Abstract

We study return shipping insurance (RSI) policies prevalent on platforms such as JD.com and Taobao.com. Retailers on those platforms can purchase and provide RSI for consumers (RRSI) or offer an option for consumers to buy RSI themselves (CRSI). With either RSI, consumers will be partially compensated by an insurer for their shipping fees associated with product returns. As the consumers' uncertainty about product fit is realized only after purchase, their decisions whether to purchase CRSI may lead to postpurchase regret. Considering these anticipated regret behaviors, we investigate the optimal RSI policy for a monopolistic online retailer and an insurer. We show that the retailer offers RRSI only if the retailer's return handling cost is relatively low and consumers' return shipping cost is in an intermediate range; otherwise, the consumers' strong propensity for uninsured regret may stimulate them to purchase CRSI. Under the optimal RRSI policy, the retailer always charges a higher product price than under no RSI, and surprisingly the consumer demand could expand. In contrast, under the optimal CRSI policy, the retailer always sets a lower product price, but resulting in consumer demand shrinkage. Counterintuitively, CRSI may become a “win‐win‐win” policy for the retailer, insurer, and consumers.

INTRODUCTION

Online retailing has witnessed rapid growth in recent years (eMarketer, 2017). However, many consumers still hesitate to purchase experience goods such as clothes and shoes online because they cannot try the products before purchasing to alleviate their uncertainty about product fit (eMarketer, 2016; Hong & Pavlou, 2014). As a result, product returns have become the new normal. According to Invesp's statistics on online return rates, at least 30% of all products ordered online are returned, much higher than 8.89% in brick‐and‐mortar stores (Spillane, 2022). U.S. return delivery costs have been steadily increasing from $350 billion to $550 billion from 2017 to 2020 (Placek, 2022).

Most online retailers offer lenient return policies to drive sales (Abdulla et al., 2019). In China, online retailers on platforms such as Taobao.com and JD.com have long been offering 7‐day “no‐question asked” full‐refund return policies (Millward, 2014). In addition, the European Union obliges online firms to offer a no‐questions return period of 14 days (Economist, 2013). Nevertheless, 100% money‐back guarantees (MBGs) do not mean online product returns are hassle‐free for consumers (Davis et al., 1998). In general, consumers are responsible for the return shipping fee, unless the products are defective (Bower & Maxham, 2012). As the return shipping fee is not cheap, it impedes online purchasing due to the high uncertainty of mismatch (Lawton, 2008). A survey conducted by Invesp shows that 79% of consumers want free return shipping, but only around 49% of retailers currently offer that policy (Spillane, 2022). Recently, we also conducted a survey1 using the popular tool SoJump and collected 976 responses. The main results are summarized in Table 1. The survey shows that only for 6.35% of our respondents, the return shipping fee does not play a role in their product purchase decisions.

Summary of the survey.

Abbreviations: RSI, return shipping insurance; RRSI, retailer‐RSI; CRSI, customer‐RSI

In response to consumer desire for free return shipping, major Chinese online platforms (e.g., Taobao.com, Tmall.com, and JD.com) adopt return shipping insurance (RSI), an innovative insurance tool, to alleviate consumers' concerns about product returns (Sheng et al., 2016). The insurer will compensate consumers with RSI for a prespecified amount, up to the actual shipping fee, in the case of product returns. Initially, Taobao.com launched RSI through Huatai Insurance Group2 to alleviate the retailers' and consumers' risks and costs associated with online returns (He, 2013). Witnessing the success of RSI, other online platforms in China, including JD.com and Suning.com, have eagerly embraced RSI policies. Now, more than 11 insurers sell RSI services, including China Life,3 China Pacific Insurance,4 and ZhongAn Insurance.5 A report from the Insurance Association of China shows that the revenue from RSI has been growing rapidly since 2016, which has become the highest among non–auto insurance category (Tu & Zhang, 2020). In 2020, Taobao.com announced that consumers from 17 overseas countries and regions (Hong Kong, Macao, and Taiwan), including the United States, can enjoy RSI when shopping on the platform (Tencent, 2020). Indeed, RSI is a key factor in consumers' purchasing decisions (for 93.44% of respondents in our survey).

There are two types of RSI policy: (1) the retailer‐RSI (RRSI) policy under which online retailers purchase RSI from insurance companies and provide it for all consumers for free and (2) the customer‐RSI (CRSI) policy under which the retailer offers an option for consumers to purchase RSI directly from the insurer during the merchandise checkout stage. For RRSI, the retailer buys RSI for the consumers, reducing their potential product return shipping cost. In contrast, under the CRSI policy, consumers must pay for RSI themselves, and thus retailers actually transfer the premium cost to consumers. Irrespective of the RSI type, it is harder for insurers to gain profitability if more consumers tend to return products, resulting in more compensation from the insurer.

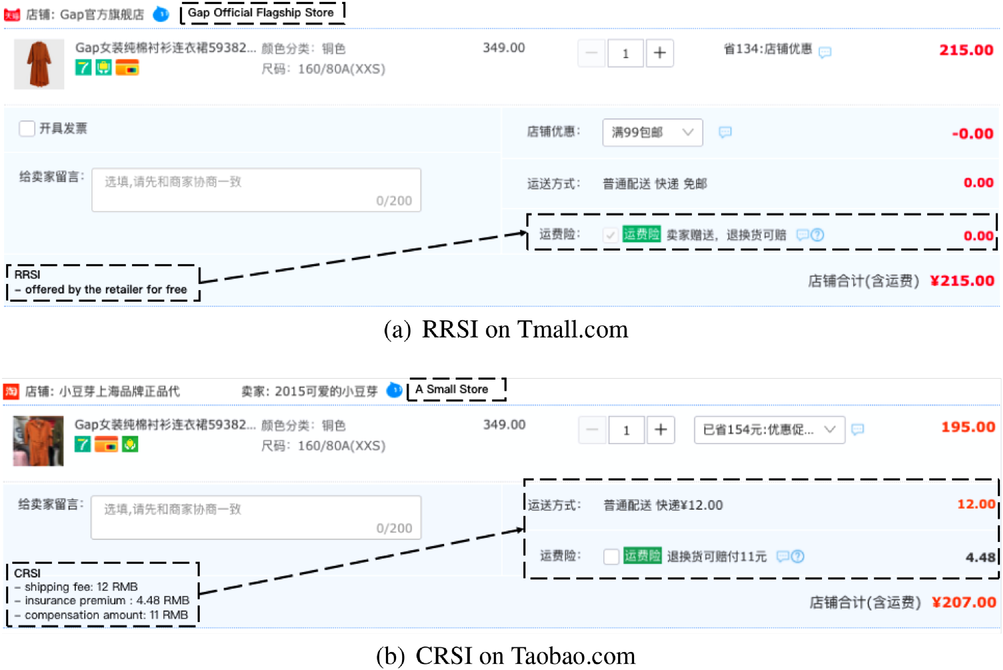

One may anticipate that retailers would prefer the CRSI policy to the RRSI policy, as consumers pay the CRSI premium themselves. However, most retailers adopt the RRSI policy (Li et al., 2021, 2023; Xiong & Liu, 2023; Zhang et al., 2022). Why do these retailers not transfer the insurance premium cost to consumers by using CRSI? More interestingly, retailers may adopt different RSI policies even when they sell the same product. Figure 1 shows that both the official flagship store of GAP on Tmall.com6 and a small seller on Taobao.com7 sell the same dress of the GAP brand, but the former offers RRSI and the latter offers CRSI. What motivates those retailers to adopt different RSI policies?

Return shipping insurance (RSI) examples of GAP.

Consumers are uncertain about their true needs at the time of purchase; therefore, they may have ex post regret about their purchase decisions of RSI under the CRSI policy (Bell, 1982; Braun & Muermann, 2004). For example, if an individual does not buy RSI but receives a mismatched product and wants to return it, the individual would experience some additional disutility of not having purchased RSI ex ante. Similarly, if an individual does buy RSI but receives a fit item, the individual would regret having purchased RSI ex ante. Our survey shows that more than 80% of respondents have experienced regret about their CRSI purchasing decisions, which reveals that regret aversion plays an important role in consumers' purchasing decisions under RSI policy. Consumer regret behaviors have attracted much attention in academia and the magnitude of consumer regret can be pronounced (Simonson, 1992; Zeelenberg, 1999), especially in the insurance industry (Braun & Muermann, 2004; Fujii et al., 2016; Huang et al., 2008; Wong, 2012). Anticipating possible postpurchase regret, consumers will take it into consideration during the purchasing process (Zeelenberg et al., 1996).

In the presence of consumer regret behaviors in online shopping, the following research questions arise naturally: (1) When is it profitable for an insurer and a retailer to adopt the RSI policy? RRSI or CRSI? (2) How do consumers' regret behaviors shape the RSI policy? (3) Will the RSI policy always increase the consumer surplus?

To address these research questions, we develop an analytical framework. We study a market with a monopolistic online retailer and focus on how the consumers' anticipated regret behavior affects the RSI policy. Consumers are heterogeneous in their knowledge about whether the retailer's product will fit them. The informed consumers know their needs exactly before purchasing the product. In contrast, the uninformed consumers are uncertain about the product's fit at the time of purchase. The retailer chooses whether to purchase RSI from an insurer and offer an RRSI policy such that the consumers' potential return shipping fee will be partially paid by the insurer. Otherwise, the retailer considers adopting the CRSI policy, under which uninformed consumers can purchase RSI from the insurer themselves. Meanwhile, the uninformed consumers anticipate that they may ex post experience regret about their RSI purchase decision under the CRSI policy. In line with the behavioral literature, we consider two types of consumer regret: aversion to the regret from not buying RSI, that is, uninsured regret, and aversion to the regret from buying RSI, that is, insured regret. For either RSI policy, the insurer determines the insurance premium to maximize its benefit.

Our analysis reveals that consumer‐anticipated regret behaviors and the heterogeneity in consumer capability of processing information shape the retailer's optimal RSI policy. Either RRSI or CRSI may be optimal, depending on the consumers' regret level. This finding differs from Zhang et al. (2022)'s argument that the RRSI policy is viable if consumers are uncertain about the product quality, but the CRSI policy never benefits the retailer. Note that, our work applies to retailers selling experience goods, such as shoes and clothes, without consumers' concerns about the product quality, while Zhang et al. (2022) focus on the market where “quality is the retailer's private information” and consumers are uncertain about the product quality. Our work explores the viability of the RSI policy through a new lens and provides an alternative explanation for the prevalent RSI policy. Although both types of RSI policy may benefit the retailer as well as the insurer, they impact the retail operations in different ways. RRSI raises the product price, exacerbating the adverse selection problem, but may expand the consumer demand, while the CRSI policy always lowers the product price, mitigates the adverse selection problem, and shrinks the consumer demand.

As a result, the RRSI policy is optimal if the retailer's return handling cost is relatively low and the consumers' return shipping cost is medium. In contrast, a sufficiently strong uninsured regret level calls for the CRSI policy when there is a relatively high return handling cost and intermediate return shipping cost. Although extensive literature (Davis et al., 1995; Huang et al., 2018) has shown the optimality of MBGs, the role of the return shipping cost is underexplored. Taking into consideration the consumers' return shipping fees, we discover that RSI, an insurance tool for possibly reducing consumers' return associated cost, further improves the profit of a retailer that offers MBG. In other words, our findings suggest that a new return policy, that is, “MBG + RSI,” is even better than the commonly adopted MBG return policy. Moreover, we show that RSI also benefits retailers who adopt partial‐refund policies, such as charging a restocking fee. Interestingly, we find that CRSI may result in a “win‐win‐win” outcome for the retailer, insurer, and consumers.

Our findings potentially explain the retailers' RSI policies shown in Figure 1. Major retailers in online platforms can handle returned products at a low cost because returned products can be cheaply repackaged due to economies of scale and resold in widespread outlets. In contrast, it costs more for small sellers to handle product returns. Therefore, major retailers favor RRSI, while small retailers adopt CRSI.

The remainder of this paper is organized as follows. In Section 2, we discuss the relevant literature and highlight our contribution. The modeling framework is laid out in Section 3. We present the results for cases without and with anticipated regret in Sections 4 and 5, respectively. We consider several model extensions in Section 6 and Section EC.1 in the Supporting Information. Finally, Section 7 concludes our work and provides directions for future research.

RELATED LITERATURE

Our study lies at the confluence of four streams of prior research: product return policy, RSI, add‐on pricing, and anticipated regret. In this section, we provide an overview of these related works and highlight our contribution.

Our paper builds on prior theoretical literature on product returns. A main research question in this stream is about the optimal refund amount for product returns: full, partial, or none. The full‐refund policy is referred to as MBG and is assumed to signal the product quality. For example, Che (1996), McWilliams (2012), and Moorthy and Srinivasan (1995) compare MBG with the no‐refund policy in a monopoly or duopoly setting. More recently, Huang et al. (2018) discover that both retailers in a competitive market should adopt MBGs, but MBGs do not necessarily favor the low‐quality retailer. Huang and Huang (2021) examine MBGs in a distribution channel consisting of one manufacturer and two retailers with different qualities. Huang et al. (2021) study the pricing and product return policies when physical and online stores compete for consumers who can visit the physical store before buying online. They find that the online store should offer MBGs when the salvage advantage outweighs the total return hassle. Some researchers (e.g., Hsiao & Chen, 2012; Nageswaran et al., 2020; Su, 2009; Yalabik et al., 2005) show that MBGs are too generous to be optimal, and the partial‐refund policies are more beneficial for retailers. Su (2009) studies the impact of product return policies on supply chain performance. Another format of partial‐refund policy is implemented by charging a restocking fee (Shulman et al., 2009).

However, Shang et al. (2017) empirically discover that even the forward shipping fee decreases the value of the MBG return policy. Fruchter and Gerstner (1999) and Yalabik et al. (2005) find that offering a more generous return policy with free return shipping in addition to MBG can be optimal.

Our paper differs from previous literature in three main aspects. First, we are more interested in the impacts of reducing consumers' return shipping fees on a retailer's profit rather than designing the optimal refund amount for product returns. Our results add to prior work (e.g., Davis et al., 1998; Yalabik et al., 2005) by demonstrating how retailers can benefit from lowering the consumers' return shipping cost. Second, we introduce RSI, an innovative insurance‐based return management tool, to reduce the consumers' return shipping costs. We find that RSI further improves retail profitability for any product return policies currently in use. Third, we capture the interplay among the insurer, retailer, and consumers in our model and illustrate that offering RSI can be a “win‐win‐win” proposition for them. Thus, our main contribution to product returns literature is characterizing how RSI can complement an existing return policy to benefit the retailer as well as consumers further.

Relevant literature on RSI is quite limited, as it is a recent innovation. Our work is most closely related to Zhang et al. (2022). They analyze the informational role of RSI when product quality is the retailer's private information and show that RRSI can be an effective signal of high quality. However, in practice, both the RRSI and CRSI policies are widely adopted in the online market. Our interests differ from Zhang et al. (2022) in that we investigate RSI from the perspective of product fit uncertainty. Consumers are heterogeneous in terms of their information‐processing capabilities, and they may regret purchasing CRSI. Our results manifest that both the RRSI and CRSI policies may arise without quality uncertainty. In this regard, our work contributes to the prior research by theoretically supporting the viability of both RRSI and CRSI policies and providing practitioners with guidelines on adopting RSI. Recently, Chen et al. (2021) consider a manufacturer selling a product through a platform through agency selling or reselling format and investigate whether an RRSI strategy with an exogenously given premium should be offered. Apparently, the insurer plays an important role in a seller's decision to offer RSI in practice. Our work endogenizes the insurer's premium decision and characterizes the retailer's optimal RSI (RRSI or CRSI) policy. Li et al. (2021) attempt to investigate whether a retailer should charge RSI for a fee without modeling consumers' likelihood of product fit.

Our work is related to add‐on pricing literature as RRSI and CRSI are essentially bundling and unbundling strategies of the product and insurance, respectively. Allon et al. (2011) explore whether a service provider should bundle a main service and an ancillary service, and unveil two motivations for unbundling the services, that is, altering consumer behavior or segmenting consumers. Fruchter et al. (2011) study a seller's strategy to offer a free add‐on (i.e., bundling) or offer it for a fee (i.e., unbundling). They show that providing a free add‐on can be more profitable for sellers with monopoly power. Shugan et al. (2017) consider different add‐on bundling strategies with a product line, that is, a high‐ or low‐end base. They find that the bundling strategies depend on the quality differentiation between base goods. Differently, Moon and Shugan (2018) focus on the bundle‐framing effect and show that bundling can signal information about product popularity. Specifically, only sellers offering popular add‐ons are incentivized to bundle add‐ons with the main products. Recently, Cui et al. (2018) investigate the impact of the main service pricing, that is, uniform‐ or discriminatory‐pricing, on the optimal add‐on unbundling strategy. They find that a uniform‐pricing (discriminatory‐pricing) firm should unbundle the add‐on if there is a large (small) fraction of high‐type consumers who value the add‐on. In addition, several papers extend the research on add‐on pricing into competition settings (e.g., Ellison, 2005; Gabaix & Laibson, 2006; Geng & Shulman, 2015; Lin, 2017; Shulman & Geng, 2013; Wang et al., 2019). Whereas all these papers study whether firms bundle or unbundle add‐on, our paper studies add‐on pricing in a distribution channel. Specifically, when the add‐on RSI is unbundled (under CRSI policy), consumers purchase the RSI from the insurance company through the retailer's platform. Under the RRSI policy, the retailer purchases the RSI from the insurance company and sells the bundle of the RSI and the product. Moreover, we explore the effect of consumer‐anticipated regret behaviors on retailers' RSI provision decisions.

Last, our work is related to the abundant literature on consumer‐anticipated regret. Researchers in the operations management and marketing areas focus on the impact of the anticipated regret, including but not limited to, bid/auction (Engelbrecht‐Wiggans & Katok, 2008; Filiz‐Ozbay & Ozbay, 2007), product customization (Syam et al., 2008), advance selling (Diecidue et al., 2012; Nasiry & Popescu, 2012), product innovation (Jiang et al., 2017; Sarangee et al., 2013; Shih & Schau, 2011), product‐line design (Zou et al., 2020), and workers' relocation decisions in an on‐demand platform (Jiang et al., 2021). In particular, Jiang et al. (2017) show that anticipated regret has a nonmonotonic effect on firms' profits and the entrant's optimal quality; Zou et al. (2020) find that overpurchase regret hurts the firm but underpurchase regret can benefit the firm; and Jiang et al. (2021) show that regret‐averse workers are more likely to relocate to the supply‐shortage zone than rational workers. However, this does not necessarily benefit the firm. Also, Braun & Muermann (2004) utilize the concept of anticipated regret to explain consumers' desire for different kinds of insurance. Their model shows that regretful consumers adjust away from two extremes: full and no insurance. Inman & Zeelenberg (2002) also show that consumers may suffer from different levels of regret contingent on the cause of the regret. Recently, Li and Liu (2022) investigate the pricing policy of a regretful seller. They find that the seller sets a lower price as a result of the regret, but the pricing policy in terms of inventory and time is similar to those of unbiased sellers. Moreover, selling more goods may yield less revenue. Jin et al. (2022) explore how consumers' optimal search behavior is affected by the anticipated regret under a classic framework of sequential search. Their results show that the anticipated regret can intensify or soften price competition among firms.

Our paper investigates the impact of the consumers' anticipated regret on the RSI policy. Similar to the previous research, we use a linear structure to capture the anticipated regret in consumers' utility function and model two distinctive consumer regrets, namely, aversion to insured or uninsured regret. Our study enriches this research stream by identifying the salient effect of regret on RSI policies. Specifically, we explore the impact of regret when consumers are uncertain about the product fit. Moreover, we extend this research stream by incorporating the insurer's decision into the model, which has not been well addressed by prior literature.

MODEL

Consider a monopolistic online retailer selling a product at price p. Throughout this paper, we use pronouns “he” for the retailer and “she” for the generic consumer. Consumers have different information‐processing capabilities in inferring benefits from product attribute information due to different levels of expertise (Alba & Hutchinson, 1987). As in Jiang et al. (2017) and Sun and Gilbert (2019), we consider the following two consumer segments. A proportion θ of consumers know their true evaluation of the product at the time of purchase. We refer to these consumers as the informed consumers. Their willingness to pay for the product v is heterogeneous and uniformly distributed over [0, 1].8 The rest of the consumers (

The retailer adopts a full‐refund return policy but does not cover the return shipping fee for consumers (e.g., 6pm.com9), so consumers must pay a unit shipping fee s for returns.10 For every returned product, the retailer incurs a unit return handling cost h (including but not limited to repackaging the returned product to resell it).11 We also investigate the partial‐refund return policy by considering a restocking fee that consumers must pay to the retailer for product returns in the model extension (Section 6.1). Without loss of generality, we normalize the retailer's other operation costs, such as procurement cost, to zero and the market size to one.

The retailer decides on the product price p, as well as whether (1) to purchase the insurance at a premium

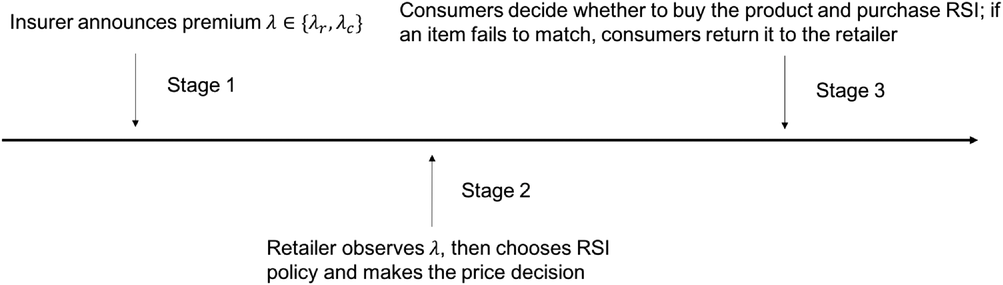

The three‐stage game sequence is shown in Figure 2. As pointed out by Zhang et al. (2022), the retailer and the uninformed consumers can observe the premiums before they make the RSI adoption decisions, so the insurer moves first to set the premiums, that is, the insurer announces premium

Game sequence.

NO ANTICIPATED REGRET

We investigate the case with no consumer‐anticipated regret in this section and will characterize the impact of consumer regret behaviors on the RSI policy in Section 5.

Benchmark: In the absence of RSI

With no RSI available, the informed consumers' utility is In the benchmark case without RSI, the retailer sells to both the informed and uninformed consumers and the equilibrium price and profit are

Next, we examine how RSI reduces the consumers' return shipping cost and benefits the retailer. Using backward induction, we first analyze the retailer's decision given an insurance premium in Section 4.2, and then characterize the insurer's optimal premium decision in Section 4.3.

Retailer's decision with given insurance premiums

In the presence of RSI,with a given premium

Suppose the retailer pays the premium

Under the CRSI policy, the informed consumers' utility is

The equilibrium prices Given the insurance premium If the RRSI premium is relatively low ( Otherwise, the retailer does not offer RRSI but adopts the CRSI policy only if the CRSI premium is relatively low ( The retailer always sets a higher product price under either RSI policy than in the benchmark case.

Under the RRSI policy, as the retailer purchases RSI from the insurer, consumers can benefit from the insurance for free; this insurance policy alleviates the uninformed consumers' concerns about product returns. Accordingly, the retailer would set a higher product price than under the benchmark case so as to transfer the insurance premium cost to consumers and extract the uninformed consumers' elevated surplus stemming from the insurance benefit. With a higher product price, informed consumers are less likely to buy the product. For the uninformed consumers, RRSI boosts their utility by

A comparison of the retailer's profit under RRSI, CRSI, and the benchmark indicates that the retailer should offer RRSI when

When the insurer sets a high RRSI premium (

Optimal insurance premiums

The insurer charges the premiums In equilibrium, if the retailer's return handling cost is relatively low ( otherwise, the insurer does not offer RSI.

As indicated in Lemma 2, under RRSI, the retailer sets a premium “bundle” product price to not only transfer the insurance cost to consumers but also absorb the uninformed consumers' increased surplus. With a higher product price, fewer informed consumers make a purchase, and AE is always in effect. The retailer employs volume‐driven and margin‐driven strategies for relatively small and high premiums set by the insurer, respectively. In the volume‐driven mode, the number of informed consumers leaving the market is less than the number of uninformed consumers entering the market. This happens only when the consumers' return shipping cost (s) is relatively high

If the return shipping cost (s) is relatively low (

Optimal return shipping insurance (RSI) policy without consumers' anticipated regret. Note:

Zhang et al. (2022) show that the RRSI policy is never optimal if consumers have no quality uncertainty regarding the product. However, in practice, RRSI is commonly used for goods like televisions and mobile phones. For these products, consumers can easily acquire product quality information by searching online. Unlike their work, we address the RSI policy from the perspective of product fit uncertainty, and we segment consumers according to their information‐processing capabilities: informed and uninformed. From this new angle, our results complement the literature by considering fit uncertainty and potentially explaining the prevalence of RRSI in e‐commerce markets.

Nevertheless, Proposition 1 shows that the insurer should never offer CRSI, which is inconsistent with real‐world practice. Resolving this inconsistency was the motivation for incorporating the consumers' anticipated regret behaviors in our analysis in Section 5.

ANALYSIS WITH ANTICIPATED REGRET

Now we explore the optimal RSI policy when consumers anticipate potential post–purchase regret about their RSI purchase decisions. Informed consumers will never experience regret ex‐post because they know their true valuation for the product before purchasing, and thus they never need to return products. In contrast, uninformed consumers are uncertain about the product fit and their need for RSI during purchasing. They will experience regret if they find that the forgone alternative would have been a better choice than their RSI purchase decision (Braun & Muermann, 2004). For instance, if an uninformed consumer purchases the product without buying RSI but later has to return the product due to misfit, she will regret not having bought the RSI, from which she would have derived a higher utility ex‐post; we refer to this as uninsured regret. Similarly, the consumer will experience regret for buying the product with RSI if she receives a product that fits well; we refer to this as insured regret. Note that consumers may experience regret after purchasing even though their product purchase decisions are optimal. Our survey shows that 80.00% of the respondents anticipate insured regret and 96.65% of the respondents anticipate uninsured regret. Therefore, the uninformed consumers' purchase decisions are based on their expected utility taking into account the disutility from the anticipated potential post–purchase regret regarding RSI (Zeelenberg et al., 1996).

To incorporate the anticipated regret in the consumer utility function, we use a linear regret term similar to the technique in Syam et al. (2008) and Jiang et al. (2017). Specifically, the disutility induced by regret aversion is proportional to the utility difference between the forgone and chosen alternatives (Inman et al., 1997). Therefore, the anticipated regret results in a disutility equal to

Using backward induction, we first analyze the retailer's decision given the insurance premiums in Section 5.1, and then characterize the insurer's optimal premium decision in Section 5.2. Based on the equilibrium analysis, we examine the impacts of consumers' regret behaviors on equilibrium outcomes and the impact of RSI policies on stakeholders in Sections 5.3 and 5.4, respectively.

Retailer's decision with given insurance premiums

With the anticipated regret, under CRSI, uninformed consumers will experience insured or uninsured regret ex‐post, if their RSI purchase decisions result in a lower utility than the forgone alternative. In particular, uninformed consumers derive a utility of

Specifically, if the CRSI has a relatively high premium, that is, Given the insurance premium If the RRSI premium is relatively low ( Otherwise, the retailer offers CRSI and sets the product price such that both H and L uninformed consumers purchase CRSI (Case 2) if the retailer offers CRSI and sets the product price such that only H uninformed consumers purchase CRSI (Case 1) if Compared with the benchmark case, the retailer always sets a higher product price under RRSI, but under CRSI, he sets a higher product price if and only if the CRSI has an extremely low premium, that is,

Under RRSI, the consumers' anticipated regret does not play a role in their purchasing decisions, and thus the insights are the same as in the case without regret (Lemma 2). The retailer should offer RRSI only when the premium is sufficiently low (

On the one hand, CRSI alleviates uninformed consumers' concerns about product misfits. On the other hand, consumers will need to pay for the insurance service and make cost–benefit trade‐off decisions. Interestingly, an extremely low premium (

Consequently, for an extremely small premium (

Optimal insurance premiums

Now we examine the insurer's optimal premium decisions ( In equilibrium, if the retailer's return handling cost is relatively low ( if H uninformed consumers are more sensitive to the uninsured regret than the insured regret ( otherwise, the insurer never offers RSI.

Optimal return shipping insurance (RSI) policy with consumers' anticipated regret. Note:

The anticipated regret does not impact the RRSI policy, so the intuitions and insights are consistent with those discussed for Proposition 1. Lemma 3 shows that, for given insurance premiums, offering CRSI benefits the retailer when the corresponding premium is extremely small (

In general, as the insured regret level

Proposition 2 reveals that the retailer should offer RRSI when the return handling cost is relatively low. In practice, major retailers on Taobao.com and JD.com pay less than small retailers to repackage returned products and resell them, that is, their return handling cost is lower. Recall that in the GAP example shown in Figure 1, the GAP flagship store can handle returns efficiently by selling the returned items through its widespread offline outlets in addition to its official flagship store on Taobao.com. Conversely, small sellers incur a higher cost to resell returned products. This potentially explains why major retailers tend to adopt RRSI, while small sellers prefer CRSI in online markets.

Zhang et al. (2022) show that the CRSI policy never arises in equilibrium, as the insurer never finds it is profitable to sell this insurance to consumers. However, the CRSI policy is indeed adopted by some retailers in practice, such as by some small stores on Taobao.com (see the GAP example in Figure 1b). By considering the consumers' regret behaviors in our model, we uncover that both RRSI and CRSI can arise in equilibrium. Our results potentially explain different RSI policies prevalent in the e‐commerce market.

It is worth noting that the positive AM effect of anticipated regret, which makes CRSI optimal, hinges on the market structure consisting of informed and uninformed customers and the assumption that the retailer cannot price discriminate between these two segments. With consumers' anticipated regret behavior, the retailer has to lower the selling price, which attracts more informed customers. In practice, if a retailer chooses to provide RSI (RRSI or CRSI), the RSI must be for all consumers, as shown in Figures A.4 and A.6 in the Supporting Information. Platforms may require sellers to offer MBG to all purchases. Only in such markets where retailers cannot separate out informed consumers can CRSI be an effective instrument to mitigate consumers' concerns about fit uncertainty.

From the theoretical perspective, our work complements the prior studies in product return and MBG. Retailers have long been offering generous return policies, but researchers still debate the optimality of MBGs (Abdulla et al., 2019). Huang et al. (2018) suggest that each firm should adopt MBGs regardless of any competitor's choice. Yet, consumers are still responsible for the return shipping fee, which is one salient factor in the consumers' purchasing decisions, especially for fashion industry goods such as apparel and beauty supplies. The survey conducted by Invesp indicates that 79% of consumers want free return shipping (Spillane, 2022), but this topic has been underexplored in the literature. We endeavor to fill this gap by examining the prevalent RSI policy. We unveil that RSI may improve the profitability of retailers who offer “MBG + RSI,” a more generous and profitable policy than MBG. As a matter of fact, in Section 6.1, we demonstrate that RSI is a profitable instrument for a partial refund return policy as well.

Our work also adds to the literature on consumers' anticipated regret. Many researchers have explored the role of anticipated regret in different contexts, such as competition between standard and customized products (Syam et al., 2008), advance selling (Nasiry & Popescu, 2012), product innovation (Jiang et al., 2017), product‐line design (Zou et al., 2020), on‐demand service platforms (Jiang et al., 2021), and sequential consumers search framework (Jin et al., 2022). In particular, Jiang et al. (2017) discover that consumers' strong switching regret differentiates the uninformed consumers more from the informed ones in a duopoly market. The alleviated price competition encourages the entrant to invest more in innovation and gain more because consumers with regret behavior are willing to pay more for innovative products. Zou et al. (2020) show that consumers' stronger underpurchase regret than overpurchase regret stimulates consumers to consider the high‐quality product. As a result, the firm can increase the quality gap in the product line when the underpurchase regret is strong.

Differently, our paper focuses on consumers' uncertain preference for product fit rather than quality and explores how consumers' anticipated regret affects their purchase of the product and RSI. We unveil that consumers' stronger uninsured regret than the insured regret avails the optimality of CRSI. In addition, the insurer's decision is incorporated into our framework. Interestingly, consumers' regret behavior can lead to a “win‐win‐win” outcome for the insurer, retailer, and consumers as shown in Proposition 4 in Section 5.4.

Moreover, we point out two distinctive types of consumer regret, that is, insured regret and uninsured regret, that play important roles in the RSI policy. In the absence of regret, when consumers' willingness to buy products with CRSI is low, the insurer cannot set a profitable premium that consumers accept. As a result, the CRSI policy is never viable, which cannot explain the practice of commonly used CRSI policies. In the presence of regret, consumers' high uninsured regret relative to the insured regret enhances their willingness to pay for CRSI, which assures the insurer's profitability and enables CRSI to appear in equilibrium.

From the practice perspective, Proposition 2 highlights the crucial role of the consumers' high uninsured regret level in the retailer's RSI policy adoption decision. This suggests that retailers and insurers may advertise a cheap insurance premium and make the potential loss from paying the return shipping cost prominent to increase the consumers' uninsured regret level in order to induce more consumers to purchase CRSI. Indeed, retailers on Taobao.com highlight the compensation amount and the relatively cheap insurance premium to evoke the consumers' uninsured regret (see the GAP example in Figure 1b). In our survey, among respondents who feel the uninsured regret is stronger than the insured regret, most (67.21%) state that the main reason is the cheap insurance premium and relatively high compensation.

Impact of the anticipated regret on equilibrium outcomes

We first investigate the impact of the anticipated regret on equilibrium outcomes. The consumers' anticipated regret impacts the equilibrium outcomes as follows: The CRSI policy is viable only if the consumers' insured regret is relatively small ( As consumers become more sensitive to the insured regret ( the insurer charges a lower premium, sells less CRSI, and profits less; the retailer charges a lower product price, attracts(repels) more (un)informed consumers, and profits more. As L uninformed consumers become more sensitive to the uninsured regret ( the insurer sets a higher premium if and only if the consumers' return shipping cost is relatively high ( the retailer charges a higher product price and thus repels (attracts) more (un)informed consumers if and only if both L uninformed consumer segment is small and consumers' return shipping cost is low (

Proposition 3 highlights the importance of the consumers' anticipated regret behaviors under CRSI. As shown in Proposition 1, in the absence of regret, the insurer cannot offer a profitable CRSI that consumers desire. Moreover, the uninsured regret stimulates the consumers' longing for CRSI, while the insured regret has the opposite effect. Therefore, CRSI is attractive to consumers only when some consumers are more sensitive to uninsured regret, that is,

One might conjecture that both the insurer and retailer would benefit from the consumers' increasing uninsured regret aversion sensitivity

As

As the insurance premium

Proposition 3 reflects that the retailer and insurer should manipulate the consumer propensity for uninsured regret in their favor. For example, they can advertise the drawbacks of not paying a small premium for a high compensation benefit in case of returns. The reinforced uninsured regret level stimulates the consumers' desire for the CRSI policy, which benefits the retailer, insurer, and possibly consumers, as shown in Proposition 4 in Section 5.4.

We next explore the magnitude of the insurer's and the retailer's benefits from adopting the optimal RSI and how the regret sensitivity impacts these benefits. We focus on the impact of regret aversion sensitivities

For illustration, we focus on Case 2, where both H and L consumers consider the product with RSI, so we choose parameters such that

Figure A.9 in the Supporting Information depicts how the average magnitude of the retailer's profit improvement changes with

Figure A.10 in the Supporting Information shows how

Impact of the RSI

The adoption of RSI policies at equilibrium certainly benefits both the retailer and the insurer. Proposition 4 examines whether consumers are better off as well. Consumers are worse off with RRSI, while CRSI leads to a “win‐win‐win” outcome for the retailer, insurer, and consumers when

Counterintuitively, although uninformed consumers can enjoy a reduced return shipping cost freely under the RRSI policy, the consumer surplus declines. To understand this, note that the retailer actually not only transfers the insurance premium to consumers but also extracts the uninformed consumers' elevated surplus stemming from the insurance benefit by charging a premium “bundle price” higher than the sum of the premium and product benchmark price. Correspondingly, some informed consumers switch to not purchasing when RRSI is introduced. In this case, RRSI actually hurts the consumer surplus. In contrast, consumer surplus may be better off with CRSI irrespective of the extra expense. This is because the retailer lowers the product price such that more informed consumers purchase the product without return. Uninformed consumers purchasing products only are also better off. Thus, CRSI could achieve a “win‐win‐win” goal for the insurer, retailer, and consumers (see Figure 5).

Customer–return shipping insurance (CRSI) (

Proposition 4 suggests that the insurer should pay more attention to CRSI, which can benefit not only itself but also the retailer and consumers although informed consumers will never be interested in it. Meanwhile, consumers should caution that “there is no such thing as a free lunch.” The retailer offering RRSI for free may actually transfer the premium cost to consumers by charging a higher product price. On the contrary, CRSI can be a more economical tool for consumers to mitigate their concerns about product fit uncertainty.

With the coronavirus pandemic spreading in early 2020, retailers' online year‐over‐year revenue growth is 129% in American and Canadian e‐commerce orders and 146% in all online retail orders as of April 21 (Columbus, 2020). Adopting RSI may provide an unprecedented opportunity for online retailers to improve profitability. Proposition 4 suggests that regulators such as the platform and government should consider promoting CRSI to benefit consumers, as well as the retailer and insurer.

DISCUSSION

Impact of a restocking fee

We have investigated RSI policies based on the retailer's full‐refund return policy. In practice, some retailers adopt partial‐refund policies, for example, by charging consumers a restocking fee. Also, some retailers use the full‐refund policy but set some restrictions for consumers, including strict time limits for returns, return of the original packaging materials, and acceptance of only those products that show no visible signs of use.18 We next extend our research by considering the retailer charging a restocking fee When the retailer charges a restocking fee

In the presence of a restocking fee r when returning an item, consumers have to pay r to the retailer in addition to the shipping fee s, and thus the consumers' return hassle cost increases from s to

Proposition 5 reveals that the results derived in the main model with the full‐refund policy are robust to changes in the retailer's return policy. Our findings shed light on the impact of RSI policies on market players and provide practitioners with valuable guidance on adopting insurance policies, showing how the optimal choices depend on the consumers' return shipping cost and the retailers' return handling cost.

Retailer offering RSI to consumers directly

If the retailer is allowed to offer RRSI directly (DRRSI), that is, not through the intermediate insurer, the retailer saves the purchasing cost of insurance premium In equilibrium, if the retailer's return handling cost is relatively low ( if H uninformed consumers are more sensitive to the uninsured regret than the insured regret ( otherwise, the insurer never offers DRRSI or CRSI.

Proposition 6 indicates that the main results shown in Proposition 2 qualitatively hold. The only difference is that the region offering DRRSI is enlarged because the retailer's cost of providing this insurance goes down.

Furthermore, we explore the case where the retailer can offer CRSI directly to consumers (DCRSI). Unfortunately, the analysis is analytically intractable; therefore, we resort to a numerical study. Under DCRSI, the retailer determines both the product price and insurance premium, which is equivalent to the case where the retailer is the central decision maker for both the insurance premium and product price. In the numerical study, we vary h from 0 to 0.35 and s from 0 to 0.25 with a step of 0.001, which generates 88,101 problem instances. Figure A.11b in the Supporting Information shows that our findings in the main model still qualitatively hold. The only difference is that both regions for DCRSI and DRRSI expand due to the retailer's centralized decision‐making.

Private information on retailer's return handling cost

In the main model, we have assumed that all the information is public. In practice, the retailer may want to keep his return handling cost h as a business secret and not want to share it with the insurer. In this section, we analyze the equilibrium in such a case. The insurer will make the premium decisions based on its expectation of h. Suppose that the insurer anticipates the return handling cost to be high ( As long as the insurer's anticipation on h does not deviate too much, that is, if the retailer's return handling cost is relatively low ( if H uninformed consumers are more sensitive to the uninsured regret than the insured regret ( otherwise, the insurer never offers RSI.

Proposition 7 shows that our main findings qualitatively hold. Generally, when the insurer expects a higher return handling cost, that is,

Beta distribution of product value

In this section, we examine whether our results hold under a different distribution. Beta distribution with parameters

With the indifference point

CONCLUSION

This paper develops a parsimonious model to investigate the optimal RSI policy for a monopolistic online retailer and an insurer considering the consumers' anticipated regret behaviors. We demonstrate that RSI can further improve a retailer's profitability, no matter whether a full‐refund or partial‐refund product return policy is employed. Interestingly, we first show that, when consumer regret behaviors are not considered, CRSI is never viable, but the retailer should offer RRSI if the return handling cost is relatively low and the consumers' return shipping cost is in an intermediate range. We then extend the model by incorporating the consumers' anticipated regret behaviors. By exploiting the consumers' high sensitivity to the uninsured regret, the retailer should offer CRSI if the return handling cost is relatively high and consumers' return shipping cost is intermediate. Counterintuitively, RRSI always leads to a lower consumer surplus, but CRSI can be a “win‐win‐win” proposition for the retailer, insurer, and consumers. Further, we uncover that the retailer has more incentive to adopt RRSI when consumers pay a restocking fee for product returns.

Theoretically, this work contributes to the literature on product return by revealing that retailers can raise their profit by offering RSI in addition to any product return policy. For example, retailers offering MBG can introduce a new return policy, “MBG + RSI,” to enhance profitability. Complementing prior studies on RSI, our work shows the viability of both RRSI and CRSI policies.

Our findings potentially explain the prevalent RRSI and CRSI policies offered by retailers on platforms such as JD.com and Taobao.com. Our results have important implications for practitioners. Major retailers tend to adopt RRSI because they can repackage and resell returned products more economically. In contrast, it is more costly for small sellers to handle returned products; therefore, CRSI may be the best policy for them. Our results also suggest that retailers and insurers can advertise a cheap insurance premium and expensive product return shipping cost to raise the consumers' uninsured regret level so as to induce more consumers to purchase CRSI. We should caution that the presence of the RSI policies may be a joint effect of multiple factors. For example, small retailers may want to use a lower price to attract more consumers, and/or they may be unable to pay the insurer a large amount of premium fee to use RRSI ahead of time.

It is worth noting that some membership services such as Amazon Prime19 and Best Buy Totaltech20 membership include a free product return benefit within certain days since purchase, which allows consumers to return products with a free return shipping fee and waiver of restocking fee in addition to other benefits. RSI is different from these membership programs in the following two aspects. First, RSI is only for a return shipping fee for one transaction. RRSI is freely provided to all consumers by the retailer and all consumers can purchase CRSI with a low premium compared to the product price. In contrast, membership programs like Amazon Prime provide a bundle of benefits including fast/free delivery, prime video, amazon music, and prime gaming over a year. The membership fee is relatively high (e.g., $119 for Amazon Prime annual membership). Consumers make a long‐term and complicated decision on whether to join the membership program. Second, the members' return‐related costs will be covered by retailers while the compensation under RSI is covered by a third‐party insurer. It will be interesting to explore whether a retailer should offer a membership program or RSI only in a future study.

Last, we point out some other interesting directions for future research. First, we investigate the optimal RSI policy using a one‐shot game. In a multiperiod game, one can extend our work and explore the impact of other types of consumer regret, for example, the regret caused by repeated purchasing or switching between buying or not buying insurance. Second, we consider a monopolistic retailer's RSI policy adoption decision. It will be interesting to extend the model to a setting with competing retailers on an online platform. Third, we investigate the optimal RSI policy for a given product return policy. A model based on endogenous return policy would generate rich insights on how retailers' return policies and RSI policy interplay. Fourth, one can extend our research by allowing consumers to buy insurance from an independent vendor. Fifth, our work provides a theoretical foundation for future empirical work. It will be worthwhile to collect data from online platforms to quantify the benefit of RSI through an empirical study.

Footnotes

ACKNOWLEDGMENTS

The authors are very grateful to the department editor, Tony Cui, the senior editor, and three anonymous reviewers for their constructive comments that resulted in a significantly improved paper. Yiming Li and Gang Li are partially supported by the Natural Science Foundation of China under Project 71832011 and the Science and Technology Innovation Team Plan of Shaanxi Province under Project 2020TD‐006. Yiming Li is also supported by “the Fundamental Research Funds for the Central Universities” (XJSJ23114). Xiajun Amy Pan is partially supported by Summer Research Grants awarded by the Warrington College of Business at University of Florida.

1

The survey is available online at

2

3

4

5

6

7

8

Alternatively, we use beta distribution in the model extension, which shows that the major results are robust.

9

10

The information on return shipping fee s is public for the retailer and insurer, as the shipping fee between any two destinations is publicly listed on the website of the delivery service company.

11

The retailer may keep the information on h as a business secret and not share it with the insurer. In the main model, we assume the insurer can expect the exact h value, a model of private h information is considered in the extension, which shows that the major results are robust.

12

According to the RRSI contract, the retailer cannot choose to provide RSI only for some consumers. Refer to Figures A.4 and A.6 in the Supporting Information.

13

14

We assume that consumers are not concerned about the product quality over time; therefore, we do not consider product warranty insurance, which is for long‐term benefit and more expensive than RSI offering one‐time benefit.

15

16

17

The CRSI policy is similar in Case 1 and Case 2. Hereinafter, we only use figures to illustrate CRSI policy under Case 2 for ease of exposition.

18

See the example of AFA stores at

19

20

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.