Abstract

Starting with an online financial community in South Korea, this article explores the simultaneous production of a new form of subjectivity and a networked ecosystem of financial cultures. Using a multi-sited ethnography to track the movements of users as they moved across different spaces, this article finds that users gifted financial information to each other, blended laity and expertise, and reappropriated financial communities into a third place defined as an informal, public place hosting sociable conversations. Through the grafting of prosocial activities (e.g. sharing, gifting, and social networking) onto financial self-management, users were shaped as networked financial subjects and exhibited a distinctive mode of selfhood informed by both financial subjectivity and neoliberal networked subjectivity. At the same time, their practices spawned countless social, convivial groups as well as entrepreneurial financial gurus. By demonstrating the complex webs of on- and off-line groups, programs, relationships, and social networks, this article illustrates how the networked ecosystem of financial cultures brought the markets and commons into coalescence.

Keywords

Introduction

This article explores an ecosystem inspired by an online financial community in South Korea and discusses networked financial subjects based on ethnographic observations of their practices. Café Ten in Ten, an entry point to this project, is an 18-year-old online financial community. ‘Café’ is a generic term for online communities in South Korea and ‘Ten in Ten’ is an abbreviation of Café Ten in Ten’s slogan Make ten eok won (roughly US$900,000) in 10 years. It is one of the most famous online financial communities, with more than 800,000 users as of April 2019. Bringing a diverse group of users together – lay investors, entrepreneurs, market professionals, salaried employees, housewives, and students – it opened up a space for like-minded people to share interests in personal finance and investment.

Two historical contexts put into perspective the creation of Café Ten in Ten and its continual growth: (1) the rise of ‘wealth-tech’ (chaet’ek’ŭ in Korean) in the wake of the Asian Financial Crisis (1997) and (2) the enrichment of digital cultures. Referring to techniques of personal finance and moneymaking, ‘wealth-tech’ mainly indicates investing in stocks, funds, real estate, and other financial products. This term entered the popular lexicon in the late 1990s under the ruins of the near-collapse of the South Korean economy. The Asian Financial Crisis brought an abrupt end to South Korea’s prior prosperity, causing massive layoffs and underemployment. In return for an IMF (International Monetary Fund) bailout, the South Korean government carried out radical economic restructuring, including labor flexibilization and financial deregulation, coupled with measures for neoliberal social governing (Song, 2009). These shifts unmade the Korean middle class in the following two decades, contracting and fragmenting its members (Yang, 2018). The initial wealth-tech boom and its sustained popularity should be understood in light of this historical transition.

Meanwhile, widespread attention to wealth-tech emerged almost concurrently with the proliferation of informatization discourses and the expansion of digital culture (see Yang, 2017). Online wealth-tech communities began to proliferate during this particular juncture in history, their numbers surging from around 600 in 2003 to more than 42,000 in 2016 (counting only those housed within a particular portal site called Daum). Created in 2001 at the intersection of financial capitalism and digital culture, Café Ten in Ten played a pivotal role in producing a new form of subjectivity, as well as what I call an ecosystem of wealth-tech culture. This article is concerned with both the subject formation and the ecosystem that arose from numerous online communities, texts, bodies, off-line practices, interpersonal relationships, and social networks.

Café Ten in Ten and the proliferation of online wealth-tech communities were emblematic of the reinvention of the self and the citizenry taking place after the 1997 crisis. During the latter half of the 20th century, South Korean citizens had been defined primarily as members of a nation – a unified, docile body – to be mobilized for state-led projects. However, at the turn of the new century, neoliberal discourses that promoted individual responsibility for one’s own well-being came to replace the paternalistic rhetoric of previous authoritarian regimes. Instead of virtual lifetime employment and wage increases by seniority, which were previously available to the urban middle-class (Yang, 2018), financialization and neoliberal reforms pushed citizens to develop themselves as adaptable, competitive, and entrepreneurial. A self-managing subject, therefore, came to represent a new model for the individual citizen (Seo, 2011). Wealth-tech was presented as a pathway toward such a reformed citizenship in this new climate.

Subjects, practices, and ecosystems: constituting field sites through a multi-sited ethnography

In exploring the new form of subjectivity constructed by wealth-tech enthusiasts, this article draws upon a multi-sited ethnography carried out for 2 years in 2014–2016. Beginning with Café Ten in Ten, I moved across various wealth-tech communities to observe the activities, interactions, and relationships of their participants. This method builds on those who consider field sites as constituted, rather than as bounded, stand-alone sites (e.g. boyd, 2015; Burrell, 2009; Hine, 2011; Lingel, 2017). Constituting field sites requires researchers to ‘follow the people’ or ‘follow the thing’ (Marcus, 1998: 90–92), rather than discovering a preexisting field. Likewise, I followed people who were interested in wealth-tech, the materials they produced and consumed (e.g. online forums and posts, particular influencers, books), groups and communities they engaged with, and events they attended (e.g. lectures, seminars, study meetings, social meetups).

If subject formation was the theory that drove this project, the ecosystem became a new object of study that materialized as I followed the people. Indeed, online wealth-tech communities did not operate separately from each other. Rather, many of them developed in close relation with other communities, forming complex webs of users, texts, and practices. Participants joined multiple online forums, interacting with other users and moving across different spaces. Popular posts that had gone viral within their original spaces spread into numerous other communities. Meanwhile, high-profile users – namely, those who might be seen as financial microcelebrities or lay financial gurus as will be described later – played a central role in mediating between financial markets and lay audiences. Such human intermediaries moved across various online communities, encouraging their followers as well to travel between one community and another. Online wealth-tech communities also spawned a wide variety of face-to-face practices – commodified/instructional (e.g. lectures, seminars, workshops) and voluntary/convivial (e.g. meetups, gatherings, study groups) – that in turn would play a significant role in sustaining online interactions. I will map out this cross-platform, cross-line (both on- and off-) ecosystem that was constantly in the making. In this regard, the wealth-tech enthusiasts I observed and interviewed were my research collaborators in generating this ethnography, as well as the builders shaping the ecosystem while making themselves into networked financial subjects.

The double focus on the ecosystem and subjectivity is a gesture toward going beyond the tendency to perceive the proliferation of financial media as either concomitant with or conducive to the expansion of financial capitalism. Scholars concerned with the relation between media and financial capitalism have shown how media discourses, complicit with financial markets, disciplined citizens and hailed them as neoliberal financial consumers (Clark et al., 2004; Davidson, 2012; Greenfield and Williams, 2007). Meanwhile, interdisciplinary research on the culture of financialization has pointed to financial innovations (e.g. derivatives, securitization) as significant technologies of circulation that are central to financial capitalism in which circulation itself takes on a wealth-producing dynamic (Langley, 2008; Lee and LiPuma, 2002; Montgomerie, 2006; Wosnitzer, 2014). In comparison with such abundant writings on top-down discourses and market devices, lesser attention has been paid to the practices of ordinary citizens and to how citizens come to embrace a system that appears dispossessive. This article fills that gap by illuminating the ways in which networked media users socialize themselves into the world of financial capitalism – not via top-down discourses or market devices – but rather through their participation in networked media, or more precisely, through the process of constructing an ecosystem of wealth-tech culture.

Like Couldry (2012), who has called attention to a broader set of media-related practices through which social processes are enacted, this article pays special attention to wealth-tech enthusiasts and the practices through which they formed subjectivity and an ecosystem. Drawing upon ethnographic data, three widespread practices were identified as central to the formation of the ecosystem and its subjects: gifting of financial information; blending of laity and expertise; and reappropriating a financial community into a kind of ‘third place’ (Oldenburg, 1991), described as an informal public place hosting sociable conversations. Building on my previous work that shows how wealth-tech enthusiasts were formed as financial subjects (Kim, 2017), I define the new form of subjectivity constructed through such practices as the networked financial subject, and argue that this subject exhibits a distinctive mode of selfhood informed by both financial subjects – self-governing subjects who take responsibility for their own financial well-being and manage themselves in accordance with norms of the financial market – and neoliberal networked subjects – subjects who engage in sharing and online social networking in consonance with neoliberal governmentality.

In what follows, I first theorize the networked financial subject by putting together a body of literature on networked subjects another on financial subjects. The theoretically driven discussion of networked financial subjects will be interlaced with empirically grounded articulations of the actual practices of Korean wealth-tech enthusiasts, including the gifting of financial information and the reappropriation of a financial community into a third place. This section will elucidate how the grafting of prosocial activities (such as sharing, gifting, and networking) onto calculative practices of financial self-management lies at the heart of networked financial subjects. Next, I will discuss Café Ten in Ten in greater detail, with a focus on its blending of laity and expertise and its welding together of community and commodification. The explicit promotion of community spirit, the creation of socially oriented bulletin boards, and widespread acts of information-gifting appear to indicate the generosity and collectivity of digital culture. At the same time, however, such practices made Café Ten in Ten – in Campbell et al.’s (2009) terms – ‘a tribal space’ composed of ‘Big Men’ and their followers, 1 producing status and commodified communities. Finally, I will demonstrate how such practices ultimately created an ecosystem of wealth-tech culture – webs of on- and off-line communities, programs, texts, and relationships – within which voluntary participation and a wider process of commodification coalesced.

Theorizing the networked financial subject

The networked subject

Far from a conceptualization of networked publics that focuses on technological affordances and the democratizing potentials of digital media (boyd, 2011; Jackson and Foucault Welles, 2015; Papacharissi, 2014), identifying web users as networked subjects draws attention to a broader logic of governing within which users’ active utilization of networked media takes place. Users of networked media exercise freedom and take pleasure in the use of networked technologies; at the same time, the ways they freely choose to use networked media are in tune with the broader logics of governing.

Sharing and online social networking exist at the core of the contemporary governing logic that produces network subjects. Whereas some scholars see the act of sharing as contributing to a less proprietary mode of cultural production (Benkler, 2006; Elder-Vass, 2016; Jenkins et al., 2013) or to greater civic engagements and political transformations (Papacharissi, 2014), others see it as fundamentally imbricated within neoliberal governance. In the latter framework, users’ (in)voluntary, passionate, and/or affectionate participation in sharing valorizes a new form of subjectivity that is tied to marketable interactivity, flexibility, and entrepreneurialism (Arvidsson and Peitersen, 2013; Payne, 2013, 2014). Dean (2009) describes this phenomenon as communicative capitalism and Terranova (2015) describes it as the grafting of sociality onto the technological capacities of digital networks.

While social actions such as sharing, liking, linking, blogging, and software modification appear to restore ‘older values of craftsmanship – reciprocity, collectivity, and fairness’ (Jenkins et al., 2013: 71), contemporary arrangements of such activities are likely to serve the reach of the market economy. Trapped in the fetishization of normative democratic values (e.g. access, inclusion, discussion, and participation), users carry out the kind of labor that secures the continuity and strength of network formations that can be capitalized by media corporations and advertisers (Payne, 2013, 2014) At the same time, contemporary practices of sharing are coupled with neoliberal conceptions of selfhood and sociality while they are encapsulated in such languages as agency, self-activation, and entrepreneurialism. Therefore, active users who engage constantly in online social networking transform themselves in accordance with such discourses and are shaped into active, entrepreneurial citizens of neoliberalism (Jarrett, 2008). As a result, the subjectivity formed through these activities is likely to echo ‘networked and entrepreneurial selves’ (Terranova, 2015: 119).

The financial subject

Abundant writings suggest that the reign of financial capitalism has transformed everyday individuals from passive savers to entrepreneurial investors (Hall, 2011; Jang, 2011). Financial subjectification takes place as ‘an individual “turns him or herself into a subject” (Foucault, 1994: 126) of finance, engaged in investment and borrowing as technologies of the self’ (Mulcahy, 2017: 224). Embracing responsibly the demands of financialized capitalism, everyday individuals have been made into financial subjects who align their goals with financial policies and manage their affairs as a series of investments and returns (French and Kneale, 2012; Mulcahy, 2017). In this regard, they have been seen as self-governing subjects who take care of their own financial well-being based on individualized cost-benefit calculations (Langley, 2008; van der Zwan, 2014). Such calculative, hyper-individual financial subjectivity has been mainly perceived as antithetical and detrimental to community (Davis, 2009).

Recent studies, however, draw attention to the social and interpersonal aspects of financial subjectivity. Anthropologists have shown that in a realm that appears to be dominated entirely by quantification and economic reduction, professional traders do seek social ties, which in turn have an impact on their trading activities (Ho, 2009; Miyazaki, 2013; Wosnitzer, 2014). In a similar vein, studies of (aspiring) lay investors find that financial investments do not necessarily destroy their social ties (Chen, 2013) while simultaneously harnessing interest and disinterest (Fridman, 2016) and creating ‘a strong sense of camaraderie’ and ‘a deep experience of community’ (Campbell et al., 2009: 462). Such invocations of community have to do with financial consumers’ disillusionment with market professionals, while simultaneously indicating the difficulty of having to manage finances on their own. In the same way that networked subjects are caught up in the neoliberal subsumption of sharing and social networking, financial subjects are now witnessing a growing need to re-embed themselves within the social and the communal.

The networked financial subject

The spread of online wealth-tech communities illustrates how contemporary processes of financialization and the development of networked media are intermeshed with each other. By responding to the call to develop themselves not only as financially responsible citizens but also as tech-savvy digital users who can skillfully navigate through networked media, Korean wealth-tech enthusiasts, in exchanging financial information and knowledge with each other, were made into networked financial subjects. Produced at this intersection of financial capitalism and digital culture, these networked financial subjects practice financial self-governing by means of sharing, gifting, and networking.

Information-gifting was one of the most prominent practices for producing networked financial subjects. In addition to simple acts of information-sharing, such as reposting financial news articles and wealth-tech events, highly refined forms of knowledge and information were often gifted as well. The latter case includes summarizing a market report in a manner more accessible to general audiences, sharing one’s own investment strategies, and explaining complex terms and formulas in plain language. This kind of voluntary labor set in motion the constitution of the wealth-tech ecosystem by producing cultural intermediaries who linked lay people to financial markets. In my research sites, those who, without monetary compensation, shared their know-how and skills with novices stressed that their practices were not motivated by self-interest but rather by camaraderie. Such a claim is illustrative of the awkward encounter between financial capitalism and the digital gift economy that is often perceived as an alternative to the market economy.

Contrary to the idea that information-gifting is emblematic of moral values in contemporary digital culture (Elder-Vass, 2016; Green and Jenkins, 2009), however, widespread practices of information-gifting within a wealth-tech ecosystem indicate that the digital gift economy bears a utilitarian value, produces status, and disciplines givers and recipients (see Velkova, 2016). In particular, information-gifting within online wealth-tech communities created a network of social obligations to participate in financial markets. Recipients of financial-informational gifts felt obligated to reciprocate by engaging with wealth-tech, or, to put it differently, to reciprocate by inserting themselves into a circuit of financial capital.

Another significant practice that shaped the networked financial subject was the reappropriation of wealth-tech communities as a kind of third place, defined as ‘a great variety of public places that host the regular, voluntary, informal, and happily anticipated gatherings of individuals beyond the realms of home and work’ (Oldenburg, 1991: 16). Third place refers to a ‘the public space used for informal social interaction outside of the home and workplace’ (Soukup, 2006: 421) and a gathering place ‘perceived as an escape distinct from other settings of daily life’ (Köhl and Götzenbrucker, 2014: 511). A number of scholars have used this concept to characterize digital culture and environments, with a focus on easy access, playful moods, sociable conversations, known regulars, neutral ground, a homelike atmosphere, and an escape from other settings of daily life (see Baym, 2010; Humphreys, 2008). Likewise, many users of online wealth-tech communities, regardless of their initial economic motivations, perceived their online forums as fun, go-to spaces that offered an escape from traditional norms. As a vibrant culture of face-to-face meetings emerged out of these many online financial communities, users also developed social and interpersonal relationships in a variety of convivial settings, such as gatherings, parties, casual meetups, and picnics.

The two notable practices of wealth-tech enthusiasts (i.e. information-gifting and the creation of the third place) indicate that a grafting of prosocial activities onto financial self-management defines networked financial subjects. Born out of a space fraught with tensions between interest and disinterest, the new subject eludes such binaries as markets versus commons, or exploitation versus participation. The next section turns our attention to Café Ten in Ten and its ecosystem.

Café Ten in Ten and the ecosystem of a wealth-tech culture

The birth of Café Ten in Ten

Based on a free online café platform, Café Ten in Ten was created by a white-collar employee in the consumer-credit sector. Heavily influenced by global self-help discourses and disillusioned with authoritarian corporate culture, he created the Café in 2001 to march toward financial freedom with like-minded people.

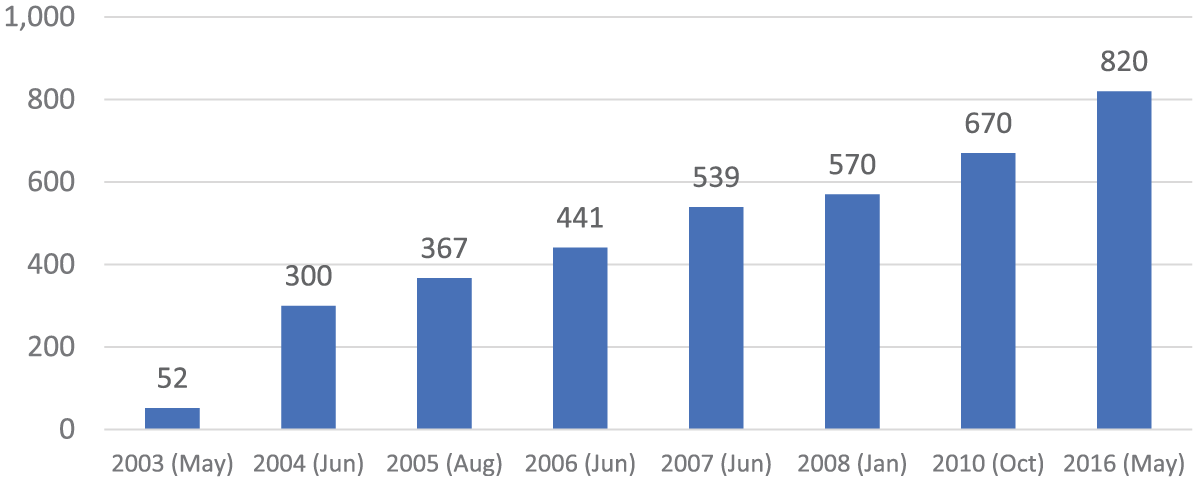

The timely, catchy ‘Ten in Ten’ slogan attracted a diverse group of people. The number of users quickly increased as they sought each other’s opinions about spending habits, household accounting, investment portfolios, and overall wealth-tech plans. The Café received a considerable amount of media coverage, which also contributed to a sharp rise in membership (see Figure 1). With the expansion of user bases and the proliferation of wealth-tech advice materials named after the Ten in Ten slogan, the phrase ‘Ten in Ten’ (transliterated as t’enint’en) was selected as one of the Words of the Year in 2004 by the National Institute of Korean Language.

Number of Café Ten in Ten users (in thousands).

Bringing together members from diverse backgrounds and circumstances (e.g. penny-pinchers, small investors, professional traders), 2 the Café opened up a space for its members to publicly share their wealth-tech experiences – ranging from threshold knowledge for novice investors in each category of wealth-tech (stocks, funds, and real estate) to personal narratives of investment to tips for efficient management of household finances. As of May 2016, Café Ten in Ten had more than 822,000 users, more than 302 million hits, 2.4 million posts, and 10.4 million comments, as well as more than 100,000 daily visitors (Kim, 2018).

The café platform affords the creation of multiple bulletin boards within one café. In the beginning, Café Ten in Ten featured three bulletin boards that set the tone of the community. The first bulletin board functioned as an archive of financial news articles. The second bulletin board allowed users to discuss personal strategies; here, users shared their financial statuses (e.g. assets, debt, salary, and spending) as well as goals and wealth-tech plans. The third bulletin board was meant to be a social forum to encourage users to write about non-financial topics. Participants frequented this specific board to chat about current affairs, celebrity gossip, and their personal predicaments (e.g. relationships, marriages, family matters, jobs). The creation of this socially oriented forum played an important role in reappropriating Café Ten in Ten as a third place that participants turned to for informal conversations, venting, and emotional support. In this way, Café Ten in Ten made itself not only an economic forum but also a convivial, third place.

Many participants virtually hung out in this community and organically formed smaller social groups based on age, location, employment, or preferred investment items. For instance, one of my research participants who was particularly fond of the socially oriented forum often attended off-line meetups and developed various interpersonal relationships within Café Ten in Ten. Even after he had stopped frequenting this community, he described the Café as his ‘childhood home’ where he felt ‘a sense of comfort’ (Interview, 5 June 2015).

Over the course of 18 years, the Café ended up establishing 36 bulletin boards in addition to a chat room. Different categories of wealth-tech were now assigned independent bulletin boards so that users could have more focused discussions. For example, bulletin boards named Real Estate Classroom, Fund Classroom, and Stock Classroom were created. However, the socially oriented board (which ended up being divided into two different boards) always remained the most popular.

Informational gifting and blending of laity and expertise

Defining himself as ‘a community CEO’ (Economy 21, 21 May 2004), the Café’s creator wanted the Café to exhibit strong hallmarks of a community, and not be solely dominated by calculative utilities or a profit-maximizing mind-set. While encouraging users to share information and network with each other, the moderator strictly banned commercial activities such as implicitly luring other users to purchase financial services. Loyal users cooperated to maintain the Café as an ‘innocent’, voluntary association of ordinary people, free from commodification.

The unabashed pursuit of community spirit was related to a widespread distrust of market professionals. In general, neoliberal governance is reliant upon social authorities and expertise, since varied forms of expertise play a crucial role in rendering things as problematic, that is, in constructing a particular phenomenon as a problem requiring a solution (Miller and Rose, 2008). Likewise, in post-1997 South Korea, the financial media, industry, and wealth-tech coaches articulated a set of phenomena (i.e. aging, involuntary early retirement, declining interest rates) in the form of problems that individuals should address.

However, there appeared to be a significant difference between financial experts and other groups of experts. Because their exhortations were seen to be ‘rational and true’, experts such as doctors were able to inculcate in people beliefs about how they should conduct themselves (Rose, 2004: 74–75). In contrast, exhortations by financial economists, professional traders, and consultants were often perceived as incomprehensible or self-contradictory. These experts were distrusted as commodifying and self-serving, given that many forms of financial information appeared to be inseparable from advertisements. In addition, due to market volatility, any ‘expert’ tips that were once perceived as rational and true could appear all of a sudden as irrational, outdated, and wrong. Therefore, instead of depending on market professionals, lay users who demonstrated rich firsthand investment experience and a commitment to sharing their know-how came to be the most esteemed within Café Ten in Ten. Café participants were particularly appreciative when technical knowledge was presented colloquially in ways that integrated real-world experience.

The voluntary practice of information-gifting by those who were not professionally associated with financial markets played a crucial role in sustaining the Café’s popularity and contributed to building a unique ecosystem. In this respect, Café Ten in Ten became a space where expertise and laity were blurred (cf. Binkley, 2014: 18–19). This blurring between expertise and laity had ambivalent impacts. While it heralded the democratization of expertise, making the Café an educational space where novices accessed investment tips (see Bourne, 2017 for a similar case), popular informational givers grew into lay financial gurus with a higher status and fans and ultimately discovered a niche for commercial enterprises.

The birth of lay financial gurus: sharing calculative skills

Lay financial gurus primarily emerged through two bulletin boards: one called Expert’s Column and the other called Leader’s Column. While anyone could write on most of the bulletin boards, these two boards were reserved as spaces where only permitted users could offer advice. One could become an expert relatively easily; if she or he proposed to write on a particular topic over an extended period of time, the moderator permitted her or him to post columns on the Expert’s Column board. But not every expert acquired the badge of being a leader. Among experts, only those who were verified by the moderator to have shown considerable expertise and commitment could attain the leader status. Furthermore, in order to become a leader, columns had to receive positive feedback from other users. The two boards gave birth to many small pundits, lay experts, and even lay financial gurus who, by building their reputations in the Café, came to publish advice books, give public lectures, appear in the mainstream media, and accrue expansive fan bases. 3

Expert Hwang (pseudonym) was one such lay financial guru in the Café. He had no professional affiliation with the financial industry but was an allegedly self-made investor. Beginning in 2004, he regularly posted to the Café as one of its experts. Covering various topics – his philosophy of wealth, effective wealth-tech plans by age, technical advice about securities trading strategies (including bonds, funds, derivatives, and others), real estate investments, and stock recommendations – he attracted many loyal followers. His posts from the Café’s early days are still read and commented on by newer fans who joined years after they had been posted. For example, his post titled ‘Nine Things You Should Know Before Starting Wealth-Tech’, in the Expert’s Column board on June 2004, drew a comment in 2009: ‘This was the beginning of the legend. I am getting a lot of help from your writings, so I tracked your posts in order to save every post of yours’. Another comment from 2014, a decade after the original posting, said, ‘I am reading Expert Hwang’s posts from the beginning. I appreciate your great advice very much’.

Expert Hwang was particularly esteemed for explaining financial intricacies in a relatively accessible way, using a colloquial tone and practical examples. Based on his fame within the Café, he began to write columns in economic newspapers and magazines on a regular basis. He also published four investment guidebooks in 2008–2015, all of which earned him a strong readership. When he published his first book based on the advice columns he had written in Café Ten in Ten and elsewhere, the Café’s moderator posted a congratulatory message that included promotional material from the publisher and described Expert Hwang as ‘our Café’s mentoring anchor’.

Expert Seo (pseudonym) also exemplifies how lay financial gurus emerged through information-gifting in the Café. His specialty was real estate investment, in particular, flipping properties bought through court auctions. He joined the Café in 2004 and, in return for the help and generosity that he had received in the Café, began to share his process of moneymaking in 2008. His initial posts were retrospective narratives of the dramatic process by which he had made his fortune. He saved US$108,000 over 4 years by working in a nightclub and investing in funds. The next stage involved extensive self-learning; after he decided to focus on real estate auctions, he apparently read, three times each, 25 books on that topic. Furthermore, to develop a real estate investor’s sensibility, he went on field trips to see actual homes and surroundings; networking was essential, especially with realtors in each town he visited. In 2005, a rumor spread that an ongoing urban redevelopment project (Seoul’s third new town project

4

) would commence in a new district; this led investors to do a great deal of guesswork concerning its whereabouts. One of Seo’s contacts tipped him off about a condo in a neighborhood that was a strong candidate for this upcoming redevelopment plan. Seo purchased the condo, judging that it was a good deal regardless of the government’s plan. This investment proved to be lucrative, turning a profit of almost US$200,000. Vividly describing such real-world tips, Expert Seo explicitly rejected expert discourses: You have to establish a simple and easy investment rule. Theories that you can’t understand shouldn’t be your principle. Expert theories and prospects never help your investment in practice. First, academic theories such as the ‘Honeycomb Cycle Model’ or Real Estate Cycle. I used them to analyze housing price patterns, whether the current prices were reasonable, and which phase the present was in according to the theories. But it was stupid. It confused me much more. I am doubtful if the authors of such theories have ever bought their properties following their models. Second, real estate experts in newspapers. At the beginning of every year, many analysts publish their predictions about real estate investments – whether you should buy commercial buildings, land, or condos each year. I always acted in the opposite direction to their predictions. When they were pessimistic about condo investment, I bought a condo. […] Now they are presenting optimistic views about condo investment. But once there are optimistic views out there, it is not profitable anymore. (Online post, 16 February 2008)

After his four initial posts, including the above example, received overwhelming responses within the Café, he soon acquired expert status and began to regularly post about property auctions. After that, he became a real estate guru by publishing five best-selling books, creating his own online café (which had attracted around 200,000 users as of 2016), offering for-pay seminars, and training other wannabe investors.

Similar to Expert Hwang, in his columns Expert Seo covered legal and technical intricacies and gave practical tips ranging from how to look up foreclosed homes and how to calculate returns, to techniques for high leveraging and tips for renting out a property. The example below, titled ‘Buying a condo

5

with $2,358’, exemplifies how in his columns he shared his experience. After a long explanation about the process, he added how to calculate the returns:

Price: $25,830 Taxes: $1,080 Bills: $135 Cleaning: $180 Other costs: $270 Total: $27,558

Loan: $16,200 (with a liability to pay interest of $90 each month) A security deposit from a new renter: $9,000

6

Out-of-pocket: $2,358

Rent: $360 Loan interest: $90 Total (rent minus loan interest): $270 I am still holding this property. By investing $2,358, I earned $270 every month. It took less than a year to recover my out-of-pocket expenses. Fortunately, the neighborhood was later selected for the new town development plan so the condo’s market price is currently $108,000 and I will sell it this year because the transfer tax is exempted when you hold it for three years or more.

Monthly rent: $7,830 ($270 multiplied by 29 months) Profit margin: $82,107 ($108,000 minus $25,830) Total: $89,937

The lesson was that average people can flip houses by taking a bank loan and that out-of-pocket expenses can be surprisingly low. Readers also learned that the return on investment (ROI) is calculated by dividing the return not by the sales price but rather by one’s out-of-pocket expenses. This post was commented on recently by his newer fans who wanted to read his writings thoroughly from the beginning.

Given such calculative tools provided by Expert Seo, he, along with other lay financial gurus, might be called ‘economists in-the-wild’ (Callon, 2007; quoted in Fridman, 2016: 11). Such economists in-the-wild offer various calculative tools, accounting logic, and lower-status forms of expertise that help to establish the conditions and knowledge necessary for exchange. In other words, they play an important role in producing financial subjects by offering people an investing vocabulary and norms of calculation (Fridman, 2016; Preda, 2001; Zaloom, 2016). The abovementioned postings by Expert Hwang and Expert Seo illustrate such calculative norms and skills. In this respect, Café Ten in Ten operated as ‘a vehicle by which economic concepts, language, and techniques reach mass audiences unlikely to have direct contact with more legitimate forms of economic expertise’ (Fridman, 2016: 12). By generously gifting such calculative techniques, Expert Seo and Expert Hwang made themselves lay financial gurus.

Indeed, over time, the followers of lay financial gurus transformed themselves into networked financial subjects. In the same way that the lay financial gurus fused generosity with calculative rationality and entrepreneurialism, the self-making by their followers into networked financial subjects involved not just practices of calculative, financial self-governing but also the routinization of information-gifting and social networking. Dongsoo, a 44-year-old computational engineer and unmarried man who had been using Café Ten in Ten for more than a decade and who had been loyally following Expert Hwang’s advice in particular, began to share his own informational gifts on Café Ten in Ten on a regular basis; these were spreadsheets for the 10 most promising mutual funds he selected based on his own formula. He decided to share such informational gifts ‘to motivate [himself] to research regularly which funds are worth buying […] and [because he hoped] more people would become interested in investing in funds’ (Interview, 8 March 2015). The birth of lay financial gurus in Café Ten in Ten and the transformation of users like Dongsoo into networked financial subjects indicate that the division between the producers and consumers of financial knowledge had become increasingly fuzzy.

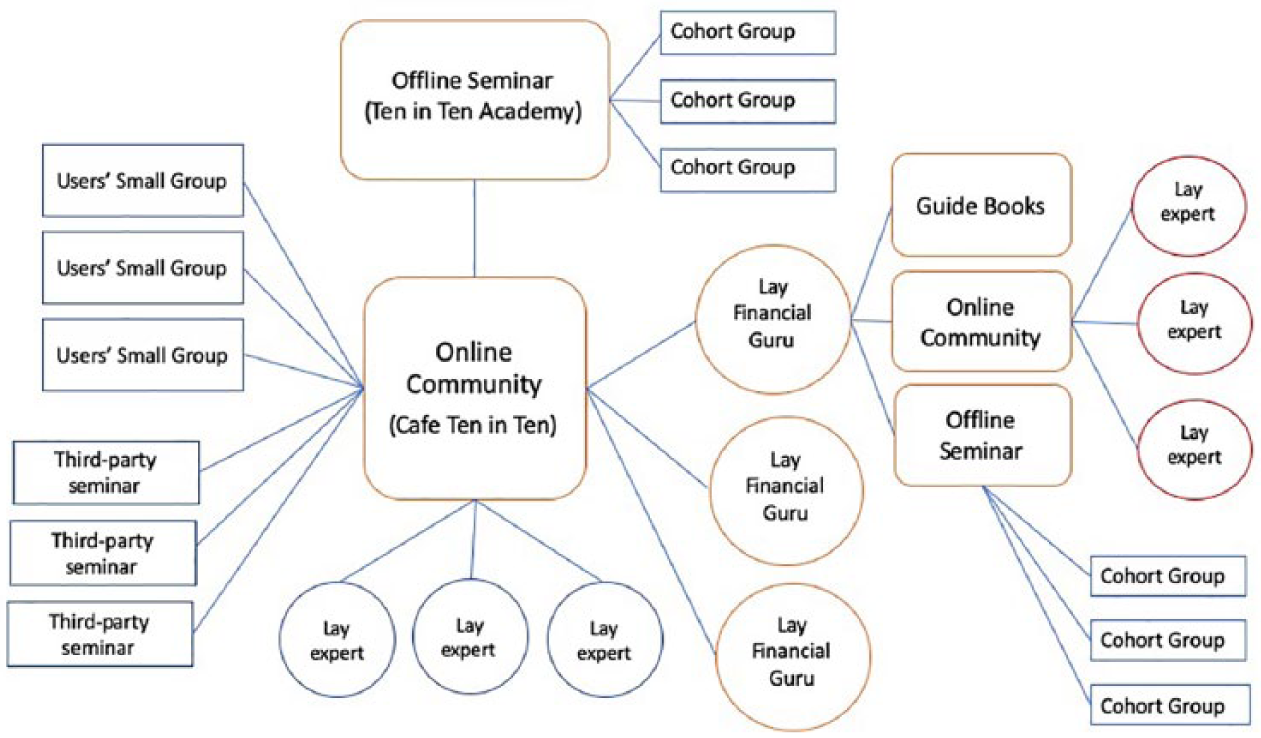

Building an ecosystem of wealth-tech culture

In the same way that the generosity and sociability entailed by information-gifting and the creation of a third place melded with the calculative rationality required for financial self-management, community began to be interwoven with commerce. Above all, Café Ten in Ten incubated a fee-based seminar in 2009, which became a lucrative self-help program during the following decade. During the first half of the Café’s history, the creator of Café Ten in Ten had limited his role to being a moderator of the online space while remaining as one of the lay experts. As he himself became a wealth-tech celebrity, however, he quit his job and began to offer an in-person seminar entitled ‘Ten in Ten Academy’. Made up of five weekly 3-hour lectures and after-parties, the seminar covered how to become rich and why wealth-tech is necessary, as well as financial literacy and ‘Investment 101’ (Kim, 2017). More than 15,000 people took this program while its enrollment fee increased from around US$90 (2012) to US$180 (as of 2018).

The Ten in Ten Academy had two significant consequences. First, it produced numerous ‘Ten in Ten’ cohort groups. After completing the program, a number of participants went on to form their own alumni groups in order to continue their collective wealth-tech learning as well as social networking. Since 2009, a vast number of cohort groups have been formed and sustained, although many of them have also withered quickly. When I repeated the seminar four times in 2014–2015, three out of the four cohorts created alumni groups, one of which demonstrated particularly dynamic interactions both on- and off-line, via study meetings, casual gatherings, and weekend picnics, as well as online chats. Like this group, many cohort groups of the Ten in Ten Academy created their own online groups on different social media platforms, held regular face-to-face meetings, and operated like smaller-scale third places. With the formation of countless cohort groups, wealth-tech cultures witnessed multidirectional, centrifugal connections among participants, all of which could circle back to the on- and off-line entities branded as Ten in Ten.

Second, the combination of Café Ten in Ten (a free online community) and the Ten in Ten Academy (a fee-based off-line program) provided lay financial gurus with a business model to emulate. Many lay financial gurus who were celebrificated within Café Ten in Ten entrepreneurially remade themselves as wealth-tech advisers, reproducing the Ten in Ten model not only by launching an online wealth-tech community where anyone could join free of charge, but also by simultaneously developing a fee-based off-line seminar promoted within the online community. When someone like Expert Hwang or Expert Seo created a new online community and developed an off-line program, his or her followers loyally participated in these new enterprises. Having witnessed the Ten in Ten model snowball from an online community to an off-line program to an unlimited number of cohort groups, latecomers also encouraged their followers to build smaller networking units.

This ever-expanding network of online wealth-tech communities, lay financial gurus, off-line programs, and cohort groups, in addition to a variety of self-organized groups of wealth-tech enthusiasts, comprised an ecosystem (see Figure 2).

Ecosystem of wealth-tech culture.

Moving across different spaces, participants built connections, formed relationships, and transformed themselves into networked financial subjects. The aforementioned Dongsoo, for example, not only used Café Ten in Ten for more than a decade but also took the Ten in Ten Academy and created a cohort group on social media as well. Furthermore, he actively participated in another wealth-tech group voluntarily organized by other Café Ten in Ten users and he gifted financial information even more enthusiastically within that group. Demonstrating a strange entwining of altruism, generosity, and financial self-management, Dongsoo articulated his life goal as becoming ‘a smart investor who helps the have-nots and makes a meaningful contribution to society’ (online post, 18 March 2015). His case illustrates how the new form of subjectivity was produced precisely through the various cross-line, cross-platform, and multi-modal activities that he carried out, all of which simultaneously formed the ecosystem that enlivened its networked financial subjects.

Concluding remarks

While Café Ten in Ten offered a starting point for this research, I followed the movement of wealth-tech enthusiasts as they navigated different spaces, made connections, and transformed themselves into new subjects. Emerging under South Korea’s interdependent development of financial capitalism and digital culture, wealth-tech enthusiasts gifted financial information to each other, blurred laity and expertise, and reappropriated their financial community as an informal, public place for social networking. The integration of prosocial activities into acts of financial self-management produced the networked financial subject, weaving financial subjectivity and neoliberal networked subjectivity together. Turning my attention to the broader ecosystem that materialized through this multi-sited ethnography – instead of focusing on a single community – allowed me to shed light on the complexity of networked financial subjects. I argue that the networked financial subject cannot be grasped simply by looking at media discourses; instead, this new subject draws our attention to the cross-line, multi-platform ecosystem – consisting of bodies, texts, practices, relationships, and networks – that encompasses voluntary organizing and a wider process of commodification.

This exploration of the simultaneous construction of a new form of subjectivity and an ecosystem makes a significant intervention in the interdisciplinary scholarship of the reproduction of capitalist subjects. Although analyses of top-down discourses and social authorities have dominated studies of neoliberal subjectivity, Fridman (2014: 110) points out that ‘much of that transformation into neoliberal subjectivities is undertaken by the subject themselves, making use of popular resources that seem far from the usual government programs of neoliberal reform’. For many Koreans, online wealth-tech communities were one of the most accessible resources when neoliberal socioeconomic reforms were presented to them. Because many of them moved across different types of communities, groups, networks, and texts, an analysis of a single, bounded entity runs the risk of simplifying the complex subjectivities that oscillate between markets and commons.