Abstract

This study is a pioneering attempt to investigate the impact of foreign direct investment (FDI) on export performance in Pakistan by using the long annual time series data from the period 1974–2012 and by using more rigorous econometric techniques. Autoregressive distributed lag-bound testing cointegration approach confirms the valid long-run relationship between considered variables. Results indicate the significant positive impact of FDI on real exports in long run as well as in short run. Results of Granger causality test, Toda and Yamamoto Modified Wald causality test and variance decomposition test confirm the bidirectional causal relationship between FDI and export performance in Pakistan. Results of rolling window analysis suggest that the coefficient of FDI in export model remains negative from 1983 to 1987, from 2001 to 2006 and in 2011. The coefficient of FDI in export model shows a positive coefficient in remaining years. It can be seen that FDI and real export are connected in complementary way in Pakistan. The policy makers should make policies that favour foreign investors so as to attract more FDI in Pakistan. It has been observed that a stable political and economic environment is desirable to attract more FDI in Pakistan.

Introduction

Significance of foreign direct investment (FDI) in developing countries has widely been discussed in the literature of international economics. Foreign direct investment is considered as a major source to promote growth-enhancing activities by supplying advanced technologies, trade expansion, employment opportunities and incorporation of global markets. In contrast, it is opposed because it is expected to create balance of payment problems, allowing exploitation of the host country’s market and shrinking capability of host country to manage its economy.

Foreign direct investment may be substitute or complement of aggregate exports of host country. When, for instance, FDI involves producing products in host country’s domestic markets that were previously producing domestic investor, the FDI and aggregate exports are expected to be substitute. This type of FDI is called horizontal FDI. On the other hand, if FDI contributes directly to the host country’s efforts for supplying output in international markets, the FDI and aggregate exports are expected to be complementary. This type of FDI is called vertical FDI. However, it should be evident that it is no easier to establish a priori the association between FDI and host country’s exports. The inquiry of the connection between FDI and exports can be resolved only by looking at the empirical investigation for particular country.

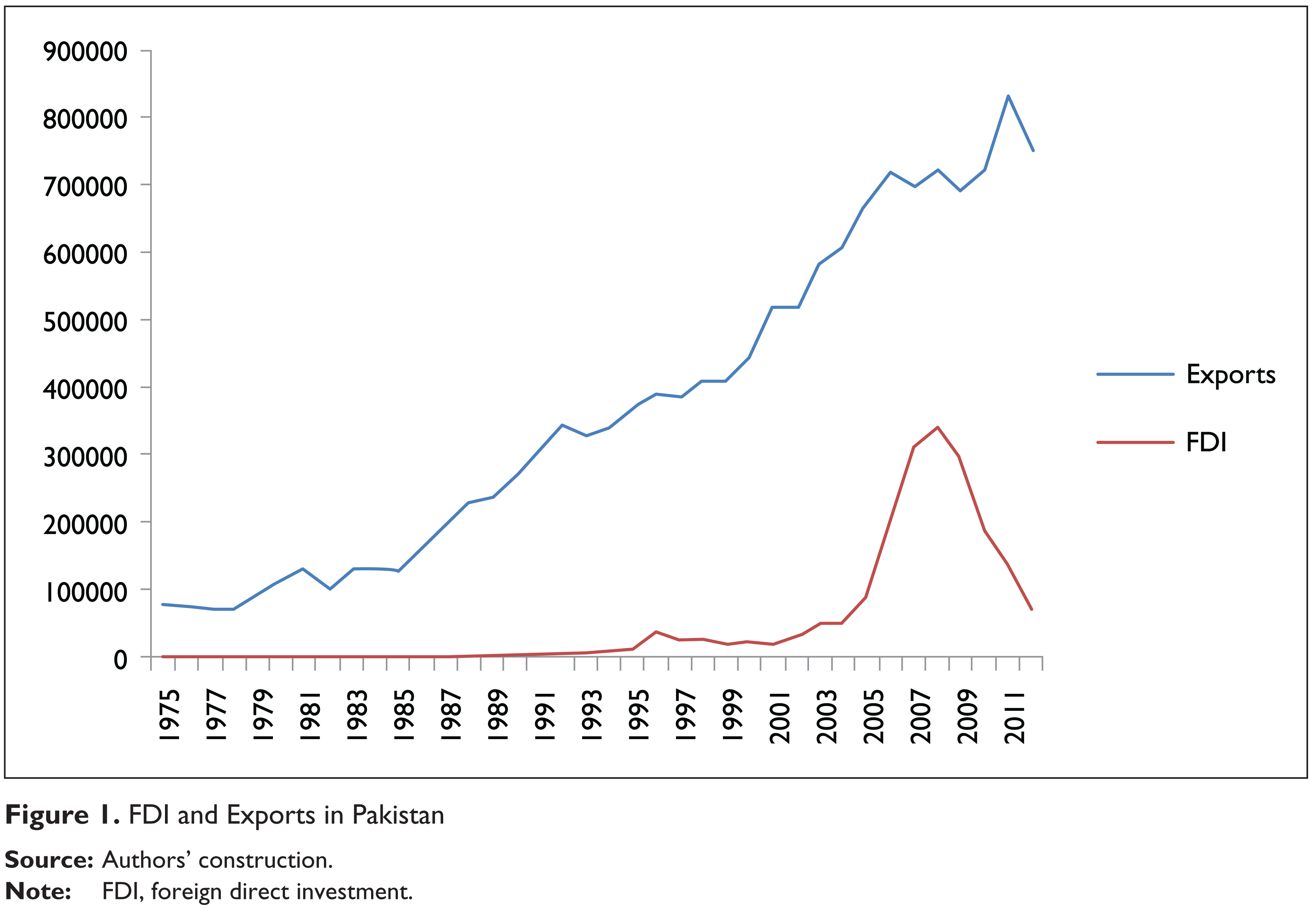

From Figure 1, we can see that in 1970s and 1980s both FDI and exports are increasing at different rates. From 1996 to 2002, FDI is decreasing while, simultaneously, export is increasing. After 2003, FDI is increasing drastically and increase in export is regular. After 2008, FDI is decreasing again but export is improving. Figure 1 has no clear indication about the relationship of FDI and export performance in Pakistan. Pakistan is the second largest country of the South Asia in terms of population. Therefore, it is an ideal economy for the multinational firms to start their operations to supply their products to a large populated country. Pakistan has made brisk progress in macroeconomic performance with the help of inward FDI especially in 1980s and 1990s. In last two decades, trade liberalization, incentives to attract FDI and market reforms were employed in various sectors to reduce restrictions on FDI and develop the scope of FDI in different sectors of the economy. The question is whether FDI is correlated with aggregate exports in Pakistan. This study examines this question using long time series annual data of Pakistan covering the period from 1974 to 2012 and by applying more rigorous econometric techniques. This research will provide some policy implications related to FDI–export nexus for developing economies like Pakistan.

The rest of the paper is organized as follows: the next section reviews some theoretical and empirical literature on the relationship between FDI and exports. Thereafter, we discuss the modeling framework. After that, the estimation and results relating to stability of long-run model, the causal relationship between FDI and export performance and rolling window estimations are shown. Lastly, we conclude the study and provide some policy recommendation.

Review of Literature

Numerous literatures discuss the relationship between FDI and export performance. In this section, some theoretical and empirical literatures have been reviewed.

Theoretical Underpinning

Foreign direct investment plays an imperative role to boost the export performance of economies (Blake & Pain, 1994; Culem, 1988; Davaakhuu, Sharma & Bandara, 2014; Jiang, Liping & Sharma, 2013; Ozawa, 1992; Pain & Wakelin, 1998; Shahbaz & Rahman, 2012; Sun, 2001). It provides competent and modern methods of production which boost domestic output, enhance quality of production and also help to penetrate the export market and launch new products for exports. Foreign direct investment also promotes the growth in human capital formation by facilitating training and knowledge sharing. All these quality and production enhancement activities lead to enhanced export performance. Host countries also get competitive and comparative advantage in international markets (Cabral, 1995; Haddad & Harrison, 1993; Jawaid & Raza, 2015, Leichenko & Erickson, 1997; Ruggiero, 1996; Sun, 2001; Yilmaz, Cooke & Dellios, 2008; Zhang, 2009).

Empirical Evidence

Conversely, FDI has some negative effects on host country’s exports by substituting domestic investment. Absorption of new technologies is not easy because of shortage of human capital, particularly for developing economies. At the same time, if domestic market of host countries is in target of FDI, export performance of host countries will decrease. Foreign direct investment also affects the performance of the potential exporters of host countries. Inattention of host country’s comparative advantage is also one the reason of negative effect of FDI on exports of host country (Zhang, 2009).

Numbers of studies have been undertaken on the relationship between FDI and export. Most of the studies show positive relationship between FDI and export. In contrast, some studies indicate negative association between FDI and exports. In this section, some selected studies have been reviewed.

Mundell (1957) and Svensson (1996) discussed negative effect of FDI on exports. On the other hand, Lipsey and Weiss (1981), Helpman (1984) and Grossman and Helpman (1989) highlighted the positive effect of FDI on international trade. The role of MNCs in exports of manufactured goods has been examined by Hood and Young (1979) in 1960s. Findings indicated that MNCs assist host countries in the expansion of exports in less developed countries. However, this capability of the MNCs is comparatively small than in developed countries.

Kojima (1985) scrutinized the difference between Japanese and American FDI in four ASEAN countries, namely, Indonesia, the Philippines, Malaysia and Thailand and four newly industrialized countries, namely, Taiwan, Korea, Hong Kong and Singapore. Results showed that Japanese FDI is trade oriented while American FDI is relatively anti-trade oriented. Chou (1988) re-examined Kojima’s (1985) work on American and Japanese types of FDI in Taiwan and found that both types of FDI have a positive effect on exports.

Leichenko and Erickson (1997) examined the relationship between FDI and export performance at US-states’ level from 1980 to 1991. Results showed that FDI has positive effect on future state manufacturing export performance. By employing gravity model on the period from 1982 to 1994, Hejazi and Safarian (2001) examined the relationship between FDI and international trade between USA and 51 economies. Findings suggested positive relationship between FDI and US export performance.

Liu, Burridge and Sinclair (2002) found bidirectional causal relationship between FDI and exports in China by using quarterly data from 1981 to 1997. Sharma (2003) examined the effect of FDI on India’s exports by employing annual data from 1970 to 1998. Result showed insignificant relationship between FDI and exports. In contrast, O’Sullivan (1993) in Ireland and for UK, Blake and Pain (1994) have found that FDI and host country exports are complementary.

Cross-country studies highlight that effect of FDI on host country’s exports possibly vary by industry, country or region. Pain and Wakelin (1998) analyzed the impact of FDI on exports performance considering panel data of 10 of 11 OECD countries. Results indicated significant positive effect of FDI on the export performance in seven countries. On the other hand, in three countries (Japan, Italy and Denmark), FDI decreased export performance. In addition, inspecting the role of FDI on China’s regional exports from 1984 to 1997, Sun (2001) found that FDI is more effective in coastal region than in interior ones.

Alici and Ucal (2003) analyzed the causal relationship between inward FDI, export and economic growth in Turkey by using quarterly data from 1987 to 2002. Foreign direct investment-led export growth was not observed in Turkey. By using the data of Brazil, Canada, Chile, Mexico and USA, Ekanayake, Richard and Veeramacheneni (2003) examined the causal relationship between FDI and exports from 1960 to 2001. Results highlighted bidirectional causal relationship in USA, and unidirectional causality run from exports to FDI was found in Brazil and Mexico.

In three Middle Eastern countries namely Egypt, Jordan and Oman, Metwally (2004) investigated the relationship between FDI, exports and economic growth by using the data from 1981 to 2000. Simultaneous equation model indicated FDI significantly influenced exports of goods and services in these countries. Pacheco-Lopez (2005) analyzed the causal relationship between FDI and exports in Mexico. Granger causality test indicated two-way causality between FDI and exports.

Vuksic (2005) scrutinized the role of FDI in export performance in the Croatian economy. Panel data of 21 manufacturing sectors from 1996 to 2002 were used. Results of fixed effect model indicated significant positive effect of FDI on exports. Yousuf, Hussain and Ahmad (2008) also empirically investigated the effect of FDI on import and export in Pakistan utilizing annual time series data of 32 years, that is, from 1973 to 2004. Results of Johansen–Juselius cointegration and error correction model specified the positive impact of FDI on export in the long run while negative association was found in the short run.

Majeed and Ahmed (2007) examined the relationship between FDI and export by using 15 years data of 49 countries (both developed and developing). Three-stage least square method to the fixed effect model was used. Results indicated that FDI had significant positive effect on export performance in selected countries. It suggested that developing countries can attract FDI by eradicating the artificial barriers and control on export.

Undertaking cross-country analysis, Nourzad (2008) explored the impact of FDI at macro-level efficiency by considering annual data from 1981 to 2001 of 46 developed and emerging countries. Results from stochastic production frontier (SPF) and regression model indicated that increase in FDI increased potential output in both developed and developing countries. By considering 16 African countries, Hailu (2010) examined the relationship between FDI and trade from 1980 to 2007. Results showed significant positive effect of FDI on trade. It was suggested that expansion of FDI is beneficial for export promotion in selected countries. Kiran (2010) scrutinized the causal relationship between FDI and trade in Turkey by using quarterly data from 1992 to 2008. Results suggested no causal relationship between FDI and trade. Prasanna (2010) found significant contribution of FDI in promoting exports in India.

Ahmadi and Ghanbarzadeh (2011) and Attari et al. (2011) found bidirectional causal relationship between FDI and export in 16 MENA countries and Pakistan, respectively. Chansomphou and Ichihashi (2011) examined the effect of FDI on export performance of Lao PDR by using the data from 1981 to 2008. Results suggested significant positive long-run relationship between FDI and exports. Tabassum, Nazeer and Siddiqui (2012) scrutinized the relationship between FDI and export in Pakistan by the data from 1973 to 2009. Cointegration and error correction model showed insignificant relationship between FDI and exports in long run as well as in short run.

After reviewing above literature we observe that the potential link of FDI and exporting is too ambiguous to draw any conclusion and vary across the country’s economic condition. The present econometric analysis is, therefore, directed to investigate the impact of FDI in the case of Pakistan to evaluate the contribution of FDI in export performance of the country.

Empirical Framework

In this study, 39 years long annual time series data of Pakistan have been used from 1974 to 2012. Data of real exports, FDI, relative price and real gross domestic product (GDP) are gathered from several issues of economic survey of Pakistan. All variables are used in logarithm form. Augmented Dickey–Fuller (ADF) (Dickey & Fuller, 1979) and Phillips–Perron (PP) (Phillips & Perron, 1988) unit root test are used to examine the stationary properties for long-run relationship of considered variables. The present study employs the autoregressive distributed lag (ARDL) technique to analyze the long-run relationship between FDI and export performance in Pakistan.

The ARDL method of cointegration developed by Pesaran and Pesaran (1997), Pesaran and Shin (1999) and Pesaran, Shin and Smith (2000, 2001) has been used with the help of unrestricted vector error correction model to investigate the long-run relationship between FDI and exports. The ARDL approach has several advantages upon other cointegration methods. ARDL approach may applies irrespective of the of whether underlying variables are purely I(0), I(1) or mutually cointegrated (Pesaran & Shin, 1999). ARDL approach has estimated better small sample properties (Haug, 2002). In ARDL procedure, the estimations of results is even possible if the explanatory variable are endogenous (Pesaran & Shin, 1999; Pesaran, Shin & Smith, 2001). The ARDL model is developed for estimations as follows:

where ψ0 is constant and μit is white noise error term, the error correction dynamics is denoted by summation sign while the second part of the equation corresponds to long run relationship. Schwarz Bayesian Criteria (SBC) has been used to identify the optimum lag of model and each series. In ARDL model we first estimate the F-statistics value by using the appropriate ARDL models. Secondly, the Wald (F-statistics) test is used to investigate the long run relationship among the series. The null hypothesis of the cointegration is (H0 = γ1 = γ2 = γ3 = γ4 = 0). The null hypothesis of no cointegration is rejected if the calculated F-test statistics exceeds the upper critical bound (UCB) value. The results are said to be inconclusive if the F-test statistics falls between the upper and lower critical bound. Lastly, the null hypothesis of no cointegration is accepted if the F-statistics is below the lower critical bound. If long-run relationship between FDI and export performance is found then we estimate the long run coefficients. The following model will be use to estimate the long-run coefficients

If we find evidence of long-run relationship between FDI and export performance then we estimate the short-run coefficients by employing the following model:

The error correction model (ECM) shows the speed of adjustment needed to restore the long-run equilibrium following a short-run shock. The ƞ is the coefficient of error correction term in the model that indicates the speed of adjustment. Cumulative sum and cumulative sum of square has been applied to analyze the stability of long run model.

Rolling window estimation has been used to find year wise coefficients of FDI of long run model. This study also employs the three different techniques of causality analysis namely, Granger causality analysis, Toda and Yamamoto-modified Wald test causality analysis and variance decomposition method to analyze the robustness of causal relationship between FDI and real exports.

Estimations and Results

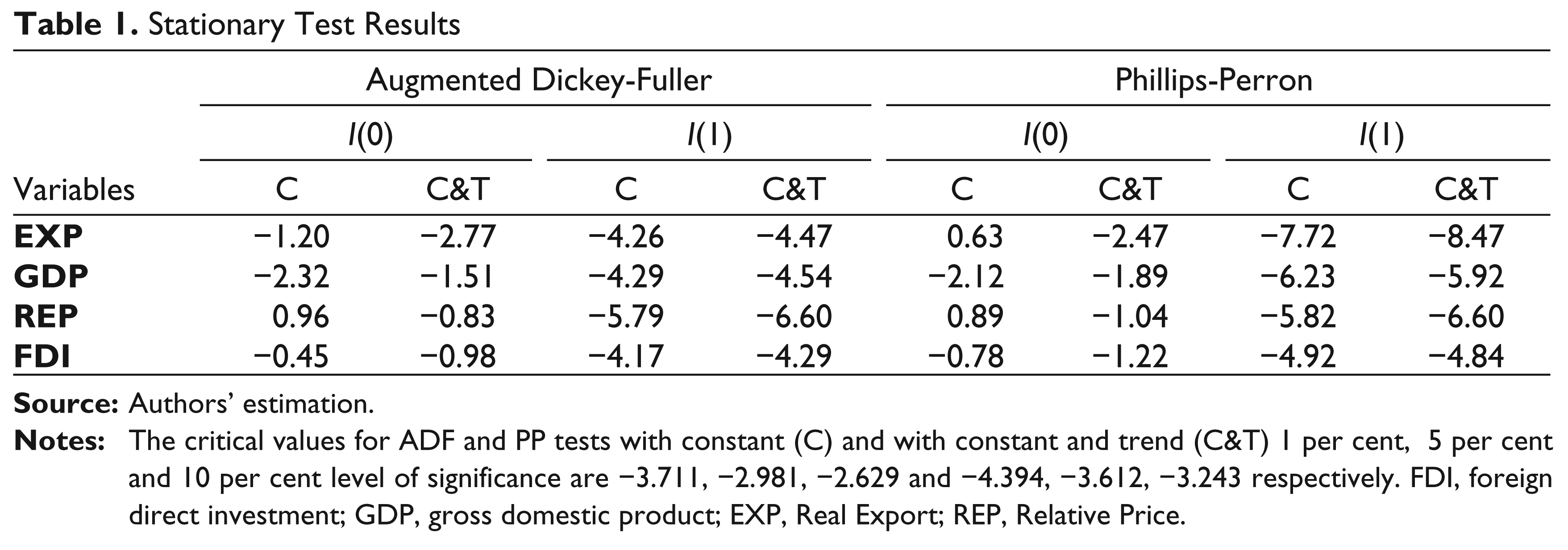

Augmented Dickey–Fuller and Phillips–Perron unit root test are used to examine the stationary properties for long-run relationship of time series variables. Augmented Dickey–Fuller test is based on equation given below

where εt is pure white noise error term, Δ is first difference operator, Yt is a time series, α0 is the constant and k is the optimum numbers of lags of the dependent variable. Augmented Dickey–Fuller test determines whether the estimates of coefficients are equal to zero. Augmented Dickey–Fuller test provides cumulative distribution of ADF statistics. The variable is said to stationary, if the value of the coefficient α1 is less than critical values from fuller table. Phillips–Perron unit root test equation is given below

The PP unit root test is also based on t-statistics that is associated with estimated coefficients ρ*. Table 1 represents the results of stationary tests. First, these tests are applied on level of variables then on their first difference.

Results of Table 1 show that all variables are stationary and integrated at first difference. This implies that the series of variables may exhibit a valid long-run relationship.

Stationary Test Results

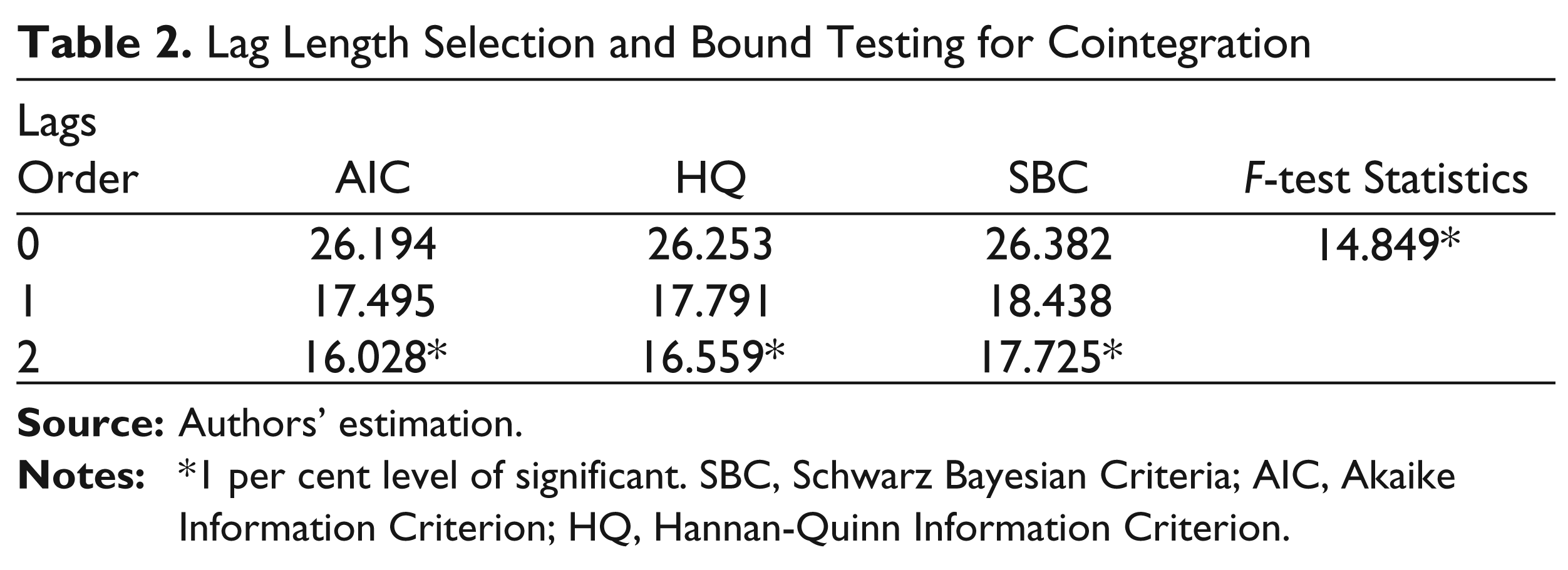

Autoregressive distributed lag method for cointegration is used to estimate the long-run relationship between FDI and export performance. The first step is to determine the optimal lag length of the model. The order of optimal lag length is decided by using the SBC. Table 2 shows the results of ARDL cointegration method.

Lag Length Selection and Bound Testing for Cointegration

The ARDL results suggest the rejection of null hypothesis of no cointegration in model because the value of the F-statistics is greater than upper bound critical value at 5 per cent level of significance in favour of alternative hypothesis that a valid long-run relationship exists between FDI and real exports in Pakistan.

Johansen and Jeuselius (1990) cointegration technique is also used to analyze the existence of long-run relationship of FDI and export performance. The J.J. cointegration test is based on λ trace and λ max statistics. First ‘trace test’ cointegration rank ‘r’ is as follows:

Second, λ max maximum number of cointegrating vectors against r + 1 is presented in following way:

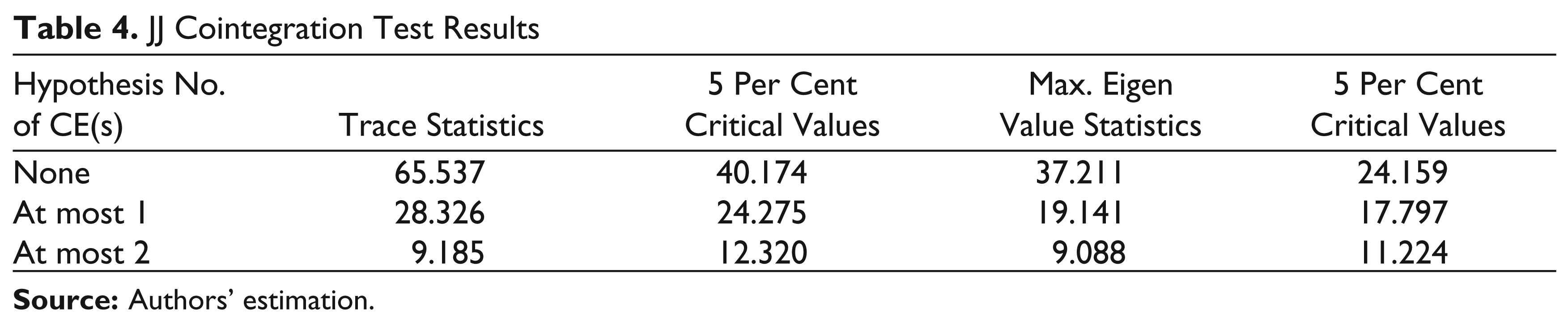

The null hypothesis of the J. J. cointegration is that there is no long-run cointegration among the variables. If null hypothesis is rejected that’s mean there is a significant long-run relationship among the series of variables and vice versa. Table 3 presents the results of Johansen and Jeuuselius cointegration. Results suggest a valid long-run relationship between the considered variables. The results from both the tests suggest that there exists a stable long-run equilibrium relationship of real exports with its major determinants such as Real Gross domestic product (GDP), Relative price (REP) and Foreign direct investment (FDI).

Lags Defined through VAR of Variables

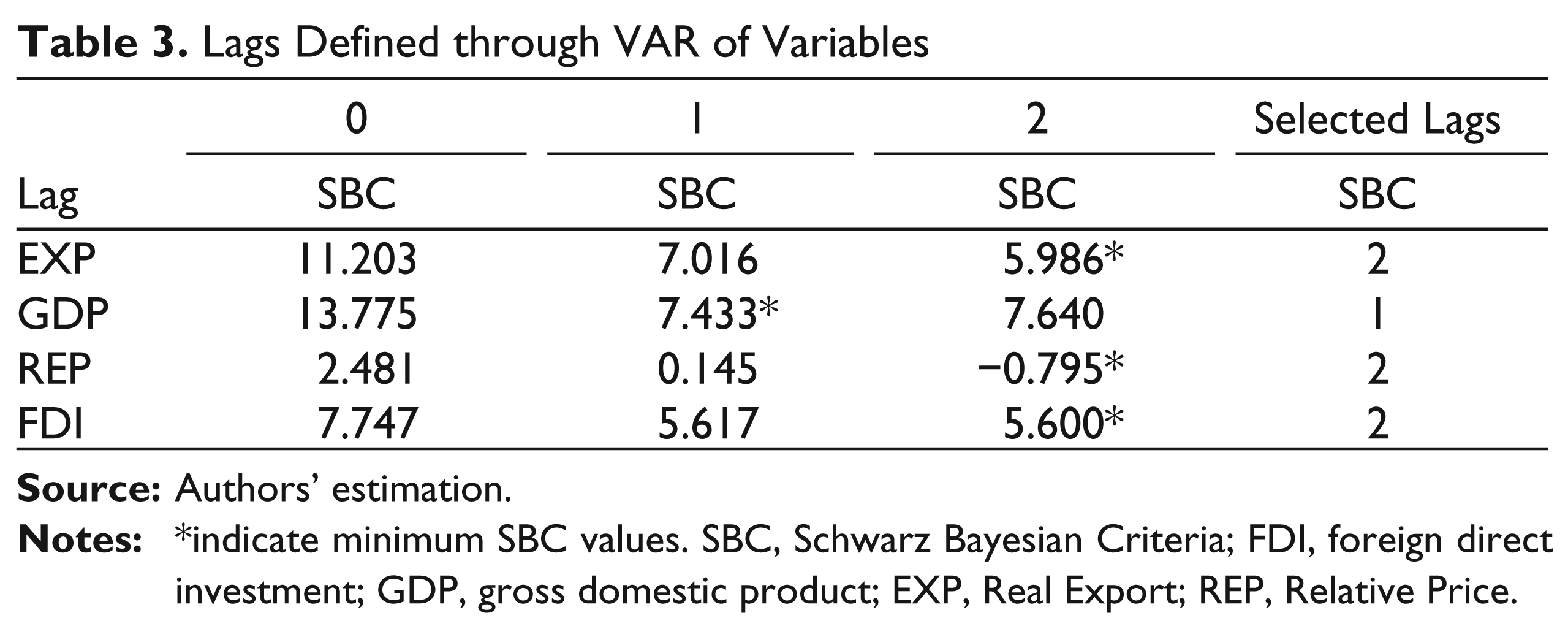

Now, we estimate the lag length order of the all variables through unrestricted vector auto regression method. The decision criterion is based on minimum value of SBC.

JJ Cointegration Test Results

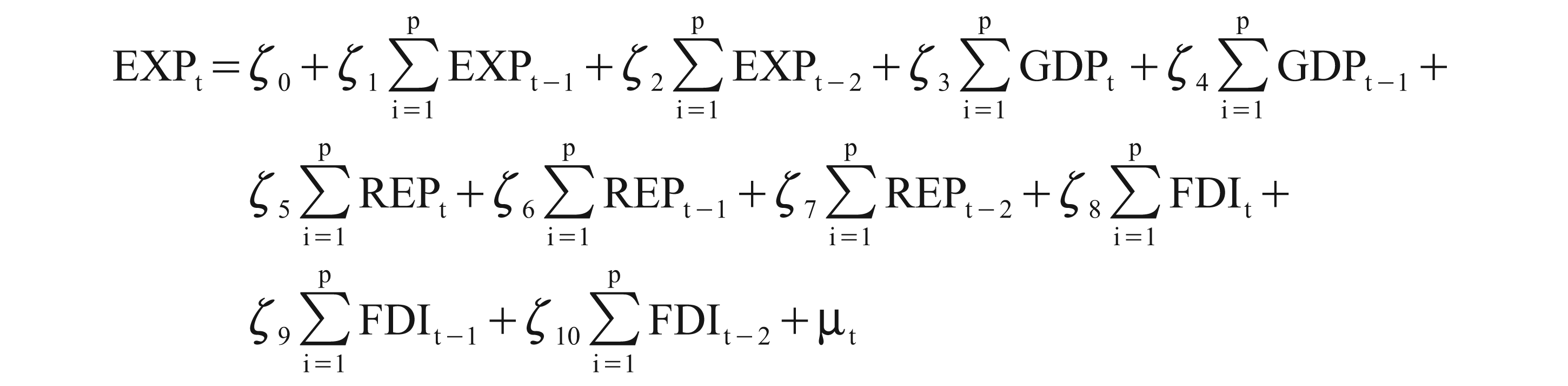

Table 4 represents the results of lag length order of all variables. Results of SBC indicate that the real export should be include at second lag, GDP should be included at first lag, relative price should be include at second lag and FDI should be include at second lag. After having the valid evidence of long-run relationship between FDI and export performance, we applied ARDL method to estimate the long run and short-run coefficients. The model for long-run coefficients as follows:

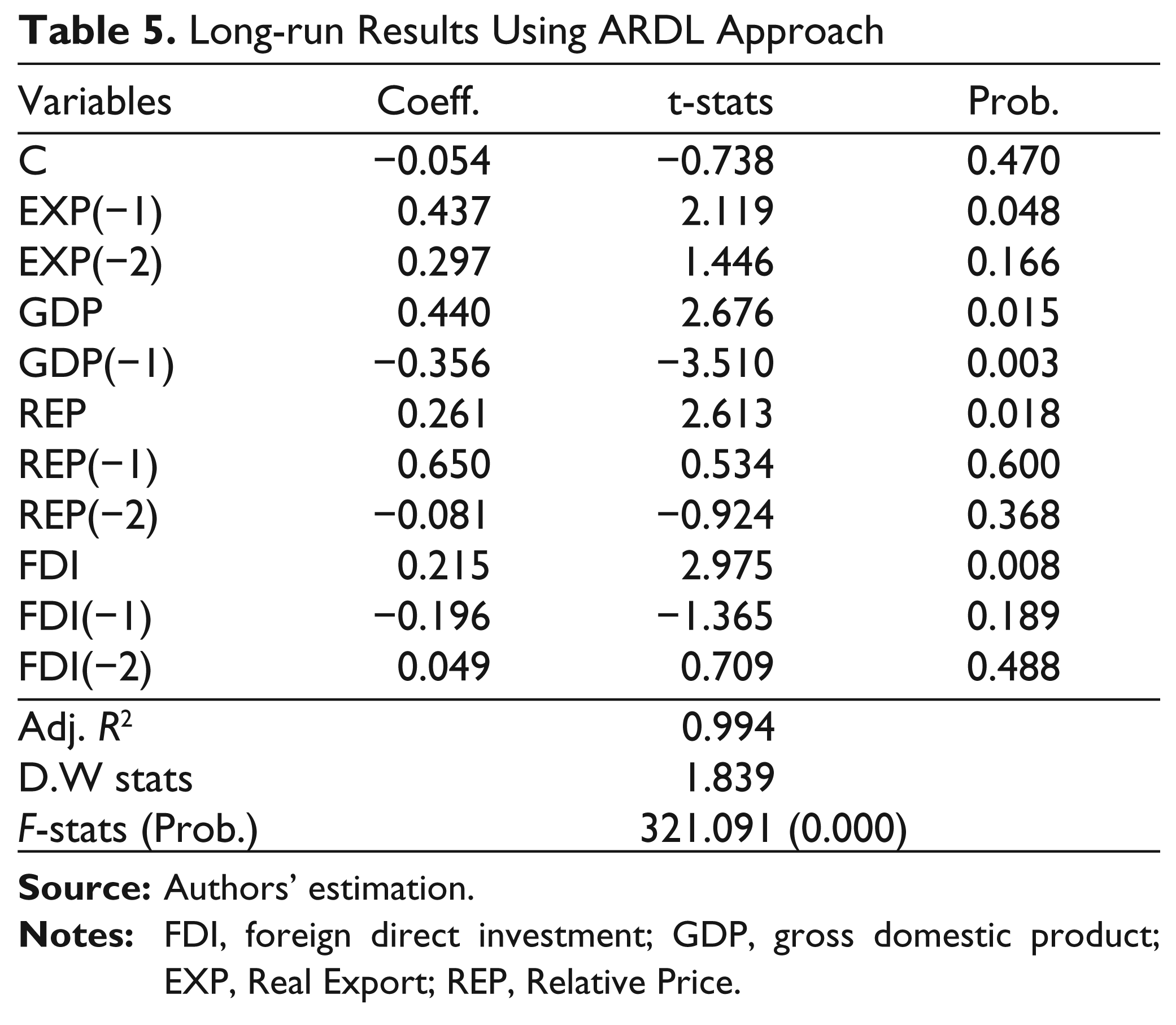

Table 5 shows the results of long-run ARDL estimations. Results indicate the significant positive long-run relationships exist between FDI and export performance in Pakistan, which means that the FDI coming into Pakistan contributes to the enhancement of export performance of Pakistan. Results suggest that most of the MNCs working in Pakistan are export-oriented companies and that they significantly contribute to the export performance. The results also suggest that the FDI coming in Pakistan is green field in nature, which means that the FDI is contributing to the increase in the GDP instead of capturing the market of domestic producers. The coefficient of FDI shows that in the long run 1 per cent increase in FDI causes the increase in the real exports by 0.22 per cent. The following model is used to check the short-run relationship among the considered variables with the different lag length:

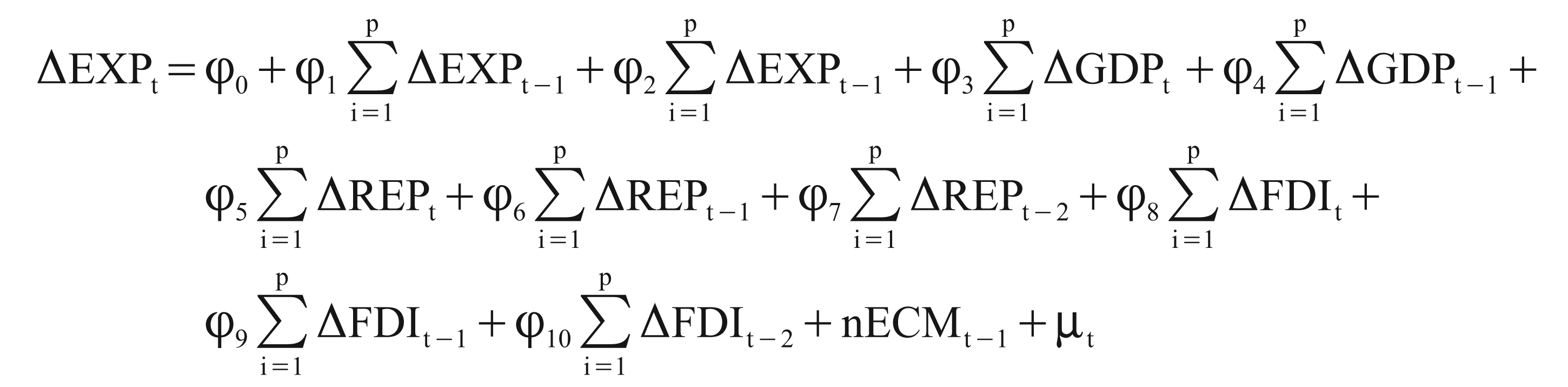

Long-run Results Using ARDL Approach

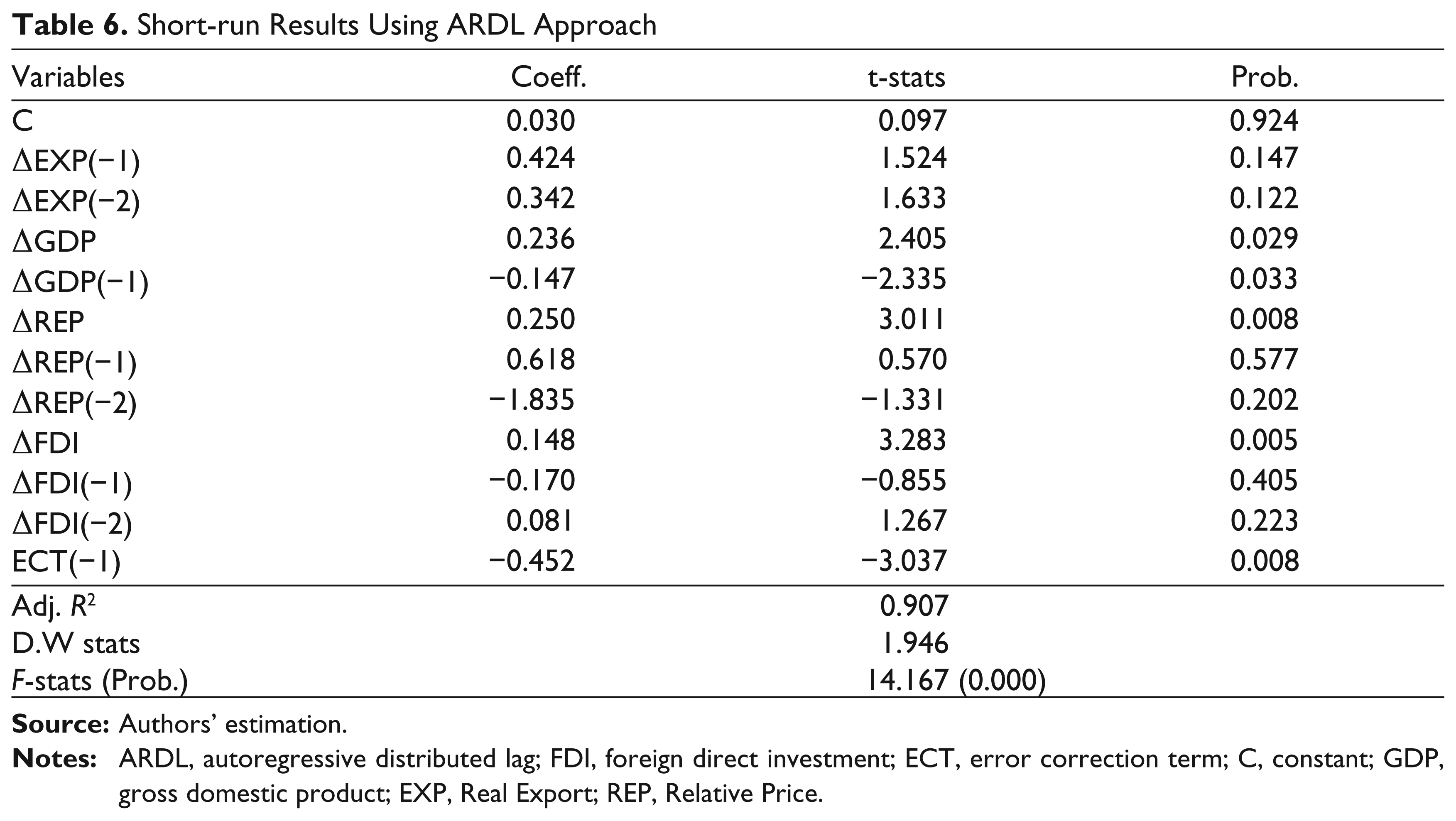

Table 6 represents the short-run relationship between FDI and export performance. Results indicate the lagged error correction term for the estimated real export equation is both negative and statistically significant. This confirms a valid short-run relationship between FDI and export performance in Pakistan. The coefficient of error term is −0.45 suggest that about 45 per cent of disequilibrium is corrected in the current year. Results indicate the significant positive short-run relationship of FDI with real exports in Pakistan.

Short-run Results Using ARDL Approach

Stability of Long-run Model

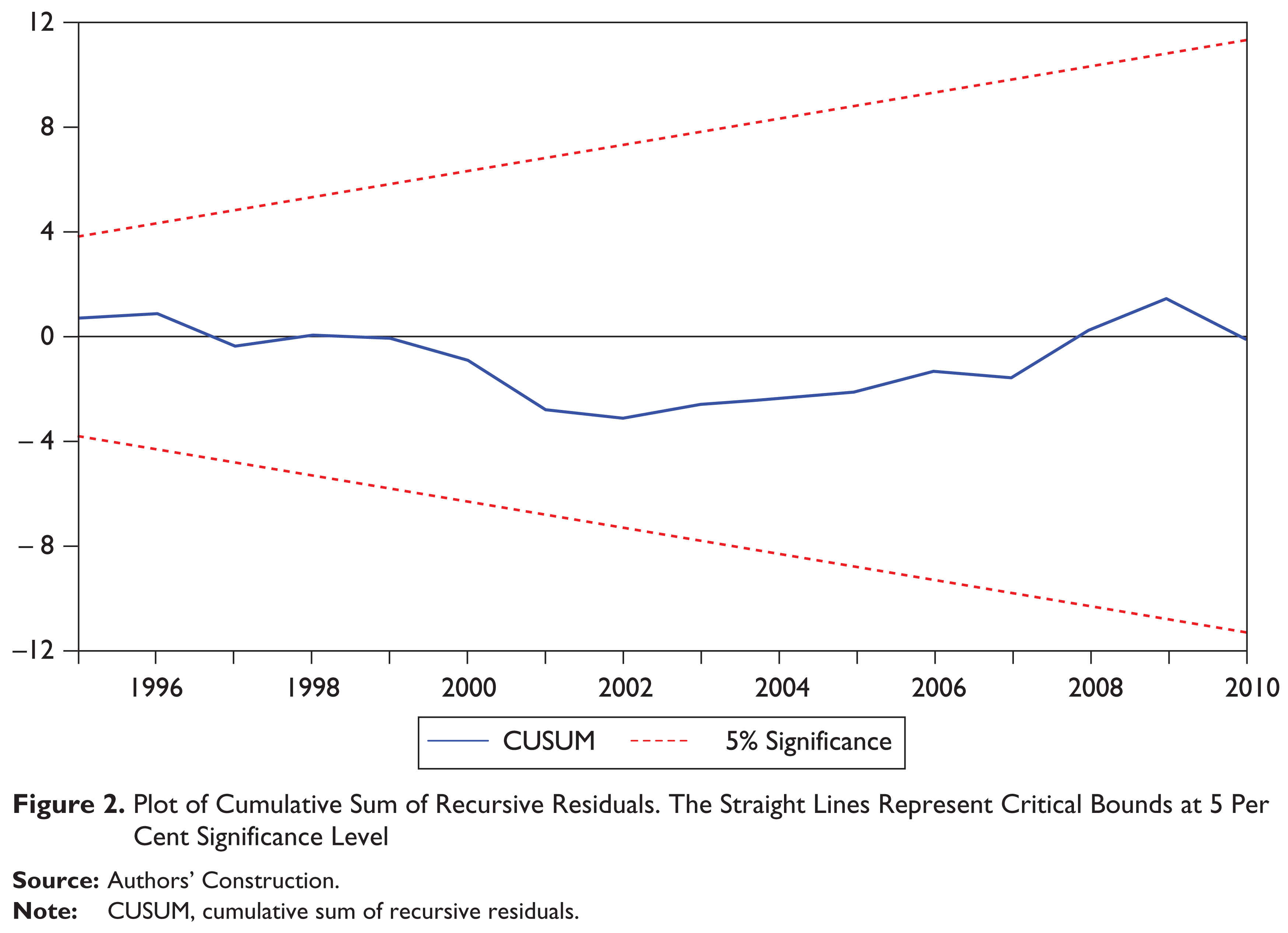

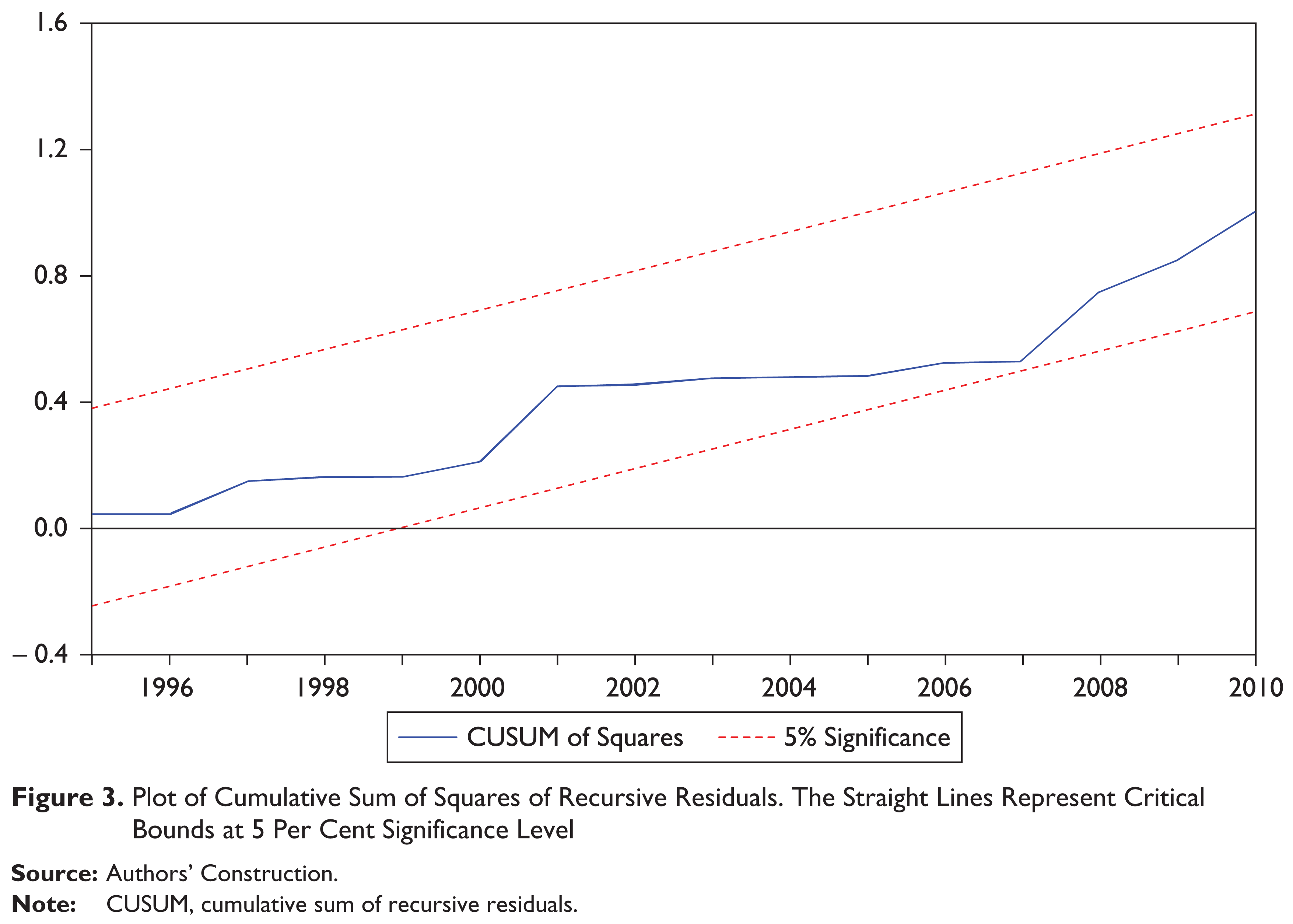

The stability of long-run model is evaluated by using the cumulative sum and cumulative sum of square test on the recursive residuals. Cumulative sum test detects systematic changes from the coefficients of regression, while, cumulative sum of square test is able to detects the sudden changes from constancy of regression coefficients (Brown, Durbin & Ewans 1975).

Figures 2 and 3 represent the results of cumulative sum and cumulative sum of square tests, respectively. Results indicate that the statistics of both cumulative sum and cumulative sum of square test lie within the interval bands at 5 per cent confidence interval. Results suggest that there is no structural instability in the residuals of equation of real exports.

Causality Analysis

In this section, three different techniques of causality analysis namely, Granger causality analysis (Granger, 1969), Toda and Yamamoto modified Wald test (Toda & Yamamoto, 1995) and variance decomposition method 1 have been used to analyze the robustness of causal relationship between FDI and real exports.

The direction of causality between dependent and independent variables is analyzed by Granger (1969) causality test. We determine the causality analysis of our export performance model on lag one. Jones (1989) favours the ad hoc selection method for lag length in Granger causality test over some of other statistical method to determine optimal lag. The equation of Granger causality model is given below

It is assumed that μ and ν are uncorrelated. There are two variables and dealt with bilateral causality. Above equation states that Y is related to its lag values and X is related to its lag values.

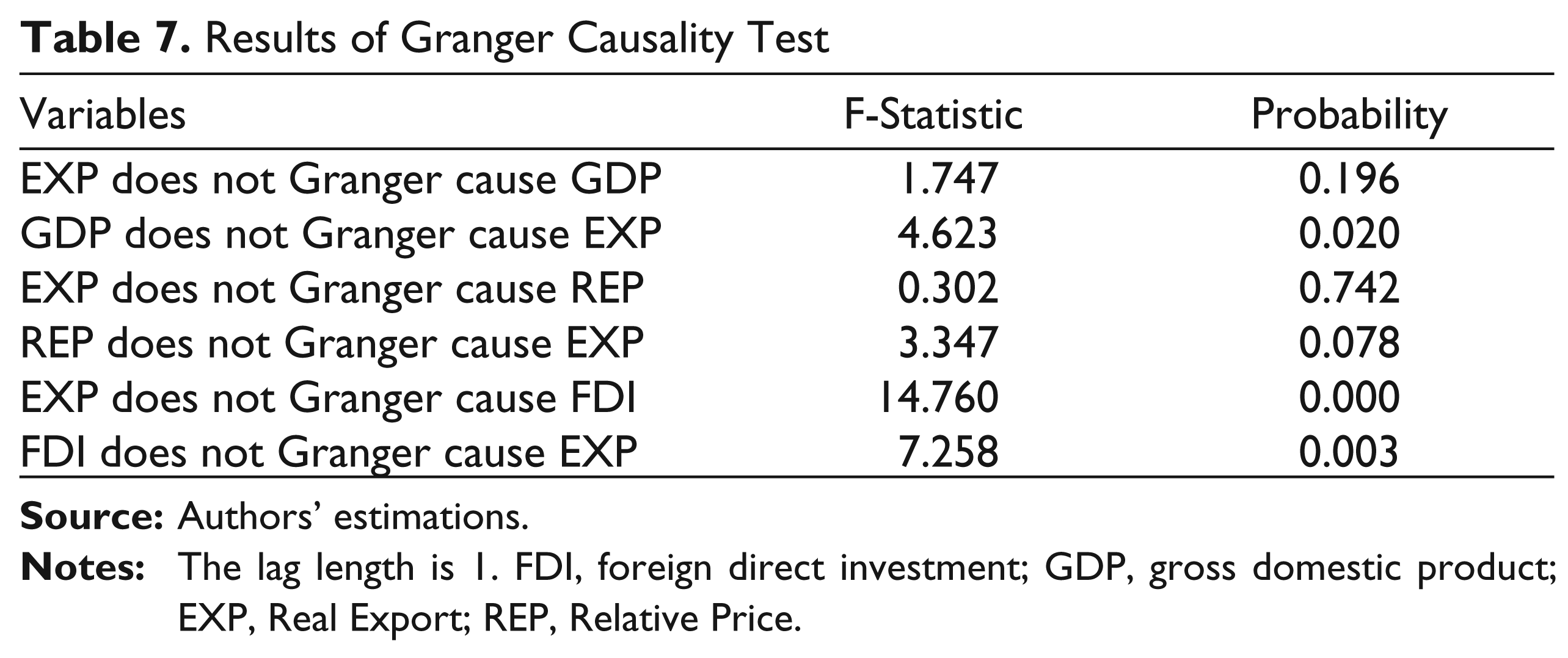

The results of Granger causality test are reported in Table 7. Results of Granger causality test suggest the bidirectional causal relationship between FDI and real exports.

Results of Granger Causality Test

The direction of causality between dependent and independent variables is analyzed by using the causality test based on Toda and Yamamoto (1995) procedure. This test use a modified Wald (MWALD) test which can be applies irrespective of the of whether underlying variables are purely I(0), I(1) or mutually cointegrated. Toda and Yamamoto (1995) augmented Granger causality test uses the seemingly unrelated regression (SUR) technique through estimating a two equation system. The Wald test improves efficiency when SUR models are used in the estimation. So, the model can be specified as follows:

where k is the optimal lag order, d is the maximum order of integration of the series in the system, and εyt and εxt are error terms that are assumed to be white noise. Usual Wald tests are then applied to the first k coefficient matrices using the standard χ2– statistics.

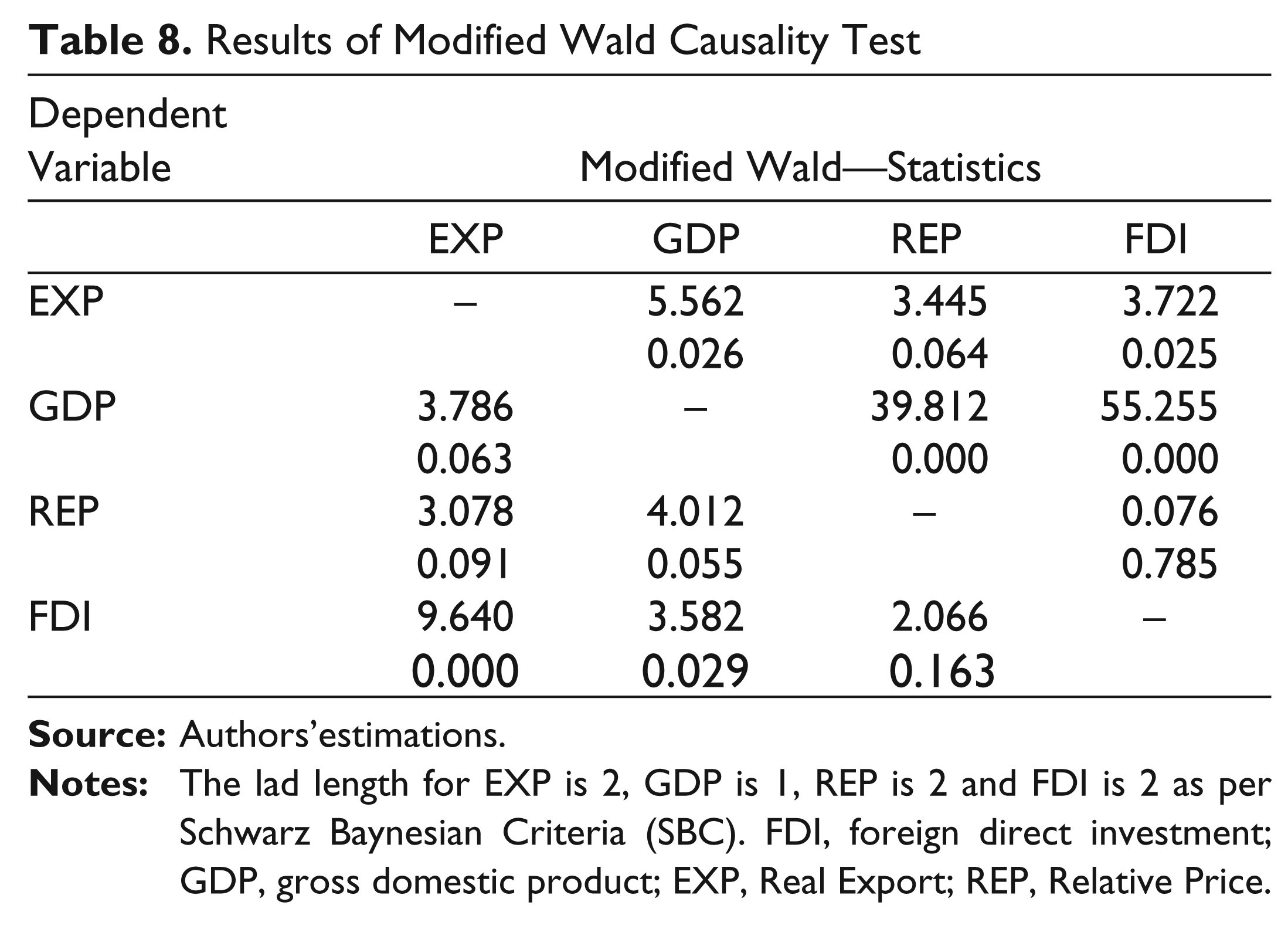

The results of Toda and Yamamoto (1995) based causality test are reported in Table 8. Results indicate bidirectional causal relationship between FDI and export performance.

Results of Modified Wald Causality Test

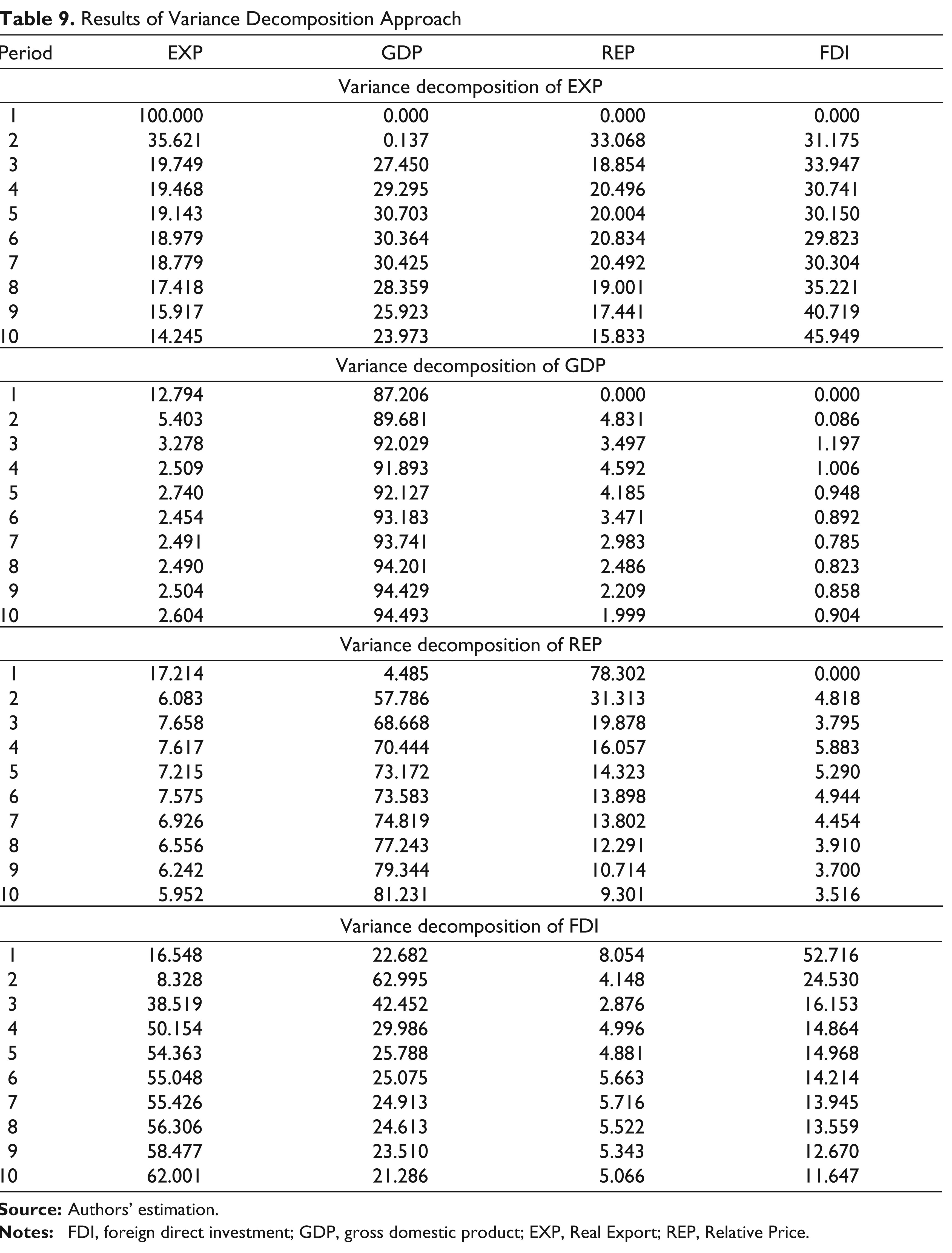

Generalized forecast error variance decomposition method under vector autoregressive (VAR) system has been used to analyze the strength of the causal relationship of FDI and export performance. The variance decomposition method provides the magnitude of the predicted error variance for a series accounted for by innovations from each of the independent variable over different time period. Wong (2010), Jawaid and Raza (2013) and Raza, Shahbaz and Nguyen (2015) have used this approach to find causal relationship. Table 9 represents the results of variance decomposition analysis.

Results of Table 9 show that in the first round the change in real exports explain completely by its own innovations. In the second period, the change in real exports explain 35.62 per cent by own innovation, 31.18 per cent by FDI innovation, 33.07 per cent by relative price innovation and 0.14 per cent by GDP. In period five, the shocks in real export explain 19.14 per cent by own innovation, 30.15 per cent by innovations of FDI, 20.00 per cent by innovations of relative price and 30.70 per cent by innovations of GDP. In tenth period, the shocks in real export explain 14.25 per cent by own shocks, while, 45.95 per cent are explained by innovations of FDI, 15.83 per cent are explained by relative price and 23.97 per cent are explained by innovations of GDP. The shocks in FDI explain 16.55 per cent, 54.36 per cent and 62.00 per cent by innovation of real exports in period 1, 5 and 10 respectively. These findings suggest the bidirectional causal relationship between FDI and real export.

Results of Variance Decomposition Approach

Rolling Window Analysis

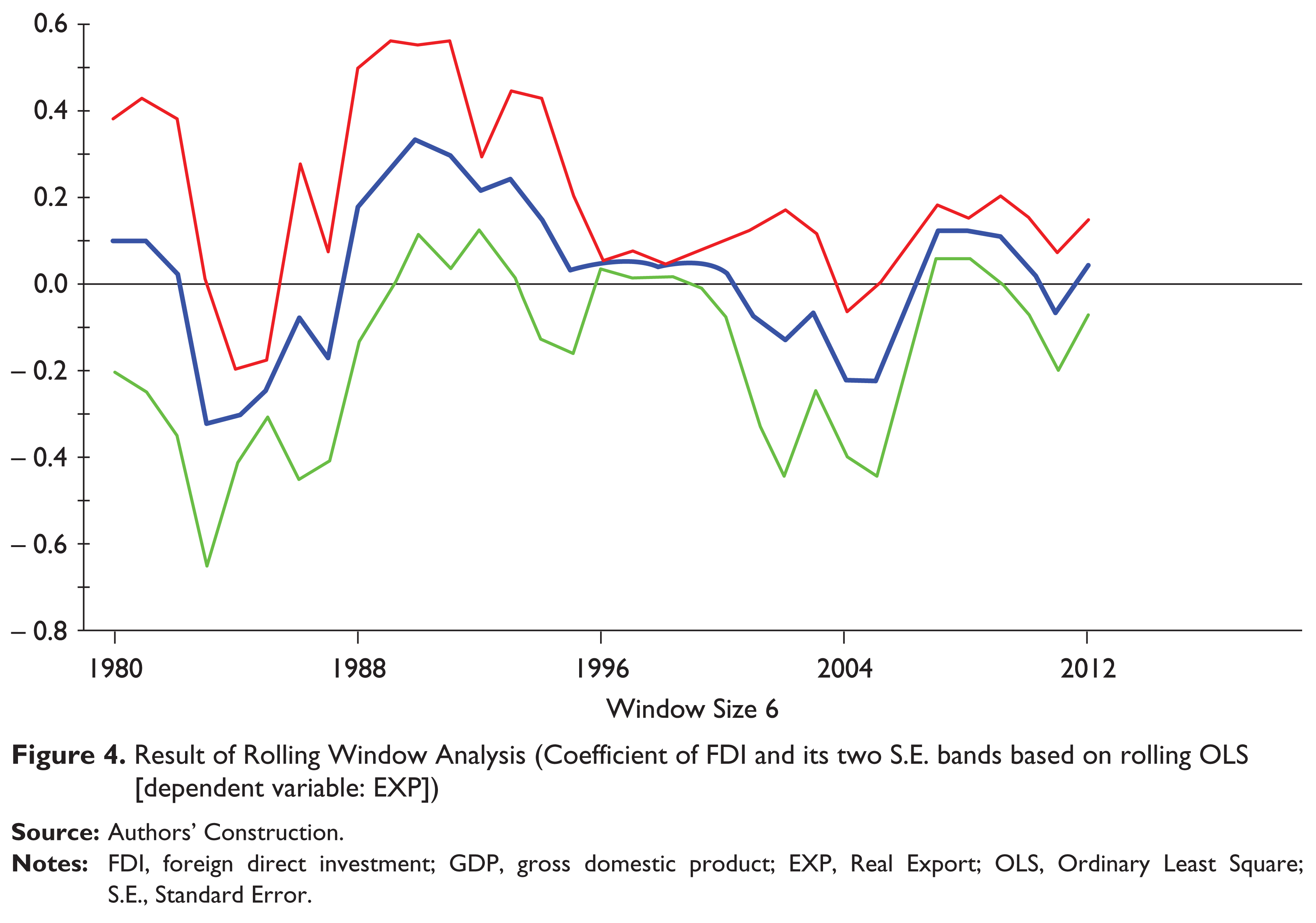

The range of coefficients of long-run model throughout the sample has been analyzed through rolling window estimation method. Rolling windows estimation method provides the coefficient of each year of a sample size which clearly shows the behaviour of the coefficients throughout the sample period. Figure 4 represents the results of yearly coefficients of FDI.

Two standard deviation bands show the upper and lower bounds. Results from Figure 3 indicate that the coefficient of FDI shows very mixed results. The coefficient of FDI in export model remains negative from 1983 to 1987, from 2001 to 2006 and in 2011. The coefficient of FDI in export model shows a positive coefficient in the remaining years.

Conclusion and Recommendations

This study investigates the impact of FDI on export performance in Pakistan by using the long annual time series data from the period of 1974–2012. Autoregressive distributed lag-bound testing cointegration approach confirms the valid long-run relationship between considered variables. Results indicate the significant positive impact of FDI on real exports in long run as well as in short run. Results of Granger causality test, Toda and Yamamoto Modified Wald causality test and variance decomposition test confirm the bidirectional causal relationship between FDI and export performance. Results of rolling window analysis suggest that the coefficient of FDI in export model remains negative from 1983 to 1987, from 2001 to 2006 and in 2011. The coefficient of FDI in export model show positive coefficient in remaining years.

It is suggested that FDI and real export are connected in complementary way in Pakistan. The policy makers should make policies in favours of foreign investors to attract more FDI in Pakistan. In the years in which FDI has negative effect on exports, a study to find the reason behind this negative effect will be beneficial. Additionally, export processing zone (EPZ) is one of the best destination of inward FDI for the country. Pakistan should encourage duty-free imports for producing export commodities in EPZ. The government should ensure that EPZ’s outputs are traded with the rest of the world. The objective of utilization of location-specific assets can be achieved through EPZ. In addition, if one accepts Jawaid’s (2014) findings on the positive effect of export performance on economic growth and economic growth leads improvement in terms of trade (Jawaid and Waheed, 2011) which is further beneficial for exports, we suggest yet another channel through which FDI may raise the economic growth in Pakistan. Foreign direct investment can provide pathway for Pakistan to enhance economic growth through increasing overall export productivity.

Pakistan is a labour-intensive country. Therefore, policy makers should invest more on human capital to absorb new technologies to get more benefit of technological transfer as a result of this inward FDI. Pakistan should encourage efficiency seeking FDI rather than market seeking FDI. Policy makers ought to take care of those firms who have potential to be an exporter against those multinationals who captures the potential of those firms. Pakistan would get more benefit from inward FDI when they utilize this investment in accordance with their comparative advantage.

In addition to this, domestic investment should be considered to enhance the export performance. It will be reasonable to progressively improve the export structure and increase competitiveness of local firms. Simultaneously, FDI does not work uniformly in all sectors, policy makers should understand the difference and identify their sector-wise policies relating with FDI. The law and order should also be maintained, which is the essential part to attract the foreign investors. At this stage we can also set the direction of future research, that is, sector-wise study should be done on the relationship between FDI and exports which will help in formulating export-promoting policies for the country.

Footnotes

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the paper. Usual disclaimers apply.