Abstract

This study aims at identifying the determinants of corporate governance that impact corporate risk disclosure in India’s top non-financial listed companies based on market capitalisation. The analysis of the study is based on risk disclosure practices of the leading non-financial listed companies using annual reports as well as risk disclosure practices in the presence of various regulations. The risk exposure is measured using manual content analysis while the impact is analysed using multiple regression. The empirical findings reveal that the corporate risk disclosure level has improved significantly. The major corporate governance variables namely board size and ownership are insignificant to risk disclosure whereas audit committee meetings and role duality are somewhat significant. Firms having bigger size plays a major role in risk disclosure practices of companies, on the other hand, liquidity and growth of the firm do not influence risk disclosure practice. Due to the constant fallouts of companies, this paper tries to analyse the role of corporate governance practices in minimising companies’ risk exposure. The results of the study help analyse the failures in corporate governance practices that lead to companies’ poor disclosure policies.

Introduction

Corporate risk disclosure is one of the most crucial terms that is gaining importance in recent times. With increasing corporate failures, this is turning all the more important for companies to have strict disclosure norms adoption. Globally the fallout of big business houses, such as Enron, Tyco, WorldCom, etc., has shaken the world and global final crisis where further events considered as the main reason for the corporate fallouts, which aggravated the problem. These major global events have shaken the trust of investors at large.

India has its experience alike Enron, i.e., Satyam Scam, wherein the CEO of Satyam Computers admitted to manipulating company accounts by US$1.47 billion. Despite regulations becoming stricter since then in India, there still exists an increase in frauds such as Harshad Mehta, Sahara India, Nirav Modi, etc., which clearly shows how promoters, financial institutions and banks are fooled easily of their invested money. The common issue that generally existed in these scams was the presence of India’s most powerful class and top business groups, who used hard-earned investors’ money of billions of dollars. Another major flaw in the Indian business structure has been the involvement of family-governed businesses. The board in such companies is usually comprised of family, friends and relatives, which lacks transparency.

Corporate governance regulations aim at providing transparency, fairness and accountability in an organisation. The scandals that occurred in the past have increased shareholders’ concern and created the need for making the board more effective. The aftermath of such a crisis has completely changed the board structure. Many countries have introduced various new codes of corporate governance to maintain the trust of shareholders, which are focussing more on board independence and the role of the board of directors (Grinstein & Valles Arellano, 2011). The demand for corporate ethics and stricter rules and regulation have aroused a need for mandatory corporate governance disclosure rules.

Global disclosure standards existed since the start of corporate failure, still, companies believe in modifying to be followed at their own ease and comfort. This situation was equally alarming for both developed and developing nations across the globe. Companies use to disclose risk information based on their own will and in their own preferred way. The information was disclosed without considering its relevance, its identification and proper measurement (Mohobbot & Noriyuki, 2005). Considering the scenario, the Institute of Chartered Accountants in England and Wales (ICAEW) (Authors, 2002) mentioned that companies are required to mention in annual reports any information relating to risk; further, it also stated for listed companies to disclose any sort of relevant information to their investors. Stricter corporate governance reforms can lead to a reduction in the risk-taking capacity of Indian companies. This would positively affect the firm value, shareholder’s trust and overall profitability and improve the investment decisions of the organisation (Koirala et al., 2020).

Many studies have been conducted internationally (Abraham & Cox, 2007; Berger, 2012; Elshandidy et al., 2013, 2015; Koirala et al., 2020; Linsley & Shrives, 2006; Miihkinen, 2012; Saggar & Singh, 2017) these studies have focussed on disclosure of risk information. In the Indian context, as well as researchers working in the same area (Ahnan et al., 2020; Khandelwal et al., 2020; Saggar & Singh, 2017, 2019), who are analysing the diversified relationship between risk and governance, there has been some work related to financial disclosure and governance consisting of some common variables such as board characteristics and ownership (Raithatha & Bapat, 2014). Risk information disclosure helps a company in gaining investors’ trust, determining stock prices of the company and further the profitability. A company that discloses risk information transparently in annual reports is considered more transparent and has a greater market reputation (Abraham & Cox, 2007; Abraham & Shrives, 2014).

With this outlook, managers in companies are involved in the voluntary disclosure of information, which is considered a part of strategic decision-making. According to agency theory, voluntary disclosure helps in curtailing the cost of the company. It is considered a primary responsibility of managers to disclose information in order to protect shareholders’ interest (Fama & Jensen, 1983). The rising need for risk information has motivated research in particular area, with a focus on analysing the relation between firm characteristics, ownership structure and risk disclosure (Abraham & Cox, 2007; Elshandidy et al., 2015; Hernández Madrigal et al., 2015).

Much of the prior research has been carried out on developed nations and their focus has been on firm characteristics, accounting disclosures, i.e., measuring of financial risk of companies (Abraham & Shrives, 2014; Mokhtar & Mellett, 2013). In the context of a developing nation such as India, with the rise in scams, risk disclosure is turning a priority, disclosure practices are considered to be voluntary practices which with multiple regulations have been made mandatory by the Securities and Exchange Board of India (SEBI) as stated in its consultative paper (Committee & Committee, 2017). SEBI in order to protect companies and shareholders trust has been working consistently to bring in more efficient and stricter norms to protect companies from falling out. Ensuring timely and efficient risk disclosure is a challenge for policymakers (Sexena et al., 2017).

This study is an attempt to bridge the gap between risk disclosure and corporate governance norms with special reference to countries like India. This paper is an attempt to figure out the existing literature in the context of corporate disclosure practices and how risk disclosure and governance are related. This paper is divided into four sections. First, we will try to explore the risk disclosure practice adopted by Indian companies. Second, we will try to explore the current risk regulations prevailing in India. Third, we find out the possible reasons for multiple corporate fallouts. Lastly, we explore a relationship between corporate governance and risk disclosure based on the literature.

Literature on Risk Disclosure

Risk disclosure focuses on the communication of risk-related information as part of companies’ annual reports. They give insight into risk exposure level of the company, which is beneficial for decision-making from the investors point of view. Risk disclosure norms in the context to India are governed by SEBI as part of corporate governance rules by clause 49, for which a separate section is mentioned in the company’s annual reports (Berger, 2012).

The ICAEW has been a pioneering institute in spreading awareness about risk disclosure. It promoted the idea mainly for listed companies that their annual reports must have risk disclosure. It raised many concerns highlighting the prime importance of risk disclosure. It also laid down the relation of risk disclosure with cost. Better risk information leads to efficient allocation of capital (Authors, 2002).

Risk disclosure is mainly required due to a number of reasons. It helps business entity in analysing their risk that will influence investing, financing and dividend decisions of a company. Series of codes have been mandatory in the United States, the UK and Germany, despite that large amount of risk information is still voluntary (Elshandidy et al., 2015).

Previous researchers have explored the concept of risk from various angles. Some focussed on quality of risk disclosure whereas some focused on the extent of disclosure (Elshandidy et al., 2018; Elshandidy & Gan, 2020; Hernández Madrigal et al., 2015; Linsley & Shrives, 2006; Meijer, 2011; Miihkinen, 2012; Saggar & Singh, 2019; Salem et al., 2019). The primary responsibility of risk disclosure lies with managers, whose mandatory task is disclosing risk to maintain shareholders interest (Berger, 2012; Elshandidy et al., 2015).

If a firm wishes to reduce its cost of capital by raising market confidence, it must disclose its risk management policies. Improvement in risk disclosure helps investors in taking effective decisions. Directors of the company are required to explain the risk-facing threats in a company (Linsley & Shrives, 2006).

Risk is described in literature with various names. All the words with their synonyms are taken as proxy to analyse the risk disclosure and governance linkage in the annual reports of the company. Risk disclosure depends from company to company and varies from country to country based on regulation and accounting standards followed, it is dependent on the nature of auditor appointment and financial reporting practices (Serafimoska et al., 2015).

Corporate Governance and Risk Disclosure Indian Scenario

Risk is defined under ISO 31000, as the effect of uncertainty on objectives. Risk management, however, deals with the overall process of identifying risk, evaluating, acceptance and management. The whole process of measuring risk is time-consuming.

Corporate governance is a concern with maximising shareholders’ wealth by promoting fairness and transparency in an organisation. It is about raising the trust and confidence among the stakeholders in the manner of working of the company. There are three major stakeholders in corporate governance. First, the shareholders who invest their money in a company. Second, the management who is responsible to the board of directors. Third, the board of directors are elected by shareholders.

Good corporate governance contributes to the better working of the company. It facilitates efficient and effective working that maximise shareholders value. Corporate governance is linked to a variety of concepts and risk management is one of the most crucial. Risk management helps organisation in taking all major decisions effectively. Better governance leads to more transparent organisation that will encourage more shareholders’ investment. It is considered that a firm which manages risk effectively has better corporate governance.

In the context of countries like India, rules pertaining to risk reporting are governed by the SEBI, Ministry of Corporate Affairs (MCA) and the Institute of Chartered Accountants of India (ICAI). SEBI over the years together with MCA has been working to provide efficient working platform for companies. The working of companies became smooth with the creation of some mandatory and voluntary committees.

In 2015, to strengthen the listed companies and to build the trust of shareholders, SEBI introduced the Listing Obligations and Disclosure Requirement (LODR) Regulations, 2015. The major focus of regulations was to build in transparency in the governance system, with SEBI introducing regulation 21, focussing on the creation of a mandatory risk management company. The regulation states that:

The board of director are required to constitute a Risk Management Committee; which shall comprise of members who are senior executives of listed companies. Further, this regulation was initially applicable to top 500 companies based on market capitalisation, which was extended top 1000 companies by SEBI. The risk management committee is required to conduct its meeting twice a year.

Further, the Companies Act 2013 also mentions certain provisions in the context of risk management. The Act does not clearly mention the creation of risk management committee, but it emphasises on the role of directors including independent directors in the context to risk management. These provisions are mentioned in Sections 134 and 177. Section 134 deals with a statement containing the development and risk management policy of the company. It is required that such report define the possible threat factors for the company. Section 177 deals with the evaluation of internal financial control and risk by the audit committee.

Despite continuous efforts of regulators, we could still find out some flaws in the existing structure of companies. Risk of companies is turning all-time high, the information on risk that could be traced from annual reports of companies is a small chunk of information that could be the only possible evident reason for measuring risk (Saggar & Singh, 2017). Risk management is directly related to good governance practices, despite the hard work of regulators—upcoming mandatory regulations, creation of committees, still the status is complicated.

Literature Review and Hypothesis Development

Compare to various other reporting practices, risk-reporting literature is scarce; there are very few studies in the context of India that examine the determinants of risk reporting. Prior studies were able to analyse the risk disclosure practices in different countries (Abraham & Cox, 2007; Hernández Madrigal et al., 2015; Linsley & Shrives, 2006; Neri et al., 2018) but we no such study is available in context to India. Risk is an inherent part of any organisation, in developing countries despite the existence of mandatory rules, timely assessment of risk is lacking (Saggar & Singh, 2017). Some of the researchers have tried hard to analyse the risk disclosure practices, voluntary and mandatory disclosure (Elshandidy et al., 2013, 2015; Miihkinen, 2012) yet they were unable to address the reason behind the risk.

Corporate Governance Variables

Board Size

Board size largely affects the firm performance and working of the board of the company. The appropriate and an optimal board size has always been a debatable topic in research. Increased board sizes are always preferred over the smaller ones as they add to a diversified board structure with a broader approach (Arora & Sharma, 2016; Fama & Jensen, 1983; Prasanna & Geeta, 2016). Prasanna and Geeta (2016) added that bigger board size further leads to more volatility and is considered better in terms of the risk-taking capacity of the board. Large board sizes are considered efficient in terms of organisations as it helps them in recusing the agency cost, leading to greater level of earnings and information disclosure (Neri et al., 2018). On the contrary, there exist theories that have highlighted that smaller board size are much better than larger ones leading to better decision-making and corporate disclosure (Fama & Jensen, 1983).

As per SEBI regulations, in the context of India, there are no clear-cut guidelines regarding board size. However, SEBI strictly mentions in context to listed companies in India to have an optimal combination of the board comprising of executive and non—executive directors. Fifty percent of board must comprise non-executive directors of which the chairman must be a non-executive director and there must be one woman director on board for all listed companies in India.

Board size has an effect on board meetings as well, bigger boards have more meetings and better risk monitoring. There exists a significant difference in the working of companies based on their board sizes. Larger boards are preferred over smaller ones, but again this is still a researchable concern (Mishra & Kapil, 2018)

Thus, board size plays a crucial role in all-important matters of the company and therefore it is directly linked to risk disclosure.

H1: There is a positive relationship between board size and risk disclosure in Indian listed companies.

Role Duality

Board leadership structure is often encountered with two schools of thought. Agency theory combines the board roles, i.e., CEO duality, where in single person dominates the board making it more effective. Stewardship theory believes in separating the two board roles, according to them centralisation of power hampers the growth of company (JENSEN, 1993). There exists no guarantee that changing the structure of firm or splitting the roles will have a positive effect on firm performance; hence, this will not affect the firm performance (Chen et al., 2008).

Steward behaviour is considered usually cooperation oriented and in general is motivated by intrinsic rewards than extrinsic ones. Hence, stewards are usually placed on higher value in terms of organisational behaviour, but they internalise organisational benefit with their self-interest (Boyd et al., 2010). Role duality leads to concentration in decision-making in a few hands due to which CEO would dominate the board and there are chances of information biases preventing access to risk information (Alshirah et al., 2020).

Most of the studies have been undertaken to identify the impact of CEO duality. Malaysia Code of Corporate Governance (2000), 1 recommended the role of CEO and chairman must be held by two people separately in order to ensure the balance of power and prevents a single person from dominating the board of companies.

Literature on CEO duality and risk disclosure shows mixed opinion among researchers., where some of studies showed no impact (Arora & Sharma, 2016; Kaur & Singh, 2018; Krause et al., 2014) while others showed a negative impact (Brickley et al., 1994; Ibrahim et al., 2019; JENSEN, 1993; Linsley et al., 2015; Mishra & Kapil, 2018). Risk disclosure literature did not find any effect of CEO duality on the disclosure norms of the company (Mokhtar & Mellett, 2013).

In context to India clause 49, has no mention of any specific guidelines pertaining to the separation of board roles or combining of roles. Recently SEBI introduced their SEBI [LODR] Regulations stating it mandatory for all listed companies in India to have a separate CEO and managing director. The rule emphasised maintaining transparency and efficient work and averting risk in companies.

H2: There is a negative relationship of CEO duality and firm performance in the case of Indian listed companies.

Ownership Structure

Corporate governance functions and practices help to develop an ownership structure for a company and are the most important aspects. Ownership structure means the proportion of shares held by various parties in the equity capital of the company. Among various shareholders in the company having different power with respect to decision-making, ownership structure plays a crucial role. In the context of India to a large extent, performance and major decisions of the company are affected by ownership structure (Manna et al., 2016). The agency theory states that there will be less information asymmetry where the ownership concentration is higher, whereas if there is greater diffusion in ownership more disclosures are required (Fama & Jensen, 1983).

Some studies have offered a different view wherein small shareholders are considered less focussed in terms of efficient management, which increases the marginal cost of the company due to increase in agency cost (Fama & Jensen, 1983; Neri et al., 2018). Companies perform well in the case of small shareholders where there exists a concentration of power as it leads to better control (Neri et al., 2018). Companies with concentrated ownership usually have less voluntary disclosure practices because controlling shareholders can easily monitor the working of the shareholders and have direct access to all-important information (Saggar & Singh, 2017). Ownership structure, to a larger extent, determines whether risk-taking and regulation are interacting with each other (Ellul, 2015). Empirically various researchers have found a negative relationship between ownership and risk disclosure information, whereas there still exists a relation between voluntary disclosure and ownership structure (Mokhtar & Mellett, 2013).

SEBI has laid down a limit of 75% for the promoter group in Indian listed companies. Since the concentration of ownership is linked to risk disclosure practices; therefore, it leads to the following hypothesis.

H3: The ownership structure affects the risk disclosure positively in Indian listed companies.

Audit Committee

The audit committee is the most important pillar of corporate governance, which plays an important role in monitoring and controlling. The audit committee of a company determines the working of the company and how efficiently and effectively the company is working. A major issue faced by the audit committee is its independence in management. The external auditor are responsible for the truthfulness of financial data and that is dependent on information provided by internal management (Almaqtari et al., 2020; Salem et al., 2019; Sarkar et al., 2012). A well-qualified and independent auditor plays a major role in protecting the interest of public at large. Larger audit committees usually prefer to have members with wider knowledge and expertise leading to efficient risk management (Salem et al., 2019; Sidhu & Kaur, 2019). Agency theory assumes that a strong audit committee with qualified staff can have control over directors and enhance risk-taking behaviour (Elamer et al., 2018; JENSEN, 1993; Neri et al., 2018). Further some researchers are also in favour of a risk management committee and they prefer a separate committee to an audit committee to deal with risk (Al-Hadi et al., 2016).

In Indian, clause 49 clearly states two thirds of members to be independent and the chairman has to be an independent director. The audit committee is responsible for financial reporting process, selection of independent auditors. The committee helps the board in fulfilling its legal requirements. Further, the audit committee is required to conduct its meeting four times in a year, which is required to attend by minimum two independent directors.

The effective audit environment in a company largely affects the voluntary and mandatory requirements positively. In an efficient audit environment, auditors are free to provide detail analysis of risk management, together with possible remedies to evade the same (Elshandidy et al., 2013).

H4: There is a positive relationship between audit committee meetings and risk disclosure practice.

Control Variables

Firm Size

Firm size is considered one of the most crucial factor, which affects the risk disclosure practices of the company. Larger-sized firms have more control in the decision-making of the company as compared to smaller-sized firms. Firm size and risk disclosure were shown to have a positive relationship in prior studies; further, it also stated that firm size has a bigger role in depicting risky information (Elshandidy et al., 2013, 2015; Miihkinen, 2012). Firm size is considered one of the crucial factors in determining the risk information symmetry in an organisation.

H5: Big Size firm affects risk disclosure practices due to stricter norms.

Liquidity

The companies that have maintained their liquidity prefer to disclose more information as they do not prefer to take risk. The presence of a risk committee in companies affects the risk-bearing capacity of a firm (Lajili, 2007). There is no evidence of liquidity in the context of Indian firms. Neri et al. (2018) have mentioned that an increase in liquidity in the market affects the information asymmetry.

H6: There is a positive relationship between firm’s liquidity and risk disclosure practice.

Firm Growth

Firm growth has been analysed both positively and negatively by researchers. While some researchers are of the view that it affects the disclosure practices, others consider it as having a neutral effect, especially in the Indian context (Khandelwal et al., 2020). In view of this, the following hypothesis is formulated.

H7: There is no association between firm growth and risk disclosure practice.

Methodology

Our sample is drawn from all non-financial listed companies on the Bombay Stock Exchange (BSE), which is the largest stock exchange in India for the period from 2017 to 2020. The sample comprises of top 100 companies listed on BSE as per market capitalisation. We excluded financial firms due to their different reporting and disclosure requirements and different accounting standards. Prior researchers have also excluded financial firms due to their different reporting practice (Linsley et al., 2015; Mokhtar & Mellett, 2013; Neri et al., 2018).

We measured the quality of risk disclosure from annual reports of companies through manual content analysis based on pre-identified keywords from the literature. The annual reports were downloaded from the respective websites of the companies. Further, for data analysis stata version 15 was used to run multiple regression in order to find the relation between corporate risk disclosure and governance variables. Data pertaining to variables have been collected from annual reports of companies.

Dependent Variable and Content Analysis

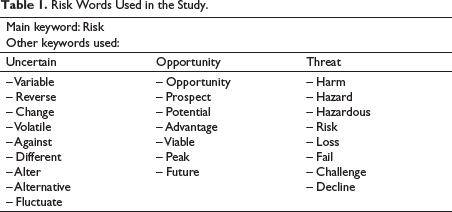

In order to measure the degree of risk disclosure and its impact on corporate governance on Indian listed companies, content analysis appears to be the best method. Prior literature (Abraham & Cox, 2007; Elshandidy et al., 2013, 2015, 2018; Hernández Madrigal et al., 2015; Meijer, 2011; Mokhtar & Mellett, 2013; Saggar & Singh, 2019) has adopted two possible ways of content analysis, it has been done either manually or automatically. The automatic and manual method of content analysis has been adopted. Further for doing content analysis we can use either counting of sentences or counting of words. Since risk is a wide area so we adopted word as a unit of analysis following prior disclosure studies (Abraham & Cox, 2007; Elshandidy et al., 2018; Ibrahim et al., 2019). Linsley and Shrives (2006) have defined risk disclosure in their study based on which we identified risk words in three different categories, namely, uncertain, opportunity and threat.

For the purpose of research, corporate risk disclosure is our dependent variable. We used manual content analysis by analysing listed keywords from the annual reports of a company; regression analysis was conducted using STATA 15. Based on available literature we have identified some major keywords mentioned in Table 1, divided into three subheads, i.e., uncertain, opportunity and threat to calculate risk disclosure. These keywords are counted based on a number of occurrences in annual reports of top 81 companies (excluding financial and banking companies, as financial companies have different reporting requirements and accounting standards) from the total sample of the top 100 companies based on market capitalisation. We excluded duplicate words and excessive repetition of words. We categorised these words based on prior research as identified by Abraham and Cox (2007) and Elshandidy et al. (2013).

Risk Words Used in the Study.

Independent Variables

Model of the Study

where CRD denotes corporate risk disclosure and is a score of the sum of all keywords mentioned above and some commonly identified risk sentences from annual reports of the top 82 non-financial companies listed on the stock exchange.

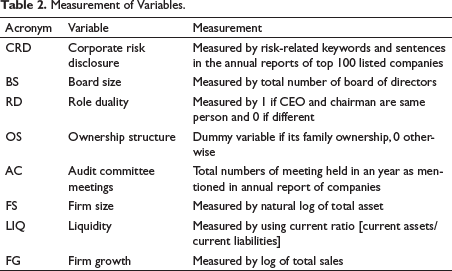

Definition of all variables used in the study is mentioned in Table 2.

Measurement of Variables.

Results and Discussion

Descriptive Statistics

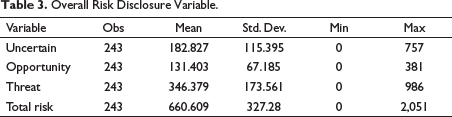

The study tries to examine the relation between corporate governance and risk disclosure practices being adopted by the top 100 listed companies in India. We begin the analysis by analysing identified risk variables based on literature. These variables were categorised into uncertain, opportunity and threat [refer Table 3 above]. The descriptive statistics reveal that the maximum number of times risk appeared in annual reports of the top 100 listed companies in 2051, over the period of three years. The variable uncertain (including keywords) occurred 757 times compared to opportunity (including keywords) at 381 times and threat (including keywords) at 986 times.

The descriptive statistics clearly point towards uncertain and threat as major players in risk disclosure practices of any company, which is indirectly targeting towards stricter norms or regulations for risk disclosure in the context of Indian companies.

Overall Risk Disclosure Variable.

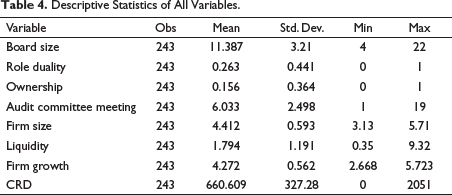

Descriptive statistics related to dependent variables (CRD), independent variable (board size, role duality, ownership, audit committee meeting) and control variables (firm size, liquidity, firm growth) are mentioned in Table 4.

Descriptive Statistics of All Variables.

It can be observed that the corporate risk disclosure (CRD) score is 660.609, with a minimum value of zero and the maximum value is 2051, which clearly states that risk disclosure practices have improved tremendously by Indian corporates.

Similarly, we have a look at board size most corporates have a sound board structure, none of the company is having a board size of fewer than 4 members which is extended to 22 as maximum board size, which is a good number as per the Companies Act 2013. Role duality is at a mean of 0.263, so there still are corporates holding CEO and chairman at the same post, this needs stricter compliance. According to SEBI (LODR) Regulation, 2015, this position needs to be held by different individuals. We can observe a wide variation in the conduct of audit committee meetings for broader transparency this ranges from a minimum of 1 meeting in a year to hold up to 19 meetings by some corporates. This also gave clarity on the constitution of the proper audit committee as per clause 49.

We can also notice a wide variation in terms of our control variables. The liquidity ratio, which is calculated as a ratio of current assets and current liabilities, ranges from 0.35 to 9.32 showing growth in the company’s liquidity firm’s growth has also raised from 0.562 to 2.668 which is calculated as a log of total sales. There is also a sign of expansion in companies, firm size has increased from 3.13 to 5.71 (calculated as a log of total assets in US$ millions).

Regression Analysis

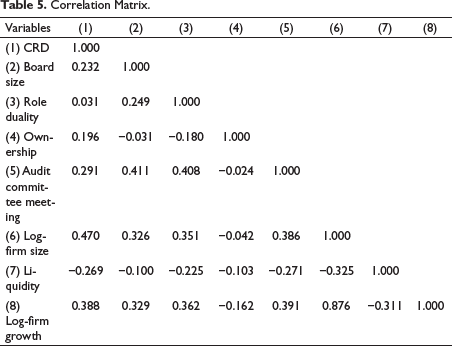

The analysis of corporate governance and risk disclosure among the sample of non-financial listed companies in India reveals some interesting results based on identified determinants (board size, role duality, ownership, audit committee meeting, firm size, liquidity, firm growth). In Table 5, the Pearson correlation matrix was deployed to measure the strength and direction of linear relationships among the variables.

Correlation Matrix.

The results above in the correlation matrix demonstrate the positive correlations between CRD and board size, role duality, audit committee meeting, firm size and firm growth. Only firm liquidity and risk disclosure are negatively correlated. However, the table shows the highest correlations among the firm size, firm growth and board size with the risk disclosure practices of the company and the lowest correlation with the role duality.

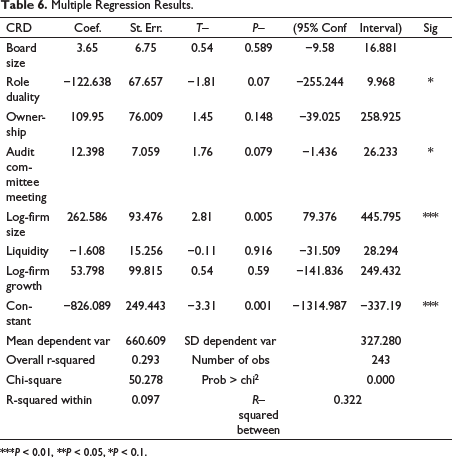

Table 6 runs the results of regression analysis while conducting the various test to check the normality, multi-collinearity and heteroscedasticity of our data. We then run the random effect model, the findings clearly state the relationship between the dependent variable (CRD) and independent variable (board size, role duality, audit committee meeting) and control variable (firm size, firm growth and liquidity). The model is statistically fit at 1% value that is at P = 0.000 and r2 = 0.322. This means that the variable selected in the study (independent variables) are showing satisfactory relation in explaining the dependent variable (CRD).

Multiple Regression Results.

***P < 0.01, **P < 0.05, *P < 0.1.

Table 6 shows the correlation between CRD and board size as positive and insignificant (t = 0.54 and P = 0.589), which means that a larger board size does not lead to transparency in an organisation. The results stand inconsistent with the agency theory concept, diversified board structure and volatility concept of Ahnan et al. (2020), Fama and Jensen (1983), Linsley et al. (2015) and Mishra and Kapil (2018). Since there are no clear-cut guidelines in India in context to board size in India, results also revealed that board size might not be a determinant of risk disclosure of top listed companies.

Role duality and risk disclosure have a negative effect and are somewhat significant (t = −1.81 and P = 0.07) which is significant at a significance level of 1%. This clearly shows that firms that divide CEO and managing director roles clearly show more transparency in terms of risk disclosure information. This supports the agency theory that combining the role of CEO and managing director will weaken the working of the company; also, this supported Ibrahim et al. (2019) and Linsley et al. (2015), which showed the negative effect of role duality on risk disclosure.

The study depicted the insignificant relation between ownership structure and risk disclosure in the context of Indian listed companies (t = 1.45 and P = 0.148). Despite the involvement of family members on board, risk information is transparent and is not affected the business. The results are inconsistent with the results of researchers, which showed a positive relationship between ownership and risk disclosure (Abraham & Cox, 2007; Muturi, 2019). Despite the existence of family business and family members of the board, our results are inconsistent with risk disclosure.

The audit committee plays a major role in risk disclosure, as per clause 49 of the Companies Act 2013, it is mandatory for every listed company to constitute an audit committee. Majorly, all listed companies have created an audit committee; the effectiveness of these companies is again a determinant of risk disclosure. The effectiveness of this committee can be judged through the consistency of properly convened meetings by the board. Table 6 shows the audit committee and risk disclosure are positive and somewhat significant (t = 1.76 and P = 0.79). These results are significant to the results of Elshandidy et al. (2018), Neri et al. (2018), Salem et al. (2019), Sarkar et al. (2012) and Sidhu and Kaur (2019), which focussed on the constitution of the audit committee and conduct of regular meetings. As per clause 49, every listed company on average must meet four times a year; risk management is one of the crucial agendas of the audit committee. Our results are somewhat significant to conduct proper meetings of the audit committee.

In the context of control variables (firm size, liquidity, firm growth), firm size is highly significant with risk disclosure at P = 0.05, whereas the other two variables liquidity and firm growth are highly insignificant at P = 0.916 and P = 0.59, respectively. Firm size is positively significant which is consistent with the results of other research studies (Abraham & Cox, 2007; Elshandidy et al., 2018; Linsley et al., 2015; Linsley & Shrives, 2006). Further, the results confirm the shareholder theory, where people at top positions prefer sharing risk information to maintain their status in an organisation. Large firms are surrounded by a large number of shareholders; in turn, the duty of managers is to share such information that will maintain the trust of shareholders.

Firm profitability is negatively related to CRD, which clearly states that small firm shares the risk-bearing information compared to large firms and which is consistent with the results of Miihkinen (2012). This is contrary to the agency and signalling theory. Liquidity is negatively related to risk disclosure, as companies that have a high level of liquidity tend to have more risk-taking capacity and hence disclose risk information freely.

To conclude our results stand positive for an audit committee meeting, role duality and firm size while there exists no significant correlation between risk disclosure and board size, ownership, firm growth and liquidity.

Conclusion and Limitation

This study is an attempt to analyse the relation between various corporate governance variables and risk disclosure practices being adopted by Indian companies. While prior research studies have focussed on individual variables in detail (Khandelwal et al., 2020; Saggar & Singh, 2019), this paper tries to explore a combination of corporate governance variables such as board size, ownership, number of audit committees meetings, role duality, firm size, liquidity and firm growth and its impact on risk disclosure policies of a firm.

The findings indicate that board size and ownership have no impact on risk disclosure norms, which is contrary to our literature review. Indian companies are mainly considered as having family-based boards, which is usually having biases in decision-making. This can clearly be stated using the ownership structure of the corporates. Companies with concentrated ownership usually have fewer voluntary disclosures in their reports. Further, role duality and audit committee meetings are somewhat significant, which states some impact of two variables on risk disclosure. In the case of the firm size, it was found to have a significant effect; larger firms have better risk disclosure than smaller firms do while liquidity and firm growth are highly insignificant factors.

The broader analysis of the study states that corporate governance and risk variables need more attention and there is a need for corporates to have more mandatory risk disclosure norms to assess the linkage and progress in risk exposure. In addition, the study has implications for regulators; there is an urgent need for stricter corporate governance norms in the context of risk disclosure.

While there has been progress in introducing guidelines for better transparency and risk disclosure, there is a need for more such steps to ensure the company’s stability. The current study has limitations such as a small sample size, limited variables in context to risk disclosure and using the word as a unit of measure while doing content analysis.

Future studies can broaden the scope of the study by including further corporate governance variables such as meetings of directors, independent and dependent directors, auditor’s details, etc., conducting sentence-wise content analysis and conducting cross-sectoral risk analysis.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.