Abstract

The Ghanaian economy relies heavily on the export of cocoa beans to generate foreign reserves, and many Ghanaian citizens rely directly or indirectly on cocoa beans for income generation. The cocoa bean price is highly volatile and largely determined at the international commodity exchange in London. Volatile prices translate into volatile revenues, income, and exchange rates, which pose challenges for the Ghanaian government to manage its internal and external balances. We build on John R. Commons’s institutional economics and propose an institutional theory of price to understand the pricing mechanisms along the cocoa chain. Drawing on interviews with cocoa stakeholders in and outside of Ghana between 2024 and 2025, we first map pricing points along the cocoa chain following our institutional theory of price and second, provide a political economy analysis of cocoa pricing and price uncertainty. We argue that Ghana’s price risk is managed by its counterparties to its disadvantage, with large multinational companies reaping the benefits from the institutional pricing arrangement. We conclude with tentative considerations about how this could change.

Introduction

Despite the central role of the price level and price volatility in the determination of value creation, extraction, and distribution along commodity chains, the direct analysis of price is largely absent from the Global Value Chain (GVC) literature. This absence is particularly puzzling as the GVC literature is a descendant of the World System Theory, which puts declining terms of trade and unequal exchange with (unfair) prices at the centre of its analysis. Some recent contributions have started addressing this literature gap for the value chains of cash crops such as coffee, cotton and cocoa, for example, Bargawi and Newman (2017), and Staritz et al. (2018, 2023).

Building on this emerging literature, this paper traces the absence of price in the GVC literature to its adaptation of new institutional economics as its theoretical foundation and the role of transaction cost economics within this framework. Drawing on economic sociology and ‘old’ institutional economics instead, we propose an analytical framework to understand pricing along commodity chains. Within this framework, pricing is understood as an institutionally embedded and politically contested process which is temporally and spatially dislocated from the exchange process of goods and services. The temporal dislocation is reflected in the notion of transaction, introduced by Commons (1934), which is adopted by our framework. Prices are conceptualised as the outcome of such pricing processes.

Within this framework, we distinguish between price negotiation, price formation, price administration, and price derivation as institutionally distinct pricing processes. These are characterised by asymmetric legal, political and economic power relationships, which uphold the institutional structures that shape pricing processes. For many commodity chains, price formation takes place in commodity derivative markets, despite these being markets for contracts and not for the physical commodity. 1 Commodity derivative markets are separate, both spatially and institutionally, in the sense that they do not directly appear in any of the transactions central to the commodity chains of cash crops. Most prices within the chain are hence derived prices; they are formed outside of the specific transaction.

We use our institutional framework, inspired by Commons (1934), as a starting point. Firstly, we map pricing points along the cocoa chain as the foundation of our analysis. Secondly, we conduct a political economy analysis of the institutional setup through which prices are determined and through which price risks are distributed within the Ghanaian cocoa sector to identify those who achieve higher value capture, those who carry the burden of price volatility and those who benefit from it. Specifically, this study traces pricing for the Ghanaian cocoa sector and its stakeholders, drawing on interviews in and outside of Ghana between 2024 and 2025 and the authors’ first-hand knowledge about the cocoa sector.

We demonstrate that the institutional structures that underpin pricing in the cocoa sector have been created during colonial times and maintained by powerful stakeholders who have continuously benefited from this arrangement; the primary beneficiaries being large commodity trading houses. Until recently, a forward-selling system protected Ghanaian cocoa farmers from downside risk, thereby managing, in parts, the unequal distribution of the burdens and benefits of price risk. However, the rigidity of the system came at a cost in a rising market for both cocoa farmers and the Ghanaian government, which relies on the sector for foreign exchange earnings. This cost was particularly felt in 2024.

In April 2024, for the first time in history, cocoa prices at the London ICE reached the £10,000 barrier per tonne, a tripling in prices compared to the previous year. While this should have been good news for cocoa farmers and the Ghanaian government, the forward-selling system 2 meant that prices far below the global benchmark were achieved. On 20th August 2024, Joseph Boahen Aidoo, the then Chief Executive of Ghana Cocoa Board (Cocobod), announced that Cocobod would no longer pursue a syndicated cocoa loan 3 for the upcoming season and thereby reduce the need for forward sales. 4 The syndicated loan had been in place for 31 years to finance cocoa sourcing in Ghana.

The Ghanaian cocoa sector is a particularly interesting case study for the political economy of pricing due to the recent contestations of the pricing processes, as well as Ghana’s unique institutional setup. Cocobod, Ghana’s cocoa marketing board, and its subsidiary, the Cocoa Marketing Company (CMC), provide the government with a monopoly on the sale of Ghanaian cocoa beans. Through Cocobod, the Ghanaian government is a considerable counterparty to large multinational commodity trading houses. While Ghana is in many ways a ‘typical’ commodity-dependent economy, its considerable market power in the cocoa sector and the government’s monopoly position on cocoa bean exports are unique. This arrangement brings challenges but also offers opportunities that would be out of reach for a more diffuse market.

The paper contributes to a small yet growing literature – for example, Bargawi and Newman (2017), and Staritz et al. (2018, 2023) – that centres pricing processes within commodity chains and the power structures embedded therein to understand how value is created and distributed along the chain. 5 It also provides a detailed account of recent changes in the Ghanaian cocoa sector and analysis of who gains and who loses from the institutional setup governing pricing processes along the cocoa chain.

The remainder of this paper is structured as follows. Section 2 reviews the studies that have addressed the absence of price in the GVC literature, and institutional and sociological approaches to pricing more generally. These contributions are taken as a starting point for our analytical framework of pricing as an institutionally embedded and politically contested process. Section 3 provides a three-part analysis of the Ghanaian cocoa sector, starting with a summary of the historical evolution of current institutional structures, then providing a mapping of pricing points located in time and space as an analytical starting point and concluding with a political economy analysis of the current institutional setup and its contestations. Section 4 reflects on ways for the Ghanaian government to gain greater control over pricing and price uncertainty.

Pricing and price risk in global commodity chains

Literature review

Macroeconomic challenges that result from the over-reliance on primary commodity exports for the generation of foreign exchange and revenues are well documented; see, for example, Corden (1984), Deaton (1999), Nissanke (2019). These challenges arise from the cyclical nature of commodity prices due to alternating episodes of over- and under-production (Maizels, 1994). In addition to their cyclical nature, commodity prices are highly volatile. Many primary commodities are traded as an asset class on derivative markets in the global financial centres, adding volatility through fast trading and quick translation of information, expectations, beliefs, fads, and sentiments into prices.

This price volatility immediately translates into volatile revenues, incomes, exchange rates, and domestic price levels (inflation) for commodity exporters, especially for the exporters of commodities that are referenced against derivative market prices. The importance of commodity prices for the macroeconomic stability and developmental trajectory of primary commodity export-dependent economies has been highlighted by economists since the early 1950s. Prebish (1950) and Singer (1950) independently identified declining terms of trade 6 for commodity exporters as a key development challenge of the newly independent nations, whose economies were largely set up for primary commodity production. The observation of unequal pricing between primary commodities and manufactured goods also motivated the unequal exchange theories developed by Emmanuel (1972) and Amin (1974).

While authors differed on the explanations for the phenomenon of declining terms of trade, the empirical observation of unequal remuneration for goods exported by countries in the Global South (periphery) and the Global North (core) emerged as a central theme of a set of theories which became known as dependency theories; see Kvangraven (2020) for a review. The concept of commodity chains, which underpins today’s GVC analysis, was originally developed as an analytical tool within the tradition of the world system theory of the 1980s, which itself is associated with the dependency theory scholarship (Hopkins and Wallerstein, 1977, 1986). Later authors adopted the chain analogy but replaced the theoretical underpinning with different theoretical traditions from management, international business studies, sociology, and new institutional economics, merging into today’s GVC scholarship (Bair, 2005).

Gereffi (1994, pp. 96-7) introduced the concept of ‘governance structure’, which became a core theme in the evolving GVC literature. He defines governance as ‘authority and power relations that determine how financial, material, and human resources are allocated and flow within the chain’ (ibid.). Power is exercised by what Gereffi (1999) calls the ‘lead firm’ in the chain, which controls access to major resources that generate the most profitable returns. These lead firms can decide over the inclusion (or exclusion) of less powerful actors and constrain less powerful actors to lower value-added activities (Raikes et al., 2000). The second iteration of the governance framework by Gereffi et al. (2005) highlights transaction cost economics as one of the three pillars that underpin their framework. They identify three variables – (1) the complexity of a transaction, (2) the ability to codify a transaction, and (3) the capability of suppliers – that explain the emergence of different GVC governance structures.

However, despite the central role of price in the determination of value creation and value distribution along commodity chains, the question of pricing, that is, where prices originate and by whom they are created, is not discussed within the GVC governance frameworks. The reason for this omission is its foundation in transaction cost economics. Prices are conceptualised as codified information or as signals of demand and supply conditions within a market exchange (Gereffi et al., 2005). Implicitly, price formation is seen as equivalent to price discovery, whereby prices reveal underlying market conditions. Prices, therefore, play a coordinating role by signalling over- or under-supply and remain exogenous to the individual exchange process. Although the GVC framework acknowledges price-setting power by monopolies and monopsonies, like transaction cost economics, the role of price beyond the market remains underdeveloped as governance structures are derived as the outcomes of lead firms’ economic optimisation processes in the presence of transaction costs. 7

The works by Bargawi and Newman (2017) and Staritz et al. (2018, 2023) seek to address this shortcoming and highlight pricing as a key variable in the understanding of value creation and distribution along commodity chains. Bargawi and Newman (2017) draw on sociological and institutional approaches to price to develop the price chain as an analytical framework for commodity price formation and transmission with applications to the coffee chain. Staritz et al. (2023) argue for the addition of price-setting power as a central scheme to the GVC approach to understand how price risk is distributed along the chain. They study cotton in South Africa (Staritz et al., 2018) and the West African cocoa chain specifically (Staritz et al., 2023).

This strand of literature emerged in the context of the financialisation of commodity markets debate (Mayer, 2012). A synchronous price rise and subsequent collapse across seemingly unrelated primary commodity derivative markets in the 2000s revived a debate about the impact of speculators on price formation in these markets and highlighted the importance of prices formed in derivative markets for pricing along commodity chains (Nissanke, 2012; Staritz et al., 2018). However, this centrality of derivative markets is commonly absent in primary commodities-based GVC studies. The above-cited studies that integrate pricing into GVC and commodity chain frameworks, therefore, turn to institutional and sociological approaches to price and stress the need to consider the interplay of institutional structures at different scales beyond the single point of exchange and the power relations embedded in these structures.

Among sociological approaches to price that are referenced by both Bargawi and Newman (2017) and Staritz et al. (2023), Beckert (2011) sees prices as the outcome of social and political forces. For him, transactions are embedded in ‘institutions, social networks and culturally anchored frames of meaning’, and prices are a result of this embeddedness of transactions (ibid., 757). The distribution of wealth, as the consequence of pricing, is therefore the outcome of the structures that shape transactions. Çalışkan and Callon (2009, 2010) distinguish between valuation and price, with valuation conventions shaping what is considered a fair price. They argue that price is the outcome of power struggles between valuation agencies (i.e. all actors that participate in defining and calculating value). Therefore, the price of any transaction is always relational as it is calculated and legitimised based on other prices.

Tool (2002) proposes an institutional theory of discretionary pricing drawing on Veblen’s theory of exchange. He defines the discretionary pricing process as the use of power by individuals to influence the monetary terms of exchange and observes that most ‘real world’ pricing processes are discretionary as large oligopolistic corporations administer prices which are determined by target rates of return to capital.

Building on Commons’s institutional economics and theory of transaction, Gloria and Palermo (1996) point out that the method of price determination is largely conventional and that pricing is an evolutionary and path-dependent process. They focus specifically on bargaining as a market-based process of price determination and one specific type of transaction within Commons’s framework. In reference to Commons’s work, they see economic power as a key factor in explaining different outcomes in bargaining transactions. Kaufman (2007) adopts Commons’s typology of transactions to specifically develop an institutional theory of price that reflects different pricing practices embedded in transactions. Akin to Gloria and Palermo (1996), he centres the bargaining transaction but also includes rationing and managerial transactions developed by Commons. We draw on Commons’ theory of transactions and Kaufman’s (2007) adaptation of this theory to pricing, but amend it to apply to the case of primary commodities.

For Commons, a transaction is the legal transfer of ownership (mode) in contrast to exchange, which is merely the physical transfer of a good or commodity (matter). Commons (1934) introduced the notion of ‘transaction’ as an antithesis to 19th-century economists, whom he accuses of wrongly conceptualising the price formation mechanism as a harmonic (equilibrium) relationship between man and nature. By focusing on exchange rather than transaction, those economists failed to account for the legal transfer, which, according to Commons, is a process characterised by conflict in a relationship between man and man. Specifically, Commons defines a transaction as: ‘[T]he alienation and acquisition, between individuals, of the rights of future ownership of physical things, as determined by the collective working rules of society. The transfer of these rights must therefore be negotiated between the parties concerned, according to the working rules of society’. (Commons 1934, 58)

Commons emphasises ‘futurity’, that is, not immediate but future physical ownership is transferred, which, inspired by Keynes’s work, introduces radical uncertainty as a key characteristic of all transactions. This means that the transaction process is temporally dislocated from the exchange process. Another core theme in his theory is working rules, which can be formal (e.g. laws) or informal (e.g. conventions). Since a transaction is a relationship between man and man, it is characterised by conflict, mutuality, and order. The interests of the parties involved are both in conflict and mutually dependent. Order is a necessary characteristic because of the radical uncertainty of the future. Commons argues that the future must, to some extent, be reliable to facilitate action in the present (Commons 1934, 58). The security of expectations is guided by working rules, which ‘work as a limiting factor on behaviour’ and guide what is legally and ethically accepted by society (Commons 1934, 140).

The enforcement of working rules is a gain for one, which comes at a loss for the other. When it creates liberty for one party, it results in exposure for the other. When it creates security for one party, it demands conformity from the other. Hence, working rules that govern transactions in which pricing processes are embedded determine not only the distribution of wealth but also the distribution of the burdens and benefits of wealth creation, including the distribution of risk. This entails who is exposed to uncertainty, which is allocated according to security and conformity, liberty and exposure. Security for one requires conformity from the other; liberty awarded to one, leaves the other exposed.

Legal (and political) power is the control over agents’ future behaviour and hence is as important as economic power in shaping the outcomes of transactions (Commons 1934, 86). Power is hence a key theme for Commons. Ultimately, ‘power […] determines whose interests count and who reaps the rewards and carries the costs of economic activity’ (Kaufman 2007: 16). Different types of transactions are reflective of different power configurations. Commons distinguishes between three types of transaction, which are characterised by different degrees of economic, political and legal power asymmetries: bargaining, rationing, and managerial transaction. The latter two are characterised by political (rationing) and legal (managerial) asymmetries, and the former by economic asymmetries but legal symmetry (bargaining).

Pricing in the bargaining transaction is driven by relative scarcity as well as the unequal economic power of those involved, which affects bargaining strength. Pricing in the managerial transaction is driven by proprietary scarcity, which means that the actor with legal control over resources can generate situations of scarcity or abundance to influence price. In rationing transactions, prices are administered according to working rules enforced by a (collective) authority. While not considered by Commons directly, later authors have interpreted the rationing transaction to include cost-plus or markup pricing, that is, administered prices set to achieve intended profit margins for powerful actors (Takahashi, 2018).

Working rules for Commons are not immutable or static. Commons adds the strategic transaction as a fourth type of transaction and a special form of the bargaining transaction. He argues that institutional change is initiated by limiting factors, which turn a bargaining transaction into a strategic transaction. Limiting factors are constraints, such as working rules, scarcity, or authority, which limit actors’ behaviour so that a bargaining transaction cannot be concluded. Strategic transactions, therefore, aim at changing existing working rules through collective action (violent or non-violent) or legal means (Commons 1934, 86).

Analytical framework

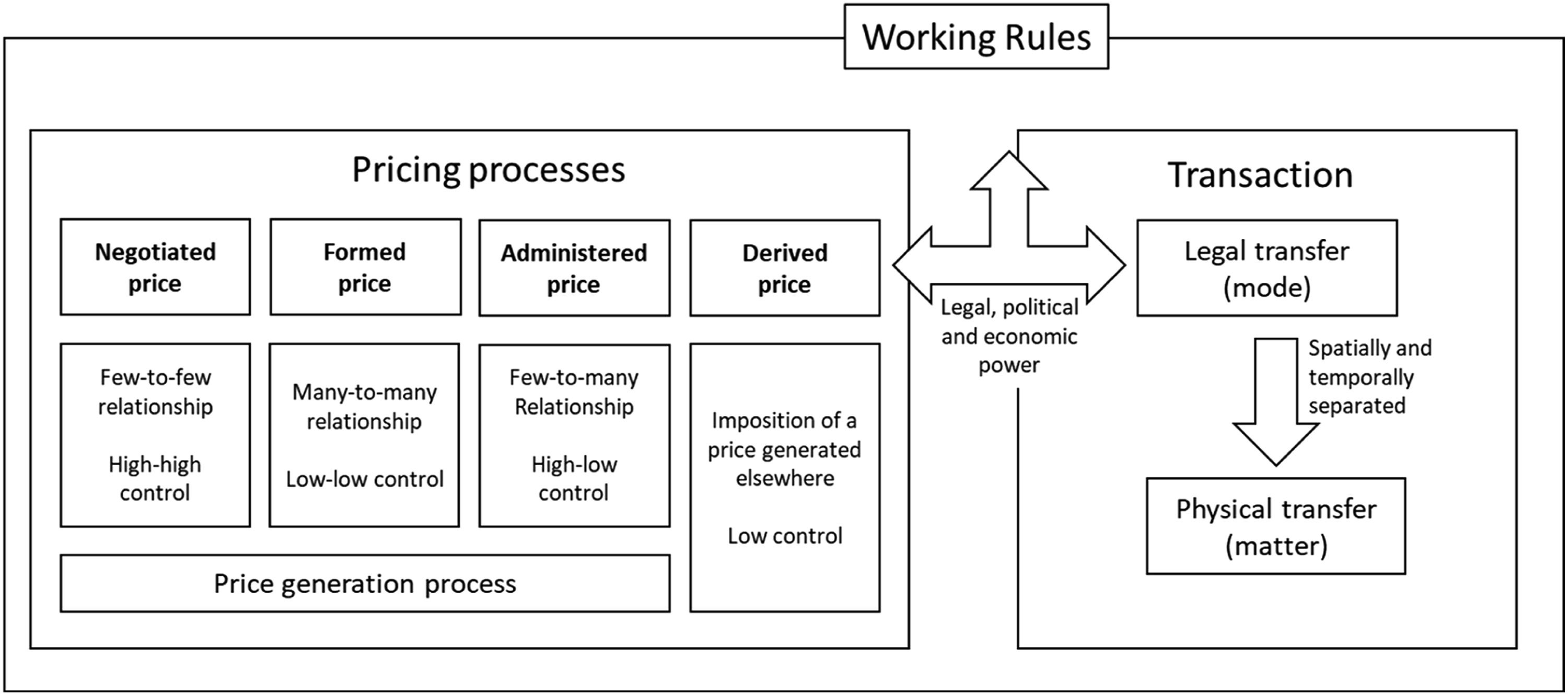

Following the existing literature, this paper understands pricing as an institutionally embedded (within a transaction) and contested process (Bargawi and Newman 2017; Beckert 2011; Staritz et al., 2023; Çalışkan and Callon 2010). We use these insights as a starting point to develop a framework that borrows from Commons’s institutional theory. Commons’s distinction between legal and physical transfer accounts for the temporal aspect of a transaction, which enables us to analyse uncertainty. Once the pricing processes within a transaction are identified, price uncertainty and the distributions of the costs and benefits that arise from this uncertainty 8 can be derived as an outcome of this process. In our framework, we distinguish between four stylised pricing processes: price negotiation, price administration, price formation, and price derivation.

Price negotiation is akin to Commons’s bargaining transaction, and is a transaction between legal equals with outcomes dependent on relative economic and political power. Price administration is akin to Commons’s rationing transaction; prices are imposed by an economic (and possibly political or legal) superior actor or collective of actors (e.g. producer pricing, cost-plus pricing, and price caps set by governments). In this configuration, control over prices lies solely with the more powerful actor. Price formation, on the other hand, is inspired by an auction-type market setup. 9 Both buyers and sellers have low control over the price, as bargaining is limited by working rules that anonymise and standardise the transaction. 10 For many commodity chains, price formation takes place in commodity derivative markets. These are markets for contracts that award the future right to buy or sell a physical commodity. Futures contracts are rarely executed and commonly closed before the delivery due date. 11

Price derivation is the process of imposing a price that is neither negotiated nor formed in the specific transaction but instead derived from another transaction (e.g. using a futures price as a reference price in a transaction). This means that price derivation is not a price generation process, as a price generated in a different transaction is transferred. Derived prices are therefore a specific form of administered prices, but without any agent involved in the transaction and pricing process directly enforcing the imposition of a price; hence, none of the parties involved has any control over this imposition within the transaction. Rather, the derived price is imposed by working rules. This does not mean that the existing working rules do not favour one party over the other (have distributional consequences) or that these working rules cannot be changed. However, challenging these working rules lies outside the transaction within which the pricing process is situated. Indeed, the imposition of a derived price might preserve or improve profit rates and provide security for one party, while reducing profit rates and increasing risk exposure for another.

The typology in Figure 1 provides a stylised categorisation of pricing processes within a transaction, and these pricing processes can emerge as a composite or combination of these stylised processes within a single transaction. Pricing and transactions. Source: Authors.

The pricing process is part of a transaction which involves the legal transfer (mode), alongside an agreement over quantity, insurance, and other modalities of the transaction. The legal transfer is both temporally and spatially distinct from the physical transfer (matter) of goods and moneys. The distinction between the transaction process, of which pricing is part, and the exchange process introduces the element of ‘futurity’ and thereby uncertainty, as in Commons’s theory. 12 We also adopt Commons’s notion of working rules as the laws and conventions that govern pricing processes within transactions. Power asymmetries are historically rooted and hence path dependent and can be challenged in what Common calls strategic transactions.

We argue that an understanding of the emergence of working rules and their contestations requires a political economy analysis. This involves an analysis of the distribution of power between different groups of stakeholders, the resources under their control, their capacity and capability to mobilise and organise around a common cause, and their ability to generate, retain, and sustain support (Khan, 2018). 13

Methodology

To better understand the institutional structures that underpin pricing along the cocoa chain, we create a temporal and spatial map of pricing points. This allows us to identify the working rules that govern pricing processes, the powers embedded in these working rules, and the distribution of burden and benefits within transaction arrangements. The mapping draws on document analysis as well as insights from semi-structured interviews conducted with key informants, including the sector regulator, licensed buyers and aggregators, civil society organisations, farmer representatives, and the Ghanaian central bank between 2024 and 2025 and the authors’ first-hand knowledge of the cocoa sector (see Appendix for a full list of interviews).

The mapping exercise and the pricing points identified build the analytical foundation for a political economy analysis of pricing, the working rules shaping pricing processes, embedded power relations and the distribution of price risk along the cocoa chain. Embedded power relations are traced through two recent contestations of working rules and their outcomes: (i) the introduction of the Living Income Differential (LID) in 2020, and (ii) the discontinuation of the syndicated loan in 2024.

Ghana’s cocoa marketing: A political economy analysis

The analysis is divided into three sections. The first sub-section provides a brief account of the history of cocoa marketing in Ghana. The second sub-section maps the temporal and spatial locations of pricing points along the Ghanaian cocoa chain and the working rules that govern them. The third sub-section provides a political economy analysis of these working rules and their contestations.

A brief history of Ghana’s cocoa marketing

Ghana is the only country that has not abolished its marketing board and has therefore maintained a state monopoly on the sale of cocoa beans. The monopoly is managed through CMC, a subsidiary of Cocobod, which is registered as a limited company. Cocobod is the institutional successor of the West African Producer Control Board, which was introduced in 1940 by the British coloniser at the onset of the Second World War (Acquaah, 1999; Wickizer, 1951). Under the board, prices were fixed, and the rising power of domestic middlemen and cooperatives was curtailed by allocating buying quotas to Licensed Buying Agents, which were registered with the board.

The system suppressed political unrest and hostility towards European buyers after several cocoa holdups in the late 1930s

14

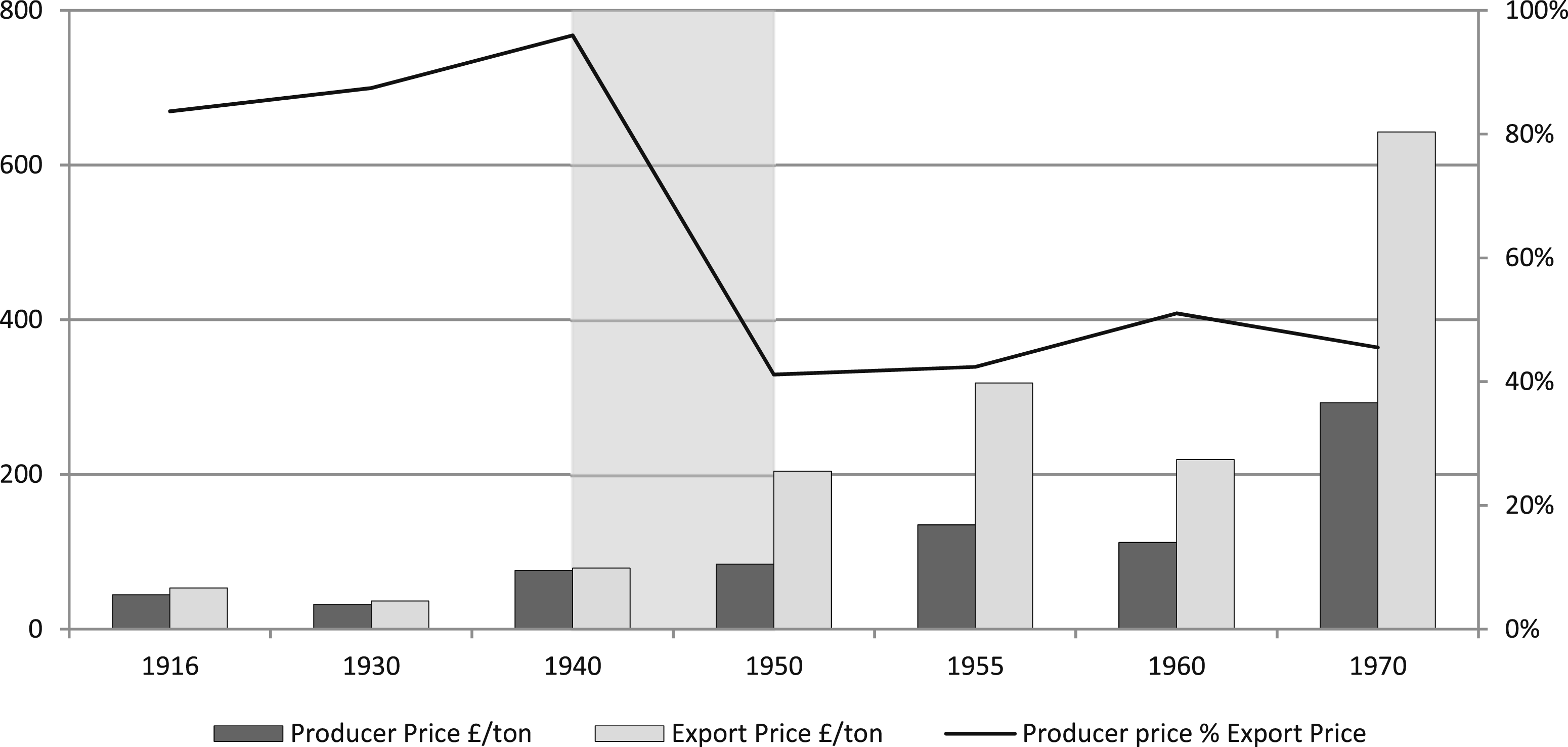

and helped finance British war efforts by dictating a low cocoa bean price (Alence, 1991). Its introduction led to a prolonged squeeze of the cocoa producer price, which deteriorated from up to 90% of the export price to as low as 40% (Acquaah, 1999). Once the board was in place, the producer price remained suppressed long after independence in 1957; see Figure 2. Export Prices (GBP per ton - left) and Producer Price Share (% - right), 1916–1970. Sources: Acquaah (1999, p. 126) and Western Africa Programmes Department (1983, p. 36); authors’ compilation. Note. The greyed-out area marks the introduction of the West African Producer Control Board.

Initially, the prices received by traders were formed at the spot exchanges in Liverpool and London (Dand, 1995: p. 82). With the development of edible chocolate in the late 19th century and growing demand for cocoa beans, forward contracts became the preferred mode of transaction. Forward contracts could be cleared via the London Produce Clearing House, established in 1888 (Cranston, 2007). Three trade associations were formed to administer standardised contracts and provide arbitration services: the Cocoa Merchants’ Association of America (CMAA) in New York, the Cocoa Association (CAL) in London, and the Association Francaise du Commerce des Cacaos (AFCC) in Paris (Dand 1995, 84). In 1925, the first standardised cocoa futures market opened in New York (today ICE US), which remained the benchmark for cocoa for the subsequent decades. The London Commodity Exchange opened in 1954 and became the second leading commodity exchange for cocoa (today ICE EU).

The forward contract system was favoured by the trading houses, not only because it mitigated price and supply risk, but also because the system was less transparent than the open auction system previously practised in Liverpool and London, and competitors were left with uncertainty over the price and volume of deals (Dand 1995, 83). This favoured large trading houses, which could trade on proprietary information and release information about stock holdings when it favoured their positions in the market. The two largest trading houses at the time were the United African Company (UCA), later owned by the Lever Brothers (Unilever), and Cadbury (later Cadbury and Fry), owned by the Cadbury Brothers (Acquaah 1999, 99-100). UCA entertained an import-export business and was the major buyer of cocoa in the 1930s, with over 1000 buying points and merchandise outlets. Due to its dual role as both importer and exporter, the company was at the centre of the cocoa holdups of the late 1930s (Acquaah 1999, 108).

Post-independence, 1957, the state monopoly on cocoa trading remained in place, albeit with some interruptions and alterations (Mikell, 1989). Like many commodity export-dependent economies, Ghana received financial assistance from the IMF in the 1980s. Anticipating the IMF’s austerity programme, the Ghanaian government drew up a reform plan for the cocoa sector, which saw the previous marketing board replaced with today’s Cocobod and partial liberalisation of the internal cocoa marketing system in the early 1990s (Akiyama et al., 2001; Gocking, 2005; Laven, 2010; Quartey, 2013). In many ways, the partial liberalisation reinstated the system in place during colonial times, with Licensed Buying Companies (LBCs) 15 sourcing cocoa beans on behalf of CMC. Although farmers’ share in the export price has improved, the working rules governing pricing processes today have largely survived since colonial times.

Mapping pricing points in Ghana’s cocoa marketing

Ghana’s cocoa marketing system has an internal and external component, with CMC managing both sides. Two crop seasons exist: the main crop, with the harvest starting in September and lasting until May, and the light crop, lasting from June to September. We focus on the main crop season, where the bulk of the cocoa is harvested and shipped. Operations are divided into two stylised periods: (1) pre-harvest and (2) during and post-harvest. We refer to this periodisation as stylised, as the two periods blend into one another. Transaction processes along the chain span both periods, with pricing mostly taking place in period 1 and the exchange of goods and moneys in period 2 (with more flexibility in the timing downstream of the chain).

Before the 2024–25 season, most of CMC’s internal marketing operations were financed by a syndicated loan. The loan, obtained at international money markets, was collateralised with fixed-price forward contracts (van Huellen, Sophie). This meant that CMC had to sell forward an adequate volume of cocoa beans to secure sufficient collateral for the loan before September. Standardised contracts are provided by the Federation of Cocoa Commerce (FCC), formed after a merger between the CAL and AFCC in 2002. FCC offers two contract types: (1) fixed price, in which the price is fixed at the time of signature to the price of the futures contract that matures close to the agreed delivery date and (2) differential, in which the price floats with the price of the futures contract. These working rules are embedded in FCC contracts, and the need to secure a syndicated loan imposed the dominant use of fixed-price contracts. Since the abolition of the syndicated loan, CMC is more flexible in its use of fixed-price and differential contracts.

The London ICE cocoa price, denominated in Pounds Sterling, is the reference price for Ghanaian cocoa beans in all FCC contracts. The GBP-USD exchange rate is derived and fixed at the time of signature. A country premium is added to the terminal price, which is negotiated between CMC and the buyer. Since June 2019 (for the 2020/21 cocoa season contracts), the LID set at 400 USD over the terminal has been administered by Cote d’Ivoire and Ghana as an additional premium to the country premium. The price that CMC receives is hence a composite of a derived price, which is formed at the terminal market, imposed by working rules embedded in standardised FCC contracts, a negotiated price, which is the country premium, and an administered price, which is the LID.

The buyers signing the contracts with CMC tend to be large multinational commodity trading houses that maintain forward contracts with processors and confectionery companies (Fold, 2001, 2008). These forward contracts are commonly on a cost-plus basis, where the buyer administers costs of sourcing and processing and a profit margin. A few large buyers (e.g. Olam, Barry Callebaut, Cargill, ECOM, Sucden, and Touton) dominate the space, and most cocoa is sold to them. The remaining contracts are signed with domestic buyers, which could be Ghanaian-owned businesses (e.g. Niche Cocoa and Plot Enterprise), but in many cases are also foreign-owned (e.g. Barry Callebaut, Olam, Touton, and Cargill all maintain processing companies in Ghana). Previously, the need for collateral forced CMC to prioritise multinationals over indigenous buyers. 16

The financing requirement for sourcing cocoa beans exceeds the domestic banking sector’s capacity. The syndicated loan was a way to access cheap financing via international money markets. It was obtained in USD via the Ghana International Bank (GHIB), a London-based subsidiary of the BoG and the receiving bank for all cocoa sales proceeds on behalf of Cocobod. The interest rate for the loan was derived as the standard borrowing rate (LIBOR), plus a risk premium, which was negotiated based on the lead bank’s assessment of CMC’s credit risk. 17 Once the loan was agreed, it was transferred to GHIB, which forwarded the USD to the BoG. The BoG then released the GHS equivalent to Cocobod. The USD-GHS exchange rate was negotiated between Cocobod and BoG, roughly reflecting rates between October and December, the loan drawdown period (interview 5). From the GHS equivalent of the loan, Cocobod extended financing to LBCs at a rate set by Cocobod relative to the BoG prime rate.

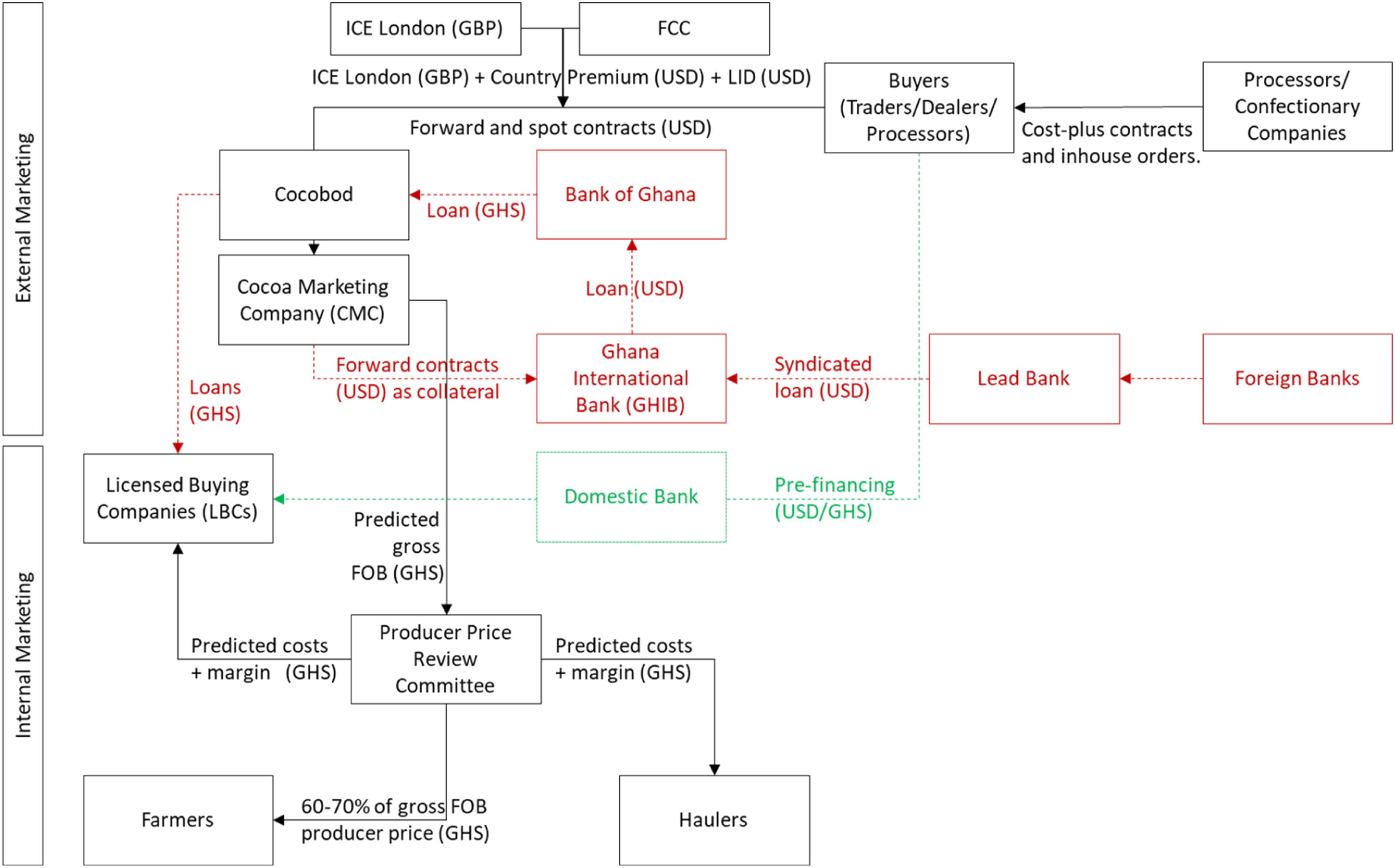

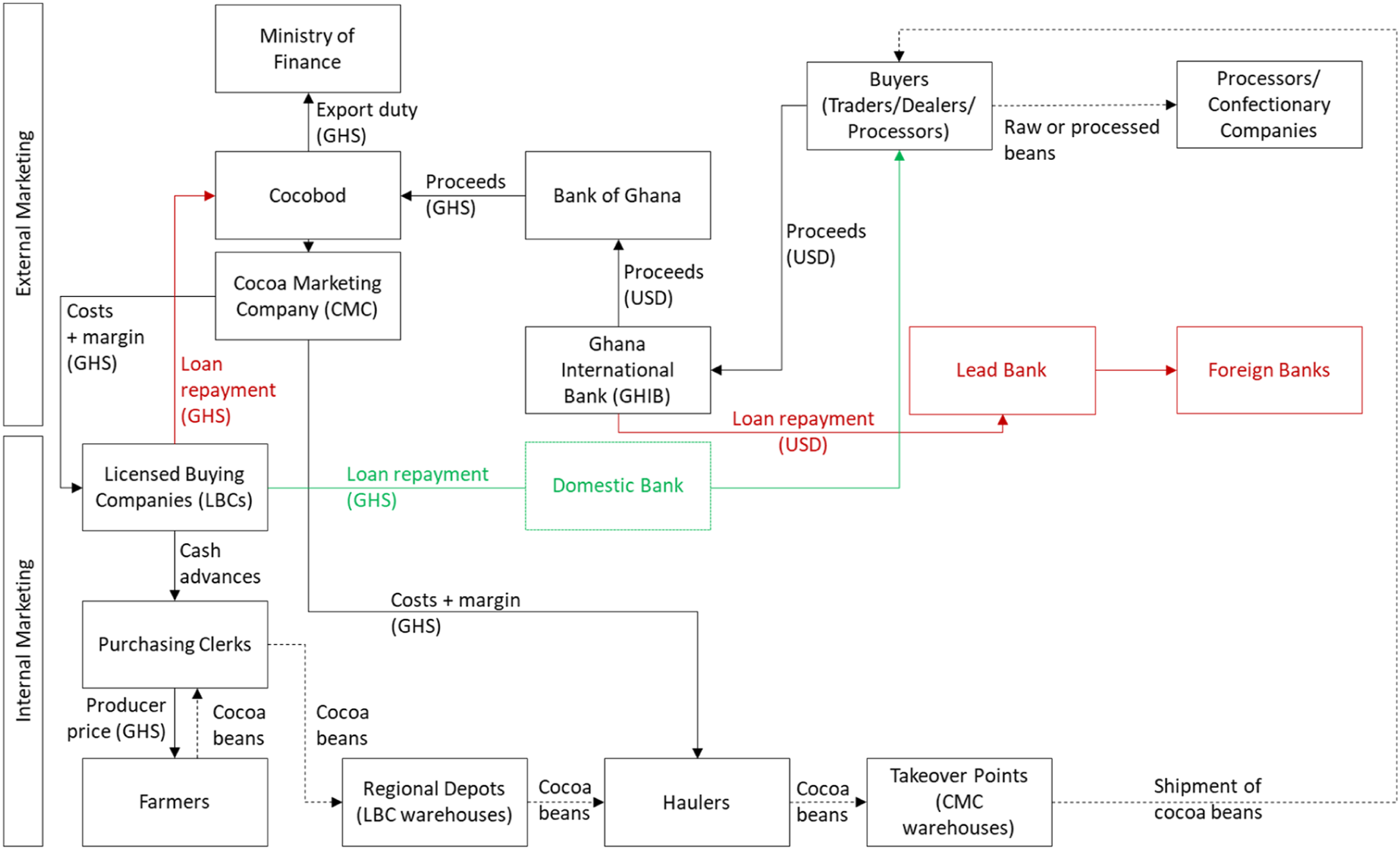

Since the syndicated loan’s discontinuation, LBCs must secure financing independently, either through bank loans, their own capital or through pre-financing of the crop by buyers (interviews 8, 9, 11). Multinational buyers emerged as the dominant financiers, either by providing financing directly or by providing securities against which a loan from the domestic banking sector is obtained (interview 8). LBCs owned by multinational trading companies have a ‘natural’ financing partner. Domestically owned LBCs, especially those with small balance sheets and limited own capital, are reliant on buyers’ willingness to pre-finance the sourcing of beans (interviews 6, 11). These pre-harvest arrangements are summarised in Figure 3, with red segments being those no longer in place and the green segment representing the new financing system.

18

Pre-harvest: Pricing and financing processes. Source: Authors.

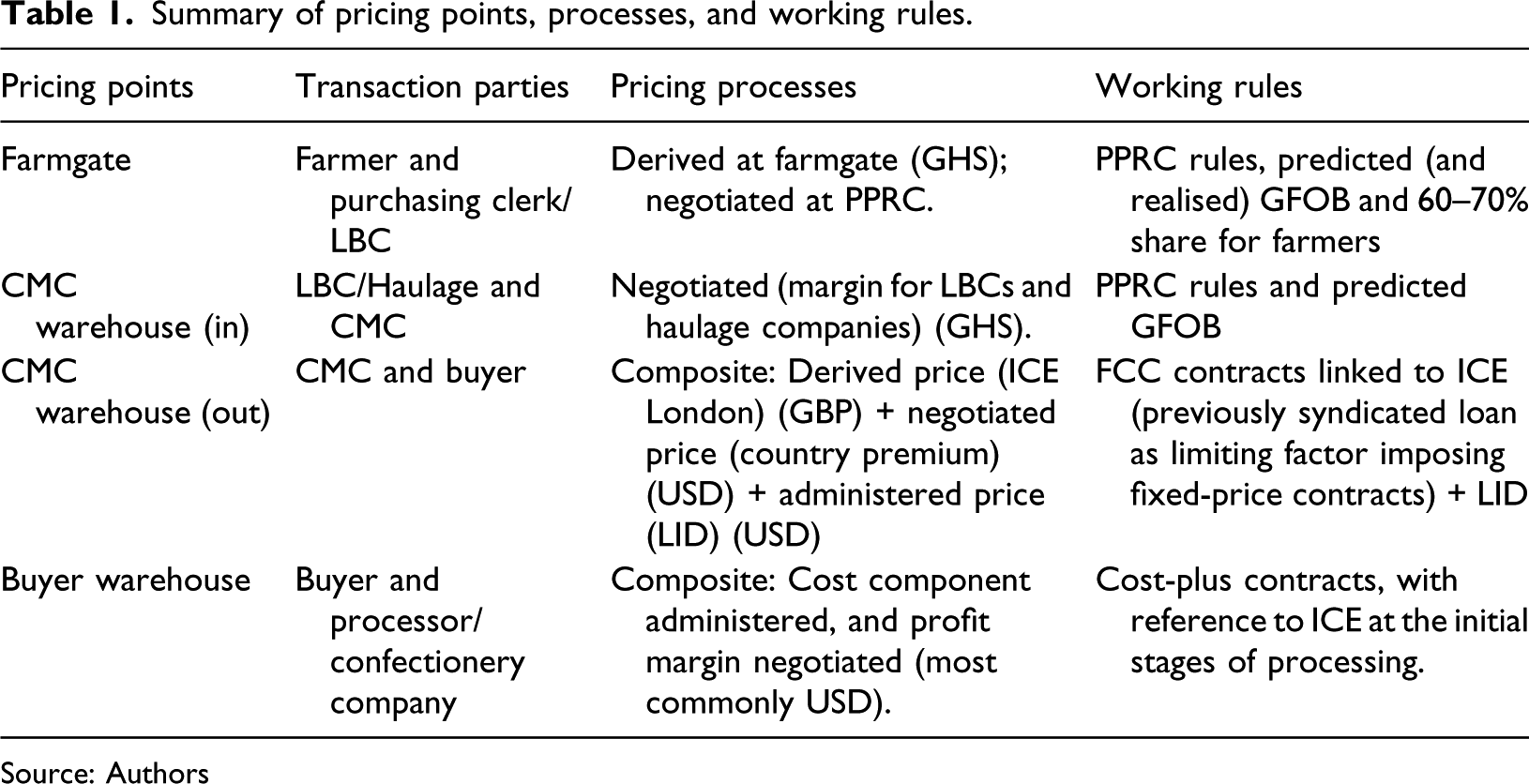

Margins received by LBCs and hauliers and the price received by cocoa farmers are negotiated within the Producer Price Review Committee (PPRC). The coverage of other costs incurred by Cocobod, like payroll, warehousing, jute bags for transport, fertiliser and pesticides, and quality control costs, as well as an export duty for the Ministry of Finance, is also negotiated. The PPRC includes farmer representatives, LBC representatives, hauliers, Cocobod and representatives from academia. The Minister of Finance chairs the committee. Before negotiations, all operational stakeholders are asked to submit an approximation of their costs and a suggested margin.

Working rules stipulate that the negotiations within PPRC are based on the projected gross free on board (GFOB). 19 The projected GFOB is the product of the forecasts for three variables: (i) crop size in tonnes, (ii) cocoa bean price per tonne in USD – itself a composite of terminal price and country premium and LID, and (iii) the projected exchange rate for 12 months starting September/October of Ghana Cedi per USD. The BoG provides the latter forecast, and Cocobod predicts the former two variables. Crop size predictions are based on pod counting and farmer surveys. Predictions on the bean price are based on the forward contracts already signed by CMC and market intelligence (and the predicted GBP-USD exchange rate).

Summary of pricing points, processes, and working rules.

Source: Authors

With the start of the harvest period, LBCs source cocoa beans from farmers through purchasing clerks and deliver them to CMC warehouses located in Tema, Takoradi, or Kumasi through haulage companies. When cocoa beans are delivered to a takeover point, the LBC receive a Cocoa Taken-Over Receipt (CTOR), which entitles them to be compensated by Cocobod (the money extended to farmers plus the agreed margin). Reimbursement is not immediate, and hence temporarily dislocated from the exchange. LBCs compete over volume, not price. A fast turnover is hence essential to remain profitable. After handover at the CMC warehouses, the LBC informs CMC of pre-financing arrangements (if there have been any), and the crop is shipped to the buyer who pre-financed the crop (interview 9).

After shipping documents are received, the respective buyer transfers payments to GHIB, which then transfers the USD to the BoG, which converts it into GHS and transfers it to Cocobod. Cocobod then settles the CTOR with the LBC, and the remainder is retained to settle operational expenses. Previously, GHIB would first repay the loan plus interest from the cocoa proceeds, before transferring the remainder to the BoG, prioritising payment to creditors over farmers; a condition of the syndicated loan. After all operational costs are deducted from the cocoa revenues, any profits are transferred to the Ministry of Finance as an additional export duty.

20

The flow of funds and goods during the harvest and post-harvest period is summarised in Figure 4, with red segments being those no longer in place and the green segment reflecting the new system. During and post-harvest: Flow of Funds and Goods. Source: Authors.

Figures 3 and 4 demonstrate the temporal dislocation between pricing processes and the flow of goods and moneys between pre and post/during harvest period. This dislocation introduces uncertainties, with benefits and costs carried unevenly by cocoa stakeholders. Who carries these risks and who benefits depends on the existing working rules governing the transactions along the cocoa chain and their contestations. These will be analysed in the following section.

The political economy of Ghana’s cocoa marketing

To understand power relations embedded in working rules and the division of the costs and benefits among cocoa stakeholders, we analyse two recent contestations of pricing processes: (i) the introduction of the LID in 2020 and the COVID-19 period, and (ii) the cocoa price surge in 2024 and the subsequent discontinuation of the syndicated loan.

The living income differential

More than 80% of the price received by CMC is derived from the terminal price over which CMC has no control. The terminal market is a market of contracts for the exchange of goods in the future. It is hence forward-looking and speculative in nature. Prices reflect traders’ expectations about future demand and supply conditions (and other interests), which are uncertain and can be subject to fads and sentiments. Prices are therefore not guaranteed to meet cocoa farmers’ intended profit margins or even their production costs in any given year.

The primacy of the terminal price and the institutions that govern the standardised contracts which impose this price, such as the FCC, are artefacts of colonial times. This working rule primarily benefits the commodity trading houses, that is, the buyers, for whom and by whom it has been established. Trading houses’ operational profits originate from both trading in physical commodities and trading in commodity derivative markets, where they use market intelligence for risk management, strategic positioning, and outright speculation. It is hence important for these companies to ensure a close relationship between the terminal price and the crop price. 21

However, decades of notoriously low prices have resulted in farmers selling their land or moving to more profitable crops such as rubber and oil palm, or to more profitable activities such as gold mining (interviews 3, 6, 7). This has put pressure on the cocoa sector regulators in the two largest cocoa bean-producing countries, Côte d’Ivoire and Ghana, to improve the profitability of cocoa farming, which gave rise to the LID. The LID was originally intended to provide a floor price to ensure that farmers receive a ‘living income’ (interview 5).

A floor price was not a mechanism that buyers could agree to, as it would have delinked the cocoa bean price from the terminal market (Staritz et al., 2023). Instead, a premium was negotiated, retaining existing working rules embedded in standardised FCC contracts with minor adjustments. The original calculation of a ‘living income’ was provided by the Fairtrade reference price and was estimated to be 2600 USD per tonne of cocoa in 2020 (interview 3). Since the terminal price hovered around 2200 USD at the time, the LID was set as a premium of 400 USD over the terminal price.

Once negotiated, the LID was administered by the two largest producer countries, leaving no room for negotiations within individual transactions. The country premium, on the other hand, remained a negotiated price between CMC and buyers. Buyers were quick to use the uncertainty of the COVID-19 crisis and a predicted drop in demand for chocolate to negotiate a reduction in the country premium to compensate for the LID. 22 Some buyers even sourced cocoa via terminal markets to circumvent the LID in a highly unusual move (interview 4). 23

The ability of producer countries to mobilise civil society in consumer countries, as well as an initially tight market, enabled them to introduce the LID. However, the introduction of a floor price as a new working rule would have undermined the business model of trading houses and turned the largest pricing component into an administered price. Trading houses successfully blocked this change in working rules. Further, producer countries’ dependence on cocoa-backed external financing limits their negotiation power vis-à-vis buyers. Refusing to sell for a low country premium would have left CMC with no money to finance cocoa sourcing.

The abandonment of the syndicated loan

Until its abolition in 2024, the syndicated loan was the most important source of access to international money markets for the BoG (interviews 1, 2) and financed most of the cocoa sourcing. However, the syndicated loan significantly curtailed CMC’s ability to time the market and thereby secure a favourable price level and exchange rates. 24 Since the loan had to be in place by September, CMC needed to commit an appropriate volume of cocoa through forward contracts, which meant locking in prices even in a rising market. While the forward-selling system enabled CMC to protect cocoa farmers against downside price risk in a declining market, it cannot benefit from a rising market.

Weather conditions brought about by particularly powerful El Niño events, aggravated by climate change, decades of underinvestment, and the expansion of gold mining, adversely impacted the 2023/24 crop (interview 6). In March 2024, Cocobod revised its cocoa crop forecast to a maximum of 425,000 metric tonnes for the season, just above half the initial forecast of 820,000 metric tonnes. Since Ghana is the second-largest producer globally, a harvest below expectations impacts prices, and the London ICE cocoa futures price tripled between January and mid-April 2024. Although a portion of the harvest was supposed to be reserved for spot sales, CMC inadvertently sold forward 333,767 metric tonnes of cocoa in excess of the realised harvest in 2023/24 (2025 State of the Nation Address). 25

Smuggling had further contributed to CMC’s over-commitment. If the producer price is lower than the terminal price during the harvest period, purchasing clerks are incentivised to smuggle beans to neighbouring countries with liberalised markets (interview 3). 26 In the reverse case, smuggling into Ghana can also cause problems, as CMC is obliged to buy at a price above the spot market. Hence, if prices move too much between the time the producer price is negotiated and harvest, price risk becomes further compounded with quantity risk. While the farmgate price was revised upward from 1575 USD to 2481 USD per metric tonne in April 2024 – financed by reducing margins for other cocoa stakeholders – the increase remained insufficient to discourage smuggling.

In a time of economic turmoil, a national debt crisis and elections (all present in 2023/24), Cocobod and CMC can face pressure from the government to sell forward a higher volume of beans to secure foreign exchange. The BoG gains direct access to around 2bn USD annually through cocoa bean sales, which makes Cocobod one of the most important government institutions in the country (interview 2). This lack of independence is perceived as a significant risk in times of crisis and has undermined CMC’s credibility to creditors (interview 4). The fact that Ghana had lost access to international capital markets 2 years earlier due to a debt crisis further increased the lenders’ perceived risk and hence interest rates. In 2021, the syndicated loan became the sole means of accessing international money markets and the largest contributor to foreign exchange reserves (interview 2). 27

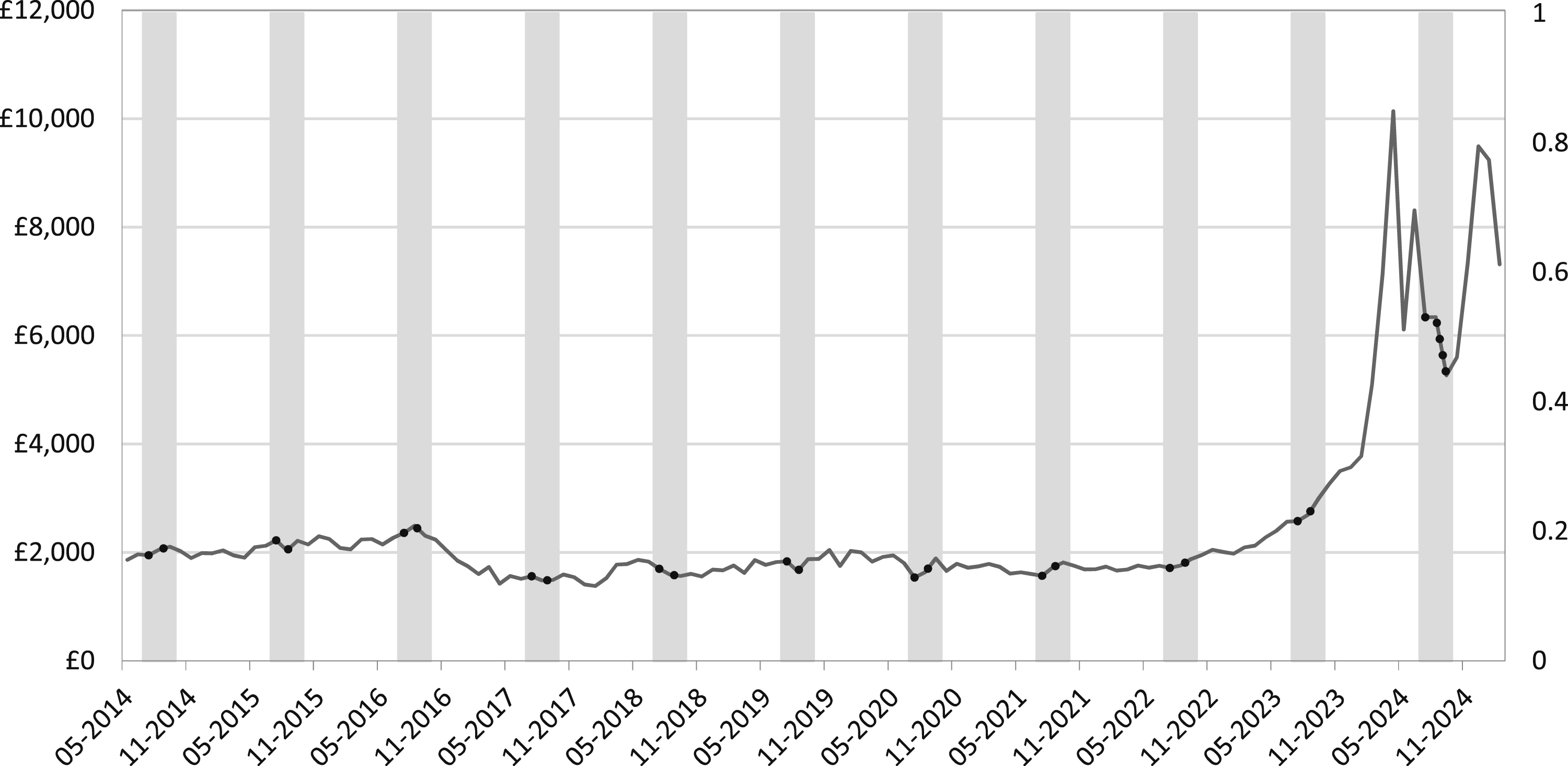

Overcommitting the crop meant that CMC was not only unable to benefit from high prices in the 2023/24 season, but also half of the predicted 2024/25 crop was committed for delivery at a price significantly below the terminal price (interview 6). Figure 5 demonstrates this situation. The grey periods mark August to October, where forward contracts are typically signed and prices locked in. For the 2023/24 season, an average price of about 2600 GBP was achieved, less than a third of the price reached in April 2024 and about half of what CMC was able to achieve for the non-committed crop in the buildup of the 2024/25 season (interviews 9, 10). The main beneficiaries of these price developments have been buyers who secured the crop at low prices and could manage the exceptional price volatility. Results, however, were mixed. While some buyers have suffered losses from open hedging positions, others have recorded substantial profits due to strategic hedging positions and passing on costs to consumers.

28

ICE London Terminal Prices (continuous next to maturity; in GBP per metric tonne). Source: Datastream.

With global reference prices skyrocketing, the agreed farmgate price for the 2023/24 season became increasingly untenable. The farmgate price was revised mid-season, and the syndicated loan and the forward-selling system underpinning it were abolished. However, the abolition had no immediate effect on the GFOB, and only in the 2024/25 season could CMC achieve higher sales prices. While defaulting on the outstanding contracts was a possibility, pressure from buyers and the IMF, which continued to manage Ghana’s debt crisis, forced Cocobod to honour these contracts (interviews 6, 9). To achieve an average sales price sufficient to meet the revised farmgate price plus operational costs, CMC mixed old (averaging around 2600 GBP) with new contracts (averaging around 5500 GBP), servicing about two-thirds of the outstanding contracts that season (interview 10).

The abolition of the syndicated loan provided CMC with greater flexibility to time the market. However, the crop’s seasonality and the need to cover operational costs still imposed limitations on the timing of sales (interview 6). During harvest, Cocobod requires liquidity to purchase the incoming crop from farmers at the negotiated farmgate price. Previously, the syndicated loan provided this liquidity. Now, the liquidity is provided by buyers who pre-finance the crop or through other financial arrangements made by the LBCs. However, after the crop is delivered to CMC warehouses, CMC is required to purchase the crop and reimburse LBCs for the money extended to farmers, plus the agreed margin for their services. 29

In the absence of external funding, independent of the cocoa trade, Cocobod relies on the sale of beans during harvest to obtain the necessary liquidity to settle its CTOR obligations as well as its operational expenses (interviews 6, 10). If unable to do so, farmers are left without a buyer or without payment, resulting in crop loss and smuggling, and LBCs are at risk of defaulting on their loans, putting pressure on the domestic banking sector. Delays in settling CTOR obligations means LBCs and farmers are extending involuntary trade credit to Cocobod. Further, under the new system, CMC is obliged to sell any pre-financed crop to the dedicated buyer, reducing both control over volume and the timing of sales (interview 6).

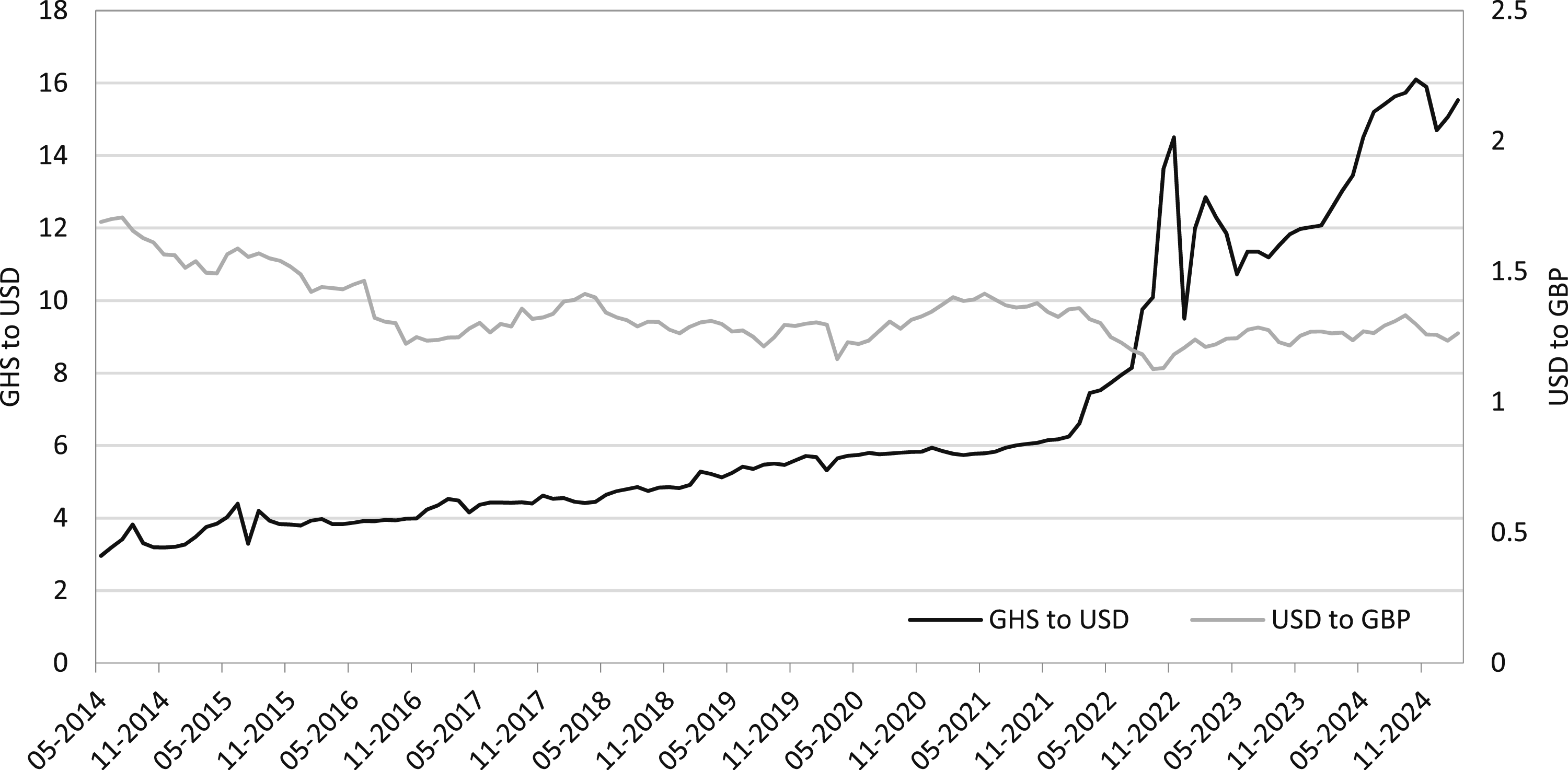

Timing sales is not only essential to securing a favourable price level but also to securing a favourable exchange rate. CMC is exposed to two exchange rate risks: GHS to USD and USD to GBP. For instance, CMC incurred large losses when the GBP depreciated sharply against the USD immediately after the Brexit referendum in June 2016 and the mini budget of the Truss administration in September 2022. 30 A weakening of the GBP against the USD affects Ghana’s cocoa revenue negatively, while it benefits buyers.

Further, the GHS has continuously depreciated against the USD since 2013, which accelerated in 2021 due to a debt crisis; see Figure 6. A depreciating currency encourages smuggling, as the farmgate price denominated in GHS loses in value during the season, leading to a suppressed producer price relative to neighbouring countries. The situation is further aggravated by payment delays, with farmers (and LBCs) carrying the costs. Since the projected exchange rate is used to calculate the projected GFOB, any depreciation beyond the prediction is a windfall for Cocobod and an indirect tax gain for the government. GHS-USD and USD-GBP exchange rates (monthly). Source: Datastream.

Since terminal prices and exchange rates are outside CMC’s control, the point in time at which these prices are derived is a crucial determinant of the GFOB and the producer price. However, CMC’s flexibility in timing the market is curtailed by its need to finance its internal marketing. Some flexibility has been gained by discontinuing the use of a syndicated loan. However, Cocobod remains dependent on cocoa revenues to finance its internal operations, which curtails CMC’s freedom to time its sales.

Multinational buyers as well as chocolate manufacturers operate on a cost-plus basis, which means they pass on rising costs to their clients and ultimately to consumers. This is either achieved by increasing the price of chocolate, lowering the bean content in a chocolate bar, or reducing the weight of the chocolate bar. Their ability to administer prices means that they can protect their profit margins. CMC cannot pass on higher costs to buyers, as all beans are referenced against the terminal price, which means most of the price achieved by CMC is derived and outside of its control.

The events leading up to the discontinuation of the syndicated loan demonstrate the importance of understanding pricing processes as being temporarily dislocated from exchange processes. This dislocation reveals the unequal division of the costs and benefits of price risk among cocoa stakeholders. Trading houses are best placed to benefit from risk due to their dual position in the market as both buyers and sellers, their capacity to store, their presence in the terminal market, and their market power. These events further demonstrate how the material and financial constraints faced by Ghana limit its ability to change the working rules governing pricing processes to its advantage. As the Ghanaian cocoa sector remains dependent on external financing, CMC’s ability to time sales remains constrained.

The analysis also reveals a broader imbalance in commodity chains between primary commodity producers and processors. The price achievable by CMC to form the GFOB is a composite. However, roughly 80% of this composite are derived and outside its control. This means that prices could fall well below the average cost of production, which has contributed to decades of underinvestment in the sector and given rise to the narrative of ‘unfair’ prices motivating the LID. Downstream stakeholders enjoy greater control over prices as cost-plus contracts underpin pricing processes, and products are more diversified, which allows adjusting different cost points.

Discussion and conclusion

We develop a novel analytical framework inspired by Commons’s institutional theory to understand pricing processes along commodity chains. We thereby contribute to a small but growing literature which centres pricing processes within commodity chains and the power structures embedded therein to understand how value is created and distributed along the chain. The concept of transaction, as defined by Commons, enables us to understand pricing as an institutionally embedded and politically contested process which is temporally and spatially dislocated from the exchange process. Within this understanding of transactions and pricing processes therein, we can identify how power asymmetries shape pricing processes as well as outcomes and how working rules set the boundaries within which these outcomes materialise.

We use our analytical framework to map pricing points along the Ghanaian cocoa chain. Based on this map, we conduct a political economy analysis of the institutional setup through which prices emerge and through which price risk is distributed within the Ghanaian cocoa sector to identify those who achieve higher value capture, those who carry the burden of price volatility and those who benefit from it. The analysis focuses on two recent episodes, the introduction of the LID and the discontinuation of the syndicated loan, as examples of contestations of pricing processes and the working rules governing them. We find that CMC has limited ability to control cocoa prices, despite being the monopoly seller of Ghanaian cocoa beans and despite Ghana having recently formed a cocoa cartel with Côte d’Ivoire. Because of the primacy of the terminal market as a reference price, CMC has no control over most of the price it receives. If costs increase, these cannot be passed on to buyers.

The use of the terminal market as a reference price, as well as multiple currency conversions, leaves CMC exposed to significant price and quantity risk. While forward selling has clear advantages during times of moderate price declines and protects cocoa farmers from downside risk, it can cause significant losses in times of high price volatility, due to both smuggling and foregone income in a rising market. The abolition of the syndicated loan has provided CMC with more flexibility in timing the market. However, since Cocobod remains reliant on the sales revenues to finance internal marketing as well as operational costs, it is forced to sell even if market conditions are not favourable. The ability of buyers to pre-finance the crop through an LBC has further undermined CMC’s control over the quantities sold.

Ghana’s quantity and price risk is therefore managed by its counterparties, which dictate the timing of the price derivation, even after the abolition of the syndicated loan. Buyers largely remain in control of timing sales. As long as CMC cannot finance the internal marketing independently from cocoa revenues, it remains dependent on buyers, undermining its bargaining position despite its considerable market power. This has severely constrained its ability to change the working rules governing pricing processes and leaves it exposed to price risk, ultimately resulting in stable but suppressed prices for Ghanaian cocoa farmers.

The ability to store the crop, ideally in or near consumer markets to reduce the risk premium attached to storage at origin, as well as the ability to secure financing independent of cocoa income, would change CMC’s bargaining position vis-à-vis buyers and therefore its ability to change working rules in its favour. A liquidity reserve fund could play this role, enabling Cocobod to extend financing to LBCs, thereby retaining competition among LBCs, supporting domestically owned LBCs, and countering the increased control of multinational buyers over the sector through pre-financing agreements. This could be combined with a dedicated risk management strategy, mimicking the operational capabilities of its buyers.

Footnotes

Acknowledgement

We are grateful to various cocoa stakeholders who have been extremely generous with their time and patience in answering our questions. We are also grateful to the participants at the workshop on ‘The Political Economy of Commodity Pricing and Price Interventions’ hosted by ISSER University of Ghana on 21 March 2024 for sharing invaluable knowledge and insights into the Ghanaian cocoa sector, as well as providing feedback and policy suggestions. We also thank the participants of the PKES 2024 annual workshop held at SOAS University of London and colleagues from the Global Development Institute (GDI) at the University of Manchester for their valuable feedback and encouragement. We dedicate this paper to the memory of Cornelia Staritz, a giant in the field, and a dear colleague and friend who left us far too early.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the International Science Partnerships Fund Institutional Support Grant (ODA) funding from 2023 to 2024 and the Simon Industrial and Professional Fellowship 2024.

Declaration of conflicting interests

The authors declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: Fuad Mohammed Abubakar serves as the Managing Head of the Ghana Cocoa Marketing Company (UK) Ltd, a subsidiary of Cocoa Marketing Company Ghana Ltd. This piece was co-authored in his capacity as an independent researcher and a fellow at the Global Development Institute of the University of Manchester. The views expressed do not represent the views of the Ghana Cocoa Marketing Company (UK) Ltd or the Cocoa Marketing Company Ghana Ltd

Notes

Appendix

List of Interviews.

1

25/02/2024

Bank of Ghana

2

22/03/2024

Bank of Ghana

3

22/03/2024

Ghana civil society cocoa Platform

4

25/03/2024

CMC

5

25/03/2024

Bank of Ghana

6

21/02/2025

CMC

7

25/02/2025

Cocoa farmer representative

8

26/02/2025

LBC

9

27/02/2025

LBC

10

27/02/2025

Cocobod

11

28/02/2025

LBC