Abstract

The purpose of this article is to empirically examine and compare the factors or determinants of financial inclusion in commercial banking institutions, microfinance banks, mobile banking platforms and table banking groups (informal banking groups) in Kenya. The data used in the study were obtained from 631 small and micro-sized (SMS) farming enterprises in Kenya. We use probit model to empirically establish the factors that determine the probability of small and micro-sized farming enterprises in accessing agricultural credit from the four major lending institutions. Also, we apply Heckman selection model to establish the determinants of agricultural credit rationing. OLS model is used to investigate the determinants of agricultural credit delinquency rates in the lending institutions. The results show that female-owned SMS farming enterprises are likely to access less agricultural credit amount from table banking groups, own small farms with no title deed and own less valued assets compared to male-owned SMS farming enterprises which access agricultural credit from commercial banks and microfinance banks. Further results revealed that household dependency ratio was a significant determinant factor in agricultural credit access from mobile banks, commercial banks and table banking groups. Additionally, agricultural credit delinquency in mobile banking is significantly reduced by distance to the banking agent. The availability of mobile banking agencies within village centres would considerably enable agri-entrepreneurs to make credit repayment within the required period.

Keywords

Introduction

It is generally accepted that extensive financial inclusion among farming households has played a significant role in the economic growth of transition economies in Asia and Eastern Europe (Swinnen and Gow 1999; Yuan and Gao 2012). The provision of affordable and accessible financial services to smallholder farmers has enabled the agricultural sector of China to be competitive in the global food market. Also, agricultural credit has the potential to increase yields outputs, enabling poor farmers to use more efficient external inputs such as chemical fertilisers, pesticides and seeds. However, lack of affordable and accessible credit services has a negative impact on the adoption of agricultural technologies and limits farmer’s ability to utilise sustainable agricultural practices in sub-Saharan African (SSA) countries (Tadesse 2014). Indeed, financial inclusion for low-income smallholder farmers has been identified as a key factor in attaining sustainable food production to feed the growing population in the region (Dong, Lu, and Featherstone 2012). In addition, affordable credit would ensure better livelihoods for rural communities by creating agricultural employment.

Just like in most of the emerging economies, commercial banks in Kenya have been reluctant to offer credit services to smallholder farmers. Smallholder farmers are considered to lack the required collateral and guarantors to qualify for commercial bank credit. Also, the success of credit applications mainly depended on savings and employment income and very little on credit scoring. Prior studies point out that the transaction cost of processing credit mainly excluded the majority of smallholder farmer populations in rural areas (Asante-Addo et al. 2017). Accessing credit from commercial banks in Kenya still requires farmers to travel more than 10 km to reach the nearest bank branch (Omwansa and Waema 2014).

The provision of financial services by microfinance banks for all the rural farming communities has widely been acknowledged as the panacea for reduction in poverty and economic growth in many developed countries (Kumar, Turvey, and Kropp 2013). The microfinance banking model has been popular for helping millions of poor people attain economic growth in Asia and Latin America. However, the success of microfinance has not been sufficiently replicated in SSA (Van Rooyen, Stewart, and de Wet 2012). The region has more than 300 million people who are economically active and in need of credit; however, only 20 million (less than 10%) have access to any form of formal credit services (Helmore and CARE/International 2009). With only 25% of the adults owning bank accounts, SSA lags behind other regions in attaining sustainable financial inclusion levels (Demirgüç-Kunt and Klapper 2013). Liberalisation and privatisation of financial services have improved credit availability to smallholders in SSA (Sheahan and Barrett 2014). Nevertheless, majority of farmers still face severe credit access and credit rationing constraints that limit their agricultural enterprises’ potential.

In emerging economies, mobile money technology has revolutionised the financial sector’s landscape. Mobile money services facilitate secure and affordable remittances and also provide quick cashless payment of goods and services and linkage to banking services (Kusimba, Kunyu, and Gross 2013). In Kenya, more people are likely to bank with mobile phones than through commercial bank account (GSMA 2012). The number of loan and deposit accounts accessed from mobile phones increased from 1.67 million in 2010 to 8.51 million in 2016 (FSD 2016). Mobile banking technology is considered to contribute towards financial inclusion for the unbanked rural farming populations. However, the penetration of mobile banking technology is still considered low in rural agricultural areas. In low-income and developing economies, majority of the population, especially women rely on traditional informal banking groups like Rotation Saving and Credit Association (ROSCA) or Accumulated Savings and Credit Associations (ASCAS) commonly referred to as table banking groups for credit (Yuan and Gao 2012). Women who are excluded from formal credit depend on informal banking schemes to finance the micro-enterprises (Gichuki, Mutuku, and Kinuthia 2015). However, despite the benefits associated with informal banking groups, some studies report that informal banking is not sustainable in bringing financial gaps in emerging economies (Gugerty 2007). In addition, the schemes are prone to fraud and default rates (Ambec and Treich 2007). Furthermore, Gugerty (2007) noted that the informal banking groups cannot sufficiently provide the financial capital needed to fund expanding micro-enterprise ventures.

Doss (2014) argued that women are likely to be involved in producing 60–80% of the world’s food, despite having lower access to agri credit, land, farm inputs and their responsibilities for household work. Regardless of growing women potential, agricultural production is still a male-dominated one. Deeply embedded cultural beliefs such as discrimination from property inheritance laws, oppressive customary laws and time constrains due to household responsibilities derail women’s entrepreneurial growth. Previous literature points out that women entrepreneurs are likely to be financially excluded from formal banking services than their male counterparts (Kumari 2017).

Therefore, the general objective of the study is to explore and compare the determinants of financial inclusion in Kenya’s lending institutions. The study will focus on commercial banking institutions, microfinance banks, mobile banking platforms and table banking groups. First, the study will seek to characterise and describe perceptions that are likely to influence agricultural credit access for small and micro-sized (SMS) agri-enterprises. Second, the study will examine and compare the factors that determine agri-entrepreneurs’ probability of accessing agricultural credit from lending institutions. Third, the study will explore and compare the factors that determine the extent of agricultural credit rationing in lending institutions. Fourth, the study will investigate the factors that are likely to regulate agricultural credit delinquencies across different lending institutions.

Research Methodology

The data used in the study were obtained from a survey that was conducted between June and July 2020 in Nakuru, Baringo, Embu and Nyandarua counties in Kenya. A multistage sampling method was used to select 631 SMS agri-enterprises. In the first step, we relied on sampling frame of SMS agri-enterprises registered with the agricultural department. In the second step, proportionately clustering techniques were used to select 198 agri-enterprises from Nakuru, 141 from Baringo, 141 from Embu and 151 from Nyandarua counties. The survey data were collected using structured questionnaires after interviews with agri-enterprises owners.

Empirical Specification

In order to examine perceptions likely to influence agri-entrepreneurs’ preference for agricultural credit, we employed Garrett ranking technique. The technique enabled us to rank farmer’s preference for agricultural credit by ranking scores. The ranking technique’s first assumption is that the percentage estimate for each respondent is converted into factor scores. For every factor, the scores of each individual are added and total value of scores and mean values of score is calculated. The ranking technique is helpful in recording cases where some traits are not easily measured by ordinary methods but can be arranged in the order of merit (Garrett and Woodworth 1969). A prior study by Asante-Addo et al. (2017) uses Garrett ranking to determine households’ reasons for participation and non-participation in microcredit programmes in Ghana. Anjugam and Ramasamy (2007) apply techniques to analyse factors that influence women’s participation in self-help groups (SHGs) in India. The factor having the highest mean value is considered as the most likely to influence farmers’ preference for mobile banking credit. The formula for score value for all factors can be written as

Where Rij is denoted as rank given for the ith variable by jth respondents, while N i denotes the number of variables ranked by jth respondents.

A number of studies have examined the factors likely to influence credit access in financial banks using different econometric models; for instance, Rahji and Fakayode (2009) applied a multinomial logit to establish the influence of credit rationing by commercial banks. Kibet et al. (2009) used propensity score matching to evaluate strategies applied by microfinance in disbursing affordable credit to smallholder farmers in Kenya. Similarly, Lukytawati (2009) investigated factors that are applied by community-based SHGs like ROSCA and ASCRA to determine members’ creditworthiness. Also, recent studies have applied probit model equation to investigate the demand for credit by farmers (Dutta and Magableh 2006; Kochar 1997). In the first stage, this study will employ probit model to establish factors likely to influence SMS agri-enterprises’ agricultural credit to be approved. The framework used in the analysis is based on the assumption that agri-entrepreneurs’ application of agricultural credit is faced by two possible outcomes: 1 for successful application of agricultural credit and 0 for failure to secure credit. Prior studies by Cheng and Ahmed (2014) and Dutta and Magableh (2006) have empirically expressed the model as

where Ld denotes the demand function for credit, HC is considered to be the vector for agri-entrepreneurs household characteristics and I denotes the personal characteristics of the household head. HF represents agri-entrepreneurs’ household financial characteristics like assets and income. I and HC are non-financial characteristics of credit applicants. In the second stage, we apply the Heckman two-step selection model to examine the extent credit rationing parameters applied by the lender. The Heckman two-stage model enables us to reduce sample selection bias when modelling for credit demand (Dutta and Magableh 2006; Okurut, Schoombee, and van der Berg 2004). In the application of the model, the first stage probit estimates in equation 1 generate the inverse Mills ratio (IMR), which is included as an explanatory variable in the second-stage estimation to correct the sample selection bias problem. The Heckman model can be exported as

Where z = f(I, HC, HF) denotes the exogenous variables perceived to affect lenders’ decision to grant agricultural credit applied;

Similarly, the probability of not accessing credit applied for is expressed as

where

In the study, we also examine the determinant factors influencing agricultural credit delinquencies among agri-entrepreneurs by using OLS model. The approach has been previously applied by Raghunathan et al. (2011) and (Weber and Musshoff 2012). The approach uses frequency of late payments during the loan repayment period to measure credit risk. Prior studies by Raghunathan et al. (2011) noted that the higher the frequency of delinquency rates increases the risk for credit defaults. Weber and Musshoff (2012) study estimated the empirical OLS model as follows:

where c

i,t

is the dependent variable, and it denotes the percentage ratio of delinquency of agricultural credit accessed. e1,t represents time constant for year t when agricultural credit was accessed, ∈ is the parameter of vector, while I and t are identical and independent distributed error terms with mean of 0 and a variance

Descriptive Statistics of the Selected Variable

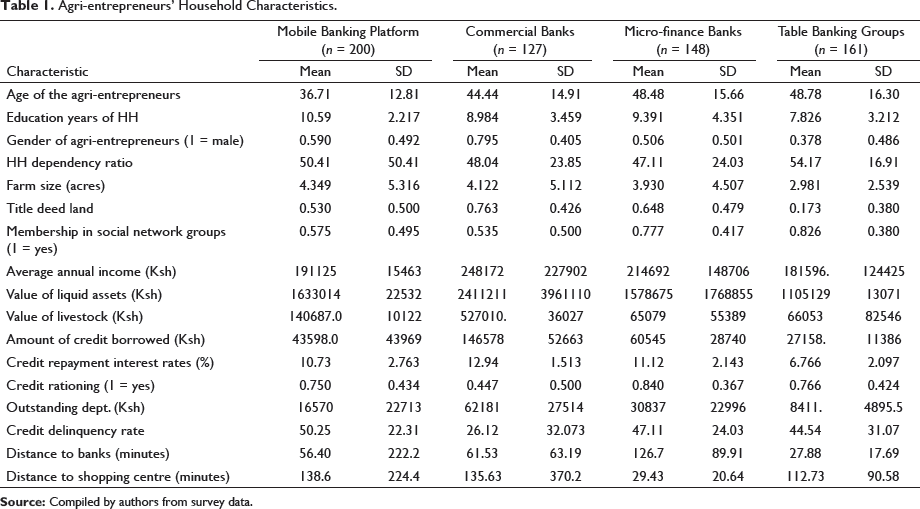

Table 1 presents descriptive statistics for the surveyed SMS agri-enterprises. We observe that 78% of the SMS agri-enterprises that accessed agricultural credit from table banking groups were female who have 7.8 years of education, earn an annual average income of Ksh181,596. In addition, women-owned SMS agri-enterprises were small in size, had no title deed farm and owned less valued assets compared to male agri-entrepreneurs who access agricultural credit form other lending sources. This is a typical feature of the study location where women have limited control over productive resources and often seek credit from informal banking sources (Mulu-Mutuku and Gichuki 2017). We further note that agri-entrepreneurs with preference for credit from table banking groups access the least amount of agricultural credit, while agri-entrepreneurs with preference for commercial banks and microfinance banks received agricultural credit of Ksh146,578 and Ksh60545, respectively. In comparison to table banking groups and mobile banking platforms, accessing agricultural credit from commercial banks and microfinance attracted highest interest rates of 12.94% and 11.12%, respectively. Interestingly, we observe that agricultural credit rationing is evident among agri-entrepreneurs with preference for microfinance (84%), table banking (76%) and mobile banking platforms (75%). Also, credit delinquency rates are least expected in commercial banks and more likely in mobile banking platform. Agri-entrepreneurs who accessed credit from mobile banking platforms are young and have more education years.

Agri-entrepreneurs’ Household Characteristics.

Factors Influencing Agricultural Credit Access

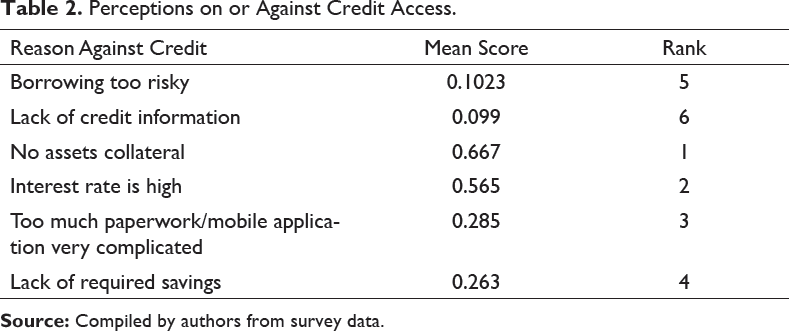

In order to characterise and describe factors likely to influence agricultural credit access for SMS agri-enterprises, we apply Garrett ranking technique; the results are presented in Table 2. We find that lack of collateral requirement, high interest rates, too much paperwork and complexity in using mobile banking applications were perceived as a major hindrance to agricultural credit access. The results further show that 10% of the surveyed agri-entrepreneurs perceive credit borrowing to be a risky venture, while lack of credit information is perceived to be the least likely factor affecting agricultural credit access. The literature on credit lending in emerging markets reveals that commercial banks are unfamiliar with unique operating characteristics of small-sized farming ventures (Reyes and Lensink 2011); for instance, despite the potential of livestock production in Ethiopia, credit markets are not easily accessible for smallholder farmers (Fitawek and Kalaba 2017). Generally, commercial lenders find it hard to establish credit worthiness of small-sized agribusiness ventures, especially in cases where they lack collateral and the path to profitability is considered to be tenuous and takes long to be realised (Kibet et al. 2009; Saldias and von Cramon-Taubadel 2012). Mukherjee (2013) shows that in India, micro-enterprises were likely not to apply for credit mainly because lenders would outrightly reject their credit application based on indebtedness, delinquency or credit supply constrain.

Perceptions on or Against Credit Access.

Empirical Results: Determinants of Agricultural Credit Access from Lending Institutions

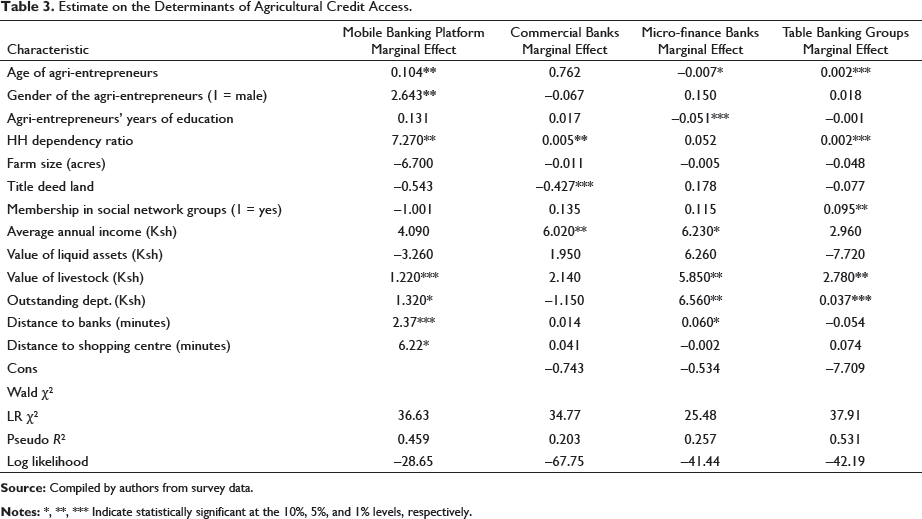

The results in Table 3 present the probit regression estimates of the likelihood of SMS agri-enterprises in successfully accessing agricultural credit from commercial banks, microfinance banks, mobile banking platforms and table banking groups. In the model, the dependent variable is a binary variable, that is, 1 for successful application of agricultural credit and 0 for failure to secure agricultural credit. The independent variables are agri-entrepreneurs’ demographic, financial and social capital characteristics. The magnitude of the coefficient from probit model is difficult to interpret; we, therefore, use the marginal effects estimates. The marginal effects for the value of livestock are positive and statistically significant for mobile banks, microfinance and table banking groups. This indicates that the value of livestock owned by agri-entrepreneurs would significantly influence likelihood of obtaining agricultural credit from mobile banks, microfinance and table banking groups. This confirms the previous findings by Mohamed and Temu (2008) that in a risky credit environment, farmers in need of credit would use livestock capital as collateral to secure required credit amount.

Estimate on the Determinants of Agricultural Credit Access.

Determinants of Agricultural Credit Rationing by Lending Institutions

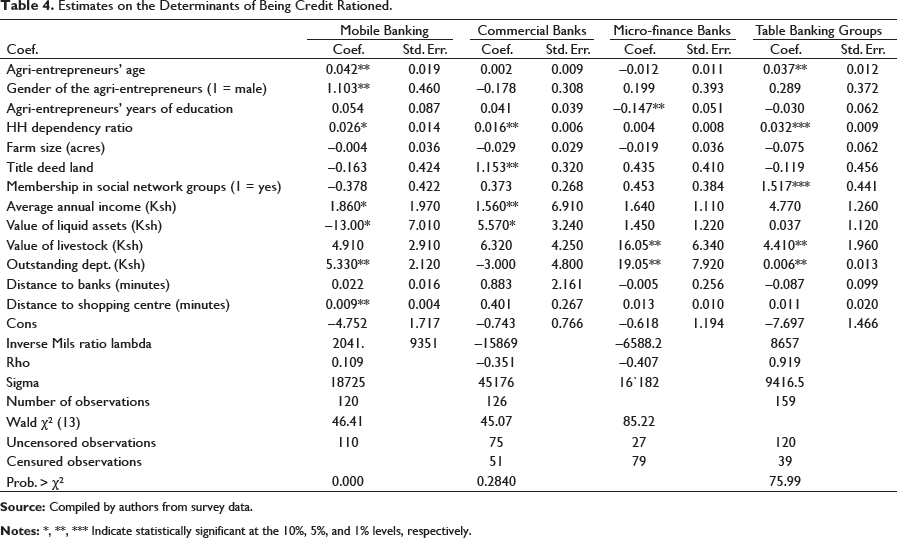

The determinants of agricultural credit rationing by the lending institutions are presented in Table 4. As previously indicated, the Heckman two-step selection model will be used to examine the factors that determine the extent of credit rationing parameters applied by commercial banking institutions, microfinance, mobile banking platforms and table banking groups. Despite Erec Heimfarth and Musshoff (2011) observing that agricultural income in emerging economies is considered to be volatile due to weather, diseases, pest and market instability, our study findings reveal that SMS agri-enterprises’ income would determine the amount of agricultural credit accessed from commercial banks.

The study results further reveal that SMS agri-enterprises’ income would determine the amount of agricultural credit accessed from the mobile banking platform. This can be explained by the fact that in mobile credit platforms, borrowers take very short time to know the decision on whether the loan was granted after application. In addition, the process is swift and requires less paperwork, and eligibility and amount credit granted requires developing good credit rating scores and less of income status. Mobile money technology has enabled easy transfer, deposit, savings and withdrawal of money; these services were previously unavailable to the majority of rural populations who rely on farming (Omwansa and Waema 2014).

The value of livestock owned by SMS agri-enterprises determines the amount of agricultural credit offered by microfinance banks and table banking groups. The findings reveal that titled deed farm would significantly guarantee SMS agri-enterprises to receive agricultural credit applied for from commercial banks. While explaining the casual relationship between land title and credit access, Boucher, Barham, and Carter (2005) noted that formal lenders with limited information on the borrowers require significant collateral to mitigate the risk of defaults. Also, lack of land titles prevents full collateralisation of the main asset owned by poor farming households in developing countries. The study estimates also reveal that shorter distance to the bank positively influenced the agricultural credit amount received from mobile banks. Generally, mobile banking has credit processing efficiency that is cost-effective and not offered by other lending platforms. Using their phones, agri-entrepreneurs easily repay credit and make cash withdrawals from mobile agents in rural centres. Unlike in conventional banks, it would take agri-entrepreneurs longer time to process credit and access cash from the banking branch located far from the farms. The study results reveal that membership in social network organisations would significantly determine the agricultural credit amount accessed from informal banking groups. Asante-Addo et al. (2017) and Cheng and Ahmed (2014) also found evidence that membership association by agri-entrepreneurs significantly increased probability of SMS agri-enterprises in accessing credit amount applied for 23%.

Estimates on the Determinants of Being Credit Rationed.

Estimates on Determinants of Agricultural Credit Delinquency.

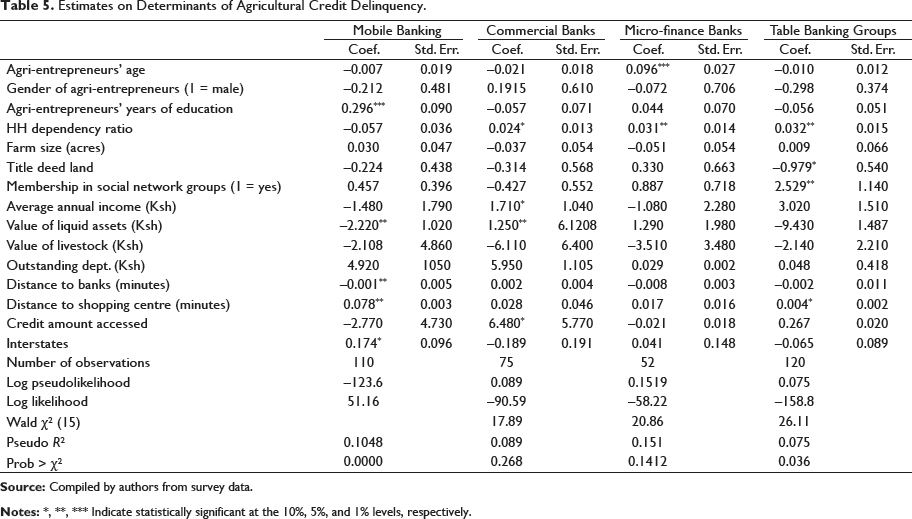

Determinants of Agricultural Credit Delinquency

The estimate results for agricultural credit delinquencies are presented in Table 5, as indicated previously. OLS model is used to conduct the empirical analysis where the dependent variable is the percentage ratio of agricultural credit delinquency rate, while the independent variable includes agri-entrepreneurs’ personal characteristics, agri-entrepreneurs’ household financial characteristics and social capital characteristics. Interestingly, our findings indicate that agricultural credit delinquency in mobile banking would be significantly reduced by distance to the banking agent. This implies that the availability of mobile banking agencies within village centres would considerably enable farmers to make credit repayment within required period. Whilst mobile banking platform is considered to provide small and low amount of credit, we note that interest rates significantly influence credit delinquency. The results further reveal that the value of assets owned would significantly reduce agricultural credit delinquency in mobile banking.

The study investigation also found that dependence ratio would influence the likelihood of agricultural credit delinquency from commercial banks, microfinance and table banking groups. Previous studies show that mainly, the unforeseen household expenses and dependence from relatives would endanger loan repayment (Maurer 2014). Interestingly, the amount of credit granted would positively and significantly influence agricultural credit delinquency in commercial banks. This finding is consistent with Weber and Musshoff (2012) who also find a significant relationship between larger disbursed loan amounts and higher loan delinquency rates. Similarly, Maurer (2014) attributes higher credit risks to larger amount of loans. Considering that more women are likely to source credit from table banking groups banks than men, we note that ownership of land that has a title deed would significantly reduce agricultural credit delinquency in table banking groups. However, the distance covered to the shopping centres where table banking group meetings take place has a significant influence on agricultural credit delinquency rates. Membership in social organisations significantly influenced the likelihood of farmer’s delinquency rates for table banking groups. This can be explained by the fact that farmers are likely to use fellow group members as credit guarantors.

Conclusion

This article explored and compared the determinants of credit agricultural credit access in commercial banking institutions, microfinance banks, mobile banking platforms and table banking groups in Kenya. In the study, we apply Garrett ranking technique to describe factors likely to influence agricultural credit access for SMS agri-enterprises. To empirically examine and compare factors that are likely to influence SMS agri-enterprises receiving agricultural credit from four lending platforms, the study used probit model. We use Heckman model to empirically explore and compare factors that determine the extent of agricultural credit rationing across different lending institutions, while in the third stage, the study used OLS model to establish the factors that would influence agricultural credit delinquency in lending institutions.

The main observations from the study revealed that lack of collateral required by banks was considered as the main impediment to agricultural credit access by agri-entrepreneurs. Also, high-interest rates were a concern when considering agriculture credit access from the available credit sources in Kenya. Nevertheless, we note that the penetration of mobile banking credit that requires less collateral and depends on credit scoring to provide credit was the preferred agriculture credit source for 31% of agri-entrepreneurs, while table banking groups is an important source of agriculture credit for 25% of surveyed agri-entrepreneurs.

The study results revealed that the household dependency ratio increased the probability of accessing agricultural credit from mobile banks, commercial banks and table banking groups. Considering the fact that some microfinance banks require clients to have required amount of savings that determine the credit amount accessed, we observe that SMS agri-enterprises income significantly determines the probability of obtaining agricultural credit from microfinance banks. Also, the proximity to mobile banking agents increases the probability of agri-entrepreneurs accessing agricultural credit from mobile banks. Similarly, banking proximity to the banks increases the probability of agri-entrepreneurs accessing agricultural credit from microfinance banks. This is partly explained by the microfinance model that facilitates banking agents to serve clients at their locations rather than making long trips to the banking halls.

With regard to factors that influence agricultural credit rationing, the study results indicate that title deed farms, the value of assets and income significantly determine whether agri-entrepreneurs received the desired agricultural credit amount from commercial banks. Conventionally, formal banking systems heavily rely on collateral such as farm machinery, titled land and household assets information to verify and determine the amount of credit to disburse to agri-entrepreneurs. The other important observation of the study was that proximity to banking agents determined the amount of agricultural credit accessed from mobile banks. Most of the agri-entrepreneurs who are financially excluded from formal banking systems are likely to seek credit from mobile banking networks. Mobile banks’ credit relies on credit scoring for loan disbursement unlike the traditional banking system, which relies mainly on collateral, profile documentation and enterprise financial cash flow to guarantee for credit. Also, credit application process takes less time, and mobile agents offer deposits and withdraw services that are easily convenient and accessible within the rural settings.

The study findings illustrate that the amount of agricultural credit borrowed would determine agricultural credit delinquency rates in commercial banks. Generally, financial banks find it more costly to lend and collect money from small enterprises than a big firm. Also, the findings showed that accessing high mount of agricultural credit would influence delinquency in mobile banks, formal banks, microfinance and informal banks.

In conclusion, we note that most of the studies report that women farmers are likely to produce less because they have lower quality land, less access to fertiliser and other inputs and receive less credit and extension support. FAO’s State of Food and Agriculture reports that if women had access to productive resources as men, they are likely to increase their farm yield by 20–30%. From the study, we observed that despite the rapid rate of financial inclusion, women agri-entrepreneurs mainly rely on informal banks for agricultural credit, which tends to be unreliable. Also, women-owned SMS agri-enterprises are likely not to control productive resources like land that has a title deed. This limits the women agri-entrepreneurs’ ability to access agricultural credit from established lending institutions. The study recommends development of agricultural credit policy accessibility in rural areas. In addition, the agricultural credit products that are flexible and have longer repayment periods to cover the periods between capital investment (planting) and revenue generation (harvesting) should be established.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.