Abstract

The recent history of finance has been widely portrayed, by both critics and practitioners, as a story about risk. As pointed out by Mary Poovey, focusing on risk entails forgetting uncertainty. In this paper, I argue forgetting uncertainty leads to an inability to distinguish between rational and mystical modes of financial thinking. Using literary-theoretical analysis, I read three exemplary texts across each other: Frank Knight’s seminal 1921 treatise, Risk, Uncertainty, and Profit, which helped justify the modern corporate financial form; Elie Ayache’s 2010 The Blank Swan, a philosophical account of derivatives trading that exemplifies more recent developments in finance; and Don DeLillo’s 2013 Cosmopolis, a novel that remediates the structures of thought implied by the other texts’ philosophical commitments. This textual nexus allows me to explicate the characteristic form of financial mysticism, rendering it visible against claims that derivatives and financial theory have fully rationalized finance.

Portent

Jim Cramer, hedge fund manager turned TV finance guru, perambulates around a studio full of talismanic objects, a fish-eye Steadicam following his every move. Looking deep into the lens, he delivers stock prognostications with the intimacy of a Saint Marks tarot reader. He pounds buttons and tosses chairs. He lets his viewers in on the Truth of the market and dispenses such vital wisdom as, for instance: Today was a good-looking day that was actually quite ugly. Yes, the inside didn’t look like the outside, and you know I don’t think you should judge a book by its cover. I know hope springs eternal, but today we saw too much hope. Too much hope springing eternal. And some of these hopes can’t be reconciled, so they won’t work in the end. (Mad Money, 2019)

In the late 1990s, Stephen Glass of the New Republic passed off a fake story about Alan Greenspan: a Wall Street investment house was keeping an office empty as their ‘Greenspan shrine’. It was littered with relics and memorabilia. Certain traders prayed to the man himself, while others availed themselves of a computer program known as ‘the Talmud of the Federal Reserve’. Though the article was bunk, Glass got away with it for so long because it was so believable. It captured something of the mystical fervor with which Greenspan’s every utterance – and even his pauses – was pored over, probed for its true, occult significance. As a 2000 Vanity Fair article put it, ‘A nod from him about the interest rate and global markets quiver along every nerve and ganglion’ (Hitchens).

In Don DeLillo’s 2003 Cosmopolis, a young and ludicrously wealthy financier, who’s made billions in the notoriously risky foreign exchange derivatives markets, rides a lavish limousine across Manhattan, seeking physical and metaphysical destruction. At a diner, his new wife, a poet, examines him: ‘Tell me this. […] What do you do exactly?’ (p. 19). She answers her own question: ‘You know things. I think this is what you do. […] I think you’re dedicated to knowing. I think you acquire information and turn it into something stupendous and awful. You’re a dangerous person. Do you agree? A visionary’ (p. 19). His art dealer echoes her while convincing him he needs to buy a Rothko. ‘You have something in you that’s receptive to the mysteries,’ she says (p. 30). And later, his Chief of Finance: ‘You should do the seeing. You’re the seer’ (p. 46, empahsis added).

These stories are familiar. Financial titans are oracles. Reading signs inscrutable to the uninitiated, they have a superhuman ability to presage the future. Masses greedily seek their predictions and jealously guard their insights. Money managers, finance wonks, financial media celebrities… they are so many hierophants in a longstanding financial mysticism. However, and at the same time, this mysticism sprouts in a field claiming to be at the cutting edge of rational inquiry. Since the 1970s, financial theory has laid claim to the nec plus ultra of scientific thought, from particle physics and quantum mechanics to all sorts of esoteric mathematics. As the ranks of financial actors filled with PhDs, as financial prediction became overwhelmingly mathematized, and as abstruse new financial instruments promised to account for every possible future, an apparent rationalization of finance bloomed alongside the mysticism. What’s more, neither the rationalism nor the mysticism, which should contradict each other, seems in the least unsettled by the other: they exert overlapping, possibly mutually-reinforcing, influence in the very same sphere, so much so that it becomes exceedingly difficult to distinguish one from the other. This essay examines how this is possible, identifying the structure of thought that allows for these positions’ coexistence and revealing the philosophical mistake that leads to their confusion.

Introduction

In 1921, the economist Frank H. Knight distinguished risk from uncertainty. Risk, he wrote, regards future possibilities one can know about, either through deduction or statistical inference. Uncertainty, on the other hand, regards future possibilities about which there are no valid grounds to judge. Risk, then, can be dealt with through rationality, while uncertainty cannot.

While the substance of Knight’s distinction has become somewhat standard in theories of finance, its consequences have not been heeded. As Mary Poovey (2018) points out, this followed on the spread of technologies during the 20th century that made the future more and more calculable. Increasingly-sophisticated accounting methods, increasingly-recondite mathematics from game and probability theory, and increasingly-ambitious efforts to manage what had recently become known as ‘the’ economy all converged to bolster the idea all risk can be managed. This tendency in mid-20th-century economics only intensified in post-1970s finance, and the story of financialization has been told as a story of risk. In the early 1970s, methods were found to quantify the risks of derivative contracts, including the Black-Scholes-Merton equation (e.g. Beunza and Stark, 2004; MacKenzie, 2006). In 1973, the Chicago Board Options Exchange opened, inaugurating a new derivatives market for hedging against or speculating on risk (Zaloom, 2006). Complex securitization processes bundled and unbundled risk (Konings, 2011), and many traders came to see their jobs as buying and selling risk (Ho, 2009). New financial instruments were praised for enabling markets to perfectly hedge risk (Amato and Fantacci, 2011), leading some to claim, before the 2008 crisis, that no crisis was possible (Frontline, 2014). Even after the crash, arguments to strip away financial regulation maintained that derivatives rationalize the market, mastering risk (Davis Polk, 2017).

Critical accounts of finance in the social sciences and humanities have followed these developments carefully, closely tracking risk. Benjamin Lee and Edward LiPuma (2004) characterize financialization as ‘the globalization of risk’. Louise Amoore generalizes the derivative’s risk-disaggregating logic to describe, to quote a title, ‘The Emergence of a Security Risk Calculus for Our Times’ (2011). Elena Esposito (2011) shows how modern entrepreneurial subjects emerge through the creation of a particularly financial ‘risk rationality’. And Randy Martin (2015) identifies derivatives as ‘instruments of risk management that generated unmanageable risks’. The list goes on.

Uncertainty, on the other hand, has borne less critical scrutiny. Some writers gloss over the distinction (Esposito, 2011; Malik, 2014) while others who insist on it nevertheless emphasize risk (Amato and Fantacci, 2011; Bougen, 2011; LiPuma, 2017). Following calls from de Goede (2005), O’Malley (2005), and Poovey (2018), this paper instead closely attends to uncertainty. Because focusing on risk emphasizes that which can be dealt with rationally, focusing on risk privileges a narrative of rationalism, and it cannot account for financial mysticism. This blind spot is important. To examine the nexus of risk, uncertainty, and mysticism in the financial sphere, I’ve selected three texts – an influential early-20th-century theoretical account of the entrepreneur’s relationship to uncertainty, a former derivatives trader’s philosophical account of the trader’s relationship to contingency, and an artistic remediation of these ideas. The first two emblematize important historical conjunctures, while the latter provides an opportunity to further explore the cultural circulation of these ideas.

I begin with Frank Knight’s 1921 treatise, Risk, Uncertainty, and Profit. Knight, with Jacob Viner and Henry Simons, constituted what’s sometimes called the ‘first Chicago school’ (Rutherford, 2010: 27), and, though he cared more about supplementing economics with ethical analysis than many of his acolytes, the postwar Chicago school grew out of the scholars that had gathered around him in the 1930s (Emmett, 2010: 3; Medema, 2010: 40). By the end of the war, Knight’s work and liberal philosophy had become influential across the United States, and his international influence expanded greatly when Lionel Robbins made Risk, Uncertainty, and Profit required reading for an economics degree at the London School of Economics (Brady, 2010: 238). Crucially, Knight’s treatise intervened in debates surrounding the emergence of the modern corporate financial form, with his argument explicitly justifying top-heavy distribution of corporate profits. Thus, I take Risk, Uncertainty, and Profit, which profoundly influenced the thought of last century’s economics movers and shakers and shaped the emergence of a still-dominant financial form, to emblematize the historical conjuncture of early-20th-century business economics.

As mentioned, following Knight’s distinction between risk and uncertainty, new mathematical techniques and data corpuses helped diminish economic uncertainty. However, during the middle of the century, an elaborate financial system relatively independent from economics (compared to earlier finance) came into power, and from the late 1960s through the 1980s, several factors greatly increased uncertainty in finance: the rise of Eurodollar markets moved many US dollar accounts offshore, out of sovereign control; fixed interest rates around since 1945 crumbled, introducing currency risk; and newly monetarist central banks, frequently changing benchmark rates to target the money supply, boosted interest rate volatility. As the authors of a derivatives textbook write, ‘These changes resulted in a quantum leap in the level of uncertainty faced in the financial markets’ (Somanathan and Nageswaran, 2015: 95). The ensuing demand for risk management tools fomented a derivatives boom that fanned the flames of the ongoing financialization. In this period – the birth of contemporary finance – the mysticism of business economics morphs. To examine the financial mysticism that emerges, I take up the work of Elie Ayache, a Lebanese-born, École Polytechnique-trained engineer who spent eight years trading derivatives before turning to philosophy in 1995. Ayache, a practitioner during the late-1980s consummation of these developments in finance, later wrote The Blank Swan – my second emblematic text – a densely-philosophical account of how traders deal with the unknowable, or, as he puts it, of markets as the medium of contingency.

Mysticism emerges as my operative concept because I’m less interested in what the financial actor does than in how financial action is understood. The slight but significant difference between my and Joshua Ramey’s consonant work clarifies this point. Because Ramey is interested in financial action, he takes up the practice of divination, defined as ‘systematic solicitation, generally on the basis of chance, of more-than-human wisdom’ (2016: 5). I, rather, take up the belief of mysticism, defined as the belief that there are domains inaccessible to rational knowledge that can nevertheless be apprehended or intervened on through subjective experience. A mystical ability is one supposed to operate outside rationality and knowledge. Beliefs in inexplicable intuition or insight, for instance, evince mysticism. 1

Pursuing belief, it will be invaluable to venture outside philosophical accounts and consider cultural portrayals of finance. While I briefly examine the financial media, I’ll move across the philosophical material with my third exemplary text, Don DeLillo’s 2003 Cosmopolis, a novel about a wealthy fund manager dedicated to the asset trading strategy known as chartism. Widely taken up to think about how finance is represented (e.g. Shonkwiler, 2017; De Boever, 2018; Sjol, 2020), Cosmopolis directly addresses the mythic status of the financial actor. Is it not rather striking that a major American novelist – particularly one known for attempting to render in narrative the experience of contemporaneity – chooses to write a novel about an asset-trading strategy? I take up the book on the following precept: if the novel constructs an edifice in which philosophical commitments characteristic of contemporary finance find coherent artistic expression, this edifice can be used to illuminate and explicate both those commitments and their consequences. Put otherwise, I value DeLillo’s novel for its emic – if stylized – depiction of financial mysticism, and I use it to enrich my readings of the philosophical material.

By interweaving readings of a germinal account at the advent of the modern financial corporate form, the philosophizing of a practitioner active during the latest financialization, and a novel that remediates financial mysticism, I knit a thick cloth in which explicit positions and implicit commitments, persistent assumptions and challenged beliefs, and baffled reverence and suspicious dubiety are stitched together, giving a textural account of this financial mysticism. The abstruse esotericism of cutting-edge financial theory, insistently foregrounding its risk management function, seeks to conceal this mysticism; by learning its folds, we can refute the occlusion. Keeping mysticism in view, we can contend with its consequences with clear eyes.

‘Nothing Applies’

Cosmopolis begins with its protagonist, an obscenely wealthy 28-year-old fund manager named Eric Packer, deciding he wants a haircut. However, since the US President is in Manhattan, it will be very difficult to get across town. Still, Packer insists. The book unfolds over one day as he rides westward on 47th Street in his limousine, speaking to several employees. All the while, he is losing exorbitant amounts of money betting against the yen. He believes the yen cannot go higher; it keeps going higher. During his voyage, he is attacked by an anti-capitalist protest that takes over the Nasdaq building, runs into the funeral of a rapper and Sufi mystic he admires, and repeatedly encounters his new wife, a poet and heiress. He learns of a credible threat on his life from his chief of security, whom he loathes. Eventually, he kills his chief of security, wipes out his whole fortune, steals his wife’s fortune and wipes it out too, and gets half a haircut. At novel’s end, he seeks out his would-be assassin and ponderously chews the fat with him. Then he peers into the crystal face of his watch and sees his own dead body. On the closing page, he waits for a bullet in the back of his brain.

Packer made his multi-multi-millions in the notoriously high-risk foreign exchange markets using a technique called ‘charting’ or ‘technical analysis’. The opposite of fundamental analysis, which focuses on economic fundamentals, technical analysis ignores fundamentals to consider only financial price movements. In a process sometimes referred to as ‘voodoo finance’, often compared to astrology (MacKenzie, 2005: 556), and sneered at by many mathematical economists (Nazário et al., 2017), the chartist seeks portents of future movements in abstruse patterns in historical movements.

Though the haircut is his stated mission, Eric’s real challenge is the ongoing yen kerfuffle. In his limousine, Packer’s currency analyst, Michael Chin, tells him they’re leveraging too rashly. Eric clearly states his mysticism: ‘Nothing applies. But it’s there. It charts. You’ll see it’ (p. 37). Saying ‘nothing applies’, Eric says precisely this: the situation is one of uncertainty.

Frank Knight’s 1921 Risk, Uncertainty, and Profit, in which Knight distinguished risk from uncertainty, refuted two prevailing theories of profit: the dynamic theory and the risk theory. The dynamic theory held change over time made profit possible, but Knight points out not change itself but only unknown change can create profit, since known change would be factored into prices. The risk theory, which held exposure to risk generates profit, made the same mistake. Risks can be treated, in large enough numbers, as certainties. While a business often can’t do this alone, several businesses’ risks can be grouped; this is the function of insurance. Neither risk itself nor change itself can explain profit: only the unknown can. To make a fine point of this, Knight distinguishes between three cases.

First, risks whose probabilities can be determined a priori, like throwing a die, exist when instances are homogeneous: each die throw is exactly like the others.

Second, the probabilities of statistical risks can be known through previous instances. Sufficient heterogeneity makes a priori calculations impossible, but sufficient homogeneity means instances can be reasoned about as a group. Knight’s exemplar is houses’ fire-risks. Historical fire rates in sufficiently-similar houses give the probability a house will burn.

Third, some risks have unknowable probabilities, meaning they are outside probability. Here no calculation, neither a priori nor statistical, is possible, as instances are so heterogeneous as to have no sufficiently-similar precedent. For this reason, Knight says these are not actually risks, since risks must admit of probability. Knight names them ‘uncertainties’.

‘Nothing applies,’ says Eric Packer: the situation is one of uncertainty. Nothing can be known a priori, nothing can be known statistically. When he says this, he means no model can be fitted. No foreknowledge is possible. ‘Nothing applies,’ he says, but then, ‘But it’s there. It charts. You’ll see it.’ If nothing applies, how can it chart? If no model applies, how can it be there? What tool of prediction can wrangle it? It cannot be known, Packer says, but we will know it.

Even though uncertainties are unknowable, Knight writes, we form ‘judgments’ about them. We conceive of these judgments as probabilities though they are not. And while there is therefore no chance of gauging the probability of whether or not we are correct, we also form a judgment of our confidence in our judgment. This idea, in itself, would not be mystical if Knight merely believed we were deceiving ourselves. However, for him, people have different aptitudes for judgment. Some people are better at apprehending the unknowable future than others. In particular, judgment’s paradigmatic figure is the entrepreneur, about whom, Poovey notes, Knight writes in almost ‘biblical’ tones (2018: 223). The entrepreneur confronts uncertainty, since almost no situation in business can be reasoned about a priori and most cannot be treated statistically, and deals with it. He forms judgments about a future he cannot know about, and, if he is a good entrepreneur, he’s usually right.

At Cosmopolis’s start, Eric receives his mission in a revelation: ‘He didn’t know what he wanted. Then he knew. He wanted to get a haircut’ (2003: 7). He makes no choice, and despite the use of ‘know’, this is not a process that happens within knowledge; it is simply given. Likewise, at novel’s end, he gets up in the middle of his haircut and steals into the night, heading for his assassin. His betrayed barber: ‘But how come?’ Eric: ‘I need to leave. I don’t know how come. That’s how come’ (2003: 169). This ‘knowing’ outside knowledge is what Knight means by judgment, which he even compares to prophecy (though later I’ll give a special sense to ‘prophecy’). Judgment often starts with ‘a lot of irrelevant mental rambling, [but] the first thing we know we find that we have made up our minds, that our course of action is settled. There seems to be very little meaning in what has gone on in our minds, and certainly little kinship with the formal processes of logic’ (Knight, 1921: 211, emphasis added). At the novel’s outset, first thing we know, our protagonist has made up his mind. There is no question of formal processes of logic. He wants a haircut. ‘The ultimate logic, or psychology, of these deliberations is obscure,’ Knight maintains, ‘a part of the scientifically unfathomable mystery of life and mind. We must simply fall back upon a “capacity”’ (1921: 227, emphasis added). There exists a non-rational capacity to deal with the unknowable future. This is Knight’s mysticism, the mysticism of the entrepreneur, the belief in what I call mystical prediction.

According to Pat O’Malley, three sequential liberalisms each had a characteristic relationship to risk and uncertainty. The laissez-faire era, in the headsprings of which we find Frank Knight swimming, focused on uncertainty. With its emblematic entrepreneur, it touted enterprise’s creative role. In the welfare state era, with planned economies in vogue, risk management through actuarial methods reigned, and the emblematic figure became the expert. Neoliberalism, refocusing on uncertainty, again stressed creative enterprise, but expert-driven risk analyses and their ‘mathematical dramas’ endured (O’Malley, 2005: 464). In this era, ad-hoc, intuitive wrangling of the uncertain future coexists with and even co-opts mathematical risk analysis. To emblematize this heady admixture of mysticism and hyperrationality in late-20th-century finance, I nominate, rather than the entrepreneur, the derivatives trader.

Disentangling Contingency from Uncertainty

Elie Ayache, after eight years trading derivatives, turned to philosophy in 1995. He then wrote The Blank Swan (2010a), which Katherine Hayles called ‘a neoliberal fantasy run wild, fueled by Quentin Meillassoux’s […] philosophical argument for the absolute nature of contingency and applied by Ayache to finance capital' (2017: 148). Slurs aside, there’s plenty to learn about the esotericisms of high finance from it.

The Blank Swan is a take-off of Nassim Taleb’s influential The Black Swan: The Impact of the Highly Improbable (2007), which argues history is routinely defined by extremely unlikely events, or ‘black swans’, and therefore probability-based preparations are bound to miss the mark. Focusing on financial markets, Ayache takes issue not with Taleb’s argument but his belief structure, for Ayache contends the black swan paradigm is hopelessly beholden to a fundamentally misguided belief that the market is a matter of probability (2010a: xvi–xvii). Ayache proposes to rewrite Taleb’s book without probability. For this, he’ll need contingency.

Ayache most clearly explains what he means by contingency when assessing the three kinds of black swans described by Taleb. Ayache dismisses the first two – both primarily psychological. Only the third, ‘the Black Swan that cannot possibly be predicted because it falls beyond knowledge and probability’ (2010a: 11–12, emphasis added), interests Ayache: these, he says, are contingencies. Knight’s interest was likewise in that which falls beyond probability, but Ayache helps us see a slippage in Knight’s terminology.

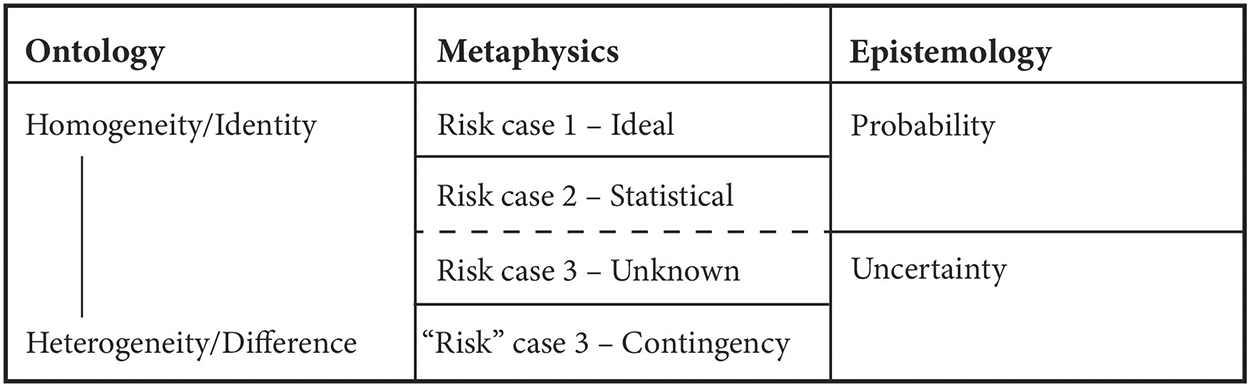

Contingency distinguished from uncertainty. Courtesy of the author.

In the primarily-philosophical chapter in which he defines uncertainty, Knight writes he is interested in what cannot be known ahead of time: what Ayache calls contingency. Yet in the subsequent, primarily-economic chapters, he’s evidently interested in that which is unknown but not unknowable. The cleavage within his uncertainty appears because he slips between epistemological and metaphysical registers. Indeed, ‘uncertainty’, which describes a condition of knowledge, is not the best word for a metaphysically-unknowable thing. I propose we think instead of two parallel divisions alongside an ontological spectrum running from homogeneity to heterogeneity (Figure 1).

Both ideal and statistical risk fall under the knowledge condition of probability. However, under the knowledge condition of uncertainty, we have two statuses. There are unknown risks, which are not in principle unknowable. Unknown risks could be brought into either of the first two cases: nothing in their nature distinguishes them. Discovering a law that governs them could make them case one risks – what I’ll call the deductive method. Identifying a sufficiently-homogenous class of instances to make historical knowledge possible could convert them into case two risks – what I’ll call the statistical method. (Both methods will be important in subsequent economic development, as we’ll see.) In principle, this category could be emptied, and all risks could become known: there would be no risks under the knowledge condition of uncertainty. However, there would still be contingencies. This is the philosophical importance of Knight’s distinction: the contingent, which can never be brought under the knowledge condition of probability, admits of no foreknowledge, no matter how advanced our sciences. His mysticism consists of believing it can be dealt with with foresight.

For Ayache, contingency evades probability because probability is always determined in relation to a context, and the black swan changes the context: it therefore definitionally evades pre-imagination, since if it were pre-imagined the context would have been changed to include it. To make this point, Ayache borrows Taleb’s example about a casino that, probabilistically computing risk, was certain it would earn money – after all, the house always wins. Then it was hit by four black swans in a row, starting with a tiger maiming an irreplaceable performer and ending with the owner ransacking the coffers to pay ransom for his kidnapped daughter (2010a: 12). While the casino may now add these events to its risk calculation, Ayache writes, that’s not the point: they did not belong to the context. To claim they could have been predicted misses the point; this imagined predictability is only a retrodiction. A backward-projected, forward-looking narrative of the past, it props up the illusion of probability.

The illusion of probability, says Ayache, is particularly given the lie by the black swan of quantum mechanics. Probability ‘is based on the prior knowledge and stability of the states of the world, the so-called universe of possibilities’ (2010a: 15). However, with quantum mechanics the universe of possibilities is neither stable nor knowable. There’s no single collection of possible ‘states of the world’: only once the context is decided will it be determined which states of the world are attainable. Experiments performed in one order obtain a different possibility space than experiments performed in another. These incompatible contexts cannot be unified under a probability regime before their determination.

For Ayache, quantum mechanics communicates a profound philosophical truth. Possibility ‘is only a copy and a replica of the real, always derivative, always occurring after the real (both in time and in style) and never before it’ (2010a: 16). It simply is not the case that there are many unreal future states of the world of which some become real. Rather, reality comes about directly through contingency. Thus probability itself, coming after the definition of context, is only a retroactive narrative that makes the event seem to have been predictable. In the world of the black swan, there is no prediction, only retrodiction.

So, when Ayache writes ‘This notion of radical change, or change beyond (or rather, before) possibility, is what I call contingency’ (2010a: 16), he is not simply pointing to change as contingency: he doesn’t fall into the trap Knight identifies in the dynamic theory of profit. He’s interested in precisely what Knight – in his philosophical chapter – was interested in: that which is unavailable to foreknowledge, outside probability (1921: 224). As with Knight, this is a matter of being far from homogeneity or identity: ‘The contingent […] departs from the plenitude of identity (i.e. it is difference)’ (2010a: 45). This is what Ayache defines as contingency, and it hides within Knight’s cleft uncertainty. 2

The Judgments of Others

When Chin, Packer’s currency analyst, says they’re leveraging too rashly, Packer responds, ‘It’s going to turn our way.’ And Chin: ‘Yes. I know. It always has.’ Here, Chin assents to Eric’s confidence because he has formed a positive judgment of Eric’s judgment.

For Knight, judgments of our own judgment are less important than judgments of the judgment of others. While both should be nonsensical since judgments are made in the absence of the possibility of foreknowledge, some people do turn out to be particularly adept, like Knight’s fabled entrepreneur. Importantly, in what Knight calls ‘one of the mysteries of the workings of mind’ (1921: 281), we can know certain men to be better at this mystical ability. ‘Men do form, on the basis of experience, more or less valid opinions as to their own capacity to form correct judgments, and even of the capacities of other men in this regard’ (1921: 228). This second-order judgment, widespread in understandings of finance, underpins the reverence for financial prophets. Hayek, for instance, held that the disciplined market actor could ‘somehow’ transcribe knowledge of the unknowable future, the proof being his success (Ramey, 2016: 2). Neither Knight nor Hayek nor anyone can explain how, since it cannot be explained, but we are able to judge the capacity of others to judge in situations in which reason is impossible.

This leads us to a peculiar kind of knowledge: even without being mystics ourselves, the existence of mystics allows us all to better deal with the contingent future. Knight asserts that instead of considering relatively homogeneous cases, we can simply emphasize the judgment, even in singular cases, of a man [sic] whose judgment we trust. ‘That is, instead of taking the decisions of other men in situations more or less similar objectively, we may take decisions of the same man in all sorts of situations’ (1921: 228). For Knight, the mystical capacity transforms the unknowable into something that can be treated as risk. The mystic intercedes between us and the unknowable, and we simply treat what we receive from the mystic probabilistically. This is the fundamental significance of his mysticism: it allows contingency to be dealt with as if it is risk.

On this fundament, the prophet stands. This is how the financial mystic becomes not only a hermit mumbling to himself but a guru surrounded by acolytes. Think of Jim Cramer in his ridiculous studio, piously imparting his opinions. Think of the ardency with which the proclamations of Warren Buffett, ‘the oracle of Omaha’, are analyzed. Think of all the minor diviners on the business channels, pronouncing judgments and attempting to inspire faith with a record of having been right. This is the significance of conspicuous trappings of wealth or the bonus number on Wall Street – they serve an evidentiary function, just as much markers of preeminence in an esoteric order as the hierarchized blooms of Catholic cassocks. From their conspicuousness, we form a judgment of their possessors’ judgment: we do not know how the prophets do it – the process is inscrutable – but we invest our faith in them.

In the limousine, Chin is confronted with the overwhelming fact of Eric Packer’s having been right. The limo itself is evidence. He knows it will turn their way, Chin says, since ‘it always has.’ Eric’s judgment has always been right. And Chin will follow it.

Mastering Uncertainty or Ignoring Contingency

Knight’s risk/uncertainty distinction was made while the number of corporations was ballooning. Who deserved the lion’s share of these corporate profits? ‘In Knight’s account, making decisions and passing judgment, the entrepreneur’s primary activities, are elevated to a new status, and every order by which judgment can be raised augments the importance of the ultimate decider’ (Poovey, 2018: 223). If profits arise directly through judgment, the entrepreneur is the sole reason corporations make profits, so it makes perfect sense for all profit to be awarded to the ‘deciders’. The deft entrepreneur’s mystical capacity to handle uncertainty justifies his immoderately elevated status, his immoderately elevated pay.

At the same historical moment that the mysticism of Knight (a co-founder of the Mont Pelerin Society) was being used to bolster anti-distributive policy, attempts to tax corporations created a massive data-collection infrastructure. Because of a modest 1% tax on corporations passed in 1909, self-reporting standards broadly expanded (Poovey, 2018: 227). With increasing data on corporations, less was unknown about them. Indeed, this helped empty the category of ‘unknown risk’ through the statistical method: new data converted unknown risks into statistical risks. At the same time, academic economists laid the groundwork for the explosion – and eventual dominance – of mathematical economics, which emptied the category of unknown risk through the deductive method (or gave the appearance of doing so): through precise formulations of the laws of economics and financial markets, more risks could be known a priori. Both methods contributed to the appearance that the uncertain future had been mastered. So too did new financial products – especially the proliferating array of derivatives used in risk management – and the increasing will and capacity of institutions like central banks to intervene in the financial economy. Uncertainty, it seemed, was coming under control.

But at the same moment, contingency was swelling. As stated in the introduction, several factors made finance less predictable. Further, risk management tools themselves created ‘unmanageable risks’, increasing uncertainty (Martin, 2015: 5). The empowerment of finance engendered unintended, often unforeseeable consequences. Here, judgment takes on an even more outsized role. Fundamentals become irrelevant: this is the meaning of chartism’s rise. Contingency swells: this is the meaning of Ayache’s market philosophy, in which contingency is total. Take DeLillo. While there are mystical experiences scattered throughout his novels, as Paul Maltby pointed out as early as 1996, it is only when chartism catches DeLillo’s eye, only in his finance novel, that mysticism saturates the book, that the protagonist become an out-and-out prophet. Finance, in which actors vie to better apprehend a contingent future, is itself an eminently mystical domain, all the more so the more uncertain the future is. No wonder, then, that here compensation is even more ludicrous than in business. Likewise, veneration of the financial actor gets overheated above and beyond veneration of the businessman: contingency’s masters gather acolytes.

We re-encounter our paradox. As Knight’s focus on uncertainty and his belief that some could master it led him into mysticism, the focus on mastering uncertainty also leads to a characteristic rationalism. Historically, a single response to uncertainty resulted, through a single process, in two very different tendencies: mysticism and rationalism. Both used the same tools and language, and both guided action in similar ways. What’s more, though they should be contradictory, the rationalism and the mysticism don’t unsettle each other: their overlapping, mutually-reinforcing influence entangles them, making it exceedingly difficult to distinguish one from the other. In fact, the rationalism cloaks the mysticism: this is how financial theory has managed to claim it fully rationalized the market in the last 50 years (against significant evidence but with significant policy ramifications). To resolve this paradox, as we will in the conclusion, we must not forget the contingency within uncertainty.

Poovey, ending her article on Knight, makes a call to contemporary economists: In pushing uncertainty away, economists and financial theorists have created the image of a world that, if not quite rational, can at least be modeled mathematically (within a probability range). […] Today’s economists […] have a special responsibility to […] face up to the reality of things none of us can know. (2018: 232)

In Cosmopolis, Eric Packer comes face-to-beak with his own black swan. The novel is implicitly set on Friday, 14 April 2000, a day the Nasdaq dropped 9%, completing a 25% nosedive on the week: the dotcom bubble had burst (Tymkiw, 2000). This eruption of contingency challenges Packer’s worldview and precipitates his rush to annihilation.

Besides his more traditional advisors, Packer brings in his Chief of Theory, Vija Kinsky. Eric explains his predicament – he’s way out over a cliff on yen – and she supposes he’s being told to draw back. Yes, he says. Then her: To pull back now […] would be a […] paraphrase of a sensible text that wants you to believe there are plausible realities, okay, that can be traced and analyzed. […] That wants you to believe there are foreseeable trends and forces. When in fact it’s all random phenomena. You apply mathematics and other disciplines, yes. But in the end you’re dealing with a system that’s out of control. (2003: 85)

Mystical Prophecy

Early in Cosmopolis, Packer’s chief of technology, Shiner, sits in the limo. ‘I know there’s a thousand things you analyze every ten minutes,’ he says. ‘Patterns, ratios, indexes, whole maps of information. I love information. This is our sweetness and light. It’s a fuckall wonder. […] People eat and sleep in the shadow of what we do. But at the same time, what?’ (2003: 14). The chief of technology knows what the fund manager does: he analyzes, he looks at patterns. Packer finds meaning in them, as his limousine attests. Shiner further espouses financial exceptionalism: the whole world’s in the shadow of what they do. The invocation of Matthew Arnold’s classicism expresses his self-assurance that they’re at the pinnacle of human culture. No longer is our sweetness and light the product of arts and letters. It’s all that’s computationally generated and gathered – all that data we started amassing when we tried to tax corporations. Sweetness and light in the arc and buckle of price graphs… ‘I love information’. But still, among the rhapsodizing, the question that could be asked of any prophet. Shiner speaks of what they do: ‘But at the same time, what?’

Ayache’s account of what the trader does centers around writing derivatives. He calls derivatives ‘contingent claims’ since they are privileged forms in dealing with contingency. A derivative does not mistakenly believe the future consists of possible worlds that might come into being, rather it brings future contingency into useful being today.

For example, think of tomorrow: either it will rain or it won’t. But do not think of those situations as two distinct worlds, one of which will be actualized while the other will remain inactual. There are not two possibilities, since possibilities aren’t real. Rather, we have two contingent claims, ‘one of which pays 1 tomorrow in case of rain and 0 otherwise, and the second of which pays 1 tomorrow in case of sunshine and 0 otherwise’ (2010b: 41). In the present moment, we now have two real contingent claims. It is contingent which will pay, but only chronological time deceives us into thinking they describe two real future worlds. There is only one real future world, and they both describe it. This is what it means to write the derivative. In writing, we make the supposed future ‘worlds’ coexist in reality because they are no longer worlds, they are writings.

Ayache’s derivatives trader, then, stands in exactly the same place as Knight’s entrepreneur. The entrepreneur interfaced with contingency and produced an output others could use. By his mystical capacity, he transformed contingency from ineffable future into present data, bringing it into the present of operational decision-making. The same goes for Ayache’s derivatives trader. By causing the contingent future to exist now as a writing, as a price, he transforms the unknowable future into something that can be used. This is done, as O’Malley says, in ‘rough’ and ‘ad hoc’ methods – through intuition (O’Malley, 2005); it’s the trader’s widely-touted ‘creative’ role (Christiaens, 2016: 5); Esposito characterizes it as allowing one ‘to use the future in the present’ (2011: 156); in this way, the trader becalms a present ‘shaken, tremulous with futurity’ (Massumi, 2014: 4). As Ayache says, ‘It is as if the market […] had the capacity of making the future happen “ahead” of time’ (2010a: 25). This is not mystical prediction, because it does not imagine several possible future states of the world and predict which will pass. It is mystical prophecy: it says this is the writing in the present of what the future will be. It draws the contingent future into the operational present.

Conclusion: Confronting Contingency

The dotcom crash is not the only contingency confronting Packer. Within himself, he has a material reminder of the unpredictable. During the confrontation with his would-be killer, who calls himself ‘Benno Levin’, Eric confides, ‘My prostate is asymmetrical.’ Benno pauses half a minute, then responds, ‘So is mine.’ Packer asks, ‘What does it mean?’ Benno tells him, ‘You should have listened to your prostate’ (2003: 199), then launches in: You tried to predict movements in the yen by drawing on patterns from nature. […] The mathematical properties of tree rings, sunflower seeds, the limbs of galactic spirals. […] The way signals from a pulsar in deepest space follow classical number sequences, which in turn can describe the fluctuations of a given stock or currency. (2003: 200) But you forgot something along the way. […] The importance of the lopsided, the thing that’s skewed a little. You were looking for balance, beautiful balance, equal parts, equal sides. […] But you should have been tracking the yen in its tics and quirks. The little quirk. The misshape. (2003: 200)

It’s time to resolve our paradox. In the face of what Knight calls uncertainty, there seems to be a single response – applying tools of advanced knowledge – that creates two contradictory outcomes: a rationalism moving toward mastery of risk and an irrationalism inculcating financial mysticism. The problem is that the first outcome overshadows the second, even making it disappear from view. Because the response to uncertainty can rationally diminish unknown risk, the claim is made that these techniques simply are rational. Contemporary finance, with its charts and its models, with its sophisticated analysis of historical data, is said, over and over, to perfectly manage risk. To puncture this claim – and account for the manifest irrationalism in so much financial thinking – we must distinguish within this response to uncertainty the part applied to unknown risks from that applied to contingency. In 1984, for instance, in the heart of the financial innovation boom, the president of the American Finance Association proclaimed to his members cutting-edge theory was moving them toward a market in which ‘every contingency in the world corresponds to a distinct marketable security’ (Van Horne, 1985: 621–2, emphasis added). But contingency is exactly what cannot be completely accounted for ahead of time. When these tools are applied to contingency, to that which cannot be foreknown, they are simply mystical. No matter how sophisticated Packer’s analysis, no matter how advanced his tools. They serve a distinct purpose: they bring the contingent future into the operational present, providing something determined with which decisions can be made. The danger comes when we forget this. When we lose sight of the contingency within uncertainty, it appears that rationalization covers all of reality. The market is complete. All risk is hedged. We cannot see that, when applied to contingency, erudite financial theory cannot help but be a mysticism.

Footnotes

Acknowledgements

This article began as a presentation at the 2019 conference of the Finance and Society Network, an organization from which I’ve received invaluable encouragement. The paper wouldn’t have gone far without Robyn Wiegman’s publication workshop. Many thanks to Robyn and all my workshop peers, particularly my reviewers, Lucas Power and Julien Fischer, and to Julien for continuing to discuss a year’s worth of drafts. The paper also greatly benefited from refreshing perspectives from Daniel Goldhaber and Rylee Hackley, careful editing by Phoebe Keyes, and the feedback of my anonymous reviewers at TCS.