Abstract

This paper studies how critical entrepreneurial finance outcomes such as the investment return and equity division are shaped by venture characteristics, financier risk preferences, and competitive searching. Our analysis uses a double-hazard agency model in which financiers determine the equity division to maximize the expected utility of their investment return while entrepreneurs search for the best deal. Model results provide new theoretical insights on the venture funding cycle, the coexistence of angels/venture capitalists (VCs) with heterogeneous risk aversion, and risk separation in the entrepreneurial finance market. The model predicts that financiers with higher funding capacity and advisory capabilities (e.g., VC firms) will prefer to fund at later stages as their expected investment return rises with the venture’s initial value and financier productivity. Competitive searching by entrepreneurs enables financiers with a diverse set of risk preferences to coexist profitably by reducing the advantage (disadvantage) of lower (higher) risk aversion financiers and making investment returns more similar. Further, the model shows the emergence of a risk separation cutoff beyond which only angels/VCs with lower levels of risk aversion can profitably fund riskier ventures.

Keywords

New start-ups and ventures formed by entrepreneurs typically obtain financing from private investors such as angels and venture capitalists (VCs) instead of traditional sources such as banks or public stock markets. Studies report that the size of the angel finance market approximately equals that of the VC market and can be larger during certain periods (e.g., Organization for Economic Cooperation and Development [OECD] report by Wilson, 2011; Sohl, 2015). Sohl (2015) reports that 71,110 entrepreneurial ventures received angel funding in 2015 from 204,930 investors and the total investment was $24.6 billion. Pure equity deals are common in angel finance in the United States and Canada where the contract stipulates a simple division of future venture value between the entrepreneur and financier (e.g., Cumming, 2005; Wong, Bhatia, & Freeman, 2009). In contrast, venture capital deals involve the use of preferred or preferred convertible securities (Kaplan & Stromberg, 2004). Recent empirical research also suggests that angel investors and VCs can act as “dynamic substitutes” in that companies that obtain VC funding are less likely to obtain subsequent angel funding and vice versa (Hellmann, Schure, & Vo, 2013).

Given that VCs can potentially provide funding in earlier or later stages, the theoretical venture finance literature has attempted to rationalize the concentration of angel funding at early stages and VC funding at later stages (e.g., Chemmanur & Chen, 2006). Further, prior to settling on a particular deal, it is in the interest of entrepreneurs to search for the best funding deal from several potential financiers (angels/VCs). This paper provides additional insights into the role played by heterogeneity in financier risk preferences and competitive searching on critical entrepreneurial finance outcomes such as the expected investment return and equity division.

Our analysis uses a double-hazard agency model in which financiers determine the equity division that maximizes the expected utility of their investment return while entrepreneurs search for the best deal. Model results provide new insights on how interactions between venture characteristics (venture risk, financier risk aversion, initial project value, funding size, and financier/entrepreneur productivities) can rationalize the venture funding cycle, the coexistence of angels and VCs with heterogeneous risk aversions, and the emergence of a risk separation in the entrepreneurial finance market. Our theoretical results can also provide valuable insights to angels, VCs, entrepreneurs, and practitioners in designing and analyzing venture deals.

Consistent with the pattern of funding activity by angels/VCs observed in the entrepreneurial finance industry, the model shows analytically that financiers with access to larger investment funds (e.g., VC firms) will benefit by funding ventures at the later stage of development because their expected investment return increases with the venture’s initial value and financier productivity. At the later stage, there is an increase in both the ventures’ initial value and VCs’ ability to add value by providing advice and management services (Shane, 2009). As the venture matures and the productivity of the VC rises (relative to the entrepreneur), the model predicts that this will lead to an increase in the expected investment return and a lower equity share for the entrepreneur.

The model further shows that competitive searching by entrepreneurs enables financiers with heterogeneous risk preferences to coexist in a market that otherwise would favor financiers with lower risk aversions. Without search, lower risk aversion financiers have an advantage in the venture finance market: their expected investment return is higher, the equity share given to entrepreneurs is lower, and they can more profitably finance higher risk projects. In addition to the expected return, high risk–averse investors are also concerned about venture risk (which is present in their expected utility). To improve risk sharing and mitigate the negative impact of uncertainty on entrepreneur effort, they provide more equity to entrepreneurs, which reduces their expected return. In the presence of competitive search by entrepreneurs, an equilibrium emerges that allows a diverse set of financiers with heterogeneous risk preferences to operate profitably by reducing the advantage (disadvantage) of lower (higher) risk aversion financiers and makes returns similar. This result is agnostic to the assumption of whether VC firms are more or less risk averse than angel investors (see Section Competitive Search and Coexistence of Angels/VCs).

Finally, a risk separation emerges in the entrepreneurial finance market beyond which higher risk ventures can only be feasibly funded by angels/VCs with lower levels of risk aversion. This arises because while the expected investment return and equity division is unaffected by venture risk for risk-neutral financiers, the expected return declines with risk and risk aversion for risk-averse financiers. To raise declining entrepreneur effort in the face of higher venture uncertainty and reduce their risk exposure, risk-averse utility-maximizing financiers respond by increasing the entrepreneur’s equity share and the net result is a lower expected investment return. The paper also introduces a number of new theoretical features in venture finance agency modeling that are important to generating analytical results that connect the expected investment return to financier risk aversion and other venture characteristics. These include generalizing the financier to be risk averse, modeling the venture’s future value as a continuous random variable that depends functionally on a rich set of inputs (e.g., initial venture value, funding size, entrepreneur/financier productivities and efforts), and using the investment return in the financier’s objective function. Many venture finance agency models assume risk-neutral financiers and outcomes take binary values (with effort affecting the probability of the higher outcome). This is also among the first papers in entrepreneurial finance that incorporates equilibrium search by entrepreneurs over financiers with heterogeneous risk preferences.

A broad theoretical literature seeks to explain the nature of venture capital contracts and explores the implications for entrepreneurs, VCs, and policy makers. As well as theories about why start-ups may find equity preferable to debt contracts (Chemmanur & Chen, 2006; De Bettignies & Brander, 2007; Ueda, 2004) and the nature of projects financed by equity (Winton & Yerramilli, 2008), researchers have attempted to offer theoretical rationales for a range of specific equity contracts. These include convertible debt–equity contracts (Berglöf, 1994; Casamatta, 2003; Hellmann,1998, 2006; Kaplan & Strömberg, 2003)); staged financing whereby VCs release funds in discrete tranches (Bergemann & Hege, 1998; Li, 2008); and vesting and control rights (Gompers & Lerner, 1999). Other theoretical work explores strategic interactions between entrepreneurs and financiers, including the possibility of opportunistic behavior (Cornelli & Yosha, 2003; Elitzur & Gavious, 2003; Fairchild, 2011; Schmidt, 2003; Schure, 2006). This work provides a rich theoretical landscape that helps us to comprehend a wide variety of equity contract forms and their role in financing entrepreneurial activity. We discuss some relevant aspects of this literature below and relate it to the model and analysis of this paper.

One of these streams explores the boundaries between VCs and bank financing. Ueda (2004) assumes that VCs have greater capabilities to screen entrepreneurial opportunities than banks and, therefore, need to rely less on collateral to finance entrepreneurs. Their model predicts that VCs are more likely than banks to finance companies with high return and risk profiles and entrepreneurs who possess relatively little collateral will be more likely to seek VC financing. De Bettignies and Brander (2007) point to financier effort as a major distinction between VCs and banks and show that equity contracts best balance the incentives for both contracting parties when the marginal value of VC effort is sufficiently high. In a similar direction, this paper extends our understanding of the coexistence of financiers with heterogeneous risk preferences and differing funding capacity (e.g., angels, VCs) in a context of searching by entrepreneurs for the best deal.

The literature has also examined strategic issues at the exit stage of the venture. Berglöf (1994) analyzes the potential conflict of interests between entrepreneurs and VCs that arises from a future sale of the company to a third party. The entrepreneur values private benefits of control that increase with firm value and is afraid of a sale that compensates him insufficiently for their loss while the VC is afraid of a premature “cheap exit” that leads to poor investment returns. Hellmann (1998) studies why entrepreneurs give up control rights to VCs who expend costly effort to search for a superior management team. This exposes entrepreneurs to the risk of being fired before their shares are fully vested. In subsequent work, Hellmann (2006) shows why VCs use contracts with convertible preferred equity to mitigate concerns regarding exit decisions as they allocate different cash flow rights for acquisitions and initial public offerings (IPOs). With a similar focus on exit, Elitzur and Gavious (2003) analyze a sequential investment game with moral hazard comprising entrepreneurs, angels, and VCs where angels invest before VCs and are concerned of value transfer to VCs; all agents are risk neutral. 1 Inderst & Müller, 2004 adopt a bargaining perspective and argue that bargaining power between entrepreneurs and VCs, as reflected in equity shares inter alia, varies with technological and economic conditions. Fairchild (2011) allows for potential “stealing” by either the entrepreneur or the financier at the IPO stage and shows how entrepreneur/angel empathy relative to the VC’s value-adding abilities affects financing choices.

Hellmann and Thiele (2015) use a costly search model on deal flows between the angel and VC markets to obtain an equilibrium relationship that endogenously characterizes market sizes, valuation levels, and exit rates. Our analysis incorporates double-sided hazard but abstracts over issues related to the mode of exit as our primary focus is on understanding how heterogeneity in financier risk preferences interacts with important venture characteristics (e.g., project risk, initial value, financier/entrepreneur productivities) to shape funding outcomes under competitive search by entrepreneurs.

Cumming (2005) finds that pure equity deals remain in widespread use around the world and are especially common in the context of angel finance. In our analysis, they provide a common benchmark for comparing the expected investment return and equity division in contracts designed by financiers with differing funding capacities and risk preferences (e.g., angels, VCs). A number of studies rationalize the use of convertible securities in VC financing contracts (Baiman, Bar-Yosef, & Sarath, 2008; Casamatta, 2003; Schmidt, 2003). Schmidt (2003) analyzes a double moral hazard model where the entrepreneur provides effort first and the VC second. With conversion, the VC has stronger equity-like incentives and the entrepreneur works hard so that the VC sees enough upside potential to convert and become a common equity holder. Casamatta (2003) also considers the possibility that an outsider can provide value-adding advice in addition to effort by the entrepreneur and shows that the provision of advice creates information rents and that convertible preferred equity (CPE) is the optimal contracting security for sufficiently large investments. Baldenius and Meng (2010) consider how entrepreneurs can signal their firm’s value to investors who have the expertise to contribute actively to the start-up company’s operations and firm decision-making.

In a different vein, Kanniainen and Keuschnigg (2003, 2004) study how a risk-neutral VC decides on the size of his portfolio of start-ups with costly advisory effort. The VC faces a trade-off in that advice could be spread too thinly, thereby reducing the survival chances of all firms in the portfolio. As projects become riskier, the VC must cede a higher profit share to entrepreneurs to secure their effort that is critical for survival. With the corresponding erosion in the VC’s own profit share, the VC eventually finds it unattractive to expand the portfolio further. Keuschnigg and Nielsen (2004) show that by failing to internalize effort costs of the other party, equity share divisions are generally inefficient and require a corrective tax to restore efficiency. Sørensen (2007) considers a matching model in which more experienced VCs add more value and bring companies public at a higher rate.

The remainder of the paper is organized as follows. The Model section presents the model and its solution. Discussion of model results and implications follow in the Discussion and Implications section. The Summary and Conclusion section concludes the paper.

The Model

The model reflects the strategic interaction between an entrepreneur E (agent) and potential financiers F (principal) willing to provide venture financing in return for an equity position. Financiers are heterogeneous in their risk aversion

Project Value and Financing

An entrepreneur E owns a project with initial value

Next, E searches for the best financing deal from financiers of types

The Financier’s Investment Problem

The financier

The utility of the financier from the venture’s investment return is given by

The financier

The financing problem of

Note that the financier’s utility in (5) is based on F’s investment return while the same for the entrepreneur in (6) is E’s value from the venture. This is because the venture is a mutually exclusive project for the entrepreneur, while it is not for the financier (VC or angel). Entrepreneurs will typically be fully engaged in their ventures while VCs and angels will invest in a number of different opportunities concurrently. Corporate finance theory suggests that the decision rule for non-mutually exclusive projects should be the profitability index (PI) constructed by dividing each project’s net present value (NPV) by the scare resource. In the venture context, the relevant scarce resource is the funding capital f so that

The weak inequality in (8) represents two possible situations. The first is that the constraint holds with equality, which implies that entrepreneurs receive the lowest equity valuation that makes them indifferent to choosing between pursuing the entrepreneurial venture and their best alternative monetary opportunity. It also implies that the equity share

An optimal contract

The equity stake

The entrepreneur’s participation inequality (8) holds, meaning that the contract

Our interest is naturally on feasible deals that the entrepreneur will accept (i.e., satisfy Definition 1). The expressions for

Optimal Equity Contract and Efforts

The problem (5–7) for financier

Both efforts increase with productivity, incentive share, initial project value, and funding size, while they decrease with the agent’s cost of effort. Incorporating the best effort response (9) and (10) into (5), the first-order condition for the equity share leads to the equity division in Proposition 1 (see Appendix A for details).

The optimal equity share for the entrepreneur that maximizes

Financier

The optimal efforts for the entrepreneur and financier in Proposition 2 follow from using the equity shares (11) and (12) in (9) and (10).

The optimal effort levels of the entrepreneur and financier

Finally, Proposition 3 reports the optimal expected investment return for the financier. The expression follows directly from substituting the financier’s equity share (12) and efforts (13) and (14) into the financier’s investment return (3) and simplifying.

Financier

The Entrepreneur’s Equilibrium Search Contract

Prior to accepting a venture funding deal, it is in the interest of any entrepreneur to search for the best deal from several potential financiers (e.g., angels, VCs). These financiers are likely to have differing risk preferences

Let

Using standard arguments, the feasible contract

Equation (17) implicitly defines the critical level of financier risk aversion

In solving (17), Assumption 1 below ensures that the optimal solution for the equity division in Proposition (1) holds during competitive search by the entrepreneur across financiers of different types. It reflects the realism that funds available from financiers are a much scarcer resource than entrepreneurial projects seeking funding. It excludes perfect competition among potential financiers of the same type

The total demand for venture funds by entrepreneurs exceeds their supply available from each type of financier

Under Assumption 1, the financier would simply wait for one of many entrepreneurs to approach and provide funding that yields the expected return of Proposition 3. Excess demand for venture funds ensures that their investment capital will be fully deployed. If there was excess supply of venture funds, perfect competition between financiers will lead them to increase the entrepreneur’s equity stake beyond the optimal level in Proposition 1 until their expected investment utility in (5) goes to zero.

6

It is also useful to note that Assumption 1 is implicitly made in other venture finance models where the analysis is based on a contract designed by a risk-neutral financier (

The expected value of the equity deal offered to the entrepreneur

Equilibrium Search Contract

If financiers

If the feasible equilibrium search contract

Comparative Statics and Numerical Results

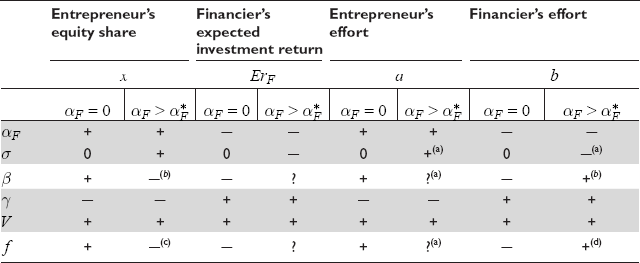

The model’s comparative statics are summarized in Table 1. The signs of the partial derivatives for the entrepreneur’s equity share, expected investment return, and entrepreneur/financier effort (columns) are reported with respect to various model parameters (rows). To aid in the analysis, the signs are reported in separate columns for both a risk-neutral financier (

Comparative Statics.

The table displays the sign of the partial derivatives for the entrepreneur’s equity share, expected investment return, entrepreneur effort, and financier effort (columns) with respect to various model parameters (rows). When

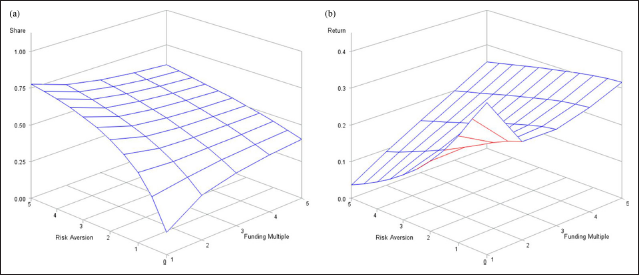

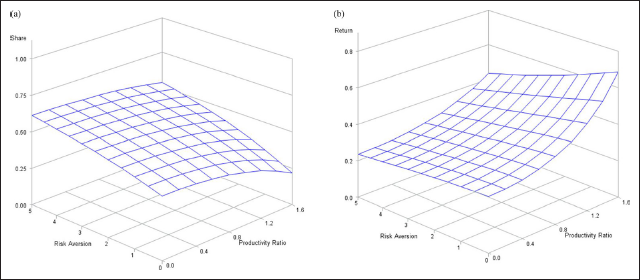

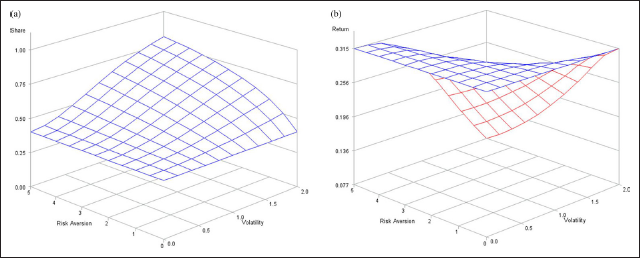

Figures 1–3 report three-dimensional graphs for the entrepreneur’s optimal equity share and angel/VC expected investment returns. They depict how these key deal outcomes respond to combinations of financier risk aversion with venture risk, financier/entrepreneur productivities, and funding size.

Venture uncertainty and risk aversion. (a) Entrepreneur’s equity share and (b) angel/venture capitalist expected return.

Productivity ratio and risk aversion. (a) Entrepreneur’s equity share and (b) angel/venture capitalist expected return.

Funding size and risk aversion. (a) Entrepreneur’s equity share and (b) angel/venture capitalist expected return.

The numerical results are generated by setting model parameters to the following values:

The graphs below show that risk aversion of the angel/VC and venture risk plays an important role in determining their expected investment return and the corresponding entrepreneur’s equity share. When F is risk neutral or venture risk is zero, the equity share and expected return remain constant. When F is risk averse, the equity share rises with venture return volatility, but the expected return declines and E’s equity share rises uniformly with risk aversion. There is also positive interaction effect where the equity share rises with risk aversion and venture return volatility; on the other hand, an increase in both these parameters leads to a fall in the expected return.

A rise in venture uncertainty discourages entrepreneur effort, as outcomes become more random. To elicit the utility-maximizing level of effort, risk-averse financiers respond by offering a higher equity share to entrepreneurs (

It is interesting that the financier’s effort and expected return decreases with

The graphs in Figure 2 show that as the angel/VC becomes more productive relative to the entrepreneur (productivity ratio γ/β rises), the financier’s expected investment return increases and less equity is offered to the entrepreneur (

Funding size has an interesting effect on the entrepreneur’s equity share that depends on the level of financier’s risk aversion (Figure 3a). When F is risk neutral, the equity share rises with the funding multiple (

The financier’s expected return generally rises with funding size; however, there is an interesting reversal pattern for lowest risk–averse angels/VCs. The return initially declines with funding size and then continues to increase. Overall, Figure 3b exhibits a funding scale effect, suggesting that financiers with access to larger pools of funding capital will benefit by investing more in fewer similar projects than investing smaller amounts in more projects.

Discussion and Implications

We now discuss the major implications of model results on how critical entrepreneurial finance outcomes (e.g., expected investment return and equity division) are influenced by venture characteristics, heterogeneity in financier risk preferences, and competitive searching by entrepreneurs. More specifically, we show how interactions between venture risk, financier risk aversion, initial project value, funding size, and financier/entrepreneur productivities rationalize the venture funding cycle, the coexistence of angels/VCs with heterogeneous risk aversions, and the emergence of risk separation in the entrepreneurial finance market. It is also useful to point out that the implications and discussion below are based entirely on the unambiguous results from the model—these are summarized in the shaded cells of Table 1 (for parameters

The Venture Funding Cycle

Model results show that the venture’s initial value

First, note that the model shows analytically that the financier’s expected investment return rises with initial project value and financier productivity:

Further, higher financier productivity reduces the equity offered to entrepreneurs (

Model results on project size and financier productivity support the emergence of a venture capital cycle (e.g., Gompers & Lerner, 1999; Hellmann et al., 2013; Shane, 2009). In this cycle, new start-ups often raise relatively modest sums initially and then seek larger funding in later rounds when the VC is in a position to add more value. Note that the model (5 – 8) with equilibrium search (17) captures the strategic interaction in any independent funding round between the entrepreneur and potential financiers (angel or VC). At the start of each such round, the initial value of the venture

Since

Finally, the numerical results in Comparative Statics and Numerical Results show a funding scale effect where the financier’s expected return generally increases with funding size (Figure 3b). This means that angels/VCs with larger amounts of funding capital can raise their expected return by investing more in fewer similar projects than investing smaller amounts in more projects.

Risk Separation in the Entrepreneurial Finance Market

An interesting risk separation emerges due to the interaction between financier risk aversion (

Model results show that the expected investment return and equity division of risk-neutral financiers is unaffected by venture risk (

While the preceding analytical results are consistent with intuitive reasoning, it is useful to note that they arise from the model’s new theoretical features. This includes allowing the generality of risk-averse financiers and defining their utility function in terms of the investment return. Venture finance models in the literature typically assume risk-neutral financiers and their objective function are based on venture profits (which are dependent on investment scale).

Competitive Search and Coexistence of Angels/VCs

We next show how competitive searching by entrepreneurs enables a broader spectrum of financiers with differing risk preferences to operate profitably in the venture finance market. Searching reduces the comparative advantage that lower risk aversion financiers have over higher risk aversion financiers.

First, note that in the absence of search, venture financiers with lower levels of risk aversion benefit as they have higher expected investment returns. This follows directly from the negative relationship between the financier’s expected investment return and risk aversion:

Next, with competitive searching by entrepreneurs, the model shows that the equilibrium outcome allows financiers with a broader range of risk preferences to coexist. Here, the equilibrium search contract

These insights from the model are visible in Figures 1b, 2b, and 3b of the numerical study (Comparative Statics and Numerical Results) which show that the expected investment return of the financier declines secularly with F’s risk aversion at differing levels of venture risk, financier/entrepreneur productivities, and funding size. Since the equilibrium search contract is interior to the range, a financier’s deal will be accepted by the entrepreneur if it is close to the one defined by (11). This means that under the equilibrium search contract, the expected return of higher risk aversion financiers increases as their return moves up the return surface, while the same for the lower risk–averse financiers decreases (they move down the return surface).

Financier Expected Returns—Equilibrium Search

The equilibrium search contract

Reduces the higher expected investment return of lower risk aversion financiers

Raises the lower expected investment return of higher risk aversion financiers

Note that the model result on the coexistence of financiers with differing risk profiles under competitive search by entrepreneurs is agnostic to the assumption of whether VCs are more or less risk averse than angel investors. The equilibrium dynamics under search means that a larger set of angels and VCs clustered around the equilibrium level of risk aversion

Empirical Implications

Given the preceding discussion of model results, we summarize below some testable empirical implications from the model.

Summary and Conclusion

This paper expands our theoretical understanding of how critical entrepreneurial finance outcomes such as the expected investment return and equity division are shaped by important venture characteristics (e.g., project risk, financier risk aversion, initial project value, funding size, financier and entrepreneur productivities). Our analysis uses a double-hazard agency framework where financiers maximize the utility of their investment return, both sides can contribute to the future value of the venture, and entrepreneurs search for the best deal. Model results provide a number of insights on the role played by funding capacity, heterogeneity in financier risk preferences and competitive searching on the venture funding cycle, the coexistence of angels/VCs, and risk separation in the entrepreneurial finance market.

The model provides theoretical support for the pattern of funding activity observed in the venture finance industry with angels funding start-ups in their earlier stage and VCs engaging at the later stage when the venture’s initial value is higher and when they have greater capability to provide value-adding advice and management services. Here, the model shows analytically that the expected investment return increases with the venture’s initial value and financier productivity. Therefore, financiers with access to larger investment funds (e.g., VC firms) will benefit by waiting to fund larger ventures at later stages of their development. Moreover, as the venture matures, the productivity of the financier rises relative to the entrepreneur (Gompers & Lerner, 1999; Shane, 2009). The model predicts that this will have a positive impact on the expected investment return of VCs at later stages while reducing entrepreneurs’ equity share. The tendency of VC firms to concentrate their investment portfolio on specific sectors (e.g., biotech, IT, social media) is also consistent with the model. This allows them to develop more focused capabilities that increase financier productivity, leading to higher expected returns.

The model further shows that competitive searching by entrepreneurs leads to outcomes where financiers with a diverse range of risk preferences can coexist in the venture finance market by making their investment returns similar. Without search, lower risk aversion financiers would have the advantage as their expected investment return is higher, the equity share given to entrepreneurs is lower, and they can profitably fund higher risk projects. With search, an equilibrium arises that reduces the advantage (disadvantage) of lower (higher) risk aversion financiers. The lower expected investment return of higher risk aversion financiers rises and the equity share given to entrepreneurs declines. Similarly, there is a decline in the higher expected return of lower risk aversion financiers and the equity share given to entrepreneurs increases.

Lastly, a risk separation emerges in the entrepreneurial finance market where higher risk ventures can only be profitably funded by angels/VCs with lower levels of risk aversion. The model shows that while the expected investment return and equity division of risk-neutral financiers is unaffected by venture risk, the expected return declines with venture risk and risk aversion. In maximizing the utility of their investment, risk-averse financiers respond to lower entrepreneurial effort (due by venture risk) by offering a higher equity share and this also improves risk sharing by reducing their exposure to venture uncertainty.

The paper also contributes to the entrepreneurial finance literature by introducing some new modeling features. The model allows the generality of a risk-averse financier and our analysis is based on the financier’s investment return, which is a primary measure of performance in the venture finance industry. Further, the venture’s future value is modeled as a continuous random function that incorporates a rich set of inputs (initial venture value, funding size, entrepreneur/financier productivities and efforts). Finally, the analysis incorporates equilibrium search by entrepreneurs over financiers with heterogeneous risk preferences. Therefore, model results regarding expected investment returns and equity division for risk-averse financiers are new contributions to the entrepreneurial finance literature. These results show analytically how financier risk aversion, venture risk, initial venture value, and funding size impact these important entrepreneurial finance quantities.

There is considerable potential to extend the model and analysis in a number of promising directions. First, the model provides a rich set of predictions and hypotheses for future empirical studies (see Table 1). For example, studies could investigate if equity shares and realized investment returns from financing deals are in line with model predictions. Second, model results can provide useful analytical guidance on the design of venture finance deals by relating the optimal equity division and expected investment return to a number of venture characteristics. Further, VC deals can include convertible features. Although this will involve some technical complexity in the extend framework (e.g., risk-averse financiers, modeling future venture value as a continuous function of a rich set of inputs), incorporating such option-like features into the model’s modeling framework with search (see (5 – 8) and (17)) can provide additional insights on the role of asymmetric risks and incentives.

Finally, although we do not explicitly explore implications for public policy in this paper, the model and its extensions can shed useful light in this direction. For example, the model shows that the positive impact of initial project value on financier expected returns and the negative impact of project risk are a source of disadvantage to investors with lower access to funding (e.g., angels) and higher risk aversion. Targeted subsidies, preferential tax treatment, and provision of partial insurance may further enhance financing opportunities in the entrepreneurial finance market for entrepreneurs with smaller and/or risker ventures.

Footnotes

The Entrepreneur’s Optimal Equity Stake

The best effort response of the entrepreneur (E) to the equity stake

This leads to the entrepreneur’s best effort response

Similarly, differentiating (7) with respect to

Next, to determine the optimal equity incentive share, the financier

The corresponding first-order condition is

Entrepreneur’s Equilibrium Search Contract

As noted earlier, the key to solving the entrepreneur’s equilibrium search contract

Equation (17) implicitly defines the critical level of risk aversion

The expected value of the equity deal offered to the entrepreneur

The expected value of the equity deal to the entrepreneur

The partial derivatives

This condition is easily satisfied because even if the financier is 10 times more productive than the entrepreneur (

To obtain a tractable result, we assume that financier types

The equilibrium search contract is given by using (B.3) in Proposition 1 leading to

Sensitivity of Entrepreneur’s Equity Stake

It is easy to show using (A.6) that the partial derivatives of the entrepreneur’s equity stake with respect to various model parameters as given below.

Sensitivities of Financier’s Expected Investment Return

The partial derivatives of the financier’s investment return (15) with respect to various –project–financier–entrepreneur characteristics are reported below (for complicated expressions, only the sign is reported; the complete expression is available from the authors).

Optimal Effort Sensitivities

Acknowledgment

The authors would like to thank the Editor, Professor Sophie Manigart, and two anonymous Reviewers for providing very detailed and useful comments on this research.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by a grant from the Canadian Social Science & Humanities Research Council (SSHRC).