Abstract

In this paper, we study how provision of product information and/or market information affects buyers' and sellers' behavior and the resultant sales in an online marketplace. We first identify the Pareto‐dominant equilibrium for the sellers' pricing decisions. Then, we study the impact of market parameters on the sales of the platform in equilibrium, under various information structures. We find that the platform's sales increase with the size of potential buyers but change nonmonotonically with the size of potential sellers. Next, we analytically characterize the platform's optimal information strategy as a function of the underlying market parameters. We find that while it is always optimal for the platform to reveal some information, it should be strategic about which information to reveal when faced with different supply and demand conditions. In particular, in a seller's market (high ratio of potential buyers to sellers), the platform should provide both product and market information to the sellers and buyers. However, in a buyer's market (low ratio of potential buyers to sellers), it is optimal for the platform to only provide the market information—providing both the product and market information would backfire on the platform by jeopardizing its sales.

INTRODUCTION

The rise of the Internet has created a spurt for online marketplaces, with 97% of U.S. consumers who shop online do so in a marketplace as of 2017 (Ali, 2018). An online marketplace is a website or a mobile application where potential buyers have access to buy products offered by many different sellers. The operator of a marketplace typically operates on a consignment basis, meaning that it does not own the inventory. Rather, the operator provides a platform for sellers and buyers to list and browse products, respectively, and for the two sides to carry out secure transactions. Leading online marketplaces include Alibaba (Taobao), Amazon Marketplace, eBay, and JD.com, but there are many others such as Buy.com, Etsy, Newegg, Rakuten, Shopify, Swappa, just to name a few. To put things in perspective, half of all online sales in 2016 occurred in online marketplaces (Howland, 2017), with this number only expected to grow each year.

Typically, an online marketplace makes money by charging sellers a commission that is proportional to the total amount of the sale of a product. For example, eBay's commission is between 5% and 15% of the total sale depending on the product category while Amazon's is 8%–17%.1 As a result, revenue of an online marketplace typically increases with total sales of the platform (i.e., total dollar amount of all transactions). It is thus no surprise that sales are being used as a standard metric to measure an online marketplace's financial success. To attract sellers and buyers to visit its platform and complete transactions, an online marketplace can leverage different information structures on its platform to increase sales. We focus on informational strategies in this paper by distinguishing two types of information that can be influenced or provided by the online marketplace on its platform, namely, product information and market information.

Product information, in this paper, refers to detailed description of a product in addition to basic textual information. It can include detailed product description and technical specification illuminated by graphics and videos, as well as Q&As and customer reviews that will allow customers to better understand and evaluate the product according to their individual needs. Although some online marketplaces allow individual sellers to post product information on their own, we focus in this paper on the ones like Amazon where it is the platform that determines the amount and type of product information to be released. Without product information, the buyers may not be able to accurately infer whether the product can satisfy their individual needs, which ultimately affects the buyers' willingness‐to‐pay for the product. For example, while Amazon provides the product information (textual, graphics, videos, Q&As, and customer reviews) for the Bose QuietComfort 35 Series II Wireless Headphones to customers in the United States, Submarino.com.br (the leading online marketplace in Brazil) and Real.de (one of the top online marketplaces in Germany) provide little or no information for the same product to their customers.2

Market information, in this paper, refers to the actual demand and supply of a product in the online marketplace. This information can be obtained by the platform through real‐time data collection (i.e., tracking website visitors and product listings) and analysis (i.e., deploying machine learning algorithms). Note that the market information is not available to the sellers or the buyers unless the platform, who owns its website, chooses to disclose it. However, whether disclosing the information is a delicate decision of the platform because the sellers can use the information to better estimate the product's selling probability and optimize their individual selling prices. Consequently, the sellers in an online marketplace could alter their pricing strategies when the platform does provide the market information and that may end up hurting the platform financially.

Intriguingly, despite the unprecedented boom in the online marketplaces and the proliferation of information in contemporary life, not much research has been conducted in the existing literature on the role of product and market information in an online marketplace and the resulting decisions made by buyers and sellers that are involved. To this extent, we take an important first step in this paper to understand the following questions: (Q1) How do sellers make their optimal pricing decisions under different product‐ and market‐information structures in an online marketplace? (Q2) What are the impacts of market parameters and information structures on sales of the platform? (Q3) When should an online marketplace provide its buyers and sellers with product and/or market information on its platform?

To address these questions, we develop a stylized model to capture four different information structures of an online marketplace: (i) In the no‐information case, the platform does not provide its buyers and sellers with the product or market information; (ii) in the product‐information case, only the product information is provided; (iii) in the market‐information case, only the market information is provided; and finally, (iv) in the product‐and‐market‐information case, both the product and market information is provided. Furthermore, the number of buyers and sellers who join the platform are randomly determined from a buyers' pool and a sellers' pool (consisting of potential buyers and sellers in the market), respectively. The sellers make pricing decisions for their products by considering not only buyers' product valuations but also other sellers' strategies, necessitating an equilibrium analysis. While the market information directly changes sellers' pricing decisions in equilibrium, the product information directly changes buyers' product valuations and, therefore, indirectly affects the equilibrium pricing strategies of the sellers and the ultimate sales of the platform.

We analytically identify the Pareto‐dominant equilibrium for the sellers' pricing decisions under all of the different information structures (i.e., no information, product information, market information, and product‐and‐market information). We find that sales of the platform increase with the size of potential buyers but exhibit a nonmonotonic pattern with the increase in the size of potential sellers. This is because increasing the number of sellers in the market, at first, increases the product availability, which raises the expected sales volume and sales. Yet, eventually, when the number of sellers outnumbers that of buyers by so much, the competition among the sellers will drive down the listing prices and hurt the expected sales. This finding contradicts the conventional wisdom that more traffic attracted to an online marketplace is always more beneficial for the platform operator and suggests that there is a “sweet spot” for online marketplaces in terms of the number of sellers.

By comparing expected sales under the different information structures, we establish the platform's optimal information strategy, which is proven to depend on specific market conditions. In particular, providing market information to sellers always benefits the platform, as it allows sellers to make informed pricing decisions based on the realized market condition. However, providing the product information could backfire. Specifically, the provision of product information widens the spread/variation of consumers' valuations, which increases the number of high‐valuation buyers. Hence, in a seller's market (i.e., high ratio of potential buyers to sellers), increasing the number of high‐valuation buyers encourages more sales at higher prices, boosting the overall sales. By contrast, in a buyer's market (i.e., low ratio of potential buyers to sellers), concealing the product information drives up the overall sales as it reduces the number of low‐valuation buyers allowing sellers to strike better deals with buyers at higher prices. In sum, we conclude that it is optimal for the platform to provide both the product and market information in a seller's market and only the market information in a buyer's market.

The remainder of the paper is organized as follows. Section 2 reviews the related literature. Section 3 introduces our model framework. Section 4 sets up the no‐information case as a benchmark and derives the platform's performance metrics. Section 5 studies three informational cases. Section 6 identifies the optimal information strategy for the platform. Section 7 considers several extensions to establish robustness of our results. And finally, Section 8 concludes the paper. All the technical details and proofs are relegated to the Supporting Information of the paper.

LITERATURE REVIEW

First and foremost, our research is related to the literature on information control strategy, and we study two types of information in this paper, namely, product information and market information.

Provision of the product information can influence buyers' product valuations. Lewis & Sappington (1991, 1994) extended the principal–agent model to study the incentives of a seller to release product information to potential buyers, concluding that the optimal product‐information decision for the seller is an all‐or‐nothing strategy: Either release all of the product information or do not release any. Johnson & Myatt (2006) further justified the all‐or‐nothing product‐information revelation strategy by a U‐shaped function of dispersion for buyers' valuations. In contrast to static models in which the seller and buyers interact only once (as in Lewis & Sappington, 1991, 1994, and Johnson & Myatt, 2006), Chu & Zhang (2011) developed a dynamic two‐period model to study the joint impact of the optimal product‐information strategy and the optimal pricing strategy under a preorder setting, and found that the seller should release some product information or none, but should never release full information. Boleslavsky et al. (2017) investigated the influence of using offline product demonstration methods, such as in‐store interaction and public exhibition, to signal product information to consumers and found that revealing product information via demonstrations helps alleviate price competition and support high prices. Yet, both Chu & Zhang (2011) and Boleslavsky et al. (2017) considered the product‐information revelation from the seller's/manufacturer's perspective. In contrast, in our paper, we consider an online marketplace's optimal product (and market) information revelation strategy. Hence, different from the above‐mentioned papers, the information in our case is possessed by a third‐party online market operator as opposed to a seller.

On the other side, provision of the market information can directly influence sellers' decisions. Research related to the market information in the operations management literature typically targets the demand‐side market information (i.e., the market information regarding the number of end customers). Information sharing decisions are then studied under vertical supply chain settings, where the downstream firm has the demand information and could potentially release it to the upstream firm. There is an extensive literature on assessing the value of demand information (see, e.g., Cachon & Fisher, 2000; Gavirneni et al., 1999; Lee et al., 2000; Li & Zhang, 2013; Zhao & Simchi‐Levi, 2002), and various mechanisms have been proposed to encourage downstream firms to truthfully reveal and share demand information (e.g., Cachon & Lariviere, 2001; Özer & Wei, 2006). Our research considers the market‐information sharing strategy for online platform. In this line of research, Liu et al. (2021) studied how market demand information influences the quantity decision of sellers and whether the platform has an incentive to share the market demand information to sellers. Li et al. (2021) (resp., Zha et al., 2022) investigated whether an online platform is willing to share demand information with an upstream manufacturer and a reseller (resp., sellers). Ha et al. (2022) considered whether a platform should share information with a manufacturer who decides whether to sell through an agency channel at the platform in addition to an existing reselling channel. Different from these papers, the platform considered in our paper faces a two‐sided market and possesses both demand‐side and supply‐side market information, and may rely on revelation of the information afterwards to influence the product listing prices in the marketplace. Most recently, Bimpikis and Mantegazza (2022) also studied the platform's demand information disclosure strategy in a two‐sided market but the platform determines and announces the policy before it observes demand signal.

Next, our research is also broadly related to the literature of online marketplaces and two‐sided market. The platform can provide information to participating buyers and sellers to facilitate the exchange of products, creating economic value for buyers, sellers, and society at large (Bakos, 1991). In particular, the role and influential factors of a platform (such as market size, prices, commission model, product design) has been an active research topic in the economics, operations, and information system literatures (see, e.g., Chen et al., 2016, 2020; Cui et al., 2019; Hagiu, 2009; Hu & Zhou, 2019; Jiang et al., 2011; Lai et al., 2022; Li & Netessine, 2020; Parker & Van Alstyne, 2005; Tadelis, 2016; Tian et al., 2018).

There is also an increasing interest in studying the influence of a marketplace under various supply chain strategies (see Grieger, 2003, and Wang et al., 2008, for detailed reviews). For example, Ryan et al. (2012) considered a single retailer contemplating selling through a new marketplace channel, in addition to a traditional direct channel. The retailer either pays a flat monthly fee or proportional commission to the platform in the dual‐channel setting, and the authors characterized the optimal pricing decisions for both the retailer and the platform. Jiang et al. (2017) considered a retailer who orders products from a manufacturer and sells to customers through an online marketplace platform where the customers can then resell products later on. Different from these works, our paper focuses on a platform's information revelation strategies.

Finally, another stream of the existing literature explores the determination of prices in marketplaces (see, e.g., Birge et al., 2021; Campbell et al., 2005; Kuruzovich et al., 2010) and the design of efficient trading mechanisms to match buyers and sellers (see, e.g., Chen & Hu, 2020; Chu & Shen, 2006; Wilson, 1985). In particular, McAfee (1992) examined the efficiency of the double auction mechanism among buyers and sellers, and Su (2010) proposed a matching mechanism in an online marketplace, which can be interpreted as a posted‐price mechanism with efficient rationing and retains similar matching outcome as the double auction. The matching mechanism of the online marketplace adopted in our paper directly follows this stream of research. We also contribute to the literature by the underlying technical analysis that identifies the Pareto‐dominant equilibrium of the sellers' pricing decisions under various informational structures. To the best of our knowledge, this is the first time an equilibrium for the sellers' pricing game is fully characterized in a two‐sided market with multiple buyers and sellers due to the complex nature of the problem (Chen et al., 2016, p. 591).

MODEL FRAMEWORK

We consider an online marketplace (hereafter referred to as the “platform”). The platform orchestrates a two‐sided market where a number of sellers try to sell the same new product to a number of buyers. For simplicity, we assume that each seller has one unit of the product in stock, and each buyer is interested in one unit of the product. Sellers and buyers make fully rational pricing and purchasing decisions, respectively, in order to maximize their individual utilities. The platform on the other hand can influence the decisions of both sides by providing (or not providing) product and/or market information. Details on the information structure will be given shortly.

The number of sellers to join the platform is described by a random variable

Formally, consider an arbitrary seller with reservation value

Notations.

For the demand side, the number of buyers that will join the platform is determined by a random variable

Next, we describe the platform, which can provide or withhold two different types of information on its website, namely, the (detailed) product information and the market information.

Product information refers to detailed product descriptions and technical specification, Q&As about the product, and consumer reviews, all of which can facilitate the decision‐making process of the buyers. We use the indicator parameter

Thanks to the development of data collection methods such as the visitor tracking technology, the platform is able to observe how many sellers and buyers are in the market, that is, the realized market sizes of

While each seller acts to maximize their expected revenue, so does the platform in our model. We assume the platform charges a commission that is a percentage of the transaction amount (Geng et al., 2018; Jiang et al., 2011; Ryan et al., 2012; Tian et al., 2018). Hence, the platform's total commission/revenue increases proportionally with the total transaction value (i.e., total sales). The commission rates are typically exogenously determined by the industry tradition (Liu et al., 2021), so we consider predetermined commission rates in our model. It is clear that for any predetermined commission rate, the platform can maximize revenue by maximizing sales. Therefore, we assume that the platform's goal is to equivalently maximize sales for the rest of the paper.

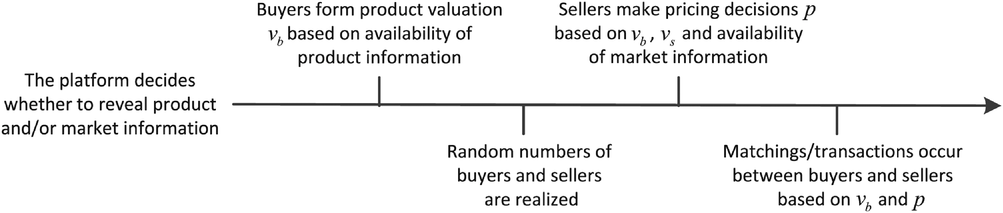

We now describe the sequence of events for our model, which is also summarized in Figure 1. First, the online marketplace determines whether it should provide product information and/or market information on its platform. Based on the availability of the product information, buyers form their valuations for the product (

Sequence of events.

In what follows, we present four models to study the role of product and/or market information. Specifically, Section 4 focuses on the no‐information model as a benchmark, that is,

NO‐INFORMATION MODEL

We first consider the

Let

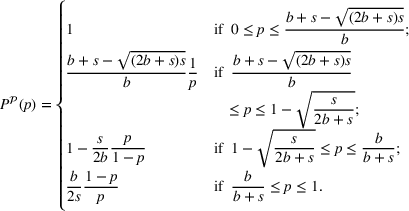

Recall from (1) that any individual seller with reservation price

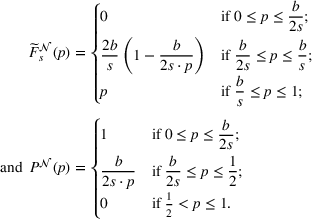

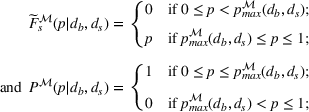

Note that in Model When

There are a few important observations from the above theorem that we will now detail. An illustration of the results is provided in Figure 2.

Illustration of

First, there exists a threshold

Second, we observe that the selling probability function

Third, recall that b and s capture the sizes of potential buyers and sellers, respectively. As the number of buyers and sellers at the platform are determined by Equilibrium listing prices (stochastically) increase in b and decrease in s, that is,

Finally, we point out that the proof of Theorem 1 is by no means straightforward and the explicit characterization of the Pareto‐dominant equilibrium for the sellers' pricing game is one of the major theoretical contributions of our paper. The complete proof of Theorem 1 and other proofs are contained in the Supporting Information of the paper (see EC.1).

Performance metrics

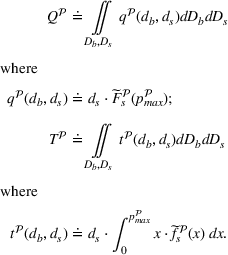

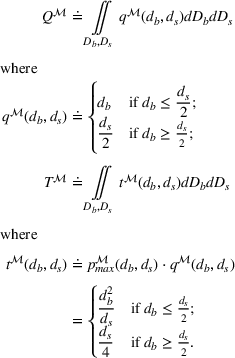

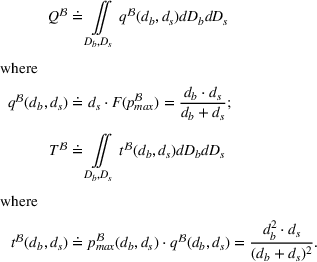

In this subsection, we derive performance metrics of the platform. While we focus on total sales (i.e., the total dollar amount of all transactions) in the paper, we also provide the derivation of sales volume (i.e., the total number of transactions), which will help explain some properties of the sales in Proposition 1.

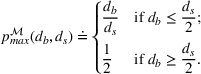

In equilibrium, the sellers list their products according to prices determined by

From Theorem 1, it can be verified that

In the next result, we establish the impact of the sizes of the potential buyers (b) and potential sellers (s) on Under the no‐information model, the expected sales volume the expected sales

Proposition 1(i) is in line with expectations, because when there is either more demand or more supply to the platform, which is a two‐sided market, more transactions will occur leading to a higher sales volume.

The more interesting result is Proposition 1(ii), which states that sales are monotonic in the size of potential buyers but not in the size of potential sellers. Intuitively, when there are more buyers in the market (i.e., an increased b), equilibrium prices (Corollary 1) as well as the sales volume go up (Proposition 1(i)), thus higher sales are expected as sales can be viewed roughly as the multiplication of price and sales volume. Yet, when there are more sellers in the market (i.e., an increased s), there are two competing forces, which now affect the sales. On the one hand, equilibrium prices go down (Corollary 1) due to increased competition among the sellers, and on the other hand, sales volume picks up (Proposition 1(i)). These two opposing effects lead to the nonmonotonic behavior of the sales with respect to the size of potential sellers s, which first increases then decreases. It may also be helpful to think of the limiting cases: When

The important managerial implication here is that while attracting more buyers is always ideal for a sales‐maximizing platform, the number of sellers has a “sweet spot.” Having more sellers is good at first because it can help boost sales by increasing the transaction volume, but eventually when the sellers greatly outnumber the buyers, the competition among the sellers will drive down prices despite driving up sales volume and start to negatively impact the sales of the platform. This is an important message for platform operators because it suggests at some point they may need to restrict the number of sellers, which runs counter to the conventional wisdom that more traffic in an online marketplace is always better for the platform. This also suggests that the platform operators should wisely allocate their resources to attract buyers and (the right number of) sellers.

INFORMATIONAL MODELS

In this section, we will investigate how product information and/or market information influence the sellers' pricing decisions in equilibrium. To this end, we will propose and analyze three informational models (when

Product‐information model

We start with the

Let

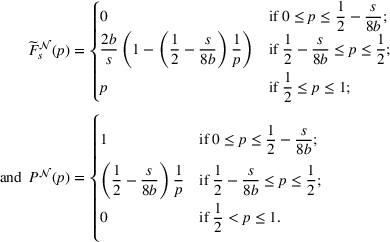

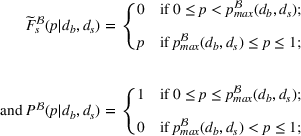

Following similar techniques used in the proof of Theorem 1, we can obtain the equilibrium listing price distribution and the corresponding selling probability function for Model Under Model

The results of Theorem 2 are illustrated in Figure 3. Similar to Model Corollary 1 is preserved under Model

Illustration of

On the other hand, the selling probability function

Finally, given the sellers' pricing decisions characterized by CDF

Furthermore, we find that the impact of b and s on the platform's expected sales and sales volume under Model Proposition 1 is preserved under Model

As the primary purpose for this section is to establish the sellers' pricing decisions in equilibrium, we will postpone the comparison of the expected sales between Model

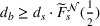

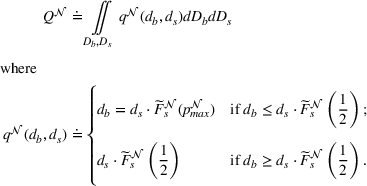

Market‐information model

In this section, we introduce the third model, the

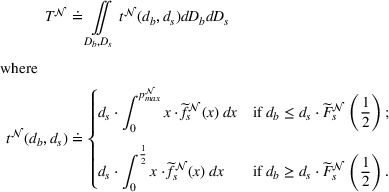

Such an information structure will significantly simplify the seller's game. In particular, denote

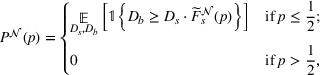

Therefore, we can directly characterize the sellers' listing price distribution and selling probability function of the unique (Pareto‐dominant) equilibrium in the following theorem. Note that the pricing decisions of the sellers with a reservation value Under Model

It is clear from (5) that Equilibrium listing prices (stochastically) increase in

Essentially, Corollary 2 for Model

From Theorem 3, we can further derive the sales volume and the sales for the platform for any given market size

Finally, we can verify that the impacts of the sizes of potential buyers (b) and potential sellers (s) on the platform's expected sales and sales volume remain unchanged from previous models. Proposition 1 is preserved under Model

Product‐and‐market‐information model

In the last model, we will analyze the scenario where the online marketplace provides

The sellers' listing price distribution and selling probability function of the unique (Pareto‐dominant) equilibrium under Model Under Model

As Corollary 2 is preserved under Model

Finally, from Theorem 4, we can obtain expressions for the platform's expected sales volume and expected sales under Model

We can verify that the impact of b and s on the platform's expected sales and sales volume remains unchanged from before. Proposition 1 is preserved under Model

OPTIMAL INFORMATION STRUCTURE FOR THE PLATFORM

Having characterized the Pareto‐dominant equilibrium for each of the four information structures in Sections 4 and 5 (i.e., Model The expected sales satisfy the following relations: (i)

The comparison results in Theorem 5 are contingent exclusively on the demand‐to‐supply ratio

First, Theorem 5(i) reveals that in the absence of the product information (i.e.,

Second, if the platform releases the market information (i.e.,

Finally, Theorem 5(iii) states that providing both product and market information leads to higher total sales for the platform compared to the strategy of withholding both types of information, if and only if the demand‐to‐supply ratio is either sufficiently low or sufficiently high but not when it is at an intermediate level (i.e., if and only if

Based on Theorem 5, we can summarize the platform's optimal information strategy in the following proposition: Consider Model

It is necessary to note that Theorem 5 and Proposition 2 do not present any comparison results under Model

Based on Proposition 2, we also know that it is always optimal for the platform to provide some information to the customers (this is true even without being able to analytically compare Model

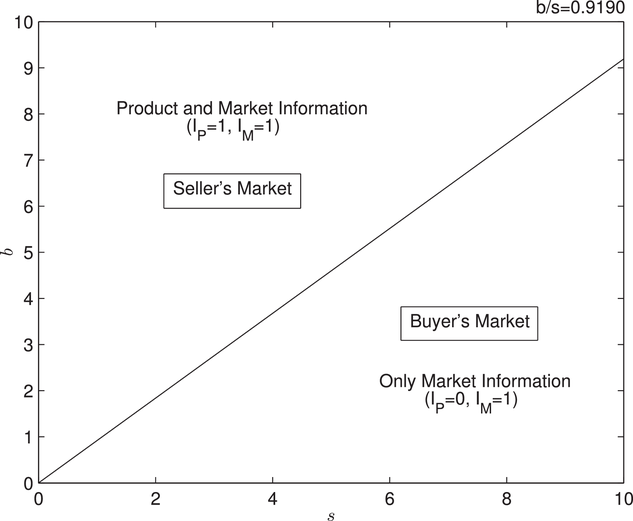

We plot the optimal information revelation strategies based on market conditions in Figure 4. Specifically, it is optimal for the platform to provide customers with both the product and market information only in a seller's market (high ratio of potential buyers to sellers). Provision of the product information can increase the number of high‐valuation buyers, which encourage more deals to be closed at higher prices in a seller's market. By contrast, when facing a buyer's market (low ratio of potential buyers to sellers), the platform will find it wise to conceal the product information so the buyers' valuations for the product are less dispersed. In this case, more buyers can strike deals with sellers without the detailed product information.

Optimal information structure for the platform as the demand‐to‐supply ratio changes.

ROBUSTNESS OF FINDINGS

In this section, we present several extensions to the main model for robustness check. Specifically, Section 7.1 considers general distributions concerning how sellers value the product. Section 7.2 examines the scenario when the platform can provide partial product information. Section 7.3 addresses the case that customers may have heterogeneous product valuations even without product information provided by the platform. Section 7.4 explores the impact of outside options. Section 7.5 studies continuous product‐information provision. Section 7.6 considers partial market information. And finally, Section 7.7 examines an alternative matching mechanism. For tractability purpose, we will modify one assumption/feature of the main model in each extension while keeping all the others unchanged.

General distribution for sellers' reservation value

In the main model, we assumed that sellers' reservation value of the product, when no market information released, follows a standard uniform distribution for closed‐form expressions. However, our insights are not driven by this assumption. To establish robustness of our results, we consider the beta distributions, whose density function can capture various curvatures depending on the two shape parameters, including horizontal lines (i.e., uniform distributions), bell‐shaped curves, or U‐shaped curves. Note that, under the beta distribution, the functional form of the unique Pareto‐dominant equilibrium for the sellers' game can still be explicitly characterized. However, numerical analyses are needed to compare the platform's sales in equilibrium across different information structures.

We find that our insights remain qualitatively unchanged. Specifically, Figure 5a illustrates the optimal information structure under beta distribution B(2, 4), B(2, 2), and B(4, 2), which exhibits a bell‐shaped density‐function curve, with mean 1/3, 1/2, and 2/3, respectively. Bell‐shaped density‐function curves imply that sellers' reservation value of the product tend to cluster around the mean, and the further from the mean, the less likely they are to occur. We observe that Figure 5a bears a close resemblance to Figure 4 under the uniform distribution. As such, our main insights regarding the optimal information structure continue to hold.

Optimal information structure for the platform when (a)

We also performed numerical analysis to explore the scenario when both the sellers' reservation value distribution and the buyers' valuation distribution (when product information is provided) follow beta distributions. The main insights from Figure 4 continued to hold.9 As such, we conclude that the results of our main model are not driven by the uniform‐distribution assumptions.

Providing partial product information

In the main model, we assumed that if the platform decides to release the product information (i.e., Model

To capture such an influence, we generalize the main model by allowing the buyers' product valuations, upon product‐information revelation, to follow a uniform distribution on the support of

We will briefly summarize our findings in this section, and defer the technical details and proofs to EC.2 in the Supporting Information. Specifically, when the platform decides to provide product information (i.e., Model

We can also observe from Figure 5b that the platform is more likely to provide product information to the buyers (i.e., the region for

Heterogeneous customer valuation when no product information is provided

In the main model, for simplicity, we assumed that when no product information is available (i.e., when

We can fully characterize the unique Pareto‐dominant equilibrium for the sellers' game (e.g., see Theorem EC.2.1 and Theorem EC.2.2 in the Supporting Information)—we provide technical details and proofs in Section EC.3 in the Supporting Information while briefly summarizing our findings in this section. The optimal information structure for the platform is reproduced in Figure 6a using

Optimal information structure for the platform when (a)

The impact of outside options

In the main model, we considered a two‐sided online marketplace where individual buyers can only purchase a product from private sellers on the platform. In practice, however, buyers may also be able to purchase the product from an outside option, for example, an online retailer, or even from the platform itself (e.g., Amazon Marketplace and Amazon are integrated). In this section, we will examine the impact of outside options on the equilibrium of the sellers' game and the optimal information structure for the platform.

For simplicity, we posit that there exists a best outside option from which any potential buyers can purchase the product at a given price

Given the price of the outside option

In addition, we derive the optimal information structure for the platform in the presence of the outside option and present the results in Figure 6b. It is clear that Figure 6b bears a very reasonable qualitative resemblance to its counterpart of the main model (Figure 4), suggesting that our findings of the main model continue to hold even with the consideration of outside options. In other words, it is optimal for the platform to provide both the product and market information in a seller's market (high ratio of potential buyers to sellers) and only the product information in a buyer's market (low ratio of potential buyers to sellers), even when outside options are present. Figure 6b also contains multiple values of

Continuous product‐information provision model

In the main paper, we have shown that providing market information (

Similar to Section 7.2, the buyers' product valuations, upon product‐information revelation, follow a uniform distribution on the support of

Providing partial market information

In the main model, providing market information means providing both realized numbers of buyers and sellers (i.e.,

In particular, in Section EC.6.1 (resp., Section EC.6.2), we consider the scenario in which the platform discloses

Alternative matching mechanism

In the main model, we assume that the product offered with the lowest price will be acquired by the buyer with the highest valuation, and so forth. In this subsection, we analyze an alternative/opposite matching mechanism where the product offered with the lowest price will be acquired by the buyer with the lowest valuation. More specifically, the lowest valuation buyer (whose valuation exceeds the listing price of the lowest price seller) will be matched with the lowest price seller with ties broken randomly, and they exit the market by completing the sale. If a buyer's valuation is lower than the listing price of the lowest price seller, then this buyer will not be able to obtain the product from this seller or any other sellers, and the buyer exits the market. Then the lowest valuation buyer among the remaining buyers (whose valuation exceeds the listing price of the lowest price seller among the remaining sellers) will be matched with the lowest price seller among the remaining sellers, and so on and so forth, until there are no more buyers and/or no more sellers in the market.

We can show that under the alternative matching mechanism, the analysis of Model

CONCLUDING REMARKS

In this paper, we study the role of information in an online marketplace. We find that information could be a double‐edged sword for the platform. On the one hand, the platform benefits from the revelation of (product and market) information in a seller's market (high ratio of potential buyers to sellers). On the other hand, it is less helpful or even harmful for the platform when all the information is revealed in a buyer's market (low ratio of potential buyers to sellers).

In particular, while market information should always be provided to reduce price competition and boost sales amount among the sellers, product information should be only provided in a seller's market and not in a buyer's market. This is because in a seller's market, there are more buyers than sellers. If all sellers can sell their products, the platform can maximize sales, especially if those sellers with high reservation values can sell their products. Provision of product information is a great strategy in this case as it allows the buyers to develop heterogeneous product valuations and buyers with high product valuations are willing to pay for a high price to acquire the product. In contrast, in a buyer's market, sellers outnumber buyers, and total sales of the platform can be improved when more buyers can successfully purchase the product, which happens when more buyers have sufficient willingness‐to‐pay. By not providing the product information, the platform can benefit from the less dispersed product valuation distribution of the customers, because fewer customers would have low willingness‐to‐pay for the product.

Our other contribution in this research is the underlying technical analysis that identifies the Pareto‐dominant equilibrium of the sellers' pricing decisions under various informational structures. As noted by Chen et al. (2016) on the seller competition for an online marketplace (see p. 591 of the paper), “it is difficult to make a comprehensive and rigorous analysis for the general seller competition case,” and we have sought to carry out the analysis under reasonable assumptions. Furthermore, we find that after taking into account sellers' strategic pricing decisions, the sales of the online marketplace increase in the size of potential buyers but are actually unimodal in the size of potential sellers. Having more sellers is good at first because it increases transaction volume, but eventually the sellers outnumber the buyers by so much that the competition among them drives down prices and starts to hurt the platform's sales revenue. This observation suggests that at some point an online marketplace may need to restrict the number of sellers on its platform, which runs counter to the conventional wisdom that more people on the platform is always more beneficial for the platform operator.

As the objective of our model framework is to capture the essential elements relevant to the information structure of an online marketplace while at the same time, keeping the analysis tractable, the model is certainly not without limitations. First, we have assumed in our model that each seller who participates in the platform only has one unit of the product in stock. In reality, when each seller represents a small business, they can carry multiple products in the inventory. However, we can extend our model without sacrificing any results to include the case where each seller has n units of the product for sale. Yet, when the market has limited number of sellers, leading to oligopoly, future work is needed to understand how limited competition among sellers influences the platform's information provision decisions. Second, products from different sellers in our model are perfectly substitutable as we focus on customers' buying and selling decisions of a particular product. In comparison, Chen et al. (2016) consider products that are not at all substitutable. Future work is needed to shed more light on the intermediate case where products from different sellers are substitutable to a certain extent.

Third, we have focused on the benefits of information to a platform, which is only half of the story—the costs of information need to be assessed to determine the overall optimal strategy for the platform. In fact, some online marketplaces do not currently provide information to customers exactly due to concerns regarding the costs of collecting information. We showed that this actually may not lead to an adverse outcome under certain situations (e.g., providing product information under a buyer's market). Fourth, we follow the matching mechanism developed in Su (2010), and future research is needed to understand whether the optimal information structure remains the same under alternative matching mechanism. Finally, we considered a monopolist platform in this paper as is typically done in the literature (see, e.g., Benjaafar et al., 2019; Cachon et al., 2017; Taylor, 2018). Under oligopoly settings, how competitive pressure influences online marketplaces' information decisions can be of an interesting yet difficult extension to this research.

Footnotes

ACKNOWLEDGMENTS

The authors are deeply grateful to the Department Editor Haresh Gurnani, the senior editor (SE), and the reviewers, for their detailed comments through the review process. This work was partially supported by the National Natural Science Foundation of China (Grant No. 71901197).

1

See

2

See

3

It is proven that the outcome of the matching mechanism can be achieved by either a double auction (McAfee, 1992; Wilson, 1985) or efficient rationing (Su, 2010). This matching mechanism has also been extensively used in experimental studies (see, e.g., Cason & Friedman, ![]() ; Plott & Gray, 1990; Smith et al., 1982). In particular, Cason & Friedman (1996) found that high‐surplus trades (between high‐value buyers and low‐cost sellers) tend to occur earlier within a trading period than low‐surplus trades.

; Plott & Gray, 1990; Smith et al., 1982). In particular, Cason & Friedman (1996) found that high‐surplus trades (between high‐value buyers and low‐cost sellers) tend to occur earlier within a trading period than low‐surplus trades.

4

While only binary product‐information decisions are considered here, we consider continuous product information in the Supporting Information (see EC.5) and show that the optimal product‐information revelation decision is still all or nothing.

5

6

Note that our insights continue to hold when buyers' valuation, without the product information, is equal to a value

7

The Pareto‐optimality maximizes the aggregate revenue for the sellers because the decisions are made by the sellers who may not be concerned about the welfare of the buyers. It can be shown that the Pareto‐dominant equilibrium actually maximizes any individual seller's expected revenue among all equilibria of the sellers' pricing game.

8

Proofs for any remarks are omitted from the Supporting Information to avoid duplication but available from the authors.

9

Numerical illustrations and results are available from the authors.

10

When modeling the impact of information revelation on consumers' valuations, the existing literature typically specifies that more information leads to higher consumer valuation dispersion/variance (see Chu & Zhang, ![]() ; Osborne, 2011). Chu & Zhang (2011) assume that consumers' valuations follow a normal distribution

; Osborne, 2011). Chu & Zhang (2011) assume that consumers' valuations follow a normal distribution

11

We consider γ as an exogenously given parameter in this section (Section 7.2). We will study the optimal product‐information level in Section ![]() .

.

12

The sellers' game for the case when the platform provides no market information (![]() . We can demonstrate that when providing the same amount of partial product information, the platform can always improve its total sales by offering market information.

. We can demonstrate that when providing the same amount of partial product information, the platform can always improve its total sales by offering market information.

13

Similar to the main model, the platform's expected sales when there is product information and partial market information on

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.