Abstract

The fact that government-owned firms are typically less proficient or at least less gainful than private owned firms is widely hypothesized. Therefore, the disinvestment policy aims at dropping the participation of the public sector in the economic actions of the country in order to support private sector. The research endeavour set out to empirically examine the financial and operating performance of 15 Central Public Sector Enterprises (CPSEs) disinvested in India through public share offering mode during 2003–2012. Sample firms represent four cognate groups, that is, manufacturing, mining, electricity and service sectors. Through ratio analysis, different ratios such as return on assets, return on equity, sales efficiency, net income efficiency, debt equity, dividend payout, real sales and employment levels have been computed. Using the traditional pre versus post privatization comparisons and panel data estimation techniques, researchers have found significant increase in sales efficiency and net income efficiency, that is, overall operating efficiency, whereas insignificant results have been witnessed in the case of profitability position. This study provides new empirical evidence about performance changes in CPSEs disinvested through involvement of retail investors, that is, public offering mode in Indian economy.

Keywords

Introduction

For a long time, public sector units (PSUs) have been a part of the socio-economic and political values of the Indian economy. Currently, PSUs in India operate at central, state and municipal levels of administration. Ownership rights and management control are held by the central government in the case of central PEs. The state level public enterprises (SLPEs) are owned and managed by the different state governments. Whereas local level government officials hold ownership and control rights in case of municipal level PEs (Sankar et al., 1994). As on 31 March 2014, according to the 54th annual report presented by the Government of India on the performance of central public sector enterprises (CPSEs), there were 290 CPSEs in India consisting of 234 operating CPSEs and 56 CPSEs under construction. With a huge turnover of ₹20,618,660 million, these CPSEs employed 1.351 million people (Public Enterprise Survey, 2014). Through these figures, one can imagine the contribution of these CPSEs in the overall growth of the nation.

Although the significant contribution of all these publicly owned, managed and controlled enterprises is widely recognized in the progress of the country, but their poor monetary return has been a matter of worry—especially since the mid-1980s when, for the very first time, revenue account of the central government became negative (Nagaraj, 2005). Also in the1990s, various problems relating to budgeting, fiscal deficit and balance of payment were faced by the Indian government. All these troubles encouraged the government to release huge finances invested in PSUs (Malik, 2003).

The fact that government-owned firms are typically less proficient or at least less gainful than private owned firms is widely hypothesized. Such PSUs are assumed to waive their profits because of their non-commercial and socially advantageous priorities (Ghosh, 2008). Since years, the governments of various nations have been trying to help the PSUs to become more profitable and efficient. Out of the many efforts, one has been the privatization policy introduced at different levels by different nations. In India, economic reforms were introduced in the year 1991, and privatization programme was an important part of the same (Ghosh, 2008). Privatization process aims at dropping the participation of the public sector in the economic actions of the country in order to support private sector (Gouri, 1997). In India, the government choose to use the terms ‘disinvestment’ and ‘public sector reforms’ to privatization (Arun & Nixcon, 2000).

This research article compares the pre and post disinvestment financial and operating performance of 15 Indian PSUs from four different sectors, such as services, electricity, manufacturing and mining, which got disinvested through public share offering mode during the time period of 2004–2012. There are several reasons that might cause various disinvestment deals launched after the millennium (the year 2000) to differ from those introduced in the 1990s. In the initial years of introduction of economic policy reforms related to privatization, almost all the disinvestment deals were completed through auction method of divestiture except the few deals for which public offering mode was used. Later on after the year 2000 till 2004, strategic sale method was the favoured one in which both ownership rights and management control transfers from public to private sector units. Afterwards, disinvestment through public offering/offer for sale gathered momentum and became the most preferred mode of disinvestment by the government. Therefore, methods of disinvestment deal execution after the year 2000 were also different from those opted in 1990s. In Indian context, almost all the research studies conducted earlier were focused towards analysis of disinvestment deals covering the time zone of 1991–2000 of partial privatization. Therefore, it is interesting to analyze the various disinvestment deals which have taken place after the millennium. This study contributes to the existing literature on disinvestment because it provides new empirical evidence about performance changes in disinvested CPSEs specifically through involvement of retail investors, that is, public offering in Indian economy.

Review of Literature

At the global level, many comprehensive studies have been conducted to check the impact of privatization on the post privatization financial and operating performance of government-owned firms and the literature has shown mixed results.

Megginson et al. (1994) compared the pre and post privatization financial and operating performance of 61 newly privatized firms from 18 countries representing 32 different industries. These firms were privatized through public offering mode and documented significant improvements in firm’s profitability, real sales, capital expenditure, dividend payout ratios and overall operating efficiency. Firm’s debt dependence was found to be significantly abridged. Considerable changes were reported in the structure of corporate board of directors after privatization along with no major decline in average employment level.

Boubakri and Cosset (1998) attempted to verify the same results in the context of 21 developing countries by examining the average effect of full or partial privatizations on 79 companies representing 32 different industries over the time period 1980–1992. Both unadjusted and market adjusted variables were tested in order to control the effect of economy-wide factors. In both the cases, significant improvements were found in all the performance indicators along with increase in employment levels. Firms debt dependence, that is, leverage position, was found to be reduced as expected in case of unadjusted figures only.

D’Souza and Megginson (1999) while reporting the results in the framework of industrialized countries studied the financial and operating performance of 85 companies from 28 industrialized countries over the time period 1990–1996 for pre and post privatization period. Similar to earlier studies, profitability ratio, output, operating efficiency, dividend payment and capital expenditure were found to be significantly improved and debt equity ratios indicating leverage position were reduced. Statistically insignificant decline was witnessed in the level of employment.

Bortolotti et al. (2002) examined the financial and operating performance of global telecommunication industry. The sample consisted of 31 national telecommunication companies from 25 different countries that were either partially or fully privatized through public share offering mode. Traditional pre versus post privatization comparisons were performed along with application of panel data estimation technique. The authors made a sincere effort to segregate the separate effects of competition, regulation and ownership structure on the performance of these privatized firms. Basically, the authors aimed to determine the sources of improvement in the performance of privatized concerns. The results found significant contribution of regulatory changes either alone or in combination with ownership changes on the improved performance of privatized concerns.

Mathur and Banchuenvijit (2007) studied the impact of privatization on the financial and operating performance of 103 firms privatized during 1993–2003 in the case of both emerging and developed economies. Contrary to earlier studies, results derived from data analysis reported statistically insignificant increase in profitability ratios and decrease in employment levels. Here, capital expenditure was found to be declined negligibly. On the other hand, consistent with earlier studies considerable increase was witnessed in this study in the case of other performance measures such as sales and net income efficiency, dividend payouts, output and leverage position.

Sun et al. (2002) studied the impact of china’s share ownership scheme on Chinese state-owned firms and the empirical results reported positive relationship between government ownership and firm performance.

Comstock et al. (2003) analyzed the long-term stock market performance of initial public offerings (IPOs) issued with the purpose of privatization of former state-owned enterprises (SOEs). Unadjusted and excess returns were measured in annual and cumulative terms in order to determine stock performance over the years. First, long-term performance of IPOs was measured and examined from the first day of trading through the period of 5 years. On an average, these IPOs yield lower abnormal returns than the market return over the years. Afterwards, different empirical tests were performed to identify the possible determinants of long-term performance pattern. Among all the determinants, size of an IPO was found to be significantly impacting the stock performance rather than the state of economic development and initial day return.

Omran (2004) premeditated the effect of post privatization ownership structure on the performance of privatized concerns in Egypt. The study advocated significant increase in profitability, operating efficiency, capital expenditure and dividends. Contrary to this noteworthy decline was witnessed in the case of employment levels, leverage and risk along with the insignificant fall in output levels.

Chen et al. (2008) tried to examine the effect of china’s modern restructuring programme on the profitability and efficiency position of SOEs in China and found no performance and efficiency improvements even after restructuring programme.

Peter et al. (2010) investigated the effect in plantation sector of Sri Lanka and have derived significantly positive results in the post privatization period.

Alipour (2013) studied the impact of privatization and organizational changes on the performance of SOEs in Iran. Performance indicators were profitability, efficiency, output, leverage and risk. Iranian firms privatized during 1998–2006 were taken in the sample. Before and after privatization, performance was analyzed, and pooled regression models were applied to check the impact. The empirical results reported negative effects on the profitability, whereas no effect was found in case of sales efficiency at all. As opposed to earlier studies leverage position and overall risk levels had been increased in this study which were tend to be declined. Ultimately, the authors realized an overall need of several economic adjustments along with ownership changes in order to have fruitful results of privatization.

In Indian context, most of the privatization studies present a thorough view of Indian disinvestment policy, related concepts and various emerging issues such as Sankar et al. (1994) studied the experience of disinvestments in Indian public sector enterprises (PSEs). Given the historical background and current scenario of Indian PSEs, the authors presented the profitability status of the same. Afterwards, detailed view was given of philosophy behind disinvestment, its process comprising selection of portfolio of PEs for disinvestment and techniques of share valuation. The study also explained the expectations of Indian government from disinvestment along with its actual outcomes.

Gouri (1997) conducted a survey of PSEs in India. Efforts were made to explore the fiscal dimensions of disinvestment by revealing total amount of revenues since the start of the disinvestment till the year 1996. Various other issues relating to selection of PSEs for disinvestment and the use of revenues from disinvestment were also analyzed and then performance measures of PSEs were studied. The main concern of the research was to study the effectiveness of disinvestment process without transferring ownership. The study concluded that to use the weapon of privatization for efficiency it is required to carefully plan out the areas open to competition and existence of monopoly characteristics where government control must be required.

Arun and Nixson (2000) examined the process of disinvestment of shares in Indian PSEs since 1991 and bring out a list of problems relating to disinvestment such as the assumed under-pricing of shares sold, ambiguity, limited public support for disinvestment and the absence of a common set of goals between the Government of India and the Disinvestment Commission. Other Studies of similar nature were also carried out by Anshuman (2003), Malik (2003), Makhija (2006) and Srivastava (2014).

As far as the studies relating to impact of disinvestment on overall performance are concerned, Naib (2003) compared the performance and efficiency ratios between the pre and post divestiture period of 38 Indian PSEs disinvested over the time period of 1991–2000. The study aimed to capture the impact of partial divestiture on the profitability and operating efficiency of disinvested PSEs. Various performance indicators such as return on sales, return on assets, return on equity, sales efficiency, employment levels and dividend payout ratios were computed with the help of ratio analysis. Paired sample t-test, a parametric one, was applied for testing the significant changes in the variables, and empirical results for the whole sample have presented significant decline in profitability levels as depicted by return on sales and return on equity ratios, leverage ratios. Statistically insignificant decline was found for employment level and liquidity position. Significant improvements were found in dividend payout ratios and efficiency ratios.

On the contrary, some studies remarked positive relationship between disinvestment and various performance indicators of disinvested PSEs such as Gupta (2005) examined the impact of sale of non-controlling equity shares known as partial privatization on the performance of SOEs in India. The sample comprised of 291 regional government-owned firms and the study period was from financial year 1990–2000. While comparing the fully state-owned and partially privatized firms, the empirical analysis found later firms as more profitable, efficient and incurring greater investment in research and development with less government borrowings as compared to former ones. With the application of various research techniques such as fixed effect regression models with dummies, unbalanced panel techniques, generalized method of moments (GMM) regression model, the researcher found positive impact of partial privatization on the profitability, productivity, investments and on the overall firm performance of partially privatized PSEs.

Ghosh (2008) compared the fully government-owned enterprises (FGOs) and partially government-owned enterprises (PGOs) to determine the difference created by disinvestment on the performance of disinvested enterprises in Indian context. Results indicated that FGOs are comparatively less profitable than PGO enterprises. Effects of state and macroeconomic variables were also controlled while measuring the performance impact. The paper concluded that although disinvested firms did not witness improved profitability levels, other performance indicators, such as labour intensity, leverage and wages, had shown significantly positive results. While comparing the methods of disinvestment, the researchers found auction method as the superior method for revenue generation.

Gupta et al. (2011) assessed the pre and post disinvestment financial performance of disinvested Indian CPSEs. In all, 18 financial ratios were calculated depicting profitability, efficiency, liquidity, leverage and productivity levels of sample CPSEs. Out of total 44 CPSEs which got disinvested partially till the financial year 2002, 38 CPSEs were taken as sample for this study. Overall the present study found positive results indicating improved performance of partially privatized public firms in majority of the dimensions after divesting non-controlling shares in the same. Robustness of the results was checked through applying paired sample t-test and independent sample t-test which also witnessed the same results.

Dinc and Gupta (2011) examined the role played by various financial and political factors in the decision to disinvest equity in government-owned firms. Using firm-wise data on both government-owned and privatized firms, hypotheses were developed regarding role of politics in the decision to privatize. Firm size and profitability were used as financial variables and variables representing political factors were political competition and strength, electoral considerations and political patronage. To examine the role of above-mentioned empirical proxies on the likelihood of privatization, regression analysis was applied. Regression analysis revealed that privatization decisions do get effected by firm-level financial variables and location specific electoral factors. This study relevantly contributed in the privatization literature as it explored the major role played by political variables in the privatization decisions.

However, the issue of pre and post disinvestment performance of CPSEs disinvested through public offering mode remains unexplored in India. Therefore, the present study attempts:

To analyze the impact of disinvestment on the financial and operating performance of those Indian CPSEs which got disinvested through public share offering during 2002–2012.

Conceptual Research Framework and Hypotheses Building

Hypotheses

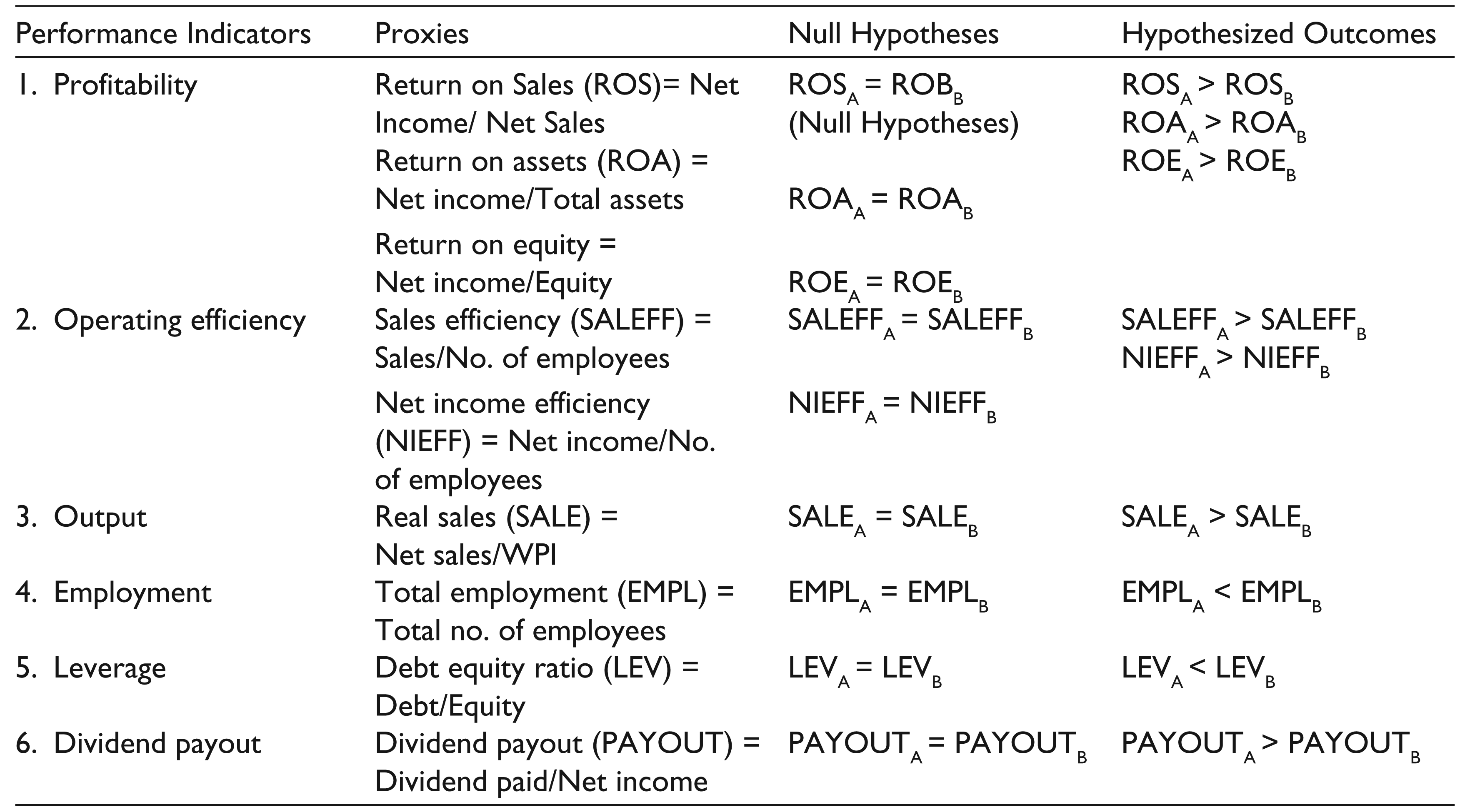

In order to compare the pre and post disinvestment financial and operating performance of disinvested CPSEs, various performance indicators and their proxies as given in Table 1 are identified from existing literature on privatization. The index symbols A and B in the hypothesized outcomes column indicate after and before disinvestment, respectively. While calculating sales efficiency, inflation-adjusted sales (i.e., net sales divided by wholesale price index 1 ) have been used. In the same way, net income is also adjusted for computing net income efficiency. Inflation-adjusted sales and net income per employee are normalized to equal 1 in year 0 (disinvestment year), so other year figures are expressed as a fraction of per capita outcome in the year of disinvestment. Real sales are also computed in the same way.

Based on different empirical studies at global and national level, following results (Table 1) are expected for the sample CPSEs.

Based on Different Empirical Studies at Global and National Level, Following Results Are Expected for the Sample CPSEs

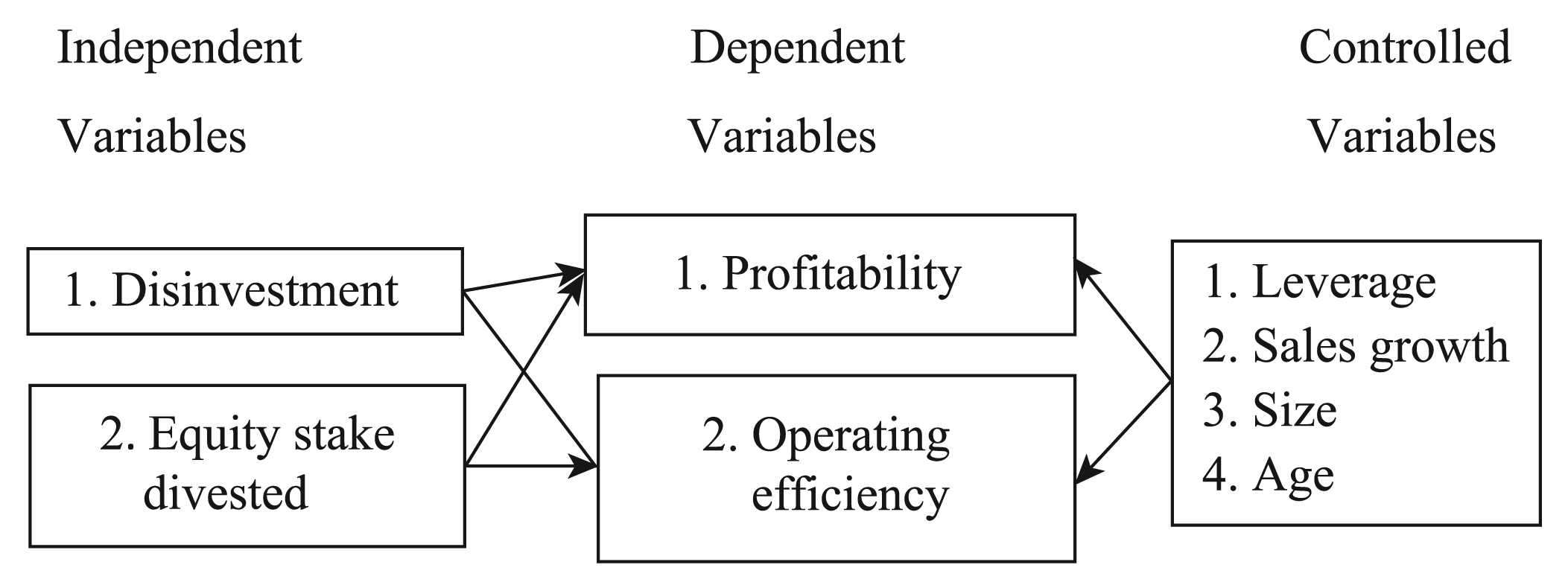

As the traditional pre versus post disinvestment comparisons do not control for several firm-specific control variables which do effect the firm’s financial and operating performance along with disinvestment. Therefore, an attempt has been made in the present study to analyze the effect of divestiture on divested units’ financial performance while controlling the effect of other firm-specific variables as shown in the following research framework (Figure 1) through panel data analysis.

Research Framework

In order to understand the relationship between the dependent and independent variables, research framework is very important. Figure 1 explains the relationship between the disinvestment and the financial as well as operating performance of disinvested CPSEs. On the basis of earlier research studies, the direction of relationship between dependent and independent variable as expected is explained below.

The panel regression framework for firm i and time t is specified accordingly as:

Based on equation (1), the positive sign of disinvestment and equity stake sold coefficients represent positive effects of post disinvestment dummy variable and percentage share sold on the financial and operating performance of divested CPSEs. Perf denotes performance indicator of sample units.

Methodology

Sample

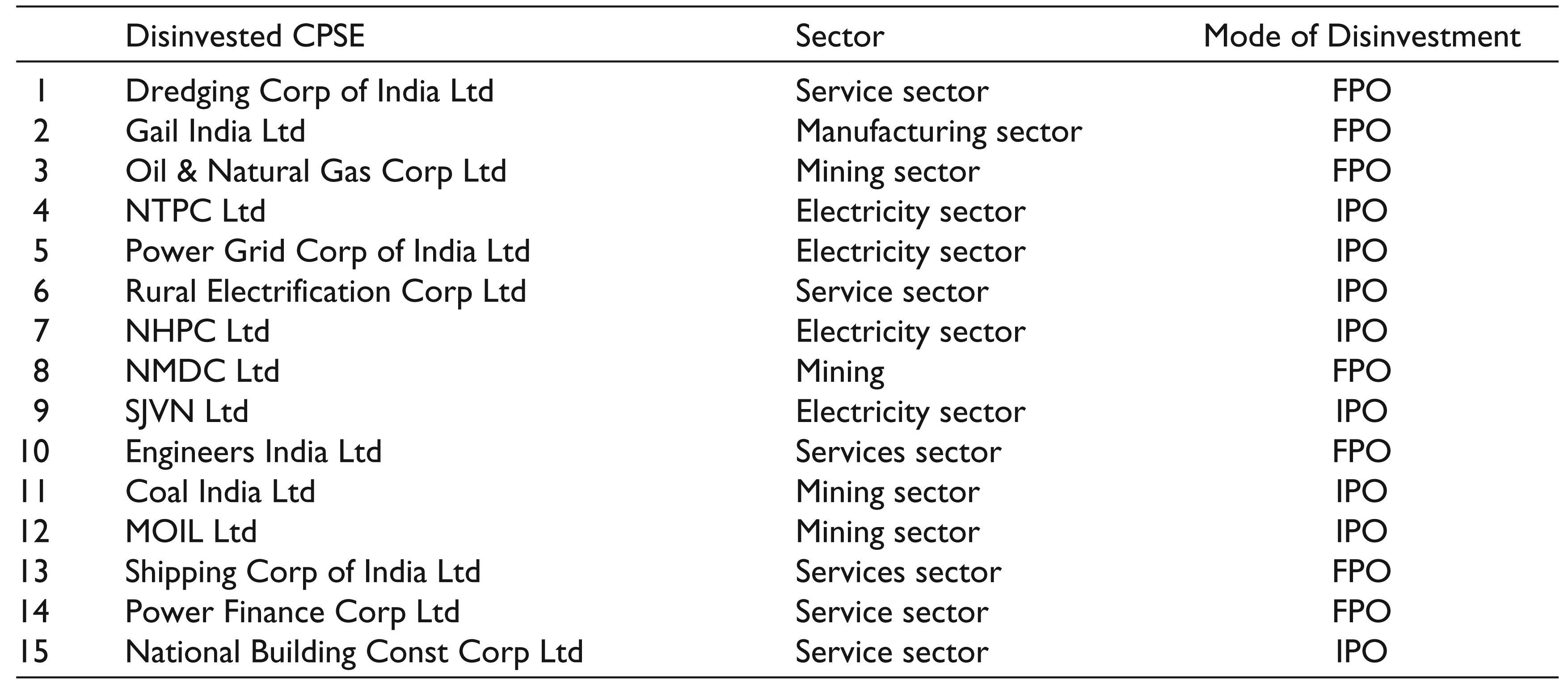

The present study covers 15 Indian CPSEs representing four different sectors, namely, manufacturing, service, electricity and mining. These CPSEs were disinvested through public offering mode during 2002–2012. One major reason for selecting CPSEs disinvested through public offering mode is that these firms keep on generating post divestiture financial and accounting data which have been used for the analysis purposes. Whereas most of the previous Indian studies relating to disinvestment covers the time period of 1991–2000, this study analyzes only those disinvestment deals which have been executed after the year 2000, thereby contributing to the existing literature.

Table 2 provides a brief overview of sample firms.

Brief Overview of Sample Firms

Data

This study is based on secondary data and the same have been collected from:

Different volumes of Public Enterprise Survey being published every year by the Government of India, New Delhi.

2

Official websites of Government of India and Bombay Stock Exchange.3. CMIE Prowess database.

Variables

Several control variables have also been used to control their effect on profitability and operating efficiency:

Techniques

Two types of statistical analyses have been performed on the sample units in order to have most authentic and reliable empirical results. In our traditional univariate tests of performance comparison, standard methodology as developed by MNR (1994) has been used. Different performance indicators as shown in Table 1 include Profitability, Operating Efficiency, Output, Employment, Leverage and Dividend Payout. Ratio analysis has been used to compute various ratios for each company for 7-year time period (i.e., 3 years before through 3 years after disinvestment) and the year of disinvestment has been taken as 0. Thereafter mean values of each variable for every CPSE over the pre and post disinvestment windows (−3 to −1 and +1 to +3) are figured out excluding the year of disinvestment. Than Wilcoxon signed-rank test has been applied to check for significant changes in the set of performance indicators between the pre and post disinvestment period. Descriptive statistics have been employed to explain percentage change in each variable.

Afterwards, panel data estimation techniques are employed to analyze the effects of disinvestment on the financial and operating performance of disinvested sample units while controlling the impact of other firm-specific control variables. A provincial panel data ranging from 3 years prior to 3 years after disinvestment including the year of divestiture itself is analyzed. Hausmen test is used in order to make a decision regarding application of either random effects or fixed effects. This test ascertains the appropriateness regarding the usage of either fixed effects or random effects regression. The null hypotheses (Ho) states that random effects are better and alternative (Ha) is fixed effects are better. Acceptance of Ho means random effect regression is appropriate and vice versa. In the present study application of Hausman test revealed the acceptance of (Ho) in all the cases. Therefore, random effects model is used to analyze the impact of disinvestment on the financial and operating performance of divested PSUs.

Major Findings

Results of Wilcoxon Signed-rank Test

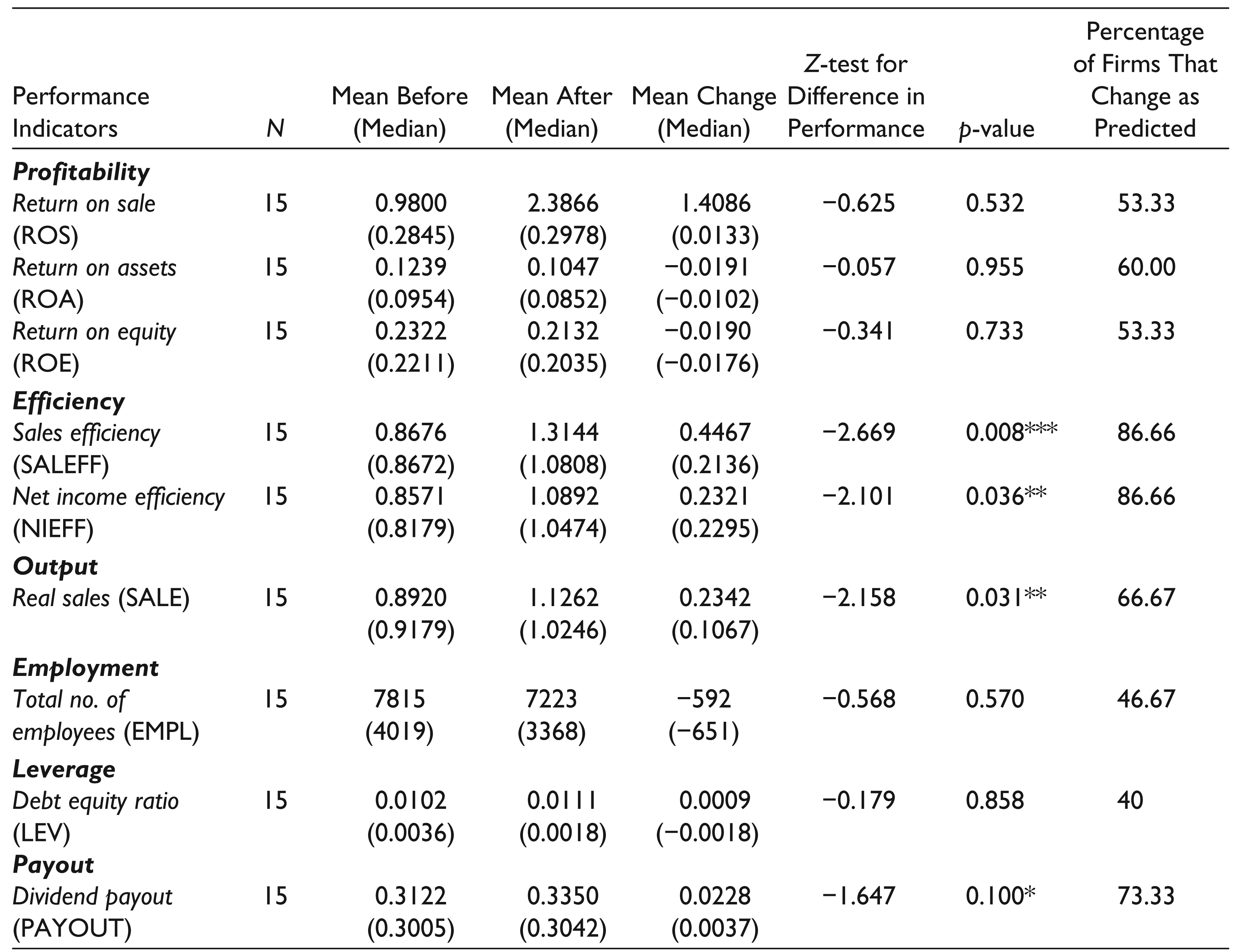

The empirical results found by applying Wilcoxon signed-rank test for the whole sample are reported in Table 3. For each performance indicator, empirical proxies are identified, and for every empirical proxy, the mean and median values are calculated two times, that is, one for 3 years before disinvestment and second for 3 years after divestiture. Afterwards, changes in the mean and median values of each proxy (after versus before disinvestment) are presented in the table. The table shows results of Wilcoxon signed test (z-statistic) and p-values for testing significant differences in the median values of proxies between post and pre disinvestment time periods. Additionally, the percentage of firms whose proxy values change in the predicted direction for each variable is also demonstrated in the last column.

Results of Wilcoxon Signed-rank Test for Disinvested CPSEs in India

Results reported in Table 3 are discussed below.

Profitability Changes

Wilcoxon test results show insignificant changes in the ROS, ROA and ROE ratios of disinvested CPSEs. The mean (median) increase in ROS is 1.4066 (0.0133) from 0.98 (0.2845) before disinvestment to 2.3866 (0.2978) after divestiture and 53.33 per cent of sample firms witness increased profit margins. On the contrary, ROA and ROE are showing insignificant decline in the post divestiture period. As explained by Boycko et al. (1996), Mathur and Banchuenvijit (2007) that transfer of both management control and cash flow rights from the government to private managers may be the one possible reason for increased profitability after privatization. Such may not be the case with our sample of Indian CPSEs where government remains the possessor of controlling and ownership rights, holding more than 50 per cent equity rights even after disinvestment.

Efficiency changes

Statistical results report significant improvements in both sales efficiency and net income efficiency at 1 per cent and 5 per cent level in the post disinvestment period and 87 per cent of sample firms have experienced improved efficiency levels. On an average, SALEFF has increased by 0.4468 (0.2136) and NIEFF by 0.2321 (0.2295). According to Mathur and Banchuenvijit (2007), overall efficiency improves in the post disinvestment period because privatized PSUs use their human, monetary and industrial sources more efficiently because of decreased government subsidies and several other changes after privatization.

Output

Wilcoxon test shows significant increase in real sales after disinvestment at 5 per cent level. Real sales go from 0.8920 (0.9179) pre disinvestment to 1.1262 (1.0246) post disinvestment and 67 per cent of sample firms experience this hypothesized increased output after disinvestment. Improved output in terms of real sales seems to be an expression of better productivity in the post event period. Previous studies such as MR (1994), BC (1998), DM (1999), Dewenter and Malatesta (2001) and Gupta (2005) support our statistically significant result of increased output. Possible reasons for increase in output after privatization as quoted by above studies include more financing opportunities, improved incentives and distended competition.

Employment

The average number of employees in the total sample has been declined to 7223 from 7815 but these results are not statistically significant. Approximately 47 per cent of sample PSUs witness expected results. This insignificant decline in total employment is supported by various privatization studies, namely, DM (1999), Naib (2003) and Mathur and Banchuenvijit (2007). The fact that PSUs are overstaffed for political reasons is widely hypothesized because of which decline in employment level was predicted after disinvestment.

Leverage

Empirical results explain statistically insignificant decline in debt equity ratio indicating no major change in the leverage position even after disinvestment. Forty per cent of sample CPSEs experienced predicted outcomes. Because of withdrawal of debt guarantees by Government, debt levels were expected to be reduced after disinvestment (Mathur & Banchuenvijit, 2007) which may not be the case of Indian CPSEs.

Dividend payout

The mean (median) dividend payout ratio of all firms increases from 31.221 (33.05) to 33.497 per cent (30.42) after disinvestment. Average increase of 2.276 per cent (0.37) is statistically significant at 10 per cent level and 73 percentage of sample firms have experienced these predicted improvements.

Results of Panel Data Analysis

Table 4 displays the statistical results found by applying panel data analysis.

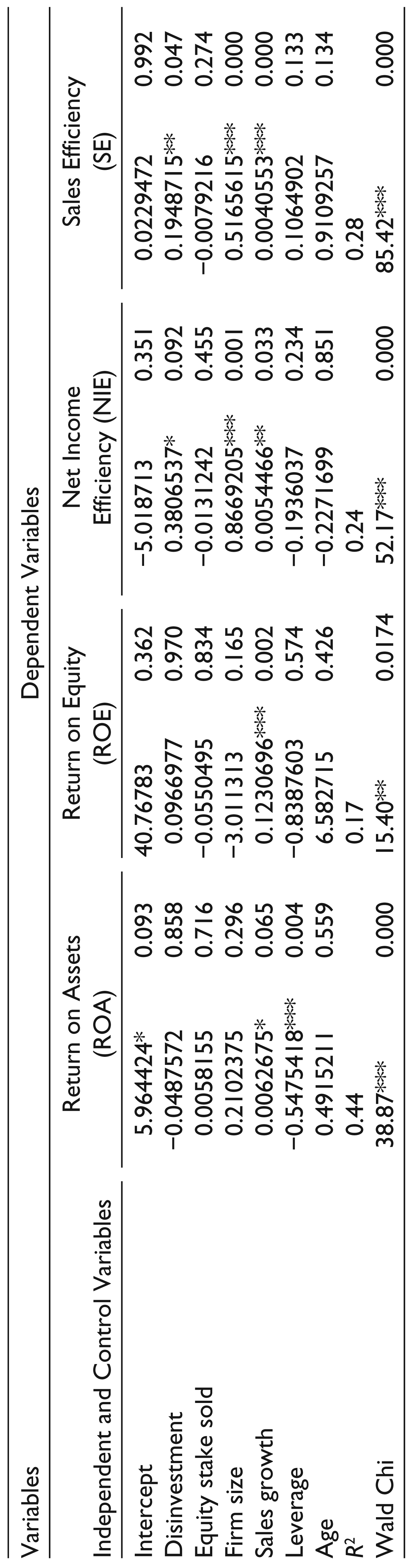

In order to analyze cross sectional variations with time series effects, we use random effects regression technique. Here all the assumption such as multicollinearity, autocorrelation and heteroskedasticity have been checked and provided for as per requirement. Results of the panel data analysis (shown in Table 4) indicate statistically insignificant effect of disinvestment on the profitability position of disinvested public concerns. However, at the same time, significant improvements have been observed in the case of variables indicating operating efficiency of the PSUs. While checking the relationship between disinvestment and net income efficiency, coefficient of disinvestment that is equal to (β = 0.3806537) and p-value < 0.10 per cent (at the confidence level of 90 per cent) shows significant effect of divestiture on the net income efficiency. In the case of analyzing relationship between disinvestment and sales efficiency, coefficient of post disinvestment dummy variable is equal to (β = 0.1948715) and p-value < 0.05 (at the confidence level of 95 per cent) which confirms increase in sales efficiency after disinvestment. Another variable that measures the impact of percentage equity share diluted by the government during divestiture is equity stake sold. The equity stake sold variable has not found to be significantly impacting the profitability and operating efficiency while analyzing the relationship through panel data. The data analysis led us to reject one of the main hypotheses of our research that there is positive impact of disinvestment on the profitability position of disinvested CPSEs. However, at the same time, while analyzing the proposed relationship between disinvestment and operating efficiency, the same is found to be statistically significant which asserts significant positive impact of divestiture on the operating efficiency of divested CPSEs. In order to control the impact of other firm-specific control variables some other variables to name firm size, sales growth, leverage and age have been taken in the regression equation. Among these variables, firm size is found to be significantly impacting the efficiency levels at the confidence level of 99 per cent (p-value < 0.01). Here Beta values in case of net income efficiency and sales efficiency are (β = 0.8669205) and (β = 0.5165615). Sales growth variable is found to be positively and significantly impacting all the four dependent variables ROA (β = 0.0062675) (at the confidence level of 90 per cent; p-value being less than 0.10), ROE (β = 0.1230696), net income efficiency (β = 0.0054466) (significant at 5 percent) and sales efficiency (β = 0.0040553). The results are found to be significant at the confidence level of 99 per cent in the remaining two indicators (p-value < 0.01). Leverage variable as measured by debt equity ratio is found to have significant negative impact on ROA ratio (β = −0.5475418), that is, increase in leverage led to decrease in return on asset ratio (p-value < 0.01). Age of the company is not found to have any significant impact on the profitability and efficiency levels.

Conclusion and Implications

The present article compares the pre and post disinvestment operating and financial performance of Indian CPSEs disinvested through public offering. Along with this, the present research endeavour also analyzes the impact of disinvestment on the financial and operating performance of divested CPSEs through random effects panel data analysis. In the case of univariate analysis, the empirical results reflect that efficiency, dividend payouts and real sales have improved significantly in the post disinvestment period. On the other hand, no such results are reported for profitability, leverage and employment. Validating the results obtained through Wilcoxon signed test, the panel data analysis also reveals significant positive impact of divestiture only on the operating efficiency and not on profitability of divested CPSEs. Coming to the aspect of insignificant improvements in the profitability it has been found that one of the major reasons for it can be attributed to partial privatization transactions in India where substantial controlling and ownership rights to the extent of 51 per cent or more remains with the government even after disinvestment. As already explained by Boycko et al. (1996), one of the major explanations behind enhanced profitability may be the transfer of both control and cash flow rights from the government to private sector. But in Indian context, government is more interested in partial privatization rather than complete privatization in which complete transfer of rights from government to private sector takes place. Most of the Indian PSUs have been disinvested by selling small percentage of ownership and that too in parts. Hence the present study implies that, improvements coupled with major changes are necessary in the present Indian policy on disinvestment. So that, as the efficiency levels have improved significantly as implied from the results of the study, profitability of these PSUs also gets enhanced considerably. In order to improve profits of divested PSUs, the present study supports the suggestions given by advisory panel of NITI Aayog. It has suggested to bring down the governments holding to less than 50 per cent in one stroke instead of selling them in batches (Ranjan, 2016). In the present study, insignificant decline in leverage and employment have been found which should have been significant as per the previous literature. Proactive government efforts are required to achieve optimum targets in terms of leverage and employment in Indian PSUs.

Results of Panel Data Analysis