Abstract

This article examines sovereign credit rating methodologies and their impact on fiscal space in developing economies. While sovereign ratings are meant to reflect default risk, the biases embedded in the rating methodologies result in overly punitive rating actions in developing economies that often limit their ability to implement countercyclical policies. In addition, with a singular focus on austerity, they tend to shift focus away from critical development priorities and social welfare spending. Using panel data of credit rating changes in 133 countries over the period 2000–2020 from Moody’s, we explored the long-term trends in the impact of ratings. Negative rating actions have been intensifying in developing economies since 2010. We found that rating changes did tend to influence fiscal priorities. Downgrades lowered the proportion of spending on health and education and increased the proportion of spending on interest payments. We situate this examination of credit ratings within the framework of the financial subordination literature. We suggest that credit ratings are a new manifestation of financial subordination and have created a new dimension in reproducing and deepening the inequalities in the global financial system.

1. Introduction

The COVID-19 pandemic drew attention to the importance of fiscal investments in social and human infrastructure. Globally, large injections of cash helped economies shore up their health systems and prevent economic collapse from the pandemic. According to the International Monetary Fund (IMF) estimates, pandemic-related fiscal measures amounted to over $10 trillion in expenditures globally (IMF 2021a). Such spending though exposed the deep inequalities in the global financial system. The majority of the expenditures occurred in developed economies given their ability to mobilize such large sums of money on short notice through inexpensive deficit financing. Developing economies, on the other hand, experienced a great financing inequity with limited access to credit markets and high cost of borrowing. This in turn intensified debt repayment burdens and threatened a looming debt crisis. A direct manifestation of this financing inequity is sovereign credit ratings. While credit ratings are intended to provide potential creditors with information about the relative risk of default, the opacity and largely short-term focus of the existing ratings frameworks have emphasized austerity as a singular goal for fiscal policy particularly in developing economies. Any expansion of spending, even on critical social development goals like health infrastructure, brought threats of downgrades or negative outlook. Even when such spending was recommended for short-term crisis relief during the COVID pandemic, developing economies were forced to limit critical expenditures to avoid rating downgrades.

While the impact of the ratings on spending was most visible during the pandemic, there is also a potential for more long-lasting implications. The general emphasis on fiscal austerity and the short-term orientation of most of the rating criteria not only impose a barrier to accessing financing during crises but can also create an incentive to limit long-term investments in social infrastructure. Downgrades particularly have the potential to spur a cycle of austerity targeting what might be considered expendable social spending in the short run, on healthcare for example, while causing harm to long-term development goals. In this article, we used a panel data set with credit rating information for 133 countries for the period 2000–2020 to examine the impact of rating changes on government spending priorities.

We found that changes in credit rating did have a statistically significant impact on health and education spending as a proportion of total government expenditures. Improved ratings or upgrades were associated with a greater proportion of spending on healthcare and education. Downgrades and negative outlooks negatively impacted spending proportions on healthcare and education. At the same time changes in credit rating have the opposite impact on interest payments (on government debt). Improved ratings were associated with a lower proportion of spending on interest payments on government debt. Downgrades or negative changes were associated with a higher proportion of interest payment expenditures. These findings lend support to the argument that rating changes increase the burden of debt repayments and have a long-term impact on the fiscal priorities of governments particularly in developing economies. We also found that developed economies were likely to withstand negative rating changes and continue to expand fiscal spending, unlike developing economies.

This is consistent with the general perception of bias toward advanced economies in the current credit ratings framework. Ratings changes, particularly negative changes, have been less frequent in advanced economies over the past decade. This has enabled them to have lower interest payments and a greater ability to maintain fiscal space for social welfare expenditures as reflected in our empirical findings. The relative ratings stability is partly a reflection of the dominant position of their currencies in the international financial hierarchy which confers automatic advantage in the ratings calculations. This, combined with their greater ability to borrow in their own currencies and domestic markets, affords advanced economies much greater fiscal policy space and perpetuates asymmetries in the global financial system. Here we evaluate the ways in which the current credit ratings methodologies reinforce global financing inequities by their disproportionate impact on fiscal space in developing economies. In doing so we also situate the critique of sovereign ratings within the literature on subordinate financialization. We argue that the imposition of an artificial short-term, austerity-oriented fiscal horizon by the current mechanisms of evaluating sovereign creditworthiness has created a new dimension in reproducing and deepening inequalities in the global financial system.

This article contributes to the literature in two ways. First, while there is some research on the fiscal impact of sovereign credit ratings it is often from the perspective of fiscal discipline. Here the impact of credit ratings is viewed positively as a disciplinary mechanism (Bianchi, Ottonello, and Presno 2019; Duygun, Ozturk, and Mohamed Shaban 2016; Hanusch and Vaaler 2013, 2015). When studies have looked at the impact of credit ratings on social investments or other welfare spending, the focus has been primarily on advanced economies (Barta and Johnson 2020, 2023). A few studies have examined the impact of ratings on pandemic-related stimulus (Balajee, Tomar, and Udupa 2020; Benmelech and Tzur-Ilan 2020). However, this remains a limited episodic evaluation. In our study, we look at the long-term impact of credit ratings on fiscal space for a combination of both developed and developing economies. We also shift the focus from austerity to the importance of fiscal space for welfare and social spending priorities. Second, we are also adding to the literature on financial subordination. A long tradition of literature on dependency theory has pointed to the subordinate position of developing economies in the global political economy (Dos Santos 1971; Sunkel 1969; Kvangraven 2020). A more recent stream of this literature has pointed to new forms of subordination created by increased financialization (Becker et al. 2010; Mushtaq 2021; Kaltenbrunner and Painceira 2018; Bonizzi, Kaltenbrunner, and Powell 2019). Based on our empirical findings and an evaluation of the biases in the ratings methodology, we argue that credit ratings should be viewed as a tool of financial subordination.

The plan for the rest of the article is as follows. In the next section, we review the crisis of sovereign rating downgrades during the COVID-19 pandemic and the ensuing discussion on ratings as a barrier to critical development finance. This is followed by a literature review in section 3. Section 4 presents the empirical analysis including data description, the empirical model, and results. In section 5, we present a critique of the ratings methodologies based on the subordinate financialization literature. This is followed by a concluding section with a discussion of potential reforms.

2. Sovereign Credit Ratings in Focus during the COVID-19 Pandemic

The impact of sovereign credit ratings and the credit rating industry drew renewed attention in 2020 during the COVID-19 pandemic. The sudden need to expand fiscal spending for critical healthcare needs and stimulus packages to prevent economic collapse from pandemic-related shutdowns heightened concerns about sovereign debt overload and debt distress. This led to a spate of credit rating downgrades. The downgrades however were disproportionately directed at countries in the Global South. Emerging and developing economies accounted for more than 95 percent of the sovereign downgrades in 2020 (Griffith-Jones and Kraemer 2021). In Africa, 56 percent of rated countries were downgraded in 2020 (Fofack 2021). This is even though as a group, developing countries accounted for much less spending expansions and experienced lower rates of economic contraction in comparison to advanced economies. According to IMF estimates, nearly $10 trillion were mobilized globally for COVID relief primarily through deficit financing. Borrowing and spending were considerably greater in advanced economies where, as a group, pandemic-related spending averaged about 12 percent of gross domestic product (GDP). In contrast, pandemic-induced spending in emerging market economies averaged about 6 percent of GDP, while in low-income developing economies the average was only about 3 percent (Battersby, Lam, and Ture 2020).

A financing divide emerged where advanced economies could access funds at lower interest rates, pushing average debt-to-GDP ratios to a little over 120 percent in 2020. Whereas for emerging market and low-income economies, debt-to-GDP ratios averaged about 60 and 50 percent respectively (Gaspar, Medas, and Perelli 2021). As advanced economies entered the COVID-19 pandemic with higher credit ratings, it was to be expected that they would have greater access to low-interest financing. Indeed, this was the case as noted by the IMF Fiscal Policy Monitor (IMF 2022). However, the extreme limits to deficit financing experienced by developing economies when countercyclical fiscal space was vital for recovery from the pandemic also drew attention. More than a few anecdotal cases highlighted the particularly debilitating extent to which credit ratings influenced access to financing during the pandemic.

In the case of Morocco, for example, the very announcement of expanded spending on healthcare, as recommended by the World Health Organization, led to a credit rating downgrade. Both Fitch and Standard & Poor downgraded Morocco’s rating to speculative grade, because of its plan to spend more on social services. This then increased the cost of borrowing for such vital spending (Jones 2020). The fear of such pre-emptive ratings downgrades prevented most countries in Sub-Saharan Africa from accessing international capital markets in 2020, even as many of the developed economies were expanding deficit financing (Group of Thirty 2020; Kharas and Dooley 2021). Pre-emptive ratings downgrade also hit countries attempting to take advantage of the Debt Service Suspension Initiative (DSSI) initiated by the G20. Created in May 2020, DSSI was meant to allow low-income economies temporary relief from debt service payments while they focused on pandemic-related spending to support a faster recovery (The World Bank 2022). However, countries became wary of applying to the DSSI since CRAs seemed to view such applications as grounds for negative rating action. In fact, in the cases of Cameroon and Ethiopia, the request to seek relief through the DSSI led to ratings downgrades (African Peer Review Mechanism 2021), discouraging others from seeking similar relief (Landers and Aboneaaj 2022).

Such prohibitive downgrades led the African Union ( 2020) to question the pro-cyclical rating changes for their potential to create self-fulfilling cycles, where, raising the cost of borrowing during times of extreme crisis only worsens the economic outlook. This potential for credit ratings to reinforce pro-cyclicality and therefore create an obstacle to recovery was also highlighted in the first report of the United Nations independent expert on debt and human rights to the United Nations Human Rights Council (UNHCR 2021). As the report noted, procyclical downgrades run the risk of activating a debt crisis as they pre-emptively shift market sentiments against the country, creating a multiplier effect of higher borrowing costs. Therefore, instead of a forewarning of a debt crisis, the ratings downgrades themselves become the cause of it.

The UN report further noted the crucial role of financing not only during crisis periods but for long-term development goals as well. In the absence of substantial domestic savings or tax base, borrowing, particularly in the international markets, enables increased investments in infrastructure. Such investments could expand productivity and promote economic and social well-being. However, credit rating frameworks fail to distinguish between such “good” investments and critical social welfare expenditures from other types of government expenditures as we explore in greater detail in the following sections. The indiscriminate emphasis on fiscal austerity therefore prevents access to such development financing not only during the crisis but also during other times. Moreover, pre-emptive downgrades can have long-term spillover effects as fiscal attention is focused on managing the fallout from the downgrades and deflected away from critical development or infrastructure needs.

In this study, we are interested in examining this extended, long-term impact of credit rating on fiscal space and priorities. We found that this long-term impact of rating changes on social and development spending, particularly in developing economies, has not been adequately addressed in the empirical or theoretical economic literature.

3. Literature Review

Much of the literature on sovereign credit ratings has focused either on the determinants of credit ratings, or the role of credit ratings in promoting fiscal discipline. For example, Hanusch and Vaaler (2013), look at the disciplinary impact of credit ratings on fiscal spending around the political budget cycle, which is the spending around national elections. Based on an empirical analysis of 18 emerging democracies, they suggest that credit ratings do impose greater fiscal discipline, with higher-rated countries tending to borrow less during election cycles. Similarly, in another study of the election cycle, the same authors found that rating downgrades tended to cause the incumbent governments to lose elections (Hanusch and Vaaler 2015). Bianchi, Ottonello, and Presno (2019) explore a theoretical analysis of the optimal fiscal spending to prevent rating downgrades and conclude that governments should be restrained in expanding fiscal stimulus even during recessions to avoid the threat of higher interest rate spreads and debt crises in the future. Duygun, Ozturk, and Mohamed Shaban (2016) also investigated the impact of credit ratings from a fiscal discipline framework. They report finding a procyclicality in ratings, that is, a country’s debt levels tended to increase when ratings improved.

These studies have the unquestioned assumption of fiscal austerity as a desired goal without evaluating the actual impact of fiscal austerity or its implications for living standards and welfare outcomes. Neither do they distinguish between the various types of spending, looking at, for example, welfare-improving expenditures, since they assume overall reductions in spending are the goal. A few have, however, questioned the procyclicality imposed by credit ratings and the negative impact of this during a recession. For example, Ferri, Liu, and Stiglitz (1999) found that during the Asian financial crisis credit rating agencies aggravated the crisis by overcompensating downgrades that only made recovery harder for the impacted countries. The procyclicality of ratings has also been studied in other contexts. Broto and Molina (2016) study procyclicality from the perspective of how ratings are determined. Their empirical study used a sample of S&P ratings for sixty-seven countries and found that downgrades tended to be deeper and more frequent. Upgrades on the other hand were infrequent and often did not follow directly from improving economic fundamentals. Thus, aggravating procyclicality, particularly in the case of downgrades. Pretorius and Botha (2017) also found procyclicality in ratings using sovereign ratings data from twenty-seven African countries. Again, this study is focused on the determination of ratings rather than the impact of ratings on fiscal spending.

Very few studies have looked at the impact of ratings on fiscal spending outside of the framework of fiscal austerity as the desired goal. Benmelech and Tzur-Ilan (2020) found that a key determinant of fiscal expansion during COVID-19 was a country’s credit rating. Similarly, Balajee, Tomar, and Udupa (2020) also found that credit ratings were the most impactful influence on a country’s ability to provide fiscal stimulus during the pandemic. They further identified the twenty-two most vulnerable countries where additional stimulus would have helped mitigate steep economic declines. These studies, however, address fiscal spending in the short term, specifically during crisis periods. Longer-term studies of the impact of credit ratings on fiscal spending, particularly spending on social welfare, are even more sparse. The few studies we found were limited to developed economies. For example, Barta and Johnston (2020) presented an empirical study of the relationship between welfare spending and credit ratings in twenty-three advanced market economies. They found that entitlement spending tended to lower credit ratings. In a 2023 study, the same authors again used data from twenty-three advanced economies from 1995 to 2019 and found that rating downgrades led to lower social services spending. To the best of our knowledge, there are no similar studies for developing economies. This is one of the gaps in the empirical literature we seek to address.

Given the long-term implications of credit ratings for social investments and the differential impacts on developed and developed economies, there also needs to be more theoretical focus on the methodology used to generate the ratings. In our analysis of the rating criteria presented in section 5 below, we found that developed countries have built-in advantages stemming from the global currency hierarchy and other historical and systemic imbalances in the global financial system. These systemic advantages can be understood through the lens of the financial subordination literature. Financial subordination refers to the subordinate integration of developing economies into the global financial system. This literature derives elements from the Latin American dependency theory and the critiques of financialization. Dependency theory pioneered the focus on the subordination of developing countries in the global political economy. With its core-periphery analysis, Dependency theory highlights the enforced dependence of developing economies on the developed core where independent progress in the former is limited and circumscribed by the progress of the latter (Dos Santos 1971; Sunkel 1969; Kvangraven 2020). Colonial trade relations where developing economies were locked into their role as suppliers of raw materials and prevented from value-added manufacturing expansion was one of the early mechanisms of subordination in the dependency literature. The financialization literature on the other hand has more traditionally focused on national economic trends of profit squeeze, contracting demand, and therefore increased credit-based activities, and the larger role of the financial sector in the economy (Magdoff and Sweezy 1972, 1987; Brenner 2004).

Since the increased prominence of the financial sector also came with greater international flows of capital, and monetary flows became as prominent as trade flows, the role of financialization in sustaining the core-periphery structure began to be scrutinized. The subordinate financialization literature thus emerged to explore how the power imbalances in the global economic system mediated the increasing financialization (Becker et al. 2010; Mushtaq 2021; Kaltenbrunner and Painceira 2018; Bonizzi, Kaltenbrunner, and Powell 2019). Musthaq (2021) noted that financial factors increasingly played a large role in reproducing subordinate relationships in the global political economy. One of the key asymmetries of the global financial system highlighted in this literature is the currency hierarchy. The United States has enormous financial power and privilege because the currency at the top of the order is the dollar. Currencies from other advanced economies viewed as part of the reserve currency basket also share in some of this privilege. Such privilege includes the ability to borrow in the domestic currency, often at lower interest rates, with relatively lower levels of volatility in capital flows. Developing economies on the other hand are subjected to greater external pressure with the inability to borrow in domestic currency and instead face the pressure to accumulate reserve currency issued by the developed economies (Tavares 1985; Belluzzo 1998).

The currency privilege has traditionally been analyzed as a failing that must be corrected by developing economies themselves. The original sin hypothesis popularized by Eichengreen and Hausmann (1999), drew attention to the dependence of developing economies on foreign currency borrowings. The potential for currency depreciation to increase the risk for creditors was suggested as one of the causes for raising risk perception and therefore the borrowing cost. The solution was for emerging economies to develop domestic financial markets and reduce dependency on foreign currency borrowings. However, as has been shown by Kaltenbrunner and Painceira (2018, 2015) and Bertaut, Bruno, and Shin (2021), emerging economies that did attempt to reduce foreign currency borrowing continued to be subjected to a great deal of volatility in capital flows particularly during crisis periods, therefore reinforcing procyclicality. Lenders continued to evaluate risk in the dominant currency (the dollar), thereby reducing the impact of switching from foreign to local currency borrowings. Several of these elements of financial subordination are reflected in the credit rating methodologies that we evaluate in the following sections.

4. Empirical Evaluation of the Long-term Impact of Sovereign Ratings

In this section, we present an empirical analysis of the impact of rating changes on long-term fiscal spending and priorities using a panel data set of 133 countries for 2000–2020.

4.1 Data and Summary Statistics

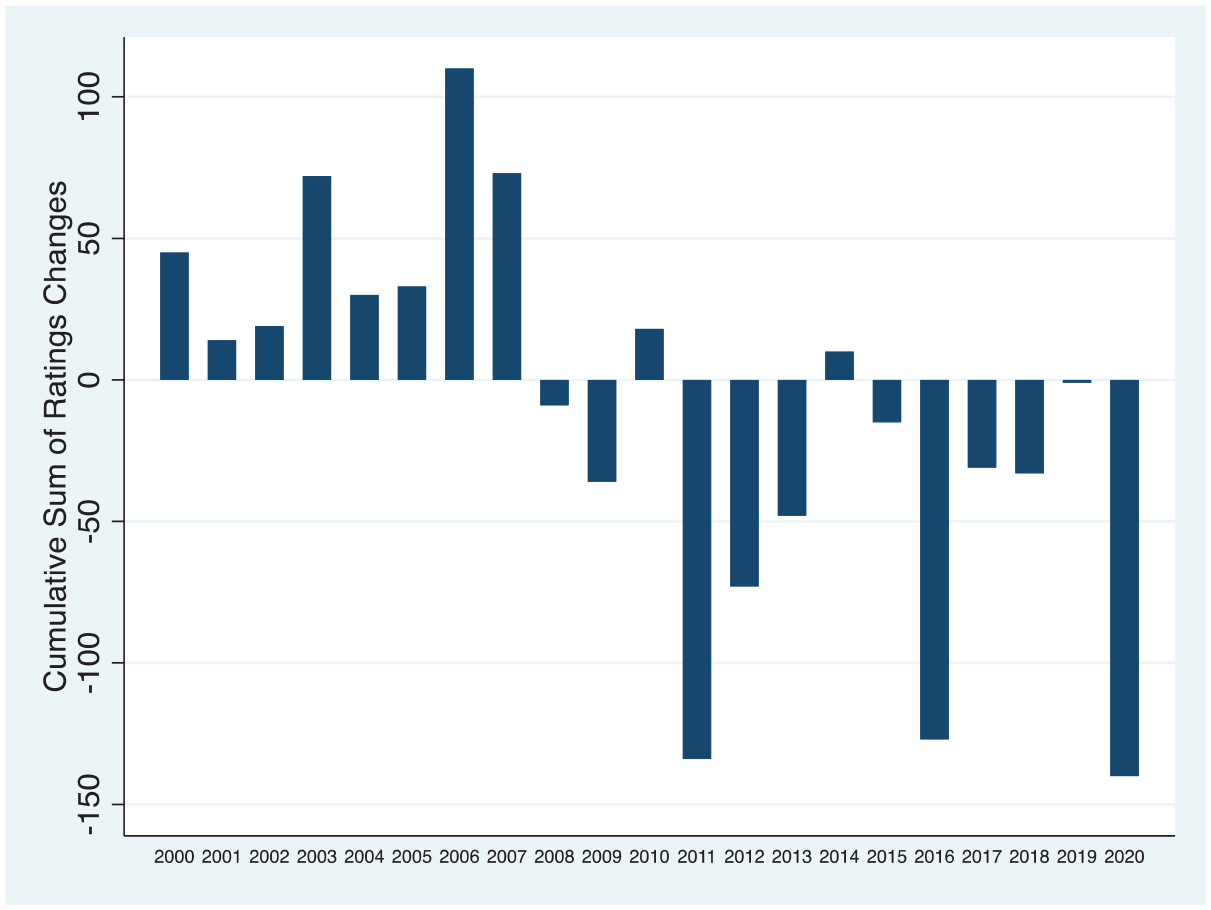

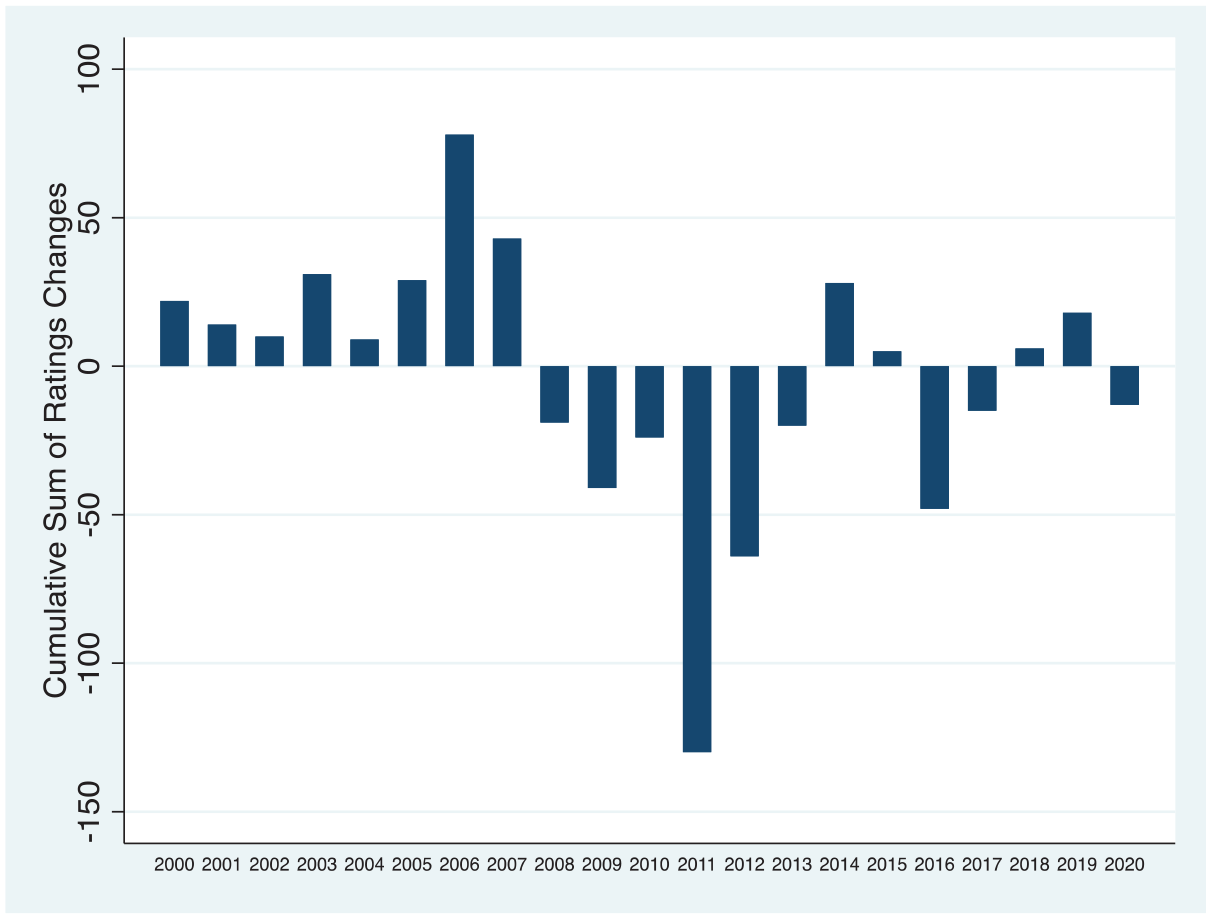

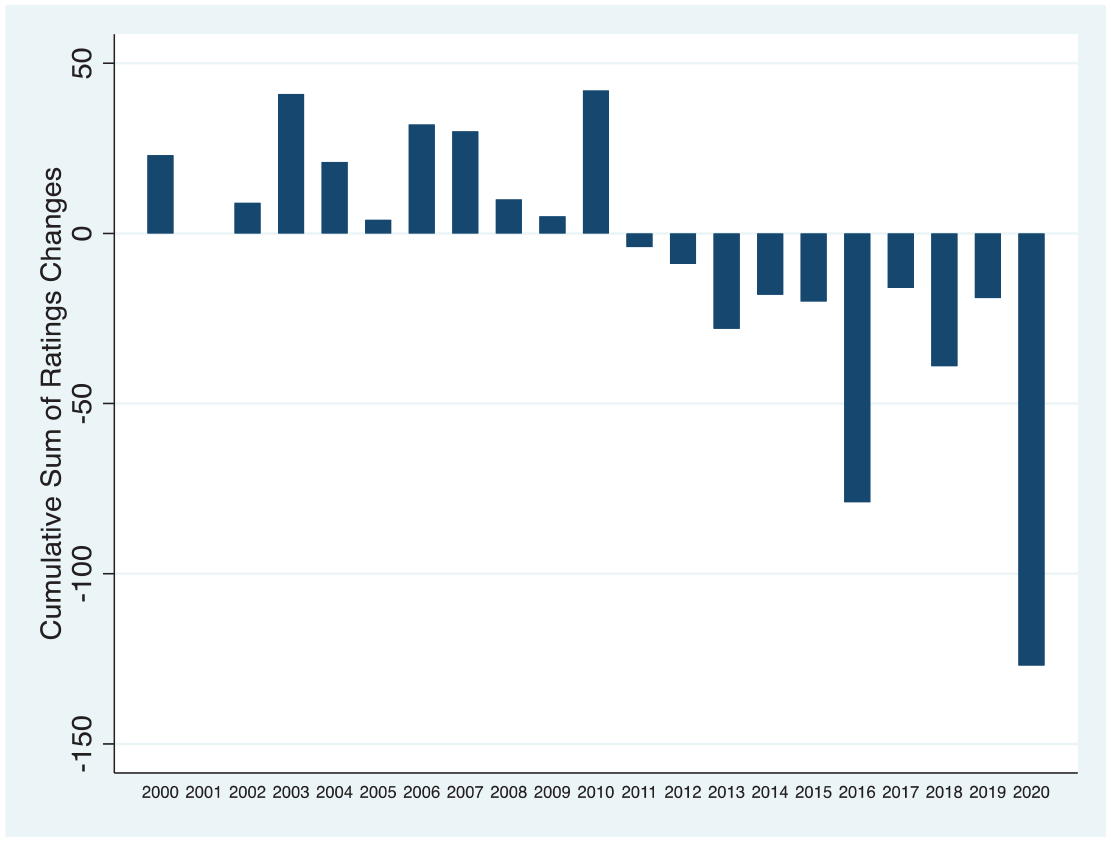

We collected available long-term sovereign foreign currency credit rating history for 133 countries for the years 2000–2020 from Moody’s Investor Services (Moody’s April 2021). The full list of countries is included in appendix A. Moody’s ratings range from the highest triple-A to the lowest C, the default grade. We converted the letter ratings to correspond to scores ranging from 1 to 21, with triple-A receiving a score of 21 and C receiving a score of 1. Using these data, we computed changes in rating for each country for each year. As per previous studies (Griffith-Jones and Kraemer 2021; IMF 2010), we assigned the following values for rating change actions: each point upgrade (downgrade) was assigned a change score of +3 (−3), each positive (negative) outlook was assigned a score of +1 (−1), and a review for upgrade (downgrade) was assigned a value of +2 (−2). The cumulative sum of all rating actions for the year was calculated for each year for each country. Countries that remained stable with no changes to the rating or ratings outlook received a change score of, 0, for that year. In figures 1 through 3, we explored the basic patterns in this two-decade data on sovereign rating changes.

Cumulative sum of sovereign rating actions, 2000–2020.

Cumulative sum of sovereign ratings action: high-income countries.

Cumulative sum of sovereign ratings actions: low- and middle-income countries.

In figure 1, we plot the cumulative changes for each year for all the 133 countries in the data set. We find that the occurrences of downgrades and negative outlook have increased considerably since 2010. We also see a surge in negative changes in 2020 in response to the COVID-19 pandemic.

In figures 2 and 3, we see that the negative rating changes since 2010 have been predominantly concentrated in low- and middle-income economies. In figure 2, we plot the rating changes over the years for the group of fifty-one high-income economies in the data set, classified according to the World Bank country classification. This group experienced substantial negative changes in ratings around the 2008–2009 financial crisis and again during the Eurozone crisis in 2011–2012. Since then, ratings and outlook have been relatively stable. In fact, in some years overall, positive rating changes have dominated. Even in 2020, during the COVID-19 pandemic, high-income economies experienced relatively smaller negative changes despite the substantial expansion of fiscal spending and deficit financing noted in the previous section.

In figure 3, we have the trends in ratings for low- and middle-income economies, a group of eighty-two countries in this data set. This group experienced relatively smaller cumulative changes before 2010. However, the number of developing countries with sovereign ratings was lower in the early part of the century. As the number of countries being rated has expanded, the intensity of ratings, particularly negative ratings, also expanded. Post 2010, negative changes have dominated. In 2020, low- and middle-income countries experienced a sharp cumulative decline in ratings and ratings outlook as the pandemic-related health and economic crisis started. Comparing figures 1 and 2 to figure 3, we found that the majority of the negative changes in ratings stemming from the COVID crisis were concentrated in the group of low- and middle-income economies.

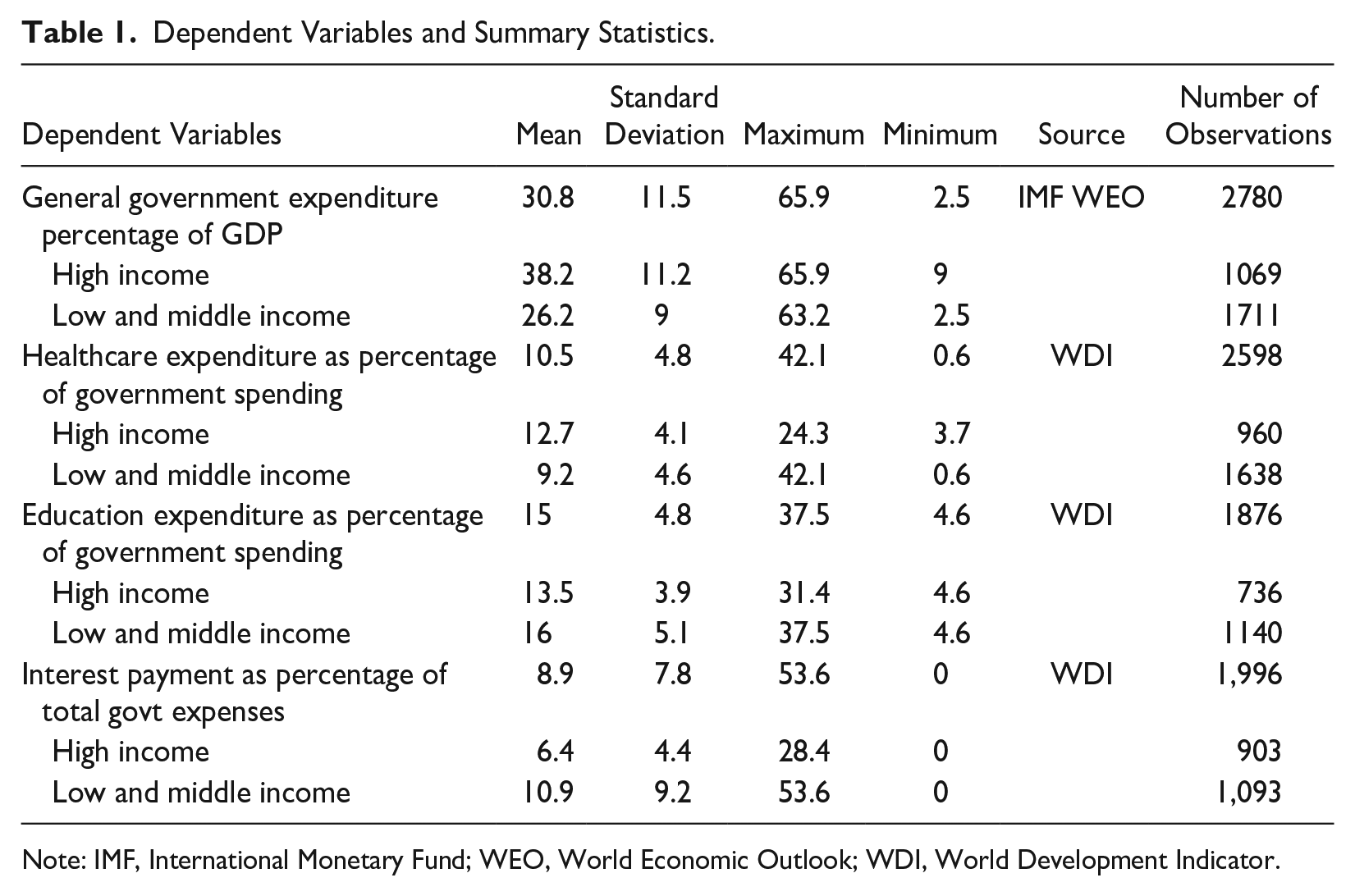

In this study, we are interested in expanding the understanding of the longer-term impact of sovereign ratings on fiscal space and priorities. We next turn to the data on fiscal spending. These data were gathered from the IMF World Economic Outlook (WEO) and the World Bank World Development Indicators databases. Table 1 lists the various fiscal-spending dependent variables we used along with some summary statistics. Fiscal spending as a percentage of GDP has varied considerably over the years and across countries with a minimum value of 2.5 percent (Democratic Republic of Congo in 2000) and a maximum value of 65.9 percent (Kuwait in 2020). The average spending is about 30 percent for all countries. High-income economies tend to have a higher average at 38.2 percent relative to low- and middle-income economies at 26.2 percent, confirming the general theme of greater availability of fiscal space for the former.

Dependent Variables and Summary Statistics.

Note: IMF, International Monetary Fund; WEO, World Economic Outlook; WDI, World Development Indicator.

Besides the overall government spending, here we are also interested in the trends in fiscal spending priorities, particularly spending on social welfare. We gathered data on the two prominent and available social welfare expenditure categories of health and education. Expenditures on health became extremely relevant in the context of the global deficiency in healthcare infrastructure exposed during the COVID crisis. Data on education and healthcare spending as a percentage of overall government spending was gathered from the World Bank World Development Indicators. Healthcare as a proportion of overall government expenditures ranged from a low of about 0.6 percent (Cameroon in 2019) to a high of 42 percent (Solomon Islands in 2002). Spending on education as a percentage of total government outlays averaged 15 percent. There was substantial variation across the countries with a minimum of 4.6 percent (Morocco in 2015) and a maximum of 37.5 percent (Ghana in 2012).

The high level of commitment to education within the government budget in Ghana is interesting. The country launched one of the more effective responses to the pandemic. The proactive response was commended for successfully saving lives and limiting economic fallout by the IMF (IMF 2021b). Yet this very commitment to social welfare spending expanded the fiscal deficit and increased the debt-to-GDP ratio from 39 in 2019 to 44 percent in 2021. As a result, Moody’s downgraded Ghana’s sovereign ratings in February 2022 to CAA1, severely limiting access to international capital markets. Ghana protested this downgrade as an “institutionalized bias” against African economies citing its record of good governance and positive investments in social welfare (Landers and Aboneaaj 2022). The African Union supported Ghana’s appeal against the Moody’s downgrade (African Union 2022). This once again brought attention to the issue of whether sovereign credit ratings truly reflected information about the relative risk of default or, by narrowly focusing on fiscal austerity, thwarted the kind of investments that might contribute to long-term growth and improved creditworthiness.

Finally, we also collected data on interest payments on government debt as a percentage of GDP from the World Development Indicators. One of the impacts of rating downgrades is the increase in the cost of borrowing and the burden of repayment. The interest payment data can be a good indicator of this burden. Interest payments as a proportion of total government expenditures averaged 8.9 percent. As expected, the average for high-income economies (6.4 percent) was lower than the average for low- and middle-income economies (10.9 percent).

4.2 Multivariate Model and Results

To explore the impact of credit ratings changes on the various measures of government spending discussed above, we estimated the following baseline regression specification for our panel data:

The dependent variables are government expenditure as a percentage of GDP and the proportion of government spending going toward health and education, with i and t representing the country and year subscripts. The main coefficient of interest is α1, which measures the effect of sovereign rating changes on the various government expenditure variables. Rating changes are reactive to ongoing economic trends, including changes in government spending. There is therefore a problem of endogeneity here since government expenditure and ratings change could likely be simultaneously determined. To address this endogeneity, an instrumental variables approach is adopted. As explained by Reed (2015), lagged values of the endogenous variable and the dependent variable can be used as instruments for such an approach. We followed this recommendation and used the lagged values of rating change and government expenditure variables as instruments for the rating change variable. All the regressions were estimated with a two-stage least squares method.

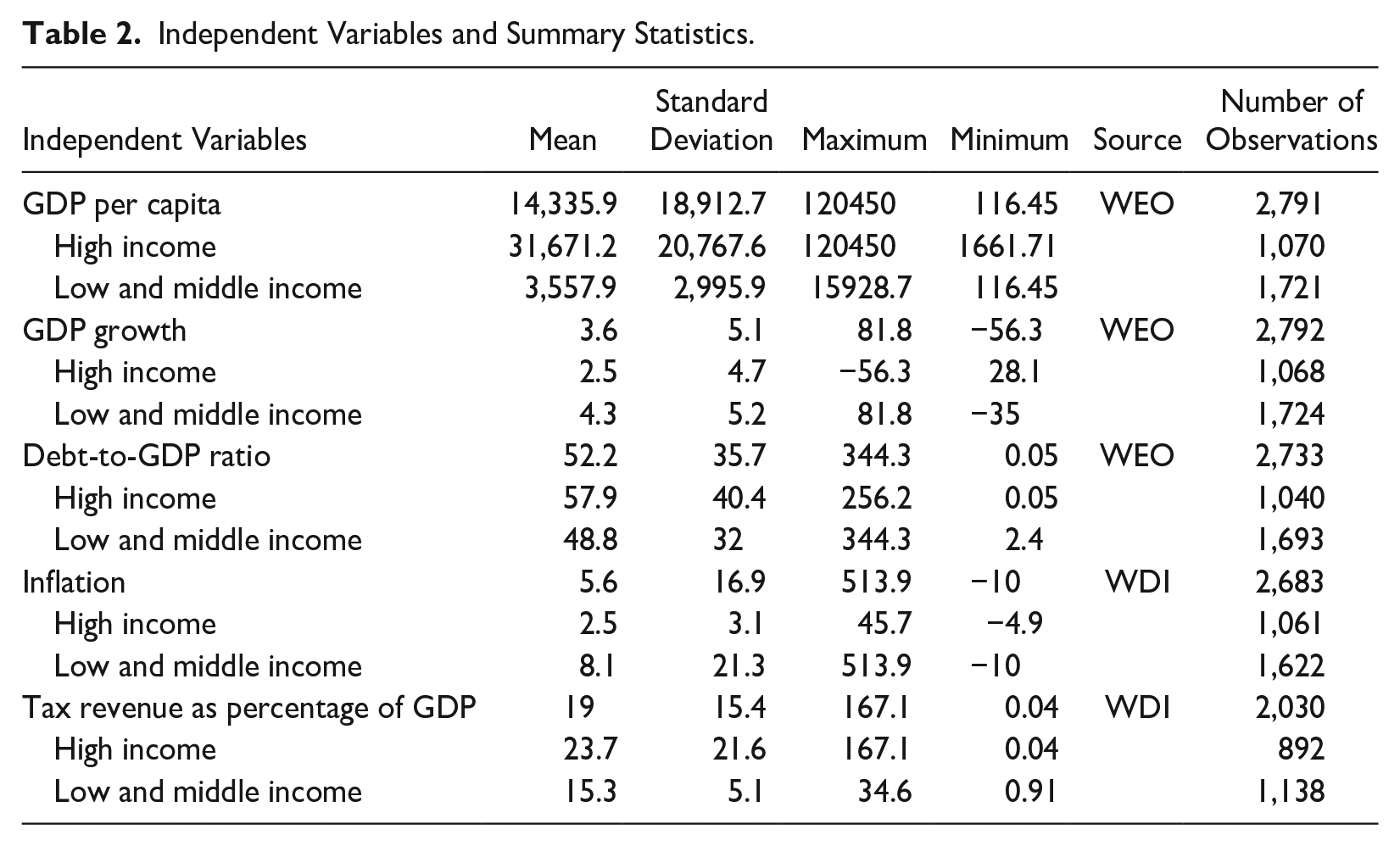

The regression estimations also included other country-level control variables (X it ). The choice of control variables was partly based on variables used in similar literature. For example, GDP per capita is commonly used to control for the vast differences in the sizes of economies (Benmelech and Tzur-Ilan 2020; Balajee, Tomar, and Udupa 2020). GDP growth was also included here to accommodate the differences in economic trajectory across countries. Measures of interest payment on debt and macroeconomic stability have been used in previous empirical work on government spending (Benmelech and Tzur-Ilan 2020). Here we used the interest payment as a percentage of total government expenditure. This was the most widely available variable for the 133 countries in our database. We also used the inflation rate as an indicator of general macroeconomic stability. Finally, we included tax revenue as a percentage of GDP variable as an indicator of governance capacity. All these control variables were gathered from the World Development Indicators. Table 2 presents the summary statistics for the control variables. Since the full panel includes advanced, low, and middle economies, there is considerable variation in GDP per capita from a maximum of $120,450 (Luxembourg) to a minimum of $116 (Ethiopia). Given this wide range and as per prior literature, we used the log of GDP per capita in the regressions.

Independent Variables and Summary Statistics.

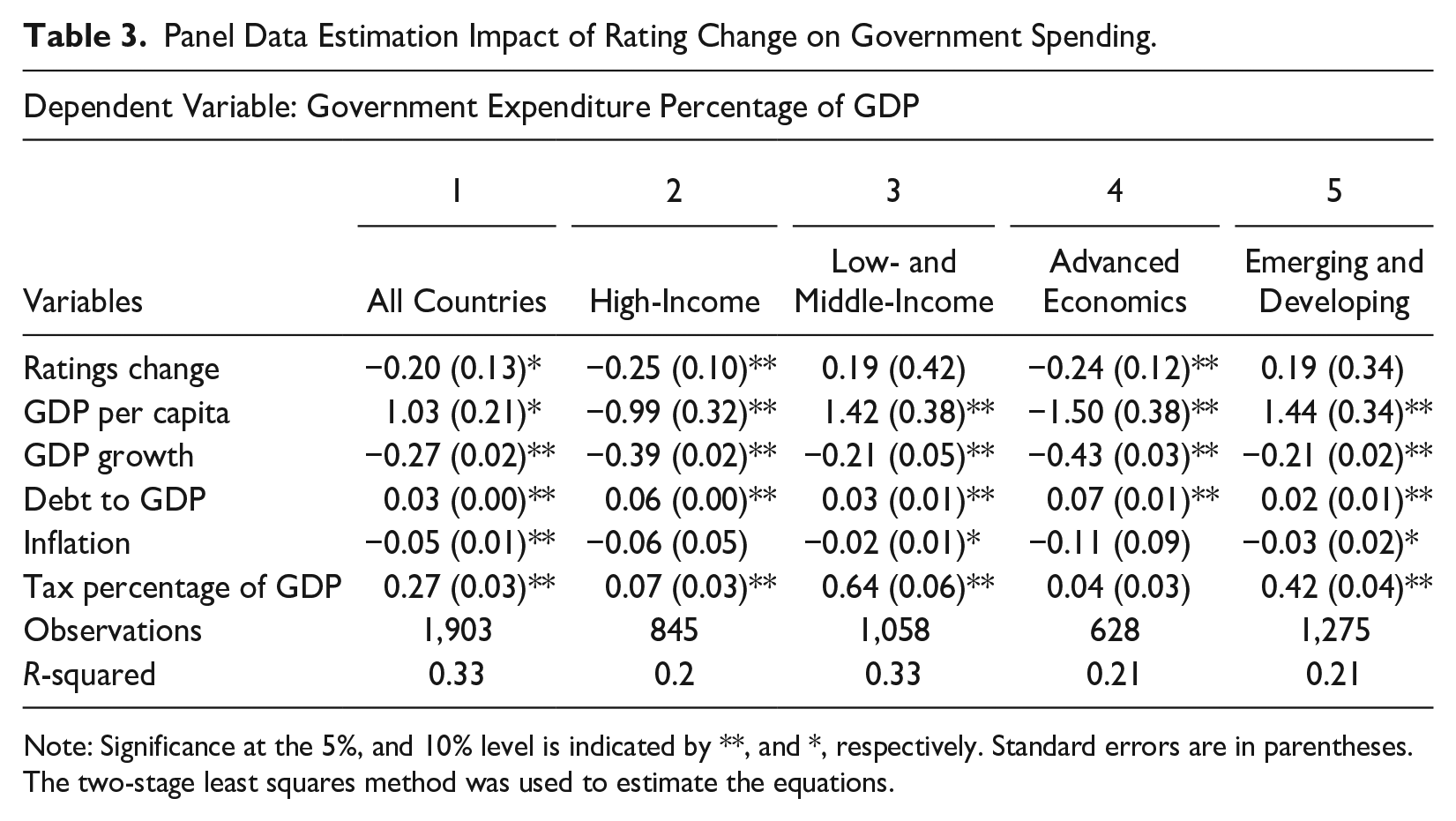

In table 3 we present the results of the various regression specifications with total government expenditure as a percentage of GDP as the dependent variable. All the panel data regressions were estimated using the two-stage least squares method with the lagged values of rating change and the dependent variable as instruments for the rating change variable. In column 1 we see that with all countries included in the panel, ratings did have a statistically significant impact on government spending. However, the direction of impact was negative. That is, a one-unit improvement or positive change in ratings led to a decrease in government expenditure by 0.33 percent in the next year. This would imply that rating downgrades or negative changes would support expanded government expenditure. However, in columns 2 and 3, when we ran separate estimations for the high-income group and the low- and middle-income group, we see that this pattern held only for the high-income group. In column 3, we found that changes in ratings did not have a statistically significant impact on government spending in low- and middle-income economies.

Panel Data Estimation Impact of Rating Change on Government Spending.

Note: Significance at the 5%, and 10% level is indicated by **, and *, respectively. Standard errors are in parentheses. The two-stage least squares method was used to estimate the equations.

To test for the robustness of the results, we also estimated the regression using different groupings of countries. In columns 4 and 5, we used the IMF WEO classification to group countries into two categories: advanced economies and emerging markets and developing economies. Under this classification, advanced economies consisted of a group of 33 countries. The results are similar. It is only for advanced economies that we see a statistically significant and negative impact of rating changes on government spending.

As for the other coefficients, per capita GDP was positive and statistically significant when all countries were combined in the regression model and for the model with only the low- and middle-income countries. However, we see some nonlinearity in the impact, with the GDP per capita coefficient being negative for high-income economies. GDP growth had a negative impact on government expenditures in all the specifications. The coefficients for the other control variables were as expected. Inflation and interest rates both had negative coefficients, indicating the negative impact of macroeconomic instability, and the high cost of borrowing. Tax revenue and debt-to-GDP ratio had positive coefficients as expected since both would be expected to support higher levels of government expenditure.

While the above findings on the impact of rating changes on overall government expenditures are inconclusive, here we are also interested in looking at whether rating changes influenced government spending priorities, particularly the proportions of social welfare spending.

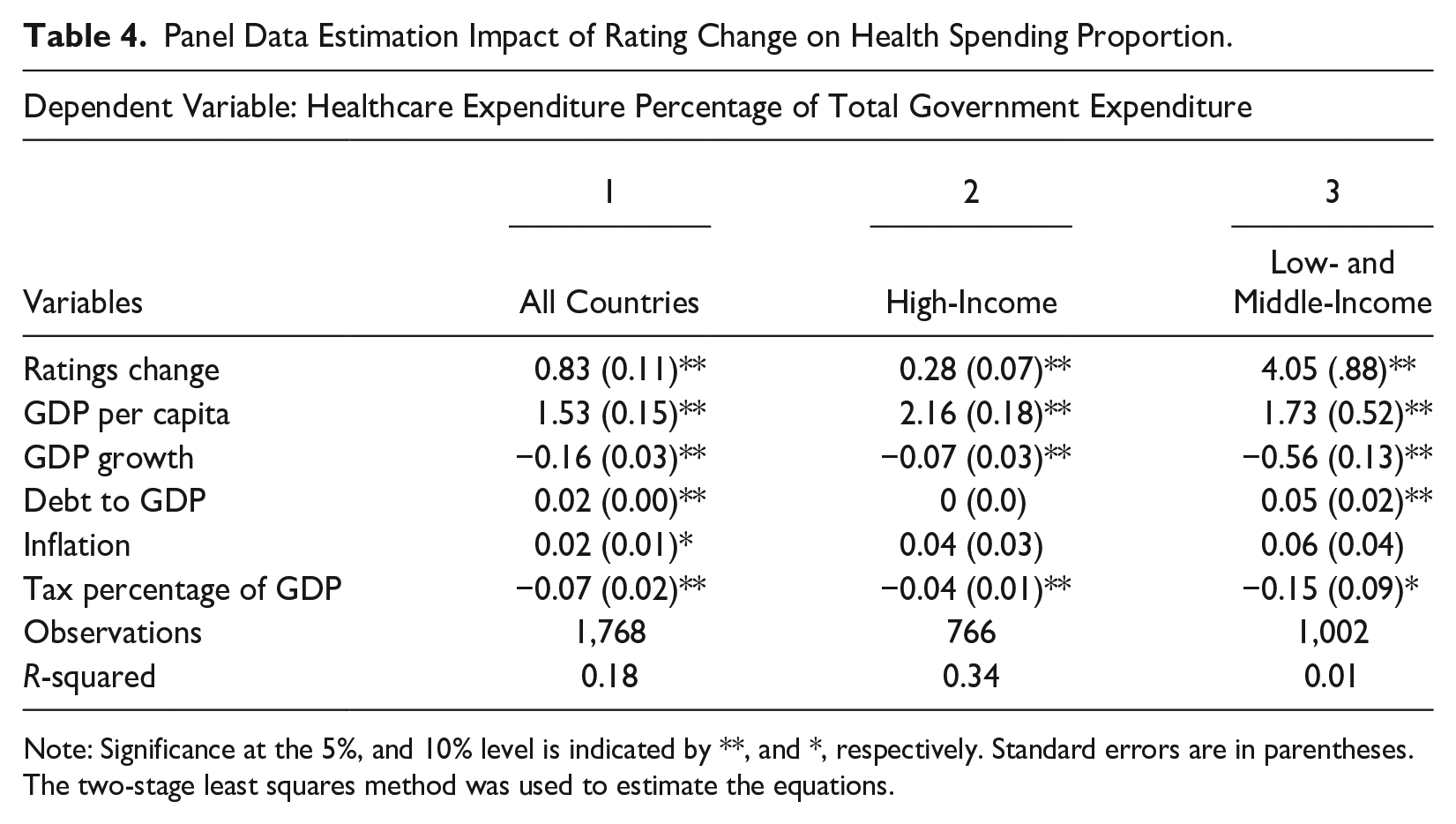

We turn next to government expenditures targeted toward health and education. In table 4, we examined the impact of ratings change on health spending as a percentage of total government expenditures. Once again, we used the instrumental variables approach for the rating change variable and estimated the regressions with a two-stage least-squares approach. Here we are looking at the shifting priorities in the government budget. In columns 1–3 in table 4, we found a statistically significant positive impact of rating change on healthcare as a percentage of government expenditures for all country groups. That is, upgrades supported a higher proportion of healthcare spending, whereas downgrades or negative rating changes led to a lower proportion of healthcare spending.

Panel Data Estimation Impact of Rating Change on Health Spending Proportion.

Note: Significance at the 5%, and 10% level is indicated by **, and *, respectively. Standard errors are in parentheses. The two-stage least squares method was used to estimate the equations.

The above findings underscored the worry that sovereign credit ratings impose constraints that deflect from long-term development priorities. Ratings downgrades did show a tendency to negatively impact healthcare spending over the long term. This impact is most pronounced for the low- and middle-income group of countries. In column 3, we see that a 1-unit increase in ratings would lead to a 4.05-unit increase in healthcare spending as a percentage of GDP. This would imply that downgrades have the potential to reduce health spending in the overall budget substantially.

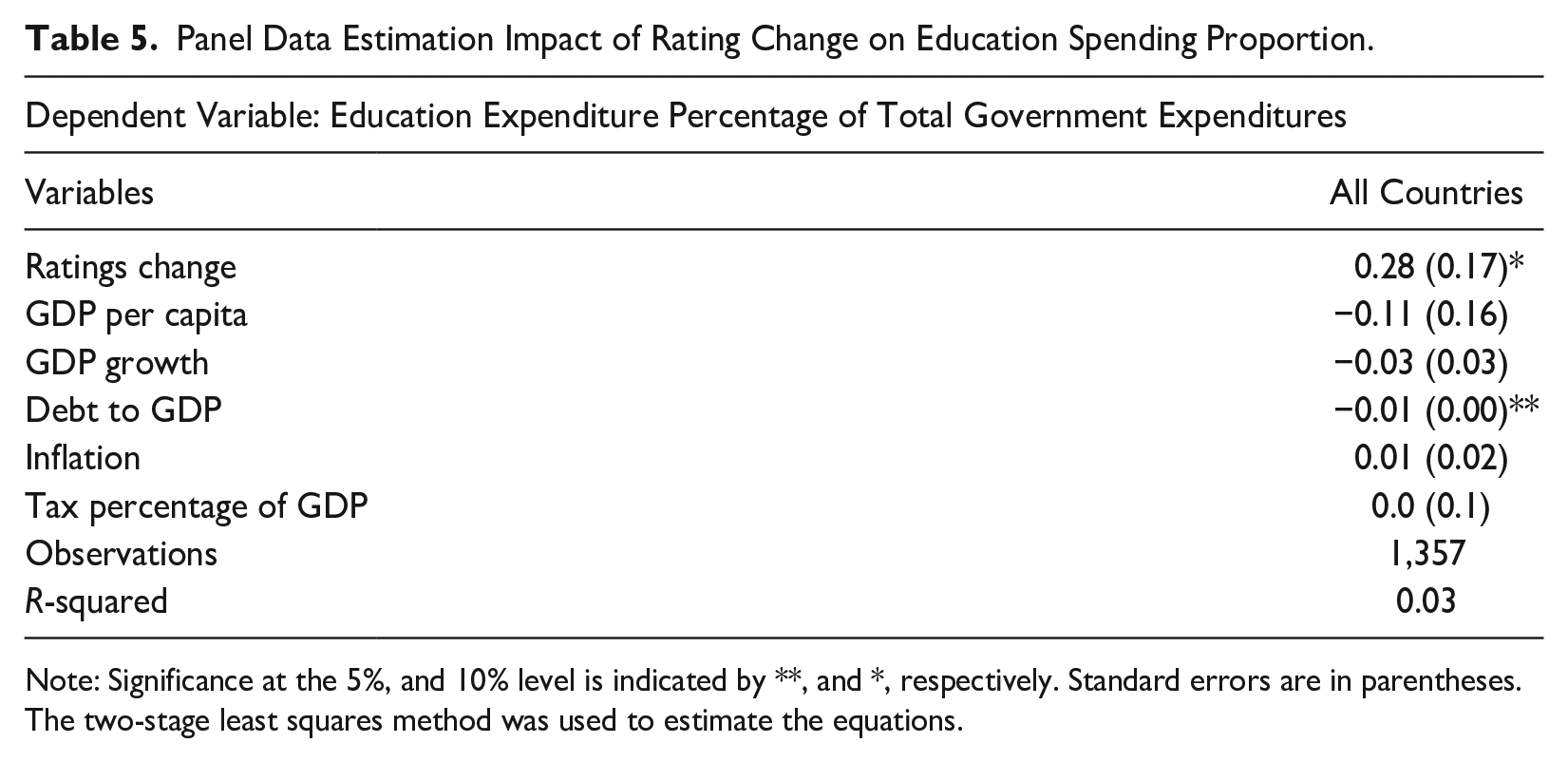

In table 5 we explored the impact of rating change on education expenditures as a proportion of total government expenditures. Here again, we see that rating change does have a statistically significant effect. Ratings upgrades led to a higher proportion of spending on education, whereas downgrades reduced the percentage of spending on education.

Panel Data Estimation Impact of Rating Change on Education Spending Proportion.

Note: Significance at the 5%, and 10% level is indicated by **, and *, respectively. Standard errors are in parentheses. The two-stage least squares method was used to estimate the equations.

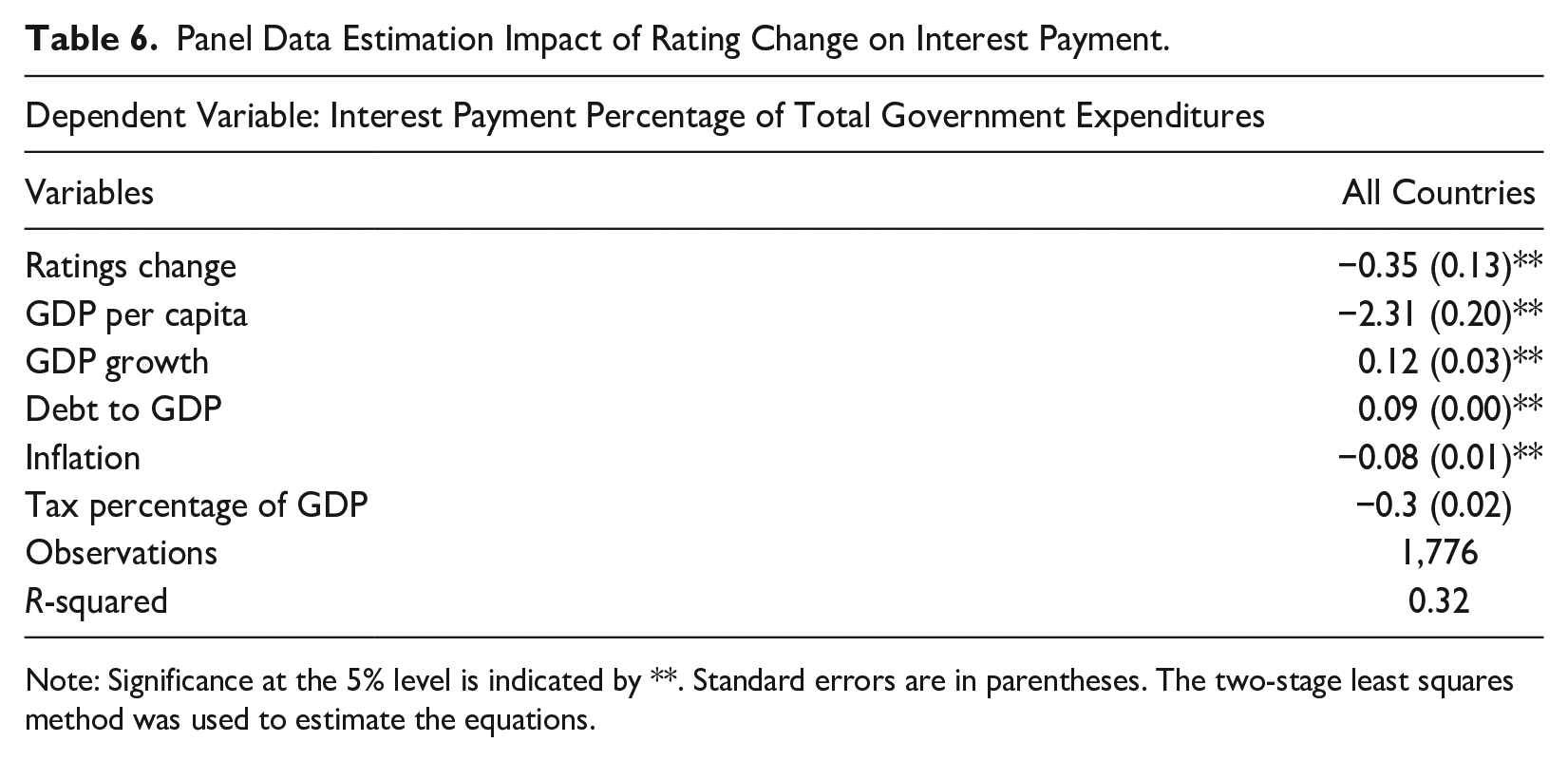

Next, we look at the impact of rating changes on interest payments as a proportion of total government expenditures. In table 6, we see that rating changes have had a negative impact on interest payments. A 1-unit upgrade in rating led to a 0.35-unit decline in the interest payments as a proportion of the total government budget. Downgrades then increased the proportion of interest payments. This points to the dual negative impact of downgrades. This finding is to be expected since downgrades increase the cost of borrowing for countries now perceived to be less creditworthy. At the same time, they also reinforce the move away from social welfare priorities in the fiscal space, as debt repayment becomes the primary focus.

Panel Data Estimation Impact of Rating Change on Interest Payment.

Note: Significance at the 5% level is indicated by **. Standard errors are in parentheses. The two-stage least squares method was used to estimate the equations.

To summarize, in this empirical analysis we did find some evidence for the potential long-term impact of sovereign ratings changes on fiscal spending trends, particularly spending on social welfare expenditures such as healthcare and education. While the crisis-related impact of rating changes during the pandemic was more pronounced, ratings changes in the preceding decades did impact advanced versus developing economies differently. The former group was more likely to withstand negative rating changes and continue spending on fiscal priorities. Overall, all economies showed signs of a shift in spending priorities due to changes in the ratings. The share of social welfare expenditures diminished as ratings declined and the share of interest payments expanded. The overall trajectory of sovereign rating changes has become more volatile particularly for developing economies only since 2010. Given this, these results suggest that the impact of the trend of procyclical ratings on fiscal priorities particularly in the postpandemic era might intensify for developing economies. In the following section, we explore components of a typical sovereign rating methodology.

5. The Sovereign Ratings Environment and Methodology

The sovereign credit rating ecosystem is dominated by three large agencies: S&P Global, Moody’s, and Fitch. Commonly known as the Big 3, they control nearly 90 percent of the ratings market. While the three agencies have different published rating methodologies, there is considerable overlap and alignment in the broad categories and indicators used. As such the ratings applied have more or less converged, with average ratings being largely similar for the three agencies (Griffith-Jones and Kraemer 2021). The methodology typically involved both quantitative and qualitative assessment within five broad categories—economic strength and stability, fiscal outlook, monetary outlook, governance and institutional strength, and external accounts. For each category, a range of quantitative indicators, with differing weights, are used to create a baseline cumulative score. Countries accumulated weighted scores based on selected indicators for each category, with higher scores leading to higher ratings. These baseline scores are then adjusted based on the assessment and judgment of the rating analysts. This is also known as the qualitative overlay. The ratings therefore are a combination of published quantitative indicators, and less transparent adjustment and weighting factors. Together they are meant to reflect default risk, based on a country’s economic performance and management.

While there is considerable debate over the lack of transparency in the qualitative overlays, particularly in the case of developing economies, even the quantitative indicators provide inherent advantages to advanced economies. For example, the quantitative measures for economic strength prioritize the size and scope of economic activity. GDP and GDP per capita (and share in world GDP according to the Fitch ratings criterion (Fitch 2022) are predominantly used as indicators of the size and scope of an economy. Larger economies automatically accumulate higher scores based on GDP size, irrespective of their performance or outlook. Smaller countries and developing economies experience a shortfall in scores for this size category irrespective of their economic performance. Moreover, the qualitative overlay for the economic strength criterion tends to recommend lowering scores for less economically diversified smaller economies. So smaller economies, dependent on exports of a few products or primarily commodities, receive lower scores (Moody’s Investors Services 2019). This criterion would largely impact developing economies negatively, reinforcing their disadvantage.

Such automatic differences between the potential scores of developed and developing economies in effect reproduce the dominant financial position of the former in a way that parallels the arguments made in the financial subordination literature. While both developed and developing economies need to access financial markets to manage fiscal policy imperatives, the lack of similar starting points in credit rating scores ensures that developing economies remain in subordinate status, with limited access to credit. It is not only the economic strength category that accounts for such biases in the score accumulation. Several other aspects of financial subordination are directly incorporated into the rating framework.

For example, for the fiscal outlook score category, economies receive upgraded overlay scores if their currency is considered a reserve currency. As discussed in the literature review, the currency hierarchy is a key asymmetry in the global financial system that is highlighted in the financial subordination literature. Only the US dollar and currencies from other advanced economies are considered part of the reserve currency basket. Here we see that this currency hierarchy is directly incorporated into the credit rating framework. Besides fiscal outlook scores, countries with designated reserve currencies also receive positive qualitative adjustments to the external accounts category of the credit score calculation. Since only developed economies have designated reserve currencies, such positive adjustments to the different scoring categories are only available to them. Besides such qualitative adjustments, reserve currency countries also benefit from the higher scores given to countries with a lower proportion of foreign currency debt in the external accounts category of scoring. As has been shown in the financial subordination literature, nonreserve currency economies’ attempts to reduce foreign currency borrowings have been hampered by increased capital volatility, particularly during crisis periods (Kaltenbrunner and Painceira 2018; Bertaut, Bruno, and Shin 2021). Finally, overall debt to GDP is also given a lower weight for reserve currency countries compared to developing economies in the Moody’s ratings methodology. Instead, interest payments as a percentage of GDP receive greater weighting, allowing advanced, reserve currency economies to accumulate higher levels of debt-to-GDP ratios without facing negative rating actions.

These inherent biases in favor of advanced economies, stemming from their dominant position in the global financial hierarchy, create a permanent ceiling for the rating aspirations of developing economies. While they are prescribed plans of fiscal consolidation to achieve higher scores, the disadvantages of size and the lower currency status will continue to prevent ascension in the rating ladder beyond a certain limit. On the other hand, the rating head start affords advanced economies greater fiscal space, allowing for expanded countercyclical policies and faster recoveries, thereby reproducing the advantages of economic size and currency privilege as described in the financial subordination literature.

While advanced economies continue to secure higher scores based on size and currency advantage, there is also no mechanism for developing economies to gain additional points for investments in economic or social welfare infrastructure that can generate long-term positive spillovers. For the fiscal outlook score, debt-to-GDP ratio and debt burden indicators such as the ratio of interest payments to GDP and interest payments to revenues are used. Positive adjustments to the qualitative overlays are primarily based on announcements of fiscal contraction or the ability to cut government expenditures. No distinctions are made between different kinds of fiscal expenditures. For example, infrastructure investments or welfare expenditures with the potential to create positive human capital spillovers for the economy would also be viewed negatively as a fiscal expansion.

Ratings therefore necessarily impose a short-term fiscal horizon on them by making long-term development financing prohibitively expensive through the threat of negative actions. Rating agencies claim that the so-called long-term ratings they issue take note of information, particularly on growth and growth prospects, over a longer time horizon. In practice such a timeline is considerably short, ranging from 5 to 10 years depending on rating grade (shorter for lower grades and longer for the higher grades). This timeline is supposed to reflect credit risk through one economic cycle. But as has been pointed out (Kraemer 2021; Griffith-Jones and Kraemer 2021), this one-cycle calculation is insufficient and myopic. Development priorities like health and education necessarily need a longer time horizon beyond one economic cycle. The positive spillovers of such investments are unlikely to be realized and therefore are unlikely to be incorporated into the ratings outlook within the span of one economic cycle. Since such expenditures are penalized in the short-term rating calculations, the potential for such long-term spillovers is curtailed.

Finally, the uncompetitive environment of the ratings industry is in itself a reflection of ongoing financial subordination. The dominance of the big three ratings agencies, with formidable barriers to entry, concentrates the power of ratings decision making in the hands of private actors located primarily in a few advanced economies. Moreover, as noted in the report of the UN independent expert on debt and human rights (UNHCR 2021), there is considerable conflict of interest in the ratings industry since the primary stream of profits for these private agencies are the fees from the very institutions and countries they rate. Given their location in the advanced economies, primarily in the United States, and that a large proportion of the (nonsovereign) institutions they rate are in advanced economies, agencies are more susceptible to pressure from regulators in advanced economies. As some have argued, they are less likely to initiate negative actions for fear of retaliation by regulatory authorities, particularly in the United States and other advanced economies. They would have less to fear from similar pressure from regulators in developing economies since their profits are less dependent on them. Moreover, the lack of a global monitoring or regulating mechanism implies that countries do not have formal recourse to appeal against ratings or to ask for transparency or clarifications. The power of the ratings agencies in the case of developing economies is therefore formidable and should be incorporated into financial subordination analysis.

6. Conclusion

In this article, we explored the impact of sovereign credit rating and rating methodology on fiscal space in advanced and developing economies. The current rating methodologies confer substantial advantages to advanced economies while handicapping developing economies and tend to impose limitations to accessing long-term development financing for the former. In the empirical analysis, we found that the intensity of negative ratings for developing economies has increased since 2011. We also found that negative actions tended to influence fiscal priorities away from health and education expenditures over the long term. This follows from the credit ratings methodologies’ disproportionate emphasis on fiscal prudence, particularly in developing economies and the tendency to penalize any expansion of fiscal space even if it is for vital human development investments.

We further explored the biases in the sovereign ratings methodology using the framework of the financial subordination literature. Beyond an emphasis on fiscal prudence, biases inherent in the rating methodology can be traced to the subordinate position of developing economies in the global financial system. The ratings methodologies in turn reinforce advantages that reproduce such subordination. While ratings are supposed to reflect default risk and countries are expected to lower that risk by fiscal consolidation, the inherent biases in the methodology create a natural ceiling for developing economies irrespective of their overall economic performance. As such the current sovereign credit rating methodologies have created a new channel for reproducing and deepening inequalities in the global financial system.

Several suggestions for reform to the rating system have already been offered by various practitioners and scholars. More transparency particularly in the qualitative overlay has often been recommended. The UN expert report (UNHRC 2021) recommended incorporating social and human development indicators into the rating criterion. The report specifically underscores that incorporating such indicators would allow the positive spillover effects of human capital development on long-term economic growth to be captured. There are also suggestions to develop more long-term ratings that reflect information beyond the one economic cycle approach and allow countries room for long-term development financing options. This suggestion has taken on urgency in the context of the looming climate crisis. Developing economies, particularly smaller island nations who are often at the frontlines of crisis will increasingly require fiscal space and credit to finance climate mitigation and coping strategies.

Beyond these changes to the methodology, the discussion of financial subordination in this article also points to the critical need for more structural changes in the rating industry. The unchecked power of the private ratings agency located in advanced economies needs to be addressed. Effective regulatory oversight can only be successful when there is a change in this oligopolistic concentration. Moreover, such regulatory oversight needs to be more multilateral in nature to address the conflict-of-interest issues arising from the location of rating agencies. One potential way to create more competition in the rating industry and have broader multilateral inputs into the rating process is the proposal for regional public credit rating agencies suggested by the African Union’s African Peer Review Mechanism (African Union 2020). Though garnering trust and buy-in for such regional agencies from international investors can be challenging. Another significant reform would be the establishment of a global public credit rating agency at the United Nations or other multilateral forum. Developing countries should prioritize building political momentum toward establishing such an agency as part of fundamental, systemic reforms to ensure the availability of fiscal space to shape economic recovery and development. Similarly, discussions of systemic inequalities in the global financial system must take into account the power of the credit ratings framework in sustaining the subordinate financial position of the Global South.

Footnotes

Appendix

Full List of Countries.

| High-Income Countries | Low- and Middle-Income Countries |

| Australia Austria Bahamas Bahrain Barbados Belgium Canada Chile Croatia Cyprus Czech Denmark Finland France Germany Greece Hong Kong Hungary Iceland Israel Italy Japan Republic of Korea Kuwait Latvia Lithuania Luxembourg Macao Malta Mauritius Netherlands New Zealand Norway Oman Panama Poland Portugal Qatar Romania Saudi Arabia Singapore Slovakia Slovenia Spain Sweden Trinidad and Tobago United States United Arab Emirates United Kingdom Uruguay |

Albania Angola Argentina Armenia Azerbaijan Bahamas Bahrain Bangladesh Barbados Belarus Belize Benin Bolivia Bosnia Herzegovina Botswana Brazil Bulgaria Cambodia Cameroon China Colombia Costa Rica Cote D’Ivoire Democratic Republic of The Congo Dominican Republic Ecuador Egypt El Salvador Ethiopia Fiji Gabon Georgia Ghana Guatemala Honduras India Indonesia Iran Iraq Ireland Jamaica Jordan Kazakhstan Kenya Kyrgyz Republic Laos Lebanon Malaysia Maldives Mali Mexico Moldova Mongolia Morocco Mozambique Namibia Nicaragua Niger Nigeria Pakistan Papua New Guinea Paraguay Peru Philippines Russia Rwanda Senegal Serbia Solomon Islands South Africa Sri Lanka St. Vincent and the Grenadines Suriname Tajikistan Tanzania Thailand Togo Tunisia Turkey Turkmenistan Uganda Ukraine Uzbekistan Venezuela Vietnam Zambia |

Acknowledgements

This article benefited substantially from the feedback received from reviewers Dr. Elif Karaçimen and Dr. Annina Kaltenbrunner and the managing editor Dr. Enid Arvidson.

Data Availability Statement

The data that support the findings of this study are available from the author upon request.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.