Abstract

Corporate social responsibility (CSR) empirical scholarship overwhelmingly relies on a few archival datasets to examine firms’ action: strengths, concerns, and controversies. Yet persistently overlooked are salient issues with no current corporate action, represented by zeroes. These zeroes, in Morgan Stanley Capital International/Kinder, Lydenberg, Domini (MSCI/KLD) data, are not missing data. Rather, zeroes signify a lack of observable action on salient issues (which we term, inaction). Persistently ignoring zeroes, we argue, distorts empirical findings and masks corporate inaction. When aggregated across companies, overlooked zeroes can legitimize firms’ failure to address salient social or environmental issues. We discuss the importance of scrutinizing zeroes, explain how scholars inadvertently ignore them, explore implications, and provide alternative modeling choices. Our goal is to highlight conceptual and methodological blind spots that may meaningfully affect environmental, social and governance (ESG) research. We conclude by exploring how theoretical attention to these potentially information-rich zeroes can illuminate corporate behavior, including inaction on salient ESG issues.

Keywords

Introduction

Empirical corporate social responsibility (CSR) and environmental, social and governance (ESG) scholarship overwhelmingly focuses on action: examining whether firms have strengths, concerns, or face controversies (Orlitzky et al., 2017). Historically, researchers have investigated the magnitude of corporate actions (positive or negative), the direction of effects on stakeholders (employees, investors, consumers, communities, etc.), and/or the impetus for acting (government mandates, mission/values, competitive pressures, voluntarism; Campbell, 2008; Wood, 1991).

Across myriad studies, however, a near ubiquitous omission persists: overlooking the lack of corporate action on salient issues, signified by a zero. The zeroes indicate neither a strength nor a concern in commonly used ESG datasets. 1 Zeroes are often implicitly treated as neutral, inferred as an absence of information, or conflated with missing information.

On the contrary, zeroes are information-rich. Zeroes typically represent no action on a topic deemed salient by a rating agency. 2 In the aggregate, the proliferation of zeroes signals collective inaction on salient issues. Then, when zeroes are arithmetically transformed through best-in-sector scores (i.e., London Stock Exchange Group or LSEG/Refinitiv data), normalized, or aggregated into overall scores, important information is lost. We argue that explicitly surfacing the assumptions underlying zeroes and theorizing the absence of action on salient topics is essential for more fully understanding corporate ESG behavior and its consequences. To illustrate how routine data transformations can obscure the meaning of zeroes, we use a recent, representative publication.

Corporate Inaction in CSR/ESG Research: A Recent Example

When ESG data are arithmetically combined and then normalized, the information contained within a zero can be obscured. Overlooking zeroes regularly occurs when researchers construct a single overall ESG score. A recent, peer-reviewed article published in a top-tier journal illustrates how common a desire for an overall ESG score is and how such an approach may yield unintended consequences. Bikmetova and Pirinsky (2026, p. 347), using longitudinal MSCI/KLD data and Sustainalytics binary indicators, explain (emphasis added): (W)e follow the literature to make the ratings comparable across time (e.g., Kempf and Osthoff 2007; Halbritter and Dorfleitner 2015). To this end, we first compute the total ESG score as

With this approach, Bikmetova and Pirinsky (2026) follow a conventional process used by many studies in the literature. However, this approach can unintentionally embed two often unexamined assumptions: first, that strengths and concerns should be summed; and second, the implications of normalizing data by year. We explicate each assumption in turn.

Assumptions in Summing “All E, S, and G Strengths Minus the Sum of all E, S, and G Concerns”

Simply put, adding and subtracting indicators within or across ESG categories creates a socially constructed metric (Eccles et al., 2020). Prior research emphasizes that strengths and concerns represent distinct constructs, with no theoretical substantiation for adding strengths and subtracting ESG concerns to form a net score (Carroll et al., 2016; Skandera et al., 2023).

Moreover, summing strengths and concerns collapses qualitatively distinct behaviors into a single dimension that may lead to unintended results. First, researchers may introduce additional heterogeneity by creating a net ESG score when subtracting concerns from strengths. In this situation, researchers create another form of zero where the count of strengths is non-zero in conjunction with an equal count of concerns. As such, researchers lose dimensionality in the data.

For example, a company with five strengths and five concerns would receive a net score of zero, the equivalent net score as a firm with no observable actions whatsoever. These two firms, however, are conceptually distinct: doing good and doing harm differ fundamentally from doing nothing. In other words, a net score that combines strengths and concerns implies that a firm that pollutes heavily would be absolved of responsibility by donating to other environmental causes and considered equivalent to a firm taking no actions (Griffin & Mahon, 1997). This implicitly assumes moral and behavioral equivalence where none exists merely due to implicit assumptions and actions taken by the researcher.

Second, subtracting concerns from strengths also makes a strong assumption that the constructs are conceptual opposites, equal in both scale and meaning, an assumption unsupported by theory (Carroll et al., 2016; Skandera et al., 2023) and unsupported by MSCI/KLD’s own definitions of the indicators. In 2018 there were 15 categories of environmental strengths and 7 categories of Environmental Concerns (MSCI, 2019), so, strengths and concerns are not necessarily balanced in count or concept. For example, MSCI/KLD measures strengths and concerns dealing with water stress, yet other measures like raw material sourcing only have a strength category and no corresponding concern measure (MSCI, 2019). Equal weighting between the two raw counts that would allow subtracting concerns from strengths lacks justification.

Importantly for our focus on zeroes, summing strengths minus weaknesses of all E, S, and G indicators renders the zeroes analytically invisible due to the mathematical identity property (i.e., a ± 0 = a). In doing so, researchers obscure the absence of action on a salient topic. This arithmetic combination also tends to advantage large firms (Dobrick et al., 2023) and firms with more opportunities to accumulate ESG strengths (Bryant et al., 2020).

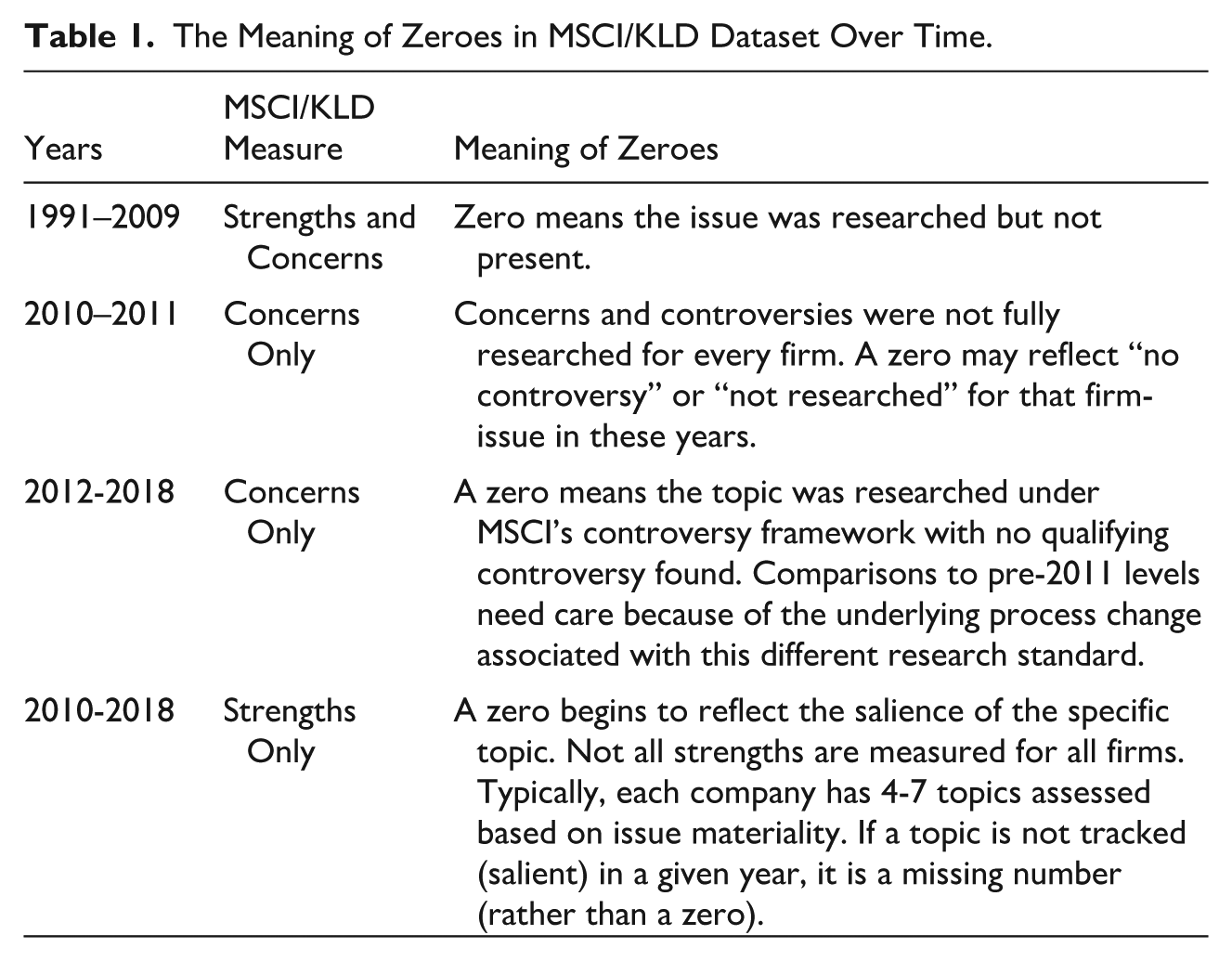

Third, inconsistencies within indicators over time are perhaps one of the biggest threats to the validity of longitudinal studies using MSCI/KLD data such as Bikmetova and Pirinsky (2026). One benefit of using MSCI/KLD data is the long history of data. However, an underappreciated issue comes from the fact that indicator meanings have shifted over time, specifically, changes regarding the measurement methodology. Prior to 2010, a zero represents similar information, an absence of the specific indicator. Yet zero represents different meanings for strengths and concerns for ratings in 2010 and thereafter. A summary of how the meaning of a zero has changed is shown in Table 1.

The Meaning of Zeroes in MSCI/KLD Dataset Over Time.

As a result, what the zeroes represent as a strength or as a concern can have different meanings. For strengths, all “positive ESG performance indicators” were researched for every company until 2010 (MSCI, 2019). Which means in 2009, for example, a zero in MSCI/KLD data signifies that the strength or concern was not present for the company. Since 2010, the dataset has used “industry-based key issues” for strengths, where companies are “typically scored on only 4-7 of the most material ESG key issues for its primary industry” (MSCI, 2019). This changes the underlying meaning of a zero for an MSCI/KLD strength: when a topic is designated as material to the firm’s industry, a zero indicates that no qualifying activity was found for that firm.

For concerns, “negative ESG performance indicators . . . analysts investigate and assess controversies involving the impact of company operations and/or products and services that allegedly violate national or international laws, regulations, and/or commonly accepted global norms” (MSCI, 2019). During 2010 and 2011, however, concerns were not researched for every company. Thus, caution should be used when comparing data before and after 2011. And concerns with the value of zero in 2010 and 2011 should be viewed differently than other times (i.e., 2009 and earlier; or 2012 and after).

MSCI/KLD has historically been most used by researchers studying ESG activity. However, MSCI/KLD is not the only data source. Many researchers, including Bikmetova and Pirinsky (2026), have turned to other datasets to better understand ESG behavior such as the LSEG/Refinitiv ratings. LSEG/Refinitiv provides ESG ratings as letter grades, A+ through D–, based on an underlying numeric score ranging from 0 to 100 (Muck & Schmidl, 2025). These scores are based on a weighted average of ten combined ESG categories: four environmental, four social, and three governance categories. This is in stark contrast to MSCI/KLD data which gives scores on different ESG dimensions “intentionally without creating an aggregate measure of ESG performance” so that each researcher must combine data on their own (Eccles et al., 2020).

A benefit of the LSEG/Refinitiv ratings is fulfilling a need for a standardized approach to ESG. But drawbacks exist too. As users of ESG data have diverse needs, this aggregation of data into a single score may decrease the usefulness of the data by decreasing flexibility. Further, the theoretical arguments not to combine categories into a single score discussed above still apply to LSEG/Refinitiv ratings. Combining these diverse constructs into a single score may be problematic, as Widyawati (2021, p. 1591) notes, “a qualitative analysis of indicators suggests that rating agencies subscribe to different interpretations of ESG, particularly for the governance dimension.”

Assumptions in “Then Normalize the Scores”

Normalizing ESG scores offers benefits such as accounting for changes over time within a dataset. However, normalization can fundamentally change what zeroes mean due to underlying assumptions. Normalized scores are inherently relative, tying each firm’s assessment to the behavior of its peer group at a given point in time. By making the analysis relative, the referent group can be obscured, researchers could lose insight due to global changes in the data, and widespread inaction can be erased. This is because between-year variation is removed, hiding temporal trends.

In normalized data, a firm that engages only in inaction (i.e., exhibits only zeroes), receives a positive ESG rating when its peer group has more concerns. The same firm receives a negative score when peers have more strengths, even if the firm itself never changes behavior. Normalization can introduce score discrepancy over time without actual behavioral change, depending on the referent group.

Additionally, adding or removing firms from the MSCI/KLD sample population, which has occurred several times, could alter the referent group of comparable firms. This means examining industry-specific contexts such as rivalry with peers, capital intensity, industry growth, differentiation, and concentration can influence a firm’s ESG strengths and concerns (Bryant et al., 2023; Griffin et al., 2015; Hoffman, 1999). Therefore, interpretations of models built by normalizing MSCI/KLD scores must consider referent groups. Transforming data can change the implications of the analysis, complicate causal inference, and blur substantive meaning.

Again, as above, using LSEG/Refinitiv ratings does not overcome these issues. Instead, the ratings are already relative as they are based on how a firm performs relative to their industry group defined by Thomson Reuters Business Classification. Normalizing data masks actual firm behaviors, as higher ESG scores can curtail an urgency to act.

If information-rich zeroes exist and matter theoretically, the question becomes how scholars should model them appropriately. In the next section, we discuss four modeling techniques to consider.

Methodological Fixes and Modeling Zeroes

Researchers often rely on a net ESG score by subtracting concerns from strengths because the MSCI/KLD data can appear amenable for ordinary least squares (OLS) regression models. While this approach has benefits, as a single, aggregated ESG score is often desired, this methodological convenience introduces conceptual problems (discussed above).

Instead of net scores, predicting either strengths or concerns (independently) with OLS would also be inappropriate due to the relatively high proportion of zeroes in the dataset and the bounded, relatively short distribution range of data. That is, strengths are only researched for at most seven items, meaning the largest count could be seven. These data characteristics likely violate OLS modeling assumptions of normality and homoskedasticity.

In sum, just because the data behaves in a manner that appears amenable to modeling by OLS regression does not mean that such an approach is the correct one. The inconvenience of having to use a non-OLS regression technique is easily overcome by using models specifically designed to predict count data.

Models designed for count data, by contrast, can explicitly predict strengths and concerns separately. Modeling techniques to predict count data are designed to handle discrete, non-negative dependent variables representing the number of occurrences within a fixed interval of time or space. In addition, some count models also allow researchers to theorize about the meaning of zeroes by providing flexibility with assumptions regarding zeroes in a dataset. Poisson, Conway-Maxwell Poisson, hurdle, and zero-inflated Poisson (ZIP) models differ in assumptions about why zeroes occur and how zeroes are treated, giving researchers choices to test theoretically derived hypotheses about inaction in the MSCI/KLD dataset.

One of the most common and straightforward models for predicting count data (0, 1, 2, 3, . . .) is Poisson regression, where counts are predicted using a Poisson distribution. Parameter estimates from such a model are easy to interpret, representing the change in the log of the expected count corresponding with a one unit change in the predictor. Under this model, zeroes are treated like any other value; that is, a Poisson process generates all values. However, real data often violates the equidispersion assumption underlying Poisson distributions, that is, the researcher must assume the mean of the dependent variable is equal to the variance.

A second model that overcomes a potential equidispersion violation is the Conway-Maxwell Poisson regression. This modeling technique introduces a dispersion parameter allowing for the mean to be either greater or less than the variance. The Poisson and Conway-Maxwell Poisson regression both assume all zeroes are the result of a data-generating process similar to other count values. There are other modeling techniques that allow for zeroes to be the result of a separate process. This means researchers can treat zeroes in a way that allows for hypothesizing that the mechanisms underlying inaction are different from those underlying action. Two common models allowing for zeroes to be from a different process are hurdle models and ZIP models, discussed below.

A third technique for handling count data, a hurdle model, contains two distinct processes: one process to describe the probability of zeroes and a second process for examining positive counts (1, 2, 3, . . .). Griffin and colleagues (2026) argue for this approach when using MSCI/KLD data because decision-making is often a two-stage process. The first decision is whether to take an action. If the answer is affirmative, that is, the hurdle is cleared, only then is a decision of how much action to take considered. The two-stage hurdle model is a conceptual match where modeling the likelihood of zeroes (a lack of action) accounts for the first decision of “whether or not” to act. Subsequently, the positive count component models the second stage describing the “how much action” decision. In other words, the hurdle model incorporates separate modeling approaches for examining action and a lack of action.

A fourth technique is a ZIP model, which also allows zeroes to be generated from a separate process; that is, inaction can be a separate process from action. The difference in assumptions between the hurdle model and the ZIP model lies with the zeroes. A ZIP model assumes that zeroes come from two different processes, one process that always generates zero, that is, a structural zero, and another process that can generate any count data including a zero. This approach should be used if the researcher assumes there are two latent groups of zeroes in the dataset, one group of zeroes that could not have positive counts and another group that could have positive counts yet does not. A classic example of this approach is if a researcher were measuring the number of fish caught by individuals leaving a park. If the number (of fish caught) is zero, one explanation could be due to the individual having bad luck while fishing that day. Or a zero could result if the individual was at the park for some other reason aside from fishing. The first situation is where the individual could have caught a fish but did not now; the second situation is where the individual would have never caught a fish, a source of structural zeroes.

Importantly, the Poisson, Conway-Maxwell Poisson, hurdle, and zero-inflated models address many common features of count outcomes, yet these models are not an exhaustive list of the available modeling strategies for count data. Models based on Poisson distributions are commonly used, but depending on the situation, other distributions may be preferred. Negative binomial-based models offer alternative ways to accommodate overdispersion and unobserved heterogeneity that could arise with standard Poisson assumptions.

In summary, these four modeling approaches to predicting count data can be useful to researchers dealing with zeroes in E, S, and G datasets. Researchers interested in assuming that zeroes are generated by a process like other counts could use a Poisson or Conway-Maxwell Poisson distribution as a modeling technique. In contrast, hurdle models assume a fundamental difference in the process of generating zeroes and the process of generating positive counts. A ZIP model also allows for two types of zeroes by assuming two latent subpopulations that differ in the reasons for having a zero. In other words, ZIP models assume heterogeneity in the meaning of the observed zeroes. The key is to recognize that the choice between these modeling approaches is ultimately a theoretical choice about zeroes. If there are multiple reasons why a lack of action (zeroes) occurs then assuming a single underlying process when using a Poisson model may hide important nuances in the data, leading to inferior model fits or different conclusions as we demonstrate in Supplemental Appendix A.

While MSCI/KLD data combine into count data where zeroes could be treated differently via different modeling techniques, the LSEG/Refinitiv ratings appear ordinal at the letter grade level and continuous at the underlying score level. Importantly, LSEG/Refinitiv ratings are a combination of ten different underlying category scores. The construction of the underlying scores also includes multiple forms of zeroes. As Muck and Schmidl (2025, p. 7) detail “some firms are assigned a score of zero by construction” such as when a firm falls short of a predefined sustainability criteria or when information is missing. This indicates that zeroes could mean either missing data or not enough action. In a situation where a researcher is modeling the underlying LSEG/Refinitiv category score, accounting for differing types of zeroes with a Heckman model or a finite mixture model (a ZIP model is a specific form of finite mixture model) may be appropriate.

Illustrative Empirical Study: Examining Environmental Inaction

In the Supplemental Appendix A, we use data from MSCI/KLD to create a model predicting a firm’s eco-friendly activities. This illustrative example uses a ZIP model that allows for zeroes to represent both “never” and “not now” forms of inaction, as described above when describing the number of fish caught by individuals leaving a park. We show that the choice of modeling technique, a ZIP model compared with a Poisson model, can lead to different conclusions in an analysis.

The analysis in Appendix A demonstrates that treating zeroes as if all zeroes are generated in a homogeneous fashion can obscure heterogeneous behaviors of firms. The data show that most firms (≈ 67%) took no eco-friendly actions recognized by the MSCI/KLD dataset in 2018. That is, approximately two of every three firms are characterized by a lack of action on salient issues.

Further, by applying a ZIP model, we explicitly account for the possibility that inaction can arise from distinct, underlying processes. We show a difference between firms that have a “never” trait, that is, producing structural zeroes, and firms that may be inactive at a given point in time but remain open to future action, having a “not now” state. The ZIP approach provides a superior fit and yields substantively richer insight into firm behavior when compared to a standard Poisson model. Our results suggest more than one underlying mechanism may exist for environmental inaction.

Further, our illustrative study shows preliminary evidence that insight is lost if researchers ignore inaction or assume corporate environmental inaction is always temporary. That is, assuming all inaction is a transient “state” might obscure an underlying fixed “trait” of a firm being unwilling to engage in eco-friendly activities. To be clear, we are not arguing that prior studies are necessarily wrong, rather the insights from traditional models might be unable to capture critical time-invariant factors helpful in theorizing and testing why firms take no action on salient issues.

We illustrate this temporality with the parameter estimate of advertising intensity which differs depending upon the assumptions around inaction, that is, whether a ZIP model is used versus a Poisson model. In the ZIP model, greater advertising intensity is associated with a greater likelihood of a firm taking no action (zero-inflated component, a structural zero fixed “trait”). Advertising intensity is also associated with more eco-friendly activities, only if a firm is willing to act (Poisson component). Contrast this with the results of the traditional Poisson model which suggests no significant relationship between eco-friendly activities and advertising intensity. Overall, the ZIP model results imply advertising intensity has a complex relationship with eco-friendly activities, with two opposing effects depending on the type of zero (inaction). This means that the way a researcher chooses to model zeroes can have a substantial effect on the conclusions drawn from a study.

For example, one interpretation of the ZIP model could imply that advertising intensity as a proxy for communications might be stronger in firms in the structural zero group (the Zero-inflated component) that are staunchly unwilling to act. As such, for firms with a “never” trait approach to eco-friendly activities, advertising may be used as a communications tool to mask or redirect attention. Alternatively, firms willing to undertake eco-friendly activities (the Poisson component) may use advertising to communicate eco-friendly activities.

Not all variables show such a complex connection. Firm Size, for example, has a relatively consistent relationship with eco-friendly activities across the ZIP model, where larger firms have higher counts and are less likely to be in the “never” class of structural zeroes. Importantly, policy implications of moving different firms from never to not now are quite different than incentives to move from not now to now.

Three Implications of Aggregating and Normalizing Data and Not Examining Zeroes

First, Omitting Inaction Masks Collective Behaviors Over Time

When firms take no observable action on salient ESG issues and face no penalty, inaction can proliferate through imitation of referent firms (Lieberman & Asaba, 2006). When widely adopted, persistent inaction can contribute to what Dyllick and Muff (2016) describe as the “big disconnect” and what Landrum (2018) labels “weak sustainability”: increasing claims of corporate ESG activity alongside planetary boundaries being approached or exceeded.

Normalization further obscures this process by rendering zeroes relative rather than absolute. As a result, models compare a firm’s (in)actions within a peer distribution at a specific point in time rather than the firm’s actual behavior, inclusive of inaction. Normalizing data means that models reflect a company’s relative actions, not the actual corporate behavior.

In addition, by transforming the raw data, thereby removing between-year variation, normalization can conceal global trends and collective dynamics. This can effectively mask widespread behaviors such as inaction and accumulation of inaction over time. In essence, researchers could miss the forest for the trees because aggregated inaction on salient issues leads to what Mitnick and colleagues (2023) describe as socially accepted yet not acceptable and potentially harmful behavior.

Rather than normalizing data, we encourage researchers to consider an alternative: directly modeling the dependent variable and including fixed effects for each year. That is, include a dummy predictor variable for each year of data. This approach flexibly absorbs year-specific shocks that vary by year but do not vary by firm, such as policy changes and measurement differences. Further, by accounting for such fluctuations within the model instead of ex ante normalization, the effects of each year are estimated jointly with the rest of the model helping standard errors reflect the overall data-generating process and heterogeneous time trends in the other covariates. Finally, and importantly for model interpretation, by not normalizing data by year and instead including year level fixed effects in a model, this approach allows zeroes to remain zeroes, preserving the informational content of zeroes. Inaction is visible rather than analytically erased.

Second, Inaction Is a Common Response

Most firms prefer inaction. After corporate environmental misdeeds, Griffin et al. (2026) found environmental inaction as the preferential “action.” Yet scholars’ choices of modeling techniques (OLS) and arithmetic transformations (subtracting concerns from strengths; normalizing data; relative best-in-sector comparisons) to arrive at an overall ESG score systematically obscure the meaning conveyed by the zeroes. The invisibilized zeroes also risk legitimizing corporate inaction.

When no observable action carries neither ill will nor costs, scholars risk reinforcing and legitimizing inaction by omission. Overlooking zeroes can reinforce perceptions that existing regulations are sufficient (Zuckerman, 1999), encouraging firms to delay action. This means that tacit acceptance of no action can encourage firms not to act until compelled by external influences: public policy change, social pressures, or competitive dynamics (Campbell, 2008). In this way, analytical choices may unintentionally normalize the absence of action as a rational response.

Third, Zeroes Are Fundamentally Ambiguous Indicators

When explicitly considered, a zero can be interpreted in at least two distinct ways. First, a lack of observable action could indicate “not now,” a temporary state that requires more time, resources, or capacity-building to implement complex routines or policies. More problematically, the absence of action can indicate “never,” a fixed trait, signaling an unwillingness or resistance to act.

In essence, inaction can be the result of a temporary “state” or a fixed “trait” of the company. The difference between the two is that states describe a company at that specific moment, that is, not now, whereas traits describe a company generally, that is, never. Treating all zeroes as equivalent obscures this heterogeneity.

Moreover, collapsing information-rich zeroes can risk implying that getting to zero is an appropriate goal – particularly when compliance itself is coded as a zero. As a result, extant regulations become, by default, the appropriate standard. Yet scholars insist that staying within planetary boundaries (Nilsen, 2024) requires the E of ESG to shift to action, as harms and moral hazards irreversibly accumulate. Modeling assumptions and proscriptive arguments are in an uneasy tension. Scholars risk misinterpreting whether inaction reflects strategic calculation, technical limits, or outright resistance. In short, the fundamental ambiguity of zeroes when interpreted as homogeneous obfuscates if inaction on a salient issue is a delay or denial, as we discuss in the next section.

Future Research Directions: Interpreting an Absence of Action

To leverage the ambiguity embedded in zeroes, future research should more explicitly theorize inaction as an organizational response rather than as missing or neutral behavior. Drawing on Oliver’s (1991) typology, we contextualize a firm’s lack of action on salient ESG issues as ranging from passive conformity to active resistance. That is, corporate inaction may be interpreted heterogeneously, with a zero being passive or an active form of resistance when autonomy is threatened or conflicts emerge.

Oliver (1991) argued that firms are not merely shaped by, and passively conform to or mirror, institutional pressures. Managers have a choice. Further, organizations exhibit a range of responses that shape and influence their institutional environment. Interpreting zeroes through this lens allows scholars to examine distinct mechanisms and consequences underlying a lack of observable action.

Oliver identified five corporate responses to external influences: acquiescence, compromise, avoidance, defiance, and manipulation. We illustrate how explicitly elevating zeroes to distinguish how a lack of action on salient issues can vary from passive to consequential across different contexts. Below, we illustrate how zeroes may map onto Oliver’s five responses to external influences, providing a foundation for future theoretical and hypothesis development.

Acquiescence: Habit, Imitation, or Compliance

A lack of action as acquiescence may reflect embedded organizational habits, taken-for-granted norms, or full compliance with regulatory standards. Legal compliance, for instance, is measured as a zero in many E, S, and G indicators. Compliance measured as a zero renders inaction seemingly unremarkable, neutral, uninteresting or unimportant since legal standards are met. In stable environments, compliance may suffice.

However, because legal standards lag social harms, inaction may persist even as harms accumulate. Controversies can shift social influences with new regulatory requirements that disrupt the equilibrium (Campbell, 2008; Suchman, 1995). Further, since ESG laws vary across countries, differences exist in how much certain ESG activities matter relative to specific firms and sectors (Sauerwald et al., 2026).

When instability or uncertainty is high, promulgating new standards might be delayed. An effect uncertainty exists when corporate actions may or may not lead to a desired E, S, or G effect (Delmas et al., 2026). In this instance, with an unclear link between action and impact, a zero may reflect deference to prevailing norms (compliance) due to complexity. For example, IKEA’s lack of substantive, beyond-compliance action due to the unknown relationships between deforestation and regeneration (Delmas et al., 2026) could reflect inaction due to acquiescence.

Compromise: Balancing, Pacifying, or Bargaining

A zero, when interpreted as a compromise, may reflect selective efforts to balance demands through satisficing, pacifying, or bargaining among competing stakeholders. That is, firms facing resource constraints or legitimacy challenges (Suchman, 1995) may selectively adopt certain, visible E, S, or G activities to pacify salient critics. Conforming to some stakeholders and not others would reflect minimal investment in some categories (a lack of action) while prioritizing beyond-compliance activities (strengths) in others. These attempts to balance, pacify, or bargain across salient stakeholders are consistent with a portfolio approach of CSR investments, with a key implication being diversifying action and inaction across categories based on relative risks (Skandera et al., 2026). Here, zeroes do not signal indifference but purposeful balancing – appeasing some stakeholders while deprioritizing others. This approach highlights how inaction and getting-to-zero efforts may coexist with substantial ESG activity directed elsewhere, complicating aggregate interpretations of a singular ESG outcome variable.

Take Shein (da Silva, 2024) and the 2013 Rana Plaza collapse that affected garment sector workers in Bangladesh (Bossavie et al., 2023). When faced with persistent allegations of forced labor, below-minimum wages, and unsafe workplace conditions, Shein issued public statements and commissioned audits. Yet decoupling the public statements and voluntary, external audits from operational changes allowed Shein to maintain low-cost oriented, efficient supply chains (da Silva, 2024). Similarly, the international scrutiny of Rana Plaza ultimately resulted in increased wages yet limited operational change (Bossavie et al., 2023). The attempts at pacifying critics by communicating corrective steps while preserving financial growth kept substantive reforms at bay while allowing questionable practices to persist.

Avoidance: Concealment, Buffering, or Escape

Inaction may also serve as avoidance. Firms can conceal non-conformity by buffering or escape scrutiny by remaining unremarkable. With no observable action on salient issues, firms remain off the radar. In this instance, zeroes can facilitate invisibility. With no strengths to publicize and no concerns to attract attention, there is a paradox of invisibility. The good news is that the firm is not newsworthy (concerns are buffered, minimized, or dismissed), while the bad news is that the firm remains unnewsworthy (strengths are not noted). Without generating a positive effect despite effort, firms may conclude that the “juice is not worth the squeeze” regarding ESG activities.

Avoidance may be conflated with strategic forbearance (Andrevski & Miller, 2022; Delmas et al., 2026). Opacity around human rights abuses or supplier disclosures in controversial sectors, for example, might blunt accountability through invisibility. Avoidance may be particularly attractive for less visible, resource-constrained, privately held, smaller, or business-to-business firms to remain “under the radar.” That is, firms that normally operate outside the media/community spotlight might use inaction to conceal, buffer or avoid ESG scrutiny. Attempting to escape notice may also result in claiming narrow domains (“we only operate locally” or “we focus on our shareholders”) to avoid mentioning E, S, or G activity.

Similarly, concealment occurs when an equal number of strengths and concerns sums to zero and is normalized, and invisibilized in a controversial industry, for example. Offsetting pre-existing harms with strengths that net to zero can obscure controversy through aggregation to create comparative parity across a group. Diversification within an ESG category (Skandera et al., 2026) might buffer environmental harms by rendering them neutral or redirecting attention to environmental strengths.

For decades, U.S. tobacco manufacturing firms attempted to conceal and deny the addictive nature of tobacco products. Once the costs of concealment were prohibitive, the firms settled with the government via the Master Settlement Agreement. Immediately afterward, concerted efforts to escape the reputational damage of tobacco products led to recruiting employees, improving workplace conditions, and satisfying suppliers to buffer lingering negative effects (Youm et al., 2025).

Defiance: Dismissal, Challenge, or Attack

A zero paired with active resistance to institutional pressures may constitute defiance. Firms may maintain inaction while actively dismissing, challenging, or attacking institutional expectations as a form of decoupling. High internal resistance might manifest in inaction to maintain the status quo while actively contesting policy changes by attacking ESG legitimacy, materiality standards, or regulatory authority.

Public defiance with persistent inaction on salient issues can shift attention away from cumulative harms and displace moral responsibility (Mitnick et al., 2023). Defiant inaction can be particularly difficult to observe when normalization renders a firm’s behavior average relative to peers, despite sustained internal, operational resistance.

ExxonMobil’s limited climate action, following years of denying responsibility, while actively advocating for global action and national energy independence (Matthews & Eaton, 2023) suggests defiance. Public efforts diverged from political efforts to derail damaging regulatory changes and muddled scientific findings. The firm remains steadfastly committed to legal challenges and a narrative of energy independence in lieu of operational changes.

Active defiance that materially misleads investors on safety standards is a form of illegal behavior. Following the 2019 Brazilian deadly tailings dam collapse that killed 270 people, for example, Vale was charged with securities fraud (U.S. Securities and Exchange Commission, 2023). Allegations of materially misrepresenting investors about ESG-related disclosures were upheld in 2023. Vale exemplified defiance by openly contesting safety standards and ESG disclosures may have obscured inaction with an accumulation of harms. When normalized across the mining industry, defiant inaction may be overlooked.

Manipulation: Co-optation, Influence, or Control

Finally, zeroes may mask manipulation. Firms may seek to co-opt, actively influence or control institutional pressures that can appear as inaction in an ESG database. Controlling narratives through omission, selective transparency, or lobbying can steer attention to symbolic commitments to avoid substantive behavioral change. Lobo (2026) argues that Purdue Pharma’s deceptive practices, including a failure to inform stakeholders of the harmful effects of OxyContin, a form of inaction, constitute deception by omission in a corporate context.

Alternatively, firms may import influential (economic, political, celebrity) stakeholders to reorient priorities. The Business Roundtable Governance Committee, an influential external stakeholder, issued its 2019 Purpose of a Corporation statement that included a commitment to all stakeholders (Business Roundtable, 2019). Yet the signatory firms did not conform to a commitment to all stakeholders. The Business Roundtable Governance Committee Chairman, who was at the time the CEO of Johnson & Johnson, only ceased selling talc-based products in the United States and Canada the following year. Talc-based products are potentially harmful due to potential asbestos contamination from the mining process. Several years later, all talcum products globally were restricted with a transition to a safer corn-starch-based formula after thousands of lawsuits with billions of dollars in litigation (Black Women for Wellness – Los Angeles CA, 2023).

In some cases, manipulation crosses into fraudulent misrepresentations where inaction is conflated with illegal behavior. Volkswagen, for example, installed software to falsify emissions tests for ≈11 million vehicles. VW deliberately manipulated vehicles to improve emissions outcomes and to retain public compliance with regulatory guidelines. The masking of diesel emissions for years is an example of controlling ESG evaluations on a salient issue. What appeared as compliance, inaction from a measurement perspective, was manipulation that was not an externally observable action for years.

Conclusions

Treating zeroes as theoretically meaningful opens new avenues for understanding when inaction reflects passive compliance or active resistance. Future research can leverage Oliver’s (1991) insights to examine contextualization of inaction, identify antecedents of persistent inaction, and assess the cumulative consequences of delay or denial.

By elevating zeroes from noise to signal, our hope is that scholars can better capture and appropriately model the dynamics of corporate (in)action that shape ESG outcomes over time. Zeroing in on the zeroes in E, S, and G datasets reveal three important lessons.

First, overlooking zeroes, which signify inaction on a salient issue, can obfuscate relevant information on corporate behavior. Zeroes are information rich. Our illustrative example shows that a zero may represent either a fixed trait or a transient state. Further, when scholars implicitly ignore zeroes, getting to zero may inappropriately limit corporate aspirations to legal standards despite scholars’ insistence that business as usual is insufficient for sustaining or regenerating the planet (Landrum, 2018).

Second, scholars’ desire to construct an overall ESG score and normalize data can render corporate inaction meaningless. In essence, normalizing data can be a structural issue within an analysis if there is a collective increase in inaction that persists. When neutrality is privileged analytically, a lack of action can become valorized by default. The net result of ignoring inaction on salient issues is a distorted view of firms’ actual behaviors and the potential for collective harm. Methodologically, normalizing data can obscure the mechanisms underlying why a firm might have no observable action.

Third, we use Oliver’s (1991) framework to contextualize how corporate (in)action can be interpreted as varying from passive conformity to active resistance. We call for a theory that explains when and why inaction is encouraged or rendered invisible based on mechanisms underlying a firm’s unwillingness or inability to act. Teasing out how no observable action (a zero) may be inferred as acquiescence, compromise, avoidance, defiance, or manipulation has important consequences for scholarship, managers, and the planet.

Overall, by zeroing in on the zeroes, a proxy for a lack of observable action on a salient issue in ESG/CSR datasets, we call for a deeper understanding of the processes, consequences, and normative foundations of inaction for theory development. Recognizing, theorizing, and interrogating the meaning of zeroes, we believe, will enable a more honest account of corporate activities.

Supplemental Material

sj-docx-1-bas-10.1177_00076503261456393 – Supplemental material for Zeroing in on the Zeroes: CSR/ESG Inaction as a Choice

Supplemental material, sj-docx-1-bas-10.1177_00076503261456393 for Zeroing in on the Zeroes: CSR/ESG Inaction as a Choice by Jennifer J. Griffin and Andrew Bryant in Business & Society

Footnotes

Acknowledgements

With gratitude to co-editor in chief Dr. Punit Arora for his deft insights and others for their nudges. The authors would like to acknowledge the incredible mentoring and ongoing support from Dr. John F. Mahon and Sara Bryant. As John, in his booming voice, with tongue-in-cheek, might have said “It’s about time!” I hear you, John, loud and clear, with gratitude and fond memories of your ever-energetic exhortations in mind.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: Artificial Intelligence (Microsoft CoPilot) was only used to assist in language succinctness and copy-editing, for example, grammar and spelling. The authors reviewed and edited the content as needed and take full responsibility for the content of the publication. The authors report there are no conflicts of interest to declare.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.