Abstract

Endowed with significant firm‐specific knowledge, inside directors can contribute to the decision‐making processes of the boardroom. However, regulatory changes, focusing primarily on the monitoring function of the boards, have driven inside directors out of the boardroom. This article argues that suppliers with firm‐ and industry‐specific knowledge are uniquely positioned to fill a critical void in boardrooms. It also suggests that the value of having a supplier on the board (SOTB) is influenced by environmental contingencies faced by a firm: operational efficiency, diversification, and demand uncertainty. Using an objective measure of supplier presence in the boardroom, the authors find that a supplier's presence enhances firm performance. They also find that the value of an SOTB in enhancing performance is greater in firms with lower operational efficiency and higher demand uncertainty and, is lower in firms with higher diversification. These results are robust to potential endogeneity issues, alternative estimation methods, and measures of moderator and outcome variables.

INTRODUCTION

Supply chain management (SCM) is increasingly seen as a source of strategic advantage to firms. Scholars in operations management have studied the importance of supply chain and operations representation within a firm's top management team (TMT) (Hendricks et al., 2015). For example, past research has examined the antecedents and consequences of including a chief operating officer (COO) (Hambrick & Cannella, 2004) or a chief supply chain officer (CSCO) (Roh, et al., 2016) in the TMT.

However, TMTs are not the only agents responsible for leading the firms. In the hierarchical ladder, the board of directors lies above the TMT and makes significant strategic decisions that impact firm performance (Castellanos & George, 2020). Traditionally, boards were responsible for monitoring the actions and performances of TMTs and safeguarding the interests of the firm's shareholders (Fama & Jensen, 1983). Since independent directors are better positioned to monitor and evaluate the TMT, there has been an increasing push toward nominating independent directors from shareholders and regulators. Besides, the Sarbanes–Oxley Act of 2002 mandates independent directors to constitute a majority of a company's board. Today, barring the CEO, who is an inside director, independent directors primarily populate the board (Joseph et al., 2014). For example, in 2019, 85% of the directors on the boards of S&P 500 companies were independent directors, and the CEO was the sole nonindependent director in 62% of the boards (Stuart, 2019).

Besides monitoring, boards have increasingly been advising TMTs on strategic matters (Lungeanu & Zajac, 2019) in recent years. For example, firms that have more female directors on the board were found to initiate not only more but also faster product recalls of defective products (Wowak et al., 2021). Further, a recent study suggests that directors consider their strategy‐setting role to more salient than their monitoring role (Boivie et al., 2021). However, Kastiel and Nili (2017) note that independent directors, who are often part of multiple boards, may lack the time and resources needed to acquire relevant firm and industry knowledge when compared to inside directors. When board members have lower firm‐specific knowledge and expertise, the board's effectiveness in providing counsel and advice is negatively affected, deteriorating the firm's value (Feldman & Montgomery, 2015).

Further, independent directors are drawn primarily from finance, accounting, legal, and administration (i.e., compliance‐oriented functional areas). There is a lower proportion of directors from marketing (Whitler et al., 2018) and supply chain areas (McKone‐Sweet et al., 2005). These two functions determine a firm's ability to adopt an outside‐in orientation critical for planning and executing market‐driven strategies (Whitler &Puto, 2020).

Against this backdrop, we propose and evaluate a novel and intriguing board choice that can enhance its effectiveness in making strategic decisions relating to the supply chain function—including an executive from a firm's supplier to the board (SOTB). Many large companies such as Intel, Chevron, and Cisco have suppliers on their respective boards. For example, in nominating an executive from Cabot Corporation, one of its supplier–firms, to its board, the CEO of Owens Corning stated, “His insights and expertise will help advance our operating priorities for the benefit of our shareholders,” and that he will “complement the skills and expertise of our other board members.” Similarly, while nominating a supplier CEO to the board, Cisco mentioned that the CEO's “business leadership, combined with technology and semiconductor expertise, will be a tremendous asset to Cisco's board” (Cisco PRNewswire, 2020). As our study observes, this action is increasingly being adopted by firms; 21.9% of companies in our sample have a supplier on their boards.

We use resource dependence theory (RDT) to argue that an SOTB's human capital (i.e., industry‐specific experience and knowledge) and social capital (i.e., ties to the firm's strategic supply partners) can improve a firm's ability to deal with its contingencies (Hillman & Dalziel, 2003; Pfeffer & Salancik, 2003). The SOTB's human capital is derived from their knowledge, skills, and capabilities, which can help reduce the board's information gap on industry conditions and trends, as well as identify and strengthen the firm's operations/supply chain resources and capabilities. The SOTB's social capital is based on their relationships with individuals and organizations, which open access to valuable resources in the upstream part of the firm's value chain. The SOTB can identify business opportunities, share market knowledge, and facilitate access to key resources through such relationships. Increased knowledge and external connections enable a board to perform its advisory role more effectively.

However, we recognize that an SOTB's value is not expected to be similar for all firms. We argue that an SOTB's human and social capital will have different values to firms based on their level of environmental contingencies. Such contingencies increase firms’ lack of control over the resources they need, thus increasing the level of their dependency on suppliers. Following Dess and Beard's (1984) classical work, recent scholarly works in operations management have theorized complexity and dynamism as two dimensions of uncertainty (e.g., Kovach et al., 2015; Modi & Cantor, 2021). To capture these contingencies, this study conceptualizes complexity and dynamism using diversification and demand uncertainty, respectively, and augments these two factors with a corresponding operational dimension using operational efficiency. 1

Typically, organizations adopt product diversification and market development strategies to facilitate growth. The greater the number and diversity of product markets firms operate in, the higher the complexity of their operations and dependence on suppliers. Dess and Beard (1984) note that diversification increases the “complexity and diversity both in the operations of the firm and its requirements for administrative control” (p. 57). Also, firms are increasingly facing dynamic environments in the markets they operate in, where the customers’ needs change repeatedly and unpredictably. The demand uncertainty that arises from market dynamism affects the entire supply chain that not only needs better visibility into changes in customer preferences but also greater willingness to collaborate with each other to respond to those changes. Beyond dynamic markets, firms also face uncertainty and disruptions due to globalization, supply sources dispersion, and increased occurrences of uncontrollable forces (such as COVID, natural disasters, and geopolitical issues). Such factors create a supply and cost imbalance, which negatively impact firms’ operational efficiency. Overall, these dependency‐increasing factors will need to be countered by dependency‐reducing relationships with firms’ suppliers. We argue in this study that an SOTB's human and social capital can help manage these dependencies and that the value of an SOTB may differ depending on the level of such contingencies.

This study tests the SOTB's performance impact and the role of the three boundary conditions (operational efficiency, diversification, and demand uncertainty), using 2557 firm‐year observations from a sample of more than 300 business‐to‐business (B2B) firms (we explain the rationale for B2B in our sample selection section). Specifically, we study the effect of an SOTB on return on assets (ROA). We choose ROA primarily because it is a universal and holistic measure of firm performance. Unlike other financial performance measures like return on equity, which can be manipulated through debt leverage, ROA is less vulnerable to manipulation as it involves multiple asset types (property, equipment, and people). These assets are difficult to tamper with (Deloitte, 2013). The ROA is also an extensively used metric in the operations management literature to capture firm performance (Modi & Mishra, 2011). We also use net profit margin, another performance metric, as an additional outcome variable to examine the robustness of the study's findings. The study's results show that (a) the presence of an SOTB enhances firm performance and (b) an SOTB's impact is greater in firms with lower operational efficiency and firms facing higher demand uncertainty but lower in firms with greater diversification.

Through this study, we make four important contributions. First, we identify an SOTB as a structural mechanism that firms can use to augment their boards to gain firm‐ and industry‐specific knowledge the board needs for making strategic supply chain decisions. It is an important contribution as firms need to balance the independence of board members who know less about the firm against well‐informed inside directors who struggle with independent oversight. 2 Second, we contribute to the research on buyer–supplier relationships. The inclusion of an SOTB expands the theoretical domain of supplier involvement in firm decisions. Specifically, we extend past research (e.g., Bowen et al., 2001; Jin et al., 2019), which has primarily focused on the relationship paradigm to study suppliers’ participation in lower level firm decisions (e.g., product development), to a higher, strategic level, where the supplier actively partakes in making strategic decisions for the firm. Third, we contribute to the nascent link connecting board characteristics to operations management. An important recent contribution in the operational area focused on board's gender composition and the role female directors play in firms’ operational decisions such as product recalls (Wowak et al., 2021). Their main premise is that increased female participation is likely to alter the tone and expectations of boards when they drive firms’ recall decisions. We extend the foundation laid by Wowak et al. (2021) and examine how boards can get more involved with operational and supply chain decisions by nominating an SOTB. Finally, while studies examine the overall board composition and its effect on firm performance (Dalton et al., 1999), few studies have addressed this question for individual board members (Nam et al., 2018). Understanding specific board members and their contributions concerning firm actions and behaviors is still an understudied phenomenon. We address this gap in a supply‐chain context.

THEORETICAL FOUNDATION AND HYPOTHESES

In this section, we summarize RDT within the realm of the boards of directors and then present our hypotheses.

Boards and RDT

A board is entrusted with two critical functions: monitoring the decisions of a firm's top managers and providing access to valuable resources (Hillman et al., 2009). While agency theory has been used to explain the monitoring function, the resource provision explanations are rooted in RDT. RDT suggests that firms depend on other entities in the external environment for key resources and that their boards can increase access to these resources (Hillman et al., 2009). RDT's central premise is that “Board capital … provides an important basis through which firms can access vital resources internally and in their external environment” (Fernandez et al., 2019, p. 134).

Board capital consists of two key dimensions: human and social. Human capital comprises board members' knowledge, skills, and experiences from their education and varied industrial and environmental exposure. In general, we expect every board member to bring valuable information about their industries. However, if a board member is a part of a connected industry (such as a supplier firm), they are likely to have a better understanding of the firm's unique operational challenges and opportunities. Also, they can contribute to the board gaining a better understanding of industry trends and uncertainties. Driving relevant strategic insights from the knowledge can help the board members offer valuable strategic advice to the firm's managers. For example, Archer Daniels Midland, while appointing an executive from Illinois Tool Works, one of its suppliers, to the board, said: …Her tremendous knowledge, experience, and leadership at a global manufacturing company will make her a strong addition to our board… She offers significant expertise in technology innovation, financial discipline, strategy development, and manufacturing excellence ‐ all key elements as we continue to advance our strategy and growth efforts around the globe…

Further, the board's expertise can lower its dependence on inside directors and TMT for information and provide unbiased advice on the firm's critical strategic decisions.

Board members’ relationships and connections with external stakeholders (such as suppliers and technology partners) and internal stakeholders (such as other board members and the firm's TMT) determine the board's social capital. Through their external network, board members can access information and critical resources valuable to the firm. Carpenter and Westphal (2001) suggest that boards with strong ties with firms, which are part of the value chain, enjoy better access to resources and information, translating into better performance outcomes. In particular, an SOTB will have access to information and resources of second‐ and third‐tier suppliers. Further, internal social ties with other board members and the TMT enable SOTBs to share relevant knowledge and expertise, enhancing the board's knowledge and skillset relating to the firm's supply chain issues, which in turn, can lead to a better quality of strategic inputs provided to the TMT.

SOTB and firm performance

Company boards regularly encounter performance‐critical strategic issues they might not have the knowledge or expertise to deal with (Cheng et al., 2021). ISS Analytics (2019) identifies the supply chain skillset as one of the top five requirements for appointing new board members. This requirement is fueled by the rapid changes and advancements in firms' supply chains caused by the increased pace of technological adoptions and globalization in the last 20 years. Today, more companies rely on suppliers, outsourcing partners, and third‐party logistics providers to reduce costs and increase operational efficiency. Simultaneously, companies face increasing product and service expectations from a more knowledgeable global customer base. The implication is that a board needs more knowledge of and expertise in a range of supply chain issues, such as forecasting, demand planning, dealing with scarcity and supply disruptions, logistics streamlining, preparing for quick and agile services, and supply visibility. However, in a research study of service companies, McKone‐Sweet et al. (2005) noted that 80% of boards in their sample lacked a representative with required SCM knowledge. The study also noted that “specific issues of supply chain management had never been raised at a board meeting and cost control responsibility was left to the individual departments” (p. 7).

Beyond knowledge, organizations also need resources from their environments. In a supply chain context, critical resources go beyond raw materials and components to include cost reduction initiatives, innovations, and access to new technologies (Ambulkar et al., 2022). The uncertainty in accessing critical supply chain resources and lack of insight into factors influencing such access are critical challenges for organizations. In turn, this elevates the board's role in playing an instrumental part in dealing with such uncertainties.

We draw on RDT to explain the role of SOTB in reducing environmental dependence and thereby increasing firm performance (Hillman & Dalziel, 2003). From a human capital perspective, an SOTB can contribute to the firm in many ways. First, an SOTB can bridge the supply chain–related knowledge gap among a firm's board of directors. Directors from the firm's supply industry are likely to have tacit knowledge about their industry's opportunities and constraints, providing a nuanced understanding of the industry (Tian et al., 2011). Moreover, SOTBs are likely to be the only (or among a few) directors on the board to possess knowledge and experience relating to the firm's broader supply network that includes Tier 2 and Tier 3 suppliers. Based on their experience within this broader supply network, the SOTB are in a unique position to anticipate upstream trends and risks and advise the rest of the board and the TMT on issues concerning supply‐side opportunities and disruptions. Second, an SOTB is likely to bring supply chain–related issues to the board's attention. Boards typically have a multitude of issues to deal with, and the presence of an SOTB ensures the board's attention on the supply chain issues. Third, an SOTB can advise on structuring the external supply chain and internal operations to meet the company's growth goals. Finally over, as companies continue to grow and/or face unforeseen environmental challenges, like COVID‐19, their supply chain configurations may also need a change. An SOTB can advise on ways to reconfigure and diversify the supply chain. In sum, boards with an SOTB are better equipped with supply chain knowledge and skills than boards without an SOTB.

From a social capital perspective, an SOTB can contribute to the firm in two distinct ways. First, drawing on RDT theory, we suggest that an SOTB can help a firm gain commitment and support from members of the firm's supply network (Hillman & Dalziel, 2003), thereby reducing dependency‐related issues. These commitments are useful for reducing material cost, lead time, and carbon footprint, increasing transparency in the supply chain, and receiving supplier support during disruptions. Second, an SOTB creates symbolic value by communicating to the suppliers that the firm is serious about its relationship with its suppliers. It also instills confidence in the customers that the firm is more likely to bounce back, especially during supply chain disruptions, as it has the suppliers’ support. In sum, the SOTB's connections and symbolic value facilitate reducing the negative effects of resource dependence and increasing the propensity of supplier–firm collaborations.

Overall, SOTB's human and social capital enhance the board's knowledge and orientation toward the supply chain and facilitates necessary connections to reduce supply chain dependencies. Thus: The presence of a supplier on the board (SOTB) is associated with higher firm performance.

Need for SOTB's knowledge and resources

An SOTB inclusion may not yield the same level of value to all firms. An SOTB's human and social capital will be more valuable to firms that face greater environmental uncertainties since they are likely to depend more on their suppliers to manage those uncertainties (Krause et al., 2013). A major source of uncertainty arises from the scarcity of materials, dispersed value chains, import restrictions, transportation disruptions, and so on. Such uncertainties induce variability in supply timing, supply quantity and quality, and purchase costs, the most important factors that determine a firm's operational efficiency (Modi & Mishra, 2011). Another type of uncertainty arises from organizational need to grow, a need driven by investors and TMTs. Firms that choose the path of diversification typically develop products that are different from their current mix of products. An increase in the number of products can result in a larger variety of materials and components and an increased number of suppliers and logistics providers the firm must deal with. Thus, a consequence of diversification is an increase in the complexity of operations. External uncertainties can also be related to the dynamism of the markets the firms operate in (Dess & Beard, 1984). Constant changes in consumer tastes and competitive actions result in variability in terms of both product design and volume needs (Wathne & Heide, 2004). Firms that face demand uncertainties will require upstream suppliers to show greater flexibility and adaptation in meeting their downstream needs, actions that will be greatly facilitated by an SOTB's social and human capital. Overall, an SOTB's value to the firm will be determined by the level of operational efficiency, diversification, and demand uncertainty faced by the firm.

Operational efficiency

Firms increasingly face uncertainties from environmental forces such as globalization and dispersion of supply sources, increased occurrence of natural disasters that cause supply disruptions, political events that lead to friction in materials movement, and a host of other uncontrollable factors. These factors cause supply imbalances that negatively impact firms’ operational efficiencies (Modi & Cantor, 2021; Modi & Mishra, 2011). We argue that an SOTB can make a greater difference in firms with lower efficiency levels for the following reasons. First, though all firms benefit from an SOTB's human capital (the knowledge and supply chain orientation), it will be more valuable for firms with lower operational efficiency. This is because firms with lower operational efficiency need (a) more supply chain–related attention from the board and the SOTB can channel the board's attention and (b) more supply chain knowledge relating to opportunities and constraints, and the SOTB can lend their expertise on these to the rest of the board.

From a social capital perspective, an SOTB's external connections are likely to be more valuable to firms operating at a lower efficiency level. Such firms may be performing so because they do not have in place an effective supply chain strategy that (a) addresses the different uncertainties in the upstream markets, (b) evaluates their impact on operations, and c) responds in efficiency‐inducing ways. To be efficient, firms have to rationalize internal processes and invest in building relationships with key suppliers to induce trust and cooperation (Brinkhoff et al., 2015). From a process perspective, to build such partnerships, firms’ directors must (a) establish communication and trust channels with top management personnel in key supplier organizations, (b) sell firms’ vision on planned efficiency‐improvement practices to them, and (c) obtain their buy‐in to engage with firms’ vision and practices. A key requirement in the above process is that suppliers must understand firms’ goals and constraints to identify ways to help the firms become more efficient. We argue that firms with a lower operational efficiency have a greater need for SOTB support to forge such relationships.

Finally, compared to highly efficient firms in which the legitimacy and importance of the operations function are not in doubt within their boards, the operations function in less efficient firms faces the challenge of demonstrating their importance and value. This poses a problem as low performance leads to lower legitimacy of the supply chain function within a firm. An SOTB helps establish the legitimacy and importance of the supply chain function within the board. In turn, legitimacy increases the ability of the supply chain function to build stronger relationships both internally and externally.

Overall, we propose that the knowledge and connections that an SOTB can bring from the supplier industry would be more valuable for a less efficient firm. Thus: The impact of an SOTB on firm performance is likely to be higher (lower) for firms with lower (higher) operational efficiency.

Diversification

New opportunities fueled by globalization, customer heterogeneity, and increasing pressure from stakeholders for higher growth encourage firms to diversify into different product categories and expand their footprint to multiple product markets. Diversification enables a firm to enter new markets different from existing markets (Jacobs & Swink, 2011), thereby reducing business risk. However, diversification can also lead to substantially higher operational complexity as firms operate in differentiated or unrelated product markets, develop products targeted toward niche segments, configure a larger and diversified supply base (Craighead et al., 2007), and incur potentially higher set‐up and inventory costs. Craighead et al. (2007) note that as complexity increases, the firm's vulnerability to material flow frictions increases, and more disruptions occur in the firm's supply chain. To minimize such frictions and disruptions, firms must coordinate among internal organizational units and collaborate and integrate with external suppliers.

What role does the SOTB play in diversified organizations? We believe that the SOTB's human and social capital roles are limited because they are more likely to be familiar with the industry they belong to and less likely to have the resources or connections required for addressing firms’ challenges in other diversified industries where they operate. In other words, an SOTB is useful for a firm operating in multiple business areas only when it attempts to develop and execute strategies in the supplier's business area. For example, Tian et al. (2011) state that the “benefits of directors’ industry‐specific experience might particularly be salient for non‐diversified firms” (p. 734). Conversely, for a firm with low diversification, the SOTB's knowledge and connections should apply to most, if not all, of the firm's businesses, thereby allowing it to take advantage of the SOTB's resources. In summary, firms that intend to exploit existing product markets and industries can rely more on the SOTB's resource provisioning capability and connections, thereby driving greater performance effects. Thus: The impact of an SOTB on firm performance is likely to be lower (higher) for firms with higher (lower) diversification.

Demand uncertainty

Dynamic environments where customer preferences and expectations change rapidly create demand uncertainty for firms. When customer preferences remain stable, demand can be more easily predicted. When preferences change, companies must constantly modify their products and services (Wathne & Heide, 2004). Poor information on such changes may lead to companies experiencing greater uncertainty regarding customers’ behaviors for products they buy, companies they buy from, and the timing of their purchases. In turn, uncertainties make sales forecasts less reliable and contribute to suboptimal operational decisions. This leads to increased cost, excess inventory, increased production capacity, and obsolescence.

Further, such uncertainties occurring downstream at the customer level increase the operational complexity for upstream players and impose challenges in balancing supply with demand. To manage this contingency, firms must develop policies to monitor demand closely, share demand information across the supply chain, and work with supply partners to enable tight coordination. They must also change inventory levels, deal with small lot sizes, and use just‐in‐time delivery of the required supplies (Angkiriwang et al., 2014). In this situation, a set of responsive and collaborative suppliers can benefit the firms.

We propose that SOTB's human and social capital benefit firms with higher demand uncertainty. The SOTB's human capital will help the firm better design the right responses for such environments. Specifically, SOTB's expertise and knowledge can help firms understand how to expand and reconfigure their supply chain to cope with uncertain market demands. Furthermore, the SOTB's social capital can shape suppliers’ integration into the firms’ operations. For example, the suppliers can receive the latest demand information, increasing their ability to respond better to demand changes. Following this, we argue that firms facing high demand uncertainty need to involve their suppliers to offer quicker responses to changing customer preferences. Thus, the presence of an SOTB, who can elicit greater involvement from suppliers, is highly valuable to such firms. In other words, SOTB's impact is more pronounced under higher demand uncertainty. In contrast, firms with stable demand can better forecast their supply chain needs, rely on their existing suppliers, and not reconfigure their supply chains frequently. Therefore, SOTB's human and social capital may be less valuable for firms with stable demand. Thus: The impact of an SOTB on firm performance is likely to be higher (lower) for firms with higher (lower) demand uncertainty.

EMPIRICAL DETAILS

Sample

Our study sample comprises firms in the Standard and Poor's (S&P) 900 index (S&P 500 index and S&P Midcap index). The 900 firms in this index account for nearly 90% of the market cap of the publicly listed firms in the United States. As the S&P list can change over time, the 900 firms in our sampling frame are based on the S&P list as of 2007. The data for these firms are collected through 2015.

The S&P 900 includes both B2B and business‐to‐consumer B2C firms. For this study, we exclusively focus on B2B firms as (a) customers can also bring valuable firm‐specific information to the board because they are familiar with the industry, (b) the information customers bring to the board might overlap with the information of the supplier, and (c) controlling for the presence of a customer on the board offers a stronger test for the SOTB's effect. Since having a customer on the board is meaningful only in a B2B context (any board member of a B2C firm will qualify as a customer if they purchase or use the firm's product or service), we use a B2B sample. From an empirical perspective, if we include B2C firms in our sample alongside B2B firms, the column capturing the presence of a customer on the board for B2C firms will be “NA” and hence those observations pertaining to B2C firms will get dropped from regression analysis.

Our final sample includes 353 firms. To collect our study's variables, we use different sources such as COMPUSTAT, ExecuComp, and S&P databases for the period from 2007 to 2015 and merge them into a single database. After excluding missing observations, the sample used for the analysis comprises 2557 firm‐year observations. Table 1 provides the definition and sources for the study variables.

Variable definitions and sources

Note: Diversity categories detailed in text.

Abbreviations: DV, dependent variable; IV, independent variable.

Variables

Focal independent variable, SOTB

Our focal‐independent variable is a binary variable that takes the value of 1 if there is an SOTB and 0 otherwise. To identify the presence of an SOTB, we utilized the firm's proxy statement (all public firms file a proxy statement before the annual shareholder vote). A component (DEF‐14A) of the proxy statement provides information on directors, which can be used to identify an SOTB's presence objectively. Specifically, a director does not qualify as an independent director if they are an employee (or partner or a controlling shareholder) at a supplier firm to which the focal firm made payments for goods or services that exceeded the greater of $1 million or 2% of gross revenues (for NASDAQ, the limits are 5% or $200,000). Thus, while determining whether a director qualifies as an independent director, firms disclose any transactions, and if so, whether they are above or below these thresholds. We collected this information manually for all firms in our sample. We classified a firm as having an SOTB if the focal firm received goods or services from a firm where a director is employed.

Dependent variable, financial performance

Firm performance can be measured using different metrics. This study uses ROA to measure firm performance. ROA captures the competence of a firm in using its assets to generate profits. We chose to use ROA as it is a universal and holistic measure of firm performance. Unlike other financial performance measures like return on equity, which can be manipulated through debt leverage, ROA is less vulnerable to manipulation as it involves multiple asset types (property, equipment, and people), which are difficult to tamper with (Deloitte, 2013). Our choice of ROA is in line with previous studies in operations management (Hendricks & Singhal, 2014; Roh et al., 2016; Swink & Schoenherr, 2015) that have used this outcome to measure firm performance.

Moderating variable, operational efficiency

We measure operational efficiency (Ops_efficiency) using inventory days. Inventory usually accounts for a significant proportion of a firm's operational capital requirement. To compute this metric, we first calculated the ratio of total inventory to the total cost of goods sold and multiplied this ratio by the average number of days in a year (Lo et al., 2009). This measure captures the average time a company's capital is locked up in inventory. The lower the inventory days (adjusted for industry differences), the higher the efficiency of its operations.

Moderating variable, diversification

We measure diversification using the number of business segments a firm operates in. As the number of business segments increases, the diversification increases (Narasimhan & Kim, 2002).

Moderating variable, demand uncertainty

Demand uncertainty is measured using the procedure recommended by Keats and Hitt (1988). First, we calculated industry sales (sum of annual sales for all firms operating in the same two‐digit Standard Industrial Classification [SIC] code). Next, for each industry, we ran a regression on industry sales for the prior 5 years using the equation:

Control variables

We included board‐level, TMT‐level, and firm‐level variables found in previous studies to affect firm performance. We included board size, board experience, board connectedness, board governance, operational experience of the board, and customer on the board (Bommaraju et al., 2019; Dalton et al., 1999; Larcker et al., 2013) as controls at the board level. We also accounted for board diversity in age, tenure, outside directorships, and functional experience. At the TMT level, we controlled for TMT size, total stock ownership, equity compensation, and CEO tenure (Carpenter & Sanders, 2002; Henderson et al., 2006). At the firm level, we included industry concentration, firm size, and leverage (Bae et al., 2017; Lee, 2009).

Board size is based on the number of directors (inside or outside directors, who can be either independent or affiliated) serving on the board. According to the RDT, board size determines the board's ability to provide critical resources to the firm. Dalton et al. (1999) have noted that board size positively influences firm performance. To measure a board's experience, we used the average age of the directors. Greater experience is likely to affect firm performance positively. We measure board connectedness by calculating the average number of other boards that a director serves on. Larcker et al. (2013) have shown that directors serving on more than one board can be effective for a firm. One often used measure of board governance is whether the CEO also serves as the board chairman. This is referred to as CEO duality and poses a conflict of interest as the chairman is supposed to monitor the actions of the management whom the CEO represents. Regulators and government agencies widely criticize CEO duality. We measured board governance using a dummy variable: 1 if the CEO is the chairman of the board and 0 otherwise. As duality leads to lower oversight, it is likely to influence firm performance negatively. We also controlled for customers’ presence in the boardroom. We coded for the customer on the board in the same way we did for SOTB.

Next, we controlled for the presence of operational experience among board members. Specifically, we coded a variable, COO director as 1 if any director is serving in an operational role and 0 otherwise. This variable captures the presence of any director in the firm's board who has operational experience such as being a COO or holding an equivalent designation, in his/her primary organization. It is important to control for this aspect, as this variable would account for any operational experience that the board may possesses over and above SOTB's experience/knowledge. 3

We calculated board diversity relating to age, tenure, outside directorships, and functional experience. We followed the procedure outlined by Harjoto et al. (2015) to calculate these measures. The logic used in the literature to measure diversity metric (e.g., Franke et al., 2021; Harrison & Sin, 2006) is to set up the variable for which diversity is being computed with a manageable spread of values (Blau, 1977). Specifically, to calculate a variable's diversity, we (a) created multiple categories of the variable, (b) computed the proportion of directors within each category, and (c) computed 1 − (prop in category1ˆ2 + prop in category1ˆ2 + …) as the diversity metric. For example, to calculate age diversity, we first created five categories of age: <40, 40–49, 50–59, 60–69, >69. Next, we calculated the proportion of directors within each age category, followed by calculating age diversity as 1 − (age_Prop_1ˆ2 + age_Prop_2ˆ2 + age_Prop_3ˆ2 + age_Prop_4ˆ2 + age_Prop_5ˆ2).

We followed a similar procedure for tenure, outside directorships, and functional diversity. For tenure, we used the following categories: years serving on the board: <3 years, 3–6 years, 6–9 years, >9 years. For outside directorships, we created four categories: number of outside directorships: 0, 1, 2, >2. For functional diversity, we relied on the eight functional experience categories (Academic, Accountant, Attorney/Counsel, Consultant, Executive, Financial Service, Prof Director, Real Estate Services, Medical Retired, and others) provided in the Institutional Shareholder Service database.

At the TMT level, we included four key variables: TMT size, total stock ownership, equity compensation, and CEO tenure (Carpenter & Sanders, 2002). We measured TMT size as the number of executives listed in the TMT. The TMT's total stock ownership is the percentage of ownership of the firm by the TMT. Equity compensation is the ratio of equity to total compensation of the TMT. CEO tenure is measured as the number of years the CEO is employed in the position (Henderson et al., 2006).

At the firm level, we controlled for Herfindahl–Hirschman index (or HHI‐score), leverage, number of employees, and total assets. HHI‐score is a measure of market concentration. The HHI‐score is defined as the sum of the squares of the firms’ market shares in the primary industry (industry is operationalized using two‐digit SIC codes; there are 48 industries). We included leverage (debt divided by assets), as the prior literature has indicated the importance of leverage in firm performance (Goddard et al., 2005). Firm size is a significant predictor of financial performance (Lee, 2009). We used two proxies for firm size: (a) the natural logarithm of total assets and (b) the number of employees.

Model

The model to test an SOTB's effect on performance is estimated using Equation (2). In a subsequent section, we rely on both instrumental variables (IVs) and matching procedures to address the possible endogeneity of the SOTB variable.

Equation (2) includes firm‐fixed effects to account for time‐invariant firm‐specific variables that could affect firm performance and year‐fixed effects to account for year‐specific effects on performance. Such two‐way fixed effect models are common in operations management (King & Lenox, 2002) and economics (Imai &Kim, 2019) as they are robust to the concerns of omitted variables (specifically time‐invariant firm‐level variables that may be potentially correlated with regressors in Equation (2)). To test the two moderator hypotheses, we augment Equation (2) with three interaction terms [SOTB × Ops_efficiency], [SOTB × DIV], and [SOTB × DU] and evaluate the significance of these interaction variables.

Results

We find that one in five firms has an SOTB. Specifically, we find that 19% of the firms had an SOTB in 2007 that increased to 22% by 2015. Moreover, 90% of the SOTBs are independent directors at the focal firm (i.e., the transaction value between the two firms is less than 2% of the supplier revenues). Thus, suppliers serving on the board are not very powerful, alleviating concerns regarding conflict of interest. We provide information on correlation among study variables in Web Appendix 1 (WA 1) provided in the Supporting Information.

Table 2 (without endogeneity correction), column 1, provides the main effect results, and column 2 provides the results of the moderating effects. In H1, we hypothesize that an SOTB influences performance. Results in Table 3 (with endogeneity correction), column 1, provide evidence that SOTB has a positive effect on firm performance (β = 0.023, p < 0.01).

The effect of SOTB on firm performance (without endogeneity correction)

Note: Standard errors in parentheses. 0.00`35 = 3.59E‐06; 0.00`13 = 1.39E‐06.

Abbreviations: Ops_effieicncy, operational efficiency; DIV, diversification; DU, demand uncertainty.

+p < 0.10, *p < 0.05, **p < 0.01, ***p < 0.001.

The effect of SOTB on firm performance—Instrumental variable approach

Note: Standard errors in parentheses. InverseMillsRatio1 = pdf/cdf; InverseMillsRatio2 = pdf/[1‐cdf]. 0.00`2 = 2E‐06; 0.00`1 = 1E‐06. 0.00`38 = 3.84E‐06; 0.00`13 = 1.39E‐06.

† p < 0.10, * p < 0.05, ** p < 0.01, *** p < 0.001.

In H2–H4, we hypothesize the effect of an SOTB under different supply chain characteristics. In H2, we theorize that the impact of an SOTB would be stronger for firms that operate at a lower operational efficiency. According to the results in column 2, as operational efficiency decreases (reverse coded), the SOTB's effect on firm performance becomes stronger (β = 0.001, p < 0.05 4 ). In H3, we hypothesize that the effect of an SOTB would be weaker for diversified firms. The results indicate that as DIV increases, the SOTB's effect on firm performance becomes weaker (β = –0.008, p < 0.05). In H4, we hypothesize that the effect of an SOTB would be stronger when demand uncertainty is high. The results indicate that as DU increases, the SOTB's effect on firm performance becomes stronger (β = 0.203, p < 0.05).

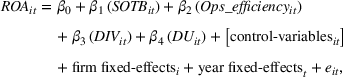

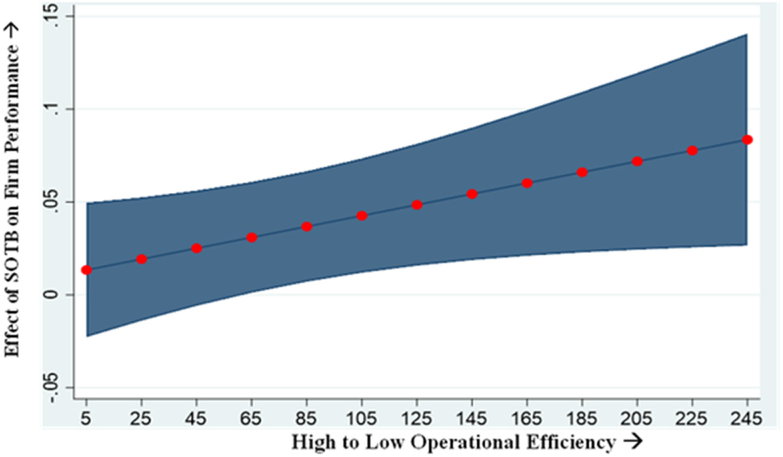

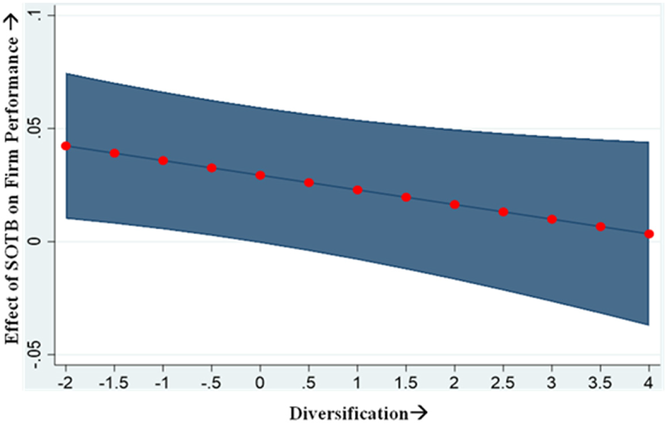

Next, we probed the interaction effects using graphical plots shown in Figures 1–3. In the graphs, the Y‐axis is the effect of an SOTB on firm performance. We examined this effect using the Johnson–Neymann technique (Preacher et al., 2006) by plotting the 95% confidence bands for legit values of the moderator (i.e., incremental values from low to high levels). This technique provides the region of statistical significance, which is the area under the confidence interval that does not cross the value of zero. As seen in the Figure 1, firms with SOTB (compared to those without SOTB) enjoy a higher performance for low to moderate levels of “operational efficiency” (operational efficiency is reverse coded). That is, SOTB's effect is more pronounced for firms exhibiting lower levels of operational efficiency, supporting H2. Figure 2 compares the effect of an SOTB on firm performance for firms with low or high diversification. We note that firms with SOTB enjoy higher performance only at low to moderate levels of diversification. As diversification increases, this positive effect decreases and becomes statistically insignificant. That is, an SOTB makes a greater impact for less diversified firms, thereby supporting H3. Figure 3 plots and compares an SOTB's effect on performance for firms with low or high demand uncertainty. As demand uncertainty increases, the effect of SOTB increases. That is, an SOTB makes a greater impact for firms that experience higher demand uncertainty, supporting H4.

Interaction effect of operational efficiency

Interaction effect of operational complexity due to diversification

Interaction effect of operational complexity due to demand uncertainty

ENDOGENEITY CORRECTIONS

SOTB, the primary variable of interest, might be endogenous with the firm performance outcome, ROA, as there could be common omitted factors that could drive both the choice of SOTB and ROA. We relied on both IVs and matching methods to address possible endogeneity.

Instrumental Variable 1

This approach is based on identifying an IV that influences the potential endogenous variable but does not directly affect the outcome variable. We used two different IVs. The first one is the presence of an SOTB in peer firms. This instrument has been used in operations literature (e.g., Bavafa & Terwiesch, 2019; Whitler et al., 2018).

For peerSOTB to be a valid instrument, it must satisfy (a) relevance and (b) exclusion restrictions. Relevance of an instrument means it should be correlated with the endogenous variable, SOTB. This can be empirically verified. We conducted the Stock et al. (2002) IV quality test using the first‐stage “Sanderson‐Windmeijer (SW) F” values (Sanderson & Windmeijer, 2016). SW F‐value of 36.71 was higher than the Stock–Yogo's 5% critical values of 16.85, and “Kleibergen‐Paap rk LM statistic” was 88.64 (p < 0.001), rejecting the null hypothesis that the test is weak and underidentified. Furthermore, the “Cragg‐Donald Wald F” statistic of 60.41 and the “Kleibergen‐Paap Wald rk F” statistic of 36.71 were well above the Stock–Yogo's 5% critical value of 16.85, supporting that the instrument is relevant.

The second assumption of exclusion means that peerSOTB does not directly influence the focal firm's performance. This assumption cannot be directly tested but one can present arguments to rule out some plausible ways in which this assumption could be violated (Bavafa et al., 2018). One possibility is that peer firms with an SOTB might make it difficult for the focal firm to bring an SOTB, affecting the focal firm's performance. We do not consider this to be a possible issue as each industry has hundreds of suppliers, and hence firms should not face constraints in bringing a supplier into the boardroom. The second possibility is that as peer firms have an SOTB, their performance will increase, thereby affecting the focal firm's performance. We rule out this possibility as peerSOTB accounts for all firms in the industry (best, good, and average) and hence the direction of influence on the focal firm's performance is not clear. Based on the above, it is reasonable to argue that the exclusion restriction is satisfied.

As the endogenous regressor SOTB is a binary variable, in the first step, we estimate the probit model specified in Equation (3) with peerSOTB as the instrument along with the other regressors. All firms operating in the same primary two‐digit SIC code as the focal firm, are considered peer firms. We measured peerSOTB as the percentage of peer firms that have an SOTB.

From Equation (3), we computed the inverse mills ratio (IMR = {probability density function pdf / cumulative distribution function cdf}). To use IMR as the control function, we followed Wooldridge (2002, procedure 18.4, p. 631) and computed the following two additional variables: SOTB × IMR and (1 − SOTB) × (pdf / [1 − cdf]). As a next step, we augmented Equation (2) with the computed control function variables—(SOTB × IMR), and (1 − SOTB) × (pdf / [1 − cdf]). This augmented model accounts for any potential endogeneity concerns of the primary variable SOTB. Here, we note that even the augmented models with the control functions have firm and year‐fixed effects. The augmented models are estimated using STATA's xtreg and reghdfe commands. We have also used a 2SLS method (instead of a control function type procedure) and results remain the same (please see the Supporting Information, Web Appendix WA2).

Our results remain robust (Table 3, columns 1 and 2). Specifically, we find that SOTB has a positive impact on firm performance (β = 0.033, p < 0.05). We also find that SOTB has a stronger effect when the operational efficiency is lower (β = 0.001, p < 0.05) and demand uncertainty is higher (β = 0.193, p < 0.05). As expected, SOTB has a weaker effect when firm is highly diversified (β = −0.007, p < 0.05).

Instrumental Variable 2

Though the “peer instrument” has been used in operations and marketing disciplines (Bavafa & Terwiesch, 2019; Whitler et al., 2018), it has an important limitation. While it addresses firm unobservable variables, it does not address industry unobservable variables. 5 To address this limitation, we borrow an idea from Wowak et al. (2021), who used the fraction of male directors who sit on other boards with at least one female director as an instrument for the presence of a female director. In our context, we use the “fraction of directors who sit on other boards that have an SOTB” as an instrument for SOTB. As more directors sit on other boards that have an SOTB (and see the utility of having of an SOTB), it is likely that those directors will appoint an SOTB on the focal board as well (instrument relevance). At the same time, since these firms are operating across other industries and not competing directly with the focal firm, they are unlikely to impact the focal firm's performance other than through the presence of an SOTB (instrument exclusion). Using this instrument, we ran the two‐stage control function approach, including the moderators. Our results remain robust (Table 3, columns 3 and 4). Specifically, we found that SOTB has a positive impact on firm performance (β = 0.072, p < 0.05). We also found that SOTB has a stronger effect when the operational efficiency is lower (β = 0.001, p < 0.05) and demand uncertainty is higher (β = 0.214, p < 0.01). As expected, it has a weaker effect when the firm is highly diversified (β = −0.006, p < 0.05).

Matching method 1 (coarsened exact matching [CEM])

The above two endogeneity corrections rely on the IV approach. Another method to address endogeneity is matching. Though matching and control function approaches may seem similar (both use a two‐stage regression approach), the identification assumptions are different for the two. In the control function approach, it is the selection on “unobservables” (an IV is needed for the control function approach but not for matching) (Heckman & Navarro‐Lozano, 2004). In matching, the identification relies on the selection on observables. Hence, we tested the robustness of our results using matching methods to provide greater confidence in our results. Specifically, we use the CEM method, which is gaining traction because of its intuitive nature (Roh et al., 2016). We matched each firm with an SOTB on industry, revenue, and year with a firm that does not have an SOTB. In other words, two firms operating in the same industry and the same revenue range are matched every year. After CEM matching, 523 observations (410 in control; 113 in treatment group; {control = firms without an SOTB; treatment = firms with an SOTB}) were lost due to matching. The matching algorithm outputted a total of 521 strata with 184 matched strata. After matching, the mean (SD) of the Revenue variable was 10435.61 (17217.417) for the control group and 10742.032 (15806.396) for the treatment group. This shows that in the matched sample, the mean and SD in the two groups are similar or comparable. Additionally, we computed the imbalance score to quantify the matching process. The multivariate L1 statistic quantifies the sample's overall imbalance such that the perfect balance is indicated by L1 = 0. Larger values indicate a larger imbalance between the treatment and the control groups. The L1 statistic decreased from 0.1798 in the unmatched sample to 0.1027 in the matched sample.

On this reduced sample, we ran a regression of firm performance on SOTB along with other variables (see the Supporting Information, Web Appendix WA 3). We found that the effect of SOTB remains significant (β = 0.018, p < 0.10). We also found that the interaction term of SOTB with operational efficiency is significant (β = 0.001, p < 0.05) in support of H2. In addition, the interaction term of SOTB with the diversification (β = −0.011, p < 0.05) is significant. Though the interaction term of SOTB with demand uncertainty has the sign in the expected direction, it is not statistically significant. We, therefore, conclude that our findings, with one exception, are robust to alternative identification assumptions.

Matching method 2 (propensity score matching [PSM])

We also tested our results using traditional matching procedures. Specifically, we used the PSM method. In the first stage, we ran a logistic regression model to predict SOTB presence using other variables (except performance). Using the weights obtained in the first stage for each observation, we ran the second‐stage regression with performance as the dependent variable (see the Supporting Information, Web Appendix WA4). We found that SOTB has a positive impact on firm performance (β = 0.017, p < 0.05). We also found support for the moderators. Specifically, the SOTB is more impactful when operational efficiency is lower (β = 0.001, p < 0.10) and demand uncertainty is higher (β = 0.288, p < 0.01) and less impactful when the firm is highly diversified (β = −0.009, p < 0.01).

ROBUSTNESS CHECKS 6

Alternative measure for operational efficiency: In our primary model, we relied on “inventory days” to capture operational efficiency in the main model. To test the robustness of our finding that an SOTB is more valuable in firms operating at lower efficiency, we used an alternative metric, cost efficiency (shown in Table WA5, in the Supporting Information). Following Krause et al. (2013), we calculated cost efficiency as the difference between COGS growth and revenue growth. COGS may rise because of higher prices for supplies and may fall because of improvements in cost controls, productivity, and technology adoption. If the COGS growth is outpacing revenue growth, then the firm is less efficient in cost management than revenue management. In our model, we replaced inventory days with cost efficiency and found the interaction term between SOTB and cost efficiency to be positive and significant (β = 0.106, p < 0.01), thereby providing further support to H2.

Alternative measure for diversification: We measured diversification as the number of business segments operated by the firm. To test the robustness of our finding that an SOTB has a lower impact for more diversified firms, we used Palepu's (1985) entropy‐based measure of diversification (shown in Table WA6, in the Supporting Information) that considers both the number of segments and the relative importance of each segment in total sales. Specifically, if a firm operates in N business segments, we compute the diversification as follows: Let Pi be the share of the ith segment in the firm's total share. Then, Diversification = N i = 1∑ Pi × ln(1/Pi). We used this measure of diversification instead of the number of segments, and our results held true. Specifically, we found that the effect of SOTB on firm performance weakens as diversification increases (β = −0.020, p < 0.10).

Alternative measure for the dependent variable: We used ROA as the dependent variable in our primary models. To test the robustness of the results, we used an alternate metric, net profit margin, as the DV (see WA7, in the Supporting Information). While the effect on net profit margin using PeerSOTB as the instrument was significant only at p < 0.10, the effect without instrument (0.036, p = 0.012) and the effect using the second instrument (0.606, p = 0.036) were significant at p < 0.05. Hence, these results further strengthen our primary findings and highlight the importance of SOTB and its relationship with firm performance.

The effectiveness of SOTB in the presence of a chief supply chain officer (CSCO): We tested the influence of SOTB on the firm's ROA in the presence of a CSCO. Specifically, we checked if an SOTB is a substitute or a complement to a CSCO. To examine this, we coded the CSCO presence in our sample firms and added an interaction term between SOTB and CSCO. We found that SOTB continues to have a positive influence on ROA. However, the interaction term is not significant, suggesting that the value of an SOTB does not depend on the presence of a CSCO. In other words, the value that an SOTB brings to the firm does not seem to substitute the knowledge and resources contributed by a CSCO.

The effectiveness of SOTB in the presence of a Buyer on the board: We also tested the influence of SOTB on the firm's ROA in the presence of a buyer on the board. Specifically, we checked if the supplier and the buyer on the board substitute or complement each other. We found that the interaction term between SOTB and buyer on the board is not significant. However, both supplier and buyer have a positive main effect, implying that they bring valuable information to the board and that information is not substitutable. In other words, the human and social capital of the supplier and the buyer are independent of each other.

DISCUSSION

This study starts with a premise that a reduction in the number of inside directors in company boards results in a deficit in boards’ knowledge of the firm, which potentially weakens the boards’ effectiveness in providing strategic counsel to the firms’ TMT. Our study investigates this phenomenon from the perspective of a firm's supply chain function. It explores the efficacy of nominating a supplier to the firm's board (SOTB) to address this deficit. The study proposes and empirically shows that an SOTB is likely to possess relevant knowledge and connections and enable the firm's board to better deal with external contingencies and dependencies, thereby contributing to higher firm performance.

The novelty of idea and findings: While past board research has examined board participation in strategic issues relating to the scope of the firm, entrepreneurship, strategic change, acquisitions and mergers, and internationalization, few board studies have focused on the functional domains of operations and the supply chain. In the operations area, Krause et al. (2013), examined the impact of including directors with operational experience on firm performance. Wowak et al. (2021) examined how the presence of female directors changes the tone of decision making with respect to product recalls in male‐dominated boards. However, fewer board studies exist in the supply chain domain. This gap is surprising given the changes in the business landscape in the last 20 years that have made the supply chain area a source of uncertainty as well as a source of competitive advantage for firms. We propose that the boards’ role in reducing this gap has not been addressed to date. A few studies have attempted to investigate organizational actions at the TMT level, such as creating positions like COO and CSCO. These actions, however, do not address knowledge gaps at the board level. This study offers a novel solution for meeting this gap—adding a supplier from the primary area of a firm's business to the board. This action can enhance a board's effectiveness in providing strategic advice on supply chain decisions since an SOTB (a) is likely to meet gaps present in the board concerning supply chain knowledge; (b) brings in the supplier‐side opinion into a firm's strategic decision making, an opinion that is increasingly becoming valuable because of the rise in the firm's supply chain complexities; and (c) brings legitimacy to the firm's supply chain function. The observation of robust performance effects for the presence of an SOTB, after controlling for board, TMT, and firm characteristics, offers a clear signal that this structural choice is valid and has promise for advancing boards’ effectiveness. Moreover, we believe our theorizing and results give us confidence in suggesting that an SOTB is valuable across industries. For example, Microsoft appointing John W. Thompson, the CEO of Virtual Instruments, its supplier to its board is a testimony that SOTB is valuable in the tech services industry.

Interestingly, prior research has noted that board size is negatively related to firm performance (Guest, 2009). Our results also show that board size is negatively related to ROA. However, we find that the action of nominating an SOTB, which increases board size, has a positive impact on firm performance after controlling for board size. The result appears to suggest that although the size of the board may matter, boards should also pay attention to gaps in board capital for improving firm performance.

We note significant research on board composition and functional representation exists outside the operations discipline. Board research is more advanced in the management, finance, and accounting disciplines (Hambrick & Cannella, 2004). However, corresponding research in the supply chain field concerning board representation and performance effects has been relatively scarce. Though we know significantly more about how other functional areas participate in firms’ strategic decision‐making processes and their subsequent impact on firm performance, we have less idea about these issues from a supply chain perspective. In our view, a paucity of research on these issues has contributed to lower visibility and importance of the supply chain function in firms.

Quantifying the performance impact of an SOTB: We compute the ROA of firms with an SOTB and compare it with the ROA of firms without an SOTB to understand the value of including an SOTB. We also examine SOTB's impact across different levels of the moderator conditions used in the study. At the mean level, the presence of an SOTB increases a firm's ROA by 11.01%. It is similar to Whitler et al.'s (2018) finding that having a director with marketing experience leads to a 7.87% higher growth in revenue. Further, we find that an SOTB's value is elevated under certain conditions; when a firm's operational efficiency is low (high), SOTB increases ROA by 24.70% (5.77%). However, when the firm has more (less) diversified operations, an SOTB increases ROA to a lower (higher) degree 3.22% (11.92%). When the firm faces higher (lower) demand uncertainty, the presence of an SOTB increases ROA by 22.29% (6.53%). These results emphasize that having an SOTB can add value to firms, and this value is enhanced for firms operating in certain environments.

SOTB's value creation mechanism: Ideally, one should examine board‐level variables such as board knowledge and involvement in supply chain decisions to answer the value creation question. However, boards’ internal workings are not public information. As an alternative, we examine if the ROA improvement comes from improving costs or revenues. If our theoretical argument that an SOTB brings unique supply‐side knowledge holds, we should observe a major improvement in costs but not necessarily in revenues. To test this argument, we regress revenue intensity (computed as total revenue/total assets) and COGS (cost of goods sold) intensity (computed as total cost/total assets) on SOTB (along with other covariates) and find that SOTB affects COGS intensity (β = –0.059, p < 0.05) but not revenue intensity (β = 0.019, p > 0.10). In other words, firms with an SOTB have lower COGS intensity, signaling better knowledge about suppliers and upstream markets and better leveraging of relationships with their suppliers. This result identifies cost influence as a possible mechanism through which an SOTB likely influences firm performance.

Antecedents to having an SOTB. To understand why some companies include an SOTB and others do not, we first relied on our empirical analysis. The first‐stage results show that firms with the following characteristics are less likely to include an SOTB: firms operating in a greater number of business segments (i.e., diversified), firms that show lower diversity in the age of directors, and firms that do not have a customer on the board. The SOTB will have knowledge and connections in their primary industry but may lack these in other industries the focal firms operate in. Our results support this premise, and this seems to influence the decision by firms to include an SOTB. When board members are similar in age, they may be less divergent in their beliefs and frames of reference, and since the supply chain function is not valued as much as other functions, the propensity of firms is not to include an SOTB. Finally, the customer on the board result signals that companies that bring directors from their value chain (either downstream or upstream) are more likely to nominate an SOTB. Next, from a conceptual perspective, supplier concentration could be a reason for not having an SOTB. When there are very few suppliers, it may be hard for the firm to select a supplier to sit on their board because of the higher potential for conflict of interest. Also, regulations require that the focal firm cannot contribute to more than 2% of the supplier revenues for a director to be qualified as an independent director. Another important factor is that boards typically focus on monitoring the TMT and hence appoint executives from compliance‐oriented backgrounds (finance, accounting, legal, and administration functional areas). Therefore, there is less representation of critical functional areas such as supply chain and marketing.

Suppliers’ role in firm strategy: Our study extends extant research on supplier–firm relationships by showing that an SOTB can fill a board's knowledge gaps in the supply chain area and thus contribute to higher firm performance. While past research (e.g., Bowen et al., 2001; Jin et al., 2019) has used the collaboration paradigm to study suppliers’ participation in strategic business unit (SBU)‐level firm decisions (e.g., product development, sustainability, efficiency, and competitiveness), our study elevates the participation frontier to a strategic space where the supplier is part of the board and actively involves in the firm's strategic decisions (Roth & Rosenzweig, 2020). Our study, using contingency analyses, identifies conditions under which an SOTB can enhance a firm's performance. Future research can build on this line of inquiry and design more comprehensive nomological models that fully account for an SOTB's role.

The role of directors beyond monitoring: Traditionally, one of the primary functions of boards is to monitor the TMT. Consequently, extant research has overwhelmingly focused on directors’ incentives to monitor. Leading academics relying on agency theory have advocated this perspective; it is also the dominant view among regulators and practitioners. However, past research has found limited support for the agency theory argument that board incentives enhance firm performance (Hillman & Dalziel, 2003). This study argues that boards should have a much broader scope than only monitoring the TMT. Specifically, we show that directors can enhance firm performance by providing valuable resources. We argue that firms with linkages to sources of dependency at the board level can access information, receive feedback, and reduce uncertainty more than firms without such linkages.

LIMITATIONS AND FUTURE RESEARCH DIRECTIONS

Though we break new ground in the research stream on buyer–seller relationships within the operations management literature by focusing on the SOTB's role, our study has a few limitations. First, an in‐depth understanding of the SOTB's characteristics—background, personality, education, social ties/capital—would shed more light on the choice of the supplier being elected on the board of a buyer firm. Second, while we focused on environmental factors to understand the value of an SOTB, we did not examine industry‐level factors that enhance/mitigate the performance effects of an SOTB. This idea primarily stems from the RDT's importance to the nature of the industry, its specific uncertainties, and regulatory issues that drive firm survival and growth. Third, while we focus on the performance effect of having an SOTB for buyer firms, an SOTB can also influence the performance of the supplier firm. In arguing from a resource dependency perspective, we can theorize that the supplier firm may enjoy greater legitimacy in the marketplace because its representative is on the board of a reputed and comparatively bigger organization. Thus, future research can also explore the dual effect of the presence of an SOTB. Fourth, future research could explore whether companies that faced major supply chain disruptions, which prompted them to realize the importance of operations/SCM would subsequently add an SOTB to the board. Moreover, one could analyze whether SOTB is helping reducing frequency and severity of supply chain disruptions. Finally, the sample firms used for our study are primarily B2B firms. Although we do not believe that the study logic and results will be different for B2C firms, future research can evaluate if there are systematic differences between B2B and B2C firms in the efficacy of including an SOTB. In summary, our study adds significant value to the general area of board composition and the specific area of enhancing the board capital through addition of a member from the firm's supply chain.

Footnotes

1

We thank an anonymous reviewer for this recommendation.

2

We thank an anonymous reviewer for this suggestion.

3

We thank an anonymous reviewer for this suggestion.

4

The exact coefficient (SE) 0.00027 (0.00014); we reported three decimal places.

5

We thank an anonymous reviewer for pointing this out and suggesting an alternative instrument.

6

We thank an anonymous reviewer for guiding us with this section. Reported tables in the Supporting Information were using peer SOTB as the IV. However, analyses were also repeated using the new IV and results were similar. See Supporting Information, Web Appendix WA5 till WA8.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.