Abstract

The Middle East / North Africa (MENA) region faces serious food insecurity, with an increasing gap between food production and consumption. Using resource advantage theory from macromarketing, we demonstrate that the agriculture / agribusiness industry would be highly competitive with economic integration of the Nile Valley (Egypt and Sudan) with the Arab Gulf countries. Individually, these sub-regions have critical disadvantages, but as a bloc, complementary strengths could make the industry quite competitive. Of course, integration within MENA has been discussed for decades, although usually as a political concept, which is unlikely to succeed in the foreseeable future. From a macromarketing perspective, economic integration is quite viable, and very beneficial to food security in the region.

Keywords

This article adapts Hunt’s (2011, 2014) resource advantage (RA) theory as used in marketing and macromarketing (as well as several other fields) to a country- and sub-region-level analysis of competitiveness in agriculture and agribusiness. The two sub-regions, the Arab Gulf States and the Nile Valley (Egypt and Sudan), are not by themselves competitive at all, and, in fact, are both quite dependent on food imports. This heavy dependence is not sustainable in the long run, and food security has become a critical issue for these countries. RA theory shows that as a unit, the two sub-regions have complementary strengths, together could become quite competitive, and could solve their food security problems.

With rapidly growing population of over 400 million, projected to be approaching half a billion by 2030 (United Nations 2017; World Bank 2018d), the Arab World is characterized by severe shortages of water and arable land. This is exacerbated by a lack of regional resource coordination and appropriate technology applications. According to most analyses, the region faces serious food insecurity, and the gap between production and consumption of food is widening. The Middle East / North Africa (MENA) currently has by far the largest dependence on imported food of any region in the world (Arab Forum for Environment and Development 2016, 2017; World Bank 2013). Food imports in the Arab world had already reached nearly US$ 90 billion by 2016 (World Trade Organization 2018), and were forecast to reach US$ 150 billion by 2050 if current trends continue (Arab Forum for Environment and Development 2014).

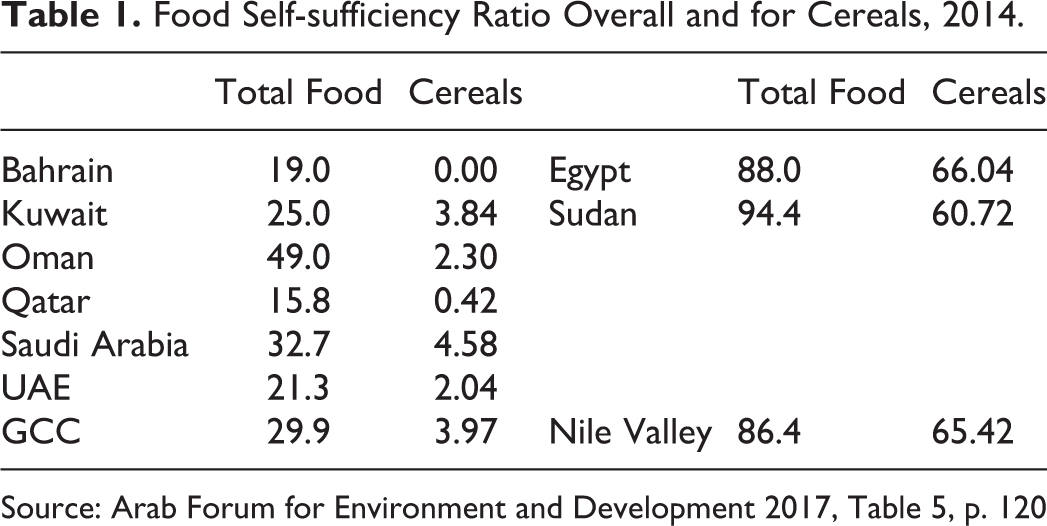

There is considerable variation across countries, although all Arab countries rely to some extent on imported food. In GCC countries (Gulf Cooperation Council – Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, UAE), total food self-sufficiency was 29.9 percent in 2014 (Table 1), i.e. dependence on imported food was about 70 percent, the greatest in the Arab world, albeit with some variation across countries. Oman had about 49 percent total food self-sufficiency, and Saudi Arabia was at about 33 percent, but Bahrain and Qatar were at only 16-19 percent.

Food Self-sufficiency Ratio Overall and for Cereals, 2014.

Source: Arab Forum for Environment and Development 2017, Table 5, p. 120

Food self-sufficiency is sometimes considered to be a separate issue from food security. Gulf countries’ strong financial position makes massive food imports feasible, and GCC countries sometimes score high on food security indices which focus on ability to buy food, rather than to produce it (e.g., Economist Intelligence Unit 2017; Food & Agriculture Organization 2017). Financial means to buy, however, cannot help if food is not available because of disruption in supply or distribution. As noted below, there is growing recognition that massive food exports can be detrimental to the exporter’s own food security, so that decreased access for importers is becoming increasingly likely (e.g., Jarosz 2014). Thus, food self-sufficiency and food security are increasingly being treated as strongly intertwined, by both countries and policy analysts (e.g., for China, Ghose 2014).

Along these lines, there is increasing recognition that trade flows and Arab investment in foreign agricultural land are themselves vulnerable, so that the financial ability to source food outside the region is no guarantee of food security (e.g., Food & Agriculture Organization 2017; Future Directions International 2017; Veninga and Ihle 2018). The GCC itself contains a striking example of politics affecting food security (which also demonstrates the political difficulties hindering integration in this region). Qatar ranks 29 in the Economist Intelligence Unit (2017) food security index for 2017, primarily because it is very rich and can import ample food. Nevertheless, Qatar’s rank represents a substantial decline from 2016. This is because of political problems with neighboring countries; Saudi Arabia and UAE have blockaded Qatar, which has had to develop new supply chains (Collins 2018; Costa Neves 2018).

Once the hope was that the Nile Valley would become the ‘breadbasket’ of the Middle East, but that did not work out, as was apparent already in the 1980s (e.g., Oesterdiekhoff and Wohlmuth 1983; Speece 1987). The concept has been revived in recent years (e.g., Woertz 2013, Chapter 6; Worldfolio 2015), but this sub-region currently lacks capability to fulfill a breadbasket role. Moreover, “Sudan’s potential as a breadbasket for the region depends on massive improvement in productivity and infrastructure” (International Fund for Agricultural Development 2009, p. 20). Even though they show the least reliance on food imports of any Arab sub-region, food self-sufficiency in Egypt and Sudan was about 88.94 percent, with relatively small differences between the two countries compared to variation in the GCC. For cereals, the main staple in all of these countries, the situation is even worse; self-sufficiency in 2014 was only about 4 percent in the GCC and 65 percent in the Nile Valley (Arab Forum for Environment and Development 2017). The 2014 figures for total food self-sufficiency were only slightly improved over 2011 figures, but for cereal grains it had gotten worse (Arab Forum for Environment and Development 2017). Some current reports suggest that the situation continues to worsen. By mid-2016 nearly 90 percent of food products were imported in the GCC ( Arab News 2016).

Sometimes it is assumed that such food insecurity is inherent, given that the Arab world consists of developing countries, most of them poor, and that much of the region is arid / semi-arid, poorly suited to traditional agriculture. However, with economic integration, the GCC and the Nile Valley, two key parts of the Arab world, could become self-sufficient. We cannot hope to solve all the policy problems which would make this difficult project possible to implement, but we can show that, given good policy, a competitive agricultural sector is very feasible. We use the resource-advantage framework from macromarketing (e.g., Hunt 2007, 2011) to demonstrate this. Basically, neither of these two sub-regions in the Arab world is at all competitive in agriculture when considered alone, but each has some strengths alongside its weaknesses. The strengths are complementary, and would cancel out weaknesses in the other sub-region, making an integrated block very competitive.

The discussion below looks first at how marketing and marketing systems issues are inherently part of the food security equation. There is already some recognition of this in the food security literature, but often on a somewhat piecemeal basis when authors cite some specific marketing element. In fact, a very wide range of marketing issues are important in food security, to the extent one cannot simply note individual marketing elements, but much touch on marketing systems ideas. The RA framework is then applied to key resources needed in agriculture / agribusiness, followed by sections showing the relative advantage or disadvantage which the Gulf or Nile Valley sub-regions have on these resources. The conclusion then initially just restates what the detailed analysis of resources makes very obvious – neither sub-region alone is competitive in agriculture, but their strengths and weaknesses are complementary. They would be quite strong as an integrated region. Finally, the conclusion section briefly discusses policy implications and future research on these issues.

The ‘Food Security’ Situation and Marketing

Many important factors contribute to poor performance of the agricultural sectors in these countries, but one major issue is ineffective marketing systems connecting production (or potential for production) with consumption on a regional scale. Even though marketing is essentially about integration between supply and demand, individual companies often focus on one or the other. They use strong operations for cost advantage, or strong marketing (and customer orientation) to build demand, rather than building an integrated package (e.g., Esper et al. 2010).

Recognition of this disconnect is also increasing on the national and regional scale as the concept of ‘food security’ has evolved from an early focus mainly on production. Based on the definition from the World Food Summit in 1996, the Food & Agriculture Organization of the United Nations says “Food security exists when all people, at all times, have physical, social and economic access to sufficient, safe and nutritious food which meets their dietary needs and food preferences for an active and healthy life” (Food & Agriculture Organization 2003, p. 29). It is widely recognized that the “four pillars of food security are availability, access, utilization, and stability” (Ecker and Breisinger 2012, p. 3).

While terminology may differ slightly, the substance of the current food security discussion overlaps substantially with Layton’s (2011) exposition of marketing systems. “The primary function of a marketing system is to offer customers an assortment consisting of a heterogeneous set of goods, services, experiences and ideas” (Layton 2011, p. 262). The Food & Agriculture Organization’s emphasis on “all people, at all times, have physical, social and economic access” (2003, p. 29) is usually considered an equity issue in food security discussions (e.g., Arab Forum for Environment and Development 2014; Jarosz 2014; Slade and Carter 2017). In marketing systems, it is more likely to be called “important issues of distributive justice”, which Layton uses to introduce a key observation that “the assortments generated by a marketing system contribute directly to the quality of life of the customer communities” (Layton 2011, p. 263). Similarly, social and economic issues of food security have always been part of marketing systems. “Economic exchange is always embedded in a marketing system”; and “marketing systems are always embedded in a social matrix” (Layton 2011, p. 261).

Improved agricultural production can certainly contribute to building the four pillars of food security, but better yields are not sufficient. Conceição et al. (2016), for example, argue that “rapid and sustainable increases in agricultural yields in Sub-Saharan Africa are feasible and the potential effects in terms of economic transformation and social uplift could be sizeable” (p. 7). Nevertheless, their discussion notes that achieving these increased yields may not be purely a technical issue, echoing both the food security and marketing systems sides of the discussion. Several papers in the special issue that they introduce address socio-economic aspects of agriculture. Grote (2014) explicitly points out that “increasing the efficiency of the food marketing system” (p. 187) is one critical need (among several). Even more broadly, we might talk about integrating supply and demand for needed technologies, and for investment to fund tech-intensive agricultural development; i.e. technology and financial marketing systems. The Arab Forum for Environment and Development cites the “lack of specific support and related services such as adequate technology, appropriate financing instruments or targeted capacity building programs” (2014, p. 107).

Many studies indicate that food security is influenced by various non-production aspects, some of the most important of which are related to marketing systems. For example, Alonso and Swinnen (2016) demonstrate how policies regarding the value chain (supply chain and/or distribution system) for wheat in Pakistan affects various players, from producers through middlemen to consumers. Cornia, Deotti, and Sassi (2016) address price volatility in Malawi and Niger, which is basically about how well the supply chain works (or does not work) under various government policies. Such examples unambiguously show that food security is not purely a technical production issue; it also depends on marketing systems.

Thus, marketing clearly must play a leading role in developing an integrated agriculture / agribusiness industry in the Arab region. Effective marketing can enhance the quantity and quality of all agricultural resources, it can guide both production and consumption of food products, and it can provide for efficient pricing and distribution of food products. Critically, marketing is necessary to pull together the advantages of the two sub-regions in Table 13, so that through integration, broader regional advantage can be built out of numerous disadvantages faced by the two separate regions. Politically motivated integration has not worked (e.g., Rouis and Tabor 2012; World Bank 2012a), not least because it does not really offer very tangible benefits to most people. Economic integration does offer substantial benefits to much of the population, and marketing helps provide the glue to hold the integrated parts together. We outline the case for marketing here, with more detailed discussion of the various resources in the following sections.

In the market economies in the Arab region, marketing activities influence both production and consumption of food products, although some degree of government market intervention distorted markets for a long time, especially in Egypt and Sudan (e.g., compare Speece and Gillard-Byers 1986 with Elgali and Mustafa 2012; World Bank 2009). Agricultural inputs and production output must move around – the sources of key inputs, and much demand for the output is in other parts of the region than where production is concentrated. Handling this requires marketing – the ‘demand and supply integration’ in Esper et al. (2010), and requires a version of their ‘knowledge management’ (KM).

In perhaps more familiar marketing terminology, this KM is marketing research and marketing information systems, needed to conduct feasibility studies, link information about demand to production of food products, and then to demand for inputs on the production side. Producers need to know about market demand for each product desired by consumers. Currently, farmers produce many crops in quantities, varieties, and qualities not needed by customers, which wastes agriculture resources. In most Arab markets, customers end up purchasing food imported from outside the region and leave many domestic food products to rot. The information must be current and available to farmers, channel members, and suppliers. Market information is often poor for small farmers in the main production areas, both for agricultural output that the farmer must sell, and for agricultural inputs (including innovations) that the farmer may wish to consume. Aker and Ksoll (2016), for example, discuss how mobile phones can give small farmers in Niger better access to market information so that they can adapt production decisions to gain higher value. The phones increased diversity of what was planted, but other market failures prevented much net benefit to farmers.

Technology itself can be regarded as a farm input, but exactly what technology is needed must be determined by the farmers. In other words, agricultural R&D needs to be managed essentially as a new product development process in marketing, where customer (farmer) voice is fully integrated into NPD (as in, e.g. Filieri 2013; Fuchs and Schreier 2011). The lack of ‘co-creation’ in developing innovations, which the farmer is supposed to adopt, has plagued agricultural research for decades. Long ago, observers already noted that “agricultural research has produced new so-called “improved” technologies which often turned out to be irrelevant to the farmer” (Winch 1984, p. 5). Today, different observers still see the same need for more extensive involvement of small-farmers themselves in the research process. Tittonell et al. (2012), for example, call for action research with ‘co-innovation’. Even with some co-production, most farmers may not learn of innovations. For example, extension services have been neglected in dryland farming areas of Sudan for decades, so farmers have little opportunity to learn of new technology and techniques. (e.g., compare Speece 1985 with World Bank 2009; World Food Programme 2009).

Looking just at two resources in Table 13, a substantial part of physical infrastructure and institutions supporting agriculture are about marketing – both the logistics and institutional aspects of supply chains and distribution channels (Alpen Capital 2017; Food & Agriculture Organization 2013a; World Bank 2012b; World Economic Forum 2017b). Supply chain logistics must be upgraded to connect the capital, energy, and demand in the GCC with the land and water in Egypt and Sudan. This is not merely about moving agricultural products from port to port. Transportation, storage, and handling from the farm to the port, and distribution to consumers on the other end, also need substantial upgrading. Supply chain issues also include shifting some of the value-added in food processing to low-wage, labor abundant areas such as Egypt and Sudan, and away from high-wage, labor-short GCC areas. These sorts of issues certainly require technology inputs, institutional reform, finance, etc. but success in any reforms needs marketing guidance to ensure that production is well coordinated with demand.

Many observers already recognize that marketing infrastructure and supply chain logistics need major improvements and upgrading (e.g., Ahmed, Hamrick, and Gereffi 2014; Lampietti et al 2011; Larson et al 2014). Sometimes the language in agricultural economics discussions sounds remarkably similar to marketing systems for food products (e.g., Myers, Sexton, and Tomek 2010; Unnevehr et al 2010). The Arab Forum for Environment and Development includes this marketing systems approach in its recommendations for improving food security in the Arab World; one key recommendation is: “adopt an integrated approach to food security, incorporating all food value-chain components, comprising harvesting, transporting, storing, and marketing, to make food available, accessible, and utilizable with good quality at the right time and place” (Arab Forum for Environment and Development 2014, p. 11).

Social marketing can be used on the demand side, especially for, among other things, fighting waste. A substantial amount of food is wasted through the inefficient logistics noted above, but on the consumption side, people in the richer societies of the Gulf also often waste a lot (e.g., Aljamal and Bagnied 2012). Social marketing about food consumption can be used in promoting healthy eating habits, and in promoting social values in the consumption and dispersion of foods, together with environmental protection, which goes to important issues even beyond food security.

Many other recommendations also imply aspects of marketing. However, to some extent, much of the policy discussion regarding marketing in MENA still focuses on research to understand how marketing systems work or should work, rather than what specific policies countries should adopt. For example, the discussion on coordinating policy across the GCC recommends “studying the effects of pricing, marketing and financing agricultural policies on developing food security” (Arab Forum for Environment and Development 2014, p. 32). One might argue, however, that we already have some basic understanding of how pricing affects demand, how marketing affects availability and access, and how financing affects productive capability. In other words, while there is some attention given to individual issues, we now need better understanding of the marketing systems’ role, to make sure policies actually accomplish their goals.

There is a long history of questionable policy in agricultural marketing systems. For example, “the policy environment in the agriculture sector in Sudan has not been conducive to growth, but is improving. In the past the government has intervened in agricultural markets through a variety of instruments that reduced incentives to produce.…Many of these distortions have been reduced, but government involvement in the sector remains strong” (World Bank 2009, pp. 70–71).

The Two Arab Sub-regions

We turn now to demonstrating how food security in the Arab region can be improved based on regional economic integration. The basic idea of integration in the region is not new, e.g. “cooperation among Arab countries based on comparative advantage in agricultural and financial resources is a key option for enhancing food security at the regional level” (Arab Forum for Environment and Development 2014, p. 10). Some degree of integration is already happening, but on a somewhat shallow, ad hoc basis without much attention by policy-makers. We aim to improve the understanding of how and why an integrated system would work, so that policy-makers can start thinking about how to better foster it.

We focus particularly on Egypt and Sudan, which have potential for mass agricultural production, and the Gulf, which has ample capital and energy, as well as high-spending power on the demand side. Markets are region-wide, but are strongly segmented, and fragmented. Market information must feed into production decisions on a regional scale, as well as into decisions about technology and management measures needed to improve production and distribution, all with a view toward serving multiple consumption segments dispersed across a wide geographic area. This is roughly the ‘knowledge management’ which Esper et al. (2010) argue can better integrate demand and supply functions, expanded across the two sub-regions. Layton (2011), who says that “the entities comprising a marketing system may themselves be marketing systems” (p. 267), might consider this construction of a cross-regional marketing system out of local national marketing systems.

The essential first step is to demonstrate that it makes sense to build a cross-regional marketing system. It does. MENA countries with agricultural potential that could help close the food production gap lack many resources necessary to make much progress at improving marketing systems, or even agricultural production itself. Even Egypt and Sudan, which arguably should be very strong in agriculture, were only about two-thirds self-sufficient in cereal grains by the late 2000s – early 2010s (Arab Forum for Environment and Development 2014, 2017; Food & Agriculture Organization 2013b). On the other side, countries with sufficient capital, technology, and logistics capability lack the agricultural resources. As a region, MENA has substantial agricultural potential, with land, capital, technology, and human resources. However, no individual country or sub-region has a sufficient package of these resources to develop a secure agricultural base, and thus, most food imports come from countries outside the MENA region.

These outside sources may become increasingly unreliable, with quotas and export restrictions at times of shortages and reduced reserves in supplier countries, or trade disruptions for political reasons (e.g., Food & Agriculture Organization 2017; Future Directions International 2017; World Bank 2012b). GCC countries have been very active in using their capital surpluses to buy agricultural land around the world for more assured supplies. In recent years, however, such foreign investment is coming to be viewed as ‘land grab’ (Cotula et al 2009; Future Directions International 2017; Grain 2016; World Bank 2010). For example, a recent study by the European Parliament (2015) recommended that member states be allowed to restrict investment in farmland, in the name of food security. In the affected EU nations, “the most active land grabbers came from western Europe, China, Kuwait and Qatar” ( Deutsche Welle 2015). Such issues have increased the volatility of international food markets, and analysts increasingly consider at least some level of food self-sufficiency to be a critical aspect of food security (Clapp 2017).

All the elements needed to alleviate the food security problem in the Arab region are available, but they are not coordinated, and thus, at present, do not contribute much to solving the problem. Egypt and Sudan, the main areas of food production, are somewhat distant from important high-spending-power markets, and lack coordination to optimally supply dispersed multi-segment demand. The GCC, the main Arab area with ample financial and energy resources to substantially upgrade agriculture, lacks productive capacity. From both the supply and demand side, inefficiency and waste are rampant in the region.

Resource Advantage Framework

We adapt the resource-advantage framework (e.g., Hunt 2007, 2011) to examine the case for economic integration between Egypt and Sudan and the GCC. “Resource-advantage theory maintains that economic growth is produced by the process of vigorous R-A competition” (Hunt 2011, p. 14). Firms scramble to gain advantage in particular market segments through use of tangible and intangible resources they have available. Various resources have differential value, depending on their quality and how they are used, and the value seen by the customer depends on market segment. Resources also have different costs, so both effectiveness and efficiency are important. So is innovation, because finding new or improved ways of using resources can change the value customers see, and change the cost structures of employing the resources.

Hunt’s RA framework was developed on the firm level. Much research on international competitiveness at the firm level has been in the context of exports. Key factors companies need to achieve export success can roughly be characterized as focusing mainly on internal resources and capabilities, or on the nature of the firm’s interaction with the market. The resource-based view (RBV) of the firm is sometimes applied to exporting; this approach assumes that sustainable competitive advantage is generated from a bundle of firm-specific resources and capabilities (e.g., Beleska-Spasova, Glaister, and Stride 2012; Kaleka 2012; Ritthaisong, Johri and Speece 2014). The other common approach focuses primarily on aspects of marketing strategy and tactics for implementation (e.g., Leonidou, Katsikeas, and Samiee 2002; Morgan, Kaleka, and Katsikeas 2004; Morgan, Katsikeas, and Vorhies 2012).

Of course, there is also considerable overlap between these two approaches. Kaleka, for example, follows the RBV approach, but nevertheless defines some key capabilities as “dynamic marketing capabilities whose deployment shapes export performance” (2012, p. 94). Morgan, Katsikeas, and Vorhies take the marketing approach, but talk about “the firm’s ability to use its available resources and skills to translate its intended export marketing strategy decisions into realized export marketing actions” (p. 272). Wheeler, Ibeh, and Dimitratos (2008) simply categorize the sorts of resources commonly used in RBV as ‘characteristics and resource base’, and the marketing strategies as ‘competencies and strategies’. They group both sets as two categories of ‘internal firm environment’ (Wheeler, Ibeh, and Dimitratos 2008, Figure 1).

Both the RBV theory and the marketing approach have sometimes been applied to agricultural and agribusiness exports. For example, Ritthaisong, Johri, and Speece (2014) use mainly internal resources and capabilities, without much reference to marketing, to examine rice exports by Thai rice mills. Ahmed et al. (2012) use a similar set of internal resources and capabilities applied to exports of processed food products from Thailand. Mbaga et al. (2011) look at marketing issues related to distribution channels in assessing date export performance in Tunisia and Oman. Karelakis, Mattas, and Chryssochoidis (2008) examine mostly marketing strategy elements in assessing export performance of Greek wines. The mixed approach is also used; e.g. Boughanmi et al. (2007) apply a mix of internal and marketing factors to fish export from Oman.

Here, we translate the RA framework back to the national level and look at how Egypt and Sudan, and the GCC, operating as an integrated region, would have strong competitive advantage on the world stage. Hunt (e.g., 2011, p. 12) notes that part of the RA framework is adapted from (national-level) comparative advantage in international trade theory. The firm’s resources can give comparative advantage, disadvantage, or parity. Competitive advantage, disadvantage, or parity comes from market position, which depends on how well firms deploy resources. However, this firm-level process is embedded in the broader environment. Ellis and Pecotich (2002), drawing on Porter (1990), argue that it is the national-level competitive advantage conditions which provide the environment supporting firm efforts to build competitive advantage. Hunt shows societal resources, societal institutions, competitors-suppliers, consumers, and public policy as key aspects of this broader business environment (e.g., Hunt 2011, Figure 1, p. 10; also Hunt 2007, p. 278).

In other words, “marketing systems are influenced by and influence the institutional and knowledge environments in which they are located” (Layton 2011, p. 264). To a substantial degree, competitive firms operating in a country with strong advantages are likely to have those advantages themselves. For example, if a country has advanced technology widely used in an industry, a successful firm in the industry is likely to have that technology; or, if a country has strong advantages in the necessary skills, a successful firm in the industry probably has those skills. Thus, firm-level vs. national-level RA frameworks are interconnected. Food security is a national or regional issue; it cannot be achieved by a single company. However, except for cases where agriculture and agribusiness are mostly in government hands, national / regional food security comes from a multitude of contributions by individual firms, which must be competitive to some degree if they are to stay in business.

Then, after looking at the national and regional level, the framework can be applied back to the firm-level. A firm operating in a region with strong competitive advantage would be in a favorable environment. Various barriers associated with operating internationally raise costs for the firm. Most such barriers are not inherent in simply operating internationally, but are imposed by policy, in (sometimes misguided) attempts to protect local firms. This is a standard issue in any international business textbook (e.g., Hill 2013, Chapter 7), so there is little need to demonstrate it here. Similarly, the benefits of regional integration are also well known (e.g., Hill 2013, Chapter 9). Thus, these general principles are well established; here we focus only on showing the case for regional integration of the GCC and Egypt and Sudan. Firms in an integrated region must still compete with each other, and with external competitors. However, as a whole, they are in a much improved environment which makes them more able to succeed in competition with outside firms, i.e. overall, the regional industry is better able to prosper.

The Resources

Hunt (2007, 2011) lists a number of key resources, which we have adapted slightly to fit the context of agriculture / agribusiness at the country level. These include: natural resources (e.g., land, water, energy, minerals, climate) capital resources (e.g., financial assets, liquidity, and reserves) physical infrastructure (e.g., roads, transportation and storage facilities, utilities, ports) human resources (e.g., skilled labor) entrepreneurship (e.g., management with strategic planning knowledge and experience) technology (e.g., state of the art know-how, and research capability) institutional (e.g., industry structures, organizations, supply chain, channels of distribution) legal infrastructure (e.g., agriculture regulations; land ownership laws, pricing, subsidies and tax laws; business, trade, environmental, anti-trust, safety, quality control, consumer protection and marketing laws and regulations).

A few researchers already looked at some of these resources across more than one MENA country. For example, the Arab Forum for Environment and Development (2014, pp. 18-19) argues that energy, water, and food policy must be coordinated on a regional basis in the Arab world. However, discussion usually focuses on coordination within the various sub-regions, e.g. ‘Food security choices in GCC states’ (Arab Forum for Environment and Development 2014, pp. 30-32). We argue that the discussion must be across sub-regions. The GCC example demonstrates, as do several others, that within a particular sub-region, strengths are similar across the countries, and the weaknesses are also similar. Within-sub-region cooperation may help, but cannot fully solve food insecurity. The sub-region needs to work with another sub-region where the strengths and weaknesses are complementary, not duplicative.

Brief assessments of international competitiveness on each of these resources are summarized in the following discussion. Note that on natural resources, and on human resources, we had to divide the categories into two type to account for differences in the two sub-regions (non-energy vs. energy agricultural resources, and agricultural labor vs. managerial skills in agriculture, respectively).

Non-energy Natural Resources

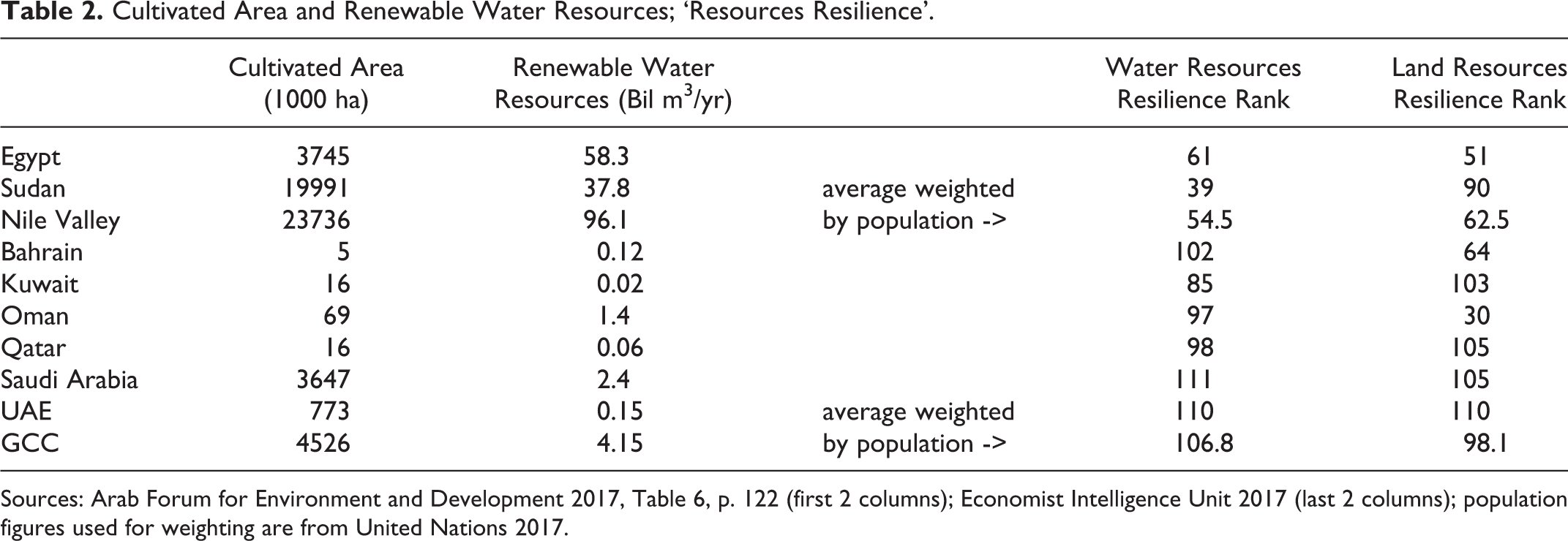

This assessment uses two ‘natural resources’ categories; non-energy agricultural (land and water) vs. energy (for use in agribusiness), to conduct a useful assessment. The arable land and water assessment is based on Food & Agriculture Organization data (2013a, 2013b), supplemented with additional sources to add some useful detail, and, sometimes, to update what is available in the Food & Agriculture Organization. The Arab Forum for Environment and Development classifies Egypt and Sudan as high potential for expansion of agriculture, based on assessment of available cultivable land and renewable water resources. Five GCC countries are considered to have “extremely limited potential”, while Saudi Arabia has medium potential (Arab Forum for Environment and Development 2017, Table 6, p. 122). The Nile Valley sub-region has more than five times as much cultivated land area as the GCC, and 23 times as much renewable water (Table 2). Most agricultural water in the GCC comes from ground water or very expensive thermal desalination (Arab Forum for Environment and Development 2017).

Cultivated Area and Renewable Water Resources; ‘Resources Resilience’.

Sources: Arab Forum for Environment and Development 2017, Table 6, p. 122 (first 2 columns); Economist Intelligence Unit 2017 (last 2 columns); population figures used for weighting are from United Nations 2017.

Summarizing the Food & Agriculture Organization (2013a, 2013b), Sudan has high availability of arable land and water, at relatively low costs. This gives it a competitive advantage in land and water resources. Egypt has fair availability of arable land and water resources, but they are poorly utilized (as also to some extent in Sudan) due to fragmentation, low levels of technology, and poor agriculture planning and practices. Productivity could be boosted if such problems are dealt with. Also, over 30,000 acres of agricultural land are lost each year to urbanization. Land cost is relatively high, but water cost is moderate and water is plentiful, although there is some political risk from claims on Nile water by upstream countries. Most agricultural land, particularly in the Nile delta and valley, can be very productive if appropriate technology and practices are utilized. Currently, these resources could be considered in a parity to slight advantage position in Egypt. These conditions seem to indicate opportunities for social marketing initiatives to promote more recognition about the importance of preserving agricultural lands from urbanization.

The Gulf Region has very limited arable land and water resources. Saudi Arabia is somewhat of an exception, where heavy investment in reclamation of the desert and application of modern irrigation methods and technology have been successful in producing good amounts of agricultural products, but at a very high financial and water cost. Saudi Arabia was actually self-sufficient in wheat production for a couple of decades, but is phasing out lower value, water intensive crops now (e.g., Ahmed, Hamrick, and Gereffi 2014; Arab News 2016; International Fund for Agricultural Development 2009). Water shortage is a serious problem limiting crop production in GCC countries. As Table 2 indicates, there is very little renewable water; most water in GCC countries comes from groundwater or desalinated water from the Gulf, which has very high long-term costs.

Egypt has the most favorable climate for traditional agricultural production due the moderate temperatures in the northern coastal area where much of the agricultural land is found. Otherwise, Egypt lies mainly in the arid / semi-arid zone, but does not need to rely on rainfall due to the Nile. Sudan also lies in the arid or semi-arid area, but has substantial agricultural production along the Nile. However, much of Sudan’s production is in rain-fed agriculture in the semi-arid regions, which is subject to variations in local climate from season to season. The climate in the GCC countries is largely unsuited to traditional agriculture except in a few local pockets, and most current production depends on methods which are unsustainable in the long term. Table 2 also indicates ‘resource resilience’, an estimate of long-term sustainability under climate change (Economist Intelligence Unit 2017). Egypt and Sudan, while in a slightly precarious situation, are far better off than most Gulf States, which rank very low by world standards.

Thus, Egypt and Sudan both have abundant land, and abundant water, at least by the standards of countries in these latitudes internationally. Their resources are moderately sustainable over the long term. Most agricultural land can be very productive, giving Egypt and Sudan advantage in these resources, although they lack necessary capital and technology to fully exploit this advantage. Overall, the Gulf region has strong competitive disadvantage in land and water, and current usage of these resources does not seem very sustainable.

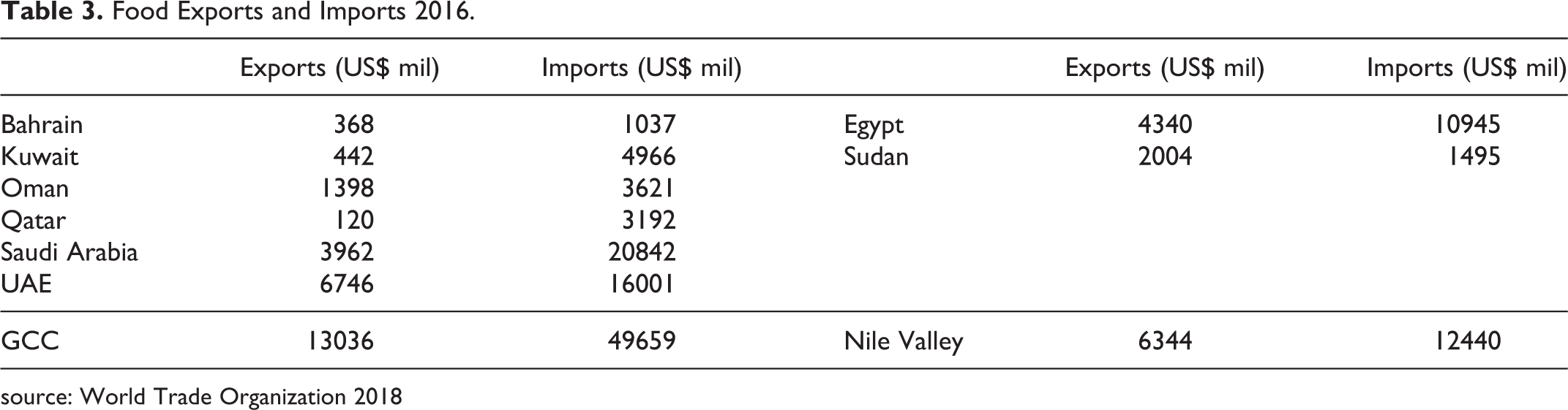

Trade patterns reflect this relative advantage of the Nile Valley. All of these countries have some food exports, but they import much more than they export (Table 3). Sudan is the only exception; its exports / imports are roughly in balance, with some recent years showing a slight surplus of export (as in 2016 in Table 3), and some years a slight deficit (World Trade Organization 2018). The majority of exports are within the region for the largest exporters (Egypt 55%; Saudi Arabia 88%; Sudan 71%), but none of these countries is able to source more than about 40 percent of imported food from within the region (Sudan 42%; next closest is Qatar 34%; Arab Forum for Environment and Development 2014, Table 1, p. 110). Reflecting the relatively stronger food self-sufficiency position, the Nile valley sub-region has much less food import than the GCC. The ratio of imports / exports is nearly twice as great for the GCC compared to the Nile valley (3.8 to 2.0, respectively, from Table 3 figures).

Food Exports and Imports 2016.

source: World Trade Organization 2018

Energy Resources

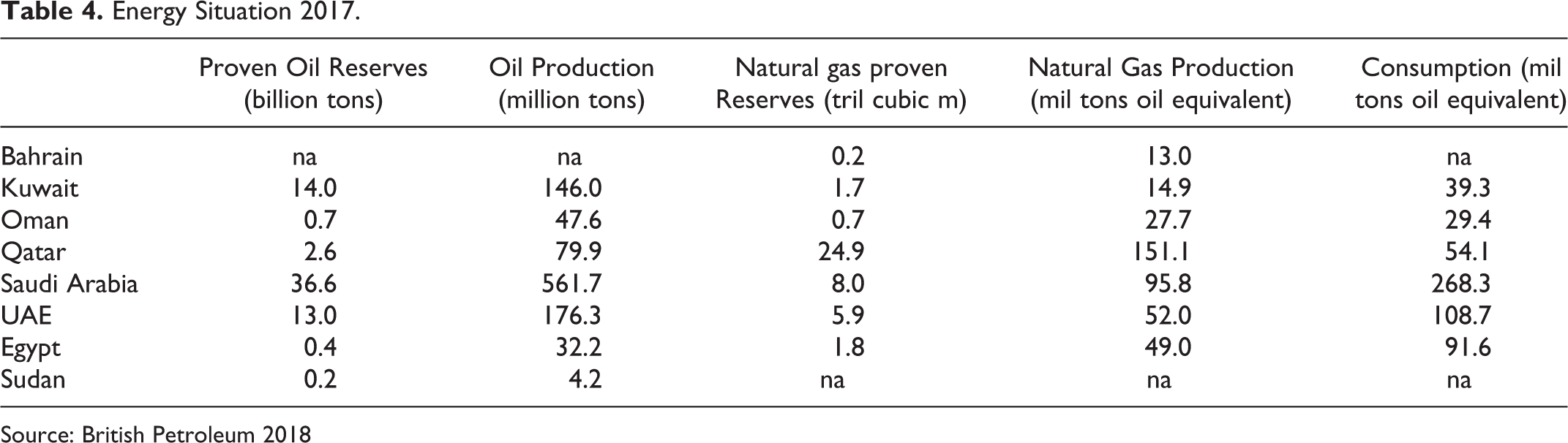

Energy is somewhat available in Egypt and the Sudan, which have modest oil and gas (Egypt) resources, but these do not meet local demand. Egypt’s energy consumption is about 20 percent greater than its energy production from oil and gas. The country is developing renewable energy resources, but they currently account for less than 4 percent of total energy production, so Egypt is a net energy importer. The situation in Sudan is even somewhat less favorable, because about 70 percent of the oil reserves were in South Sudan, which gained independence from Sudan some years ago (British Petroleum 2018).

On the other hand, the Gulf States are very rich in oil and gas reserves, accounting for around thirty percent of global petroleum reserves, and nearly a quarter of current production. The GCC countries also account for over 21 percent of natural gas reserves, but only produce about 11 percent of world output at present (British Petroleum 2018). With energy available locally at very low prices, GCC countries have very high per capita energy consumption by world standards (e.g., Arab Forum for Environment and Development 2015). Nevertheless, except for Bahrain, less than half of energy production is needed locally, and GCC countries are major exporters. One downside is that such wide availability of oil and gas has inhibited development of renewable energy sources, which still account for only around one percent or less of energy production. Because of this, Gulf countries get low rankings on ‘energy architecture’ indices, roughly a measure of diversification of energy supply (e.g., Arab Forum for Environment and Development 2017; World Economic Forum 2017c). Social marketing initiatives can be used to promote energy conservation and development of renewable energy resources, both of which are goals in most GCC development plans, but this is more of a long-term issue, not critical in the short-term.

Thus, as Table 4 clearly illustrates, Egypt and Sudan can be classified as at a slight disadvantage in energy resources, while the GCC has strong advantage. This is not likely to change in the next few decades. At current production levels and with current proven reserves, Egypt will deplete its resources within a few decades, but several Gulf States still have a century or more of reserves (British Petroleum 2018). Only Oman is likely to run out within several decades, while Bahrain has already largely run out. (Bahrain is still a major player in the refinery industry, a legacy of its past as an oil producer.) The Gulf sub-region has strong advantage on this factor.

Energy Situation 2017.

Source: British Petroleum 2018

Capital Resources

Capital is relatively abundant in the Gulf countries, which took advantage of high oil and gas revenues to accumulate a large amount of wealth. The popular perception that the Gulf countries are rich is only somewhat accurate, mostly only in the sense that they have a range of per capita income similar to the developed West, which much of the world does consider ‘rich’. Outside observers also often neglect the fact that these are essentially developing countries, which are spending heavily to catch up with the developed West. Thus, while they used the period of high oil prices to develop rapidly, they do not really have the huge surpluses sometimes attributed to them in popular perception, especially over the past few years when oil prices have been low. Nevertheless, they do have ample financial resources compared to most countries of their size and level of development.

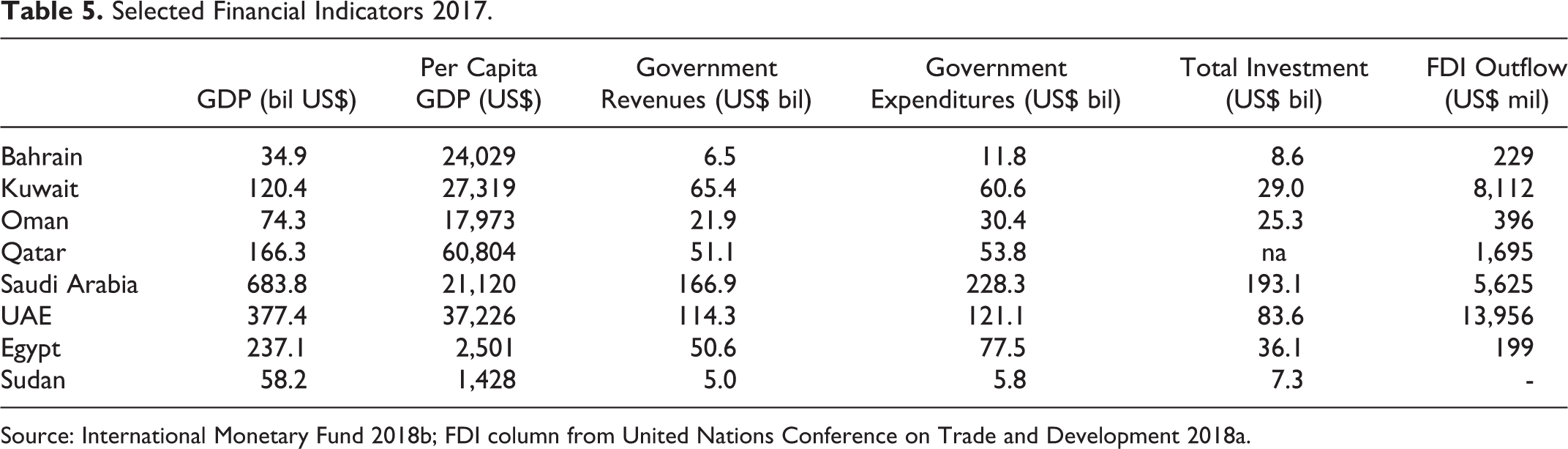

According to International Monetary Fund (2018b) statistics, per capita income in the Gulf States is similar to Western Europe (Table 5). Qatar has the highest, at US$ 60,804, which, for comparison, is still lower than Norway, also an oil state (US$ 74,941) or Switzerland, a non-oil state (US$ 80,591). Oman has the lowest per capita income in the GCC, at US$ 17,973, similar to the level in Greece (US$ 18,637). The other GCC countries have per capita income levels in a range similar to Western European countries such as Portugal (US$ 21,161) or Italy (US$ 31,984). On the other hand, Egypt’s nominal per capita income was only US$ 2501 in 2017; and Sudan’s was only US$ 1428. Of course, the difference in living standards between the two sub-regions is not quite as great as the nominal per capita GDP figures suggest. Cost of living is lower in Egypt and Sudan, so purchasing power parity reduces the gap somewhat, although it is still very large.

Selected Financial Indicators 2017.

Source: International Monetary Fund 2018b; FDI column from United Nations Conference on Trade and Development 2018a.

Several Gulf countries also have large sovereign wealth funds, mostly built in the days of high oil prices. Abu Dhabi (UAE) has the largest such fund in the Middle East, and third largest in the world, at US$ 828 billion in 2018 (Sovereign Wealth Fund Institute 2018). (It should be noted that the largest sovereign wealth fund, also built from oil revenues, is not in MENA, but in Norway. The second largest is in China, which was not funded from oil revenues.) Kuwait and Saudi Arabia had the fourth and fifth largest, at US$ 524 and 494 billion, respectively. Worldwide, seventeen sovereign wealth funds have over US$ 100 billion in 2018, including one in Qatar, second one in Saudi Arabia, and three others in UAE. (The rest are in China, Singapore, Korea, and Australia; Sovereign Wealth Fund Institute 2018). This gives most GCC countries the ability to withstand many years of unfavorable economic conditions without much difficulty, a luxury that Egypt and Sudan lack.

Government revenues, expenditure, and investment are more appropriate to judging competitive advantage between the two sub-regions. On the surface, the figures in Table 5 for Egypt may look similar to those of several GCC countries, but Egypt must deal with a population 20 to 40 times as large as populations in the smaller Gulf States. Sudan also has a population larger than any Gulf state, including Saudi Arabia, but far less money than even Egypt (International Monetary Fund 2018b). Most GCC governments ran fiscal deficits after 2014 when oil prices declined sharply. They have adjusted with reforms to reduce government spending and improve efficiency, and oil prices are up slightly now, so the deficits are declining (World Bank 2018b, 2018c).

GCC countries mostly have strong outward FDI flows, and remain important sources of outward foreign investment (United Nations Conference on Trade and Development 2018a, 2018b). Even the smallest GCC economy, with the least outward FDI, has more outward FDI than Egypt. While Egypt is a recipient of some of this FDI, the majority of it, including investment in agriculture, goes outside the Arab region (e.g., Arab Forum for Environment and Development 2017). There is no doubt that the Gulf countries have solid competitive advantage in capital resources, while Egypt and Sudan are at a competitive disadvantage. Here again, marketing communications can contribute to promoting investment opportunities to shift some of GCC investment toward Egypt and Sudan and away from outside destinations.

Physical Infrastructure

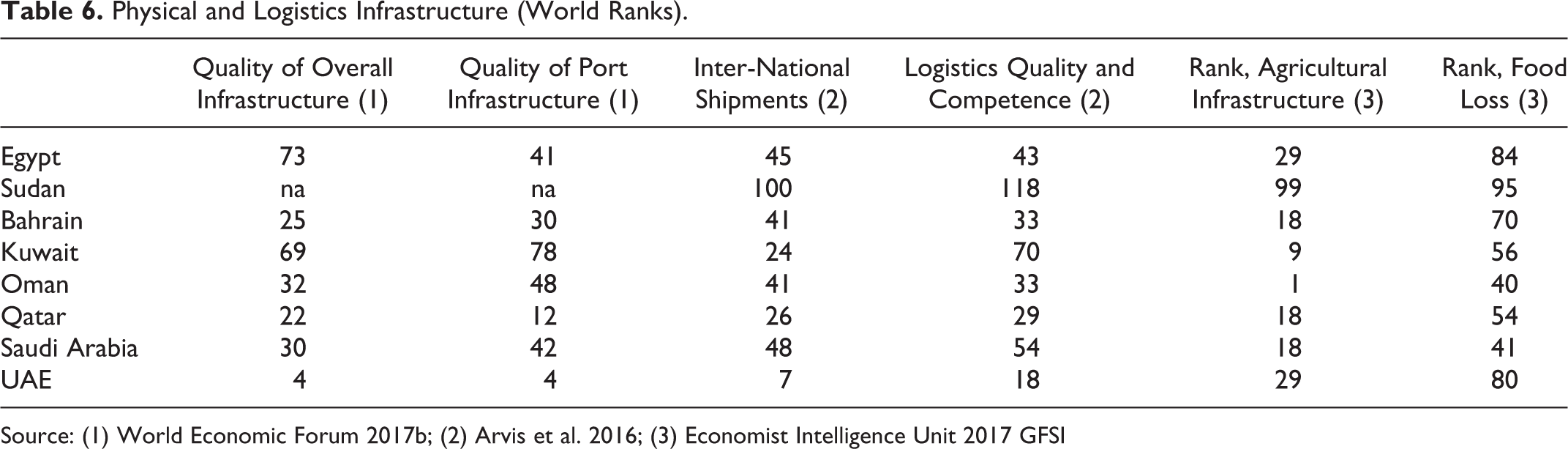

This resource is moderately well developed in most GCC countries, but the situation is much worse in middle to low income Arab countries, which have not had financial capability to implement large, costly infrastructure projects. Infrastructure in Egypt and Sudan is generally inadequate in terms of roads, ports, storage and transportation facilities, airports, and utilities, and is particularly poor in rural areas. Almost a decade ago, the United Nations Development Programme (2011) already singled these two countries out (along with Yemen) as most deficient, and the situation has not improved much since then. This affects all aspects of production and marketing of agricultural products. It should be noted that it is more difficult and costly to upgrade physical and logistics infrastructure widely than it is to upgrade production, where some impact can be gained even if implemented only locally. This suggests that richer GCC countries would rank better on infrastructure.

Table 6 indicates that all GCC countries rank much higher on ‘quality of overall infrastructure’ than does Egypt, although Kuwait is only slightly higher. (World Economic Forum 2017b; Sudan is not included in the Global Competitiveness Index because of insufficient data.) Most GCC countries also rank higher than Egypt on various aspects of logistics (Arvis et al. 2016), and for these indicators, there is sufficient data to include Sudan, which ranks very low. In addition to hindering international shipments, poor logistics can cause loss and wastage in domestic storage and transport. Egypt has the highest food loss and waste in the Arab world, over 90 kg/yr/capita, well above the average in the Arab world of about 57 kg/yr (Arab Forum for Environment and Development 2014, Figure 4, p. 116). In the Economist Intelligence Unit (2017) food security index, Egypt ranks 84 in the world for food loss, and Sudan ranks 95 (Table 6). GCC countries also have substantial loss/waste, but largely on the consumption side (e.g., Aljamal and Bagnied 2012), rather than in storage and transport of agricultural outputs. Their ranks on ‘agricultural infrastructure’ in Table 6, largely the logistics side, are higher than for Egypt and Sudan. However, “most waste in developed countries occurs at retail and consumer levels, while it happens at the post-harvest and processing stages in developing countries” (Arab Forum for Environment and Development 2014, p. 116). Because of this, GCC food loss ranks in Economist Intelligence Unit (2017) are somewhat lower, still ahead of Egypt and Sudan, but not usually very substantially. The lowest ranks in the GCC are UAE, for example, ranked 80, while Bahrain, ranked 70.

Physical and Logistics Infrastructure (World Ranks).

Source: (1) World Economic Forum 2017b; (2) Arvis et al. 2016; (3) Economist Intelligence Unit 2017 GFSI

Overall, therefore, both Egypt and Sudan are at a strong competitive disadvantage in this important resource. Physical infrastructure is in much better condition in the more modern, richer Gulf States. Some elements of agriculture-related infrastructure still need improvements in some Gulf countries like Saudi Arabia, Bahrain, and Kuwait, but the whole Gulf has had sufficient financial resources to make rapid progress in constructing needed infrastructure in the past few decades. Their food loss is the result of wastefulness from more food than they need, not from deficiencies in physical infrastructure. This resource may be considered to be in an advantage position in the Gulf.

Human Resources (Agricultural)

Allocating more land to agricultural production cannot have a very large impact on food security in MENA. The Arab Forum for Environment and Development (2014, p. 48) estimates that only about seven percent of potential increases in food production in Arab countries could be achieved by bringing more land under cultivation. In other words, improvement will mostly need to come from better application of skills and technology. Agricultural R&D is one critical component of this. Egypt historically has devoted far more resources to agricultural research and extension than any other Arab country. For example, about 58 percent of research years in the entire Arab world in 2009 were in Egypt (International Fund for Agricultural Development 2009, Table 5.2).

Skills are the other key ingredient to improvements in agriculture. Egypt already has the highest grain yields in the Arab world (Arab Forum for Environment and Development 2014, Table 5, p. 20), far above world average. Of course, Egyptian grain is grown with irrigation, while much grain production in the Arab world is rain-fed agriculture. However, Egyptian grain yields are far above yields in GCC countries, even when GCC grain production is entirely irrigated. Egypt has consistently shown modest growth in agricultural productivity since the early 1960s (Arab Forum for Environment and Development 2014, Table 3, p. 82). Between 2000-2009, the average annual growth was 2.76 percent.

Figures for Gulf countries, where available, show widely fluctuating growth in productivity. Two of the more extreme cases, for example, are UAE and Kuwait. Average annual growth in agricultural productivity for 1991-2000 was 8.20 and 7.05 percent, respectively. However, in the decade 2000-2009, average annual growth was negative, -4.73 and -0.23, respectively for UAE and Kuwait. Essentially, Gulf productivity figures simply represent how much water use government policy is willing to permit. Output declines as it becomes apparent that the increased output is not sustainable and government changes water-use policy, as was noted above regarding wheat in Saudi Arabia (e.g., Ahmed, Hamrick, and Gereffi 2014; Arab News 2016; International Fund for Agricultural Development 2009).

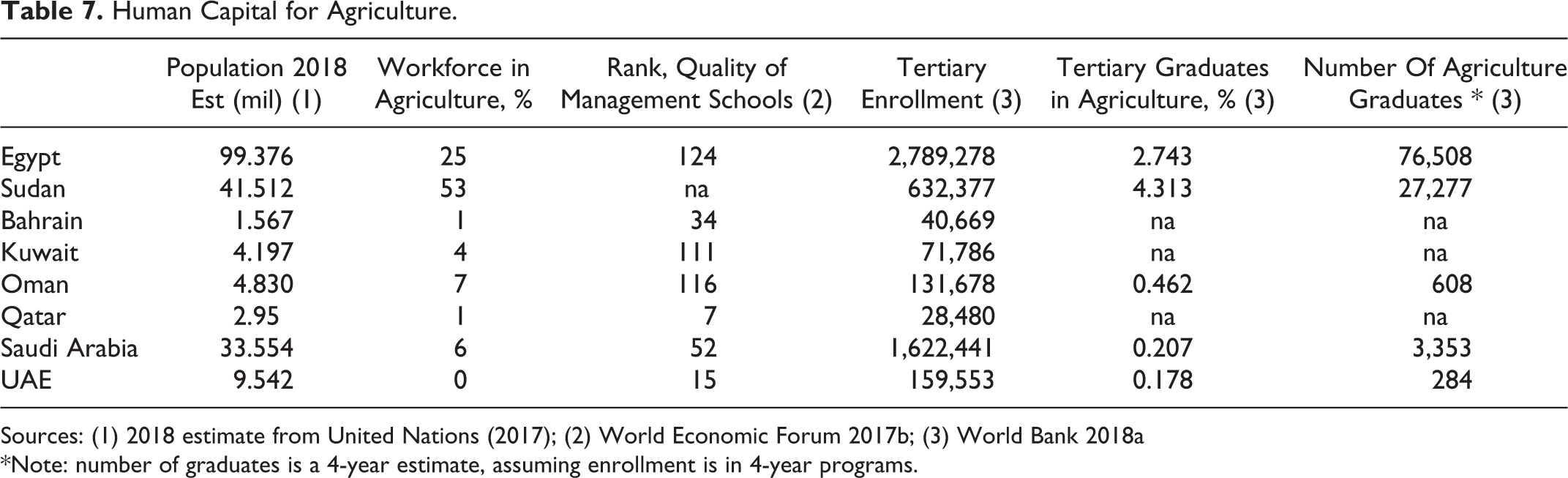

In terms of the quantity and cost of skilled labor for agriculture, Egypt is by far the leading country in competitive advantage. Egypt is the most populous Arab country with a population reaching 100 Million. Sudan has around 41 Million, while the total population of the Gulf countries is approximately 56 million, with 33 million of those in Saudi Arabia (Table 7). Egypt is well known as one of the leading suppliers of skilled labor (as well as managerial talent, see below) to Gulf countries. Many of them prefer importing skilled labor from Egypt and some other Arab countries, while most of unskilled labor comes from South Asia. Sudan, despite its relatively large population with low labor cost, has not been a major exporter of skilled labor to other countries. In 2014, for example, Egypt recorded US$ 19.6 billion in remittances from workers abroad; Sudan, by contrast, had a little over US$ 432 million (International Organization for Migration 2018).

Human Capital for Agriculture.

Sources: (1) 2018 estimate from United Nations (2017); (2) World Economic Forum 2017b; (3) World Bank 2018a

*Note: number of graduates is a 4-year estimate, assuming enrollment is in 4-year programs.

A substantial part, often a majority, of the population in most Gulf countries, other than Saudi Arabia, is guest labor, mostly from South Asia, although many are also from Middle Eastern and Far Eastern countries. The Gulf region has a major shortage of skilled labor, and has been a major importer of labor since oil prosperity dominated the region. While the ease of finding skilled employees is above the world average in several Gulf States (World Economic Forum 2017a, Fig. 13, p. 9), most of this skilled workforce is foreign. Consequently, the Gulf region may be classified as having a competitive disadvantage in human resources for agriculture.

Human Resources (Managerial)

While Egypt and Sudan clearly have far more skilled agricultural labor than the Gulf region, their strong advantage may not be quite as obvious for the case of managerial talent. Egypt’s weak economy and the GCC’s well-funded universities tend to cloud the issue. In fact, Egypt has probably the most educated workforce in MENA (World Economic Forum 2017a, Fig. 8, p. 5). Egypt’s economy actually requires a higher proportion of highly skilled jobs, and a lower proportion of low skilled jobs, than any other MENA country (World Economic Forum 2017a, Figure 4, p. 3). Thus, while the economy is not able to absorb so many educated people, those who get jobs generally gain useful experience. The lack of enough good jobs in Egypt is a key driver of managerial talent toward labor migration. Nearly two-thirds of Egypt’s migrant workforce is in the Gulf, and the majority of migrants are relatively well educated at intermediate or university level (e.g., Arouri and Nguyen 2018). Much of this is skilled labor, but Egyptians also contribute substantially to the professional and managerial workforce.

Unfortunately, the current quality of education in Egypt is not as good as in the Gulf. GCC countries have spent heavily over the past few decades to upgrade higher education, and have made substantial progress. With respect to the quality of management schools, in particular, the Global Competitiveness Report (World Economic Forum 2017b) ranks them much higher than Egypt. (Sudan lacks sufficient data to be included in the Global Competitiveness Report.) However, this does not actually give the Gulf economies much of a boost, because few Gulf nationals work in private sector business. A key problem across the GCC is “low levels of participation of Gulf nationals in the private sector activity and their high levels of reliance on the public sector for jobs, subsidies and transfers” (World Bank 2017, p. 20). Bloated public sectors are serious impediments to further economic development. In Kuwait, for example, over eighty percent of employed nationals work for the public sector (World Bank 2018b), and the public sector wage bill is nearly 12 percent of GDP (International Monetary Fund 2018a). The public sector wage bill in most GCC countries is a substantially higher proportion of GDP than in Egypt (International Monetary Fund 2018a, Fig. 2.4, p. 8).

Further, even if nationals move into the private sector more strongly, they are not well positioned to contribute substantially to agriculture in an economy integrated across the GCC and Nile Valley. Because agriculture is a negligible part of the economies in Gulf countries, the educational system does not give it very much attention. Table 7 illustrates that the well-educated managerial workforce for the industry will mostly need to come from Egypt and Sudan. Egypt and Sudan graduate over 100,000 students with agricultural degrees over a four-year period. The three largest tertiary systems in the Gulf (which coincide with the largest populations and the most agriculture) graduate only a little over 4000 students with agriculture degrees over the same period.

Entrepreneurship

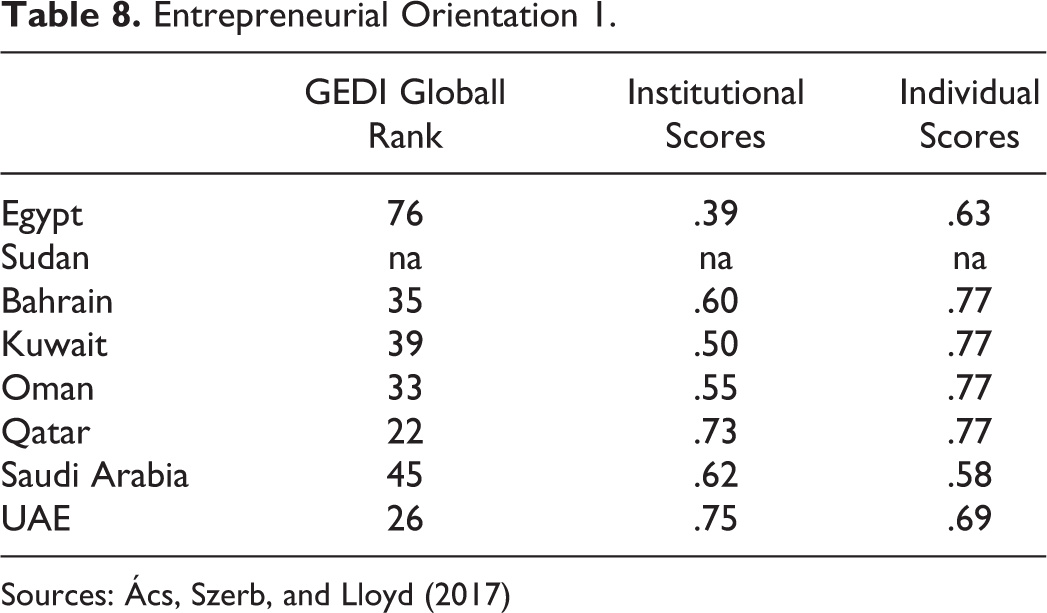

Again, Egypt is a leader on this resource, although this is not immediately obvious from some of the standard data. In the Global Entrepreneurship and Development Institute (Ács, Szerb, and Lloyd 2017), GCC countries are considered well ahead of Egypt (Table 8 col 1; Sudan lacks data for comparison). However, “the Global Entrepreneurship Index is a composite indicator of the health of the entrepreneurship ecosystem in a given country” (Ács, Szerb, and Lloyd 2017, p. 3). This ‘entrepreneurship ecosystem’ is largely about institutions and policy. For example, the Global Entrepreneurship and Development Institute (GEDI) says that MENA would see the quickest gains by improving competition, reducing barriers to the entry for new firms (Ács, Szerb, and Lloyd 2017). This is clearly an institutional / policy issue, more appropriate to discussion of other key resources in Hunt (2007, 2011), notably, institutional and legal infrastructure (below).

Entrepreneurial Orientation 1.

Sources: Ács, Szerb, and Lloyd (2017)

GEDI does not really assess an entrepreneurial mindset among the people who would be starting businesses, which is what Hunt’s (2007, 2011) entrepreneurship resource is about. While GEDI does use some individual-level primary data, it gives high weights to country-level secondary data, similar to what we use here under many of Hunt’s (2007, 2011) resources. Egypt does not score well on institutions or infrastructure, so the weak infrastructure gets heavy weight, and the entrepreneurial mindset aspect is obscured. Table 8 hints at this; Egypt’s ‘institutional’ score is much lower than for GCC States, but its ‘individual’ score is much closer. Primary data in GEDI actually come from the Global Entrepreneurship Monitor, which directly surveys people in participating countries. Global Entrepreneurship Monitor has more complete data at the individual level, although only Egypt, Saudi Arabia, Qatar, and UAE currently participate. Nevertheless, taking these three GCC countries as representative, Global Entrepreneurship Monitor’s individual-level data clearly show Egypt’s entrepreneurship advantage (Ismail, Tolba, and Barakat 2017; Global Entrepreneurship Monitor 2018).

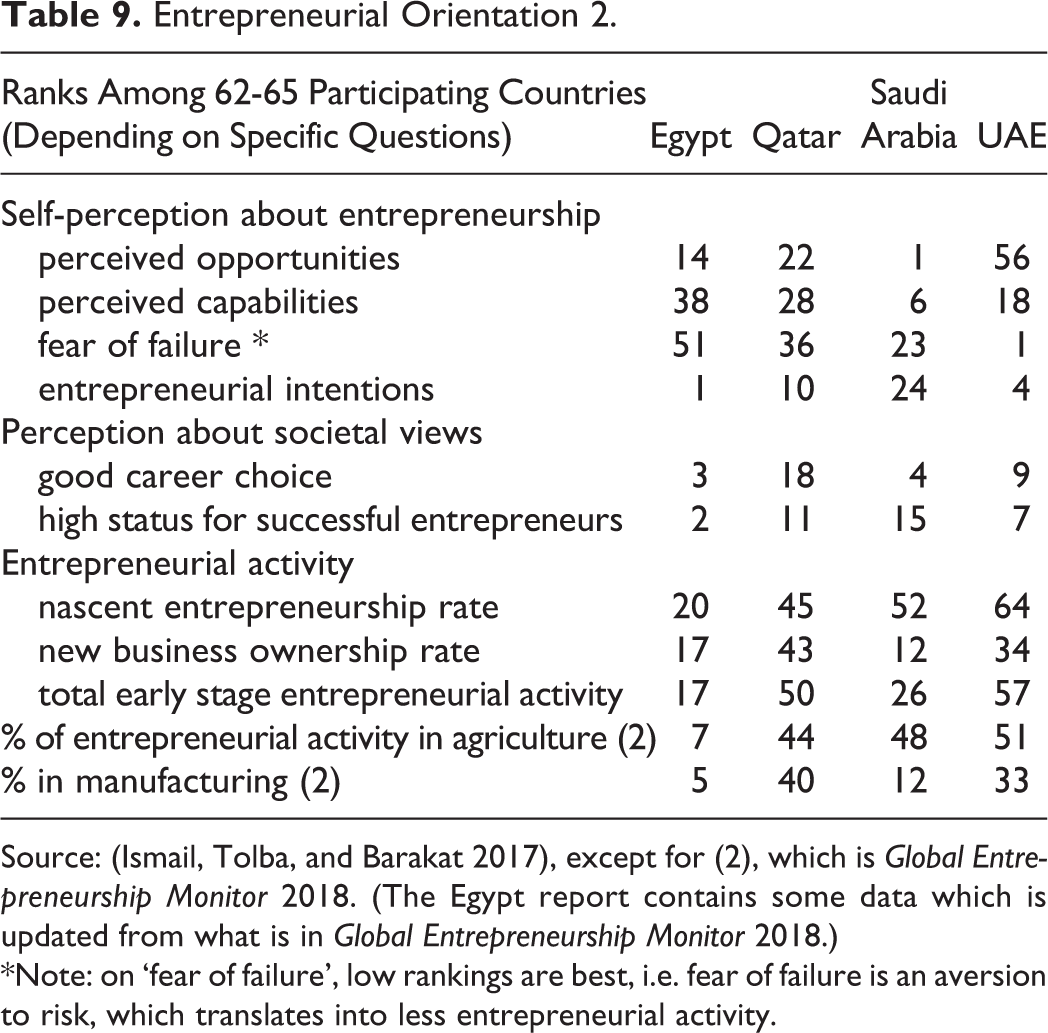

Table 9 demonstrates Egypt’s advantage in the entrepreneurship resource. Saudi Arabia is much stronger in ‘perceived opportunities’, otherwise, Egypt leads the participating GCC States. ‘Perceived capabilities’ lags somewhat in Egypt. Ismail, Tolba, and Barakat (2017) note that this represents a sharp decline over the past decade, probably reflecting reaction to Egypt’s economic difficulties. However, Egypt is ranked quite low on ‘fear of failure’, which is a reversed scale where low rankings represent less risk aversion in starting a business. High ranks here indicate serious obstacles to entrepreneurship. Social views toward entrepreneurship are very favorable in Egypt, even compared to the Gulf, where views are generally positive.

Entrepreneurial Orientation 2.

Source: (Ismail, Tolba, and Barakat 2017), except for (2), which is Global Entrepreneurship Monitor 2018. (The Egypt report contains some data which is updated from what is in Global Entrepreneurship Monitor 2018.)

*Note: on ‘fear of failure’, low rankings are best, i.e. fear of failure is an aversion to risk, which translates into less entrepreneurial activity.

Entrepreneurial intentions are highest in Egypt among the 65 countries surveyed, with 65 percent of Egyptian non-entrepreneurs stating an interest in starting a business within the next three years. Of course not all of them may actually follow through, but actual ‘entrepreneurial activity’ also ranks fairly high. On the other hand, while the GCC data show moderately positive views, and participants do express fairly high ‘entrepreneurial intentions’, this does not actually translate into entrepreneurial activity nearly as much as in Egypt. On ‘nascent entrepreneurship rate’, which is percentage of adults (18-64) who are currently setting up a business, and ‘new business ownership rate’, those who have set one up within the past three and a half years, Egypt ranks far higher than the three GCC countries with data. (Total early stage entrepreneurial activity’ is a composite of these two measures.)

Equally important for the discussion here, Egypt ranks far higher in proportion of entrepreneurial activity related to agriculture. It also ranks higher for entrepreneurial activity in manufacturing, relevant because much manufacturing by small start-up businesses would be in food processing (e.g., Alpen Capital 2017). Overall, when focusing on entrepreneurial thinking and action by people, rather than on the institutional framework supporting entrepreneurship, Egypt has a clear advantage. Of course, the ecosphere is important; but in itself it will not contribute much if people do not take advantage of it much. And, the ecosystem issues are present in the other resources discussed here, both above and in the next few sections.

Technology

The situation is mixed with respect to this resource. Many specific projects in both the Nile Valley and the Gulf utilize modern technology in agriculture, but for mass production, technology is not particularly advanced anywhere in the Arab world. It is, however, available, and better technology implementation (which needs stronger funding) could substantially improve agricultural production, as well as post-harvest handling. It was noted above that there is not much scope for expanding the land under production, and climate restricts gaining much from additional cropping cycles during the year. The Arab Forum for Environment and Development (2014) estimates that about three-fourths of increased production in MENA must come from intensification of agriculture, i.e. mostly better yields, which come from improved practice and application of modern technologies. The Arab Forum for Environment and Development (2014, pp. 56-57) report on field trials across a number of Arab countries over multiple years, in which farmers participated in demonstration projects to learn modern applications. Non-participating farmers in the Egyptian control group had much higher yields than in other countries, and their average yield still remained slightly above that of participating farmers in most countries. Nevertheless, the intervention improved yields everywhere they were implemented. In the 2012-2013 season, participating farmers were able to increase grain yield by an average of 25 percent (Egypt) and 68 percent (Sudan).

Although the scale is too small for mass production of many crops, many Gulf States are developing advanced agricultural technologies. The Hague Centre for Strategic Studies (2015), which mainly takes the view of potential investors, rates several GCC countries high on potential for the agribusiness industry, and Egypt quite low. “Richer Gulf countries are interesting markets for high-quality food products.…The region offers opportunities for agribusinesses that are less land and water intensive. And there is a large market for innovations that lead to more effective use of water resources, and companies with water efficient means of production” (Hague Centre for Strategic Studies 2015, p. 18). Kim and van der Beek (2018), for example, have considerable discussion about technology initiatives in Saudi Arabia, the largest Gulf economy. Alpen Capital (2017) focuses on developing hydroponics capabilities in Saudi Arabia and several other Gulf States.

Downstream from primary production, food processing technology is strong in the GCC (e.g., Dowling and Vanwalleghem 2018). Many major food processing multinationals have been attracted to the high-spending-power markets and invested, often in joint ventures (e.g., Alpen Capital 2017). Many domestic food companies have also had plenty of capital to invest in advanced food processing technology (Alpen Capital 2017). The Hague Centre for Strategic Studies (2015) also notes the potential in Egypt for development of food processing, even though it thinks the Gulf offers better agribusiness investment opportunities. In fact, some Gulf food processing companies have already started acquiring Egyptian food processing companies (Dowling and Vanwalleghem 2018).

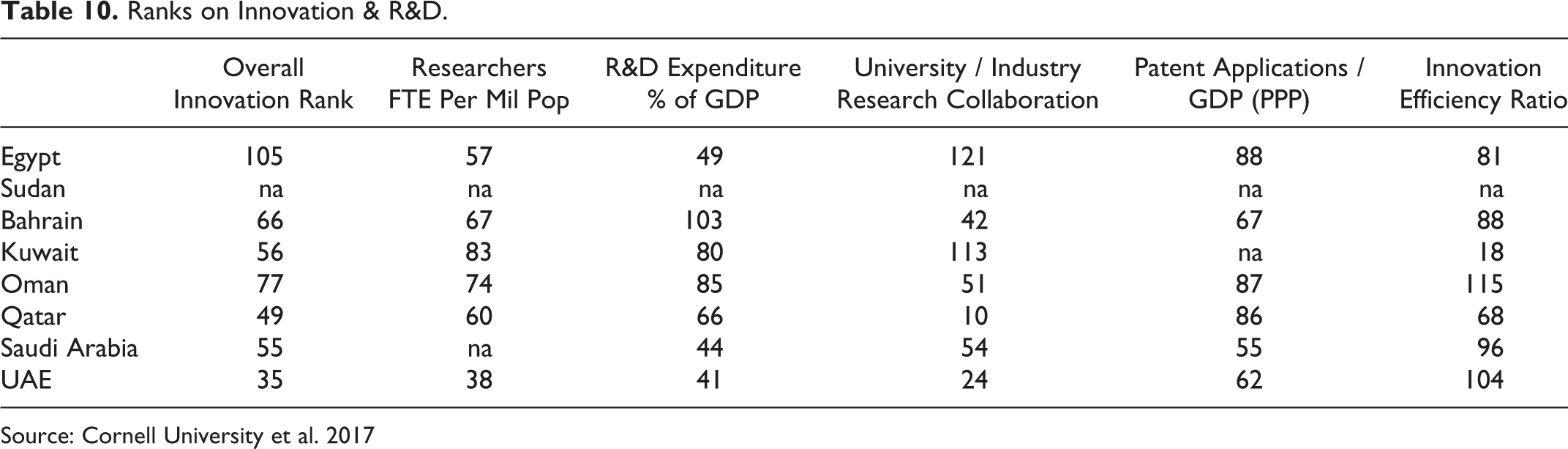

The Global Innovation Index (GII) gives a sense of technology development relative to the rest of the world. Usefully, “the 2017 edition of the GII is dedicated to the theme of innovation in agriculture and food systems” (Cornell University et al. 2017, p. v). Table 10 indicates that generally GCC and Nile Valley countries are roughly middle of the pack out of the 127 countries ranked on a range of measures. Each region has some slight strengths and some slight weaknesses relative to the other, as a few specific indicators show. Egypt, for example, has more researchers per capita than most Gulf countries, and higher R&D expenditure as a proportion of GDP. However, it is weaker than most Gulf countries on university – industry collaboration, and on developing technology which can be patented. The innovation efficiency ratio (last column), which assesses results relative to inputs, shows that most of these countries are weak at translating R&D into practical application.

Ranks on Innovation & R&D.

Source: Cornell University et al. 2017

Nevertheless, with regional integration, there is high potential for turning the technology resource into competitive advantage. Part of the problem in Egypt (and Sudan) is lack of resources to make the somewhat more extensive R&D activity more effective, while the Gulf often seems to throw money at things without as much impact as it should be able to expect. Clearly there is scope for synergy here. Even though it does not really use technology very effectively, the Gulf States do have an advantage in technology. Egypt (and even more, Sudan) lacks needed technology in agriculture. Each area individually has its own strengths and weaknesses relative to the other area, and each with only mid-level capability relative to the rest of the world. Working together, they would likely be much stronger.

Institutional

Egypt and Sudan have old well established institutions in agriculture, particularly for major crops such as cotton, wheat, sugar cane, fruits and vegetables, as well as for dairy and meat production. They have Government and private organizations that deal with production, distribution, marketing and export of these products through traditional supply chains. Unfortunately these institutions and supply chains are usually very inefficient, with much red tape, corruption, poor management, and lack of modern facilities and equipment (Alpen Capital 2017; Arab Forum for Environment and Development 2014, 2016, 2017; Food & Agriculture Organization 2013a, 2013b; World Bank 2018b; World Economic Forum 2017b). Therefore, this resource is in poor condition and will require substantial funding to improve, and should be considered at somewhat of a competitive disadvantage in Egypt and Sudan.

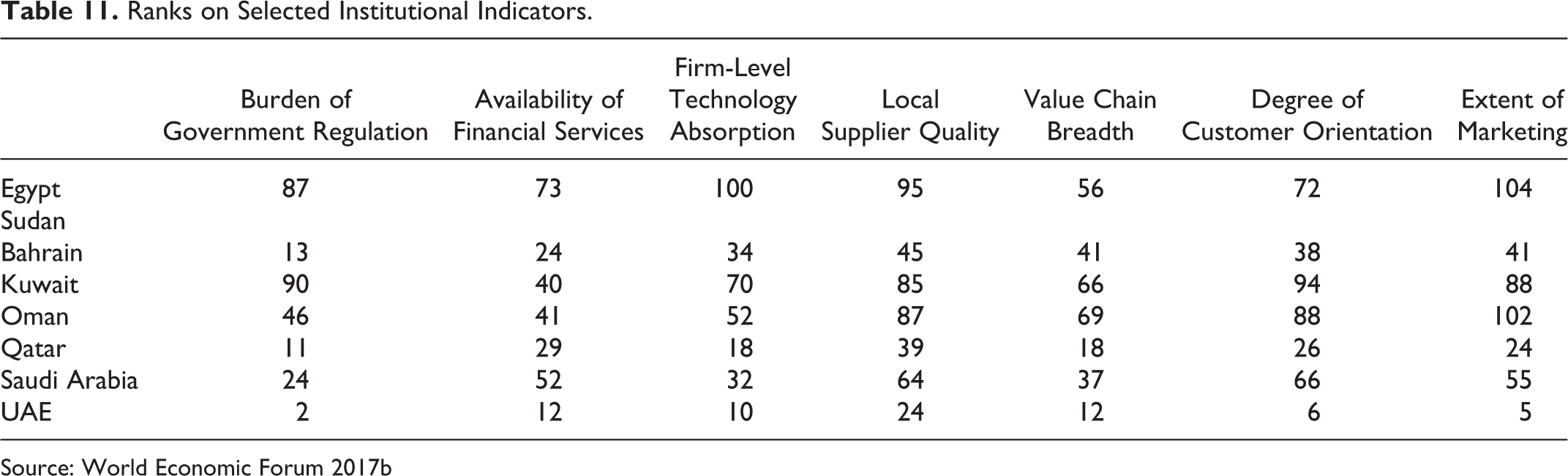

The Gulf States are developing fairly strong institutions to support a modern economy. The discussion above indicates this specific to entrepreneurship, but institutional development in the GCC is actually much broader. Even though institutions specific to agriculture are not yet a major part of this, the foundation covers the small agricultural sector and can easily accommodate agriculture as it becomes a somewhat larger component of the economy. Table 11 indicates that government is more supportive, while less intrusive, in most Gulf States compared to Egypt and Sudan. Financial services are more widely available. The business sector is more open to using new technologies (which is a separate issue from simple availability of technology noted above). Local supplier quality is stronger in some Gulf States, as is the breadth of the value chain. In some Gulf countries, business is becoming strongly customer oriented, probably because marketing is expanding its role in these economies. Progress in these areas is somewhat uneven across countries, but many GCC countries show substantially stronger performance on a range of institutional issues.

Ranks on Selected Institutional Indicators.

Source: World Economic Forum 2017b

Legal Infrastructure

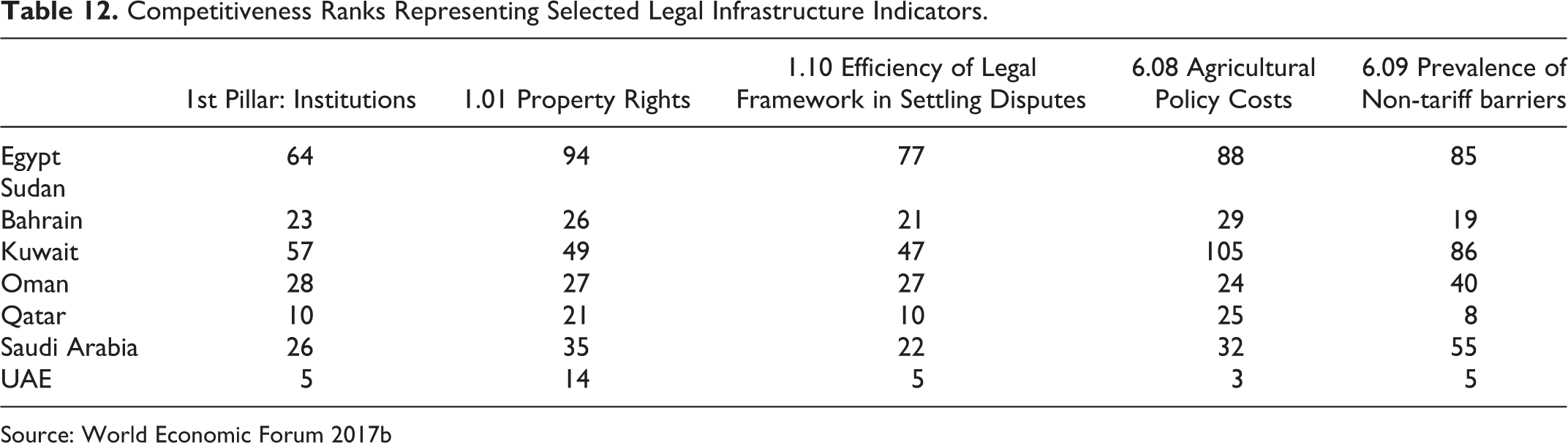

The legal infrastructure in Egypt is still somewhat based on a socialist system originally imposed by President Nasser over 50 years ago. There have been some deviations from heavy government involvement in agriculture and a gradual move toward privatization and a free market. In the past few years, reform has brought some progress (e.g., World Bank 2018c), but there remains much to do. Many laws and regulations are outdated, anti-competitive, and led to inefficiencies in production and distribution. These laws led to fragmentation of land, and dependence on Government support through subsidies and Government purchasing of some crops. These laws affecting productions need reexamination and updating, although politically sensitive. On the other hand, laws affecting marketing, the environment, safety, and consumer protection are either lacking or inadequate. Sudan has somewhat different legal infrastructure, but is, if anything, in a worse position than Egypt (Arab Forum for Environment and Development 2016, 2017; United Nations Development Programme 2011; World Bank 2009; 2013; 2018b, 2018c). Thus, this resource has a strong competitive disadvantage.

In Table 12, the GCI’s 1st Pillar ‘Institutions’ measures government performance, including a number of indicators on law and policy. This table confirms that overall, Egypt is well behind most GCC countries. It also substantially lags most of the GCC on a range of individual indicators, including, for example, property rights and the efficiency of the legal framework to settle disputes. (Kuwait stands out as an exception in the GCC, with poor performance on most of these indicators.) While agriculture is a much smaller proportion of the economy in the GCC, policy interferes with the sector much less than in Egypt (and Kuwait), and the economy is relatively open, important for upgrading agricultural inputs and agricultural technology. The GCC clearly has an advantage here.

Competitiveness Ranks Representing Selected Legal Infrastructure Indicators.

Source: World Economic Forum 2017b

Economic Integration for Improved Food Security in the Arab region

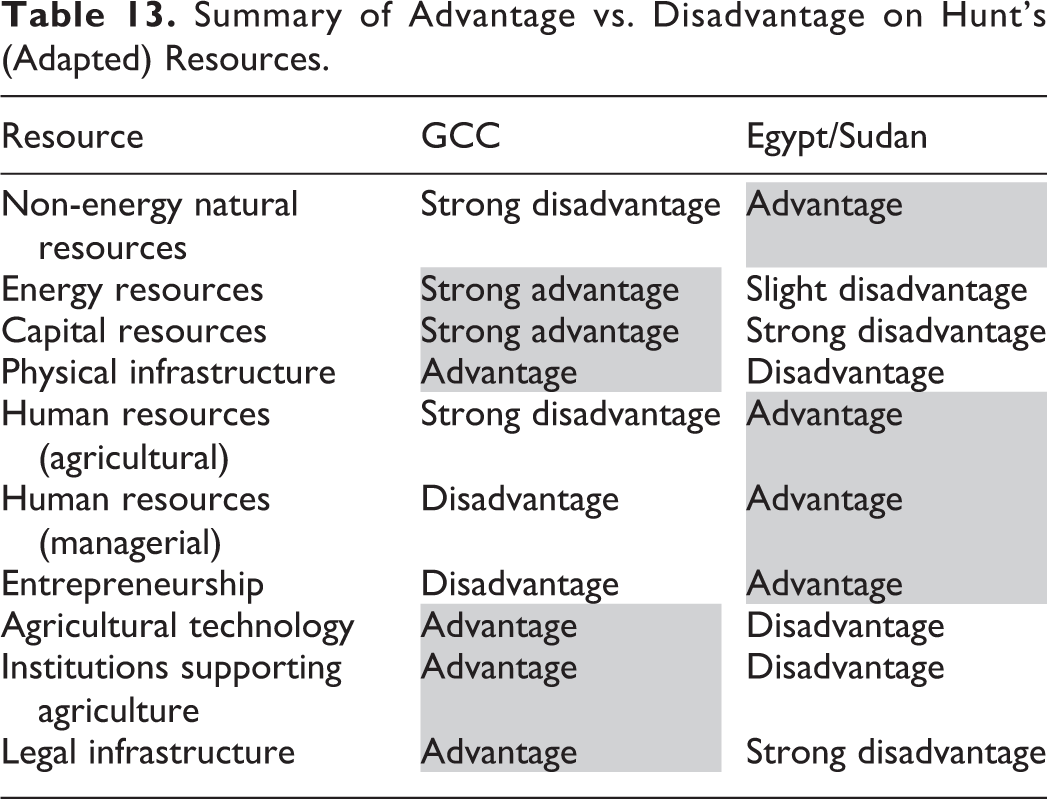

Table 13 summarizes the ten key resources adapted from Hunt’s (2007, 2011) resource advantage framework. A simple inspection of the table shows that the Egypt and Sudan sub-region has some competitive advantage in four of these elements, and disadvantage in six. The GCC countries have some advantage in six elements, and disadvantage in four. But on every element where Egypt and Sudan are weak, the GCC is strong, and where the GCC is weak, Egypt and Sudan are strong. Furthermore, on a few elements, an influx of GCC resources could potentially shift disadvantages in Egypt and Sudan to strengths. Observers might quibble with a few details of our assessment, but the overall pattern is clear – these two separate parts of the Arab world lack the ability to escape food insecurity on their own, but as an integrated bloc, they would be very strong. Strengths and weaknesses are completely complementary; in each case where one side is at a disadvantage, the other side shows advantage.

Summary of Advantage vs. Disadvantage on Hunt’s (Adapted) Resources.

Economic integration is now a must for economic advancement and prosperity in the MENA region. In agriculture, “cooperation among Arab countries based on comparative advantage in agricultural and financial resources is a key option for enhancing food security at the regional level” (Arab Forum for Environment and Development 2014, p. 10). Freer flow of goods, services, capital, and labor in an integrated region will increase productivity of resources as each resource will move freely to where it is needed most, and thus will gain the highest return. This can lead to better availability of goods and services in the integrated region. This is not a new concept, but it has not been carried forward in the past.

For example, Abedini and Péridy (2008) show that The Greater Arab Free Trade Area has resulted in increased trade, but they also noted that despite much talk about economic integration for many decades, the Arab region has not really implemented much from the various integration frameworks. They recommended deeper integration a decade ago. Continued talk about economic integration has not gained much from the various integration frameworks, and current discussion continues to point out the need for deeper integration (e.g., Rouis and Tabor 2012; World Bank 2012a). Often, the talk seems more about political positioning than economic implementation; for example, while MENA countries have generally reduced tariffs, they have constructed an impressive set of non-tariff barriers to negate most benefits from tariff reduction (e.g., Péridy and Ghoneim 2013).

If these difficulties can be overcome, the abundant financial resources from the Gulf States can be utilized in Egypt and Sudan to advance agricultural technology, land reclamation, scientific research, and for upgrading physical infrastructure and supply chains. These resources can be applied to the fertile land and water resources in the Nile valley in raising food production with the aid of abundant affordable skilled human resources in that region. Obviously low cost energy from the Gulf Region can be used in mechanization of agricultural production, food processing, packaging production, and transportation and storage, which will make such operations more efficient and competitive. All these resources complement each other, but in isolation they contribute little to food security.

Conclusion

This brief discussion has only begun to scratch the surface of how marketing practice and marketing systems are deeply interwoven into actual use of Hunt’s Resource Advantage Theory. Examining the problem in much more depth would show even more scope for a wide range of the marketing implementation tools. Nevertheless, the limited discussion possible here already clearly demonstrates that marketing is fundamental in applying the RA framework theory to foster food security in the MENA region. No single country or sub-region can realistically hope for any advantage in the agriculture / agribusiness industry, but economic integration offers strong potential for dealing with this problem.

“Arab countries still have a very long way to realize the underutilized agricultural potential in the Arab world that could enhance food security at both national and regional levels. It is essential for Arab countries to enhance regional cooperation to promote agricultural production based on complementarities and their comparative advantages to achieve regional food security and reduce the unwarranted food import bills” (Arab Forum for Environment and Development 2017, p. 115)

Application of the RA framework here confirms that frequent recommendations for more regional cooperation are not unrealistic, at least on the level of whether it would actually provide substantial benefits if actually implemented. Different sub-regions have complementary sets of advantages and disadvantages, and integrating the sub-regions could produce very strong competitiveness. The RA framework works. It can be used effectively to demonstrate that as an integrated region, Egypt and Sudan and the Gulf could have strong competitive advantage in agricultural industries. Combining these two parts of the Arab world cancels out a number of disadvantages that each part separately has in Hunt’s resources. The value of these resources could be enhanced and better utilized if coordinated with resources available in other Arab countries. This can be done with regional economic integration.

The Nile Valley (Egypt and Sudan), and the Arab Gulf Countries were used as an example, but the basic concept is likely to hold even more broadly in the Arab world. This paper stays at the modest level of only looking at these two sub-regions, but future work could examine whether integration of other major Arab regions, such as the Maghreb or Levant could contribute to stronger food security. And, of course, this analysis can be applied to other industries beyond agriculture / agribusiness, and other regions beyond the Arab world.