Product evaluation is an essential business process, and digital innovation has made it possible for companies to immediately process available information. We develop a model where a company continuously assesses information that follows a doubly stochastic Poisson process with a mean‐reverting and stochastic intensity. Accordingly, the company faces a two‐dimensional optimal stopping problem in which the company continues to evaluate the product if and only if the product reputation and information intensity remain in a continuation set. We employ a probabilistic approach to prove that the continuation set takes the form of an open interval for any fixed information arrival intensity. Given the complicated nature of the optimal solutions, we develop an asymptotic expansive solution, and numerical studies show that our solution performs well. We also analyze a heuristic solution where the company substitutes the dynamic intensity with a constant intensity. Interestingly, we find that this heuristic company does not necessarily benefit from having a higher product reputation.

Product evaluation is an important yet challenging task in business. For example, platforms such as Amazon.com, Taobao.com, and JD.com have used advanced data mining and analysis technology to monitor abundant information about products and continuously evaluate a product's reputation (or word‐of‐mouth). In fact, each piece of information (such as the author's background; the publisher and the contents of a book; and the color, dimension, compatibility, pixels, and water resistance of a digital camera) can either increase or decrease a company's expected valuation of the product, which renders the companies a better understanding of the product. However, information processing is costly so that companies have to stop evaluating at some point. In practice, platform companies might eventually promote reputable products by adding these products to a list, such as “Amazon's Choice,” “Best Goods in Taobao,” and “JD Best Sells,” or choose to remove products with a low reputation from the companies' platforms.

Certain information important to product evaluation can be obtained from product reviews generated by consumers who have purchased and used the product. The literature (Huang et al., 2020; Shen et al., 2015) empirically shows that, as measured by the review count, the rate at which information is passed on to companies fluctuates randomly over time because review information depends on exogenous factors, such as the enthusiasm that reviewers have for writing reviews and the operation of online platforms. More specifically, the information arrival rate exhibits unpredictable fluctuations, such as temporary dips or surges, so that the variance in the number of new reviews over a fixed period tends to dominate the mean; this characteristic, as a common feature for count data, is known as over‐dispersion. Accordingly, this literature suggests that the Poisson process with a random intensity is ideal for modeling the information arrival process.

Against this backdrop, we present a continuous‐time framework where a company continuously evaluates its product. The company updates the product reputation by considering each of the information pieces that can affect the reputation positively or negatively. As abundant information can be available, we approximate the product reputation by using a Brownian motion as information continues to arrive. Moreover, we model the information as a doubly stochastic Poisson process. Specifically, the information arrival intensity—referred to as information intensity—follows a time‐varying and stochastic Cox–Ingersoll–Ross (CIR) process (Cox et al., 1985). The CIR process is one of the first—and, perhaps, the most important and commonly used—diffusive models introduced to simulate intensity, the processes associated with which fluctuate over time, but with a tendency to return to the mean level (Brown & Dybvig, 1986; Pearson & Sun, 1994).

In our model, the company faces a two‐dimensional (product reputation and information intensity) optimal stopping problem. In this setting, the company benefits from having a higher product reputation—that is, the company's value function (i.e., the expected benefit of continuing evaluation minus the cost of continuing information processing) increases in the product's reputation. Moreover, central to this problem is the company's continuation set, which is crucial for establishing the optimal thresholds. However, identifying the geometric structure for our two‐dimensional optimal stopping problem is much more complicated than that for the one‐dimensional case. To address this complexity, we apply a probabilistic argument to demonstrate that the continuation set depends on information intensity and can take the form of an open interval (Proposition 1). The left boundary of the interval represents the abandonment threshold, that is, the valuation at which companies stop evaluating and abandon the product; on the other hand, the right boundary represents the promotion threshold, that is, the valuation at which companies stop evaluating and promote the product. This in turn underpins five key results.

First, when the information intensity is higher, the company's value function is higher (Lemma 2). That is, the company benefits from having more information. Second, when the mean‐reverting value of information intensity is higher, the continuation set is larger (Proposition 2(i)) because a higher mean‐reverting value implies that continuing to evaluate the product has more value. Third, the continuation set is also larger when the intensity increases at a slower speed (Proposition 2(ii)) because a slower increase in information intensity can steer companies to learn more in the long run, thereby resulting in a higher continuing value and, consequently, a larger continuation set. Fourth, we establish the condition where the continuation set will become larger with higher volatility in intensity (Proposition 3). Last, we develop a double‐layered asymptotic expansion with respect to information intensity (Proposition 4). A comparison of the value function and stopping thresholds calculated from Monte Carlo simulations with the asymptotic expansion solutions reveals the conditions where our asymptotic expansion solution performs well.

The CIR intensity significantly complicates our solution procedure, thereby motivating us to look for heuristics that can be easily solved. In practice, decision makers tend to rely on heuristics (such as information‐processing shortcuts or rules of thumb) when their decision‐making is computationally complex and information‐intensive (Tversky & Kahneman, 1974). According to the attribute substitution theory proposed by Kahneman and Frederick (2002), decision makers often unwittingly substitute a complicated problem for a more easily calculated one. Accordingly, we propose a behavioral model, in which a heuristic company applies heuristic thinking and behaves as if the information intensity is a constant rather than a dynamic process. We demonstrate that adopting this heuristic always leads to lower performance for the company, especially when the product reputation is moderate. Interestingly, we find that the heuristic company with a higher reputation is not destined for a higher profit.

LITERATURE REVIEW AND OUR CONTRIBUTION

There is a vast literature on optimal stopping problems in various forms and application contexts. Peskir and Shiryaev (2006) connect the optimal stopping problem in probability and free‐boundary problems. Oh and Özer (2016) characterize the optimal policy structure when a manager needs to determine when to stop a process and study the performance of a simple heuristic, namely, myopic policy. The optimal stopping problem has been applied in contexts such as job searching (Nishimura & Ozaki, 2004), contract design (Oh & Özer, 2013), capacity expansion (Bensoussan & Chevalier‐Roignant, 2019), supply chain management (Kadiyala et al., 2020), competitive investment (Sunar et al., 2021), and medical equipment management (Jain & Rayal, 2023).

The literature has also applied the optimal stopping problem in one key business context: product management. For example, Branco et al. (2012) analyze a product valuation diffusion model based on one‐dimensional Brownian motion by solving a one‐dimensional optimal stopping problem, where the search intensity for product attributes is one per unit time. Özer and Uncu (2013) study the new product introduction timing and subsequent production decisions faced by a component supplier and establish the optimality of a threshold policy. Following this policy, the supplier should optimally stop preparing for qualification and decide whether to enter the market if his or her order among qualified competitors exceeds a predetermined threshold. Sunar et al. (2019) study the optimal development and stopping of a product, where the technology of the product evolves as a controlled geometric Brownian motion (GBM) with the development strategy appearing in the drift term. This evolution results in a class of one‐dimensional optimal stopping problems coupled with a regular control (development policy). Lon and Zervos (2011) investigate a class of singular stochastic control problems with optimal stopping that are motivated by the so‐called goodwill problem. The evolution of the product's image is described as an Itô's diffusion process with a singular. The firm's objective is to maximize the utility of launching the product minus the associated “dis‐utility”. Relative to this literature, our work has one distinctive feature on product evaluation: the dynamic information arriving procedure. The arrival intensity is stochastic and time‐varying, thus resulting in a challenging two‐dimensional optimal stopping problem.

This work is particularly related to the literature on the two‐dimensional optimal stopping problem; this literature has explored contexts such as American options (Assing et al., 2014; Medvedev & Scaillet, 2010) and irreversible investment (De Angelis et al., 2017). This literature has established the one‐sided optimal boundary surface (De Angelis et al., 2017; Monge, 2014). We add to this literature by using a probabilistic argument to establish the two‐sided boundary surfaces. Accordingly, we make four key contributions. First, we establish that the company's continuation set is a connected open interval form for any fixed information intensity; this form is not always guaranteed for a two‐dimensional problem (Peskir, 2019). Compared to Özer and Uncu (2013), who establish the optimality of the one‐side threshold policy for the problem of whether to enter the market on new product introduction timing, our paper provides the two thresholds policy for abandoning or promoting the product. Second, using the probabilistic argument with the change of time, we characterize a series of structural properties of how the continuation set is impacted by information intensity, mean‐reverting level, reverting speed, and volatility, which adds to the product evaluation literature such as Sun (2012), Branco et al. (2012), Altug and Sahin (2019), who make decisions without considering information dynamics. Third, we propose a two‐layer asymptotic expansion approach that is computationally tractable and more general than the other approaches in the literature (Pichler et al., 2022). The latter numerically displays the distribution of the optimal stopping time, while our two‐layer asymptotic expansion approach provides a more explicit representation of stopping boundaries that extends its application by providing abandonment and promotion strategies in the field of operation management. Fourth, our paper is among the first to compare the heuristic and optimal stopping rules in the context of product evaluation. Interestingly, we find that improving the product reputation does not necessarily benefit a heuristic company, although improving the product reputation always benefits a sophisticated company. In particular, although the common wisdom is that the reputation is beneficial, there are empirical studies (Lee & Shin, 2014) showing that a company's positive product rating might have a negative effect on the company. We complement this literature by theoretically showing that the (heuristic) company may suffer from a higher product reputation.

THE MODEL

Consider a product whose information arrives over time. Let

be a complete probability space and

a reference filtration that satisfies the usual conditions. In this section, we first describe the product reputation model based on the dynamic information arrival and then establish a diffusion approximation to this product reputation model.

Product reputation. Product information can impact reputation (or word‐of‐mouth); the empirical literature (Huang et al., 2020; Shen et al., 2015) has shown that the information content is random and the product reputation (or valuation) often fluctuates over time. To formalize this, we assume that, at any time

, the product's reputation is

, where

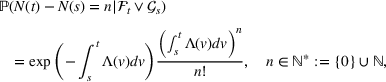

is the initial product reputation, which is known before information arrival. We follow the literature (Asea & Ncube, 1998; Banerjee & Breon‐Drish, 2022; Sannikov & Skrzypacz, 2010) to assume that the amount of information arrival,

, follows a doubly stochastic Poisson point process (DSPP), and the processes

are mutually independent. Here,

denotes the goodwill generated by information piece i, and

denotes a random variable sequence that represents the deviation from the initial reputation. Each information piece can positively or negatively affect product reputation; if the company ignores the ith information piece, then

. Without loss of generality, we assume that

is a random variable with mean zero and variance z2, where z denotes a positive scale constant measuring the product reputation deviation caused by the company receiving a piece of information. Taken together, for any

, the conditional expected reputation is

Information intensity. Recall that the information arrival process

follows a DSPP. We introduce an

‐adapted stochastic intensity

, thereby implying that, for any

,

where the sigma‐algebra

for all

. Multiplying both sides of (2) by n and summing up all

, we obtain

for any

. Accordingly,

measures the information intensity—the expected number of information arrivals per time unit—at time t:

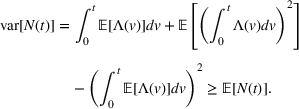

One might assume that the intensity process of information arrival is a deterministic but time‐varying function. This assumption implies that the variance and the mean of the arrival counts in a given period are equal; this implication may contradict the empirical observation (Shen et al., 2015). In fact, for DSPP

with stochastic arrival intensity

, we have from (2) and Jensen's inequality that, for any

, the mean satisfies

and the variance satisfies

This equation reflects an overdispersed characteristic for the DSPP arrival (Ata & Peng, 2020; Kingman, 1992). Throughout this paper, the intensity

follows the following CIR process:

where

and

are constants and

denotes a standard Brownian motion; parameter α characterizes the long‐term mean of information intensity and parameter β characterizes the adjustment speed of

toward the long‐term mean. The information intensity is expected to move up whenever its realization is below the long‐term mean and expected to move down whenever above the long‐term mean. This is to capture the temporary waves in information arrivals. The adjustment speed increases with parameter β. The variance of the information intensity process is

, which is proportional to the level of intensity. To guarantee a positive information intensity, we also require the so‐called Feller condition

Model (4) has been widely adopted in finance and economics to model the mean‐reversion and stochastic oscillation of financial state variables (see, e.g., Brown & Dybvig, 1986; Pearson & Sun, 1994) and has been adopted recently in operations (Ata & Peng, 2020; Sun & Liu, 2021). This model is a natural candidate for modeling the intensity of a counting process with unpredictable and temporary fluctuations. This model is ideal because the CIR process never becomes negative under a mild condition and periodically spikes but has a tendency to return to its mean level. Moreover, this process is amenable to statistical inference—the generalized method of moments (GMM) can be easily implemented.

Diffusion approximation. To simplify the company's problem, we consider the case where there are many pieces of information. In the online review example, there are many reviews and each of them can consist of many small pieces of information regarding the product features and specifications. As the number of information pieces reaches infinity, we have a continuous‐information analog of the discrete‐information model. Alternatively, one can think of an information piece of a product as a quantum of valuable information within an infinitesimal period. Recall that the information arrival process

follows a DSPP at an

‐adapted stochastic intensity

described in (4). Consequently, we can obtain the following diffusion approximating valuation process (see the Appendix for details):

where

is a standard Brownian motion. In view of (4) and (5), the reference filtration

is the natural filtration generated by

with a right‐continuous augmentation by null sets (see Karatzas & Shreve, 1998, Chapter 2, Definition 7.2). This approximation involves a Brownian motion, thereby simplifying the solution procedure of our problem. For a similar approximation, see Bolton and Harris (1999), Jiang and Jain (2012), Branco et al. (2012), and Kumar et al. (2020). For the sake of generality, we allow the correlation between

and

, such that

, where

denotes the correlation coefficient. A special case would be if B and W are independent, such that

. In our product evaluation model, for simplicity and tractability, we assume that the product reputation value is observable and measured by the company with digital technology; however, this value is not necessarily observed by consumers. Consequently, a higher product reputation cannot directly imply a higher interest from consumers, or a higher information intensity.

THE OPTIMAL STOPPING RULE

Building upon the company's product evaluation model (5) with the information intensity process (4) in Section 3, this section focuses on the characterization of the company's optimal decision by studying a two‐dimensional optimal stopping problem.

Structural results

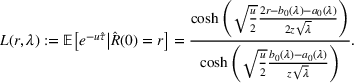

To determine the company's optimal decision, we examine the value function

of an optimal stopping problem—that is, the expected benefit of the future evaluations minus the cost of the continuous evaluation: for

,

Here,

is the cost of information processing in unit time,

is the discount rate representing the company's patience,

is a utility function representing the company's evaluation for the product, and

is the set of stopping times with respect to the market information. In addition, the conditional expectation operator is

, for a given company's initial valuation

and information intensity

.

For

, we associate the value function

with the following variational inequality (Friedman, 1982, Theorems I.3.2 and I.3.4):

Here,

is the infinitesimal generator of the Markov process

:

where

(respectively,

) denotes the first‐order (respectively, second‐order) partial derivative operator with respect to variable r, and a similar definition applies to the notations

,

, and

.

For any

, the value function

satisfies

for all

with

;

is convex in

;

is continuous on D.

Lemma 1 verifies that the company's value function

is increasing in the product reputation r and that

is decreasing for each

. Moreover, Lemma 1 shows that the company's value function is continuous in product reputation. Consequently, the company gradually benefits from an increasing product reputation when the company applies an optimal solution. However, this benefit is not absolute for the company adopting a heuristic solution in Section 5.

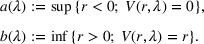

Lemma 1 helps establish the optimal boundaries of our optimal stopping problem. According to the optimal stopping theory (see Peskir & Shiryaev, 2006, Chapter VII), the company stops at

where the set

In other words, the company continues to evaluate the product if and only if the valuation and information intensity remain in

—that is, the continuation set. Correspondingly, for

, the λ‐section of the continuation set is

The stopping time

given by (9) is optimal for problem (6). Moreover, the continuation set in (10) has the following representation:

For

, the optimal boundaries are

In particular, if

, then

(in this case,

); if

, then

and

.

Proposition 1 indicates that our optimal stopping problem (6) boils down to determining the threshold

and threshold

. On the one hand, the company stops evaluating when it is indifferent between continuing the evaluation process and stopping the evaluation to recommend the product—that is,

. Thus, we refer to

as the promotion boundary. On the other hand, the company stops processing information and abandons the product when the agent does not expect any positive utility from having the product—that is,

. Thus, we refer to

as the abandonment boundary. Consequently, the company keeps learning about the product when r is moderate—that is,

—but stops evaluating when r is either sufficiently high or sufficiently low. When r is sufficiently high, the likelihood of r returning to zero is low. Even if r returns to zero, the company would have to pay substantial processing costs before seeing it happen. Therefore, when r first hits

, the company recommends the product right away. Rather, when r is near

, the expected valuation is far below zero and is unlikely to return above zero again. Rather than paying more information processing cost for the low probability event, the company terminates the evaluating process and abandons the product.

Proposition 1 implies that if the information processing cost is zero (

), the company should never abandon the product—that is,

—because the value function

for any

. In addition, if

—that is, the company currently has zero valuation for recommending the product and expects zero utility under optimal decision‐making—then, the company should not learn. The company would initiate information processing, in the hope of eventually making a recommendation only if the company's valuation r is between the thresholds

and

. Even if

, the company can expect a positive utility from the possibility of recommending the product—that is,

; then, the company would learn the product in the hopes of a good evaluation.

Below, we study the impact of information intensity λ on the value function

and stopping boundaries

and

.

For any

,

is increasing on

.

The abandonment threshold

is decreasing on

, while the promotion threshold

is increasing on

. Moreover,

is left‐continuous on

, while

is right‐continuous on

.

Lemma 2(i) indicates that the company's value function depends on the information intensity λ: a higher information intensity causes a larger value function for companies, thereby implying that a company benefits from more information associated with a higher information intensity. Moreover, Lemma 2(ii) indicates that the stopping rule also depends on the information intensity. In particular, as the information intensity increases, the company's promotion threshold

increases, and the company's abandonment threshold

decreases. Thus, a higher information intensity inhibits the company from stopping its evaluation.

We now investigate the impacts of the mean‐reverting parameter α and reverting speed parameter β on the company's value function and stopping rule. We use

and

to denote the value function and stopping boundaries, respectively, to highlight their dependence on

.

Given

:

Suppose

. Then,

. Accordingly,

and

.

Suppose

and

. Then,

;

. Accordingly,

and

.

Proposition 2(i) indicates that a greater mean‐reverting level α implies a higher information intensity, thereby benefiting the company (Lemma 2(i)). Moreover, a higher mean‐reverting level drives the company to learn more, thereby creating a larger continuing evaluation value. Consequently, the promotion threshold increases and the abandonment threshold decreases with respect to α. In a similar vein, Proposition 2(ii) indicates that a slower (respectively, faster) reverting speed β along with a higher (respectively, lower)

implies a higher (respectively, lower) promotion threshold and a lower (respectively, higher) abandonment threshold. Intuitively speaking, this indication implies that a slower increase (respectively, faster decrease) in the information intensity can steer (respectively, stifle) companies to process more information in the long run, thereby resulting in a larger (respectively, smaller) continuation set.

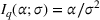

We now explore how the company's evaluating behavior depends on the stochasticity of information intensity. To do this, we introduce the (squared) contrast‐to‐noise ratio of the information intensity as

for any intensity level λ. Harrison and Sunar (2015) use a similar ratio to measure the information quality or the signal quality: the higher the ratio is, the higher the information quality is. When the intensity process is deterministic (

), we set this ratio to

. Note that

when the intensity level equals the mean‐reverting level (

).

Let

for

satisfy

,

,

, and

. Then, for any

,

. Therefore, the abandonment and promotion thresholds satisfy that

and

.

Proposition 3 indicates that the impact of parameter σ on the company's decision depends on the contrast‐to‐noise ratio. This characterization requires that the contrast‐to‐noise ratios become larger—that is,

and

—as the intensity becomes more stochastic in that

. Then, a more stochastic intensity (together with a higher contrast‐to‐noise ratio) implies a higher promotion threshold and a lower abandonment threshold.

Solution procedure and insight

Given the stopping boundaries established in Proposition 1, we reformulate the original optimal stopping problem as a free‐boundary problem (Peskir & Shiryaev, 2006, Chapter III):

Condition (15) is related to a continuous pasting condition, which can be obtained from (13) in Proposition 1. The left‐hand sides are the utilities a company expects if it continues processing information, while the right‐hand sides are the expected utilities a company can obtain right away by abandoning or promoting the product. The continuous pasting condition can be considered as a zero‐order condition. Condition (16) is related to a smooth fit condition that holds by applying the argument in Example 12 of De Angelis and Peskir (2020). This condition implies that the value function is differentiable across both the optimal abandonment boundary

and the optimal promotion boundary

. Compared with the continuous pasting condition, this may be viewed as a first‐order condition.

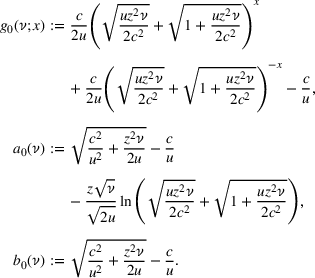

The two‐dimensional free‐boundary problem in (14)–(16) is difficult to solve. For efficient computation, we develop an asymptotic expansion technique. To this end, for

and

, we introduce the following benchmark functions:

The benchmark function

is in essence the closed‐form solution of the free‐boundary problem (14)–(16), which corresponds to the (one‐dimensional) optimal stopping problem (6) when the information intensity model parameter

. Our asymptotic expansive solution will converge to the closed‐form solution of the one‐dimensional free‐boundary problem when the intensity is constant with

. This closed‐form solution is used as a heuristic in Section 5.

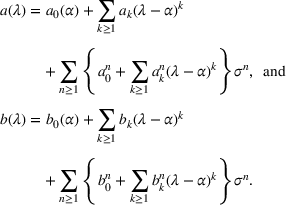

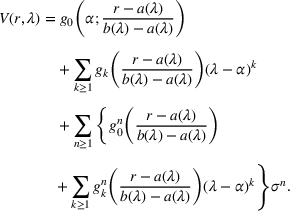

The optimal boundaries and the value function of the company's optimal evaluating problem characterized by (14)–(16) admit the following asymptotic expansions.

are defined in (EC.2) of the Supporting Information. The coefficients

and

for

are given by (EC.3) and (EC.4), respectively, of the Supporting Information.

The extant literature has also exploited the idea of substituting the optimal stopping rule with a suboptimal rule for which an approximate solution is easy to find and fast to compute. For example, Medvedev and Scaillet (2010) develop a one‐layer asymptotic expansion to solve a diffusion model for the American option price. Proposition 4 proposes a two‐layer asymptotic expansion, where the coefficients

, and

are independent of parameter σ.

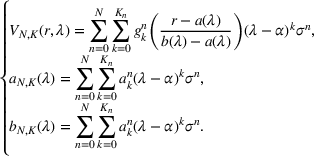

To calculate our expansion solutions in Proposition 4, we apply the following truncation:

We compare these truncated solutions with the solutions from a Monte Carlo simulation. In the simulation, we first generate 104 sample paths of

, defined in (4)–(5). Then, we generate the dynamic programming recursion as in Peskir and Shiryaev (2006) and Oh and Özer (2016) to calculate the optimal pair

and maximize the company objective in (6).1 We follow the literature (Medvedev & Scaillet, 2010) to set the mean absolute difference between our truncated solution and the Monte Carlo simulation solution at a magnitude of 10−3. As per Table 1, we achieve this target difference for low values of N and K at

and

with the mean absolute differences of

given as (0.0056,0.0078,0.0098). This result implies that our asymptotic expansion solution performs effectively and efficiently.

The mean absolute differences (on the value function V and optimal boundaries a and b) between the asymptotic expansion and the Monte Carlo simulation.

V

0.0515

0.0102

0.0068

0.0049

a

0.3130

0.0568

0.0513

0.0483

b

0.1817

0.0358

0.0168

0.0117

V

0.0513

0.0511

0.0509

0.0508

a

0.3287

0.3212

0.3199

0.3038

b

0.1784

0.1780

0.1770

0.1741

V

0.0105

0.0104

0.0102

0.0099

a

0.0348

0.0298

0.0285

0.0281

b

0.0254

0.0251

0.0244

0.0217

V

0.0060

0.0058

0.0056

0.0054

a

0.0144

0.0083

0.0078

0.0074

b

0.0107

0.0105

0.0098

0.0071

V

0.0050

0.0048

0.0046

0.0043

a

0.0082

0.0048

0.0044

0.0038

b

0.0059

0.0057

0.0049

0.0040

Note: The parameters are

,

,

,

,

,

,

, and

.

Using the asymptotic expansion solution above, we derive the so‐called abandonment probability for the product—that is, the probability that the company stops the evaluation and abandons the product. For

, the abandonment probability is

Define

and

. Then,

. Correspondingly, the promotion probability is

.

For any initial information intensity

, the abandonment probability

defined by (18) is decreasing in the product's reputation

. Accordingly, the promotion probability

is increasing in the product's reputation

.

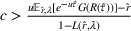

We formulate the abandon probability

for

in the form of the following likelihood equation (see, e.g., Karlin & Taylor, 1981, pp. 192–196):

We now derive insights regarding the abandon probability. As per the left panel of Figure 1, the company's abandon probability can either increase or decrease in information intensity λ, depending on the product's reputation. If product reputation r is less (respectively, greater) than threshold value r0, then the abandon probability decreases (respectively, increases) with the information intensity. This finding implies that when the product reputation is close to the abandonment (respectively, promotion) threshold, a larger information intensity stifles (respectively, excites) the company from abandoning the product because a higher information intensity decreases the abandonment threshold and increases the promotion threshold (Lemma 2). In a similar vein, under mild conditions, a higher intensity mean, a lower reverting speed, or a larger volatility also decreases the abandonment threshold and increases the promotion threshold (Propositions 2 and 3). Consequently, when the product reputation is close to the abandonment (respectively, promotion) threshold, a larger α, a smaller β, or a larger σ stifles (respectively, excites) the company to abandon the product; see Figure 1 for an illustration. In the top right panel,

is fixed, and in the bottom right panel, the contrast‐to‐noise ratios become larger as σ becomes larger.

The sensitivity of abandon probability to the product reputation. The parameters are

,

,

,

,

, and

. Moreover,

,

in the top left panel;

,

in the top right panel;

,

,

in the bottom left panel; and

,

,

in the bottom right panel.

THE HEURISTIC STOPPING RULE

The complex solution procedures in Section 4 motivate us to study a simpler heuristic. In practice, “people rely on a limited number of heuristic principles which reduce the complex tasks of assessing probabilities and predicting values to simpler judgmental operations. In general, these heuristics are quite useful, but sometimes they lead to severe and systematic errors” (Tversky & Kahneman, 1974, p. 1124). Moreover, Kahneman and Frederick (2002) propose a process called attribute substitution, where the decision maker assesses a specified target attribute of a judgment object by substituting another property of that object (the heuristic attribute). This is also consistent with our idea of developing asymptotic expansions in Subsection 4.2.

We thus develop a heuristic thinking approach in that the company substitutes the main complex attribute in the model—that is, CIR information intensity—by a constant value (i.e.,

so that

). That is, the company behaves as if solving

where

is the valuation process with constant intensity, that is,

Here, λ takes the value of the initial information intensity. Essentially, the company behaves as if it is solving Equations (21)–(22) for a heuristic solution, rather than solving Equations (5) and (6). We call the company applying the optimal stopping rules derived from (5) and (6) the sophisticated company.

The heuristic stopping boundaries solved from (21)–(22) can be characterized by

and

in (17). These heuristic boundaries are much simpler than the optimal boundaries

and

. Similar boundaries have been explored in the literature; for example, the solutions of the one‐dimensional free‐boundary equation in Branco et al. (2012) can be expressed as

That is, although the heuristic company solves (21) to obtain the stopping rule, the resulting value function is based on the underlying information dynamics.

Given (23), we first evaluate the company's loss caused by using the heuristic:

always holds meaning that the company always suffers from using heuristics. Moreover,

when the product reputation is relatively low

or high

. Intuitively, under these conditions, both the sophisticated company and the heuristic company reach the exit threshold and abandon or promote the product; please see the right panel of Figure 2 for the sophisticated company's value function

and the associated stopping boundaries

and

. Rather, when the product reputation is moderate (

), the loss due to the heuristic thinking is positive. More interestingly,

jumps at

but drops at

. The finding implies that with a slight increase in product reputation, the loss due to the heuristic thinking can significantly increase or decrease. Intuitively speaking, when the product reputation is such that

or

, the heuristic company continues evaluating the product, although the optimal strategy is to stop the evaluation. Rather, the heuristic company's decision is optimal when

and

. Consequently, when the reputation changes from the region

to the region

—or from the region

to the region

—the change helps correct the company's decision, thereby significantly reducing the company's loss due to heuristic thinking. Moreover, calculated by

, the low reputation around

results in up to more than twice the utility loss of the heuristic company; however, the higher reputation can reduce such a loss rate. This observation also motivates us to check the characteristic of the value function

.

Let

. Then, the Laplace transform of

is given by

Moreover, we have

if

for some

, then

is not decreasing in r when

;

if

for some

, then

is not increasing in r when

.

The loss

due to heuristic thinking, and the sophisticated company's value function

. The parameters are

,

,

,

,

,

,

,

,

, and

.

As per Proposition 5(i), when the product reputation r is close to the heuristic promotion boundary

,

can increase rather than decrease in r; this result is in contrast to Lemma 1(i), where

is constantly decreasing in r. For insights, when the heuristic company is about to recommend a product (i.e., the product reputation is around

), a better product reputation can increase the benefit of continuing evaluation. Thus, in addition to the traditional view that product reputation is a company's fortune, we uncover a new characteristic of product reputation: a higher reputation might inspire the heuristic company continuing evaluation, thereby increasing the loss due to the nonoptimal decision. Proposition 5(ii) indicates that a higher reputation can also potentially decrease the heuristic company's benefit of continuing evaluation, especially when r is close to the heuristic abandonment boundary

. Specifically, the heuristic company may suffer from a higher product reputation because the continuing evaluation benefit is negative when

(i.e.,

). Then, when the heuristic company is about to abandon a product, a lower product reputation can drive the company to stop evaluating, thereby reducing the company's loss.

CONCLUDING REMARKS

This paper studies a setting where a company evaluates a product according to dynamic information. The company balances its expected benefit and the associated cost in a process of information, and accordingly solves a two‐dimensional optimal stopping problem. Solving this problem essentially involves determining a connected and open interval whose left boundary represents the abandonment threshold and whose right boundary represents the promotion threshold. To compute these thresholds, we develop an asymptotic expansive solution. The computational complexity is due mainly to the complicated nature of the information arrival intensity. If the company chooses to implement a heuristic solution by ignoring the dynamic nature of information intensity, the company suffers from heuristic thinking. Interestingly, this company might even suffer from a higher product reputation (Proposition 5), although the company never does so when it employs an optimal stopping strategy. This echoes the empirical studies (Lee & Shin, 2014) showing that a company's positive product rating might have a negative effect on the company.

Our work generates the following managerial implications at the dynamic information arrival level, while most prior studies have focused on product management at the static information arrival level (e.g., Branco et al., 2012; Özer & Uncu, 2013; Sunar et al., 2019). First, for a company deciding to promote (or abandon) products, our study suggests that the company should factor in the information arrival process. When the information arrival becomes more intense, the company should check more for promotion (or abandonment). Second, for a seller thinking to disclose information to the platform, our results indicate that the seller should consider the position of the platform. If the platform is about to abandon the product, then the information disclosure decreases the abandonment threshold. However, providing information to a platform close to recommending the product may backfire. Third, for a company initiating a process to improve the product reputation, our study suggests that the platform should consider the company's sophistication level. Specifically, improving the product reputation does not necessarily benefit a heuristic company, although improving the product reputation always benefits a sophisticated company.

Footnotes

JUSTIFICATIONS AND PROOFS

ACKNOWLEDGMENTS

We thank the Department Editor, Senior Editor, and two anonymous referees for their constructive and helpful feedback. We thank the core algorithm team in Alibaba and the supply chain team in Amazon for providing us with numerous valuable suggestions and comments. One of the authors of this paper , Lijun Bo, is partially supported by Natural Science Basic Research Program of Shaanxi (No. 2023‐JC‐JQ‐05), National Natural Science Foundation of China (No. 11971368), and the Fundamental Research Funds for the Central Universities (No. 20199235177).

1

We investigate a special case with a constant information intensity, where we can derive closed‐form formulations for the value function and thresholds. In this special case, we find that the absolute error of our Monte Carlo simulation is negligible, thereby justifying our specification on the simulation paths.

ORCID

Meng Li

References

1.

AltugM. S.SahinO. (2019). Impact of parallel imports on pricing and product launch decisions in pharmaceutical industry. Production and Operations Management, 28(2), 258–275.

2.

AseaP. K.NcubeM. (1998). Heterogeneous information arrival and option pricing. Journal of Econometrics, 83(1–2), 291–323.

3.

AssingS.JackaS.OcejoA. (2014). Monotonicity of the value function for a two‐dimensional optimal stopping problem. The Annals of Applied Probability, 24(4), 1554–1584.

4.

AtaB.PengX. (2020). An optimal callback policy for general arrival processes: A pathwise analysis. Operations Research, 68(2), 327–347.

5.

BanerjeeS.Breon‐DrishB. (2022). Dynamics of research and strategic trading. The Review of Financial Studies, 35(2), 908–961.

BrancoF.SunM.Villas‐BoasJ. M. (2012). Optimal search for product information. Management Science, 58(11), 2037–2056.

9.

BrownS. J.DybvigP. H. (1986). The empirical implications of the Cox, Ingersoll, Ross theory of the term structure of interest rates. The Journal of Finance, 41(3), 617–630.

10.

CoxJ. C.IngersollJ. E.RossS. A. (1985). A theory of the term structure of interest rates. Econometrica, 53(2), 385–408.

11.

De AngelisT.PeskirG. (2020). Global C1 regularity of the value function in optimal stopping problems. The Annals of Applied Probability, 30(3), 1007–1031.

12.

De AngelisT.FedericoS.FerrariG. (2017). Optimal boundary surface for irreversible investment with stochastic costs. Mathematics of Operations Research, 42(4), 1135–1161.

13.

FellerW. (1951). Two singular diffusion problems. Annals of Mathematics, 54(1), 173–182.

14.

FriedmanA. (1982). Variational principles and free boundary problems. John Wiley & Sons.

15.

HarrisonJ. M.SunarN. (2015). Investment timing with incomplete information and multiple means of learning. Operations Research, 63(2), 442–457.

16.

HuangH.SunarN.SwaminathanJ. M.RahulR. (2020). Do noisy customer reviews discourage platform sellers? Empirical analysis of an online solar marketplace. Working paper, University of North Carolina at Chapel Hill, North Carolina.

17.

IkedaN.WatanabeS. (1981). Stochastic differential equations and diffusion processes. North Holland.

18.

JainA.RayalS. (2023). Managing medical equipment capacity with early spread of infection in a region. Production and Operations Management, 32(5), 1415–1432.

19.

JiangZ.JainD. C. (2012). A generalized Norton–Bass model for multigeneration diffusion. Management Science, 58(10), 1887–1897.

20.

KadiyalaB.ÖzerÖ.BensoussanA. (2020). A mechanism design approach to vendor managed inventory. Management Science, 66(6), 2628–2652.

21.

KahnemanD.FrederickS. (2002). Representativeness revisited: Attribute substitution in intuitive judgment. Heuristics and Biases: The Psychology of Intuitive Judgment, 49, 81.

22.

KaratzasI.ShreveS. E. (1998). Brownian motion and stochastic calculus. Springer.

23.

KarlinS.TaylorH. E. (1981). A second course in stochastic processes. Elsevier.

24.

KingmanJ. F. C. (1992). Poisson processes (Vol. 3). Clarendon Press.

25.

KumarS.TanY.WeiL. (2020). When to play your advertisement? Optimal insertion policy of behavioral advertisement. Information Systems Research, 31(2), 589–606.

26.

LeeE.‐J.ShinS. Y. (2014). When do consumers buy online product reviews? Effects of review quality, product type, and reviewer's photo. Computers in Human Behavior, 31, 356–366.

27.

LonP. C.ZervosM. (2011). A model for optimally advertising and launching a product. Mathematics of Operations Research, 36(2), 363–376.

28.

MedvedevA.ScailletO. (2010). Pricing American options under stochastic volatility and stochastic interest rates. Journal of Financial Economics, 98(1), 145–159.

29.

MongeA. O. (2014). Time‐change and control of stochastic volatility (Ph.D. thesis, University of Warwick, UK).

30.

NishimuraK. G.OzakiH. (2004). Search and Knightian uncertainty. Journal of Economic Theory, 119(2), 299–333.

31.

OhS.ÖzerÖ. (2013). Mechanism design for capacity planning under dynamic evolutions of asymmetric demand forecasts. Management Science, 59(4), 987–1007.

32.

OhS.ÖzerÖ. (2016). Characterizing the structure of optimal stopping policies. Production and Operations Management, 25(11), 1820–1838.

33.

ÖzerÖ.UncuO. (2013). Competing on time: An integrated framework to optimize dynamic time‐to‐market and production decisions. Production and Operations Management, 22(3), 473–488.

34.

PearsonN. D.SunT.‐S. (1994). Exploiting the conditional density in estimating the term structure: An application to the Cox, Ingersoll, and Ross model. The Journal of Finance, 49(4), 1279–1304.

35.

PeskirG. (2019). Continuity of the optimal stopping boundary for two‐dimensional diffusions. The Annals of Applied Probability, 29(1), 505–530.

36.

PeskirG.ShiryaevA. N. (2006). Optimal stopping and free‐boundary problems. Birkhäuser.

37.

PichlerA.LiuR. P.ShapiroA. (2022). Risk‐averse stochastic programming: Time consistency and optimal stopping. Operations Research, 70(4), 2439–2455.

38.

RevuzD.YorM. (2013). Continuous Martingales and Brownian motion. Springer.

39.

SannikovY.SkrzypaczA. (2010). The role of information in repeated games with frequent actions. Econometrica, 78(3), 847–882.

40.

ShenW.HuY. J.UlmerJ. R. (2015). Competing for attention: An empirical study of online reviewers' strategic behavior. MIS Quarterly, 39(3), 683–696.

41.

SunM. (2012). How does the variance of product ratings matter?Management Science, 58(4), 696–707.

42.

SunX.LiuY. (2021). Staffing many‐server queues with autoregressive inputs. Naval Research Logistics, 68(3), 312–326.

43.

SunarN.BirgeJ. R.VitavasiriS. (2019). Optimal dynamic product development and launch for a network of customers. Operations Research, 67(3), 770–790.

44.

SunarN.YuS.KulkarniV. G. (2021). Competitive investment with bayesian learning: Choice of business size and timing. Operations Research, 69(5), 1430–1449.

45.

TverskyA.KahnemanD. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124–1131.

46.

WhittW. (2002). Stochastic‐process limits: An introduction to stochastic‐process limits and their application to queues. Spinger.