Abstract

This study, utilizing bank-level data for India, investigates the relationship between funding liquidity and banks’ risk-taking behavior. The study uses two risk measures: risk-weighted assets (encompassing credit, market, and operational risk) and liquidity creation (encompassing intermediacy risk). Findings reveal that banks with higher funding liquidity exhibit higher risk-taking behavior. This risk-taking behavior is more pronounced during economic recuperation and expansionary monetary policy phases. Notably, during economic recuperation, banks display heightened intermediacy risk, contrasting with the absence of such evidence during expansionary monetary policy phases. Larger banks with higher deposit shares demonstrate lower risk-taking behavior. Additionally, banks with a return on equity (ROE) below the average ROE exhibit a proclivity for increased risk-taking. This study advocates for liquidity regulation as a crucial complement to bank capital regulation, offering empirical support for moderate risk-taking among highly liquid banks and fortify their balance sheets for a stable banking system in India.

1. Introduction

The liquidity shortage during the global financial crisis (2007−2009) played a pivotal role in the failure of various financial institutions, notably banks (DeYoung & Jang, 2016; Hong et al., 2014). In response to such vulnerabilities, Basel III implemented liquidity and funding risk management measures, including the liquidity coverage ratio (LCR) and net stable funding ratio (NSFR) (BCBS, 2010). The LCR, a short-term liquidity requirement, aims to protect banks from funding liquidity risk and mitigates the risk of bank runs. On the other hand, the NSFR serves as a long-term risk measure to decrease the likelihood of bank failures (Vazquez & Federico, 2015). Notably, raising stable funds to comply with NSFR is a costly endeavor for banks (King, 2013). Given that interest income from loans constitutes a primary source of permanent revenue for banks, they may be incentivized to undertake higher risks by extending loans to riskier borrowers offering higher returns, thereby increasing profits.

To address excessive risk-taking behavior, Basel III introduced liquidity regulation in addition to existing capital regulation. Capital regulation diminishes incentives for credit, market, and operational risk-taking, while liquidity regulation curtails intermediacy risk. Both regulations may impact a bank’s risk-taking behavior in opposing directions. For instance, a well-capitalized bank with ample funding liquidity may invest in relatively less risky assets over a more extended period, thereby increasing intermediacy risk.

A theoretical principal−agent framework by Acharya and Naqvi (2012) suggests that managers may be inclined to take risks when there is abundant funding liquidity, as measured by total deposits, for the prospect of higher returns. Empirical evidence from studies such as Khan et al. (2017) for banks in the United States (US) and Dahir et al. (2018) for BRICS countries (Brazil, Russia, India, China, and South Africa) supports the contention that lower funding liquidity risk, indicative of higher funding liquidity, is associated with increased risk-taking by banks.

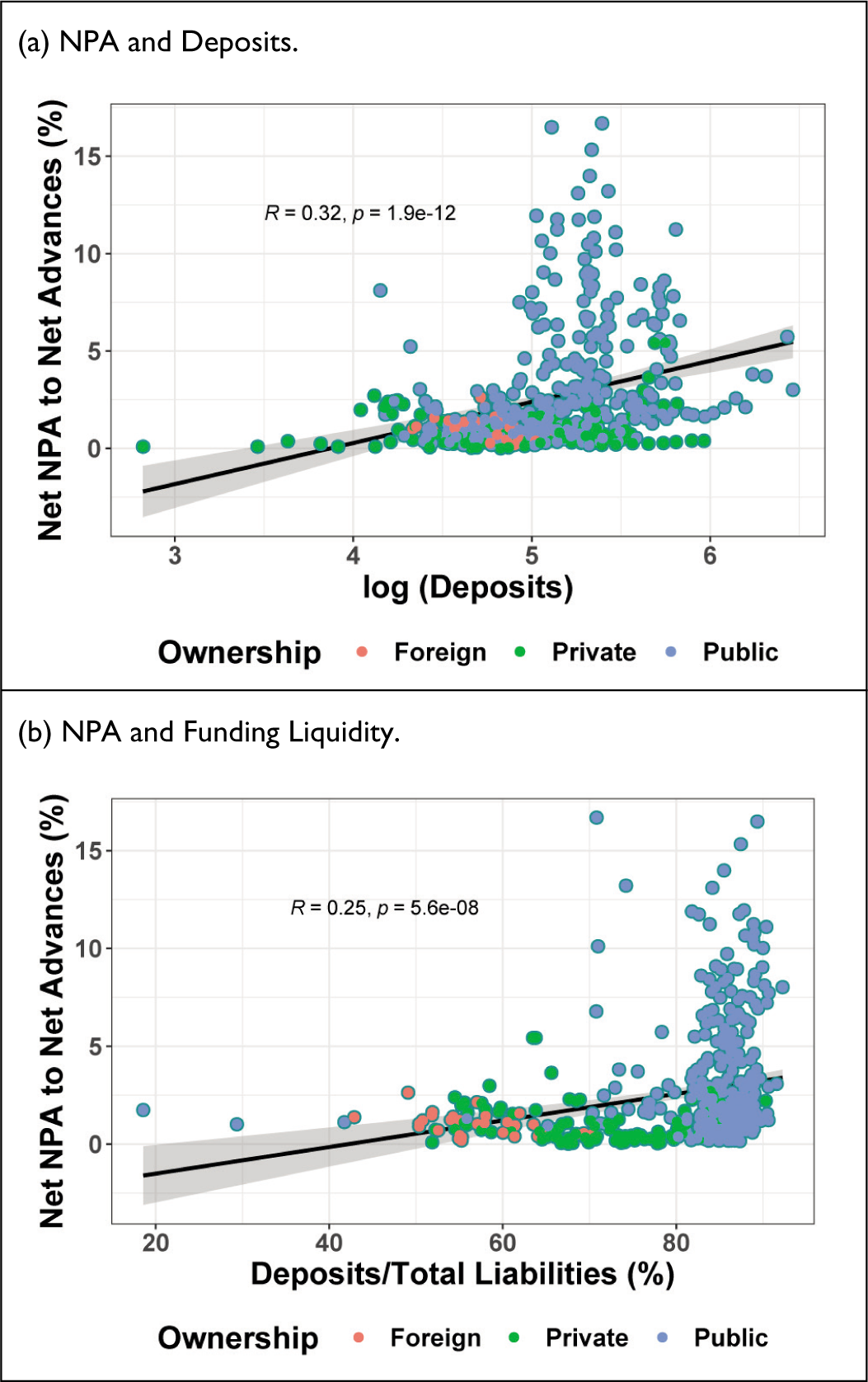

In Indian contexts, following the implementation of the Narasimham Committee recommendations in 1991, banks experienced a period of exceptionally high deposit growth, averaging nearly 18% on a year-on-year basis. This robust growth continued until the global financial crisis of 2007−2009. In the post-crisis period, deposit growth moderated to a level of around 11%. Looking at non-performing assets (NPAs), from March 2015 to March 2018, the gross NPAs of the Indian banking system more than doubled, soaring to 11.5% of the total advances within the banking sector. Notably, Public Sector banks (PSBs) bore the brunt with their gross NPAs peaking at a staggering 14.6%, while net NPAs hovered around 8.5%. There is also a strong correlation between NPAs and banks deposits (Figure 1). This underscores the need to examine the risk-taking behavior of Indian banks in the context of funding liquidity. There is a notable dearth of studies exploring a crucial macroprudential implication—the correlation between funding liquidity and bank risk-taking behavior. This study empirically investigates whether elevated funding liquidity corresponds to increased risk-taking among Indian banks, utilizing a panel data sample comprising the top 30 banks ranked by their credit share. Our contribution to the literature lies in the comprehensive examination of three dimensions of the risk-taking channel: (i) state-dependent risk-taking behavior influenced by macroeconomic conditions; (ii) performance-based risk-taking behavior; and (iii) risk-taking behavior contingent on systemic importance.

We assess two distinct types of risk—credit risk and intermediacy risk, aligning with established literature practices (e.g., Dahir et al., 2018; Khan et al., 2017). First, we employ risk-weighted assets (RWAs), a fitting proxy for credit risk considering its incorporation of market and operational risk. Second, we utilize liquidity creation (LC) as a proxy for intermediacy risk (Berger & Bouwman, 2009). As these two risks may not always correlate, a dedicated empirical examination for credit risk and intermediacy risk becomes imperative.

Our findings affirm that banks with higher funding liquidity, proxied by the deposit-to-total-liabilities ratio, exhibit heightened levels of both credit risk and intermediacy risk in India. The econometric analysis controls for various factors, such as accumulated non-performing loans, size, and risk-taking habits, to ensure robust statistical conclusions. Considering state-dependent factors, it is noteworthy that during crises like the global financial crisis (2007−2009), if the efficient equilibrium prevails (i.e., depositors remain calm without simultaneous withdrawals in the Diamond and Dybvig (1983)), banks may adopt a risk-averse stance, refraining from undertaking risky investments despite having ample liquidity (Odonkor et al., 2016). To investigate this, our study examines the influence of funding liquidity on risk-taking in distinct economic states—specifically, economic slowdown and recovery phases. Additionally, we extend this analysis to monetary policy phases, observing that banks assume higher credit risk during monetary expansion phases when ample liquidity is present. In contrast, this behavior is absent during tight monetary policy phases. This alignment with the risk-taking channel of monetary policy transmission supports previous literature (Altunbas et al., 2014; Gambacorta, 2009).

Furthermore, the study considers the influence of a bank’s performance relative to its peers. Underperforming banks, aiming to enhance shareholder returns, exhibit a proclivity for higher risk-taking when equipped with ample funding liquidity. In addition, we explore the impact of deposit market share. A bank’s balance sheet in financial markets is predominantly shaped by deposits, making deposit share an indicator of its size and the trust depositors place on the bank. Our study reveals that banks with a higher deposit share exhibit a more prudent risk-taking behavior, underscoring the cautious approach of large banks and the benefits of regulatory oversight.

The structure of the study is as follows. In Section 2, a review of pertinent literature on funding liquidity and risk-taking behavior is presented, yielding testable hypotheses tailored to the Indian context. Section 4 delineates the study’s hypotheses, outlines the dataset, and employs an appropriate econometric methodology to scrutinize the hypotheses. Finally, Section 5 encapsulates the study’s findings, drawing conclusions from the empirical analysis, and delving into macroprudential policy implications.

2. Related Literature

The International Monetary Fund (IMF) defines funding liquidity as “the ability of a solvent institution to make payments in a timely fashion” (IMF, 2008). In the literature, funding liquidity is characterized as the immediate settlement ability of a solvent financial institution for its current obligations, while funding liquidity risk represents the likelihood that the institution cannot meet its obligations promptly (Drehmann & Nikolaou, 2013). Other studies define funding liquidity as a financial institution’s capability to raise cash, specifically for banks to address depositors’ liquidity demands (Brunnermeier & Pedersen, 2009). The literature often measures funding liquidity by the ratio of deposits to total liabilities (Acharya & Naqvi, 2012; Dahir et al., 2018; Khan et al., 2017). Ample studies discuss banks’ risk-taking behavior from various perspectives, such as the risk-taking channel of monetary policy transmission, deposit insurance and bank risk-taking, and liquidity risk and bank risk-taking (Altunbas et al., 2014; Gambacorta, 2009; Keeley, 1990). Banks’ risk-taking behavior is influenced by institutional and contract design factors, including deposit insurance, shareholders’ incentives, and managers’ payoff contracts (Jeitschko & Jeung, 2005). Deposit insurance, as an institution, covers a portion of depositors’ savings, introducing moral hazards through the extension of risky loans (Keeley, 1990). The design of the manager’s payoff contract can also influence risk-taking behavior; for instance, if the manager’s benefits contract is linked to higher bank profits, they may engage in investing in riskier assets, a manifestation of moral hazard. When there is a strong penalty in the form of reduced benefits for significant credit defaults, managers have less incentive to extend credit to risky borrowers. Thus, the design of the payoff contract is a crucial factor in determining risk-taking behavior (Acharya & Naqvi, 2012).

Given that deposits represent households’ hard-earned money, banks need to be regulated to prevent excessive risk-taking. The BCBS provides a standardized framework for banking regulation and supervision, initially focusing on capital regulation and later introducing liquidity regulation (BCBS, 2010). Capital regulation mandates that banks hold more capital when they have a riskier credit portfolio (Shim, 2013). The relationship between capital and risk-taking behaviour is debated in the literature, with some studies finding that banks with higher capital may take higher risks (Shrieves & Dahl, 1992), while others propose a U-shaped relationship (Calem & Rob, 1999).

Liquidity regulation, introduced post global financial crisis (2007−2009), helped in moderating the failure of banks due to liquidity crises (DeYoung & Jang, 2016; Hong et al., 2014). Ivashina and Scharfstein (2010) show that during the financial crisis, banks depending on deposits for extending credit were less affected than those relying on short-term debt. Larger banks, with a greater ability to raise funds, have an advantage (Bertay et al., 2013). However, the “too big to fail” argument suggests that the failure of large banks incurs substantial costs for the economy, necessitating stringent regulations to discourage excessive risk-taking by these entities (Abbas et al., 2020). Larger banks, being more stable and holding higher regulatory capital in Asia’s emerging economies, may be less inclined to take risks (Abbas et al., 2020). The size of a bank also influences its stability, with larger banks exhibiting higher Z-scores, 1 indicating greater stability (Mercieca et al., 2007).

There is limited research on credit risk in Indian context. In a threshold analysis, Bardhan et al. (2019) finds that above certain level of capital adequacy ratio (CAR) and credit growth, Indian banks tend to lower risk. Sarkar and Sensarma (2016) show that higher competition leads to lower market and asset risk but higher funding liquidity risk. Nevertheless, the literature on funding liquidity and bank risk-taking in the Indian banking sector remains scarce, forming the main objective of this study to fill this research gap.

3. Testable Hypotheses

The study specifically explores two distinct types of risks—credit risk and intermediacy risk. The credit risk pertains to the potential default on loans, adversely affecting a bank’s balance sheet, while intermediacy risk involves the bank’s decision to employ liquid liabilities to generate illiquid assets, posing a risk to the continuity of the bank’s intermediary services. Therefore, a comprehensive examination of their relationship with funding liquidity necessitates considering both types of risks.

We also investigate our primary hypothesis from the perspective of monetary policy. To facilitate liquidity, the monetary authority typically reduces the policy rate. If this lower policy rate persists, banks may seek higher yields, prompting them to extend credit to riskier sectors in pursuit of higher returns (Rajan, 2006). This phenomenon is recognized in the literature as the risk-taking channel of monetary policy transmission, wherein banks increase lending to risky borrowers during expansionary monetary policy phases (Borio & Zhu, 2012; Gambacorta, 2009). Consequently, the surge in liquidity could potentially lead to higher intermediacy risk across different monetary policy phases. We systematically examine the risk-taking channel during both expansionary and tight monetary policy periods.

Subsequently, we explore various phases of the business cycle to scrutinize whether banks engage in higher risk-taking behavior under different economic conditions. Banks may find an incentive to extend credit based on optimistic future expectations. Supporting this notion, Shim (2013) presents evidence that bank default risk is lower during economic booms. During prosperous economic phases, borrowers’ enhanced “ability to pay” may also lead to lower credit defaults, assuming borrowers are not acting as wilful defaulters. The economic recovery phase presents a favorable environment for heightened risk-taking. Another plausible reason for increased risk-taking during boom phases is the lower funding liquidity risk, attributed to higher cash flows of firms.

Conversely, during economic slowdown phases, banks may adopt a risk-averse stance owing to lower net worth of borrowers and economic uncertainties. Consequently, it becomes crucial to scrutinize whether banks exhibit a proclivity for higher risk-taking during economic expansionary phases compared to economic slowdown phases.

Now, we turn our attention to one of the pivotal services offered by banks—the intermediary service, encompassing the acceptance of deposits and the ability to meet depositors’ liquidity demands promptly. In the event of a failure to provide this service, banks could face unanticipated cash withdrawals, potentially triggering bank runs. Within the deposit market, a bank boasting a substantial share of household deposits indirectly signifies a higher level of depositor trust. This trust could stem from various factors, including the bank’s size, effective liquidity management history, extensive branch network with cash withdrawal services, or superior product designs. Given the critical role these banks play as financial intermediaries for households, ensuring a robust depositor trust is paramount. Consequently, these banks are expected to exercise caution and take on lower intermediacy risk.

However, a potential counterargument arises based on our premise that banks with higher deposit shares might engage in riskier activities, assuming depositors will not immediately withdraw funds due to their trust in the bank. Our investigation aims to ascertain whether banks with higher deposit shares, implicitly indicating greater depositor trust, indeed exhibit a propensity for higher risk-taking. This analysis holds significance from a policy perspective, particularly for large and systemically important banks.

From a managerial perspective, banks may engage in risky investments if the return to shareholders falls below the industry’s average return. This aligns with the argument presented by Jensen (1986) in a principal−agent framework, where the manager’s incentive to invest in risky assets is heightened if their payoff is explicitly tied to the return on capital. In this study, we consider two metrics for assessing the return on equity (ROE). First, we examine it based on the book value of equity, and second, we evaluate the return on stock prices in the capital market.

The first measure, derived from the book value of equity, holds particular significance as shareholders wield substantial influence over managerial decisions. Shareholders provide future guidance and closely monitor managers, exerting more direct control than stock market participants. Although stock market participants may not engage in direct managerial oversight, they price the bank’s stock based on managerial decisions (Falato & Scharfstein, 2016). Consequently, any unfavorable or risky actions, publicly observable, may swiftly manifest in the stock price. Thus, a manager cannot entirely disregard the stock market performance of their bank. For empirical examination, we propose the following hypothesis:

4. Empirical Analysis

4.1 Data and Methodology

The empirical analysis utilizes data sourced from the Statistical Tables Relating to Banks in India (STRBI) provided by the Reserve Bank of India (RBI). The sample comprises 30 banks selected based on their credit share during the 2018−2019 financial year. Collectively, these banks capture more than 90% of the total credit in India. The dataset includes annual bank-level information spanning from the financial year 2004−2005 to 2018−2019 (as of March), the pre-COVID-19 period.

In the empirical analysis, funding liquidity is defined as the ratio of deposits to total liabilities, a definition commonly employed in the literature (see, e.g., Khan et al., 2017; Tran, 2020). A higher funding liquidity ratio indicates lower funding liquidity risk. For risk measures, the natural logarithm of risk-weighted assets (RWAs) is utilized as an ex-ante measure for credit, market, and operational risk. Due to the unavailability of direct measures for RWAs, we derive the measure for RWAs from publicly available variables—capital and capital to risk-weighted assets ratio (CRAR) using the following formula:

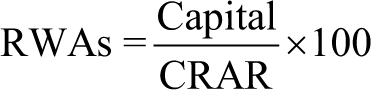

The RWAs defined above could serve as a proxy for an ex-ante measure of credit risk. On the right-hand side of Figure 2(a), it is evident that funding liquidity decreased from 90% to approximately 87% and remained stable until 2013. Subsequently, it declined further to around 83% until 2016 before experiencing an upward trend, ultimately reaching the 2013 level. The RWA to total assets ratio declined during the pre-Global Financial Crisis (GFC) period and sharply increased from 2016 onwards (Figure 2a). The decline and stability of RWA density until 2016 may be attributed to the implementation of Basel III in the aftermath of the GFC.

To assess intermediacy risk, LC is employed. The LC of a bank gauges its decision to generate illiquid assets using liquid liabilities. This is achieved by acquiring illiquid bonds and offsetting it by selling liquid deposit contracts. When banks possess a substantial amount of illiquid assets, they may encounter challenges in promptly meeting liquid demands from depositors, such as unexpected withdrawals. In such instances, the bank may fail to fulfil its role as an intermediary. We measure the LC as proposed by Berger and Bouwman (2009):

This is cat nonfat version of LC which does not take into account off-balance sheet items. Illiquid assets refer to advances with a maturity exceeding one year, while liquid assets pertain to advances with a maturity less than or equal to one year. Detailed classification of a bank’s asset and liability items is provided in Appendix A. The right-hand plot in Figure 2(b) illustrates that LC increased until 2014 and subsequently started declining. The decline observed since 2015 could be attributed to the gradual implementation of the LCR by the RBI from 2015 onwards. It is crucial to note the discontinuity in RWA density and liquidity creation from 2009 to 2014. During this period, RWA density remained low and stable, while LC gradually increased. This might be indicative of banks investing in relatively safer assets with longer maturity.

4.2 Macroeconomic Environment

We consider monetary policy and business cycle phases as state of the economy. For monetary policy phases, we consider the Hodrick–Prescott filter (HP filter) to estimate the cyclical component r˜t by taking the monetary policy repo rate announced by the RBI. Then we say phases with r˜t < 0 as the phases of expansionary monetary policy. Considering the above identification, for econometric analysis, the monetary policy phase dummy MPt is defined as

In the later part, we examine whether banks take risk during the expansionary monetary policy phase in time t for funding liquidity in time t − 1. This will identify the role of different phases of monetary policy. Next, we define the business cycle recovery dummy in the time period t. Similar to monetary policy, we obtain an output gap y˜t using the HP filter. To capture the recovery phases, we consider a dummy BCRt defined as follows:

Notice that, instead taking y˜t, we have taken Δy˜t to partition the recovery phases. The reason behind taking the above specification is to avoid a downward fall in the cyclical component just after the crest. Moreover, the region just after the trough and before the crest in a business cycle is the phase where government and monetary authority intervene to fuel up the economic recovery by maintaining price stability. The market value of the firms also improves which leads to further investment. Once the recovery starts, uncertainty gets reduced and future business sentiment improves. In these phases, banks with adequate funding liquidity might take the risk by extending credit to the riskier sector for higher returns.

Based on the above argument on bank funding and risk-taking, the dynamic panel methodology has been used to examine the hypotheses discussed Section 3 (Arellano & Bond, 1991; Blundell & Bond, 2000). The reason behind choosing the dynamic panel is to address the issues related to endogeneity. As usual in a standard format, the independent variables include the lagged values of the dependent variable, measure for funding liquidity, and other explanatory variables.

Here, Ri,t represents a measure for risk: the logarithms of the RWAs derived in Equation (1) and liquidity creation in Equation (2) for bank i in time t. Li,t represents funding liquidity measure defined by total deposits to total liabilities for bank i in time t. MPt represent dummy for different monetary policy phases as defined in Equation (3) at time t. Similarly, BCRt is a dummy that shows economic recovery phases defined by Equation (4) at time t. And Xi,t represent other bank specific characteristics such as size, capital, non-performing loans, and so on. The regression has been controlled for time and bank fixed effects. Other control variables are, profitability defined by return on advance adjusted to cost of funds, and asset quality defined by net NPA to net advances.

Here, it is important to note that RWA represents the weighted average of bank credit based on their risk-weights. Therefore, any change in RWAs may result from alterations in assets and substitution. For instance, a bank might not extend additional credit but shift existing credit from a lower risk-weighted category to a higher one. In this scenario, even though total advances remain constant, the bank has effectively taken on higher credit risk. To control for this substitution effect, the study incorporates bank size, proxied by the logarithm of total assets, as an independent variable. Building on the risk-absorption hypothesis proposed by Bhattacharya and Thakor (1993), which posits that banks with higher capital may have the incentive to take on greater risks due to an increased risk appetite, the study explores the impact of capital adequacy on risk-taking.

4.3 Results

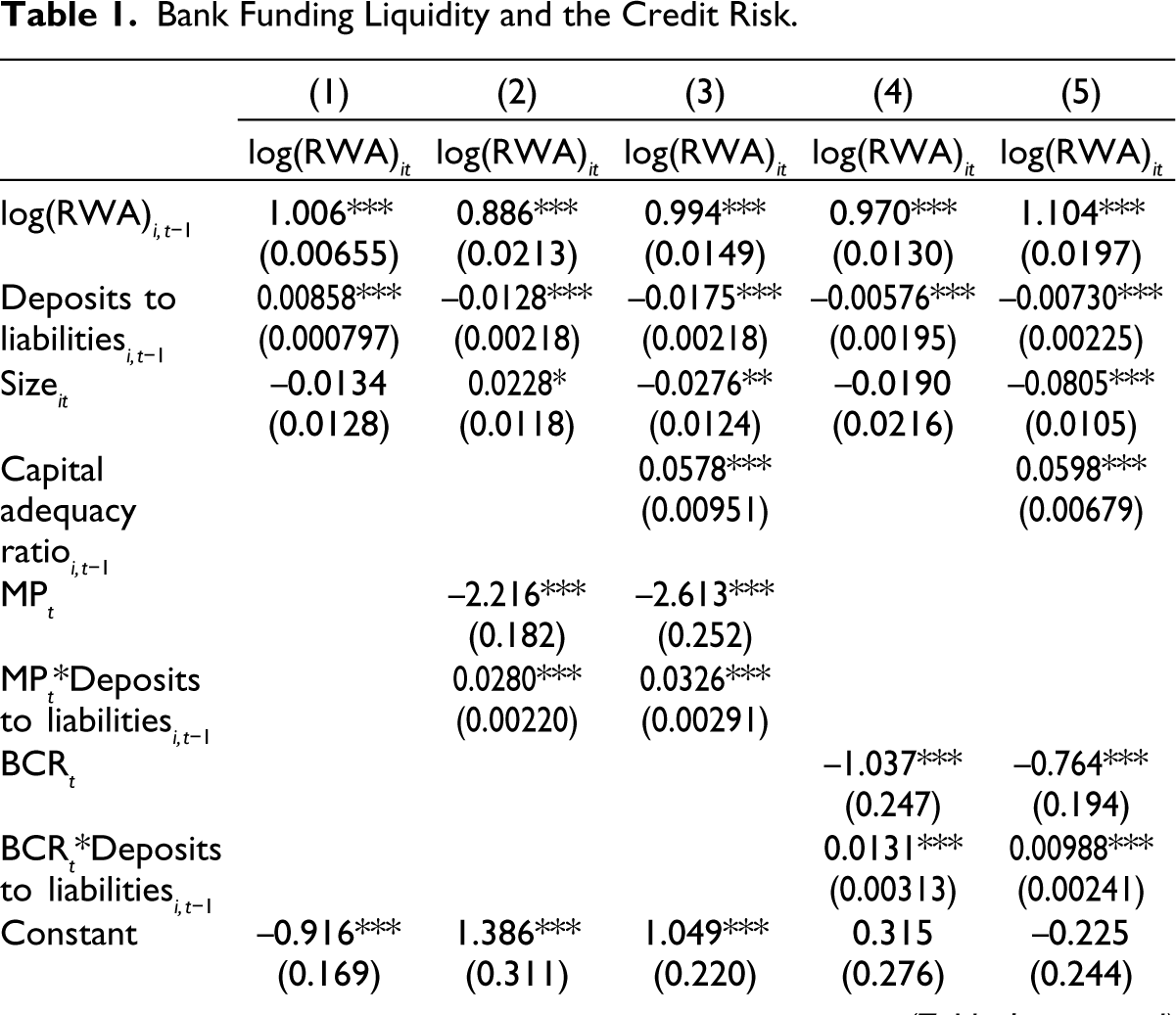

The results presented in Table 1 indicate that in India, higher bank funding liquidity is associated with increased credit risk-taking. Moreover, the magnitude of the funding liquidity coefficient tends to rise during periods of low monetary policy. This finding aligns with the risk-taking channel of monetary policy transmission. Similarly, during economic recovery phases, banks with higher funding liquidity exhibit a higher risk appetite compared to economic slowdown phases. In summary, banks in India demonstrate a proclivity for risk-taking when they possess sufficient funding liquidity. This behavior is more pronounced during expansionary monetary policy and economic recovery phases. Additionally, banks with higher capital tend to take on more risk, supporting the risk-absorption hypothesis. Consequently, banks with elevated CARs and a significant share of deposits require close prudential monitoring to mitigate potential risk-taking behaviors.

Bank Funding Liquidity and the Credit Risk.

To analyze intermediacy risk-taking behavior, the study employs liquidity creation as a proxy for intermediacy risk, investigating whether banks with higher funding liquidity engage in greater intermediacy risk (Berger & Bouwman, 2009). LC, defined in Equation (2), reflects the asset-liability mismatch of the bank. While extending long-term credits using borrower deposits is crucial for real economic activities, it simultaneously increases intermediacy risk—the bank’s ability to meet immediate obligations to depositors. In the event of a sudden demand for liquidity by depositors, banks may struggle to meet it, potentially leading to a bank run. It’s important to note that banks may be solvent in the long run but fail to meet short-term depositor demands, limiting their intermediary role. Thus, LC serves as an indicator of intermediacy risk. Banks with higher liquidity, that is, a higher deposits-to-total-assets ratio, may be incentivized to take on higher risk.

Given the post-global financial crisis (2007–2008) focus on liquidity regulation, banks are closely monitored to ensure adequate liquidity. This is particularly crucial for larger banks, as they hold a significant portion of household deposits. The study also investigates whether larger banks exhibit higher intermediacy risk. Additionally, CAR is considered to examine intermediacy risk-taking. While CAR does not explicitly account for intermediacy risk, banks with sufficient CAR may benefit from a lower cost of funds in the capital market. This lower cost of funds aids in raising funds in the interbank market to meet liquidity demands from depositors. Although not a direct consideration, there may be an implicit link suggesting that banks with higher capital might undertake higher intermediacy risk.

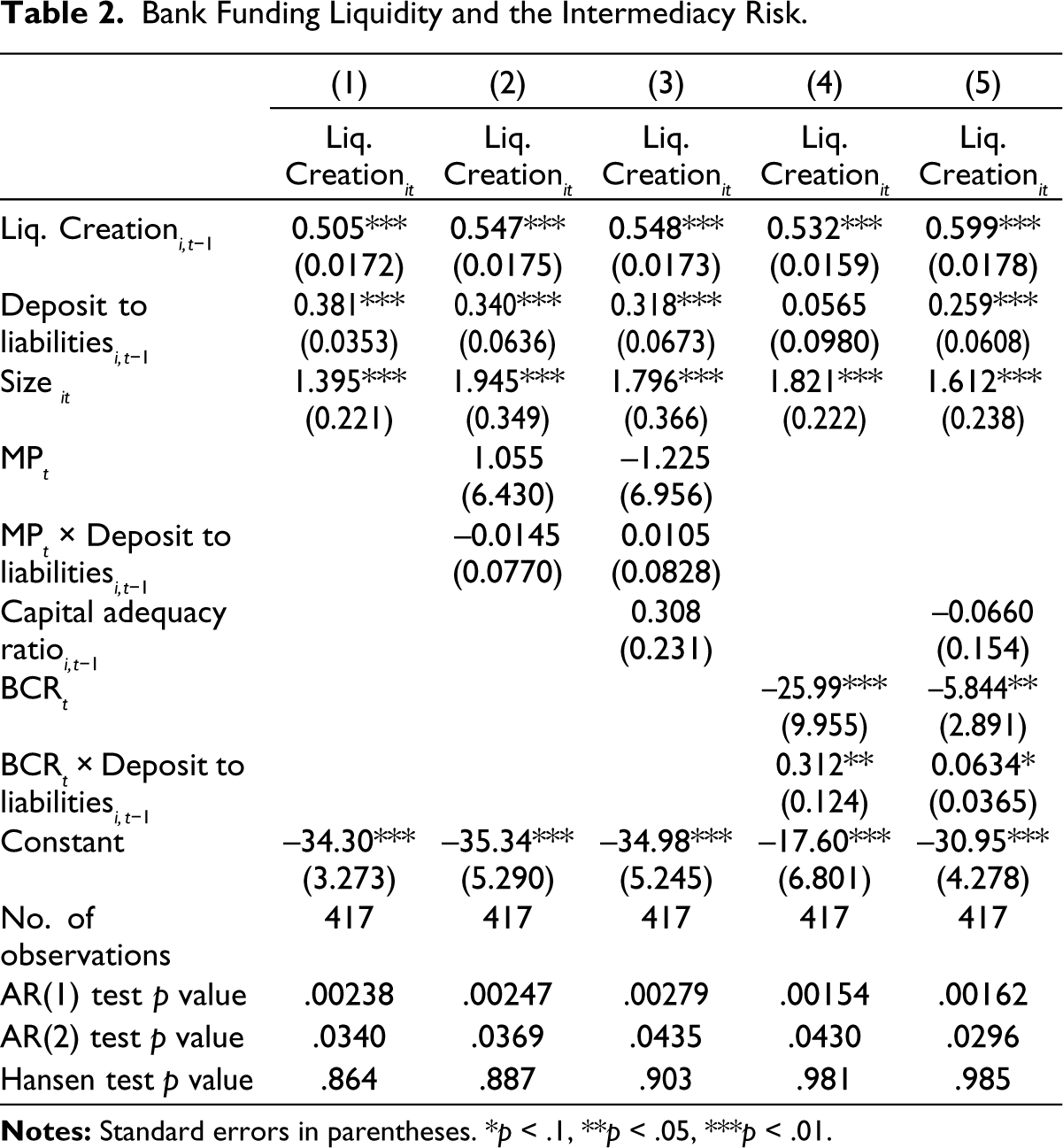

Similar to credit risk, the macroeconomic environment is taken into consideration in this analysis. The results presented in Table 2 indicate that banks with higher funding liquidity indeed take on higher intermediacy risks. Another noteworthy finding is that larger banks tend to take lower intermediacy risks, thereby exhibiting lower funding risk. On the other hand, banks with higher CAR show a propensity for higher intermediacy risk, aligning with the argument based on the lower cost of funds. When considering the macroeconomic environment, the study observes that expansionary monetary policy does not significantly impact intermediacy risk. However, during economic recovery phases, banks tend to take on higher intermediacy risks. This may be attributed to banks creating liquidity by extending more long-term credits during economic recovery, supporting real economic activities, and reducing the likelihood of excessive liquidity demand by depositors. Overall, the results suggest that banks with higher funding liquidity are more inclined to take on higher intermediacy risks.

Bank Funding Liquidity and the Intermediacy Risk.

4.4 Depositors’ Trust and Banks’ Risk-Taking Behavior

Depositor trust plays a pivotal role in influencing the likelihood of bank runs, potentially stemming from factors such as implicit public guarantees, trust in the local government, network affiliations, and more. A study by Schoors et al. (2019) on Russian banks reveals that familiar banks experience a lower likelihood of a bank run during a crisis. Notably, there is a discernible shift from non-familiar banks to familiar ones during a crisis, driven by regional affinities.

In the context of Urban Cooperative banks in India, an empirical study conducted by Iyer and Puri (2012) find that the relationship between banks and depositors serves to mitigate the probability of a bank run. Specifically, depositors with long-standing relationships with the bank, as proxied by the age of their accounts, are less prone to liquidating fixed deposits. Similarly, concerning transaction accounts, these depositors are less likely to withdraw more than 75% of their deposits during a crisis. The heightened trust among depositors, resulting in a lower likelihood of unexpected withdrawals during crises, may incentivize banks to undertake higher risks.

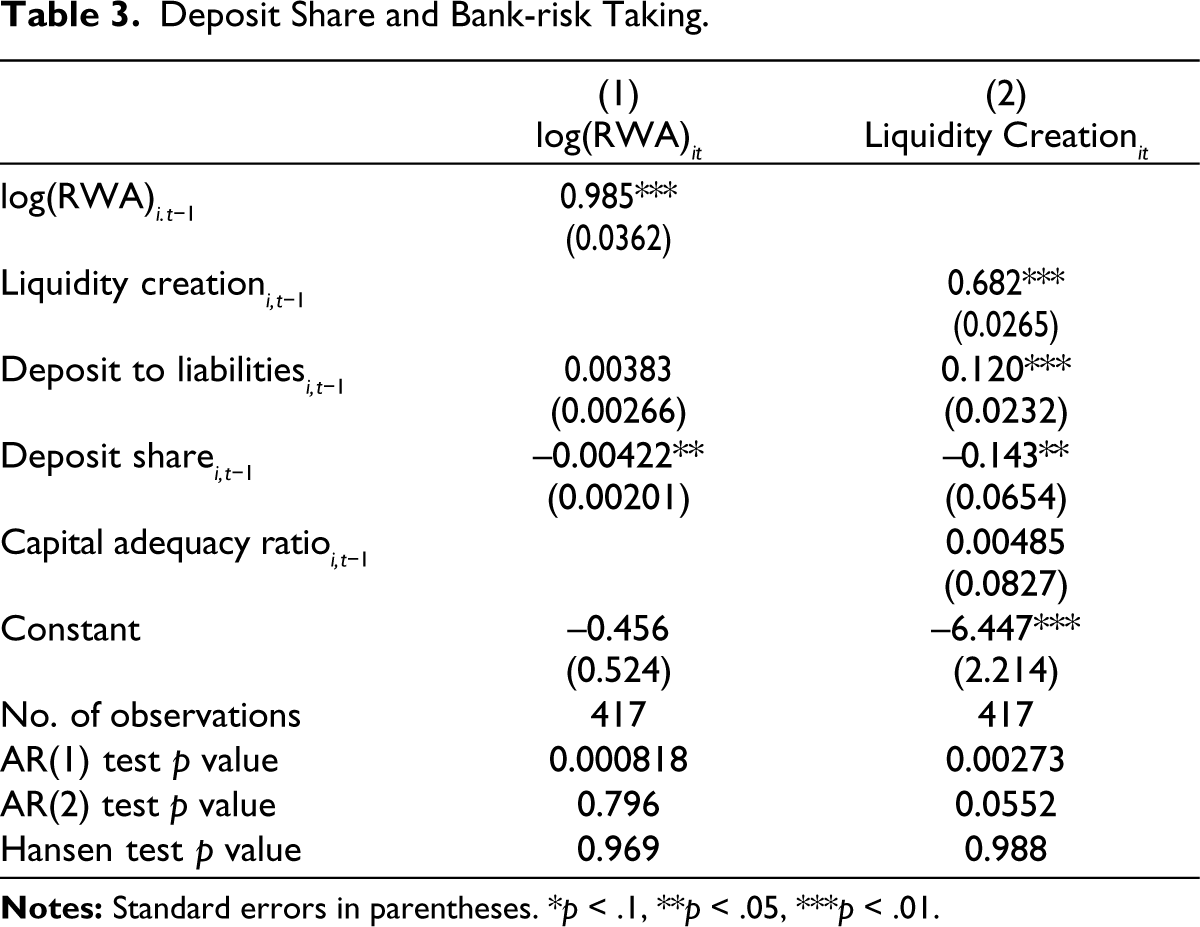

As discussed earlier, engaging in higher-risk activities may constrain the bank’s role as an intermediary. Therefore, it becomes crucial to investigate the hypothesis of whether banks with higher deposit shares exhibit a propensity for higher risk-taking. To examine the same, we estimate the following regression:

Here, DSi,t is the deposit share of the bank i in time period t. The results presented in Table 3 confirm the hypothesis that banks with higher deposit shares exhibit a lower propensity for both credit and intermediacy risk. This robust pattern underscores the stability of the Indian banking sector. A fundamental objective within the regulatory and supervisory policies of the RBI is to ensure the protection of depositors’ funds held in banks. Notably, when a bank commands a significant share in the deposit market, regulatory authorities closely monitor these institutions to safeguard public funds. Consequently, banks with higher deposit shares are inclined to undertake lower risks. This outcome is of paramount significance, providing compelling evidence of the efficacy of regulatory measures in preserving financial stability.

Deposit Share and Bank-risk Taking.

4.5 Shareholder Returns and Banks’ Risk-Taking Behavior

Shareholders of a firm consistently strive to maximize their wealth, whereas managers or executives are incentivized to maximize their private benefits. These benefits are determined by contracts based on various performance parameters of the firm, including profitability, turnover, and firm valuation. Depending on these parameters, managers may act to optimize their benefits. For instance, if a manager’s contract ties benefits to profitability, they might choose to invest in risky projects for higher returns, introducing moral hazard and deviating from shareholders’ objectives. Shareholders, aiming to align managerial actions with their interests, closely monitor managers to mitigate moral hazard.

Studies such as Nielsen and Ohnemus (2020) explore this phenomenon through the lens of targeting ROE. Bank managers set a target ROE and commit to achieving it. Studies like Pennacchi and Santos (2021) indicate that ROE has become a primary target for bank managers, supplanting the focus on earnings per share observed in non-financial firms in the US. The ROE is directly linked to managers’ private benefit contracts. Given the definition of ROE, managers may adjust leverage to expedite the achievement of the targeted ROE (Pagratis et al., 2014). Although the explicit target for each bank is not publicly observable, this study considers the average ROE of banks in the sample. Banks with ROE below this average are examined to assess whether they undertake higher-risk investments to achieve increased profits. This study delves into this issue by scrutinizing banks’ risk-taking behavior from the perspective of ROE, considering two measures: one based on shareholders’ equity in the balance sheet and the other based on returns in the stock market.

First, the ROE based on the balance sheet shows the profit-generating ability of the bank using its shareholders’ equity. Based on the sample, we have divided the bank into two categories for each year. For a year, the mean ROE is calculated. Then we consider banks with ROE below the mean ROE, the first category, and banks with ROE above the mean ROE. If there are N banks in a sample, then a dummy DROE is created for bank i with ROE

it

for time t as follows:

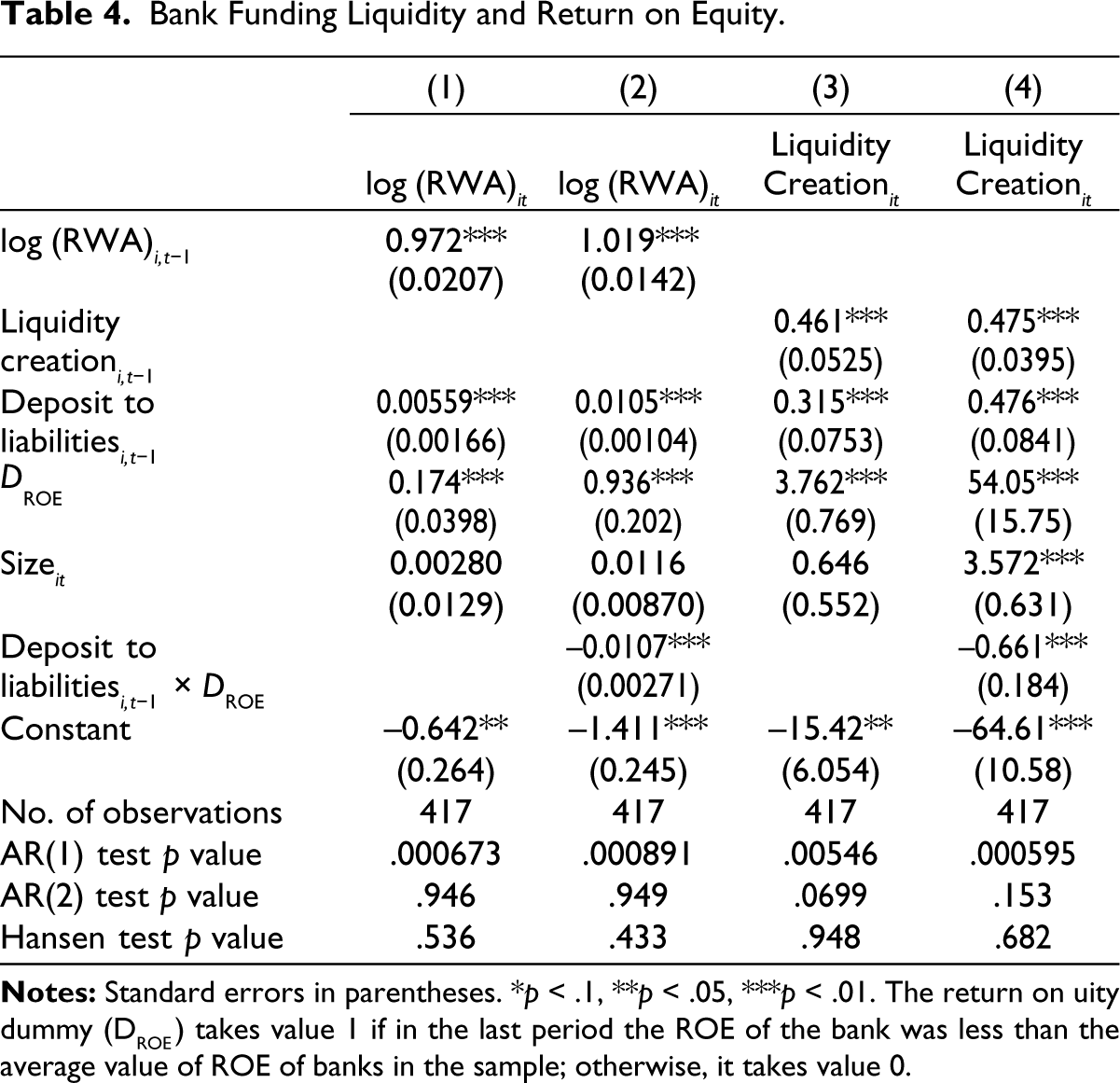

It can be anticipated that if a bank manager’s benefits are linked to profitability, then banks with ROE below average should take higher risks when they have higher funding liquidity, that is, when funding liquidity risk is low. The specifications for the estimation is given below:

The results of the empirical analysis are presented in Table 4. According to the findings, banks with ROE below the average in a given year tend to exhibit higher risk. Similar outcomes are observed for intermediacy risk, which is proxied by liquidity creation. However, the responsiveness of risk measures to funding liquidity diminishes for these banks. It is noteworthy that the risk-taking behavior of banks with higher ROE demonstrates a greater sensitivity to funding liquidity in influencing their risk, whereas banks with lower ROE already exhibit higher RWAs. This implies that banks with lower ROE may require both close monitoring of bank capital and adherence to liquidity regulations, while banks with higher ROE necessitate relatively heightened scrutiny and liquidity regulation.

Bank Funding Liquidity and Return on Equity.

Second, we examine the stock returns of the bank in the stock exchange. Although stockholders do not participate in the decision-making of the bank, they incorporate the decisions made by the bank when pricing its stock. If the decisions taken by the bank have better prospects, it will enhance its future stock cash flow valuation and, consequently, result in higher returns for its stockholders. In the literature, some studies shed light on this kind of myopic behavior of managers based on efficient stock market performance (Falato and Scharfstein, 2016). Therefore, a bank that performs below the average of other banks in the sample may engage in riskier activities to enhance its stock price returns. Similar to ROE, we also construct a dummy DMarket Return for each bank based on its market performance. For bank i with stock return SRit for time t, the dummy is defined as

The regression to be estimated is given by as follows:

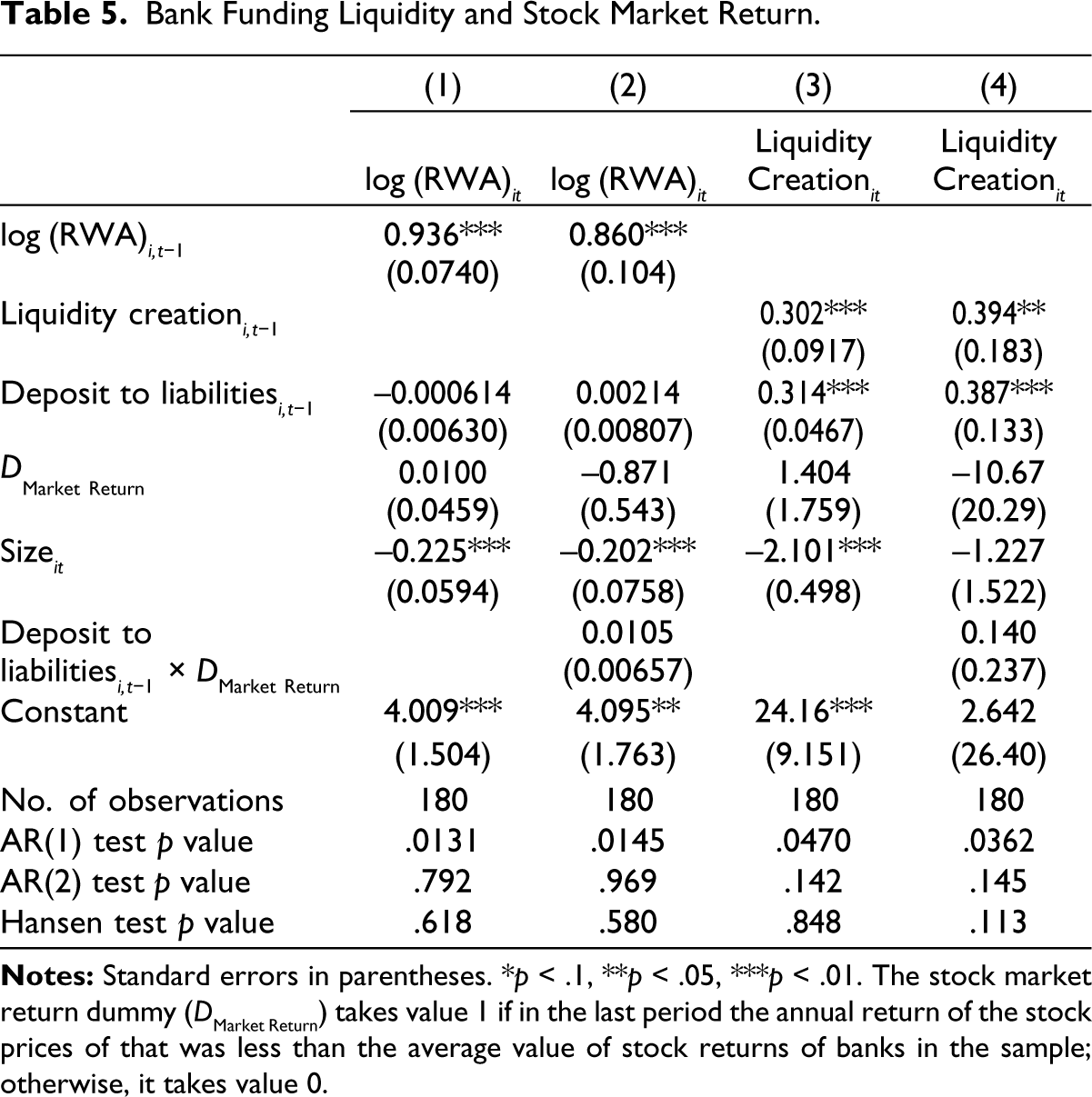

The results of this analysis are presented in Table 5. According to the empirical findings, the stock market performance of a bank does not exert any influence on the bank’s risk-taking behavior.

Bank Funding Liquidity and Stock Market Return.

In the third scenario, we examine the case where ROE is less than the stock market return. The hypothesis aims to investigate whether bank managers undertake higher risks when they perceive that the bank’s shareholders receive a lower return based on the bank’s net income compared to selling their ownership in the stock market. There exists a notable distinction between these two measures of return: ROE is an accounting measure reflecting past performance, whereas stock market return is grounded in the future outlook of the bank over a long time horizon.

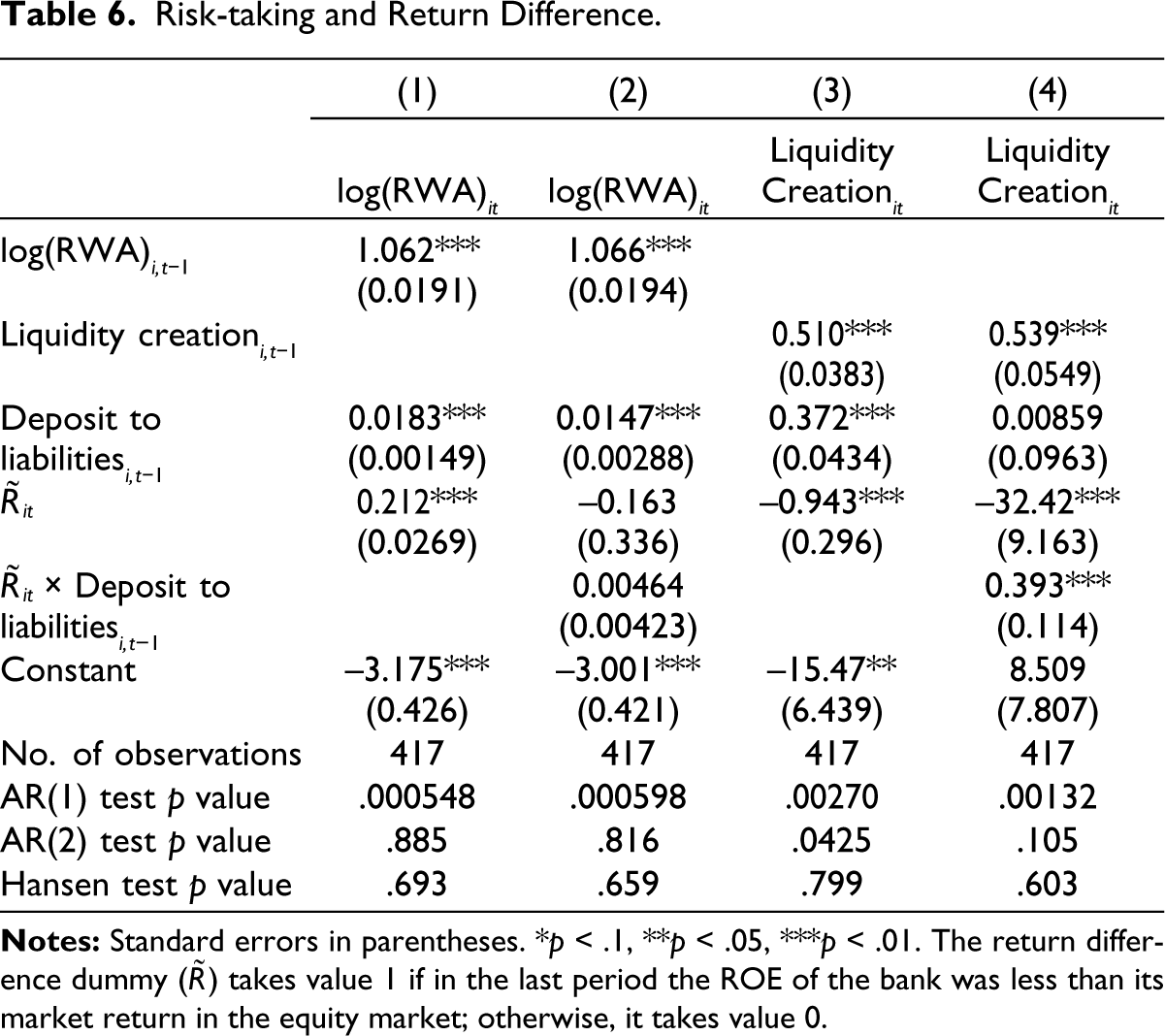

Risk-taking and Return Difference.

To examine this, we construct a dummy variable R˜ which takes value 1 if stock market return is higher than the ROE; 0 otherwise.

The results presented in Table 6 indicate that banks tend to assume higher credit risk when the ROE is less than the market return. This may serve as an incentive for bank managers to enhance the profitability of their banks, as shareholders in the market value the bank at a higher price. Conversely, concerning liquidity creation, the pattern is reversed. Banks for which stock market return surpasses the ROE exhibit lower intermediacy risk. However, in the presence of higher funding liquidity, banks demonstrate a greater willingness to engage in liquidity creation. It is worth noting that if a bank maintains very low intermediacy risk alongside higher funding liquidity, it may still harbor an inclination to create liquidity to enhance its ROE.

5. Conclusion

Based on the empirical analysis of bank-level data, the study concludes that banks indeed exhibit higher risk-taking behavior when they possess higher funding liquidity, indicative of lower funding liquidity risk. Analyzing the macroeconomic context of risk-taking, the study finds that credit risk-taking behavior with higher funding liquidity is more pronounced during expansionary monetary policy and economic recovery phases. However, banks with higher funding liquidity demonstrate elevated intermediacy risk solely during economic recovery phases, possibly influenced by heightened business expectations during these periods. In terms of intermediacy risk, large banks consistently display lower levels, aligning with the favorable perspective of the “too big to fail” argument, given the substantial economic costs associated with the failure of large institutions.

Further analysis incorporating deposit share and bank risk-taking reveals a strong association, indicating that banks with higher deposit shares tend to take lower risks. This outcome suggests effective monitoring by the regulator, particularly the RBI, and underscores the positive impact of supervisory policies. In examining risk-taking behavior based on ROE and stock market return, the study observes that when a bank’s ROE falls below the average return of all banks in the sample, it tends to take higher credit risk. Notably, the pace of risk-taking is dampened for banks with higher funding liquidity.

Drawing policy implications from these findings, the study recommends that regulators and supervisors intensify scrutiny of banks’ balance sheets, credit portfolios, and risk-taking behavior, especially during expansionary monetary policy and economic recovery phases when risk-taking tends to be heightened. This vigilant oversight could serve as a deterrent against excessive risk-taking during these phases. Additionally, banks with higher deposit shares should receive special supervisory attention, acknowledging the positive outcomes of regulatory policies, particularly for larger banks.

Footnotes

Acknowledgements

The authors thank the anonymous reviewers for their insightful suggestions that helped to improve the paper. The views expressed in the paper are those of the authors and not necessarily those of the institution to which they belong.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.