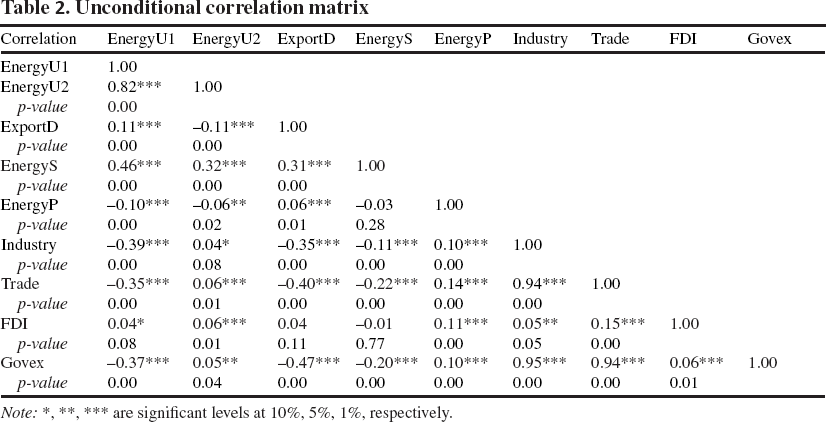

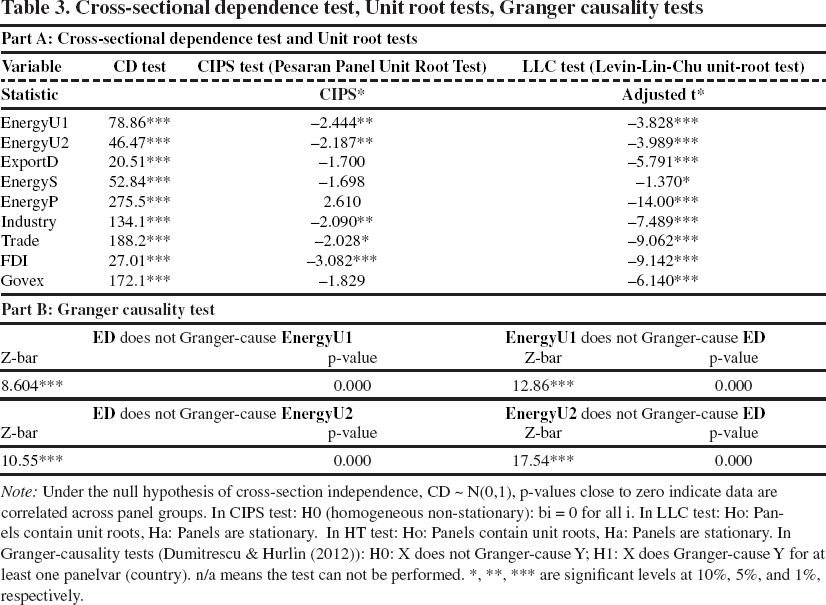

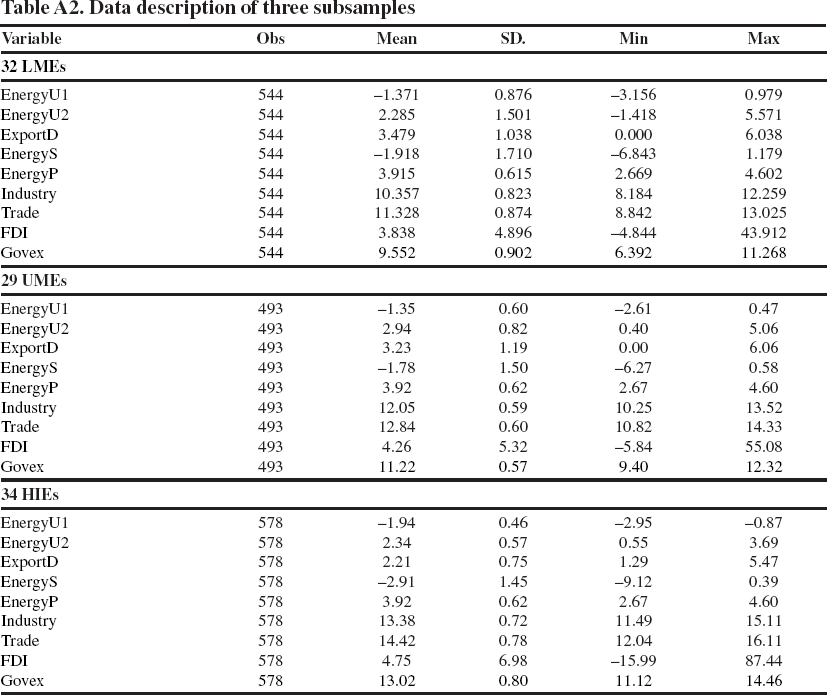

In terms of data, the primary energy consumption and production are collected from the U.S. Energy Information Administration (EIA), which has data until 2013, and most countries have data from the late 1997s. We also collect the fossil energy consumption ratio from World Development Indicators (World Bank) to use as an alternative proxy of energy use besides the primary energy consumption from EIA. The export diversification index is collected from the Direction of Trade Statistics (IMF), which has data until 2014. All remained variables are collected from World Development Indicators (World Bank). The energy use (total primary and fossil energy consumption) is calculated per real GDP. The export diversification is the index from IMF, which is kept as original. The energy supply (primary energy production) is calculated per capita. The industrial value, trade value, and government expenditures are calculated per capita. All variables, excluding the case of export diversification and FDI inflows, are taking in logarithms forms as a standard procedure to normalize data. Due to the availability of data and time constraints of data, the final sample includes 95 countries (see Table Al, Appendix, for list of countries) over the period 1997-2013 (see column 5 in Table 1 for the available time range of each variable). Variables, definitions, detailed calculations, sources, available time range, and data description are presented in Table 1. Moreover, the full sample is divided into three subsamples, including 32 low- and Lower-middle-income economies (LMEs), 24 upper-middle-income economies (UMEs), and 34 high-income economies (HIEs) (see Table A2, Appendix, for the data description of three subsamples). Table 2 reports the unconditional correlation matrix among variables.

Econometrical speaking, our sample has many countries (N=95) but a relatively short time period (1997-2013, i.e. T=17 years). The Pesaran's CD test by Pesaran (2004) is recruited to examine the existence of cross-sectional dependence. The Pesaran (2007)'s CIPS (Z(t-bar)) unit root test and Levin-Lin-Chu unit-root test (Levin et al., 2002) are employed to check the stationarity of variables. Table 3 shows that all variables have cross-sectional dependence, while most are stationary at levels. In this case, the panel-corrected standard errors model (PCSE) estimation is suggested as a suitable estimator for small panel data with short T and large N in the existence of cross-sectional dependence (Bailey & Katz, 2011; Jönsson, 2005; Marques & Fuinhas, 2012), which is recruited as a primary technique in this study.

Variables, Definition, Calculation, Sources, and Data description

Variables, Definition, Calculation, Sources, and Data description

Notes:

EIA is international data on energy from the U.S. Energy Information Administration; WDIs is World Development Indicators Database (World Bank); DOT-IMF is Direction of Trade Statistics (IMF); Fred is the Federal Reserve Economic Data (FRED) of St. Louis Fed US.

the primary energy consumption per real GDP is calculated by dividing the total primary energy consumption (from EIA) by real GDP (from WDIs).

the fossil energy consumption per real GDP is calculated by multiplying the ratio of fossil energy consumption (% total primary energy consumption—from WDIs) with total primary energy consumption (from EIA) and then dividing by real GDP (from WDIs).

the primary energy production per capita is calculated by dividing total primary energy production (from EIA) by total population (from WDIs).

The data on primary energy production and consumption is available into 2013 (from EIA), while the data on the ratio of fossil energy consumption is mostly available from the 1990s.

In addition, the data on industrialization, trade, and general government expenditures are available for most countries from the late 1990s. As a result, the period of 1997-2013 is the best period of study with 95 economies (if we use a longer time period, the data from the US will be missed).

Unconditional correlation matrix

Note:

are significant levels at 10%, 5%, 1%, respectively.

Cross-sectional dependence test, Unit root tests, Granger causality tests

Note: Under the null hypothesis of cross-section independence, CD ∼ N(0,1), p-values close to zero indicate data are correlated across panel groups. In CIPS test: HO (homogeneous non-stationary): bi = 0 for all i. In LLC test: Ho: Panels contain unit roots, Ha: Panels are stationary. In HT test: Ho: Panels contain unit roots, Ha: Panels are stationary. In Granger-causality tests (Dumitrescu & Hurlin (2012)): HO: X does not Granger-cause Y; H1: X does Granger-cause Y for at least one panelvar (country). n/a means the test can not be performed.

are significant levels at 10%, 5%, and 1%, respectively.

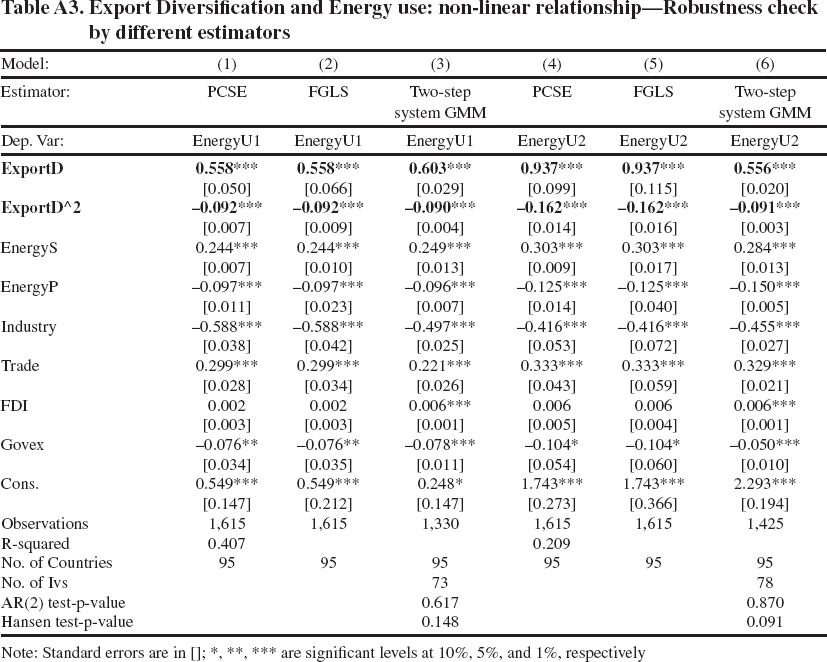

We apply the PCSE model for Eq. [1] with one adjustment to deal with the endogene-ity issue. All independent variables in Eq. [1] are regressed using one-year lags. However, using the PCSE model and one-year lags of independent variables may only partially solve endogeneity. Therefore, we apply the two-step system GMM estimator as a robustness check. The GMM estimator is proposed by Arellano and Bond (1991) and then developed to become system GMM in Arellano and Bover (1995) and two-step system GMM in Blundell and Bond (1998). Two-step system GMM estimator is argued to reduce the bias associated with the fixed effects in short panels (Roodman, 2009). The Feasible Generalized Least Squares (FGLS) (Liao & Cao, 2013; Reed & Ye, 2011; Zhang & Nian, 2013) is also recruited as a robustness estimator to deal with heteroscedasticity in panel data. The study adds control variables one by one to check for the sensitivity of the results. At last, the predictive margins analysis is done for the squared term of ED to illustrate the non-linear impacts of ED on energy use.

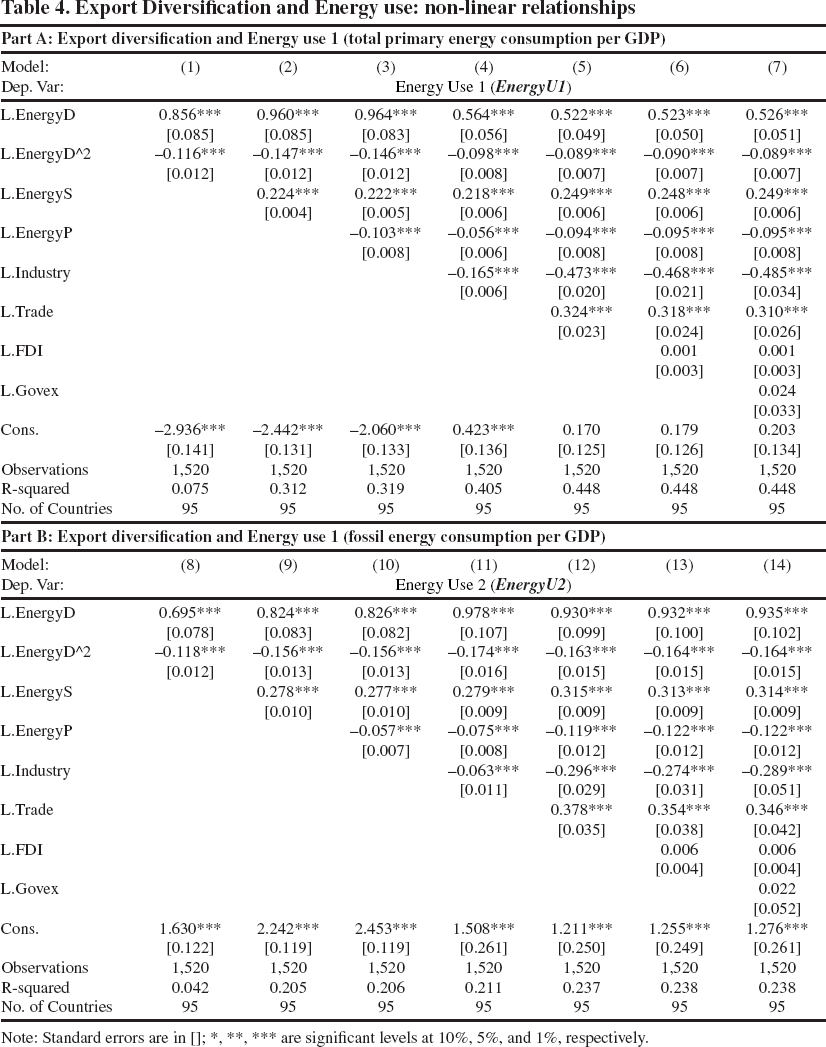

Tables 4 and 5 present the study's main results, while Table A3 in the Appendix reports the robustness check. All results are consistent and robust when each control variable is added to the estimation or by different estimators.

Table 4 reports the impacts of ED on two kinds of energy use, i.e., primary energy consumption per GDP (EnergyUl) in Part A and fossil energy consumption per GDP (EnergyUl) in Part B, in the global sample. In terms of control variables, the energy supply (EnergyS) has significant positive impacts, which implies the increasing effects of a higher energy supply on energy use. The energy price (EnergyP) has a significant negative impact, which means the higher energy price would reduce energy use. These effects are in common wisdom that a higher supply or low price would stimulate the consumption of a product, which is energy. The industry value (Industry) also has a significant negative impact, which suggests that industrialization would reduce energy use per output unit. That is, the increases in industrial sectors would be a more energy efficient one. Trade openness (Trade) and FDI inflows (FDI) have positive impacts but only statistical significance in the case of trade openness. This result implies that higher trade openness may cause higher energy use, while the impacts of FDI are unclear. At last, the government expenditures have positive but also statistically insignificant.

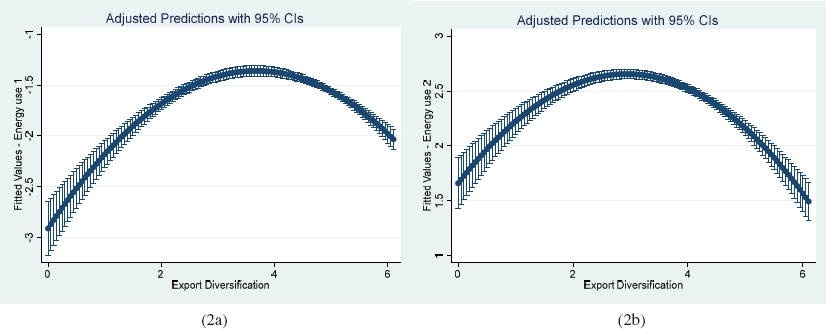

In terms of the main variable, ED has a significant positive impact, while its squared term has significant negative impacts. The results are consistent and robust when each control variable is added. The results are also consistent with different estimations, i.e., PCSE estimator with all independent variables in the current year, FGLS, and two-step system GMM (see Table A3, Appendix, for these results. The results confirm that ED has non-linear impacts on energy use following invert-ed-U shapes. The increases in ED at the initial level would cause higher energy use (or higher energy inefficiency) until a certain level. After that threshold, the increases in ED would help to reduce energy use (or increase energy efficiency). The finding confirms our hypothesis that ED has non-linear influences on energy use following an inverted-U shape. The results are the same for both kinds of energy use (EnergyUl—primary energy consumption per GDP and EnergyU2—fossil energy consumption per GDP). Figure 2, the predictive margins analysis for the impacts of ED on energy use, illustrates these non-linear impacts clearer. Figure 2a illustrates the inverted-U shape impacts of ED on primary energy consumption, and Figure 2b is the case of fossil energy consumption.

The results highlight that the diversification of exports benefits the domestic economy and costs the environment in the initial stage. This finding adds new evidence to the current literature on the non-linear relationship between ED with economic factors such as productivity or income inequality (e.g., see Xuefeng and Yaşar (2016), Le and Nguyen (2019)). The results, on the other hand, highlight an important policy implication. That is, the country with the export-led development strategy in line with export diversification should focus on regulations and supports, especially policies to reduce using fossil energy, for domestic firms in entering new markets or new products, which help reduce initial costs of entry and exposures to global risk. As a result, domestic firms' transformation would lead to low energy-intensive sectors or high technology production. This result will lead to low energy use and environmental protection. Above that, low energy use would improve energy security and stimulate economic growth in the long run (Le & Nguyen, 2019).

Export Diversification and Energy use: non-linear relationships

Export Diversification and Energy use: non-linear relationships

Note: Standard errors are in []; *, **, *** are significant levels at 10%, 5%, and 1%, respectively.

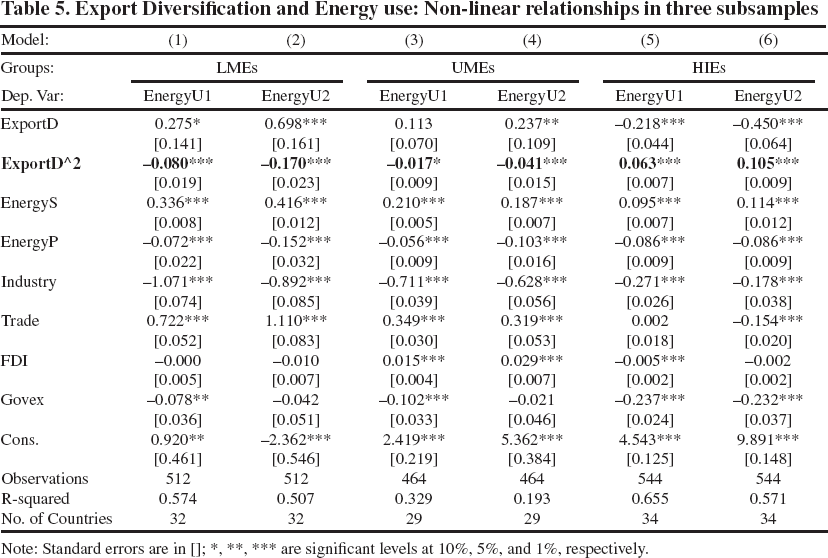

Next, the estimations for three subsamples are presented in Table 5. In the case of LMEs and UMEs, ED has significant positive impacts, while its squared term has significant negative impacts. This result re-affirms the inverted-U shape impacts of ED on energy use in both LMEs and UMEs. This result makes sense in the case of LMEs and UMEs since they mostly have a low level of technological production and are in the process of industrialization. Export diversification would transform their economic sectors from agricultural to industrial ones.

Export Diversification and Energy use: Non-linear relationships in three subsamples

Note: Standard errors are in []; *, **, *** are significant levels at 10%, 5%, and 1%, respectively.

Export Diversification, Export Quality and Energy use: Non-linear evidence

Meanwhile, they are constrained by financial issues by investing vast amounts of money in high-technology production. As a result, they would invest and expand economic activities to high-energy-intensive sectors. This process may be happening until a certain level of ED, where the economics of scale and the relative advancement in their production would turn the impacts of ED on energy use from positive to negative. The results imply that governments in LMEs and UMEs should support ED as much as possible to overcome the threshold, whereas the higher ED would help reduce energy use. Meanwhile, governments in LMEs and UMEs should also provide support to reduce the positive impacts of ED on energy use in the initial phase.

Export Diversification and Energy use in three subsamples: non-linear evidence

In the case of HIEs, there are opposite impacts. ED has a significant negative impact, while its squared term has a significant positive impact. That means ED has a U-shaped impact on energy use in HIEs. This result is very interesting to notice the difference in HIEs and may be explained by the fact that the production of HIEs has already been in high technological advancement. The increases in ED, especially in new markets, would push their firms to international competition.

Meanwhile, the producers in LMEs and UMEs are advanced by low costs of labour, which put back challenges for producers in HIEs in cost savings. In return, they may choose products or sectors with high energy-intensive use to compete since they need help to cut labour wages. As a result, the technological advancement in HIEs can only bring benefits to the environment through decreased energy use when they expand the exports to new products or markets. After a threshold, producers may follow the wisdom of the EKC by focusing on high energy-intensive sectors. As a result, ED would then induce higher energy use in HIEs.

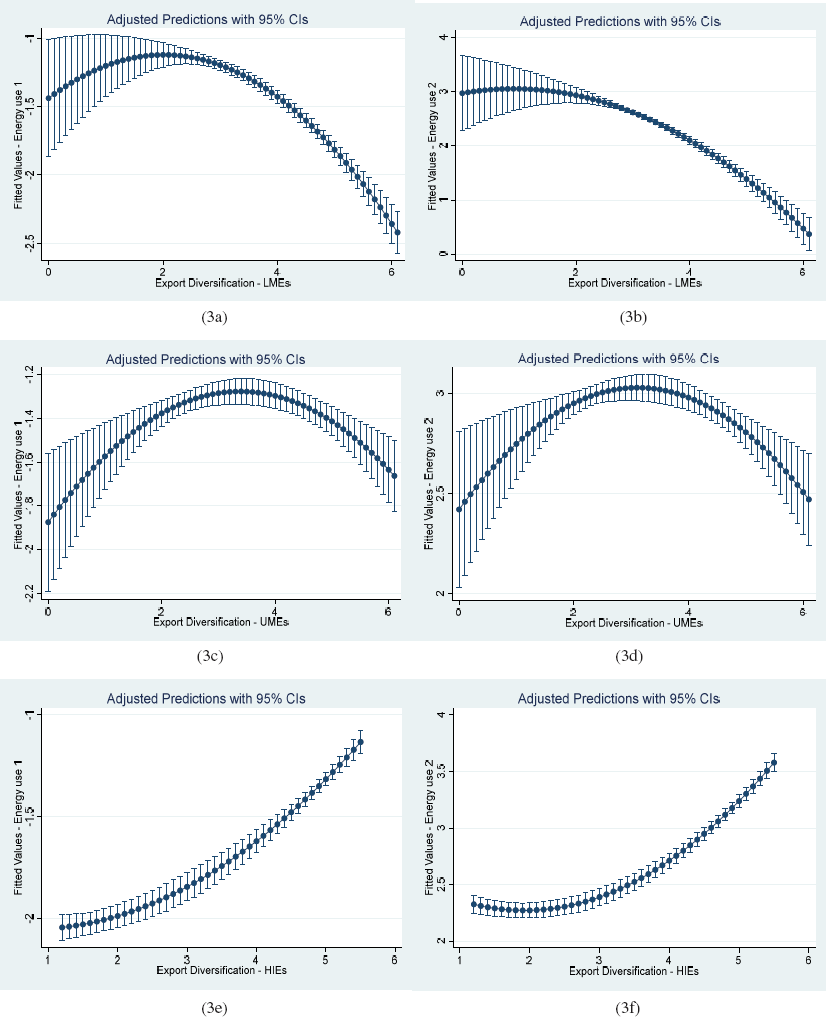

Figure 3 illustrates the predictive margins analysis for the impacts of ED on energy use in three subsamples (Figures 3a and 3b for the LMEs, Figures 3c and 3d for UMEs, and Figures 3e and 3f for HIEs). This result shows a clear inverted-U shape impact of ED on both kinds of energy use in LMEs and UMEs, while it is likely a U-shaped impact of ED on energy use in HIEs. However, the U-shaped impacts in HIEs are not strong ones. That confirms that ED can only bring some short-term benefits in reducing energy use in HIEs.

Expanding exports to new markets or products in the process of export diversification brings benefits and costs. On the one hand, ED helps to improve productivity and employment while it creates new economic activities and economic development. On the other hand, ED exposes domestic firms to international risk and high entry costs. That is, ED is likely a process with pros and cons, and it has a non-linear impact on domestic economic activities. In this context, the subject study adds to the existing evidence on the nexus between ED and energy consumption and in so doing, draws on global evidence while accounting for the non-linear impacts of ED on energy use. In light of a comprehensive empirical exercise and results, we conclude on the presence of non-linear linkages between export diversification (ED) and energy consumption. More specifically, we conclude that there is an inverted-U shape ED effect on energy use per output unit. This implies the increases in energy inefficiency in the progress of diversification improvement in exports until a threshold level from which ED would help to enhance energy efficiency. Our analysis of the three subsamples shows consistent findings regarding the effects of ED across income levels. The inverted-U shape effects of ED are consistent in LMEs and UMEs, while it is ambiguous in HIEs. It leads to the further conclusion that low and middle economies should diversify exports as much as possible to pass the threshold, where diversification can improve energy efficiency.

This paper contributes to the existing evidence on export diversification and energy consumption in two main aspects. First, the non-linear impacts of ED on energy consumption are examined and the case for the underlying nexus is established in the light of robust empirical evidence. Second, this relationship is investigated from a very broad global perspective and three subsamples (i.e., LMEs, UMEs, and HIEs) that provide deeper insight while accounting for the heterogeneities in the level of development across countries. The empirical results and the conclusion we have drawn are also robust from the PCSE model and various robustness estimators (i.e., FGLS, two-step system GMM) and estimation strategies (using one-year lags of independent variables and adding each control variable to check for sensitivity). We also conclude on significant Granger causality between ED and both kinds of energy use, including primary energy consumption and fossil energy use. Notably, the inverted-U shape impacts of ED on energy use are documented in global and two subsamples, including LMEs and UMEs. Meanwhile, a U-shape relationship is found in HIEs. Our findings have propounding implications for trade policy and energy policymakers.

Footnotes

Appendix

List of countries

Note: Income classification follows the World Bank's one. Data description of three subsamples Export Diversification and Energy use: non-linear relationship—Robustness check by different estimators Note: Standard errors are in []; *, **, *** are significant levels at 10%, 5%, and 1%, respectively

Bangladesh

Egypt

Kyrgyz Rep.

Nicaragua

Tajikistan

Bolivia

El Salvador

Moldova

Nigeria

Tanzania

Cambodia

Georgia

Mongolia

Pakistan

Tunisia

Cameroon

Ghana

Morocco

Senegal

Ukraine

Congo, Dem. Rep.

India

Mozambique

Sri Lanka

Uzbekistan

Congo, Rep.

Indonesia

Nepal

Sudan

Vietnam

Cote d, Ivoire

Kenya

Albania

China

Guatemala

Mexico

Russia

Azerbaijan

Colombia

Iran

Namibia

South Africa

Belarus

Costa Rica

Jamaica

Macedonia

Thailand

Botswana

Dominican Rep.

Jordan

Paraguay

Turkey

Brazil

Ecuador

Kazakhstan

Peru

Venezuela

Bulgaria

Gabon

Malaysia

Romania

Argentina

Estonia

Italy

Norway

Spain

Australia

Finland

Japan

Panama

Sweden

Austria

France

Korea

Poland

Switzerland

Chile

Germany

Latvia

Portugal

United Kingdom

Croatia

Hungary

Lithuania

Saudi Arabia

United States

Czech Republic

Ireland

Netherlands

Slovak Rep.

Uruguay

Denmark

Israel

New Zealand

Slovenia

Variable

Obs

Mean

SD.

Min

Max

Energy U1

544

-1.371

0.876

-3.156

0.979

EnergyU2

544

2.285

1.501

-1.418

5.571

ExportD

544

3.479

1.038

0.000

6.038

EnergyS

544

-1.918

1.710

-6.843

1.179

EnergyP

544

3.915

0.615

2.669

4.602

Industry

544

10.357

0.823

8.184

12.259

Trade

544

11.328

0.874

8.842

13.025

FDI

544

3.838

4.896

-4.844

43.912

Govex

544

9.552

0.902

6.392

11.268

29

Energy U1

493

-1.35

0.60

-2.61

0.47

EnergyU2

493

2.94

0.82

0.40

5.06

ExportD

493

3.23

1.19

0.00

6.06

EnergyS

493

-1.78

1.50

-6.27

0.58

EnergyP

493

3.92

0.62

2.67

4.60

Industry

493

12.05

0.59

10.25

13.52

Trade

493

12.84

0.60

10.82

14.33

FDI

493

4.26

5.32

-5.84

55.08

Govex

493

11.22

0.57

9.40

12.32

Energy U1

578

-1.94

0.46

-2.95

-0.87

EnergyU2

578

2.34

0.57

0.55

3.69

ExportD

578

2.21

0.75

1.29

5.47

EnergyS

578

-2.91

1.45

-9.12

0.39

EnergyP

578

3.92

0.62

2.67

4.60

Industry

578

13.38

0.72

11.49

15.11

Trade

578

14.42

0.78

12.04

16.11

FDI

578

4.75

6.98

-15.99

87.44

Govex

578

13.02

0.80

11.12

14.46

Model:

(1)

(2)

(3)

(4)

(5)

(6)

Estimator:

PCSE

FGLS

Two-step system GMM

PCSE

FGLS

Two-step system GMM

Dep. Var:

Energy U

Energy U

Energy U

EnergyU2

EnergyU2

EnergyU2

[0.050]

[0.066]

[0.029]

[0.099]

[0.115]

[0.020]

-0.092***

-0.092***

-0.090***

-0.162***

-0.162***

-0.091***

[0.007]

[0.009]

[0.004]

[0.014]

[0.016]

[0.003]

EnergyS

0.244***

0.244***

0.249***

0.303***

0.303***

0.284***

[0.007]

[0.010]

[0.013]

[0.009]

[0.017]

[0.013]

EnergyP

-0.097***

-0.097***

-0.096***

-0.125***

-0.125***

-0.150***

[0.011]

[0.023]

[0.007]

[0.014]

[0.040]

[0.005]

Industry

-0.588***

-0.588***

-0.497***

-0.416***

-0.416***

-0.455***

[0.038]

[0.042]

[0.025]

[0.053]

[0.072]

[0.027]

Trade

0.299***

0.299***

0.221***

0.333***

0.333***

0.329***

[0.028]

[0.034]

[0.026]

[0.043]

[0.059]

[0.021]

FDI

0.002

0.002

0.006***

0.006

0.006

0.006***

[0.003]

[0.003]

[0.001]

[0.005]

[0.004]

[0.001]

Govex

-0.076**

-0.076**

-0.078***

-0.104*

-0.104*

-0.050***

[0.034]

[0.035]

[0.011]

[0.054]

[0.060]

[0.010]

Cons.

0.549***

0.549***

0.248*

1.743***

1.743***

2.293***

[0.147]

[0.212]

[0.147]

[0.273]

[0.366]

[0.194]

Observations

1,615

1,615

1,330

1,615

1,615

1,425

R-squared

0.407

0.209

No. of Countries

95

95

95

95

95

95

No. of Ivs

73

78

AR(2) test-p-value

0.617

0.870

Hansen test-p-value

0.148

0.091

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.