Abstract

Taking advantage of low tax rates using transfer pricing and taking advantage of low production costs using offshoring are two strategies multinational firms (MNFs) use to increase profits. We identify an important trade‐off that MNFs face in setting their transfer prices: the conflict between (i) the incentive role and (ii) the tax role of the transfer price. For MNFs, we find the profit‐maximizing transfer‐pricing strategies that motivate divisional management to (i) make good sourcing decisions and (ii) take advantage of favorable tax rates. We quantify the absolute and relative maximum inefficiency in terms of the after‐tax MNF's profit change from using a single transfer‐pricing system as compared to the dual transfer‐pricing system. We show that the highest relative loss is attained when the average sourcing cost and the tax differential are high. We demonstrate that the highest absolute loss is attained when the average outsourcing cost is approximately equal to the offshoring cost. We extend our results to two practical variations in MNF structures: an MNF that faces operational constraints on its offshoring capacity and an MNF that uses compensation contracts linked to after‐tax firm‐wide profits. Our insights help MNFs' managers identify when to use single and dual transfer‐pricing systems.

Introduction

Tax‐efficient supply‐chain management is poised to be a new frontier of excellence for multinational firms (MNFs). Supply‐chain activities such as procurement decisions and distribution‐network design have traditionally been done independently of tax‐planning activities such as transfer pricing. Recently, however, there is ample evidence that MNFs have recognized that significant savings can be achieved if these two sets of activities are coordinated. For example, a global transfer‐pricing survey conducted by Ernst & Young found that 80% of US‐based MNFs involve tax directors at the “concept or initiation phase” of business planning and that only 5% of MNFs reported that they do not (Ernst and Young 2007). Deloitte expounds in its “strategic tax vision” that, at the beginning of any new business project, MNFs should involve tax departments to assess supply‐chain strategies that may lead to a reduced structural tax rate and, consequently, to improved after‐tax earnings (Deloitte 2008).

The importance of tax strategies and their integration into supply‐chain modeling has also attracted much attention in trade journals. Irving et al. (2005) claim that, “by aligning its tax and global supply‐chain strategies, a company can establish tax and legal structures that will create significant tax savings—often tens or hundreds of millions of dollars—while ensuring compliance with applicable laws and regulations.” They specifically see significant opportunities in the areas of procurement and logistics. Murphy and Goodman (1998) mention that “millions of dollars that could be adding to the value of multinational corporations instead are ending up in the hands of tax authorities and diminishing hard‐won savings achieved through supply‐chain improvements.” They argue that this can be achieved by a careful combination of supply‐chain and tax planning. Sutton (2008) stresses the importance of tax considerations in supply‐chain management and identifies procurement and sourcing as major areas that can be enhanced via tax planning and alignment.

Motivated by these observations, we focus on the sourcing decision of a decentralized MNF that operates in different tax jurisdictions and study how it can use transfer prices to reduce its tax burden. In effect, this is a multinational variation of the traditional “make‐or‐buy” decision: One sourcing option is to produce in‐house at an offshore facility, referred to as offshoring. Another option is to source from an external supplier, referred to as outsourcing. The external supplier may be located onshore or offshore; however, as the external supplier is not a part of the MNF, the location does not impact the MNF's tax liability. Both options have advantages and drawbacks: Producing in‐house at an offshore facility may be more expensive than outsourcing; however, it presents a possible tax benefit and can avoid some of outsourcing's uncertainties (e.g., quality, delivery) that might increase costs because the full production process is under the MNF's control. Sourcing from an external supplier, however, may be cheaper on average (due to specialization and economies of scale) but involves variability because the MNF has no control over the supplier's processes. When the cost advantage of the offshoring option is certain and the foreign country has a tax advantage, the solution is trivial: The MNF should offshore and transfer as much profit as is legally allowed to the foreign country. Hence, we focus on the case when the cost advantage is uncertain and the MNF faces a trade‐off between the possibly higher cost of outsourcing and the tax benefit of offshoring. As it is commonly observed in practice (for numerous examples, see Anand and Mendelson 1997), the sourcing decision in our model is made by the divisional manager, who possesses private knowledge about the supplier's cost owing to prior experience or local expertise. The MNF can affect the divisional manager's decision by selecting the performance measure by which she will be evaluated.

For MNFs operating in a decentralized manner, transfer prices affect divisional profits, which, in turn, impact the performance measures of divisional managers charged with making local operational decisions. Cools and Slagmulder (2005) perform an extensive case study of a semiconductor company that operates in several tax jurisdictions in Europe and in the United States. The goal of their study was to analyze how MNFs use transfer pricing in the context of managers' performance measurement and reward computation. They find that to efficiently use transfer pricing for taxation purposes using Organisation for Economic Co‐operation and Development (OECD 2010) Transfer Pricing Guidelines, companies should manage their divisions as profit centers. Kaplan (2006) defined profit center as “a unit, in which the manager has almost complete operational decision‐making responsibility and is evaluated by a straightforward profit measure.” Abdallah and Keller (1985) perform a study on performance evaluation of divisions of MNFs by surveying 64 firms and report that 82% use the same measures to evaluate divisional managers as they use to evaluate divisions. Duangploy and Gray (1991) surveyed 135 MNFs and found that divisional profit is used as a performance measure by 90.1% of the respondents. These studies provide ample motivation for using local profits to evaluate and encourage local managers' performance.

Of course, companies could use two different transfer prices. MNFs are allowed by law to keep dual accounting systems: one used for tax reporting and one used for managerial evaluation (Baldenius and Reichelstein 2006). Cools and Slagmulder (2005) found that the company in their study used a single transfer price. The company claims that using such a system allows them to argue that the transfer‐pricing methods are set based on business fundamentals rather than on tax considerations, which helps to convince the tax authorities that there is no tax avoidance. Baldenius et al. (2004) document that numerous MNFs use the same transfer price for tax and managerial purposes for several reasons: (i) This practice avoids the cost of maintaining “two sets of books” and the risk that internal records may “alert” tax authorities of suspicious practices in case of transfer‐pricing disputes and (ii) the differences between the transfer prices used in managerial books and those used in tax books can become evidence in legal proceedings, which complicates the tax disputes. The decision to use dual or single transfer prices is complex and, to the best of our knowledge, has not been addressed in a rigorous manner. We compare the effectiveness of these two strategies and provide insights on how firms should approach this decision.

Before we present the details of our model and its analysis, we summarize several important results: First, we show how incorporating tax considerations with a single transfer‐pricing system into a global sourcing model introduces inefficiencies because of the conflicting roles of transfer prices. We find the optimal sourcing and transfer‐pricing policies within this setting. Second, we quantify the absolute and relative maximum inefficiency from doing so in terms of the MNF's after‐tax profit and show when the inefficiency is the highest. Third, we extend our findings to several practical MNF structural variations: a case with operational restrictions on the offshoring amount and a case where the MNF uses contracts linked to the after‐tax profit measures to provide incentives to the local managers. These insights are helpful for MNFs trying to design tax‐efficient global sourcing strategies in various business settings.

The rest of this study is organized as follows. In section 2, we introduce the concept of transfer pricing and its potential role in determining the sourcing strategy. In section 3, we summarize relevant literature and position our work. In section 4, we describe the MNF model setting and parameter. In sections 5 and 6, we present the model analysis and discussion. Section 7 concludes the study with a summary of our observations.

Transfer Pricing and Its Role in Sourcing

A transfer price is an intrafirm price used for transactions between affiliated companies within the same enterprise. Transfer pricing is used to determine divisional profits and to shift income to lower tax jurisdictions. Over 90% of the companies Ernst and Young (2007) surveyed indicated that transfer pricing is an important international taxation issue, and 31% indicated that transfer pricing will be absolutely critical for them over the next few years.

As an example, consider a company incorporated in the United States that is taxed at 35% and sells 1 million units of a product per year at $100 per unit. The company has an opportunity to buy the product from its subsidiary in Ireland that produces at a cost of $30 per unit where the corporate income tax rate is 12.5%. If the company produces in Ireland and buys from the subsidiary at a cost of $70 per unit, its after‐tax profit would be 1,000,000(($100 − $70)(1 − 0.35) + ($70 − $30)(1 − 0.125)) = $54.5M. Notice that if the company did not transfer any profits to Ireland (i.e., purchased at cost), its after‐tax profit would only be 1,000,000($100 − $30)(1 − 0.35) = $45.5M. By using a transfer‐pricing strategy, the company is able to realize a higher after‐tax profit. Now, consider an opportunity for the company to source from a supplier in the United States at a cost of $20 per unit instead of producing them in Ireland at a cost of $30 per unit. Without considering taxes, the profit made in the United States is 1,000,000($100 − $20)0.65 = $52M, which makes the optimal choice for the company to source locally. However, when taxes are considered, we have shown that, by producing in Ireland and using a transfer price of $70, the company can realize an after‐tax profit of $54.5M. Thus, by incorporating the availability of a transfer‐pricing strategy into the sourcing decision, the company is able to increase its after‐tax profit by $2.5M. We will next explain some of the related legal rules and regulations.

Literature Review

In spite of the importance of combining tax and operational considerations in the design and management of supply chains, the operations management literature barely addresses taxation issues. Cohen and Lee (1989) develop a mixed‐integer nonlinear model for analyzing a global firm's resource deployment decisions by maximizing after‐tax profits. Vidal and Goetschalckx (2001) consider a global firm that moves some of its production to foreign facilities and optimizes after‐tax profit by selecting optimal flows between facilities and by setting transfer prices. Even though these studies use transfer prices and look at after‐tax profits, the aim of this stream of literature is to develop a procedure for optimizing large‐scale supply chains rather than to analyze the impact of taxation and transfer‐pricing policies on the sourcing decisions, which is the focus of our study.

Transfer pricing in these studies is considered to be an income‐shifting mechanism that determines taxable profit (referred to as the tax role of transfer pricing). However, in decentralized firms, transfer pricing is also crucial for determining profit‐based incentives for divisional managers (referred to as the incentive role of transfer pricing). The importance of addressing the conflict between the incentive role and tax role in understanding the impact of transfer prices has recently been raised in the accounting literature (Hiemann and Reichelstein 2012). None of the articles cited above incorporates the incentive role of transfer prices, which is an attribute of our model. Kouvelis and Gutierrez (1997) study a global newsvendor network aiming to optimize production quantities considering the impact of exchange rates and transfer prices. They explore the centralized and decentralized decision‐making structures and find that the centralized model performs better. We, however, focus on decentralized supply chains that face information asymmetry between the headquarters and the subdivisions about the outsourcing cost and use transfer price as a coordination mechanism as well as an income‐shifting mechanism.

Shunko and Gavirneni (2007) consider a supply chain in which the only sourcing option is production at a foreign facility. They analyze transfer‐pricing and selling price decisions in the presence of price‐dependent demands with an additive random component; they then show that transfer pricing has larger benefits when there is demand randomness. We allow sourcing to be a decision variable with options covering the whole range from no offshoring to full offshoring. We do this for deterministic demand with randomness in the cost of outsourcing. 2 Huh and Park (2013) analyze the effect of different transfer‐pricing methods on supply‐chain performance when sourcing from a foreign facility with random demand in the local market. Their model does not consider sourcing decisions and also does not optimize over the transfer prices, but rather takes the transfer‐pricing rules as given.

Liu and Nagurney (2011) study how firms make the pricing, production, and outsourcing decision in the presence of competition and exchange rate uncertainty. They further evaluate how the risk attitude of a firm affects these decisions. They find that the risk‐averse firm outsources less and the risk‐seeking firm outsources more when exchange rate variability increases. They do not incorporate transfer pricing in their analysis. Villegas and Ouenniche (2008) analyze an MNF in the presence of transport costs and duty drawbacks in addition to the standard criteria such as exchange rate risk, tariffs, ownership configurations, and tax rates. With the objective of maximizing the repatriated earnings, they formulate the optimization problem that can help companies decide trade quantities, prices, and transport cost allocations. They show that in low‐risk conditions, transfer‐pricing decisions are independent of trade quantities, whereas under high‐risk conditions, these decisions are intertwined. Their analysis does not, however, incorporate uncertainty.

After focusing extensively on demand uncertainty, the operations management community has recently started focusing on uncertainty in cost. Tang (2002) observed that “while most work focuses on demand uncertainty, not much work has been done in the area of uncertain supply cost.” Li and Kouvelis (1999), the seminal article on this topic, develops flexible and risk‐sharing contracts for a setting in which the demand is deterministic and the price is uncertain. Recently, Boyabatli et al. (2011) studied the price fluctuations in the beef industry, Goel et al. (2008) analyzed cost uncertainties in the gasoline industry, and Devalkar et al. (2011) studied cost uncertainties in the soybean industry.

Model Setup

We consider an MNF that consists of three entities: (i) the headquarters (HQ), (ii) a local division that sells a single product 3 in the local market and is governed by a local manager (LM) with profit–loss responsibility, and (iii) an offshore facility capable of manufacturing the product. We focus on how tax and transfer‐pricing considerations impact the LM's strategies and, hence, the MNF's profits.

Modeling Assumptions

T ∈ [c,p],

5

where c ≤ p ≤ 1.

The tax differential is nonnegative: δ ≥ 0.

Distribution F(·) has monotone nondecreasing hazard rate:

This assumption is satisfied, for example, by the normal, exponential, and uniform distributions, as well as Beta(A,B) with A ≥ 1 and B ≥ 1. We complement our analytical results with a numerical study that extends our findings to distributions that do not satisfy Assumption 3.

To guarantee that the LM's information is potentially valuable, we ensure that the greatest value of profit from offshoring (i.e., (1 − τ − δ) − c(1 − τ) + pδ) is less than or equal to the profit from outsourcing evaluated at the lowest realization of

Cost advantage is potentially valuable: c(1 − τ) − pδ ≥ 0.

To summarize our parameter restrictions, Δ is the set of all feasible parameter combinations.

The HQ's after‐tax profit is

Second, we use the price of anarchy (PoA)—the minimum possible ratio of the profit in Model S to the profit in Model D—to establish a relative bound on the inefficiency of the single transfer‐pricing system. The PoA is a standard measure of inefficiency used in economic analysis (see, e.g., Nisan et al. 2007).

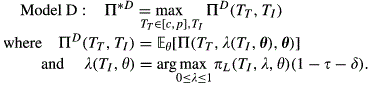

To set a benchmark, we develop Model D: A system with dual transfer pricing using two separate mechanisms for tax and incentive purposes.

6

For tax reporting, the HQ sets the transfer price

In the dual transfer‐pricing system, the transfer price for tax purposes,

In the dual transfer‐pricing system,

The optimal dual transfer prices are as follows:

Notice that the incentive transfer price

Next, we develop Model S, a system with a single transfer price used for tax and incentive purposes. As the LM will choose the cheapest supply source as determined by the comparison of θ and T, the HQ has to take the LM's sourcing incentives into account when setting the transfer price T. The HQ's expected profit—with

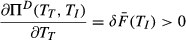

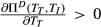

Equation 5 illustrates that the transfer price, T, has two impacts on the HQ profit: It affects the LM's sourcing decision through its incentive role, and it impacts the expected tax benefit through its tax role. This can be easily seen from a comparison of the first derivatives in Models S and D.

In the next proposition, we characterize the optimal transfer price in Model S.

The optimal transfer price for the HQ is

Note that, unlike the dual transfer‐pricing system, the optimal single transfer price,

Next, we compare the transfer‐pricing policies in Models S and D and state the properties of

For all

In Lemma 1, we first show that the transfer price in the single transfer‐pricing system is between the two transfer prices in the dual system. This result is expected because

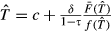

It is interesting to see how the transfer price and the profit will change if the external supplier increases its average cost. To address this question, we consider the change in transfer price when the outsourcing cost,

In the second part of Lemma 1, we show that the MNF facing outsourcing cost

As a result, when the firm faces a more expensive (on average) source of supply, it might be beneficial for the firm because of higher tax savings. That is, an increased outsourcing cost impacts the profit in two directions: a decrease because the firm is supplying at a higher average cost and an increase because of the greater tax benefit.

We illustrate this logic using a numerical example in Figure 1. The outsourcing cost follows the beta distribution (Beta(A,B)) with A = 1 and B varying based on the average outsourcing cost:

HQ Profit Increases in the Average Outsourcing Cost μ when μ Is High; Parameters: c = 0.24, τ = 0, p = 0.6, and δ = .35.

Having solved Models S and D, we next examine the inefficiencies caused by a single transfer‐pricing system.

In this subsection, we focus on the increase in the expected after‐tax profit using the dual transfer‐pricing system instead of a single transfer‐pricing system, the opportunity cost of using the single transfer‐pricing system. In the previous section, we focused on characterizing the optimal sourcing and transfer‐pricing policies and treated (c,p,τ,δ) as parameters. Hence, we suppressed them in the definitions of

CoC is attained when p = 1, τ = 0,

It is intuitive that the CoC is attained when the legal upper bound on the transfer price p and the tax differential δ are the highest: In this case, the potential tax benefit (

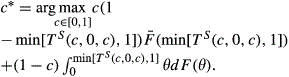

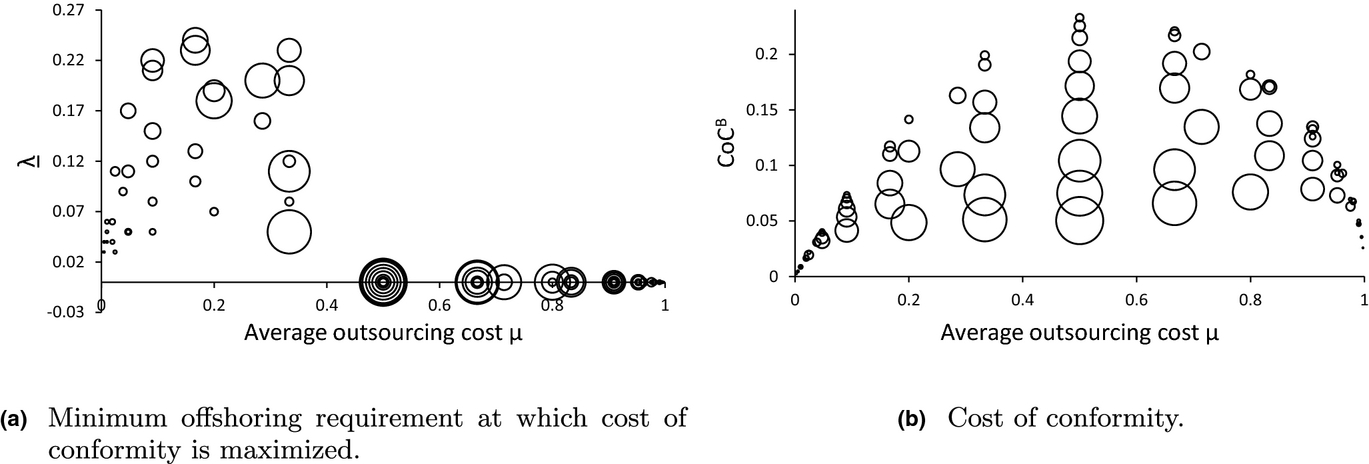

We perform the numerical analysis by finding CoC for 81 test problems where each problem represents a different beta distribution of the outsourcing cost:

First, notice that CoC is the highest when the average outsourcing cost, μ, is close to

This intuition is complemented by the plot in Figure 2(b), in which we observe that (i) CoC is the highest for distributions that have zero or small skewness, γ = 0, and (ii) CoC decreases faster as γ increases in the positive domain than when γ is in the negative domain. When

Finally, in Figure 2(c), we look at the offshoring cost,

CoC Results for the Test Problems with Respect to the Mean μ (x‐axis) and Variance V (bubble area) of the Outsourcing Cost; θ ∼ Beta[A,B] and {A,B} ∈ {1/20,1/10,1/5,1/2,1,2,5,10,20}.

Part of the intuition above relied on the fact that the profit in both models will be high (low) if μ and c are both low (high) and, hence, the CoC is low in both cases. This intuition applies only to the absolute difference in profits captured by CoC. Next, we examine PoA, the relative measure of inefficiency, to see how the results differ.

We define PoA as the smallest ratio of the expected after‐tax profit in the single transfer‐pricing system (Model S) and the dual transfer‐pricing system (Model D). Hence, PoA = 1 implies that there is no inefficiency from using a single transfer‐pricing system:

It is intuitive that the lowest PoA is attained when τ = 0 and δ = 1, when the tax advantage is the highest. It is also intuitive that the loss is highest when the selling price (p) is the highest: As p acts as a bound on the transfer price, the firm can extract the largest tax benefit when p is high.

It is more subtle to interpret why the PoA is minimized when c is the highest. Recall from Assumption 1 that the transfer price is bounded by c from below; hence, as c increases, the transfer price in the single transfer‐pricing system has to be set higher as well, and the HQ cannot motivate the LM to offshore. Nevertheless, there exist realizations of the outsourcing cost that make offshoring optimal for the HQ, as ensured by Assumption 4, which guarantees that the LM's information is valuable. Hence, when c is high, PoA is low. In other words, the lowest PoA is attained when the difference between the incentive transfer price in Model D and the transfer price in Model S is the highest. Notice that the same logic does not apply to the CoC because as c increases, the profit in both systems goes to zero and the absolute difference goes to zero as well. For PoA, however, the logic described above makes the profit in Model S go to zero faster than the profit in Model D.

We apply similar logic to understand why PoA is equal to 1 − μ in the limit: When the average outsourcing cost is very low, the efficiency loss is minimal because it is almost always optimal to outsource. Such a solution is attainable with a small transfer price, and the transfer price has a very limited tax role because the HQ rarely offshores. In contrast, when the average outsourcing cost is high, the efficiency loss is large because offshoring is almost always optimal. However, such a solution is hard to attain because of the transfer‐pricing restrictions. Finally, the transfer price has a very significant tax role because the HQ frequently offshores.

The results in Proposition 4 hold for all outsourcing cost distributions satisfying Assumption 3. We relaxed this assumption using a numerical study, in which we find PoA and the set of parameters (c,p,τ,δ) at which the PoA is attained. 10 The results of Proposition 4 held for all the test problems.

In this section, we discuss how our results extend to two practical variations of the basic model setup. In the first variation, the MNF faces operational constraints on the offshoring capacity, for example, local content rules that put restrictions on what portion of production can be offshored. In the second variation, the MNF provides an incentive contract to the LM that includes both divisional and firm‐wide profit measures. 11

Impact of Operational Constraints

In this subsection, we address a system in which the MNF faces restrictions on the offshoring quantity. That is,

The lower bound on the offshoring quantity,

In the presence of operational constraints, the CoC is defined as the maximum absolute difference between the dual transfer‐pricing system and single transfer‐pricing system that can be attained over all system parameters including the bounds on the offshoring proportion,

Cost of Conformity Results for Test Problems with Respect to the Average Outsourcing Cost μ (x‐axis) and Variance V (Bubble Area) of the Outsourcing Cost; θ∼Beta[A,B] and {A,B} ∈ {1/20,1/10,1/5,1/2,1,2,5,10,20}

Similar to Model S above, the PoA in the scenario with operational constraints refers to the largest relative difference in profits due to using the single transfer‐pricing system instead of the double transfer‐pricing system over the set of parameters that includes the bounds. On the basis of the numerical experiments using our set of test problems, we observe that the PoA in this scenario equals the PoA in Model S and is achieved when

Multidivisional firms use different models to evaluate divisional managers' performance. Keating (1997) performed a survey of 175 firms with three or more divisions asking the participants to rate on the scale from 1 (low) to 5 (high) the importance of divisional (

We show that when β is smaller than

Notice that the existence of β in the LM's objective function lets the HQ “mimic” the system with dual transfer prices without actually having two mechanisms. The system is favorable from the HQ's standpoint because the HQ avoids disputes with the tax authority about the discrepancy between the tax and incentive transfer prices. However, it partially achieves the benefit of separating the incentive and tax roles of transfer price. The extent to which this model can approximate Model D depends on β, the choice of which is unique to every organization.

Including a fraction of the firm‐wide profit (β) in the LM's objective function decreases the incentive role of the transfer price without affecting anything else. Hence, the efficiency loss in the scenario with an incentive contract will always be smaller than in Model S in both relative and absolute terms: The PoA will decrease, and the CoC will increase, in β.

Conclusion

Our study analyzes a multinational variation of the traditional “make‐or‐buy” decision, in which the “make” decision is hindered by the fact that the manufacturing facility is located offshore, forcing the MNF to make a transfer‐pricing decision in addition to a sourcing decision. We identify an important trade‐off the MNF faces in setting transfer prices: namely, the conflict between (i) the incentive and (ii) tax roles played by the transfer price. We characterize the optimal transfer‐pricing strategies that accomplish the dual goals of (i) motivating divisional management to make favorable sourcing decisions and (ii) taking advantage of favorable tax rates at offshore locations. Our analysis leads to three insights for managing MNFs.

Footnotes

Appendix

1

Methods include (i) the comparable uncontrolled‐price method, (ii) the resale‐price method, (iii) the cost‐plus method, (iv) the comparable‐profit method, (v) the profit‐split method, and (vi) unspecified methods.

2

3

Without loss of generality, price is normalized to 1.

4

5

6

7

8

9

We observe the same phenomenon in numerical examples that use the truncated normal and triangular distributions.

10

For brevity, we do not report the detailed results.

11

For brevity, we present only a qualitative discussion of the main results for these variations. Mathematical formulations and analysis of these models are available from the authors.

13

Given complete freedom, it is always possible to choose a contract that mimics the dual transfer‐pricing system. However, we focus on realistic contracts that are more common in practice and evaluate their effectiveness.