Abstract

This study examines the impact of access to formal credit on the technical efficiency of farms. The stochastic frontier analysis (SFA) is used to estimate technical efficiency by utilising primary survey data collected through a multi-stage random sampling technique. The results reveal that technical efficiency scores range from 0.56 to 0.97. There is a relatively high level of technical efficiency among borrower households (score 0.88) compared to non-borrower households (score 0.67), which implies that credit access enables farmers to use better technologies and optimise input use. The major inputs, such as labour, chemicals, machinery and farm size, are positively associated with farm technical efficiency, whereas land tenancy, seed price and fertilisers tend to decrease farm efficiency. The gamma coefficient (0.76) justifies the application of SFA, implying that inefficiency in the farm inputs is more likely than random shocks. In addition, the age of the household head, farming experience, education, occupation, membership, farm size, household assets and access to credit are the primary factors determining efficiency. These findings highlighted the requirement to have policy interventions in order to improve the socio-economic environment, institutional support, access to credit and managerial skills of farmers, which would increase productivity and achieve sustainable agricultural development.

Introduction

Formal credit accessibility is commonly considered to be the most important factor to boost agricultural productivity and technical efficiency, as it helps to overcome liquidity constraints, allows farmers to obtain their timely inputs and promotes the use of efficiency-enhancing technologies (Adjognon et al. 2017; Feder 1990; Narayanan 2016). Access to formal credit has enhanced the efficiency of resource allocation by enabling farmers to utilise price signals and mitigate climatic and market risks through diversification and the adoption of climate-resistant practices (Birthal and Hazrana 2019). Increases in agricultural efficiency lead to reduced production costs, increased competitiveness, and enable the adoption of more diversified and climate-resilient systems (Narayan and Bhattacharya 2019). Bravo-Ureta et al. noted that technical and allocative efficiencies are critical indicators of total factor productivity growth. Therefore, they moved efficiency enhancement as a core policy goal of sustainable agricultural development (Bravo-Ureta et al. 2007). Since agriculture supports a large percentage of the Indian labour force and rural livelihoods, the efficiency will increase agricultural profitability and macroeconomic stability (Chand and Parappurathu 2012). Empirical evidence from India shows that the growth of agricultural credit has increased capital formation and mechanisation, which in turn has indirectly improved farm productivity and efficiency. Still, considerable regional and farm-scale heterogeneity exists (Ramasamy and Malaiarasan 2023). In Jammu and Kashmir, land fragmentation and limited resources necessitate efficiency in supporting agricultural income and livelihoods (Bhatt and Bhat 2013). In line with this, the study focuses on the association between access to formal credit and farm efficiency.

Over the past few decades, there has been a wide range of credit policies to increase financial inclusion and the adoption of digital technology. Efforts to increase the rural credit architecture include bank nationalisation in 1969, the establishment of Regional Rural Banks (RRBs) in 1975, and the establishment of NABARD in 1982. The Kisan Credit Card (KCC), established in 1998, made short-term credit accessible to the farmers, and so did Priority Sector Lending (PSL) guidelines for commercial banks, Self-Help Group-Bank Linkage Programme (SHG-BLP) and Joint Liability Groups (JLGs), designed to embrace landless and tenant farmers. Newer schemes have eased the process of credit access for a larger population and made credit affordable for small borrowers, like the Interest Subvention Scheme, Pradhan Mantri Jan Dhan Yojana (PMJDY) and Pradhan Mantri Mudra Yojana (PMMY). Two other path-breaking schemes that collaborate to support farmers who face difficulties due to inadequate investment and risk are the Pradhan Mantri Fasal Bima Yojana (PMFBY) and the Agricultural Infrastructure Fund (AIF) (NABARD 2022; RBI 2023). Despite these initiatives, the disbursement of farm credit is still inequitable since small and marginal farmers are still experiencing persistent barriers due to collateral requirements, administrative delays and low financial literacy (Chand and Kumar 2004). Credit and financial access are vital for improving farm efficiency because they help adopt risk-control mechanisms, mechanisation and more efficient use of inputs in a timely manner (Singh and Gill 2021). Formal credit accessibility influences the intensity of input use, especially fertilisers, quality seeds and mechanisation, leading to increased yields and better resource-use efficiency (Kumar et al. 2021).

Although there is extensive literature on agricultural credit and farm efficiency, gaps remain in the existing literature regarding agricultural credit and farm technical efficiency in the study area. The investigation of the area has little empirical evidence, as institutional restrictions, farm organisation, agro ecology and access to formal finance are quite different compared to the national standards. It is against this background that the current study aims to fill these gaps by evaluating the effects of agricultural credit on the farm technical efficiency. Namely, the research questions are: (a) to develop a hypothesis on the significant impact of credit accessibility on farm technical efficiency; and (b) to determine some of the most important socio-economic and institutional determinants of efficiency in the framework of a Tobit regression model.

Review of Literature

Formal credit access can significantly increase farm technical efficiency by alleviating liquidity constraints and facilitating the adoption of improved inputs (Feder 1990; Haryanto et al. 2023; Jimi et al. 2016). However, other researchers argue that credit endowment can be inadequate if farmers lack the information required to make effective use of credit (Kapoor and Shushma 2024; Mahmood et al. 2009; Olagunju 2007). As Sharma et al. (2019) underscored, the effective operation of existing technology can increase agricultural production without additional inputs. Yadava (2023) examined technical inefficiency in Indian agriculture, especially the use of chemicals and fertilisers. They found that optimisation of input use could help maintain farm yield. Similarly, Chandel et al. (2022) stated that timely access to credit and information is critical in enhancing the technical efficiency of rice farmers in the Indo-Gangetic Plains. Their evaluation of cooperative lending in states further underscores the need for extensive reforms to correct the inefficiency in the cooperative credit system. Narayanan (2025) showed that the availability of credit contributes to output by 24% and risk reduction by 16%. According to Singh (2023), only 33% of Indian farmers have access to formal credit, and disadvantaged groups face massive challenges. Chandio et al. (2020) discovered that a one-unit change in agricultural credit has a 0.19% increase in total production. However, there are still issues, such as the misuse of credit for non-agricultural use (Rehman et al. 2019). Although it is generally acknowledged that institutional credit is capable of increasing farm production, the process through which it improves the efficiency of farms is multifaceted and requires further research (Rahman 2010).

The widening gap between supply and demand for food is a strong reminder of the need to increase productivity, especially with the severe limitations that exist due to the lack of land available to be cultivated (Deshpande and Bhende 2003). Ghoshal and Goswami (2013) found that the technical efficiency had significant inter-state differences and thus indicated the need to use state-specific policy interventions. On the same note, Mathewos (2019) found that smallholder farmers who get institutional credit are very productive, and thus he supported the policy of increasing agricultural performance by increasing access to credit in rural areas. Bhatt and Bhat (2014) determined a causal correlation between landholding size and farm technical efficiency in Jammu and Kashmir, and found an inverse-U-shaped relationship. All these studies taken together approve the fact that formal credit access has a strong positive impact on agricultural efficiency.

Especially, marginal and small farmers are facing financial constraints, which reduces their farm efficiency (Sharma and Bansal 2019). Other factors influencing farm inefficiency consist of institutional failures, physical differences in access to formal credit and dependence on non-institutional sources of credit (Patil et al. 2022). Kumar et al. (2020) pointed out that the main contributors to these problems are the excessive dependence on informal lending businesses. These issues are mainly based on the high interest rates, lack of accessibility to formal credit and lack of capital investment. According to Reddy and Mishra (2018), other than reliance on informal credit, farmers are often faced with inefficiencies in production, rising costs and increased vulnerability to external shocks like market volatility and climatic change. These are particularly intense among small and marginal farmers, which is one of the main reasons that holds a good barrier to the efficiency of farms nationally (Sharma and Bansal 2019).

Formal credit distribution in India is not homogeneous across locations and farmlands, which makes it difficult to find the empirical results on the correlation between credit availability and its working (Chavan 2017; Misra et al. 2018). A regional outlook is essential, mainly because of the differences in infrastructure, institutional backup and policy application. Whereas some states have established systems of agricultural credit, some have to face the problem of low banking penetration and poor credit disbursement. India is a heterogeneous country, and agro-climatic, economic and geographical diversities are prevalent in the country; therefore, conducting a study in this environment has high potential. A more detailed analysis of the state and district is needed to understand how credit constraints are heterogeneous and how they impact farm efficiency.

The study aims to fill research gaps in the existing literature by examining the link between formal credit and technical efficiency among farmers in Pulwama district, Jammu and Kashmir, India. Some of the salient factors that characterise the area that hamper agricultural development include small landholdings, absence of irrigation facilities and inaccessibility to market despite the fact that the area has considerable potential (NITI Aayog 2021).

Methodological Framework

Study Area

The current research is based on the Pulwama district, which is centrally located in Jammu & Kashmir, India. Pulwama district lies between approximately 33°33′ and 34°10′ north latitudes and 74°45′ and 75°35′ east longitudes of the union territory of Jammu and Kashmir, India. High-value horticultural activities complement cereal-based agriculture in the district, particularly the production of apples and saffron (Malik and Hussain 2012), thereby providing a strong foundation for studying technical efficiency at the farm level, within heterogeneous production systems. Moreover, Pulwama is characterised by high heterogeneity in terms of gaining formal access to agricultural credit (Baba et al. 2014). This diverse credit environment allows a regulated analysis of the effect of credit on technical efficiency.

Data Collection

Household-level survey data were collected using a random sampling method to ensure the data were representative and helping to minimise the selection bias. In the first stage, Pulwama was selected as it had unique characteristics mentioned above, which matched the objectives of the study. In the second step, two blocks, Pulwama and Kakapora, were selected randomly out of five blocks. In the third stage, 10 villages in each block were selected based on the geographical dispersion of the villages in order to represent the heterogeneity within the farming conditions and practices. Lastly, on the fourth stage, the farm households were chosen among each village based on the list of agricultural credit application and approved borrowers provided by the available banking institutions. In each village, 10–12 borrower households were chosen at random, this was in proportion to the number of borrower households that belonged to three loan-size categories (below 2 lakh, 2–5 lakh and above 5 lakh) so that small, medium and large borrowers are represented and to ensure that there is sufficient statistical power to compare the outcomes of the analyses. The same number count of control group was selected from the same villages, as suggested by Heckman et al. (1997). The final sample was 412 farming households, which was selected through the Krejcie and Morgan (1970) formula. Further data analyses were made with the help of Stata version 16.

Rationale Behind Using Stochastic Frontier Analysis (SFA) and the Tobit Model

This study uses SFA to estimate farm-level technical efficiency, given that agricultural production is inherently prone to random shocks, including weather variability, pest incidence and measurement errors beyond farmers. In contrast to deterministic or non-parametric approaches, SFA explicitly separates the stochastic noise component and the non-negative inefficiency component of the error term, providing a more realistic description of the agricultural production processes (Aigner et al. 1977; Battese and Coelli 1995). Moreover, SFA has been widely used in the literature to understand the links between access to credit and farm efficiency, and they are thus ensuring comparability and methodological robustness.

Given that the technical efficiency scores are bounded between 0 and 1, the Tobit model is suitable; it accounts for the censored nature of the dependent variable and partially addresses the bias that may arise from ordinary least squares estimation. The Tobit framework has been widely used in efficiency studies to analyse the effect of socio-economic, institutional and credit-related factors on the level of farm efficiency (Bravo-Ureta et al. 2007; Coelli and Battese 1996). The combined SFA-Tobit approach, therefore, offers a coherent framework for first measuring efficiency and then explaining its variation among farm households.

Econometric Specification and Variables

SFA is a parametric approach that assumes a specific functional form among the various functional forms available in the literature. This study adopts the Cobb–Douglas functional specification, with the model for the ith farm specified as follows:

where

yi is the observed farm productivity of the ith farm;

xi is the representation of inputs;

vi captures statistical noise and is supposed to be independent and identically distributed (iid) with N(0, σv2);

ui is the inefficiency term, independently identified, with N(µi,σu2), truncated to zero to ensure non-negativity.

For the ith farm, technical efficiency is assessed on a scale from 0 to 1, where 1 signifies full technical efficiency and 0 denotes complete inefficiency. The composite error terms

The conventional two-step SFA may produce biased and inconsistent estimates due to the independence violation; therefore, Battese and Coelli (1995) proposed a one-step, parameterised approach that jointly estimates the frontier and inefficiency effects.

where

The vector

Building confidence intervals is straightforward, as it involves specifying the distributional conventions for the random variables. Li and Ui are the lower bound and upper bound of (1 – α). The TEi is a monotonic transformation of

From the above equations, the quantiles zL and zU are calculated as:

Z~N(0,1), so the corresponding quantiles can be obtained through:

Follows the standard normal cumulative density function.

Empirical Model

The empirical model used to calculate the technical efficiency uses the following Cobb–Douglas function specification, given below:

Following Equation (2), the SFA parameters are predictable using maximum likelihood estimation (MLE), with the likelihood function derived in terms of the two variance parameters, as specified in Battese and Coelli (1995).

The parameter

Tobit Model

To examine the determining factor of farmers’ technical efficiency, a Tobit regression model is employed, as it is appropriate for dependent variables that are censored and may take both continuous and limited values. The model is quantified as follows:

Latent variable yi* represents the score of the efficiency level of farm j, and 훽 is a group of unknown parameters. Xjm is a pattern of independent variables of farm j (m = 1, 2… k). The error term

In Equation (8), yi is the limited dependent variable that is the score of technical efficiency, and yi* is the censored (observed) variable. The independent variables are denoted by the vector Xi, and the unknown parameters are illustrated by the vector β.

The Tobit model has the following explanatory variables: Age, education, farming experience, farming experience squared, occupation, household size, membership, farm size, household assets, credit access and distance to the farmland. The error term

Definitions and Units of Measurement of Variables.

Empirical Findings

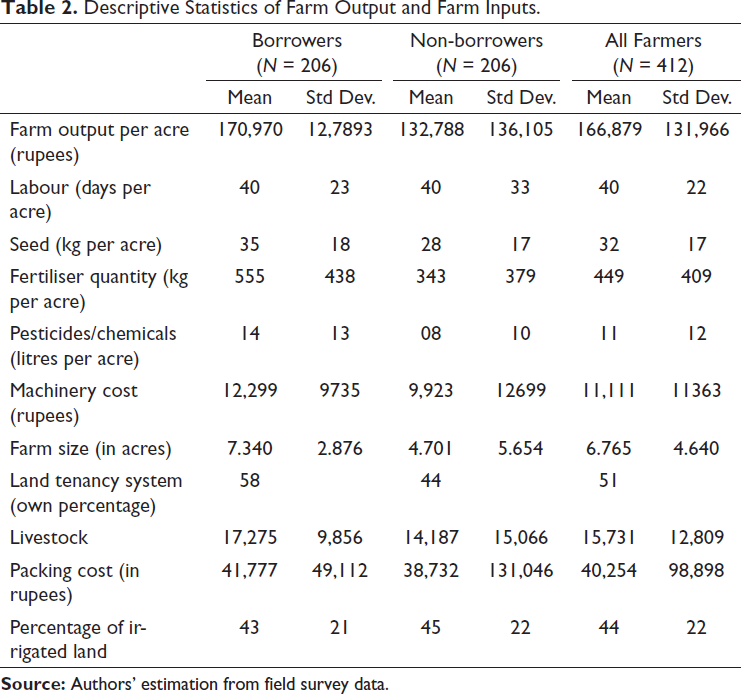

Descriptive Statistics of Farm Output and Farm Inputs.

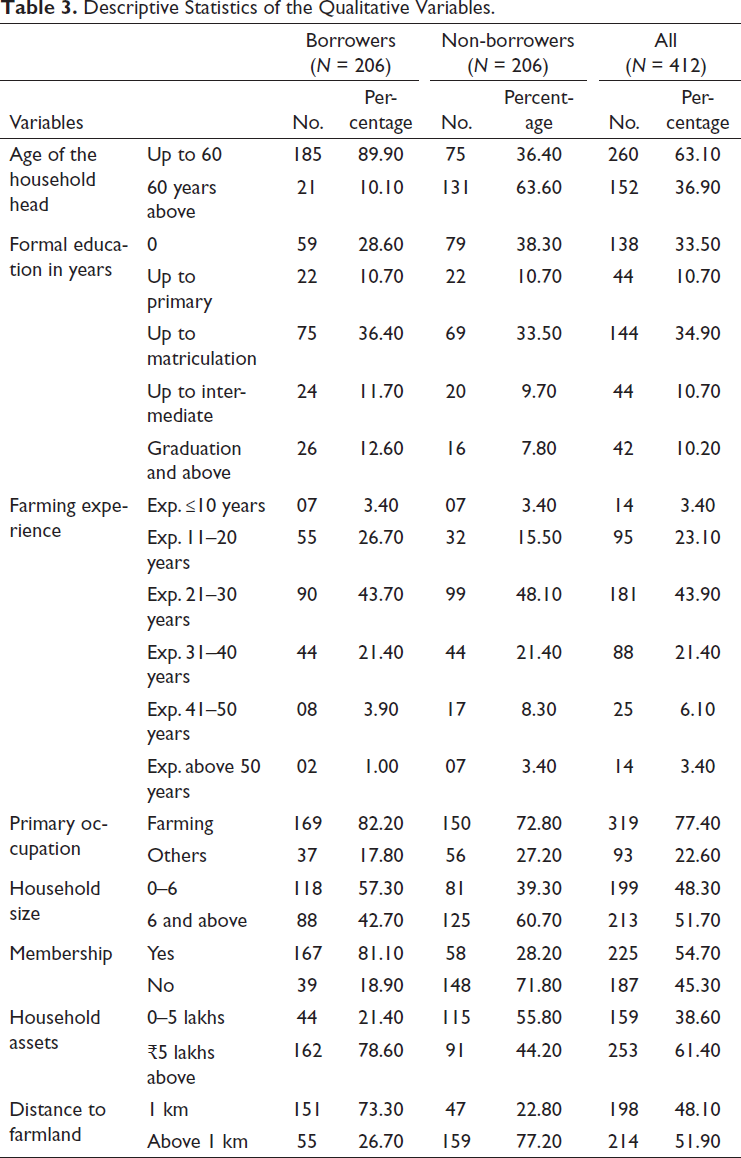

The descriptive statistics are presented in Table 3, which indicates that nearly 90% of borrowing farmers are under 60 years old. In contrast, only 36.4% of respondents were in the non-borrower group. The household size among borrowing households is 57.3%, comprising groups of 0–6 members, whereas among non-borrowers, only 39.3% belong to this group. 60.7% of non-borrower farmers have families comprising more than 10 members, while 42.7% of borrower farmers fall into this category. Overall, 82% of borrowing farmers identify farming as their primary occupation, while 17.8% engage in other professions (government, business, shopkeeper, private employee or other). In contrast, these figures are 72.8% and 27.2% among non-borrowing farmers. Additionally, only 28.2% of non-borrower farmers have a membership, whereas 81.1% of borrower farmers do. Only 21.4% of borrowing farmers had household assets valued below ₹5 lakhs, while 78.6% had assets valued above ₹5 lakhs. In contrast, only 44.2% of non-borrowing farmers own household assets exceeding 5 lakhs.

Descriptive Statistics of the Qualitative Variables.

Regarding the distance to the farmland, over 73% of borrowing farmers have their nearest farmland within 1 km. In comparison, just 22.8% of non-borrowing farmers. The education status indicates that 33.5% of farmers are illiterate, and 10.7% of farmers have an education level up to primary school. The non-borrowers had a lower school matriculation rate than those who did borrow (33.5% compared to 36.4%). Furthermore, only 10.2% of the sampled farmers had a graduation level or higher; however, this ratio was lower among non-borrowers than among borrowers (7.8% vs 12.6%). Farming experience is quantified by the number of years of farm experience. 44% of Non-borrower farmers had 21–30 years of farming experience, but over 48% of borrower farmers did. Farmers with more extensive agricultural experience tend to obtain credit more readily than those with less experience.

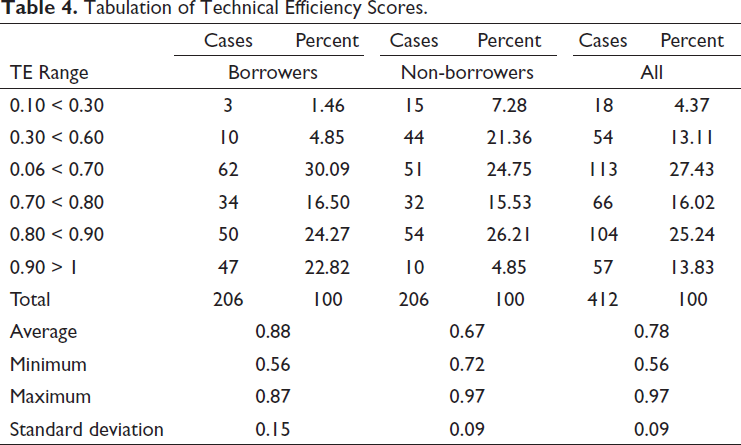

The technical efficiency scores for borrowers and non-borrowers are presented in Table 4. The technical efficiency score ranges between 0.56 and 0.97 for the selected sample formers. On average, the technical efficiency score is 0.78. The findings revealed that 78% of the farmers are technically efficient and 22% are relatively inefficient. Only 13.83% of respondents reported a technical efficiency above 90%, with the highest proportion, 22%, among borrowers. Moreover, 25% of the respondents indicated that their scores ranged from 80% to 90%, which is almost the same with both the borrowers and non-borrowers. Another 16.2% of respondents received a mark of 70%–80%. Most (27.4%) were in the 60%–70% range. In general, the statistics indicate that the rise in technical efficiency is linked to an increase in the percentage of borrowing farmers and a subsequent decrease in the percentage of non-borrowing farmers.

Tabulation of Technical Efficiency Scores.

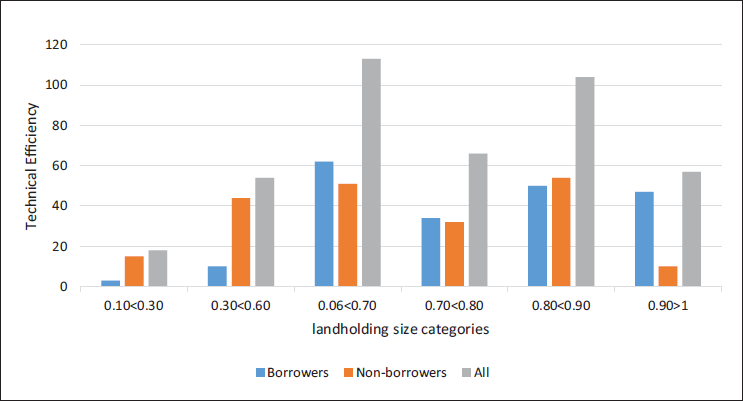

Figure 1 shows a bar chart of average technical efficiency scores for borrowers and non-borrowers, with a great difference between the two groups. Borrowers are more technically efficient than non-borrowers, suggesting that access to credit plays a significant role in farm performance. The greatest differences are observed in the efficiency range above 0.90; therefore, interventions are required to close the gap between the two samples. Overall, the model proves that access to credit is a key indicator of technical efficiency among farm households.

Technical Efficiency of Borrowers, Non-borrowers and Total Farmers Across Different Landholding Size.

Results from the SFA

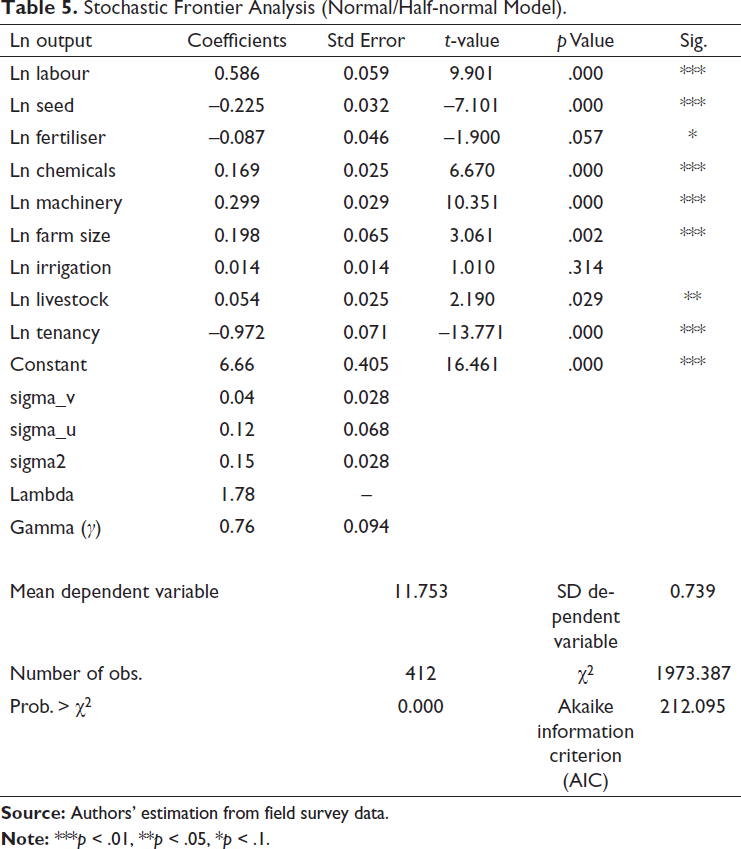

The stochastic production frontier estimates shown in Table 5 indicate that factors such as labour, chemicals, machinery, livestock and farm size positively influence agricultural output, and the relationship is also significant. The labour elasticities are quite large, indicating that the marginal productivity growth exceeds the proportional growth in labour input. One unit of labour will increase farm productivity by 0.58%. By keeping other determinants unchanged, a 1% increase in chemical use results in a 0.16% increase in productivity. Mechanisation is also found to have a positive and significant influence on agricultural output; that is, a 1% increase in machinery inputs leads to a productivity improvement of 0.29%. Moreover, animal assets have a significant positive effect; a one-unit increase in the stock of animals leads to a 0.05% increase in productivity. Irrigation projections indicate that the productivity would be positively influenced, but this relationship is not significant. On the same note, farm size is positively linked to productivity, and an increase of 1 acre in farm size is estimated to increase productivity by 0.97. Agricultural productivity is negatively influenced by seed costs, and the relationship is also significant. A 1% increase in seed costs resulted in a 0.22% decrease in agricultural productivity. In the study area, 76% of farmers continue to use conventional seeds, as indicated by descriptive statistics. Moreover, the findings suggest that chemical fertilisers have an adverse effect on agricultural productivity; however, this effect is insignificant at 5% level. The link between land tenancy and productivity is negative and very strong. It appears that tenant farmers are significantly less productive than landowners. Lastly, the computed λ suggests that TE is significant in elucidating output variability. The gamma value is 0.76, indicating that 76% of the inefficiency is attributed to the input constraint, rather than to random shocks. It can be concluded that technical inefficiency measurement is important, making the SFA method the most suitable for this analysis.

Stochastic Frontier Analysis (Normal/Half-normal Model).

Factors Determining Technical Efficiency (Tobit Model Results)

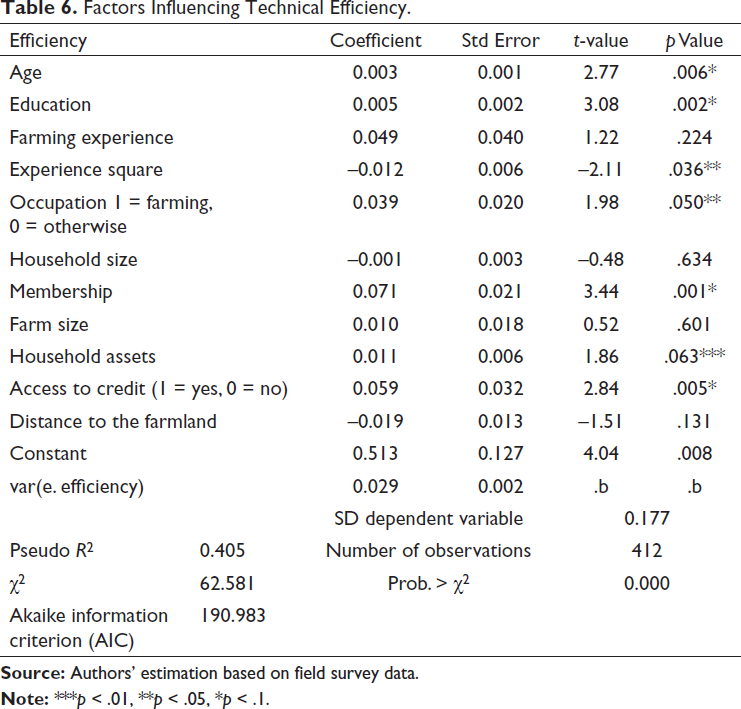

The estimated outcomes from the Tobit regression indicate that several factors significantly influence farm technical efficiency. The factors that determine farm technical efficiency are presented in Table 6. The estimated results indicate that Pseudo R² = 0.405 and χ² = 62.58, p < .01, indicating that the encompassed variables have a substantial impact on farm technical efficiency. The age of the household head has a positive and significant impact on farm technical efficiency, which suggests that older farmers are more likely to use the resources available to them efficiently, thereby reflecting greater technical efficiency. Farm experience has been found to be non-linear with farm technical efficiency, indicating that the number of years spent in farming does not always have a consistent influence on the technical efficiency. The potential causes can be related to the decreased physical abilities and slower adaptation to modern technologies. The findings indicate that farmers’ educational attainment contributes positively and significantly to improvements in technical efficiency. Generally, it has been observed that the higher a farmer’s level of schooling, the higher the technical efficiency. This implies that the more years of education a farmer has attained, the more they are able to grasp new and innovative agricultural production methods. Farming as a primary occupation has positively and significantly influenced farm technical efficiency, indicating that the greater a farmer’s dependence on agriculture, the higher their farm’s technical efficiency. Membership and farm technical efficiency are positively and significantly related, meaning that the higher a farmer’s position within a cooperative, self-help group, farm organisation or similar network, the higher their farm technical efficiency. The size of the farm has a positive and significant influence on its technical efficiency, indicating that larger farms are more efficient than smaller ones. The potential causes could be due to economies of scale and enhanced access to resources. The technical efficiency of farms is also positively associated with household assets, indicating that the more assets farmers possess, the more efficiently the household manages farm operations. In addition, the research found that credit access is a significant factor that increases farmers’ technical efficiency. The availability of credit can help farmers purchase inputs on time, invest in new technology, manage liquidity constraints and mitigate production risks more effectively. The high and strong level indicates that credit has a strong and steady influence on efficiency improvement. On the other hand, distance to the farm land and household size show a negative correlation with farm technical efficiency, although the correlation is not significant, suggesting that the impact is not strong enough to make a meaningful conclusion.

Factors Influencing Technical Efficiency.

Result Discussion

The estimated results from stochastic production results provide insights into the structure of agricultural production and its efficiency. The variables that positively and significantly affect agricultural output are labour, chemicals, machinery, livestock and farm size. The coefficients indicate the percentage change in the output against each input. The coefficient of labour (0.586) indicates that a 1% change in labour use increases output by 0.58%, highlighting labour-intensive farming. The use of chemicals is also a positive contributor (0.169) and hence a 1% growth will lead to a 0.16% growth in output. The results are consistent with previous studies by Battese and Coelli (1995) and Bravo-Ureta and Pinheiro (1997). Output is further increased by mechanisation and livestock holding, with the elasticity of 0.229 and 0.054, respectively. Similar results have been reported by Binam et al. (2004), who found that mechanisation and livestock holdings are complementary, helping to alleviate labour shortages, enhance soil fertility with manure and assist farmers in carrying out their agricultural activities on time. The size of the farm has a very strong positive impact, where a 1-acre increase in farm size leads to a 0.97% increase in output. The results are in line with Coelli and Battese (1996) and Ogundele and Okoruwa (2006). Seed prices, on the other hand, have a negative effect on farm production; the effect of seed price increase by 1% decreases farm production by 0.22%. The finding is consistent with the findings by Haji (2007) and Tadesse and Krishnamoorthy (1997), who have indicated that an increase in input prices discourages optimal input utilisation among the smallholders. It is also indicated that the output per acre of tenant farmers is lower compared with that of landowners. Same results are reported by Rahman and Umar (2009). Moreover, the fact that the percentage of output change that can be attributed to the technical inefficiency (76%) is high proves that inefficiency is more of a constraint to farm output, which is consistent with Battese and Coelli’s (1995) findings.

Besides production inputs, the study found that age and farming experience are positively and significantly related to technical efficiency, as more experienced farmers make better decisions and choices. The results are in agreement with those published by Battese and Coelli (1995) and Rahman and Umar (2009). However, the squared term of experience coefficient is negative, which is consistent with Coelli and Battese (1996) and Abdulai and Huffman (2000). Education is also positively related to technical efficiency, indicating that the educated farmers are more knowledgeable and use modern technologies to enhance farm production. These results are consistent with Bravo-Ureta and Pinheiro (1997) and Binam et al. (2004). Farming as a main occupation of farmers is more productive, and this finding has been affirmed by Haji (2007) and Ogundele and Okoruwa (2006). Membership of any far group is a key way of increasing efficiency since it makes information, common resources and extension services available, as is evident in the case of Tadesse and Krishnamoorthy (1997) and Binam et al. (2004). The farm size has a positive effect on the technical efficiency, which is consistent with the findings of Coelli and Battese (1996) and Bravo-Ureta and Pinheiro (1997) that larger farms enjoy economies of scale and are able to invest in modern inputs. Household asset ownership is also a factor of increased technical efficiency, as also reported by Binam et al. (2004). Technical efficiency is significantly positively correlated with access to credit, which is supported by Abdulai and Huffman (2000), Ogundele and Okoruwa (2006) and Arshad (2022). By providing credit, the farmers get to buy high-quality inputs and technology that reduces risk, hence stabilising production. The combination of these outcomes suggests that the key factors affecting farm technical efficiency in small and marginal farmers are human capital, institutional participation, asset ownership and financial accessibility.

Conclusions and Policy Implications

The study investigates the effect of institutional credit on farm technical efficiency from the field experiment. The estimated results indicate that institutional credit exerts a positive and significant impact on farm-level technical efficiency. Borrower farmers not only achieve higher output but also utilise available resources more efficiently, indicating that access to credit relaxes liquidity constraints, enables timely input use, and facilitates the adoption of productive-enhancing technologies and farming practices. The mean technical efficiency for borrower farmers (0.88) is higher than that for non-borrower farmers (0.67), indicating that output could be increased by 12% and 33%, respectively, without increasing inputs. The model further reveals that the output differences are due to inefficiency rather than random noise, as the estimated gamma value of 0.76 signifies that 76% of fluctuations are attributable to inefficiencies. Age, education, farm experience, primary engagement in farming, membership in an organisation, farm size, household assets and access to institutional credit all positively influence technical efficiency, whereas experience square, household size and distance to farmland negatively affect efficiency.

The study suggests that strengthening socio-economic, farm and institutional support to improve credit access can significantly reduce inefficiency levels. Additionally, it will facilitate the adoption of modern agricultural practices, thereby helping reduce the technological gap. Timely and adequate credit aligned with crop calendars and complemented by credit delivery with basic advisory support should be ensured by financial institutions to enhance the productive use of funds. To facilitate easy access to credit, cooperatives should strengthen their role in providing access to credit, shared assets and knowledge dissemination, particularly for small and asset-constrained farmers. Policymakers should integrate credit expansion with farmer financial education and promote asset-building and farm consolidation initiatives, and invest in rural infrastructure to reduce efficiency losses associated with distant farmland. These coordinated actions are essential to translate institutional credit access into sustained efficiency gains, higher productivity and improved rural livelihoods.

Limitations of the Study

Although this study provides important insights into the nexus between access to formal credit and farm technical efficiency, it faces several constraints. First, the study uses cross-sectional data, which means it cannot account for temporal variations in farm technical efficiency. Second, the results are area-specific and cannot be extrapolated to other areas that lack agro-ecological and socio-economic similarities. Third, the SFA assumes a particular functional form (Cobb–Douglas), which implies that the production process can be largely non-linear and complex. Lastly, whereas observations of borrowers and non-borrowers are useful for controlling for observable variability, unobserved heterogeneity can affect the estimated effect of credit access. Despite these limitations, the study provides important empirical data on the effects of formal credit on agricultural efficiency and subsistence livelihood.

Footnotes

Acknowledgement

The authors thank anonymous reviewers for their valuable comments and suggestions to improve the manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.