Abstract

In many European democracies, fiscal consolidation is back on the agenda. A common claim is that electoral constraints—stemming from public resistance to tax increases and spending cuts—limit policymakers’ ability to pursue deficit reduction. However, recent research suggests that public support for fiscal consolidation may be stronger than previously thought, calling this line of reasoning into question. This paper re-examines the issue in the British context. We find that, while a majority of respondents express support for fiscal consolidation in principle, only a minority prioritize it when faced with concrete trade-offs. Moreover, voters appear receptive to counter-narratives portraying public debt as sustainable and fail to link high debt levels to future economic hardship, undermining claims that this pro-consolidation minority will grow as fiscal conditions worsen. Overall, support for consolidation appears too shallow to generate pro-consolidation electoral incentives, even in a high-debt context. We discuss implications for future research.

Keywords

Introduction

To mitigate the economic consequences of the COVID-19 pandemic, governments have spent and borrowed on a scale not seen since the Second World War. For high-debt countries like France or Great Britain, stubborn inflation and slow economic growth have increased borrowing costs, raising concerns of a fiscal crisis absent major fiscal consolidation.

Do voters in Western democracies make it easier or harder for governments in high-debt countries to prioritize fiscal discipline and engage in fiscal consolidation? There is no agreed-upon answer to this question. For scholars that emphasize electoral incentives against fiscal consolidation, a major fiscal crisis remains a distant threat with uncertain distributional consequences. This limits voters’ ability to form strong opinions on the issue (Jacobs, 2011; Jacobs & Matthews, 2012). As a result, people more strongly oppose the short-term consequences of fiscal consolidation than they worry about the long-term consequences of doing nothing (Baccini & Sattler, 2025; Bremer & Bürgisser, 2023; Hübscher et al., 2021). For scholars that emphasize electoral incentives in favor of fiscal consolidation, a high-debt context can decrease the uncertainty over the consequences of action and inaction, generating the type of strong support for fiscal consolidation that makes austerity measures electorally attractive (Alesina & Passalacqua, 2016). Recent evidence seems to support this claim (e.g., Bansak et al., 2021). We contribute to this debate by providing new evidence on mass opinions on fiscal consolidation in high-debt and high-income countries.

Each line of inquiry implies different observable implications regarding (1) the share of voters who care about prioritizing fiscal consolidation over competing goals, and (2) the potential for this group to grow in the face of worsening fiscal conditions. To test these implications, we use observational and experimental survey data collected in Great Britain, a country where—in the aftermath of the Great Recession—the Conservative government famously prioritized deficit reduction and implemented spending cuts without losing its post-austerity reelection bid (Barnes & Hicks, 2018, 2022; Fetzer, 2019). Assuming demand-side factors help explain this outcome, Great Britain constitutes a most-likely case for finding attitudinal evidence in support of arguments that fiscal consolidation need not be electorally costly. To collect this evidence, we rely on two separate samples of roughly 2,000 British citizens each, one surveyed in December 2021, when inflation was low, and the other in July–August 2022, when inflation was substantially higher.

First, using a diverse set of measurement strategies, we examine the share of respondents who prioritize debt consolidation over other policy issues (e.g., health care, climate spending, social benefits). We find that only a minority do. We also give respondents the opportunity to express their opinion to the government in a letter. We find that people who prioritize debt consolidation over higher spending are more than four times less likely to share their opinion in writing than people who prioritize higher spending. In other words, while many respondents agree with fiscal consolidation in principle, few prioritize this issue to the point of taking action.

Second, we examine two mechanisms that could plausibly contribute to an increase in the share of people who prioritize fiscal consolidation. The first mechanism focuses on elite messaging and how it is received by voters. Mass opinion on complex issues like public debt partially echoes what elites have to say about them (Barnes & Hicks, 2018; Bisgaard & Slothuus, 2018; Fernández-Albertos & Kuo, 2020). Yet, even if people rely on elites to form an opinion, elite rhetoric does not deterministically shape people’s preferences: all else equal, some lines of reasoning are easier to agree with than others. We consequently investigate whether people find anti-consolidation arguments less persuasive than pro-consolidation ones, potentially explaining why anti-austerity narratives have struggled to gain traction in Great Britain. Our experimental evidence does not support this claim: pro-debt arguments, we find, are as persuasive as arguments about the necessity to prioritize debt consolidation.

The second mechanism pertains to voters’ understanding of debt (un)sustainability. We examine whether people connect unsustainable debt to low growth, high inflation, higher taxes, or spending cuts. Evidence that they do would suggest that popular support for fiscal consolidation is underpinned by mental models that connect high debt today to economic losses tomorrow. Such basic understanding could favor an increase in the share of voters who prioritize fiscal consolidation, supporting preventive consolidation now to limit more costly adjustment later. Against this line of reasoning, we find no evidence that the British public connects deteriorating finances to future threats of tax increases, spending cuts, or worsening macroeconomic conditions.

Paraphrasing Schattschneider (1960), when it comes to fiscal issues, the British public sings with an anti-consolidation accent, with limited evidence that this will change in response to worsening fiscal conditions. These findings cut against claims that high-debt contexts generate strong—and growing— public backing for deficit reduction. Instead, they align with the view that well-documented public resistance 1 to tax increases and spending cuts limits policymakers’ ability to pursue deficit reduction. We conclude by outlining priorities for future research on the fiscal politics of Western democracies, including incorporating insights from research in international political economy on the politics of debt management and debt pricing.

Competing Accounts of Mass Opinions on Fiscal Issues

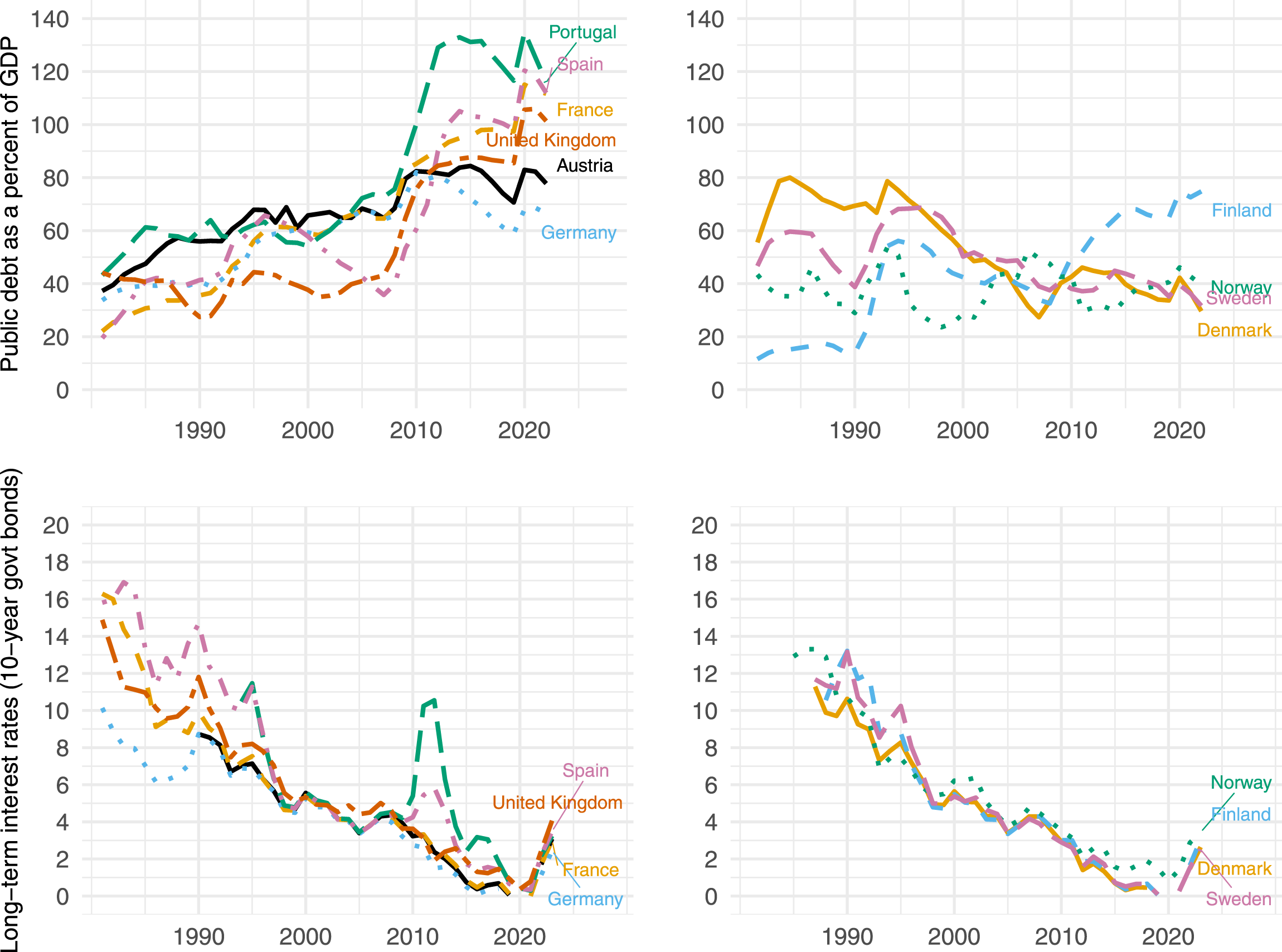

Many advanced economies (though not all, see Figure 1) face high levels of debt. High debt need not always imply a debt crisis, only “unsustainable” debt levels do. In today’s globalized financial system, a country’s debt level is deemed “sustainable” if domestic and international investors maintain demand for the debt at interest rates that the country can afford. For rich but high-debt countries like France or Great Britain, declining and volatile investor demand, combined with slow economic growth limiting how much debt the country can afford, has raised concerns that their debt trajectories are becoming increasingly unsustainable.

2

Absent the possibility of “growing” out of fiscal stress, French and British policymakers strive to maintain investor demand for government bonds. One strategy, called fiscal consolidation, focuses on improving the country’s primary budget balance and signaling to investors a credible long-term commitment to balancing the books (Trichet, 2011).

3

Trends in debt-to-GDP ratios and long-term interest rates in Western Europe. Source: Mbaye et al. (2018); OECD, Long-term and short-term interest rates (indicator), https://doi.org/10.1787/662d712c-en and https://doi.org/10.1787/2cc37d77-en (Accessed on 17 April 2024).

Models of fiscal policy in high-income democracies come in at least two flavors. The most common one argues that voters and electoral politics undermine governments’ ability to engage in fiscal consolidation in the face of rising debt. A second line of reasoning has revised this conventional account, arguing that voters can help tilt the balance in favor of fiscal consolidation. We discuss each in turn.

Conventional Account

According to public choice theorist James M. Buchanan, governments always prefer opportunistic deficit spending over balanced budgets. This happens because voters value public expenditure and consistently underestimate its costs in terms of higher future taxes, in line with Buchanan's (1975) “fiscal illusion” assumption. Globalization and population aging further contribute to debt buildup in the form of a downward pressure on tax revenue and an upward pressure on social spending. Given Western democracies’ large welfare states, structural reforms that would improve the primary balance are politically risky as they tend to affect the pocketbook of key constituencies (Campbell, 2003; Pierson, 2002). Jointly, fiscal illusion and exposure to benefit cuts not only contribute to deficit spending but they also undermine voters’ support for fiscal consolidation in times of fiscal stress.

Theoretically, this line of work contrasts the uncertainty of consolidation’s long-term benefits with the certainty of its short-term costs (Jacobs & Matthews, 2012). A major fiscal crisis remains a distant threat with uncertain distributional consequences. This means that voters are more concerned about the immediate, certain consequences of consolidation than the long-term, unspecified consequences of failing to consolidate. This uncertainty about future consequences limits voters’ ability to form strong opinions on the issue and support consolidation, especially if it comes at the expense of valued social programs or higher taxes (Jacobs, 2011). As a result, fiscal consolidation is unpopular as documented by evidence of mass opposition to austerity measures in the aftermath of the Great Recession (e.g., Bojar et al., 2022; Ciobani, 2024; Hübscher & Sattler, 2017; Jacques & Haffert, 2021; Talving, 2017), which can feed political protest (Ponticelli & Voth, 2020), polarization (Hübscher, Sattler, & Wagner, 2023), and the decline of mainstream parties (Bremer, 2023) to the benefit of more extremist ones (Baccini & Sattler, 2025; Cremaschi et al., 2024; Fetzer, 2019; Gabriel et al., 2026; Galofré-Vilà et al., 2021).

Revised Account

Because fiscal consolidation was unexpectedly common in the aftermath of the Great Recession, recent research has re-examined the assumption that fiscal adjustment is politically self-defeating (e.g., Bansak et al., 2021). According to this work, there is limited support for the claim that fiscal consolidation leads to electoral backlash (Alesina et al., 2019; Arias & Stasavage, 2019), with even evidence that some parties gain electorally from spending cuts (Giger & Nelson, 2011). The reason is that rising levels of public debt and fiscal stress cause enough voters to worry about the state’s finances and demand corrective policies, making austerity measures and fiscal consolidation more politically viable. In other words, voters react to increasing fiscal stress in a thermostatic fashion (Wlezien, 1995), meaning they adjust their preferences dynamically in response to government policy outcomes, creating electoral space for corrective action.

This assumes that voters’ understanding of the government’s intertemporal budget constraint is sophisticated enough to generate support for fiscal consolidation despite its short-term costs, especially so in high-debt countries where debt sustainability is a salient and debated issue (e.g., Brender & Drazen, 2008; Fernández-Albertos & Kuo, 2020; Peltzman, 1992). Alesina and Passalacqua (2016, p. 2604) summarize this line of reasoning as follows: “Given the extensive discussion of the deficits, the pros and cons of austerity policies in the U.S. and Europe, it is hard to believe that today’s voters are unaware of the potential costs of deficits because of fiscal illusion.” In support of this claim, public opinion data show that voters are concerned about the state of public finances. For example, in most European countries, a large majority of individuals surveyed between 2010 and 2020 agree that “measures to reduce the public deficit and debt cannot be delayed,” from a high of 85 percent in 2011 to a low of 67 percent in 2020 (European Commission, 2022).

Which of the conventional or revised accounts best captures the demand side of fiscal politics? Answering this question is important for theory development and future research on political change in post-industrial democracies. Under the conventional account, fiscal consolidation is best conceived as a top-down policy response to macroeconomic imperatives that happens in spite of its potential electoral costs, with downstream consequences for institutional trust and partisan politics. Under the revised account, a bottom-up approach that identifies a pro-consolidation voting bloc and theorizes its political influence would be more fruitful.

Should the Conventional Account Be Revised? Observable Implications and Empirical Design

The conventional and revised accounts lead to distinct expectations about how many people prioritize fiscal consolidation and whether this group can grow in response to fiscal stress. For the conventional account, people are myopic, and few prioritize fiscal consolidation over competing policies. There is also no reason to expect strong support to increase in response to rising debt. For the revised account, the extent to which people are myopic—weighing policies’ short-term impact more heavily than their long-term consequences—changes with a country’s fiscal conditions. As debt increases, so does information on the budget constraint and its implications. Voters also learn about the macroeconomic consequences of unsustainable debt. As a result, the share of people who prioritize debt consolidation grows in response to rising debt, creating an electoral pathway for fiscal consolidation. In the next two sections, we discuss prior evidence and explain how we propose to use observational and experimental attitudinal survey data to test these contrasting predictions.

Who Cares? Measuring Strong Support for Fiscal Consolidation

Survey data show that voters in advanced economies express concerns about government deficits and debt and support fiscal consolidation, with a majority agreeing with the claim that fiscal consolidation “cannot be delayed” and is “necessary” (e.g., Aspide et al., 2023; Barnes & Hicks, 2021, 2022). With this type of measurement strategy, respondents can “have it all,” that is, express their principled support for fiscal consolidation without acknowledging or confronting the trade-offs it entails. But politics, and fiscal politics in particular, is about prioritizing some policy goals at the expense of others. We consequently rely on measurement strategies that make key trade-offs explicit: specifically, we measure the share of people willing to prioritize fiscal consolidation in spite of its short-term costs. One type of cost is the one induced by the budget constraint. A straightforward measurement strategy is to make this constraint explicit by designing survey items that pit fiscal consolidation against spending cuts and tax increases (Barnes et al., 2022; Bremer & Bürgisser, 2023; Hübscher, Sattler, & Truchlewski, 2023). Beyond the budget constraint, there is also the political supply constraint whereby fiscally conservative voters willing to support spending cuts and tax increases might still vote for a fiscally irresponsible candidate because of that candidate’s stance on a non-budgetary issue they comparatively care more about. As a result, we also measure the share of voters who prioritize fiscal consolidation over other high-salience issues such as immigration control.

Measuring people’s policy priorities and willingness to compromise is not enough. We also need to assess whether those who prioritize debt consolidation care enough to act on that preference, thereby constraining anti-consolidation politicians and improving the electoral viability of pro-consolidation candidates. This points to a third measurement strategy, one that captures people’s propensity to behave in opinion-congruent ways, i.e., translate opinions into politically consequential action.

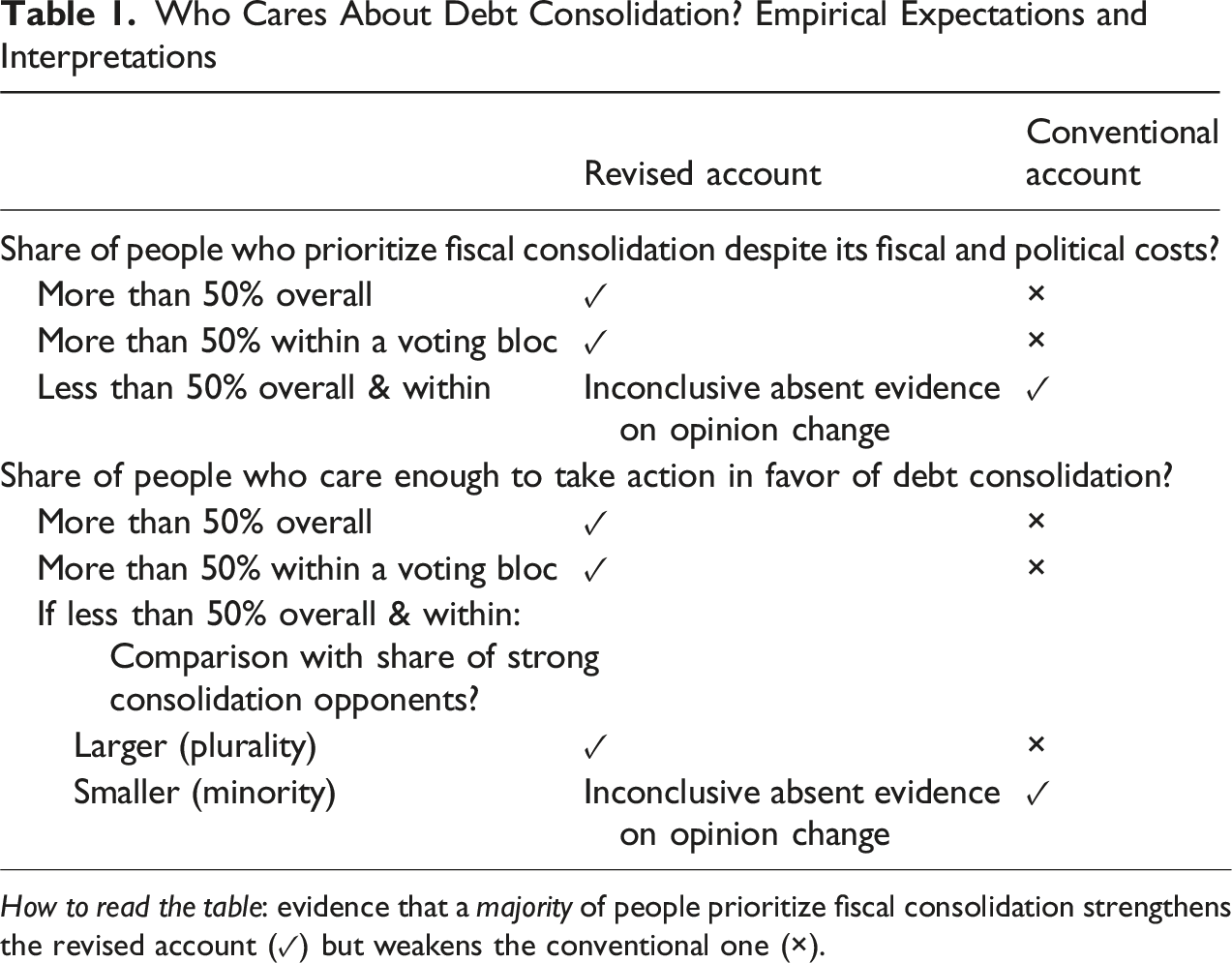

For the conventional account, the share of people who strongly prefer fiscal consolidation—as captured using these alternative measures—is too small to have real political clout. In contrast, for the revised account, the share of people who prioritize fiscal consolidation remains large enough to exert political influence. The definition of “too small” or “large enough” depends on a country’s political institutions. In most majoritarian representative democracies, the implicit benchmark is the one defined by the majority rule. If the majority opinion is to prioritize fiscal consolidation, elected officials will take notice. In Great Britain, one does not need to be “in the majority” to gain policy influence. Its “winner-take-all” political system means that a party with a plurality of votes can still receive a majority of seats in Parliament and control both the executive and the legislative branches. We consequently examine whether a majority of supporters within a voting bloc prioritizes fiscal consolidation. Beyond being “in the majority” overall or within a given voting bloc, another source of political influence stems from differences in opinion-congruent behavior between pro- and anti-consolidation voters (Hill, 2022). Indeed, if pro-consolidation voters are a minority overall but a plurality (relative to anti-consolidation voters) when it comes to taking action, then this can also generate an environment favorable to fiscally conservative policies, even in the absence of a majority strongly in favor.

Who Cares About Debt Consolidation? Empirical Expectations and Interpretations

How to read the table: evidence that a majority of people prioritize fiscal consolidation strengthens the revised account (✓) but weakens the conventional one (×).

Can Strong Support for Fiscal Consolidation Grow?

According to the revised account, in high-debt contexts, the salience of fiscal policy is high and information regarding the consequences of delaying fiscal consolidation is readily available, decreasing the share of people under the fiscal illusion and increasing support for fiscal consolidation. In the absence of longitudinal data measuring fiscal policy preferences before and after a change in the salience of debt (un)sustainability, 4 scholars have turned to survey experiments to test this argument (e.g., Behringer et al., 2024; Fernández-Albertos & Kuo, 2020; Roth et al., 2022). Fernández-Albertos and Kuo (2020), for example, find using a Spanish sample that, when “specific reasons or benefits are made salient,” principled support for fiscal consolidation measured using standard survey items goes up. Does this information also increase people’s willingness to prioritize fiscal consolidation over competing policies and engage in opinion-congruent behavior? To answer this question, we examine how pro-consolidation information presenting British debt as unsustainable affects the strength of fiscal preferences along these dimensions. We also examine whether people reason about the consequences of debt sustainability in ways that align with the type of intertemporal consequentialist reasoning assumed by the revised account (versus the myopic reasoning assumed by the conventional account). The following sections discuss our approach in more detail.

Learning in a High-Debt Context

The previously mentioned evidence suggests that people update their opinion on fiscal policy when faced with pro-consolidation information, but what explains the extent of voters’ exposure to pro-consolidation information in the first place? Existing scholarship focuses on political elites and the media (e.g., Barnes & Hicks, 2018; Bisgaard & Slothuus, 2018). Mass exposure to pro-consolidation information is maximized when elites share the same pessimistic diagnosis about their country’s fiscal situation and advocate for the same policy goals, flooding voters’ discursive environment with unidirectional information on the implications of delaying consolidation. But elite consensus is not something that can be assumed: what happens if insurgent and populist actors with short-term horizons strategically break ranks and provide the opposite narrative? A recent example of this phenomenon is the populist far right’s politicization of climate change. The evidence suggests that it has undermined support among its voting base for policies that prioritize decarbonization (Colantone et al., 2024; Voeten, 2025).

If we cannot assume that pro-consolidation elite consensus will be the norm, then evidence that strong support for fiscal consolidation increases in response to information on the costs of unsustainable debt becomes harder to interpret. On the one hand, it strengthens the revised account by documenting a key mechanism. On the other, this evidence does not speak to expectations of a group-level thermostatic response to rising debt when elites are divided over the need to prioritize fiscal consolidation.

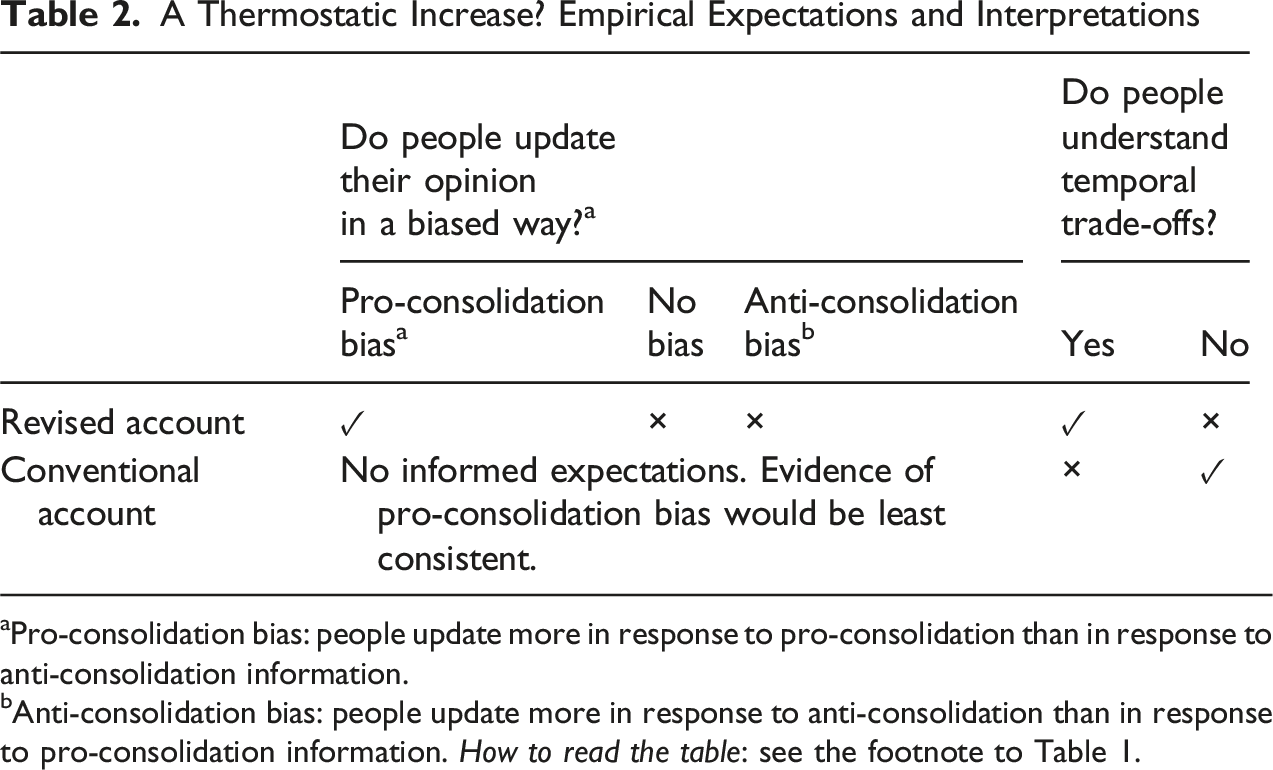

We consequently compare and contrast the consequences of both pro- and anti-consolidation information on strong support for fiscal consolidation. For inspiration, we turn to Zaller’s work on opinion formation. As Zaller (1992) famously argued, exposure to elite rhetoric does not have a deterministic impact on opinions: people exposed to discursive statements will “accept” some and “resist” others. In other words, an increase in the share of the population that prioritizes fiscal consolidation over competing goals requires a combination of (1) higher rates of exposure to pro-consolidation claims and (2) “resistance” to anti-consolidation claims. Given this study’s emphasis on mass opinions (and not elite behavior that could explain variation in exposure), we focus on testing the resistance mechanism. Specifically, we examine whether, relative to pro-consolidation messaging pointing to unsustainable debt levels, anti-consolidation messaging emphasizing sustainable debt levels is less likely to affect people’s opinions toward fiscal consolidation. We call this mechanism a pro-consolidation persuasion bias (DeMarzo et al., 2003).

Evidence of a pro-consolidation persuasion bias would, in line with the revised account, suggest that growing support for fiscal consolidation is more than a reflection of elite consensus on this issue: it is also shaped by individual-level resistance to anti-consolidation information. This resistance, in turn, contributes to a positive feedback loop between mass preferences and pro-consolidation elite consensus. Conversely, evidence of the opposite bias (i.e., more opinion change in response to anti-consolidation information than in response to pro-consolidation information) would seriously weaken the revised account. While less damaging, evidence of no persuasion bias (both types of information trigger opinion change) would still weaken this account, as it suggests that people are easily swayed by both pro- and anti-consolidation informational narratives and that elites—and what they choose to say about the national debt—rather than voters, are doing most of the heavy lifting.

A Thermostatic Increase? Empirical Expectations and Interpretations

aPro-consolidation bias: people update more in response to pro-consolidation than in response to anti-consolidation information.

bAnti-consolidation bias: people update more in response to anti-consolidation than in response to pro-consolidation information. How to read the table: see the footnote to Table 1.

Rising Awareness and Declining Uncertainty: Fiscal Illusion No More?

As previously discussed, underpinning the conventional account is the assumption that voters struggle to accurately evaluate the long-term effects of public finance policy choices such as delaying or prioritizing fiscal consolidation. In contrast, the revised account assumes that, as debt levels increase, so does voters’ ability to engage in intertemporal rational economic thinking, thanks in part to more information about the country’s fiscal conditions and the salience of this issue. We consequently examine how voters make sense of public debt. Specifically, we investigate the existence of two simple mental models, whose existence underpins disagreements between the conventional and revised accounts.

One is an accounting model that ties more unsustainable debt today to a higher likelihood of tax increases and spending cuts tomorrow. 5 According to the conventional account, it is the absence of this accounting mental model that explains debt buildup: citizens struggle with intertemporal trade-offs and are too myopic to form expectations about future tax increases (Jacobs, 2011). Proof that they do form such expectations would provide evidence against the assumptions underpinning the conventional account.

A second important mental model, advanced by orthodox macroeconomists, links unsustainable public debt to weaker growth and higher inflation. According to this macroeconomic model, elevated debt raises the risk of destabilizing sovereign-debt and financial crises and can crowd out productive private investment (Cochrane, 2020; Reinhart & Rogoff, 2009). Following a stripped-down version of monetary theory, experts also worry that authorities will seek to inflate away the debt, at the cost of higher inflation (Coibion et al., 2021). One might plausibly expect such arguments to be too complex for ordinary voters, something we might call the macroeconomic illusion. Yet, since the Great Recession, debt reduction has been a particularly salient issue in advanced economies, giving the public ample opportunities and time to learn about debt and fiscal issues. Evidence of a macroeconomic mental model among at least some voters would be additional evidence that learning about the consequences of debt unsustainability does take place in high-debt contexts. This evidence would weaken the conventional account, which assumes that people do not understand the long-term consequences of unsustainable debt. Table 2 (right column) summarizes these expectations.

Data and Empirical Strategy

To examine the demand side of fiscal consolidation in times of fiscal stress, we rely on observational and experimental survey data collected in Great Britain. We focus on Great Britain for several reasons. First, in Great Britain, popular support for fiscal discipline is already well documented (Barnes & Hicks, 2021, 2022). Based on evidence collected in the context of this study, only 9.5 percent of British respondents disagree that “debt is a serious issue”, against 13 percent in Germany and 23 percent in the Netherlands (Appendix A.1). Second, over the past three decades, successive governments have repeatedly signaled their commitment to fiscal consolidation. Up until the Great Recession, Great Britain’s record in keeping its public debt at a sustainable level was mostly on par with that of Germany, which is often considered the paragon of fiscal conservatism. In response to fiscal imbalances triggered by the Global Financial Crisis, the government sought to limit borrowing by implementing extensive austerity measures. Third, despite the fact that people exposed to cuts were more likely to vote for Brexit (Fetzer, 2019), there is no indication that the Conservatives have faced durable electoral backlash for the austerity measures they enacted. Furthermore, with the exception of Jeremy Corbyn’s tenure as party leader, the Labour Party has made fiscal consolidation an important element of its political strategy, and successive leaders cited electoral reasons for this decision. Evidence consistent with broad support for fiscal discipline among both elites and the masses makes Great Britain an ideal case for investigating the strength of this support and the need to revise the conventional account.

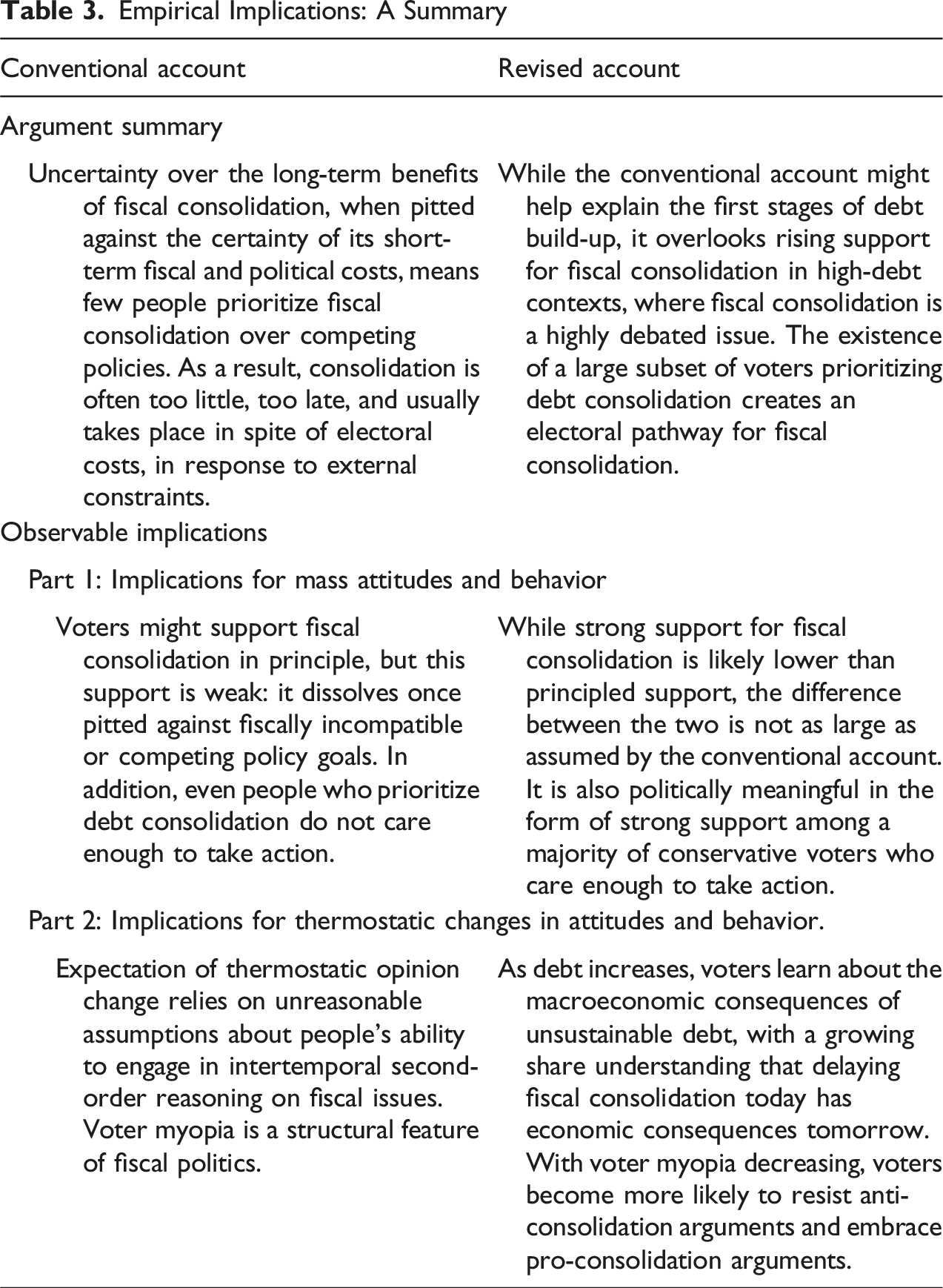

Empirical Implications: A Summary

Respondents from both Survey 1 and 2 were recruited through the survey firm Kantar. For Survey 1, a sample of 2,018 was recruited from Kantar’s online access panel in the UK. For Survey 2, the sample size was 2,124. For both surveys, we focused exclusively on respondents living in Great Britain (excluding Northern Ireland) who were eligible to vote. Samples for both surveys match the general population on age, gender, and education. Data collection and the subsequent analyses were pre-registered and received IRB approval. 7

Who Cares About Debt Consolidation?

Echoing previous research, the descriptive evidence collected in Survey 1 shows that a majority of respondents support fiscal consolidation in principle. Specifically, 61 percent think it is either “completely necessary” or “important but not completely necessary” to “eliminate the deficit” (Appendix C.1, Figure C.1). A similar share (65 percent) thinks that it is necessary or important to reduce public debt. In total, 67 percent of respondents believe that debt “is a serious problem”, while 15 percent believe that “it is not a serious problem” and 18 percent are “uncertain what to think” (Appendix C.2, Figure C.2). These numbers are comparable to those found for other benchmark issues asked about in the survey including climate change (78 percent think it is a serious problem), illegal immigration (67 percent), or the rise of China (72 percent). Comparing across issues, we find that only 4 percent of respondents evaluate Great Britain’s level of public debt as less serious than all the other three issues, while 14 percent perceive it as more serious than all the other three issues (Appendix C.2, Table C.1). We also asked respondents if “reducing Britain’s government debt” is an issue that is “personally important” to them. While 49 percent say it is “not important at all” or “not that important,” 51 percent answer that it is “somewhat important” (40 percent) or “very important” (11 percent, see Appendix C.1, Figure C.1).

Based on this evidence, it appears that a majority of respondents worry about their country’s finances and support fiscal consolidation in principle. But how many care enough to prioritize fiscal consolidation and compromise over other competing goals? Furthermore, is this share large enough to cast doubt on the conventional account? To answer these questions, we use measurement strategies where expressing support for fiscal consolidation involves a cost. 8 We examine responses in the aggregate and describe differences between voters of the two main British parties—the Conservatives and the Labour Party. 9 Unless stated otherwise, we present evidence from Survey 1 and focus on respondents in the control group, who were not exposed to video manipulations. Survey 2 results are available in Appendix C. Despite the high-inflation context, these do not differ substantively from Survey 1 results. In Appendix B.1, we address potential concerns regarding our reliance on quota-based sampling for descriptive inference.

Debt Consolidation as Something Worth Compromising for

We first rely on a set of binary forced-choice items pitting deficit and debt reduction against other competing policy goals. 10 Two items, which pit fiscal consolidation against government spending to improve the NHS and to fight climate change, speak to trade-offs induced by the budget constraint. A third item focuses on the political agenda constraint: it forces respondents to choose between prioritizing debt consolidation and prioritizing the “fight” against “irregular” immigration, a policy issue that has been highly politicized in Great Britain in recent years.

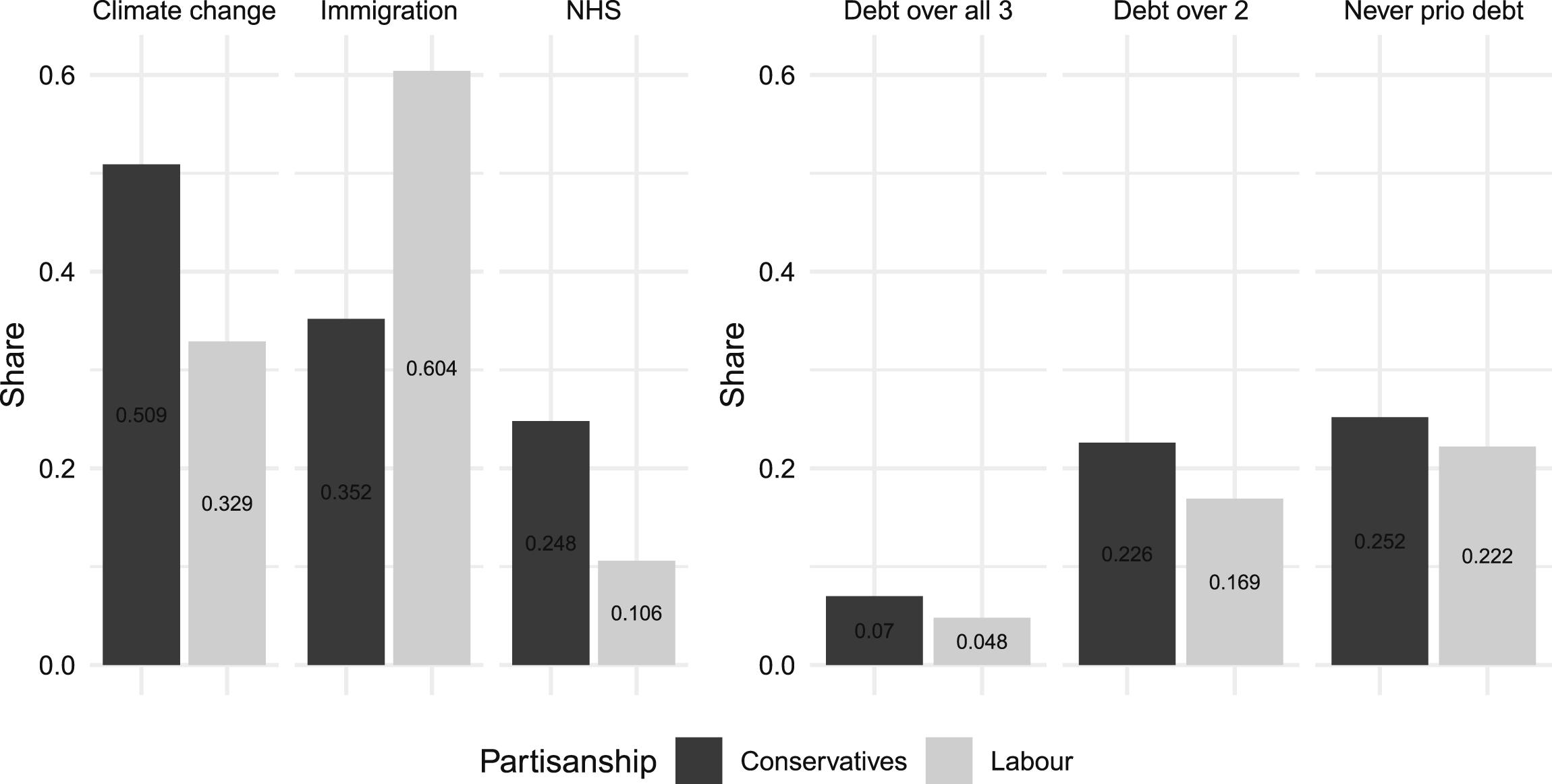

Figure 2 (left panel) shows results for each of the three trade-off items broken down by partisanship. Less than a fifth of respondents support debt reduction over the NHS, and Conservative supporters (25 percent) are more than twice as likely to do so as Labour supporters (11 percent). Labour supporters strongly prioritize fighting climate change: more than two-thirds of Labour sympathizers prioritize this policy goal over debt consolidation. The only instance in which a majority (60 percent) of Labour Party supporters prioritize debt over something else is in the case of immigration. For Conservative voters, we find the opposite pattern: they prioritize immigration over debt but prioritize debt over climate change. In Survey 2, we added a fourth survey item that pits debt reduction against income support for those adversely affected by inflation. The results—shown in Appendix C.3, Figure C.3—indicate that Labour supporters overwhelmingly prioritize income transfers (80 percent) over debt reduction. In contrast, Conservatives are more divided: 56 percent prioritize income support over debt reduction, while 44 percent have the opposite preference ranking. Share of respondents who prioritize debt over competing issues. Note. Control group only, Survey 1. Item wording: “Which issue should the government prioritize: reduce the deficit and public debt OR [example] tackle climate change?”

Based on these binary items, between 18 and 33 percent of respondents prioritize debt reduction above spending that directly benefits British citizens (NHS and inflation-related income support). Large partisan differences emerge when debt reduction is pitted against policy goals associated with the opposite party (immigration for Labour and climate change for Conservatives), suggesting that respondents are signaling strong opposition to these policy goals more than strong support for debt consolidation. When combined, answers collected in Survey 1 indicate that very few respondents prioritize debt in all three trade-offs, as shown in Figure 2 (right panel). Around 22 percent of Labour supporters and 30 percent of Conservatives prioritize debt over at least two issues, which is only slightly larger than the share that never prioritizes debt (22 and 25 percent, respectively). Overall, these patterns remain mostly the same when we include the measure that pits debt reduction against income support in Survey 2 (see Appendix C.3, Figure C.3). To sum up, per this measurement strategy, less than a third of respondents care enough about debt consolidation to prioritize it over important policy goals. Because these respondents are not concentrated in a particular party, their influence within a voting bloc is not larger than their weight in the overall population.

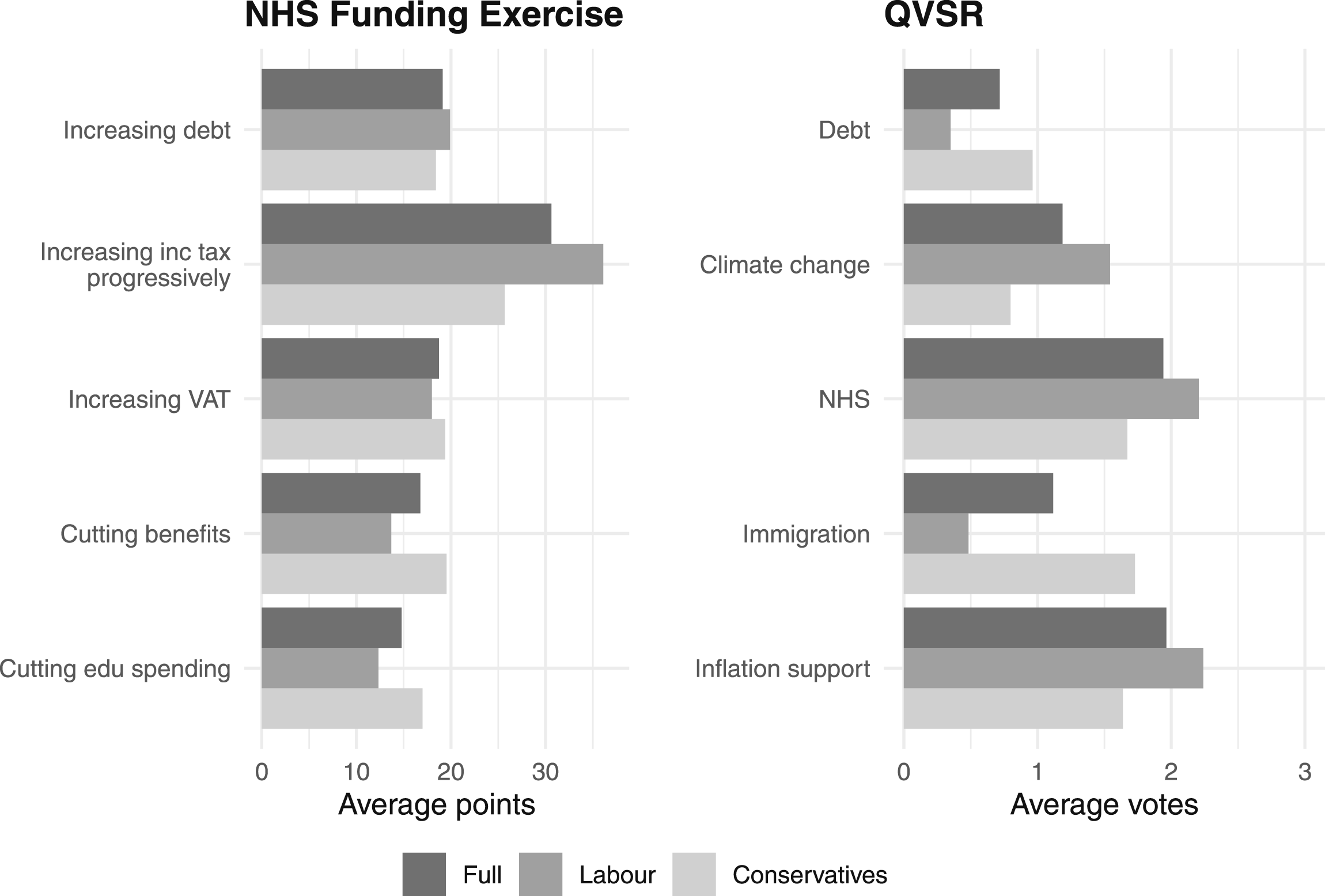

In practice, however, governments do not face simple binary choices. Fiscal policymaking entails complex trade-offs across multiple policy areas. What happens once we compel voters to think beyond a binary choice set and jointly consider a larger set of trade-offs? To answer this question, we rely on measurement strategies involving multidimensional trade-offs. First, we asked respondents about their preferred ways of raising funds for the NHS. We use the NHS because it is a chronically underfunded public service that most people living in the UK rely on. Respondents had 100 points to distribute across the five revenue-raising options, namely a debt increase, spending cuts on education, spending cuts on social security (welfare), progressive taxation, and an increase in value added tax (VAT). As a starting point, each of the five options is allocated 20 points (out of 100) of the total funds to be raised, and respondents could choose to increase or decrease this share.

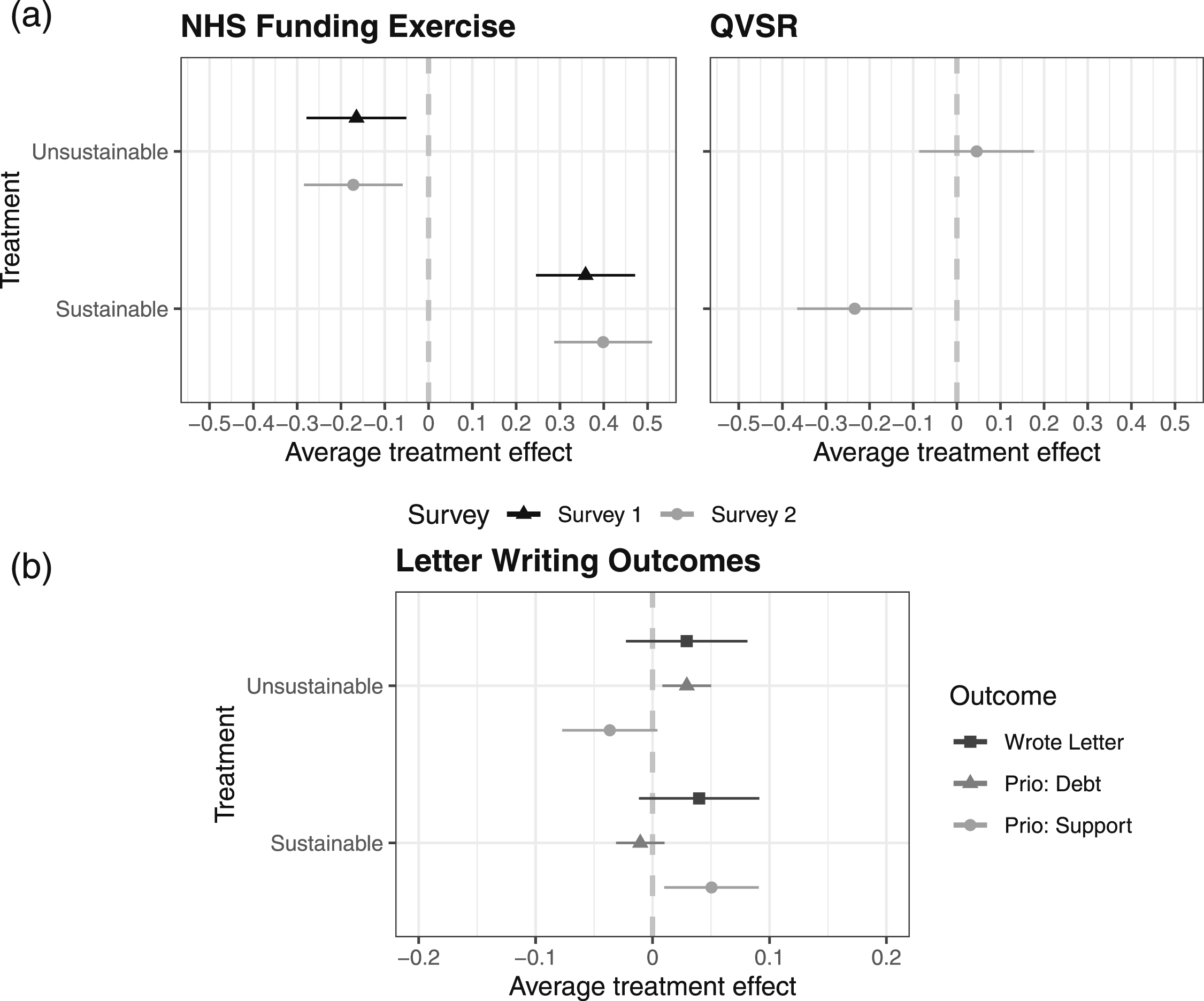

As shown in Figure 3 (left panel), increasing debt is the second most popular way to raise funds for the NHS overall. Partisan differences are limited, with Labour supporters allocating 19.9 points to debt financing, while Conservative Party supporters allocate 18.4 points. Increasing income tax on higher-income individuals is the most favored option (30.6 points), something that applies to both Labour and Conservative supporters. Among Labour supporters, increasing debt is more popular than increasing VAT and much more popular than cutting welfare benefits or education spending. For Conservative supporters, increasing VAT and cutting benefits is still slightly more popular than increasing government debt, but they prefer debt financing over cuts in education spending. These preferences remain mostly unchanged in a high-inflation context (Survey 2), except that now, debt financing is marginally more popular than before (Appendix C.4, Figure C.5). On average, Survey 2 respondents allocate 20.4 points to debt financing, where it is the second most preferred option to fund the NHS, even among Conservatives. Average points or votes allocated to different fiscal policies in budgetary tasks. Note. Control group only, Survey 1 for the NHS funding exercise, Survey 2, Wave 2 for QVSR.

In Survey 2, Wave 2, we further explored how people deal with trade-offs induced by both fiscal constraints and the political agenda. Specifically, we replaced the NHS funding exercise with a second measurement strategy—Quadratic Voting for Survey Research (QVSR)—that gives respondents a fixed budget to buy “support” or “oppose” votes, with the price for each vote increasing quadratically (1 vote costs 1 credit, 2 votes cost 4 credits, 3 votes cost 9 credits, etc.). This combination of a budget constraint and quadratic pricing means that expressing intense support or opposition to a given policy goal (by casting more than one vote) comes at the expense of expressing one’s preference on other issues. As a result, respondents have to choose which subset of issues to focus their credits on, providing a proxy measure of how much people want to see this issue prioritized, given agenda and fiscal constraints (Cavaillé et al., 2025). In Wave 2, respondents were given 25 credits to vote on five different issues that governments can address, namely reducing government debt, addressing climate change, investing in the NHS, reforming immigration and border control, and providing inflation support.

As shown in Appendix C.5, Figure C.6, debt consolidation is the least prioritized policy issue, receiving fewer votes (be they in favor or against) than all other policy issues. Figure 3 (right panel) plots the average of the sum of both positive votes (votes in favor) and negative votes (votes against). This captures the relative difference in the number of votes cast between people in favor and people against. While the number of votes in favor of consolidation is larger than the number of votes against (i.e., the average is positive), the intensity of net support for consolidation is dwarfed by that found for the NHS or income support. In other words, the intensity of support for more NHS spending is much larger than that of support for debt consolidation, especially among Labour voters. In Appendix C.5, we further decompose these differences by measuring the share of respondents who strongly favor a given policy issue. Specifically, we create an indicator variable—one for each policy issue—that captures the share of respondents who both favor an issue (i.e., cast a positive number of votes) and prioritize it (i.e., spend the most credits on this issue). 11 As Appendix C.5, Figure C.7 shows, this analysis reveals that only 14.6 percent of respondents strongly prioritize debt consolidation, with a partisan divide (9.7 percent of Labour voters versus 19.2 percent of Conservative voters). In contrast, NHS funding receives strong support from 43.5 percent of respondents (49.6 percent of Labour voters and 35.5 percent of Conservative voters), with similar patterns for income support in times of rising inflation. The starkest partisan difference exists on immigration control, where 39.3 percent of Conservative voters prioritize this issue compared to only 10.9 percent of Labour voters. These findings demonstrate that debt consolidation is a low priority for the vast majority of voters, with fewer than 1 in 7 respondents strongly supporting it. Under QVSR, partisan differences, while larger than with other measurement strategies, remain substantively limited.

Letter-Writing Exercise

Our final measurement strategy aims to better approximate real-world behavior. For this, we gave Survey 2 respondents the opportunity to contribute to a letter to the Chancellor of the Exchequer regarding the trade-off between balancing the budget and increasing spending to help people cope with inflation. Specifically, respondents were prompted to either advocate for more spending for income support or advocate for prioritizing debt consolidation. This came at the very end of Survey 2, Wave 1. Behavior on this letter-writing task enables us to move beyond stated fiscal priorities and examine whether respondents care enough about this issue to take the time to contribute to a letter. Appendix C.6 describes the procedure used to code respondents’ written contributions. 12 This coding procedure was not pre-registered.

Based on this analysis, only 4 percent of respondents wrote about the need for fiscal consolidation and/or in support of limiting government borrowing. The share that wrote about prioritizing more spending to help people cope with inflation is more than 4 times larger, at 18 percent, with low-income respondents more likely to belong to this group (see Appendix C.7, Figure C.8). In total, nearly 38 percent of respondents contributed, with an additional 3 percent writing too few words to enable interpretation. 13 In other words, pro-consolidation advocates represent around 11 percent of letter writers against 47 percent for pro-spending advocates (see Appendix C.7, Table C.3). Conditional on having contributed to the letter, around 15 percent of Conservative voters and 5 percent of Labour voters explicitly mentioned the need to prioritize the debt. For every supporter of the Conservative Party who wrote about the debt, there were 2.5 who explicitly mentioned in their contribution the need to spend more to support people struggling with inflation (39 percent). For every Labour supporter who wrote about the debt, 13 wrote to advocate for income support (60 percent). This more than tenfold difference for Labour supporters (versus 2.5 for supporters of the Conservative Party) reflects their stronger support for income support relative to debt consolidation, which is also captured when taking the ratio of average QVSR votes on debt and average votes for inflation support (Figure 3, right panel).

Depending on how we measure who cares about debt consolidation, we find a number that ranges from 4 percent (letter writing) to a third of respondents (binary items), with QVSR returning an intermediary value of 15 percent. At the group level, debt consolidation is the least preferred option (QVSR) while a debt increase is the second most preferred option (budgeting exercise). The share of people who strongly support more spending is 2 to 4 times larger than the share who prioritize fiscal consolidation (QVSR and letter writing). Partisan differences on this issue are limited, meaning that those who care about debt consolidation are a minority in both mainstream parties. These results strengthen the conventional account (see Table 1).

Examining Mechanisms that Foster Pro-Consolidation Opinion Shifts

Next, we examine mechanisms of opinion formation that can foster a thermostatic reaction to rising debt. Evidence in support of these mechanisms would strengthen the revised account by demonstrating that strong support can grow when fiscal stress becomes a salient issue. This, in turn, would suggest caution when interpreting the results presented in the previous section: minority status today need not imply minority status in the future.

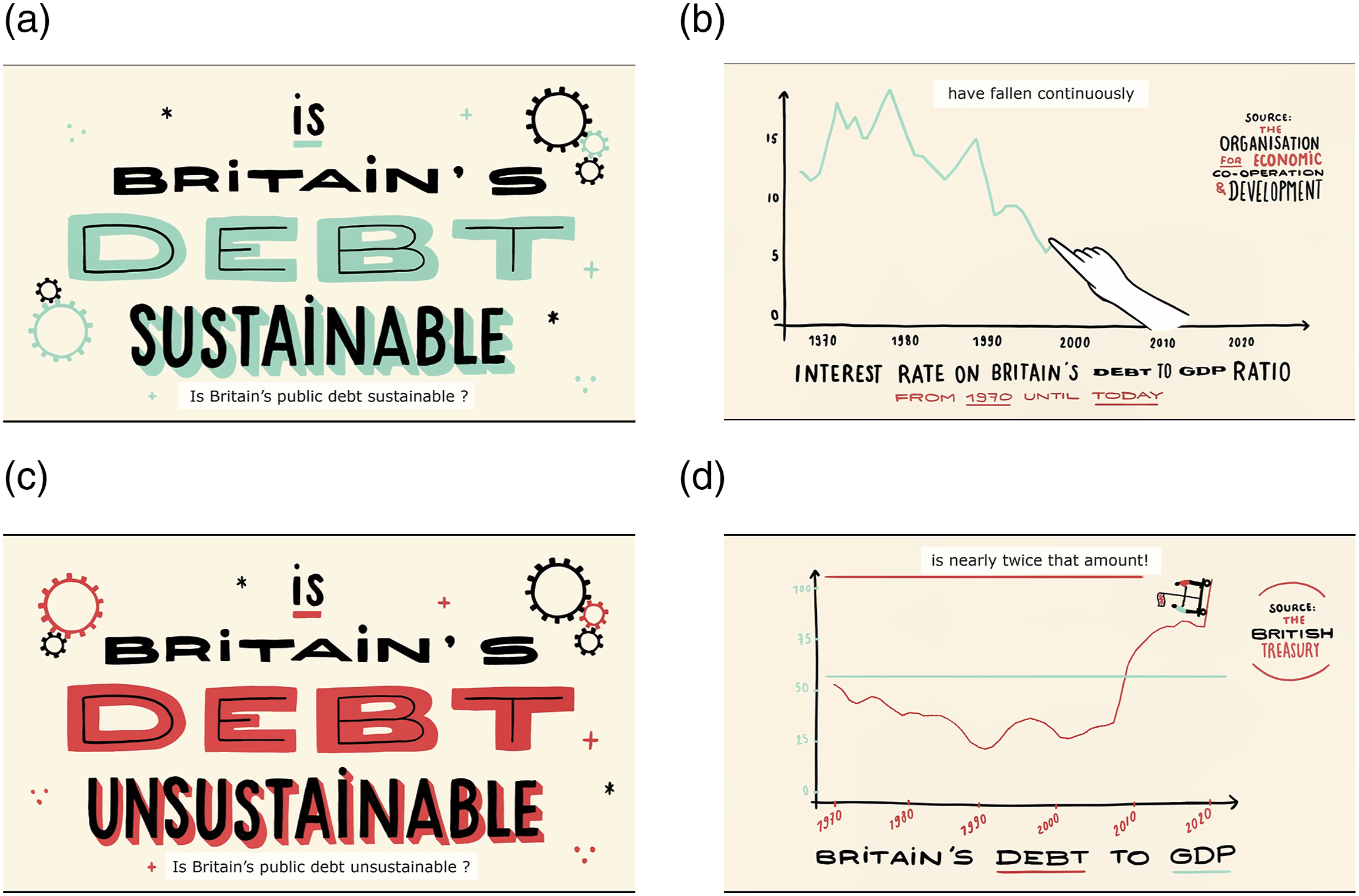

We focus on two types of cognitive mechanisms. One is a pro-consolidation persuasion bias, whereby people discount anti-consolidation information. The other is an understanding of intertemporal trade-offs sophisticated enough to suggest, against the conventional account, that people do internalize the long-term costs of high debt. To this end, we use a survey experiment in which we randomly assigned respondents to be exposed to either a pro- or an anti-debt consolidation narrative presented using animation videos. Each video explains one side of expert-driven debates over debt sustainability, one summarizing elite consensus over the country’s unsustainable debt trajectory (the unsustainable treatment)

14

and the other summarizing a dissenting view. This view, championed by economists such as Blanchard (2023), points to exceptionally low interest rates and declining debt-servicing costs as a structural feature of globalized economies, which makes debt sustainable and speaks against prioritizing fiscal consolidation (the sustainable treatment).

15

We described the animated videos to respondents as summarizing the state of the expert debate on “what existing levels of public debt imply for Great Britain.” Both videos start with the same introduction and define key concepts, such as deficit and public debt. The unsustainable video emphasizes the growing debt-to-GDP ratio and the resulting vulnerability to economic shocks. The sustainable video emphasizes the decline in borrowing costs, arguing that “Great Britain is (…) in a better position to borrow and pay back its debt today than it ever was in the past.” Respondents in the control group see no video. Screenshots of the videos are shown in Figure 4; for more information and exact treatment wordings, see Appendix A.5. These videos allow us to convey apolitical expert-based arguments and information about debt in a user-friendly way, ensuring treatment compliance, even on a complex issue such as debt sustainability.

16

Screenshots from the sustainable (upper row) and unsustainable video treatments (bottom row).

To check that the videos affected concern about government debt, we asked the question about the seriousness of public debt twice, once before the treatment and once after.

17

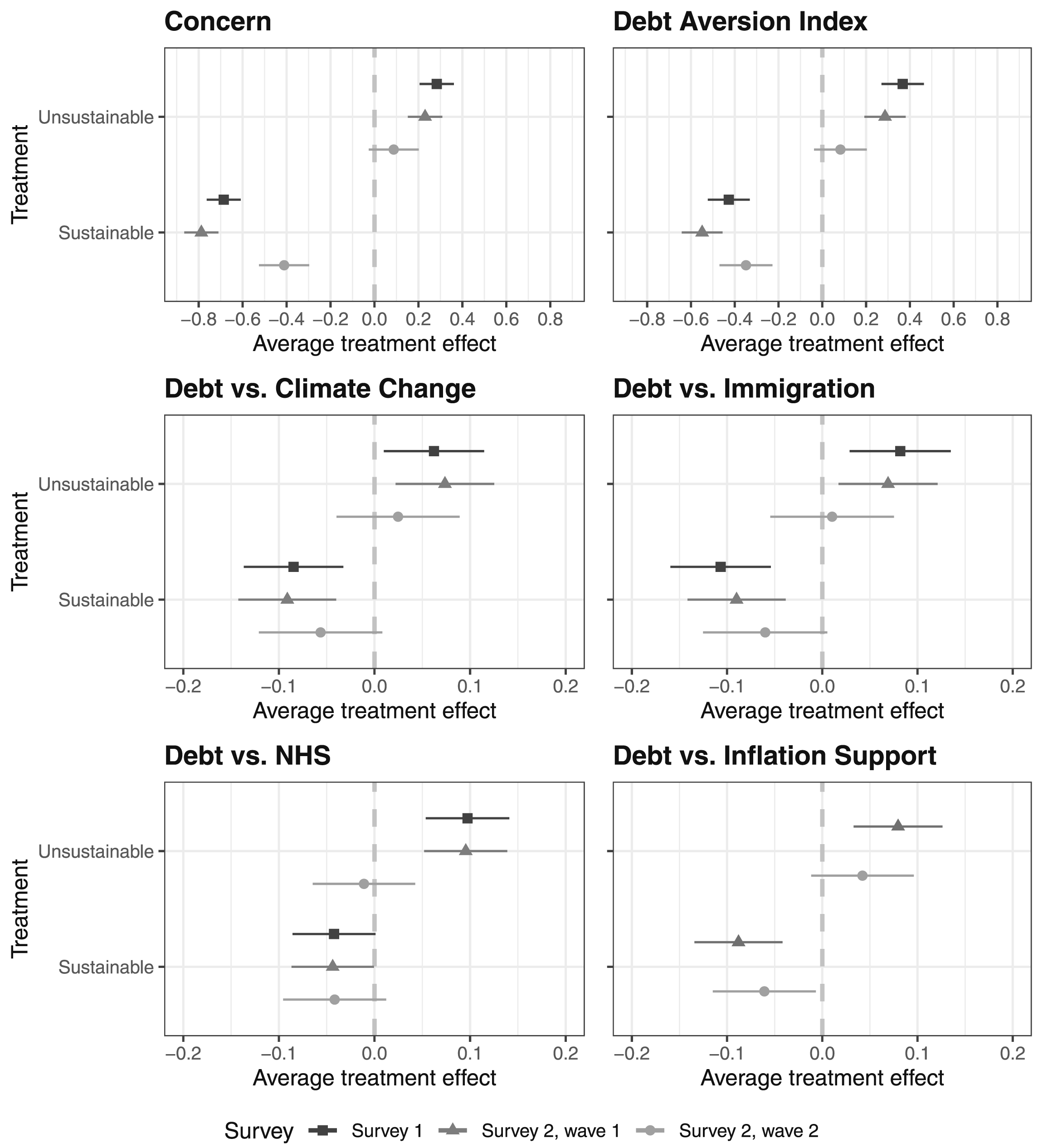

To limit priming effects, the question was included in a bloc of items asking not only about public debt but also about climate change, the rise of China, and illegal immigration. As shown in Figure 5 (top left panel), watching the videos affects perceptions of debt seriousness in the expected directions: less serious in the sustainable treatment and more serious in the unsustainable one. Effect sizes are similar in both surveys. As discussed in Appendix A.6, the vast majority of respondents understood the key message of both videos and rated their instructional qualities as high. Average treatment effects of video treatments on policy preferences and priorities. Note. The ATEs are estimated by regressing each outcome on the treatment dummies, controlling for pre-treatment answers to a question on the seriousness of the country’s level of public debt. Dependent variables in the top panel are z-standardized (mean = 0, standard deviation = 1), where higher values indicate that respondents are more concerned or more debt averse, respectively. Dependent variables in the middle and bottom panels are binary, where 1 indicates that respondents prioritize lowering debt. See Appendix D, Table D.1 for the corresponding regression table.

To assess ATEs beyond their immediate effect, we re-contacted Survey 2 respondents one month later (Survey 2, Wave 2) and asked the same outcome questions (with the exception of the NHS budgeting item, which was replaced with QVSR). As described in Appendix A.8, treatment assignment in Wave 1, the individual treatment effect on the perceived seriousness of debt, and the interaction between the two do not predict participation in Wave 2. The same holds for post-treatment policy preferences.

Are Some Narratives More Convincing Than Others?

To test for the existence of a persuasion bias, we compare the causal effects on policy preferences of pro- and anti-debt consolidation information, which we proxy using the unsustainable and sustainable videos described above.

We start with our unconstrained “cheap talk” measures of fiscal preferences. Specifically, we combine the two items asking about the necessity of decreasing the debt and balancing the budget with the item asking how important this issue is personally to the respondent, creating a “debt aversion index” (Cronbach’s α = 0.78). Figure 5 (top right panel) shows that changes in levels of concern about debt seriousness are reflected in the debt aversion index: respondents are less debt averse in the sustainable treatment, while the opposite is true for the unsustainable treatment. Specifically, in Survey 1, the sustainable treatment reduces debt aversion by 0.43 standard deviations (SD), while the unsustainable treatment increases it by 0.37 SD. Effect sizes are similar in Survey 2.

Does this pattern replicate once support for fiscal consolidation comes at a cost in the form of support for competing policies or exerting an effort to convey one’s opinion to the government? The answer is yes (see Figures 5 and 6), though most effect sizes are smaller than for unconstrained preferences. For the binary trade-off measures, the sustainable treatment decreases the likelihood that respondents prioritize debt over climate change mitigation by 8.5% points (0.17 SD), while the unsustainable treatment increases it by 6.2% points (0.13 SD) in Survey 1. Similar patterns emerge for NHS spending, migration control, and inflation support, and results are consistent across surveys 1 and 2. In the NHS funding exercise, respondents in the sustainable treatment allocate 4.9 (0.36 SD) more points (out of 100) to debt financing for NHS investment compared to the control group, while those in the unsustainable treatment allocate 2.3 (0.16 SD) fewer points in Survey 1. Again, the results are nearly the same in Survey 2, Wave 1. Average treatment effects of video treatments on prioritizing debt across budgetary tasks and letter writing outcomes. Note. ATEs in the top panel are estimated by regressing the number of points/votes allocated to debt in two survey exercises on treatment dummies. Dependent variables are z-standardized (mean = 0, standard deviation = 1). ATEs in the bottom panel are estimated by regressing binary outcomes from the letter-writing exercise on treatment dummies. Outcomes measure whether respondents wrote a letter and whether they prioritized lowering debt over income support in their letter. All regressions control for pre-treatment responses to a question about the seriousness of the country’s public debt level. See Appendix D, Table D.2 for the corresponding regression table.

In Survey 2, we also find that the treatment affects letter-writing behavior. While watching either video does not affect the likelihood that people contribute to the letter, respondents exposed to the sustainable video are 6% points more likely to write about income support than people in the control group (17 vs. 23 percent). People exposed to the unsustainable video, in turn, are around 3% points more likely to write about prioritizing debt relative to people in the control condition (3 vs. 6 percent). After watching the sustainable video, and conditional on contributing to the letter, 57 percent of respondents write about income support, while 6 percent write about debt reduction. After watching the unsustainable video, the shares are 36 and 17 percent, respectively (see Appendix D, Table D.3).

One month after watching the video, differences between treatment and control remain significant for those who watched the sustainable video (see Figure 5 and the QVSR analysis in Figure 6). Moreover, in the QVSR exercise, people in the sustainable treatment group, on average, allocate fewer credits to reducing government debt than people in the control group, even though this exercise was only included in Survey 2, Wave 2. This is not the case for the unsustainable video. Still, given overlapping confidence intervals, we cannot reject the null that one month after treatment, absolute effect sizes are the same in the sustainable and unsustainable conditions.

Overall, we find no evidence that people are more persuaded by the pro-consolidation argument. Instead, people update in similar ways in response to both types of information, suggesting no bias, 18 which weakens the revised account and is consistent with the conventional account (see Table 1, left column). 19

Fiscal Illusion No More?

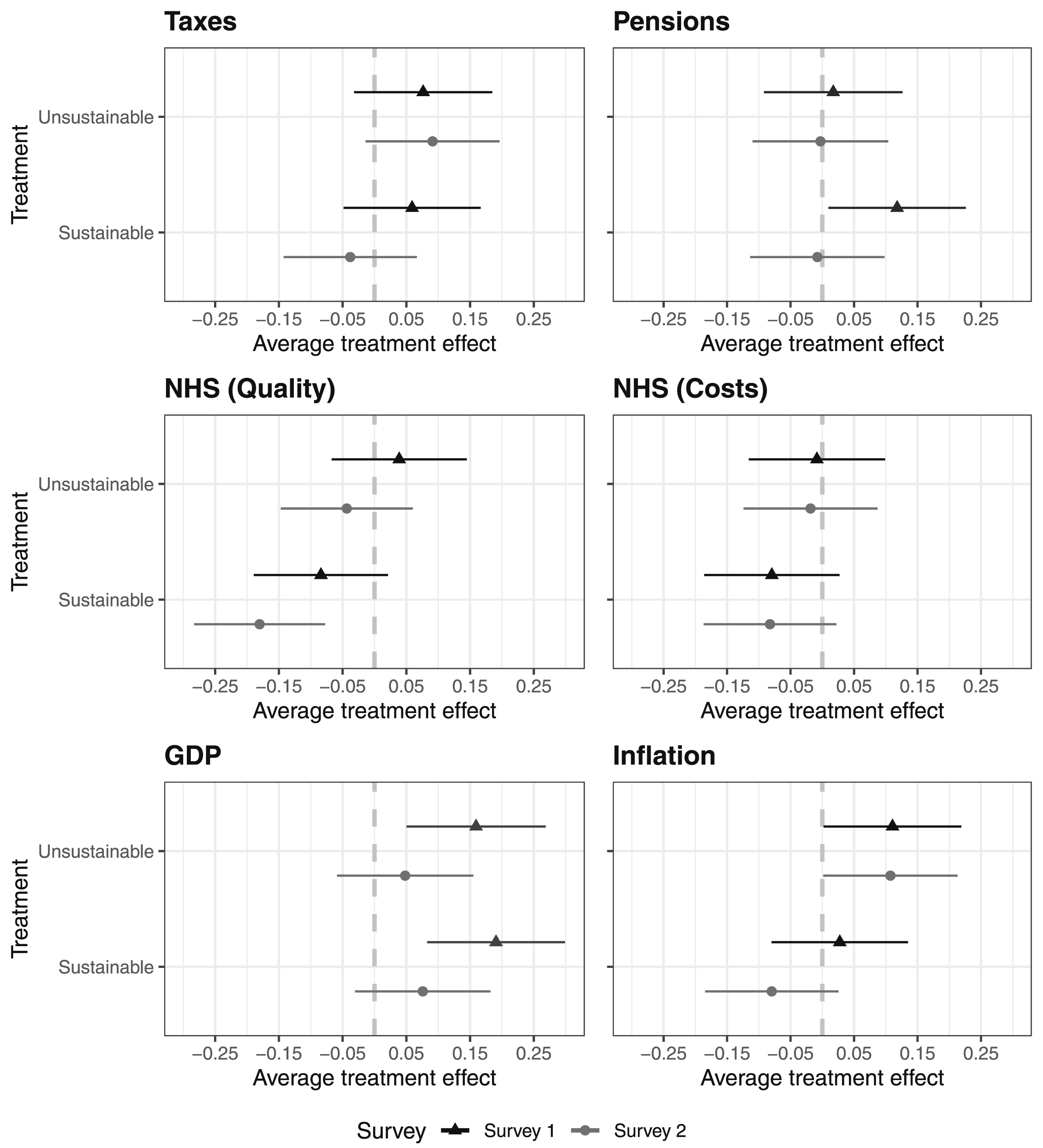

The revised account assumes that people have some minimal understanding of the consequences of high and unsustainable debt levels. We probe two types of understanding. First, if British respondents rely on an accounting model, they should connect a change in debt sustainability to future threats of tax increases and/or spending cuts. We consequently ask respondents about their expectations regarding the average tax rate and the quality and costs of services provided by the NHS. Assuming they rely on a macroeconomic model, they should connect a change in debt sustainability to future economic downturns. We measure expectations about the future state of the economy in two ways: first, in the form of a question about future GDP growth, and second, in the form of a question about rates of return to private pensions. We included this latter item because most British voters have an asset-backed pension plan, with defined-contribution plans being the norm. To the extent that they expect poor economic performance, this should affect pension return expectations. Finally, we ask respondents about their inflation expectations, as the unsustainable treatment should lead them to anticipate higher inflation. 20

Figure 7 plots the videos’ ATEs on fiscal and economic expectations. In both surveys, expectations do not differ markedly across treatment conditions. The unsustainable treatment has a small positive effect on inflation expectations, which would be in line with the macroeconomic mental model. Surprisingly, in Survey 1, exposure to both treatments improves expectations about future GDP, but this effect does not replicate in Survey 2. Additionally, in Survey 1, respondents exposed to the sustainable video are more likely to have positive expectations regarding pension returns, an effect that does not replicate in Survey 2. Counterintuitively, we also find a significant negative effect of the sustainable treatment on NHS quality expectations in Survey 2, but this effect does not exist in Survey 1. For all other Survey 1 outcomes, we cannot reject the null that the treatments did not affect expectations. These null results extend to Survey 2 data, with one exception: respondents exposed to the sustainable video are more likely to have positive expectations regarding pension returns, an effect that does not exist in Survey 1. Average treatment effects on expectations. Note. ATEs are estimated by regressing each expectation outcome on the treatment dummies, controlling for pre-treatment answers to the question on the seriousness of the country’s level of public debt. Dependent variables are z-standardized (mean = 0, standard deviation = 1). See Appendix E, Table E.1 for the corresponding regression tables.

The disconnect between information about debt and people’s fiscal and economic expectations can be interpreted in at least two ways. One interpretation is that voters have no understanding of the government’s budget constraint and do not think like orthodox macroeconomists. The second interpretation, implicit in the conventional account, is that voters understand that the future is shaped by both current fiscal imbalances and policymakers’ reactions to them. Given that the latter is unknown, making any predictions is difficult and depends on people’s beliefs about future government action (Jacobs, 2011; Jacobs & Matthews, 2012). Regardless of which interpretation is correct, the conclusion is unchanged: whether due to misunderstanding or uncertainty, people do not use mental models that connect unsustainable debt with negative economic consequences in the mid- to long-run. In other words, our evidence strengthens the conventional account by providing evidence that people systematically underestimate the future costs of unsustainable government spending.

Heterogeneity Analyses and Robustness Checks

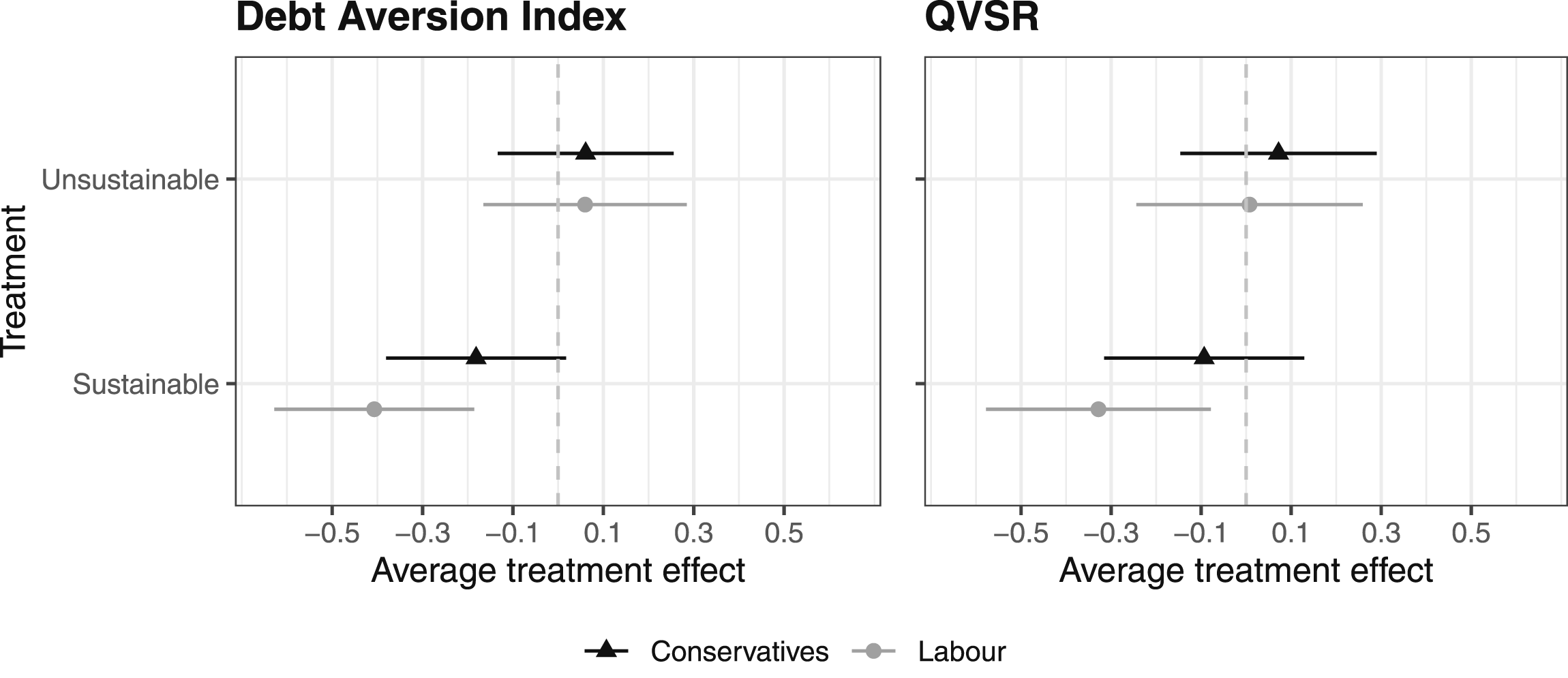

Do treatment effects vary across individuals in informative ways? Regarding partisanship, Labour and Conservative supporters generally respond to our video treatments in similar ways, at least in the short-run (see Appendix F.1). As shown in Figure 8, we find tentative evidence of partisan differences with regard to persistence, though these appear limited to the sustainable treatment. While the lasting effect of watching the sustainable video four weeks after treatment (Survey 2, Wave 2) is only statistically significant for Labour supporters, the overlap in confidence intervals means we cannot conclude with confidence that treatment decay is slower for Labour supporters. Based on these tentative results, follow-up research might investigate the existence of an anti-consolidation bias among left-wing respondents in particular. Heterogeneous treatment effects of video treatments on preferences and priorities four weeks after treatment (Survey 2, Wave 2). Note. The HTEs are estimated by regressing each outcome on an interaction of the treatment dummies and a variable measuring partisanship, controlling for pre-treatment answers to a question on the seriousness of the country’s level of public debt. Dependent variables are z-standardized (mean = 0, standard deviation = 1).

Beyond partisanship, we find no evidence that treatment effects vary with education (Appendix F.2), income (Appendix F.3), and age (Appendix F.4). Given that fiscal policy has redistributive implications across birth cohorts and income categories, these results are noteworthy. Appendix F.5 expands on this analysis by testing for the existence of age and income differences that might suggest a latent economic and/or generational divide on fiscal issues (Aspide et al., 2023). Overall, this correlational analysis shows no meaningful income gradient and only a modest age gradient.

We also conduct several robustness tests. First, a placebo test shows that the videos did not affect respondents’ concern over the rise of China (Appendix G.1, Figure G.1). We also examine possible ceiling effects that may reduce the impact of the unsustainable treatment, meaning that our design could be biased against finding evidence of a pro-consolidation bias. For this, we focus on respondents who, pre-treatment, had “middle-of-the-road levels of concerns,” meaning they could easily be pulled in either a high- or low-concern direction. Given that prior research shows that people with a formed opinion on an issue are more likely to resist contradictory messaging (Zaller, 1992), we also examine ATEs for respondents who, pre-treatment, perceived debt as a serious issue and were certain of their opinion. For both groups, similarly-sized ATEs suggest that respondents do not find the sustainable treatment less convincing than the unsustainable one (Appendix G.2, Figure G.2). We also find no evidence that respondents who are certain about their opinion on public debt before treatment are more likely to resist the sustainable treatment.

Relatedly, differences across treatment conditions could be attributed to how we designed the videos, unwittingly making one more convincing than the other. As we describe in Appendix A.4, we worked with a professional designer to make the videos as comparable as possible in terms of their length, design, graphics, official statistics, and the number of arguments and pieces of information presented. Respondents, on balance, rated the quality of the videos similarly across treatment groups (Appendix A.5). Still, novelty could bias the sustainable ATEs upward: less used to hearing more optimistic arguments about debt, respondents may pay more attention to the sustainable treatment. As a result, they might be more likely to update their preferences in line with that treatment, which could explain why these effects still exist up to one month after exposure. This possible novelty effect, however, is not a design flaw per se but a result of the British context in which there is elite consensus over the need to balance the books. Why this consensus? Our results suggest that voters are unlikely “culprits” as we fail to document any fundamental resistance on the part of voters to the anti-consolidation narrative.

Finally, while we show that respondents update in response to the sustainable treatment in a survey setting, this may still leave open the possibility of self-selection in real life. If people are more likely to seek out information that aligns with the unsustainable rather than sustainable narrative, this could still help tilt the discursive environment in favor of a pro-consolidation narrative. In our study, respondents were not given a choice between the two videos, and we did not allow them to skip the videos. In Survey 2, however, we asked respondents in the control group (who had not watched any video) if they were interested in watching one of the two videos, which we briefly described. If they chose one, then a link to the appropriate video appeared for them to click on at the end of the survey. The share of people who asked to watch the unsustainable video was higher than the share who asked to watch the sustainable one (43 versus 33 percent, see Appendix G.3, Figure G.3), but those who clicked on the link spent more time watching the unsustainable video than the sustainable one (see Figure G.4). In other words, we find no clear evidence that respondents sought out one type of information more than another.

Conclusion

In the face of rising debt, is there space for pro-consolidation politicians to leverage well-documented widespread debt concern in line with the revised account, or can we expect voters to ultimately balk at the short-term costs of consolidation in line with the conventional account? To address this question, we considered the following three sub-questions: “Do ‘enough' people care about debt consolidation to accept the possible policy trade-offs?”, “Do people dislike high debt enough to resist arguments that justify de-prioritizing it?”, and “Do people understand the consequences of unsustainable debt well enough to form conservative fiscal policy preferences in response to a deteriorating environment?”

Evidence from Great Britain provides a negative answer to all three questions. First, only a plurality of voters prioritizes the benefits of fiscal consolidation over competing policy goals; this is true for both Labour Party and Conservative Party supporters. Second, people, especially Labour sympathizers, do not resist updating their preferences when presented with plausible information that portrays debt as sustainable. Third, people do not hold mental models that would turn them into fiscal conservatives, even in a high-debt context, when debt is presented as unsustainable. Overall, we find no reason to revise the conventional account of fiscal politics, which argues that voters, because they fail to internalize the future costs of rising sovereign debt, more strongly oppose fiscal consolidation’s short-term cost than they support its long-term benefits. This asymmetry makes it difficult for politicians to campaign on fiscal discipline.

Our results also suggest caution when interpreting attitudinal surveys documenting concerns about high sovereign debt and support for debt consolidation. While many people support debt consolidation in principle, fewer prioritize it in the face of fiscal and political trade-offs. As a result, support for fiscal consolidation is hard to gauge without reference to specific consolidation packages. One study addresses this issue by measuring support for actual consolidation packages implemented in the wake of the Great Recession (Bansak et al., 2021). It finds that, in many countries, a (thin) majority supports these measures. Still, our results suggest that these consolidation packages were likely timed strategically (Hübscher & Sattler, 2017) and designed to leverage principled support without triggering a backlash among the government’s own voting base (Patashnik, 2023). Such a compromise approach is unlikely to address structural imbalances, meaning that the main insight of the conventional approach to fiscal policy still holds: in electoral democracies, fiscal consolidation tends to be too little and too late relative to what orthodox fiscal principles would prescribe.

Under what conditions then might people perceive delaying fiscal consolidation as a direct threat to their pocketbook and thus worth prioritizing (i.e., small pain today to avoid larger pain tomorrow)? One possibility is that our treatment was too general: while people struggle to understand the implications of debt and deficits as a whole, they might have an easier time when fiscal stress is discussed for its implications with regard to specific programs or public goods such as education, healthcare, or public pensions. Another possibility is that such perceptions tend to come “too late,” once the country is gripped by a debt crisis in the form of capital flight, IMF intervention, and sharp spending cuts that directly affect people’s pocketbook. We leave it to future research to explore these lines of inquiry. A third possibility is that our results are specific to the post-COVID, high-inflation context that put short-term costs of living concerns (and thus the consumption value of public spending and income support) at the forefront of respondents’ minds. In such a context, documenting strong and growing support for a policy with immediate short-term material costs might be more difficult. This means that support for prioritizing fiscal consolidation might be larger in “good times.” While this might be the case, the timing of our study remains substantively meaningful. In high-income countries with high debt, the central issue is not the debt level itself but its sustainability. Concerns about debt sustainability tend to intensify when tax revenues weaken—typically during periods of low or negative GDP growth, when dependence on public spending is also highest. In other words, fiscal consolidation becomes most politically salient precisely in the kind of economic environment that followed the COVID-19 pandemic, which underscores the relevance of our findings.

Based on our findings, politicians who propose policies funded through deficits and debt are unlikely to face pushback from voters. The short-lived premiership of Liz Truss in Great Britain in 2022 is informative in this regard. In the midst of global economic turmoil due to rising inflation, energy supply issues, and the war in Ukraine, British Prime Minister Liz Truss presented budget plans that would have significantly increased government borrowing. In line with our findings, even dues-paying members of the Conservative Party—a group we might expect a priori to be most committed to fiscally conservative policies—expressed few concerns about deficits and debt. This budget sent bond markets into a tailspin, forcing Liz Truss to step down and increasing the prevalence of information on the country’s unsustainable level of debt. Based on our findings, exposure to such information should increase principled support for debt consolidation. Still, we find no evidence that people engage in the type of economic thinking that could turn principled support into strong support tied to pocketbook concerns about future taxes, future spending cuts, or higher inflation and lower growth. Assuming future studies successfully demonstrate that similar episodes significantly increase strong support for fiscal consolidation, the determinants of this support remain to be identified. More importantly, our evidence that persuasion is the same for anti-consolidation messaging suggests that attitudinal change is endogenous to elite dynamics, not a determinant of the latter.

In light of our results, the relative scarcity of politicians willing to break with fiscal orthodoxy is puzzling. We find that left-wing voters in particular are open to informational narratives that de-prioritize debt concerns. Why then is the Labour Party so reluctant to deviate from fiscal orthodoxy? One hypothesis is that Labour elites avoid doing so out of concern that they would lose some voters to the Conservative Party. Our evidence suggests that only a small group of Labour voters in our sample fit this profile. Another hypothesis is that non-electoral factors explain bipartisan fiscal restraint. In the case of the Truss government, restraint was seemingly imposed by bond markets. But the relationship between markets and politics flows both ways: while bond markets can discipline policymakers, policymakers reluctant to engage in politically costly fiscal consolidation can also choose policies that make market discipline less constraining. Abdelal (2007) and Dutta (2018), for example, describe how global capital markets were “made” (Vogel, 2018) by policymakers seeking to guarantee their country’s access to cheap credit (see also Lemoine, 2022). By the early 2000s, and due in part to high demand for safe assets, borrowing became cheap enough for many high-income countries to sustain deficits “without causing explosive debt dynamics” (Mian et al., 2021, p. 22). Future research should explore how a country’s global position, debt ownership structure, or monetary governance affect its ability to achieve and sustain this policy goal. This will require moving beyond public opinion polls and the study of electoral politics and focusing instead on institutionalist analyses of market power (Barta & Johnston, 2023; Braun, 2020; Farrell & Newman, 2019) or game theoretic approaches to debt default and repayment (Pitchford & Wright, 2013; Tomz, 2012).

Supplemental Material

Supplemental Material - The Limits of Public Support for Fiscal Consolidation: Survey Evidence From Great Britain

Supplemental Material for The Limits of Public Support for Fiscal Consolidation: Survey Evidence From Great Britain by Björn Bremer, Charlotte Cavaillé, Lisanne De Blok and Catherine E. De Vries in Comparative Political Studies.

Footnotes

Acknowledgments

The authors thank seminar participants at the University of Konstanz, Leiden University, McGill University, Northwestern University, University College London, the University of Michigan, the University of Zurich, and the ZEW–Leibniz Centre for European Economic Research. We are especially grateful to Ben Ansell, Lucy Barnes, Sebastian Blesse, Jack Blumenthal, Thomas Sattler, and three anonymous reviewers for detailed feedback. Jack Blumenthal generously provided the voice-over for the videos used in this study. We thank Sara Luxmoore and Robin Hetzel for excellent research assistance.

Ethical Considerations

This research received ethical approval from the Institutional Review Board of Bocconi University (FA000371.01).

Consent to Participate

All respondents voluntarily opted into the study and provided informed consent before participation.

Author Contributions

All authors jointly conceived and designed the survey. BB and LdB implemented the survey and CdV provided the funding. BB and CC did the statistical analyses and interpreted the data. CC and BB wrote the manuscript. CdV critically revised the manuscript. All authors approved the final version of the manuscript and agree to be accountable for the accuracy of the work.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the European Research Council (No. 864687) and Bocconi University’s Senior Research Grant. CC acknowledges funding from the Agence Nationale de la Recherche under grant ANR-17-EURE-0010 (Investissements d’Avenir program).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

All data and replication material are available at the Comparative Political Studies Database: https://doi.org/10.7910/DVN/OYJOXP (Bremer et al., 2026).

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.