Abstract

Due to the nexus of wealth effect and cost effect, the impact of housing price on fertility is ambiguous in theory. However, the relation between housing price and fertility is essential for policymakers, especially in developing countries. This paper constructs an individual-level panel data set of over 40,000 randomly selected Chinese females with detailed fertility history during 2006–2010 from the Census 2010. Exploiting variation of housing price growth across cities over time and conditional on marriage status, we show that a 1,000 yuan upward shift in housing price induces the possibility of new birth by 13.9% for homeowners. Homeownership plays a vital role in housing price on fertility. These findings suggest that the wealth effect of housing price dominates the cost effect during the sample periods in China.

Introduction

Housing is the critical component of lifetime wealth. Since the late 1990s, many countries have experienced spectacular housing booms. To fully understand the economic impacts of housing booms on households, extensive literature has focused on consumption (Aladangady 2017; Campbell and Cocco 2007, Mian, Rao, and Sufi 2013), labor supply (Charles, Hurst, and Notowidigdo 2019; Gu, Jia, and Qian 2018; Li et al. 2020; Zhao and Burge 2017), as well as education attainment (Charles, Hurst, and Notowidigdo 2018; Lovenheim 2011). However, life-cycle outcomes, such as fertility choices, receive less attention.

Understanding how housing booms affect fertility is essential, given the dramatic housing market fluctuation and demographic transition in the last several decades. However, theoretical predictions for the causal relation are ambiguous. On the one hand, as part of household wealth, increases in housing price would transmit into rises of household wealth and might incentivize fertility decisions (Dettling and Kearney 2014; Lovenheim and Mumford 2013). On the other hand, if housing price is the shadow price of an additional child, investment incentives might induce cost effects (Simon and Tamura 2009). Besides, it is also possible that housing price fluctuation has negligible effects on fertility because homeowners with higher fertility desire might sacrifice living quality for more children (Easterlin and Crimmins 1985).

To understand the above question, this paper exploits the impacts of housing price on fertility in China, a country with the largest population but a low fertility rate. The urban housing market has been prosperous since the 1998 housing reform. According to National Bureau of Statistics of China, from 2002 to 2018, the national average residential housing price skyrocketed from 2092 yuan to 8,544.11 yuan, which offers substantial changes in city housing price across years. Furthermore, housing wealth constitutes over 60% of total household wealth (Cooper and Zhu 2017). 1

We construct extensive, individual-level panel data using Census 2010 data from NBS for 5 years from 2006 to 2010. Considering the potential endogeneity and measurement error of self-reported housing price (Choi and Painter 2018), we use city-level housing price to investigate their effect on fertility. If the housing price (at city level) reflects the cost of living in a city, and a higher living cost would arguably increase the cost of raising a newborn child. However, the negative cross-sectional correlation might be confounded by common local factors such as higher education or nominal income level, other than the real effects of housing price. Therefore, our specifications are conditional on marriage status, year, and city fixed effects. We find that when housing price increases by 1000 yuan, the probability of new birth by 13.9%. Furthermore, the effects are mainly driven by homeowners and urban households. These findings suggest that the wealth effect of rising housing dominates the cost effect, and the net impact on fertility is positive conditional on homeownership status.

Moreover, our results show that the effects increase with age, implying lifetime effects. We also identify heterogeneous responses to the rise in housing price with detailed information on fertility histories, education, year of the first marriage, and migration history. In particular, the housing wealth effect on fertility is primarily driven by females with more than one child and with senior high school education. Furthermore, we also utilize the supply-side variation in housing price as an instrument, and the results are robust to the alternative specifications.

Our analysis contributes to several strands of the literature. First, we directly speak to the literature on how the housing booms affect fertility decisions. Despite the importance of this relation, the findings are mixed between developed countries and developing countries in the previous literature. In developed countries such as the US, researchers have reached a consensus that housing wealth could prompt new births for homeowners. For example, Lovenheim and Mumford (2013) distinguish homeowners from renters in the US context. Specifically, their findings show that a $100,000 increase in housing wealth results in an over 15% increase in the probability of new births. At the MSA-level, Dettling and Kearney (2014) also provide evidence that the housing wealth effect for fertility also exists, especially for MSAs with higher ownership.

In stark contrast to their findings of wealth effects, housing booms in Asia seems to generate negative effects on fertility and consistent with low fertility patterns in these countries and regions. For instance, using the annual data of Hong Kong, Yi and Zhang (2010) find that a 0.45% decrease in total fertility rates follows a 1% increase in housing price at the aggregate level. Lin, Chang, and Foo Sing (2016) also observe that homeowners during the housing boom period delay their first child in Taiwan. The underlying model treats housing as a shadow price for children. Furthermore, Wrenn et al. (2019) also find housing prices significantly delay the age of first marriage for the young living in 35 big cities in China. In some recent practices, researchers also suggest that the housing cost in China might negatively correlate with the birth rate (Clark, Yi, and Zhang 2020, Liu, Xing, and Zhang 2020b). Yet few of them consider the potential endogeneity of housing prices and the heterogeneous roles of homeownership. 2

Furthermore, given that housing price in China has risen dramatically during the period we study, and the homeownership rate is relatively high in China, housing booms might also contribute to the accumulation of household wealth, and subsequently increase the birth rate. Therefore, our distinct contribution is our focus on the context of a country with the largest population, utilizing the recent large-scale housing booms and cross-city price variation in China to shed some novel insight on the relation between housing price and fertility.

Second, the paper broadly contributes to the literature on fertility decisions. Back to Becker (1960), children are regarded as normal durable goods. The crucial prediction of the Beckerian framework is that households adjust to the changes in children’s marginal price, while the effect of income changes is limited due to quantity-quality tradeoff. That is, parents can substitute the quantity of children with quality such as education investment when income increases. However, early empirical observations might be attributed to the fact that and suffer from the cross-sectional or time-series nature of data. 3 Recent literature has exploited exogenous sources of income, such as energy price shock (Black et al. 2013) and additional financial incentives (Cohen, Dehejia, and Romanov 2013). Most of this strand of literature consistently finds that income increases have positive causal impacts on fertility. Among them, Liu, Xing, and Zhang (2020b) further find that housing booms in China increase reproductive intentions for homeowners. We complement this ongoing literature by exploring the variation in housing wealth, a key component of household economic resources, on fertility.

The remaining part of the article is structured as follows. In institutional background, we briefly introduce China’s residential real estate market and the recent fertility trend. Data and methodology introduces the data sources and empirical specifications. Result and discussion discusses the results, and concluding and remarks draws concluding remarks.

Institutional Background

In the last two decades, China has been experiencing a booming urban housing market (Glaeser et al. 2017). Before 1998, urban housing in China was welfare-oriented, and there was no residential housing market. In the late 1990s, China shifted from a housing distribution system to a market-oriented housing system. In 1998, State Council issued a document declared that working units would no longer allocate public housing. Specifically, since the second half of 1998, with monetary compensation from their working units, urban households need to pay for a house (either buy or rent) from the housing market. To accelerate the process, the government complements the private housing market with a mortgage market to help individuals finance their own houses. The marketization policies successfully stimulated China’s real estate market, making the sector a new pillar of the country’s economic growth in the recent two decades. The reform raises the curtain on the persistent housing booms in China. Since then, urban housing price has risen significantly.

From 2002 to 2018, the national average residential housing price skyrocketed from 2,092 yuan to 8,544.11 yuan, over three times. On the one hand, soaring housing price becomes a burden for young couples without many economic resources. As reported in The Economist on Feb 8th, 2018:

“Would-be parents frequently tell pollsters that they balk at the cost of raising children. As well as fretting about rising house prices and limited day care, many young couples know that they may eventually have to find money to support all four of their parents in old age.”

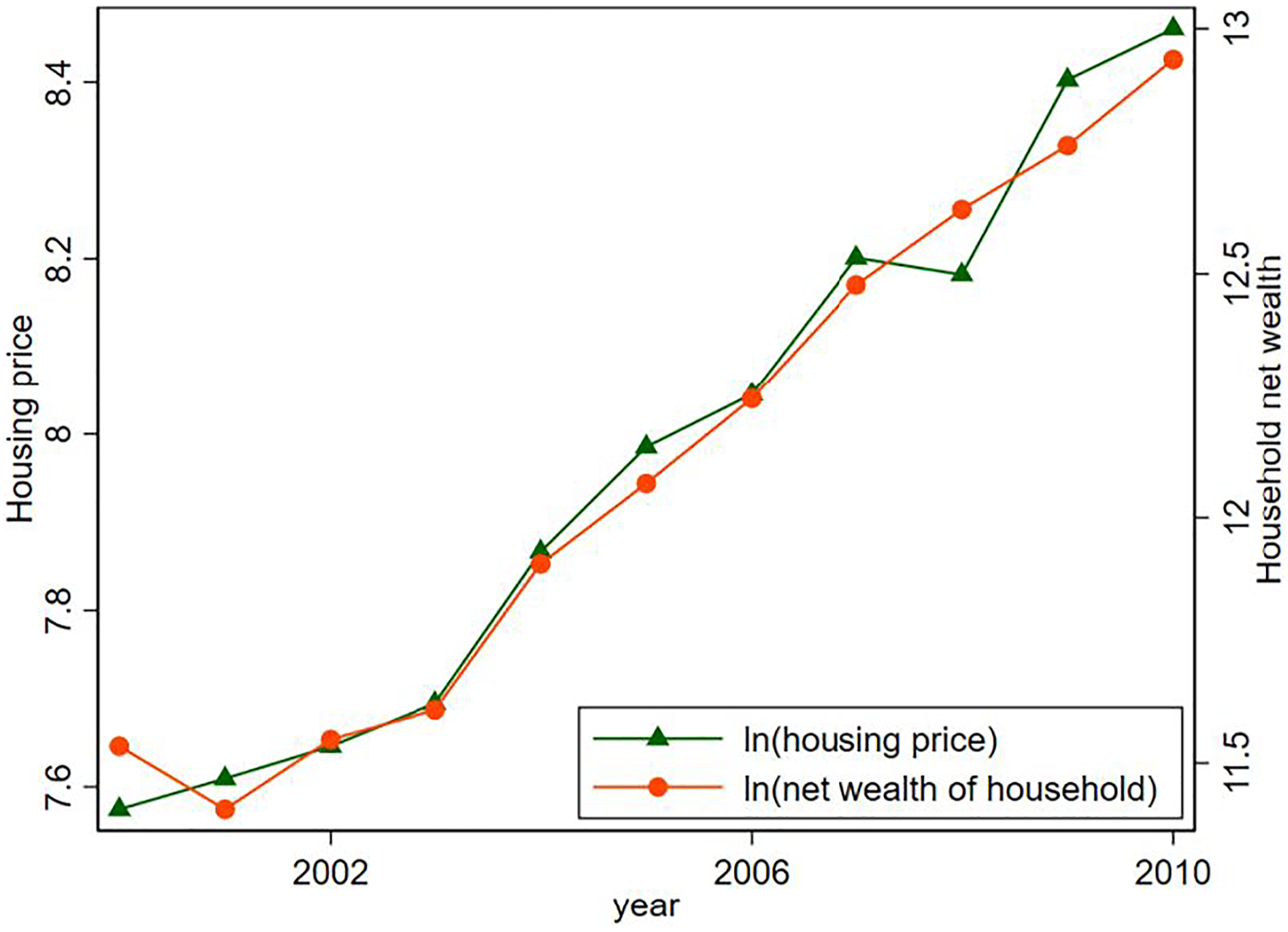

On the other hand, the housing booms seem to generate a large amount of wealth for Chinese people, especially for those with homeownership (Li et al. 2020). As shown in Figure 1, with the increase in housing price, the household net worth has grown substantially. Due to the expectation of increasing housing price, some housing speculators even buy several houses for investment (Glaeser et al. 2017, Fan and Pan 2020). Meanwhile, since a house is regarded as a prerequisite for marriage, most Chinese young people bought their properties by the intergenerational transfer from their parents and became homeowners (Cheung, Chan, and Monkkonen 2020).

4

Although they still need to pay for the monthly mortgage for their house, higher housing price might help young couples accumulate wealth, given the collateral effects of housing wealth. Housing price and household wealth. Notes: This figure visualizes the comovement of housing price and household net wealth. The data sources are China Statistical yearbooks. The green line denotes the housing price change, and the red line denotes the household net wealth change.

Data and Methodology

Data Sources and Description

China’s Census 2010

The primary dataset is from the 2010 Census. The available random sample covered 5% of the total population in 2010. The data contains comprehensive information on income, type of employer, fertility histories, and housing conditions. We apply several criteria to construct the individual data. Firstly, we exclude individuals in autonomous regions and those who are minorities because fertility policies are quite different for these individuals. Secondly, we drop those living in government-subsidized apartments because the housing market fluctuation is less relevant for them. Thirdly, based on individual marriage and fertility histories, we expand the individual cross-section into a 5 -year panel from 2006 to 2010.

Moreover, considering the suitable age range for life-cycle fertility, we keep females between 20 and 45. Finally, we make restrictions on our sample to married females with urban hukou in 2010. Overall, our final sample includes over 190,842 observations for 40,898 females and covers 252 cities.

Other City-level Data

We obtain city-level data from CEIC database, including city-level housing price, average annual salary, government revenue, and GDP. Our city-level land supply information is from CREI (China Real Estate Information). For some of the missing values, we interpolate by using data from another database, EPS. Given the original data sources are mainly from NBS, data across different databases are consistent.

Summary Statistics

Summary Statistics.

Notes: This table reports the descriptive statistics of our baseline sample. The data sources are from Census 2010 and CEIC.

Furthermore, the total fertility rate for homeowners is 1.003, and renters have a rate of 0.977. Since we only use an urban sample, the total fertility rate for both groups of females is slightly lower than the overall low fertility rate of 1.18 in Census 2010. The average marriage rate for homeowners is as high as 92.8%, while only 88.8% of renters are married. On average, the age at the first marriage for both groups is about 24 years old. Last but not least, typical homeowners finish more education than renters.

Methodology

To quantify the immediate impact of city-level housing price on fertility, we run the following linear probability model:

Our identification strategy highly relies on the exogeneity of

To address these concerns, we isolate supply-side variation in house price driven by local governments at the city level. Specifically, unlike the US, the housing supply in China is strictly under the control of local governments via their land supply plans for each year. In other words, the annual land supply is predetermined in advance rather than follows the housing demand dynamics. The intuition is that land supply affects fertility only via the change in housing price. On the other hand, the regulated land supply market influences the land using cost, directly affecting housing price.

Results and Discussion

This section provides empirical results on how housing price affects the probability of new birth in China. First, we present some facts by graphics. Then, we magnify the effect by various specifications. Additionally, we investigate whether the effects we find are timing effects or lifetime effects. Next, we exploit the heterogeneity among different groups of females. Finally, we apply various alternative specifications to check the validity of our findings.

Graphical Analysis

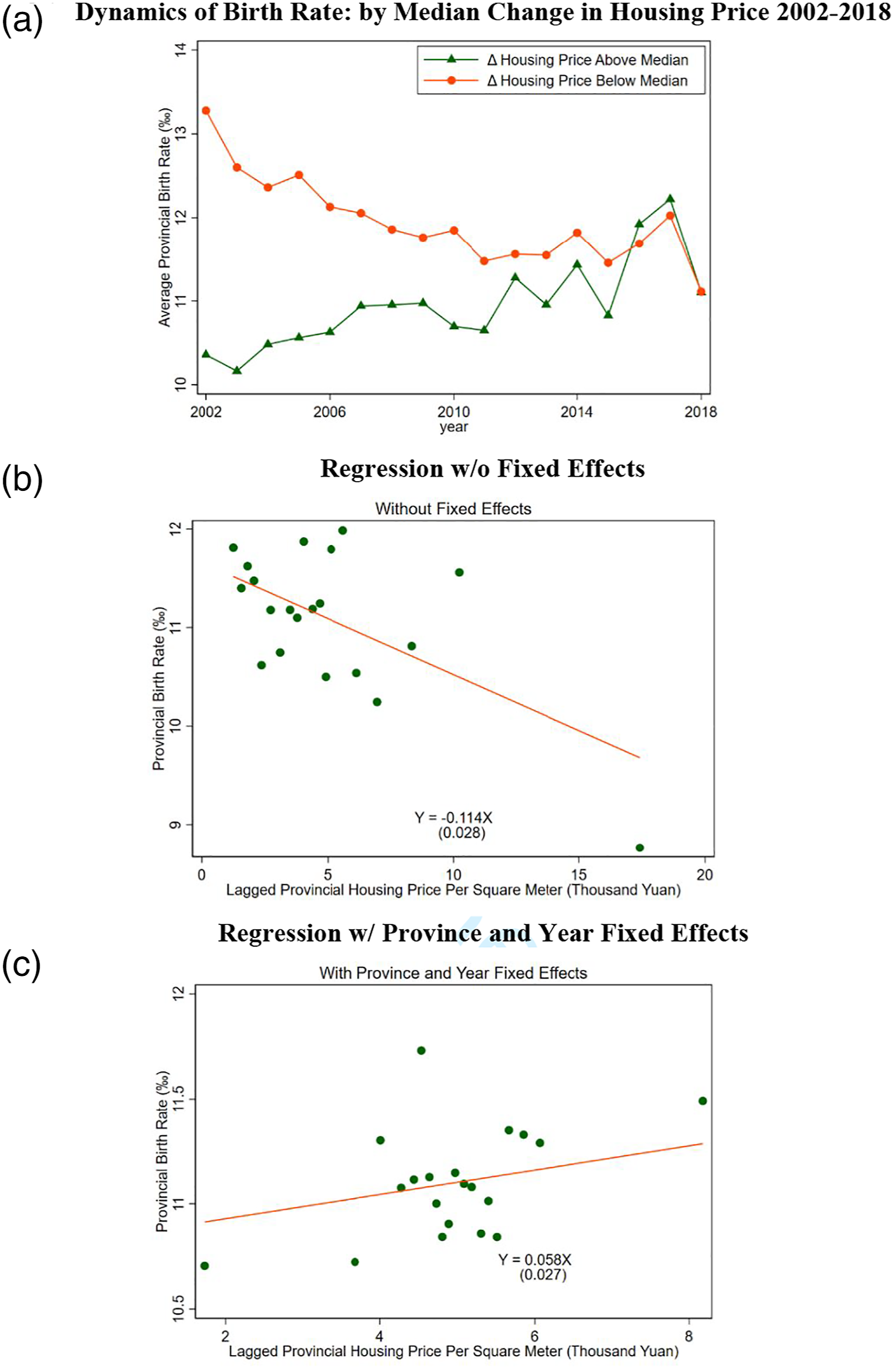

We start our investigation with some graphical evidence. Figure 2 presents the relationship between lagged provincial housing price and birth rates in the period from 2002 to 2018. Panel A visualizes the birth rate dynamics by the change in the median change in housing price 2002–2018. The green line denotes the provinces with the above-median housing price change, and the orange line denotes the provinces with the below-median housing price change. The pattern reveals a wide range of stylized facts. First, birth rates in provinces with above-median housing price change were initially lower than those below the median. Second, birth rates in above-median provinces gradually grow, while there is a constant reduction for provinces with below-median change. Finally, birth rates in both groups of provinces converge to a certain level of about 11% in recent years. Effects of provincial housing price on birth rate. (a). Dynamics of birth rate: by median change in housing price 2002–2018, (b). regression w/o fixed effects, and (c). regression w/province and year fixed effects. Notes: This figure shows binned scatter plots of lagged provincial housing price per square meter and provincial birth rate. The data sources are Provincial Statistical Yearbooks. It covers a time period from the year 2002–2018. Panel A visualizes the dynamics of birth rate by median in housing price growth during 2002–2018. The green line denotes the provinces with above-median housing price change, and the orange line denotes the provinces with below-median housing price change. Panel B presents binscatter of the relation between lagged provincial housing price per square meter and provincial birth rate, without any control. Panel B presents binscatter of the relation between lagged provincial housing price per square meter and provincial birth rate, with province and year fixed effects.

Panel B implies that a 1000 yuan increase in provincial average housing price correlates with a statistically significant decline of 0.114% in the aggregate birth rate, without any control. This original pooled estimate is commensurate with the anecdotal evidence that high housing price reduces total fertility worldwide.

Intuitively, if the housing price (at city level) reflects the cost of living in a city, and a higher living cost would arguably increase the cost of raising a newborn child. However, the negative cross-sectional correlation might be confounded by common local factors such as higher education or nominal income level, other than the real effects of housing price. Conditional on province and year fixed effects, the negative relation turns into significantly positive in Panel C, suggesting that fixed effects wipe out the negative correlation. Specifically, the practice implies a rise of 1000 yuan in provincial housing price is related to an increase of 0.058% (0.5% of mean) in the provincial birth rate. Since our provincial birth rate is calculated as an average for all populations in each province, it takes different groups of people, such as rural individuals and minorities, into account. As a result, the estimate here might be a lower bound for the housing wealth effects. According to NBS, the nationwide housing price increase rises from 2092 yuan to 8,544.11 yuan; a back-of-the-envelope calculation suggests that the birth rate rises by 0.374%.

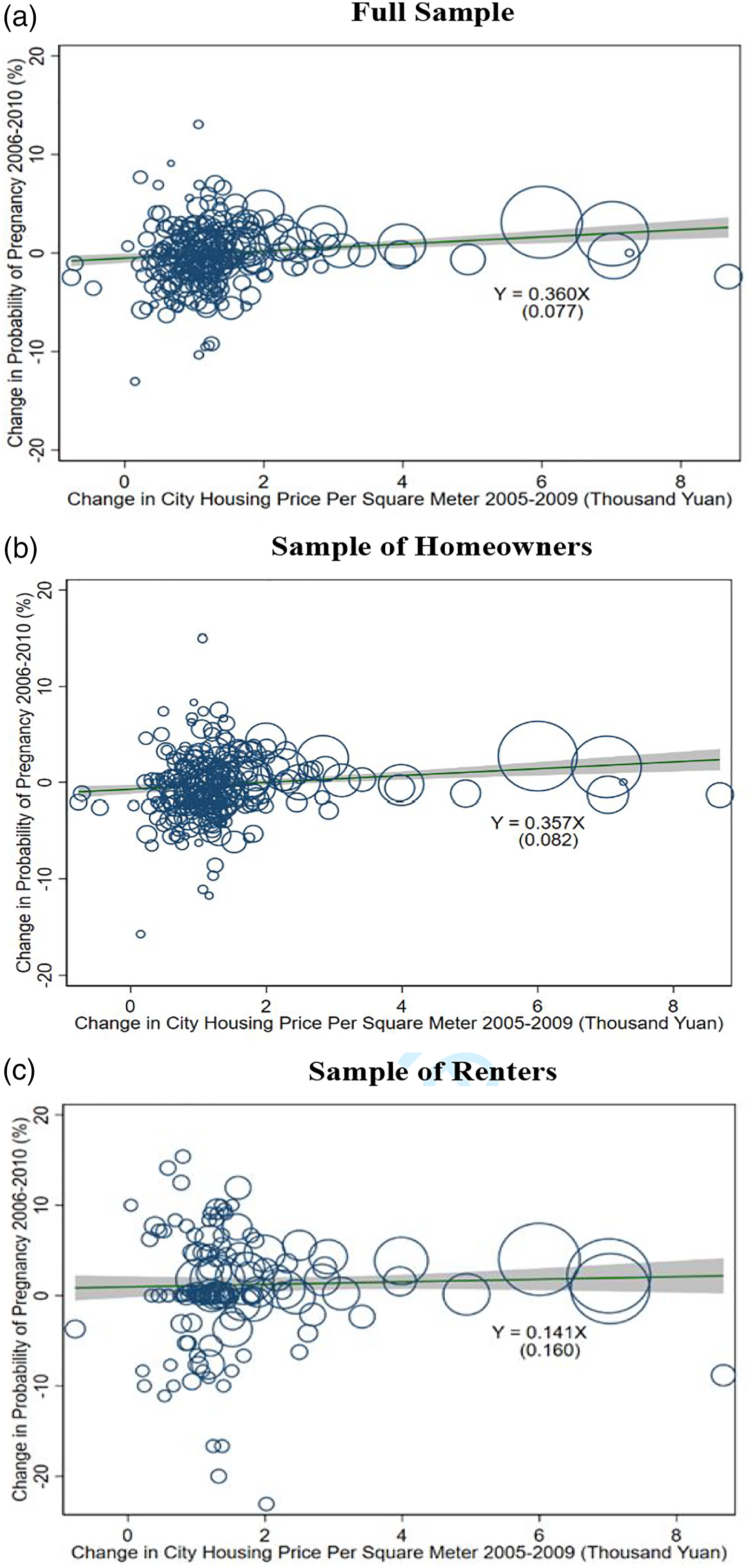

As a confirmation, Figure 3 further visualizes the relation between the first difference of city housing price and the probability of new birth based on our basic sample of urban households.

6

The circle area reveals the sample size of each city in 2010. Panel A reveals an overall pattern that a greater housing price increase is associated with relatively higher fertility growth. The estimated coefficient of 0.360 suggests that a 1,000 yuan increase in the city housing price induces a 0.360-percentage-point (i.e., 9.35%) increase in new-birth probability. Effects of Change in City Housing Price on the Change in Probability of New Birth. (a). Full Sample, (b). Sample of homeowners, and (c). Sample of renters. Note: This figure visualizes the effects of change in city housing price on the change in probability of new birth. Each circle represents a city. The sample is constructed based on Census 2010. Circle size represents the sample size of the city in our sample. X-axis denotes the change in city housing price per square meter between 2005 and 2009 in 1000 yuan. Y-axis denotes the change in probability of new birth between 2006 and 2010. Panel A presents the results for the full sample; Panel B presents the results for the sample of homeowners; Panel C presents the results for the sample of renters.

It is well acknowledged that housing wealth effects rely on homeownership. Under similar economic conditions, owners’ responses to changes in housing market conditions should arguably be different from those of renters. Since we have disaggregate level ownership information, we also divide the sample into homeowners and renters, in Panel B and C. Reassuringly, the slope for homeowners is economically and statistically significant, while that for renters is insignificant. Altogether, they suggest that the housing wealth effects for fertility are mainly driven by housing price variation instead of other common economic shocks. Collectively, both Figures 2 and 3 imply a positive relation between lagged housing price and fertility. These results align with the evidence from developed countries, such as the US (Dettling and Kearney 2014; Lovenheim and Mumford 2013). However, the aggregate level analysis might overgeneralize the housing price at the city level as an individual’s housing wealth affect fertility decision. Therefore, we move on to the individual-level evidence in the next subsection.

Baseline Results

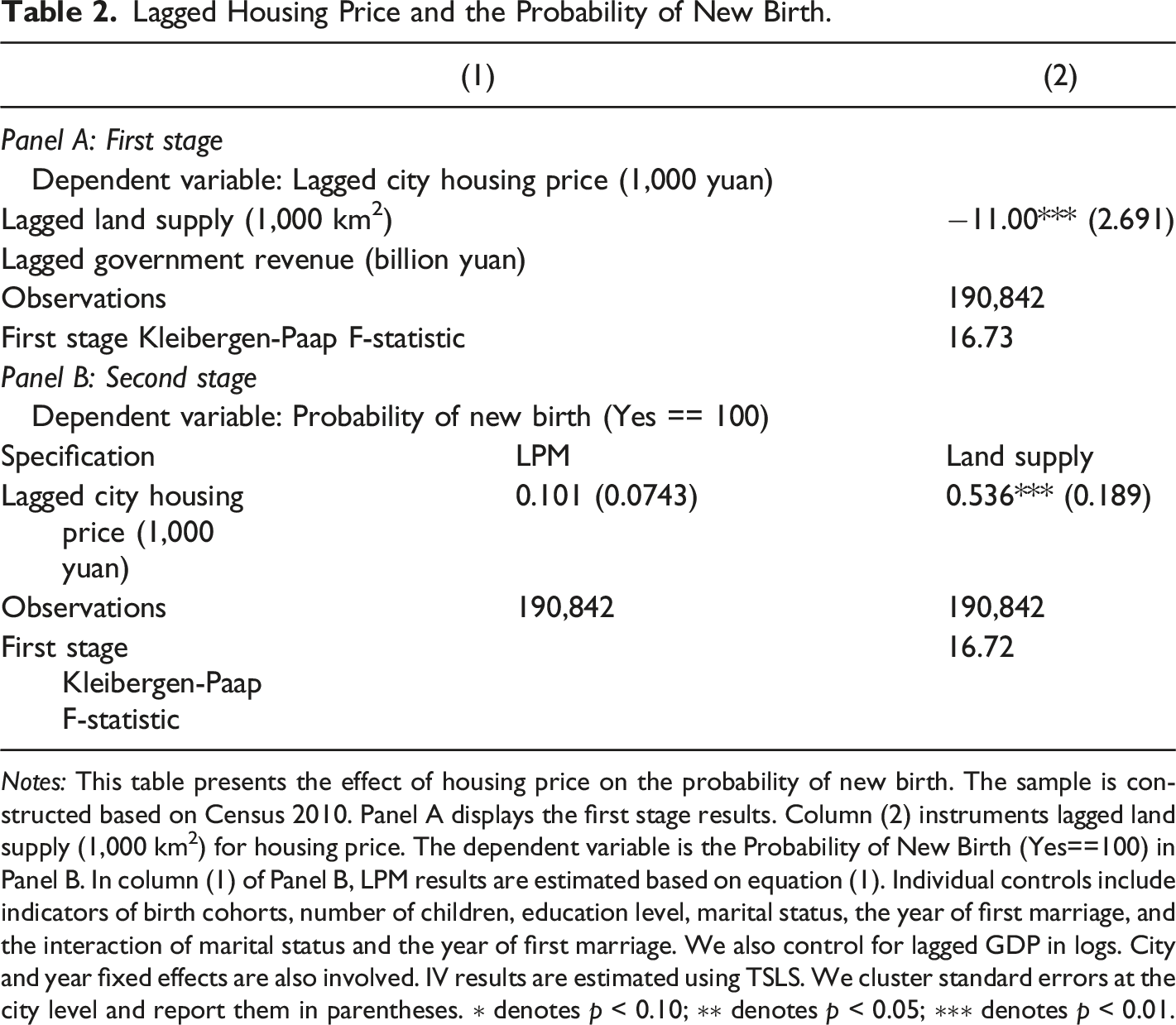

Lagged Housing Price and the Probability of New Birth.

Notes: This table presents the effect of housing price on the probability of new birth. The sample is constructed based on Census 2010. Panel A displays the first stage results. Column (2) instruments lagged land supply (1,000 km2) for housing price. The dependent variable is the Probability of New Birth (Yes==100) in Panel B. In column (1) of Panel B, LPM results are estimated based on equation (1). Individual controls include indicators of birth cohorts, number of children, education level, marital status, the year of first marriage, and the interaction of marital status and the year of first marriage. We also control for lagged GDP in logs. City and year fixed effects are also involved. IV results are estimated using TSLS. We cluster standard errors at the city level and report them in parentheses. ∗ denotes p < 0.10; ∗∗ denotes p < 0.05; ∗∗∗ denotes p < 0.01.

In Panel B of Table 2, we show results from LPM as well as IV. We observe that all specifications return consistently positive signs. The LPM results suggest that a 1000 yuan increase in lagged city housing price is associated with a 0.101 percentage point increase or 2.62% (=0.101/3.849) in new-birth probability. As compared with the results of IV, the insignificant positive coefficient of 0.101 (p = 0.175) in column (1) indicates a downward bias. This is possible because people with lower fertility desire are likely to move to cities with higher housing price (Simon and Tamura 2009), contaminating the causal inference from LPM. Our preferred specification in column (2) implies that a rise of 1000 yuan in lagged city housing price per square meter leads to a 0.536 percentage point increase in the probability of new birth, which could be translated into a 13.9% (=0.536/3.849) increase.

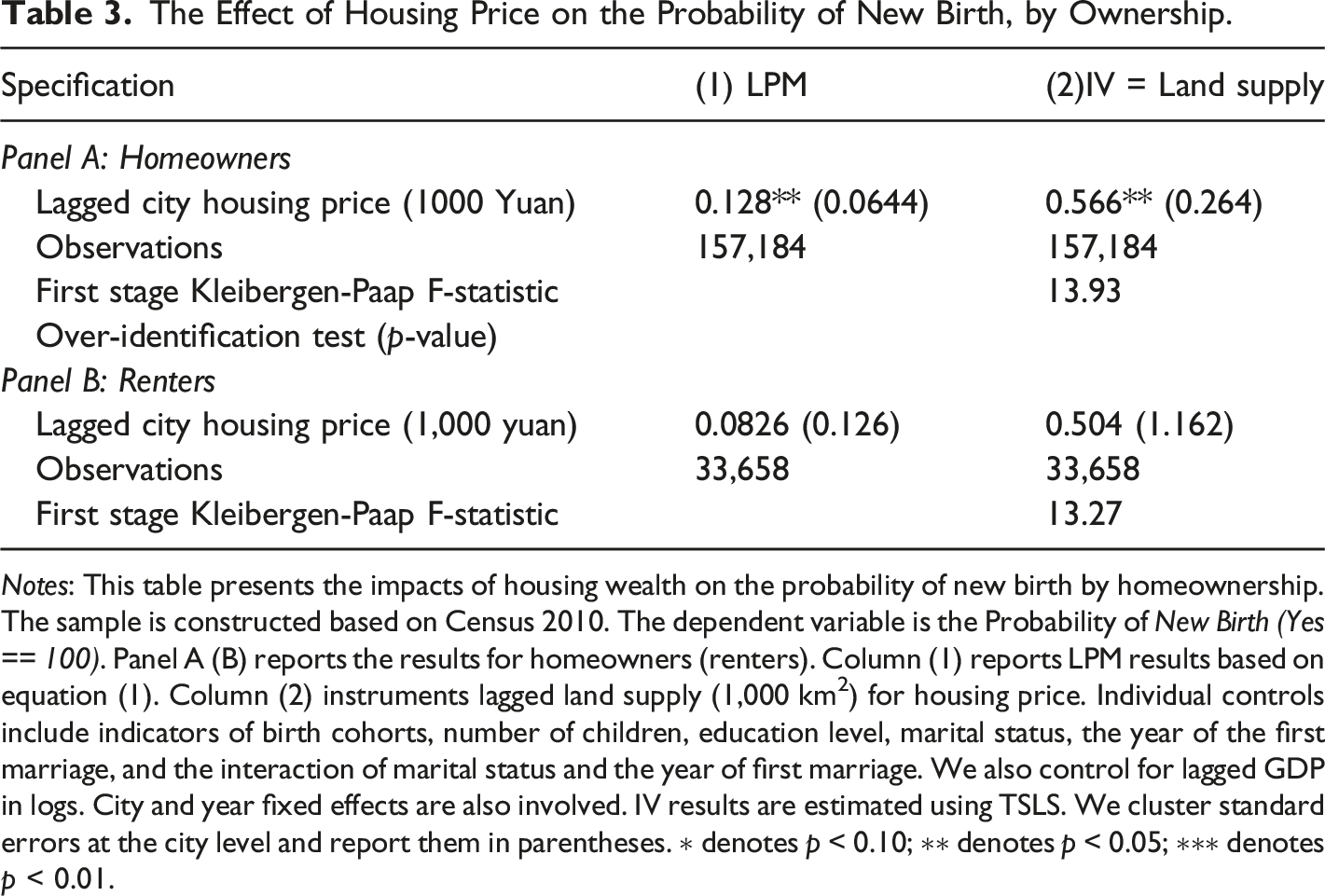

The Effect of Housing Price on the Probability of New Birth, by Ownership.

Notes: This table presents the impacts of housing wealth on the probability of new birth by homeownership. The sample is constructed based on Census 2010. The dependent variable is the Probability of New Birth (Yes == 100). Panel A (B) reports the results for homeowners (renters). Column (1) reports LPM results based on equation (1). Column (2) instruments lagged land supply (1,000 km2) for housing price. Individual controls include indicators of birth cohorts, number of children, education level, marital status, the year of the first marriage, and the interaction of marital status and the year of first marriage. We also control for lagged GDP in logs. City and year fixed effects are also involved. IV results are estimated using TSLS. We cluster standard errors at the city level and report them in parentheses. ∗ denotes p < 0.10; ∗∗ denotes p < 0.05; ∗∗∗ denotes p < 0.01.

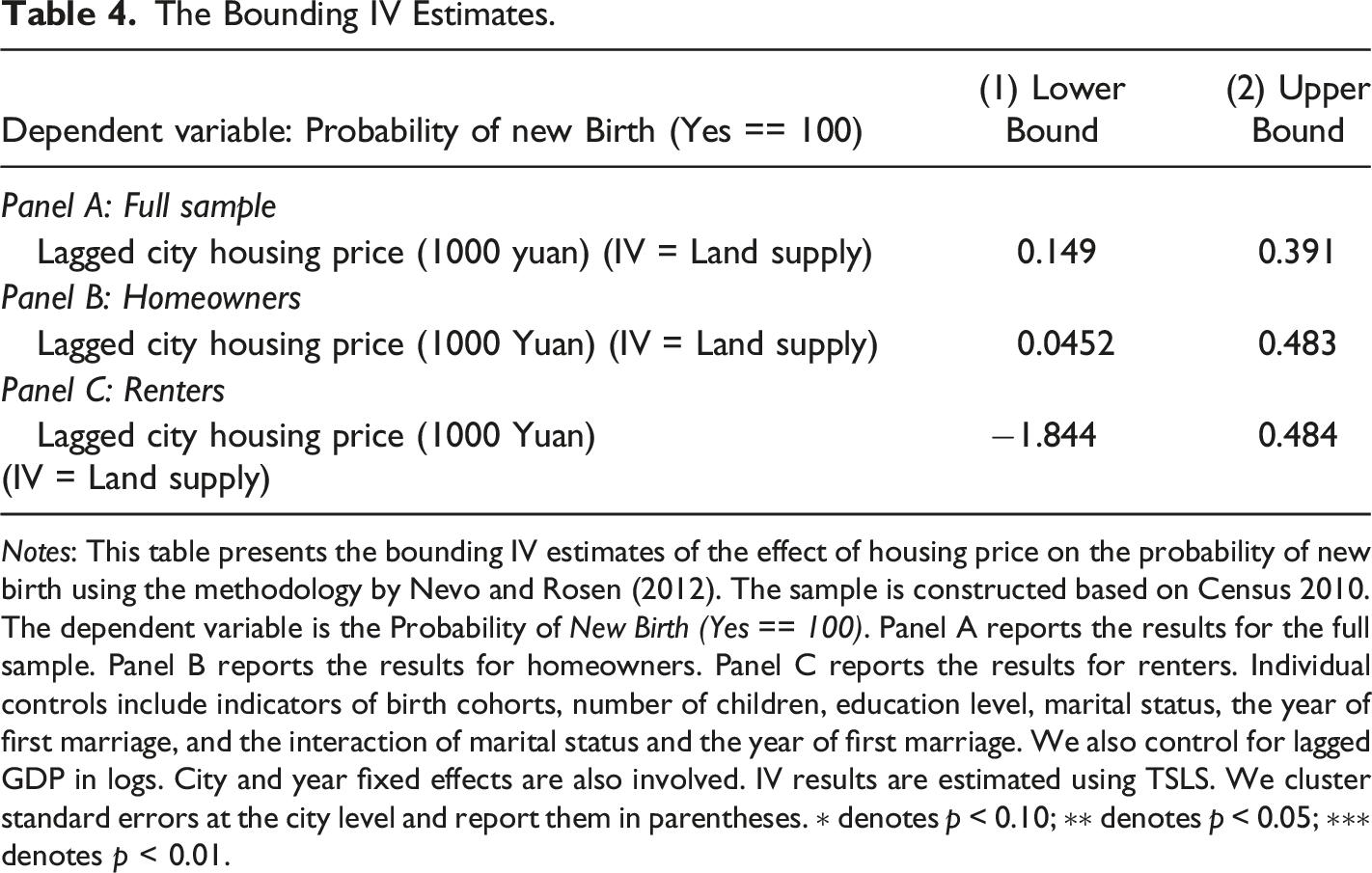

The Bounding IV Estimates.

Notes: This table presents the bounding IV estimates of the effect of housing price on the probability of new birth using the methodology by Nevo and Rosen (2012). The sample is constructed based on Census 2010. The dependent variable is the Probability of New Birth (Yes == 100). Panel A reports the results for the full sample. Panel B reports the results for homeowners. Panel C reports the results for renters. Individual controls include indicators of birth cohorts, number of children, education level, marital status, the year of first marriage, and the interaction of marital status and the year of first marriage. We also control for lagged GDP in logs. City and year fixed effects are also involved. IV results are estimated using TSLS. We cluster standard errors at the city level and report them in parentheses. ∗ denotes p < 0.10; ∗∗ denotes p < 0.05; ∗∗∗ denotes p < 0.01.

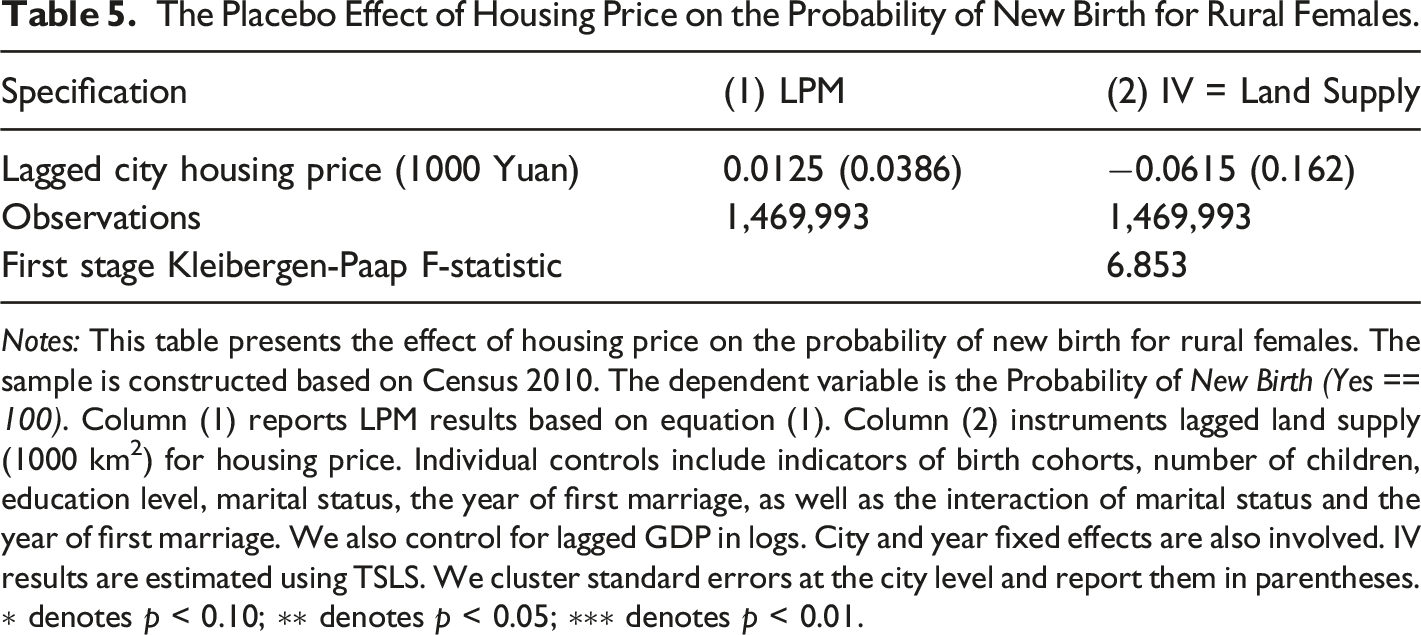

The Placebo Effect of Housing Price on the Probability of New Birth for Rural Females.

Notes: This table presents the effect of housing price on the probability of new birth for rural females. The sample is constructed based on Census 2010. The dependent variable is the Probability of New Birth (Yes == 100). Column (1) reports LPM results based on equation (1). Column (2) instruments lagged land supply (1000 km2) for housing price. Individual controls include indicators of birth cohorts, number of children, education level, marital status, the year of first marriage, as well as the interaction of marital status and the year of first marriage. We also control for lagged GDP in logs. City and year fixed effects are also involved. IV results are estimated using TSLS. We cluster standard errors at the city level and report them in parentheses. ∗ denotes p < 0.10; ∗∗ denotes p < 0.05; ∗∗∗ denotes p < 0.01.

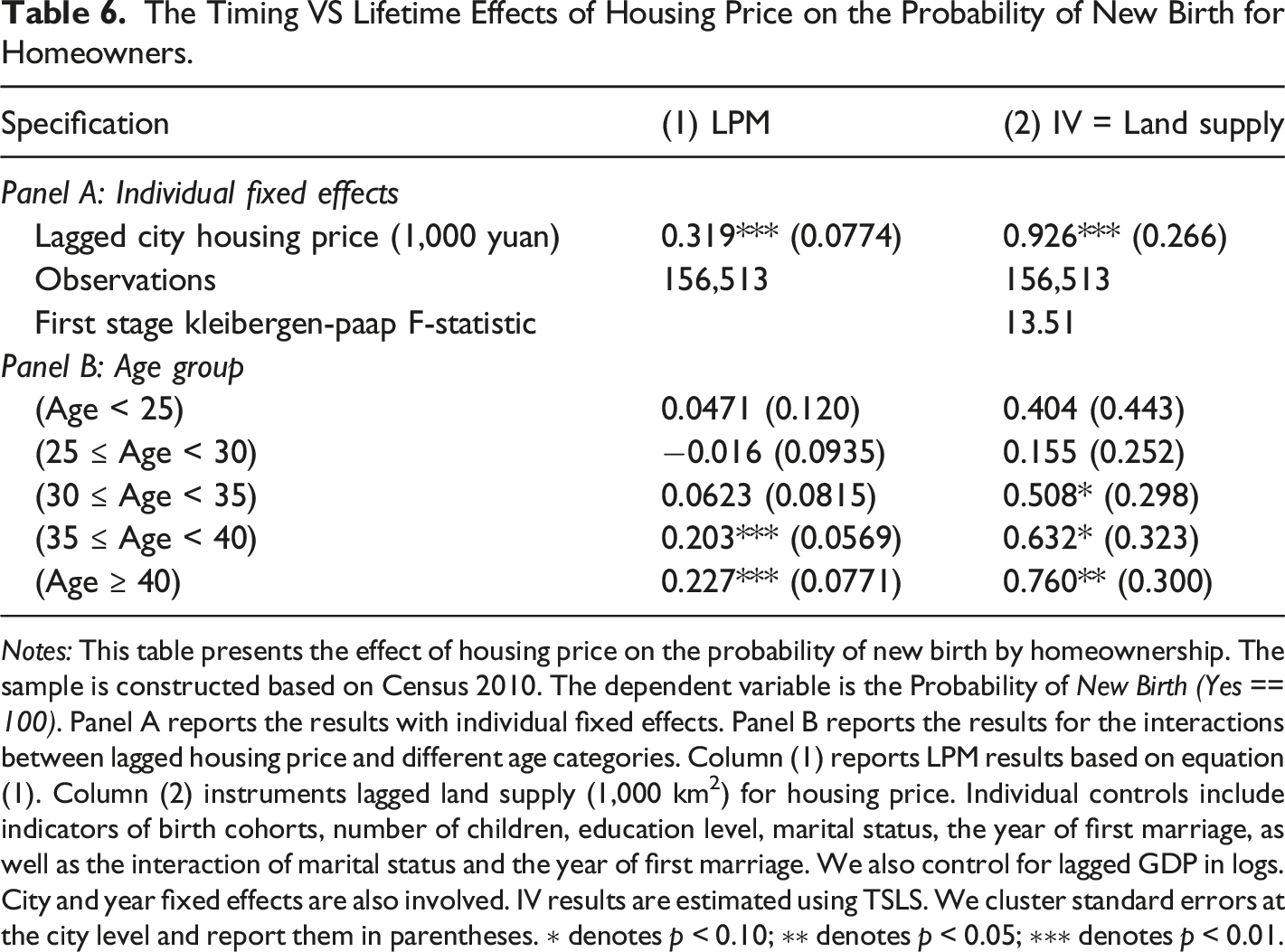

Timing Effects VS Lifetime Effects

The Timing VS Lifetime Effects of Housing Price on the Probability of New Birth for Homeowners.

Notes: This table presents the effect of housing price on the probability of new birth by homeownership. The sample is constructed based on Census 2010. The dependent variable is the Probability of New Birth (Yes == 100). Panel A reports the results with individual fixed effects. Panel B reports the results for the interactions between lagged housing price and different age categories. Column (1) reports LPM results based on equation (1). Column (2) instruments lagged land supply (1,000 km2) for housing price. Individual controls include indicators of birth cohorts, number of children, education level, marital status, the year of first marriage, as well as the interaction of marital status and the year of first marriage. We also control for lagged GDP in logs. City and year fixed effects are also involved. IV results are estimated using TSLS. We cluster standard errors at the city level and report them in parentheses. ∗ denotes p < 0.10; ∗∗ denotes p < 0.05; ∗∗∗ denotes p < 0.01.

Individual Fixed Effects

One of the advantages of the panel dataset is that it allows us to re-estimate the baseline model with restrictive individual fixed effects. In other words, we can control for a series of time-invariant unobservables, such as fertility preference and persistent income level. In Panel A of Table 6, we observe that all magnitudes of these effects are almost twice our baseline results, suggesting that households could respond to price change by timing fertility.

Different Age Groups

In Panel B, we observe a significantly positive effect of the housing wealth on fertility for each age category, with the coefficient increasing among older mothers. The coefficient for 40–45-year-olds is 20% ((0.760–0.632)/0.632) larger than the coefficient for 35–39-year-olds and almost twice the coefficient for 20–24-year-olds. Since the probability of new birth decreases significantly with age, the effect’s magnitude is most significant among females aged 40–45. As older females are less likely to delay fertility, an immediate fertility increase could be translated into a permanent fertility rise.

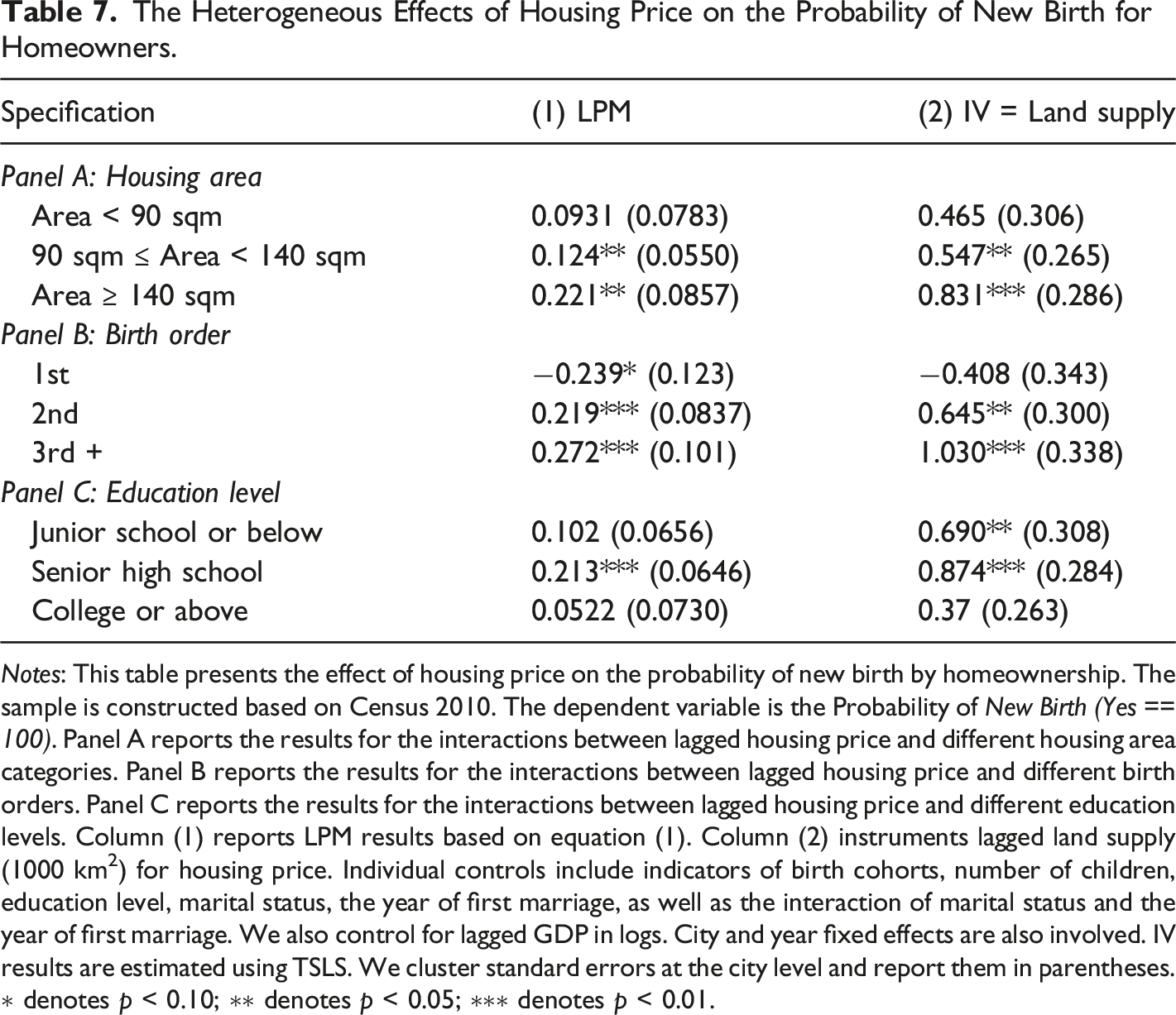

Heterogeneity

In this subsection, we investigate heterogeneous responses of fertility to housing market fluctuations. In particular, we focus on the housing area, birth order, and education level.

Housing Area

The Heterogeneous Effects of Housing Price on the Probability of New Birth for Homeowners.

Notes: This table presents the effect of housing price on the probability of new birth by homeownership. The sample is constructed based on Census 2010. The dependent variable is the Probability of New Birth (Yes == 100). Panel A reports the results for the interactions between lagged housing price and different housing area categories. Panel B reports the results for the interactions between lagged housing price and different birth orders. Panel C reports the results for the interactions between lagged housing price and different education levels. Column (1) reports LPM results based on equation (1). Column (2) instruments lagged land supply (1000 km2) for housing price. Individual controls include indicators of birth cohorts, number of children, education level, marital status, the year of first marriage, as well as the interaction of marital status and the year of first marriage. We also control for lagged GDP in logs. City and year fixed effects are also involved. IV results are estimated using TSLS. We cluster standard errors at the city level and report them in parentheses. ∗ denotes p < 0.10; ∗∗ denotes p < 0.05; ∗∗∗ denotes p < 0.01.

Birth Order

In Panel B, we see that the magnitudes of the first birth are negative and statistically insignificant at the conventional level, suggesting that increases in housing price might delay first birth timing. Given the mean level for the probability of new birth is 15.378%, the size of decrease is about 2.6% (=0.408/15.378) in our specification. However, the signs of all estimates turn into positive for the second birth and becomes significant.

Moreover, the IV estimate on the third and higher-order birth is as large as 1.030, statistically significant at the 1% level. In the sample period, China still implemented strict family planning policies and imposed social maintain fees for “illegal” children. Thereby, the wealth effects we detect here might partially offset the tangible costs imposed by the local governments. Considering that birth order increases with mothers’ age, the results are consistent with the finding that the increase in housing price mainly shifts up the fertility of those females older than 35.

Education

In Panel C, we categorize the individual in our sample according to their education level, including junior school or below, senior high school, and college or above. The housing growth leads to the largest rise in the probability of new birth for females with senior high school degree. For this group of females, a 1000 yuan increase in housing price significantly increases probability of new births by 0.874 percentage points or 21.4% (=0.874/4.076). The effects for those who have taken a college degree or above are neither economically nor statistically significant, which is consistent with the low fertility desire for females with higher education levels (Rindfuss, Bumpass, and John 1980).

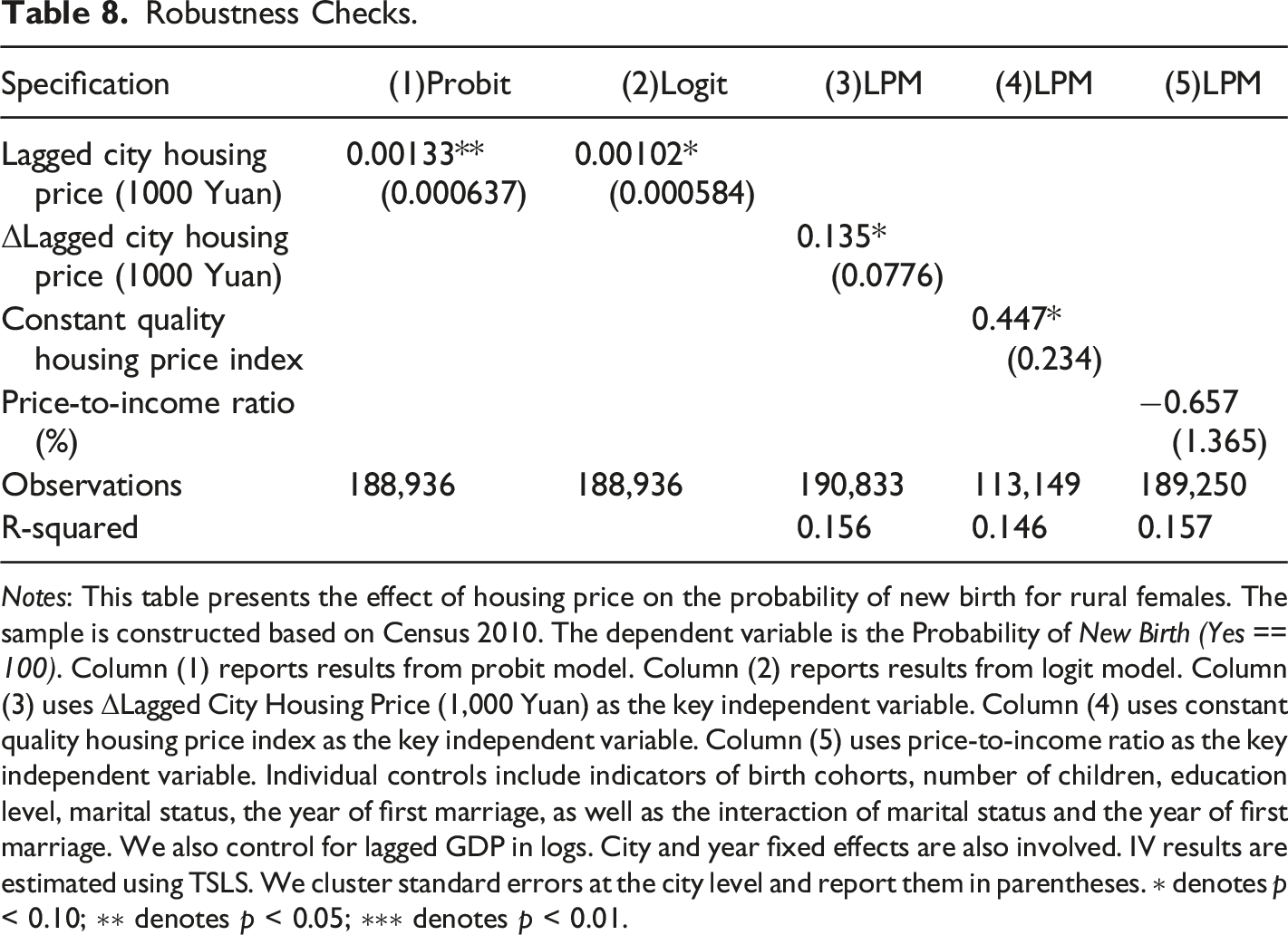

Robustness Checks

Non-linear specifications

Robustness Checks.

Notes: This table presents the effect of housing price on the probability of new birth for rural females. The sample is constructed based on Census 2010. The dependent variable is the Probability of New Birth (Yes == 100). Column (1) reports results from probit model. Column (2) reports results from logit model. Column (3) uses ΔLagged City Housing Price (1,000 Yuan) as the key independent variable. Column (4) uses constant quality housing price index as the key independent variable. Column (5) uses price-to-income ratio as the key independent variable. Individual controls include indicators of birth cohorts, number of children, education level, marital status, the year of first marriage, as well as the interaction of marital status and the year of first marriage. We also control for lagged GDP in logs. City and year fixed effects are also involved. IV results are estimated using TSLS. We cluster standard errors at the city level and report them in parentheses. ∗ denotes p < 0.10; ∗∗ denotes p < 0.05; ∗∗∗ denotes p < 0.01.

Alternative Measurements

In addition to the city-level average housing price we use in the baseline regressions, we also consider three alternative measurements. The first proxy variable is the change in city-level housing price between t-2 and t-1. In column (3) of Table 8, we observe that the results for this measurement are slightly higher than our baseline LPM results. The second alternative measurement is the Constant Quality Housing Price Index from Fang et al. (2016). 11 In column (4) of Table 8, we still obtain a significant relationship between the alternative housing price index and the probability of new birth. The last measurement is the price-to-income ratio, regarded as affordability in the previous papers (see Glaeser et al. (2017)). 12 However, we would not expect any significant effects on housing affordability if our interpretation of housing wealth effects is correct. Results in column (5) assure a negative but insignificant association between the two.

Migration

A potential concern of our approach is that households may migrate across cities in response to housing price shock, inducing the selection bias (Li 2019). We try to mitigate the migration concern by keeping only those individuals who lived in their current province before 2006. 13 Supplementary Appendix Table A2 suggests that restricting the sample to people who lived in their current province before 2006 does not affect our conclusion about the positive impacts of housing wealth on new births.

Concluding Remarks

Based on China’s Census 2010, we constructed individual panel data to probe the relation between housing price and fertility from 2006 to 2010. Our specification reveals that the estimated effect of a 1,000 yuan increase on the probability of new birth was as large as 13.9%. We also show that housing price growth accelerates wealth accumulation for homeowners and encourages fertility choices throughout a lifetime. Further investigation implies that the housing wealth effect is mainly driven by females with more than one child and with senior high school education. Furthermore, a wide range of robustness checks reassures that our estimates are less likely to be confounded by other common economic conditions.

Our results are useful for understanding how fertility choice changes in response to the housing market fluctuation. Since homeownership plays a crucial role in fertility, improving housing affordability, especially for low-income households and young couples, is the priority when designing supplementary fertility policies.

There are also some caveats in our research. First, we show the correlation between housing wealth and housing prices at the city level, but the ecological bias of using city-level variables to proxy individual wealth is still a pronounced limitation of our research. Future research should collect detailed individual-level housing wealth data. Second, the hypothesis in our study is only verified in a static state, rather than transition dynamic. Our specification cannot consider any intertemporal discount rate between housing prices and housing wealth (i.e., a critical variable in the permanent income hypothesis by Friedman (1957)). Thus, our findings should be interpreted with caution. We leave these for future research.

Supplemental Material

sj-pdf-1-irx-10.1177_01600176211066472 – Supplemental Material for Impacts of Housing Booms on Fertility in China: A Perspective From Homeownership

Supplemental Material, sj-pdf-1-irx-10.1177_01600176211066472 for Impacts of Housing Booms on Fertility in China: A Perspective From Homeownership by Yinghao Pan and Hao Yang in International Regional Science Review

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Hao Yang thanks the Ministry of Education Humanities and Social Sciences Youth Fund Project (Grant No. 21YJC790143) for support.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.