Abstract

Mobile payment (m-payment) still lacks widespread acceptance among Bangladeshi users despite its enormous possibilities. Previous studies have identified the reasons behind such reluctant usage intentions based on the data collected from regular m-payment users in Bangladesh. However, in Bangladesh, no study has considered the first-time user experience, which reflects initial trust yet. Therefore, the study was undertaken to identify the factors determining initial trust and their impact on m-payment usage intention in Bangladesh. We applied the structural equation modelling method to conduct an analysis of 284 first-time m-payment user data in Bangladesh. Initial trust was found positively influenced by perceived ubiquity, perceived security and perceived ease of use; perceived usefulness and the intention to use m-payments were found positively affected by initial trust. The study also revealed the positive association of users’ personal innovativeness and the negative association of perceived cost on m-payment usage intention. The mediation effects of initial trust were also found significant. The study recommends building initial user trust and service provider measures to encourage m-payment usage intention.

Introduction

Mobile phone-enabled services are opening the doors of possibilities by making our everyday life more convenient than ever before. Among them, mobile payment (m-payment), offering anytime, anywhere financial transactions via mobile devices supported by wireless communication technology, is noteworthy (Srivastava et al., 2010; Talwar et al., 2020; Yang et al., 2012). In line with technological advancements in wireless communication technology, both m-commerce- and e-commerce-based transactions had become familiar around the world in the past few years (Bhat et al., 2016; Chou et al., 2018). Simultaneously, the m-payment system has become an indispensable part of dealing with e-commerce as well as m-commerce activities (Yan & Yang, 2015; Yang et al., 2012; Zhang et al., 2019). It facilitates cashless, checkless and card-less payment (Chin et al., 2020). Ubiquity and the least transaction fee are the main reasons for its attractiveness as compared to any other form of payment options (Bezhovski, 2016; Shaw, 2014). It is assumed that, in the payments industry, m-payment will be dominant unquestionably (Bezhovski, 2016; Pisani & Moormann, 2018).

However, the encryption system of mobile networks is less robust and integral, making it accessible to information interference (Gao & Waechter, 2017; Zhou, 2011). Thus, it is considered that m-payment involves greater security issues and uncertainties when compared to traditional payment systems and other forms of online payment systems (Linck et al., 2006; Wang et al., 2016; Wong & Mo, 2019; Yan & Yang, 2015; Yu et al., 2018). Moreover, due to cellular network instability and bandwidth limitation, users experience service interruption and delay while using mobile-based services (Gao & Bai, 2014; Yan & Pan, 2014). Therefore, despite being a promising technological solution, m-payment still has a sluggish growth in countries with different economic conditions and customer base (Gao & Waechter, 2017; Garrett et al., 2014; Kongaut & Lis, 2017; Zhou, 2011).

Studies conducted in previous years revealed the barriers and facilitators behind users’ behavioural intentions concerning m-payment adoption and usage. Among them, trust (or perceived trust) has received a special spotlight from researchers as a major factor in m-payment adoption and continuous use intention since m-payment involves monetary transactions (Pal et al., 2020; Qasim & Abu-Shanab, 2016). Trust, in the case of service delivery, means the optimistic expectations of users regarding service issues from their service providers (Mayer et al., 1995; Shankar & Datta, 2018). Dimensions of trust includes integrity, ability and benevolence (Palvia, 2009). According to Shankar and Datta (2018), integrity means the service providers’ capability to maintain their responsibilities towards users; ability means sufficient technical knowledge to deal with user issues; and benevolence means upholding users’ interest with the highest priority. Studies from different parts of the world have reported that users’ desire to accept and use m-payment services is significantly influenced by their trust perception (Al-Saedi et al., 2020; Chin et al., 2020; Dlodlo, 2014; Duane et al., 2014; Mallat, 2007; Manrai & Gupta, 2020; Kar, 2020; Keramati et al., 2012; Pal et al., 2020; Park et al., 2019; Patil et al., 2020; Phonthanukitithaworn et al., 2015, 2016a, 2016b; Raman & Aashish, 2021; Shankar & Datta, 2018; Shao et al., 2019; Srivastava et al., 2010; Talwar et al., 2020; Wong & Mo, 2019; Xin et al., 2013; Yan & Yang, 2015; Yan et al., 2009; Zhou, 2013). Conversely, researchers have validated the significant influence of initial trust, a more intensified view of trust perception, in some studies about m-payment adoption, in the context of China (Lu et al., 2011; Zhou, 2011, 2014), Australia (Gao & Waechter, 2017) and India (Talwar et al., 2020). They reported that users’ constant trust perception about a technology is subject to a continuous development process. The process depends on users’ provisional belief grown after the initial interaction with that particular technology. Such provisional beliefs of the users were termed as initial trust in those studies. Lu et al. (2011) identified initial trust as an influential factor of m-payment adoption in the future. They conducted a multi-sample analysis of worker and student groups who were the non-adopters of m-payment but had experience of using Internet payment services. The study was carried out on the basis of a proposed decision-making model emphasizing customers’ trust. The results showed that people’s initial trust in m-payment-based services is strongly affected by how they felt about the reliability of Internet payment services in the past. This was true for both sample groups. The study also reported that initial m-payment trust negatively affected perceived risk and positively affected relative advantage. These factors in turn influenced the behavioural intention of using m-payment. Zhou (2011) identified that perceived ubiquity, perceived ease of use and perceived security positively determine initial trust. The study concluded that if the m-payment service providers (PSPs) can ensure ease of service use, security and ubiquitous connections, then they will be able to lessen perceived risks and amplify the perceived usefulness of their services, which will magnetize users. Moreover, he reported the negative association of perceived cost with m-payment usage intention. In one of Zhou’s (2014) later studies, the impact of factors based on self-perception (i.e., ubiquitous connection as well as effort expectancy) and factors based on transference (i.e., structural assurance along with trust in online payment) on initial trust was empirically tested for identifying the tendency of m-payment usage intention. The study concluded that both factors positively influence initial trust, and initial trust consecutively influences performance expectancy and the intention to use m-payment.

Gao and Waechter (2017) used an extension of the valence framework to understand the facilitators and inhibitors of initial trust for further detection of its impact on m-payment usage intention. In addition, it reported the positive effects of three positive valence components (i.e., perceived service quality, information quality and system quality) and the negative effects of one negative valence component (i.e., perceived uncertainty) on initial trust. All these valence components’ effects on initial trust were found to have an influence over the intention to use m-payment. Moreover, initial trust through perceived benefits and perceived convenience were found to influence the intention of m-payment usage. Talwar et al. (2020) proposed a two-step framework, representing pre-adoption and post-adoption factors, in order to explore the significance of initial trust in case of intention to use m-payment continuously. Their study reported that at the pre-adoption stage initial trust is influenced by both perceived quality of information and quality of services. Further, as an antecedent, initial trust influences the post-adoption determinants like perceived usefulness and confirmation, which finally justify the continuous m-payment usage intention.

These prior findings have made us think about the influence of potential users’ initial trust in the case of m-payment acceptance and usage intention in Bangladesh. Currently, Bangladesh possesses a large subscriber base with services from four mobile phone operators. At the end of May 2022, the overall number of verified subscriptions having any kind of mobile activity was 184.23 million, and the number of mobile Internet users was 125.52 million (Bangladesh Telecommunication Regulatory Commission, 2022a; 2022b). Besides, the applications of fourth generation wireless (4G) technology are providing faster Internet connectivity through the country. A study by Rogers (2018) reported that mobile Internet penetration rate in Bangladesh at the end of 2017 was 21%, and it will be 41% by the end of 2025; Smartphone adoption rate was 31% in 2017, and it will be 75% by 2025. Hence, it implies that the consumer market in Bangladesh has the potential for m-PSPs. M-payment is popularly known as mobile banking to the common people of Bangladesh (Rahman et al., 2021). Currently, there are 15 scheduled banks’ subsidiaries exclusively providing mobile financial services (MFS) in Bangladesh (Bangladesh Bank, 2021a). Besides, a significant number of PSPs are licensed as digital wallets, e-wallet, digital financial services, etc., and working solely or in collaboration with some scheduled banks (Bangladesh Bank, 2021d). Users can access these services using both offline mobile menu options and mobile app platforms for cash in and out, personal payment (P2P), business payment (P2B or B2B) or government payment (P2G or G2P) (Bangladesh Bank, 2021c). Moreover, few global brands also have license of their operations in Bangladesh.

Due to the Coronavirus Disease 2019 (COVID-19) outbreak, the number of people using MFS has increased as dependency upon e-commerce, m-commerce and other digital platforms has increased. Concerned people are now reluctant to go for the traditional payment option. The number of registered MFS accounts increased by 11.35 million from April 2020 to April 2021 (Bangladesh Bank, 2021b). The Government of Bangladesh is also liberal about MFS and PSP operations in Bangladesh. At present, almost all of the P2G and G2P payments can be made by m-payment platforms. However, according to the statistical report of Bangladesh Bank (2021b), only 38.09% (36.75 million) of the MFS accounts were active among 96.48 million registered accounts in April 2021, and it was only 22.90% of the overall population in Bangladesh (Macrotrends LLC, 2021). It implies that, despite a promising service, the m-payment penetration rate has not reached to a satisfactory level. As a result, it has become imperative to investigate the reasons behind such a reluctant intention towards m-payment adoption in Bangladesh. Some earlier studies have been conducted reporting the facilitators and barriers of m-payment adoption in Bangladesh (Hossain & Mahmud, 2016; Hossain et al., 2018; Islam, 2016; Rahman et al., 2021). However, no previous research has focused on the impact of initial trust in the case of m-payment usage intention in Bangladesh considering the non-adopters. Hence, the study objective was to mitigate the aforementioned research gap by investigating the factors of initial trust and the influence of initial trust on the usage intention of m-payment in Bangladesh, and the research questions (RQs) were as follows.

RQ1: What factors determine the initial trust of potential m-payment users in the case of Bangladesh?

RQ2: What are the impacts of initial trust on m-payment usage intention in the case of Bangladesh?

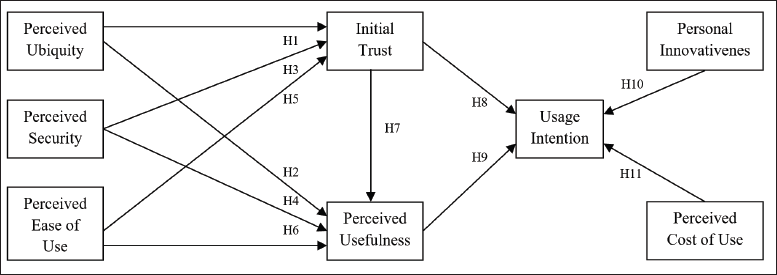

The research model suggested by Zhou (2011) was followed for developing the study’s conceptual model with a view to answering the above-mentioned two questions. The finding of the study is expected to be significant as it would provide some critical insights for the researchers in the field of service marketing in case of consumers’ perception, psychology and behaviour analysis. Marketing professionals and the service providers will get insights for marketing strategy development based on the findings of users’ feedbacks and expectations.

Theoretical Framework and Hypotheses

The fundamental notion of the conceptual model (Figure 1) proposed for the current study has been adapted from Zhou’s (2011) research model used previously in examining initial trust’s effects on m-payment adoption in China. We have adopted the model with a slight adjustment due to the similar investigation purpose but in the context of Bangladesh. The conceptual model comprises three main constructs: perceived ubiquity, perceived security and perceived ease of use, acting as determinants of initial trust and perceived usefulness. Further, initial trust is acting as a determinant of perceived usefulness and usage intention, whereas perceived usefulness is determining usage intention. Two control variables: perceived innovativeness and perceived cost of use are also included in our proposed model with the view to analysing their direct association with usage intention.

Technology adoption in the case of developing countries is always subject to some major barriers, such as illiteracy, lack of tech know-how, risks due to doubts about losing confidential information and conflict of interest between the users and the service providers, and inaccessibility to the Internet and strong network (Ansari, 2018; Rahman, 2013). These hostile factors to the technology adoption are conceptually conversant to the antecedents of initial trust and usefulness such as perceived ease of use, perceived ubiquity and perceived security addressed by Zhou (2011). Hence, considering the emerging economic context of Bangladesh, we have adopted the antecedents of initial trust and perceived usefulness from Zhou’s (2011) model and proposed them in our study with no modification. Some studies reported that perceived cost of using m-payment has a direct influence on its usage intention in the countries having majority of low- to mid-income users (Hongxia et al., 2011; Humbani & Wiese, 2018; Lu et al., 2011; Phonthanukitithaworn et al., 2015, 2016a; Sobti, 2019; Zhou, 2011). They prefer services that are cost-effective and financially beneficial to them. Besides, most of the users feel anxious and show loath attitude to embrace or experiment any technological change. Consequently, personal innovativeness was also reported to have a direct influence on m-payment usage intention in developing countries (Hunafa et al., 2017; Patil et al., 2020; Shankar & Datta, 2018; Thakur & Srivastava, 2014; Upadhyay & Chattopadhyay, 2015). Hence, assuming that the income level of people of Bangladesh and inertia to accept new technology may have direct effects on the m-payment use intention, we have included perceived cost of use and personal innovativeness as control variables in our study. The description of the constructs and hypotheses are conferred in the subsequent parts.

Perceived Ubiquity, Initial Trust and Perceived Usefulness

Perceived ubiquity represents the notion that technology can be accessed at anytime from anywhere, and it is considered as the major benefit of m-payment systems in comparison to both traditional and online banking (Bezhovski, 2016; Shaw, 2014; Varshney & Vetter, 2002). If ubiquity is ensured, users of m-payment systems need not face any spatial or time-related limitations, and they can make payments conveniently (Gao & Waechter, 2017). Moreover, ubiquitous connection enhances perceived usefulness (Kim et al., 2010), which represents users’ optimistic conviction regarding a products’ utilities that the product will increase their performance efficiency (Shankar & Datta, 2018; Talwar et al., 2020). Earlier studies have validated the positive impact of perceived ubiquity on initial trust (Zhou, 2011, 2014), and perceived ubiquity on perceived usefulness (Zhou, 2011). The proposed hypotheses for further validation are as follows.

Perceived Security, Initial Trust and Perceived Usefulness

Users’ conviction that the confidentiality of both personal and financial information will remain secure while using m-payment system is termed as perceived security (Zhang et al., 2019). Users prefer the highest security of their confidential information, and therefore, perceived security is a very sensitive issue in the case of m-payment adoption (Moorthy et al., 2020). Users do not find it useful if m-payment is unsecured (Zhou, 2011) as perceived security facilitates users’ m-payment adoption intentions (Zhao & Bacao, 2021). The positive impact of perceived security on initial trust and perceived security on perceived usefulness was observed by Zhou (2011) in the case of m-payment adoption. Nevertheless, the study concluded an insignificant association of perceived security and perceived usefulness. The proposed hypotheses for further validation are as follows.

Perceived Ease of use, Initial Trust and Perceived Usefulness

The users’ expectations regarding the level of difficulty they will experience while making m-payments are reflected in the perceived ease of use of the system (Shankar & Datta, 2018; Zhou, 2011). Users prefer a clear, flexible and friendly interface while using any mobile platform (Phonthanukitithaworn et al., 2015). A simple yet comprehensive interface with easy navigation positively persuades m-payment users’ experience. Tew et al. (2022) reported that mobile ease of use and mobile usefulness play a crucial role in determining the intentions of m-payment acceptance in the case of a developing country. Earlier studies have confirmed the positive impact of perceived ease of use on initial trust (Zhou, 2011) and perceived ease of use on perceived usefulness (Kim et al., 2010; Liu et al., 2019; Srivastava et al., 2010; Zhou, 2011). The proposed hypotheses for further validation are as follows.

Initial Trust, Perceived Usefulness and Usage Intention

Users’ provisional belief, termed as initial trust, after using a technology for the first time is considered very critical for mobile service providers to recognize since it mitigates perceived risk (Zhou, 2011). Chakraborty et al. (2022) also explained the significance of initial trust in m-payment app adoption process in their study. According to Gao and Waechter (2017), initial trust results in the assurance of getting useful outcomes from a service in the future. They added that being unable to trust a service makes them think about the lack of capability and compassion of the service providers of m-payment; consequently, they will not prefer it as useful. Hence, earlier studies have identified initial trust as a critical factor to perceived usefulness (Talwar et al., 2020; Zhou, 2011) and usage intention (Gao & Waechter, 2017; Zhou, 2011, 2014). Again, perceived usefulness was also found associated with m-payment usage intention (Andavara et al., 2021; Liu et al., 2019; Talwar et al., 2020; Zhou, 2011). Generally, people plan to use a system once they believe it is useful and offers quick, speedier and convenient transactions (Singh et al., 2021), and it is seen as a crucial ‘moment of truth’ that helps to build a strong foundation for sustainable use (Rafdinal & Senalasari, 2021). The proposed hypotheses for further validation are as follows.

Personal Innovativeness, Perceived Cost of Use and Usage Intention

Users’ eagerness for trying out a new technology is termed as personal innovativeness (Chang et al., 2005; Kim et al., 2010). A person with high innovativeness is dynamic in nature, and they are responsive to new information and technology (Tariq, 2007). Regardless of how sophisticated a technology is, innovative people adopt it (Senali et al., 2022) as they are not afraid of taking risks (Abubakre et al., 2020). These sort of people have the ability to observe ease of use and usefulness of any new technology comprehensively (Lu et al., 2005). Kim et al. (2010) reported a significant association of personal innovativeness with m-payment usage intention. On the other side, users’ estimation concerning the expenses of using m-payments is termed as perceived cost of use (Liu et al., 2019). Excessive usage may discourage users to adopt m-payment services (Zhou, 2011). Prior studies have reported the negative association of perceived cost of use with m-payment usage intention (Liu et al., 2019; Lu et al., 2011; Zhou, 2011). The proposed hypotheses for further validation are as follows.

Methodology

Questionnaire and Scale

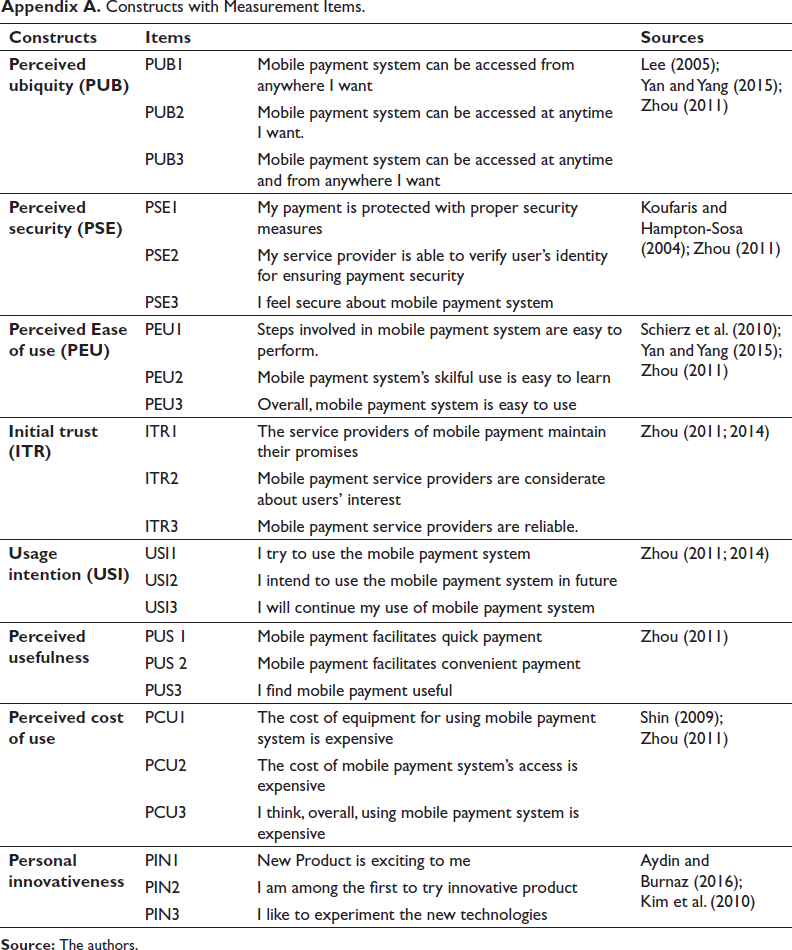

Initially, the measurement items under the constructs were adapted from the previous studies for a pilot test with 20 respondents to confirm the measurement instruments’ validity. Based on the findings of the pilot testing and the final suggestion of the experts in the relevant field, a final structured questionnaire was developed primarily in English and then translated into Bangla (native language) for collecting respondents’ precise opinions. Two sections were included in the questionnaire: section A—containing respondents’ demographic data and section B—containing measurement items. A 5-point Likert scale was used to collect the responses (1 = strongly disagree and 5 = strongly agree). They are presented in Appendix A with legitimate sources.

Sampling Protocol and Data Collection

The data collection process was conducted in Bangladesh’s capital Dhaka city for a duration of 5 weeks (between February 2021 and March 2021). Dhaka is the most privileged city in the country where people from all over the country keep coming to make a living. The population of Dhaka is highly diversified in terms of culture, the standard of living, income, tech know-how, education and profession. Due to the opportunity to gather varied responses and experiences from the users belonging to the different parts of the country, Dhaka has been selected as the sampling location for our study.

Roscoe (1975) recommended that in the case of multivariate research, the number of the sample should be a minimum of 10 times of the items’ number. Kline (2016) reported 200 as a fair sample size and 300 as a good sample size for statistical analysis with structural equation modelling (SEM). However, for further statistical analysis, a total of 297 data were collected based on the judgemental sampling technique. People, with smartphones, who have no prior user experience with m-payment services, were considered the basic parameter for the judgemental sampling technique.

In step 1 of data collection, we asked respondents to use the country’s two leading (anyone of their preference) MFS platforms installed in their smartphones for at least 2 weeks. After 2 weeks, in step 2 of data collection, we started reaching them again and provided them with the questionnaire for collecting their first-time use experience. It took 3 more weeks to collect their user experience.

Common Method Bias

The Harman’s single-factor test was carried out with the help of the IBM SPSS program in order to determine whether or not the data set has any common method bias. The findings showed that common method bias was not a significant issue with the data because the variance of the first factor (31%, which is less than 50%) did not account for the majority of the variance in the data (Podsakoff, 2003; Srivastava et al., 2010). After that, partial least squares (PLS)-SEM was employed for the identification of common method bias based on variance inflation factor (VIF) values. The test result revealed that the model had no common method bias as all of the VIF values were less than 3.3 (Kock, 2015).

Data Analysis

A total data of 297 were given input into Microsoft Excel. After cleaning 13 unengaged data applying the standard deviation method, a total data collection of 284 were given input into SmartPLS software for validating the proposed research model and testing the hypothesized relationships among constructs by applying the PLS method. SmartPLS software was widely applied for the PLS-SEM (Hair et al., 2014).

Results

Demographical Information of the Respondents

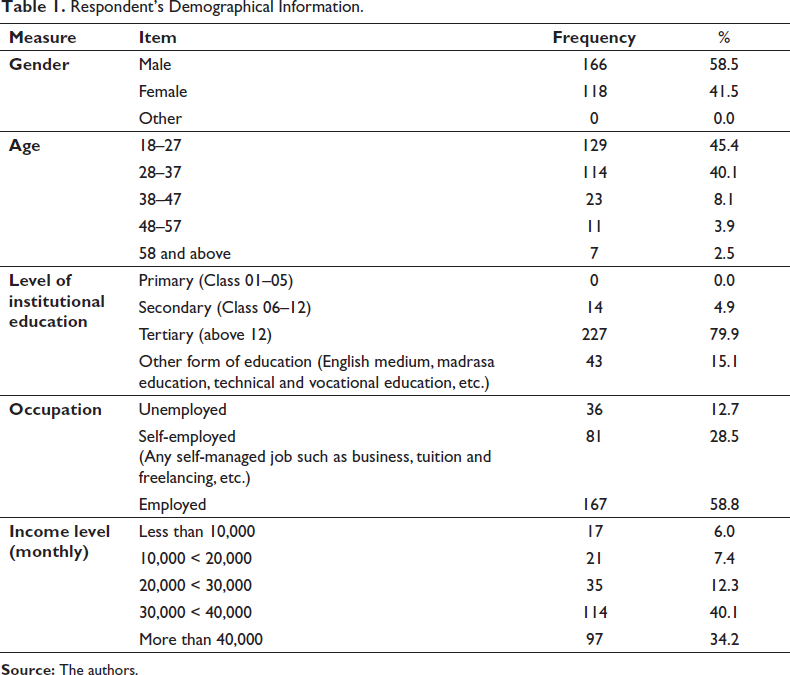

The respondent’s demographical information is presented in Table 1. In terms of gender, most of the respondents using m-payment system among 284 respondents were male with 58.5%, followed by 41.5% of the female respondents. Again, 45.4% of the respondents were from the 18–27 age ranges, which is highest in total. A total of 79.9% of the respondents with tertiary-level education were the majority in proportion. Majority of the respondents were employed (58.8%), and majority (40.1%) of them reported their monthly income between BDT 30,000–40,000.

Respondent’s Demographical Information.

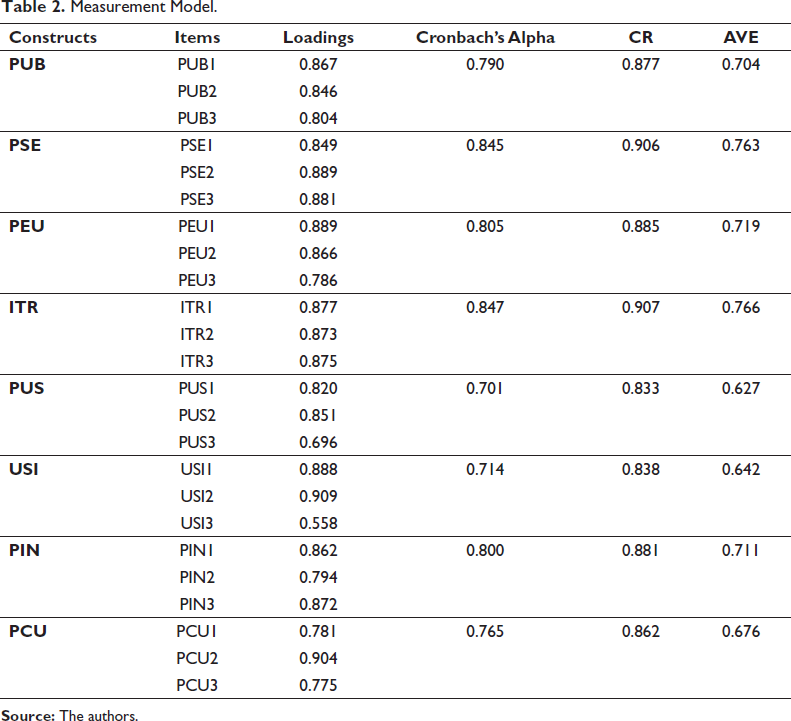

Measurement Model

Internal reliability, convergent validity as well as discriminant validity were examined for analysing measurement model of the study. The Cronbach’s alpha (CA) value and the composite reliability (CR) were considered for evaluating internal reliability of the constructs. For CA and CR, value of 0.70 is considered acceptable (Hair et al., 2006). Further, item loadings and average variance extracted (AVE) were considered for evaluating the convergent validity where value not less than 0.50 can be accepted (Hair et al., 2014). From Table 2, values of loadings—CA, CR and AVE—can be observed. All the CA values were between 0.701 and 0.847, and CR values were between 0.833 and 0.907. It indicated a strong internal reliability of the constructs. However, AVE values were between 0.627 and 0.766 and item loadings were between 0.558 and 0.909, and all of the values were higher than their recommended values. Hence, the model satisfied the convergent validity.

Measurement Model.

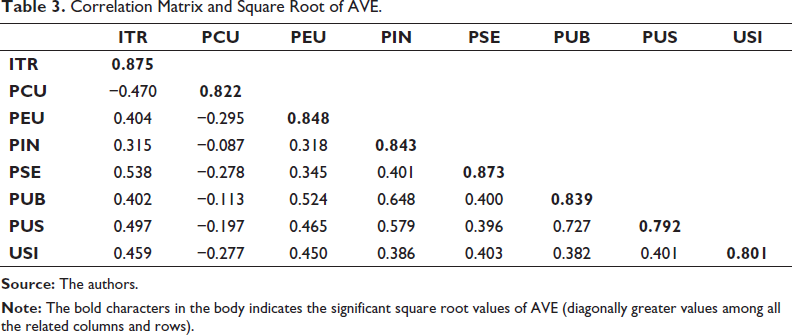

After that, the model’s discriminant validity was checked by the square root of AVE and correlation of the constructs. It is considered that the square root of the AVE of each construct should be higher than the construct’s correlation with other constructs in order to satisfy discriminant validity (Hair et al., 2014), and diagonally, the values must be greater than all the values in related columns and rows (Henseler et al., 2009). Values represented in Table 3 meet all conditions, hence indicating that the model has also satisfactory discriminant validity.

Correlation Matrix and Square Root of AVE.

Structural Model

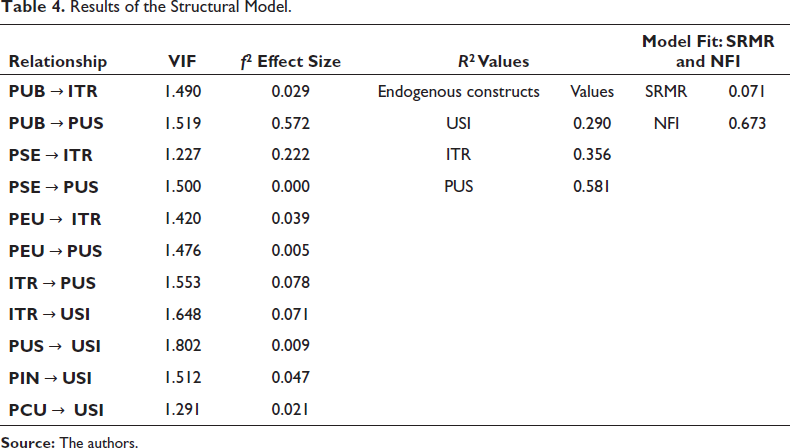

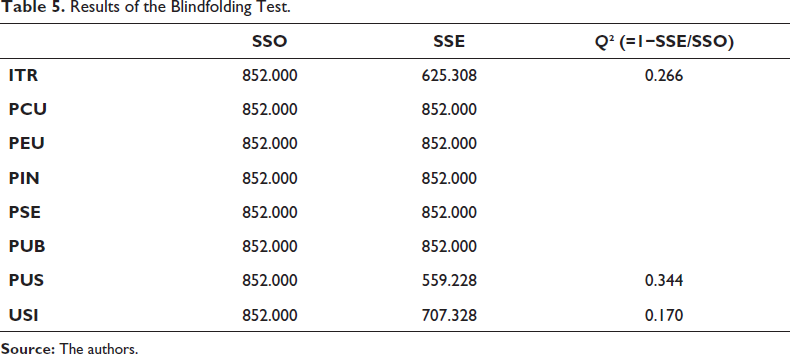

After getting satisfactory results from the measurement model, the structural model was assessed. The inner VIF values, the coefficient of determination (R2) values of the dependent variables, the f2 effect size, the standardized root mean square residual (SRMR) value and the predictive relevance Q2 were examined to evaluate the structural model suggested by Hair et al. (2019). The VIF values were checked to detect whether any collinearity issues existed, and the R2 value was also checked to assess the model’s predictive accuracy. In addition to these, the f2 effect size was examined to assess the impact of a specific exogenous construct’s omission on the R2 value of the endogenous construct. For VIF, value less than 5.00 was considered acceptable, and the recommended value for R2 varies based on the study context, like the value of 0.20 was considered satisfactory in the consumer behaviour discipline (Hair et al., 2014). The acceptable values for small, medium and large f2 effect sizes, respectively, are represented by values higher than 0.02, 0.15 and 0.35 (Cohen, 1988). The inner VIF values of all constructs were between 1.227 and 1.802, indicating that no collinearity issue exists in the study. The R2 value of usage intention was 0.290, revealing that the model is explaining 29% of usage intention to m-payment adoption behaviour, indicating strong predictive accuracy. The R2 values of all other dependent variables, like initial trust and perceived usefulness, were 0.356 and 0.581, respectively. All of the values (except PEU, PSE, PUS having no effect on PUS and USI, respectively) regarding construct effect size were between 0.029 and 0.572, which indicate that small, medium and large effect sizes exist in the model. Again, the SRMR value was checked to evaluate the model fitness (Raman, 2020). The model also satisfied the recommended value of SRMR (less than 0.08) for model fitness (Henseler et al., 2015). All of the results, except the Q2 value associated with the structural model assessment, were reported in Table 4. Finally, the Q2 value was examined to assess the model’s predictive relevance (Geisser, 1974). The values obtained from the blindfolding test with an omission distance of 7 are presented in Table 5. The Q2 value presented in the Table 5 indicates adequate predictive relevance of the model.

Results of the Structural Model.

Results of the Blindfolding Test.

Hypotheses Testing

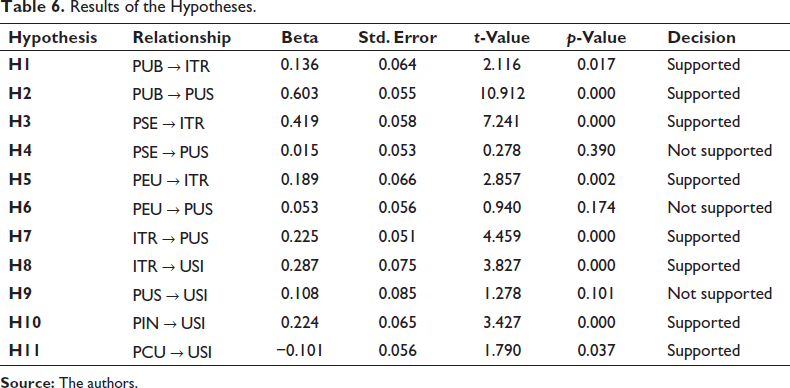

The standardized path coefficient (β), t-value as well as the p-value were examined for evaluating the hypotheses of the study. Table 6 reveals the relationship between PUB and ITR (β = 0.136, t = 2.116, p < 0.05), PUB and PUS (β = 0.603, t = 10.912, p < 0.05), PSE and ITR (β = 0.419, t = 7.241, p < 0.05), PEU and ITR (β = 0.189, t = 2.857, p < 0.05), ITR and PUS (β = 0.225, t = 4.459, p < 0.05), ITR and USI (β =0.287, t = 3.827, p < 0.05), PIN and USI (β = 0.224, t = 3.427, p < 0.05) and PCU and USI (β = −0.101, t = 1.790, p < 0.05). Hence, hypotheses H1, H2, H3, H5, H7, H8, H10 and H11 were supported at the 5% level of significance. In contrast, the relationship between PSE and PUS (β = 0.015, t = 0.278, p > 0.05), PEU and PUS (β = 0.053, t = 0.940, p >0.05) and PUS and USI (β = 0.108, t = 1.278, p > 0.05) were not supported at the 5% level of significance.

Results of the Hypotheses.

Mediation Analysis

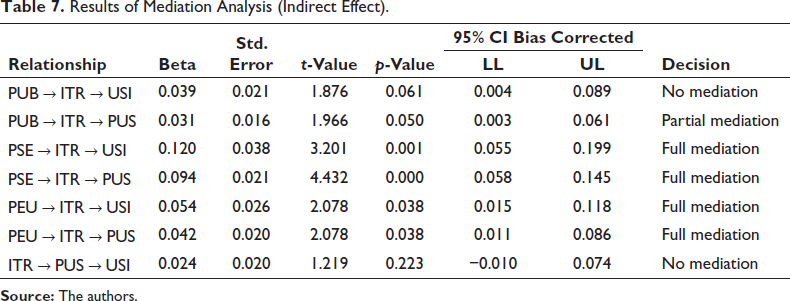

For mediation analysis, indirect effects of initial trust (mediator) on perceived usefulness and m-payment usage intention were assessed using the bootstrapping method (Preacher & Hayes, 2004; 2008). Table 7 reveals the result of mediation analysis: PUB→ITR→USI (β = 0.039, t = 1.876, p > 0.061), PUB→ITR→PUS (β = 0.031, t = 1.966, p > 0.050); PSE→ITR→USI (β=0.120, t = 3.201, p > 0.001); PSE→ITR→PUS (β=0.094, t = 4.432, p > 0.000); PEU→ITR→USI (β = 0.054, t = 2.078, p > 0.038); and PEU→ITR→PUS (β = 0.042, t = 2.078, p > 0.038). All the indirect effects of initial trust are statistically significant, except PUB→ITR→USI. The result indicates that initial trust does not mediate the association between perceived ubiquity and usage intention as the direct effect is significant. Initial trust partially mediates the association between perceived ubiquity and perceived usefulness as direct effect is significant too. The result also indicates that initial trust fully mediates all the other associations among perceived security, perceived ease of use, perceived usefulness and usage intention since the direct effects are insignificant. Therefore, it can be concluded that initial trust has significant mediation effects in the case of m-payment usage intention. Moreover, perceived usefulness has no significant mediation effects on the association between initial trust and usage intention (ITR→PUS→USI) as direct effect of ITR is significant but the indirect effect is insignificant.

Results of Mediation Analysis (Indirect Effect).

Discussion on Findings

This study was undertaken to spot the determinants of initial trust in the case of first-time m-payment users in Bangladesh and to identify whether their initial trust has any consequential influence over m-payment usage intention. The results show that perceived ubiquity, perceived security and perceived ease of use are the determinants of initial trust. The results indicate that if ubiquity, security and ease of use can be ensured, the potential users will start believing the service providers. If service providers fail to ensure the features, they will not be able to convince the potential users. The findings are compatible with the previous findings—the positive effect of perceived ubiquity on initial trust (Zhou, 2011; 2014); the positive effects of perceived security on initial trust (Zhou, 2011); and the positive effects of perceived ease of use on initial trust (Zhou, 2011). The result of the current study also shows that initial trust has a significant association with perceived usefulness and usage intention. It provides insights that initial trust helps developing customers’ perception of usefulness of m-payment services in a positive manner and also helps in intensifying usage intention of m-payment services. The findings are compatible with the prior findings—the positive effects of initial trust on perceived usefulness (Talwar et al., 2020; Zhou, 2011) and usage intention (Gao & Waechter, 2017; Zhou, 2011; 2014).

While conducting the survey, we found that most of the m-payment non-users were employed (58.8%), and they were educated enough (79.9% with tertiary-level education). It was quite unanticipated because this class of people was supposed to be innovative enough to adopt technological changes. However, responses collected through the questionnaires reflect their justification for not adopting m-payment until we insist that they use the service. They prefer ubiquitous connectivity in order to access the service at any time and from any location. They feel their confidential information needs protection, and they are well concerned about the security of their confidential information while using the service. Moreover, they want a user-friendly interface and unparalleled quality in service, which will allow uncomplicated and sophisticated operations. Users from different parts of the world reported similar requirements from the m-PSPs. A study by Yan and Yang (2015) and Shao et al. (2019) found ubiquity or mobility of service as one of the major determinants of m-payment usage intention to the Chinese users. A qualitative study by Mallat (2007), in the context of Finland, revealed that reliable and well-established service providers are better accepted among the users since they are able to build trust and reduce the perceived risk of using m-payment services. Malaysian m-payment users expressed their readiness to use m-payment systems only if they found it safe and secure with their confidential information (Yan et al., 2009). Irish users also preferred safe and reliable m-payment services (Duane et al., 2014). Security was again reported as the prerequisite to m-payment adoption by the users from Hong Kong (Wong & Mo, 2019) and China (Shao et al., 2019). Srivastava et al. (2010) reported that effortlessness of using m-payment determines its adoption intention to the users in Singapore. Similar finding was reported in the case of Chinese users (Yan & Yang, 2015), whereas Zhou (2013) and Dlodlo (2014) reported service quality as a significant prerequisite to continuous m-payment usage intention consecutively in China and South Africa.

Prior studies have validated the significant relationship between perceived security and perceived usefulness (Zhou, 2011) between perceived ease of use and perceived usefulness (Kim et al., 2010; Liu et al., 2019; Srivastava et al., 2010; Zhou, 2011) and between perceived usefulness with usage intention (Liu et al., 2019; Talwar et al., 2020; Zhou, 2011). However, we found these associations as insignificant. Only perceived ubiquity was found to be positively affecting perceived usefulness in our study, and it is consistent with the findings of Zhou (2011). The insight of the finding is that in the case of a financial tech service, ubiquitous serviceability is more critical to the development of the perception of usefulness among the users than perceived security and ease of use. People expect m-payment services to be accessible from any location at any time because consumers care about convenience while using financial technology. However, perceived security and ease of use, as well as perceived ubiquity, are important in the development of initial trust among potential m-payment users.

Moreover, personal innovativeness and perceived cost of use were found to have a direct significant effect on usage intention consecutively in a positive and negative way. Our findings are consistent with the previous findings—positive effect of personal innovativeness on usage intention (Kim et al., 2010) and negative effect of perceived cost of use on usage intention (Liu et al., 2019; Lu et al., 2011; Zhou, 2011). People in Bangladesh are enthusiastic enough to embrace new technologies, and they have no inertia in receiving m-payment as their regular means of financial transactions. However, cost is a barrier to m-payment usage intention. As most of the people in Bangladesh belong to low- to mid-income group, they prefer value for money from a service. We have observed that 40.1% of the respondents of our study earn BDT 30,000–40,000 per month, which is good enough for living in the context of Bangladesh. Even these people had never shown any interest to m-payment until we let them use the service. It indicates that a cost-effective m-payment service can substitute their habit of traditional financial activities.

The result of the mediation analysis shows initial trust’s significant mediation effects in the case of perceived usefulness and m-payment usage intention, and it is consistent with the findings of Zhou (2011). This highlights the importance of focusing on the development of initial trust by the service providers to capture the potential market shares.

Implications

Theoretical Implication

Theoretically, this study makes a contribution to the literature on the adoption of m-payment systems. Previously, there had been very few research attempts to investigate the impact of initial trust in the case on m-payment usage intention and adoption in different countries. However, to the best of our knowledge, this study is the first attempt at research undertaken to analyse the impact of initial trust on m-payment usage intention in the context of Bangladesh. Since it reports the significance of building initial trust to influence m-payment usage intention in the case of the potential users, future researchers in related study areas will get literature support and insights on the research direction. Moreover, we have added a new control variable (personal innovativeness) to the research model of Zhou (2011) and proposed the extended model for our study purpose, and it was found significantly effecting m-payment usage intention. Hence, theoretically, this extension will also contribute to the literature.

Managerial Implication

The findings of the study provide useful guidelines for existing and potential m-PSPs as well as practitioners in the field. In Bangladesh, m-PSPs are gradually capturing the consumer market with their immense competitive moves. Therefore, it is imperative for the service providers to concentrate on the significant determinants of m-payment adoption in order to maximize users’ perceived benefits. The findings of the current study offer an understanding of a very critical cognitive measurement in the case of m-payment adoption in Bangladesh, which is initial trust. The study offers the insight that initial trust can be a novel way of measuring m-payment users’ perceived benefits in the context of developing economies like Bangladesh. The study shows initial trust’s significant influence on m-payment adoption decisions as well as the meaningful influence of perceived ubiquity, perceived security and perceived ease of use in the development of initial trust. Therefore, the findings suggest that service providers have to warrant ubiquitous, secured and uncomplicated m-payment services to ensure initial trust development and to encourage usage intention. To do so, for instance, they can take measures to be transparent and easily reachable by establishing an experience centre and customer service points at customers’ doorsteps. Customers’ queries should be solved in no time with a customized service design. They should make customers feel special by giving special attention and priority to service experience irrespective of customers’ genres. Moreover, positive reviews obtained from the users should be promoted on a regular basis by leveraging their presence on social media. Competitive advantages can be obtained by organizing loyalty programmes for building initial trust among the m-payment service users. The findings suggest that, as m-payment services are primarily associated with the financial transactions, users’ credentials should be dealt with the highest priority with no compromise. Service providers should try to get certification from the financial regularity authorities regarding the reliability of their process and partner with global fintech service providers. The steps involved in the m-payment apps should be minimized and simplified for better navigation and an easy-going experience for the users. Bulky and highly data-consuming features should be avoided along with some offline features to ensure a smooth user experience. Moreover, service providers can engage in various CSR programmes to enhance their social presence, positive brand image and trustworthiness. In the current study, the cost of using the m-payment is also found to create a barrier to the m-payment’s usage intention. So, the results suggest that m-payment service fees should be kept at a reasonable level for users, and that cost-effectiveness should be a key factor for service providers who want to get ahead of the competition.

Limitations of the Study and Scope of Future Research

There are some limitations in our study despite its distinctiveness. First, we have picked the sample from the capital city of Bangladesh only. The selection of a more diversified sample group and size from other areas of Bangladesh may lead to different findings. Second, the study was conducted in the context of Bangladesh; thus, the study results could be different in the case of countries with unlike economic conditions. Third, the study has considered only three antecedents of initial trust such as perceived ubiquity, perceived security and perceived ease of use. Effects of other antecedents of initial trust (i.e., performance expectancy, effort expectancy, social influence, facilitating conditions, etc.) may result in dissimilar outcomes. Fourth, we observed the effect of only two control variables on usage intention regarding m-payment like perceived innovativeness and perceived cost of use. Effects of other control variables (i.e., age, income, self-efficacy, technology anxiety, etc.) on m-payment usage intention may provide additional significant insights. Hence, future studies should be conducted avoiding the limitations of the current study.

Conclusion

The factors determining initial trust and initial trust’s effects on m-payment usage intention were investigated in this study. The study population was Bangladeshi natives, especially from the capital (Dhaka), who had no prior experience of using m-payment services. Respondents were asked to use two of the country’s leading MFS platforms before providing their first-time use experience to us, and a structured questionnaire with eight constructs was employed to collect their experience or responses on a 5-point Likert scale. Based on the analysis, using the SEM method, we found perceived ubiquity, perceived security as well as perceived ease of use as significant factors positively affecting the user’s initial trust; consequently, initial trust determines perceived usefulness and also usage intention. Initial trust’ mediation effect was found to be significant. Moreover, the relationship of perceived innovativeness and perceived cost of use with m-payment usage intention was found consecutively positively significant and negatively significant. The findings imply that m-PSPs in Bangladesh should take effective measures to influence the initial trust perception of the potential users regarding their services to increase their market share.

Constructs with Measurement Items.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was partially supported by Research Cell of Noakhali Science and Technology University, Bangladesh (NSTU/RC/20/B-141).