Abstract

Angel investment research has grown rapidly; yet, when and under what conditions angel investors recommit remains understudied. Integrating escalation of commitment (EOC) theory with the conflict management styles (CMSs) perspective, we examine these conditions through archival data investigation, a conjoint experiment (2,368 decisions by 148 angel investors), and a field study (214 ventures by 112 angel investors). We show that prior commitment increases angel investors’ reinvestment likelihood, contingent on entrepreneurs’ CMSs. We advance EOC theory by identifying relational boundary conditions and conflict management research by theorizing its moderating role in reinvestment decision-making, revealing escalation as a socially embedded process shaped by investor–entrepreneur interactions.

Keywords

Introduction

Angel investors (hereafter angels) play a pivotal role in early-stage ventures by providing not only capital but also mentorship, networks, and strategic guidance that shape new venture trajectories (Maxwell et al., 2011; Wiltbank et al., 2009). While prior research has focused extensively on why angels make initial investments (Ferrati & Muffatto, 2021; Svetek, 2023; Warnick et al., 2018), much less is known about what drives their decisions to reinvest in or withdraw from the same venture. This literature gap is consequential because, in practice, entrepreneurs frequently rely on initial investors for follow-on capital, with such continued support often influencing subsequent financing and venture survival (Lefebvre et al., 2022). Without a clear understanding of angels’ reinvestment decisions, entrepreneurship research remains incomplete in explaining how early investor involvement shapes whether new ventures scale, stall, or dissolve.

Traditional rational models explain follow-on investment primarily as a function of venture performance (Nanda et al., 2020). However, empirical evidence suggests that performance alone is an insufficient factor (Lefebvre et al., 2022). As one experienced angel noted during the interview in a podcast, “ventures that are looking good today can look like they are going under just a few months later.” Early-stage performance is inherently uncertain and volatile, limiting its usefulness as a sole decision criterion (Bork, 2019). Consequently, angels’ reinvestment decisions are likely shaped not only by economic factors but also by psychological and relational influences (Lefebvre et al., 2022), which remain comparatively understudied. Accordingly, in this study, we ask the following question: When and under what conditions does prior commitment lead angels to reinvest in ventures they have already backed?

To address this question, we draw on escalation of commitment (EOC) theory, which posits that individuals tend to persist with prior decisions due to sunk costs, self-justification, and psychological ownership, even when objective indicators are ambiguous (Brockner, 1992; Staw, 1997). In angel investing, escalation captures the tendency to continue supporting previously funded ventures, distinguishing reinvestment from initial investment decisions (Whyte, 1993). Although escalation research has focused on failing projects, escalation mechanisms also operate in ongoing and ambiguous contexts (He & Mittal, 2007). Extending this logic, we argue that angels may escalate their commitment more or less depending on ambiguous, socially embedded reinvestment contexts shaped by the psychological and relational dynamics between the angel and entrepreneur.

Angels’ commitments extend beyond financial capital to include time, energy, and relational resources, which can foster psychological ownership and emotional attachment to the venture (Lin et al., 2022). Apart from the psychological force, angel investment is inherently relational. Following the initial investment, entrepreneurs and angels interact closely, exchange information, and jointly shape venture development (Huang & Knight, 2017). These interactions often involve disagreements and tensions (Collewaert, 2012; Tetteh et al., 2024); how such conflicts are managed can significantly influence relationship quality and continued support (De Clercq & Sapienza, 2006). Therefore, EOC is not purely an internal psychological process; rather, angels interpret their prior commitments through the lens of ongoing interpersonal interactions with entrepreneurs. Consequently, we propose that entrepreneurs’ conflict management styles (CMSs)—namely, cooperative, competitive, and avoidant CMSs—constitute critical relational cues that shape whether angels escalate or de-escalate their prior commitments.

To examine this framework, we draw on data from the Angel Investor Performance Project (AIPP) and conduct a conjoint experiment (Study 1) and a field study (Study 2) to assess how each style strengthens or weakens the relationship between prior commitment and reinvestment likelihood.

Our study makes three contributions. First, we advance EOC theory by identifying entrepreneurs’ CMSs as boundary conditions, demonstrating that escalation is not merely an isolated cognitive bias but a socially embedded process shaped by relational interactions. This contribution moves escalation theory beyond its traditional focus on internal justifications and situates it within the ongoing dynamics of investor–entrepreneur collaboration, thereby responding to calls for more socially grounded models of entrepreneurial decision-making (Shepherd, 2015). Second, we contribute to conflict management research. By examining the moderator role of CMS in the relationship between EOC and angel reinvestment, we expand the explanatory power of CMSs beyond their well-known main effects. Finally, we contribute empirically to angel investment research by shifting attention from initial investment decisions to reinvestment decisions. While prior studies have typically considered economic or relational factors in isolation (Lefebvre et al., 2022), we offer an integrated framework that explains reinvestment as the joint outcome of psychological commitment and relational dynamics.

Theoretical Background

EOC Theory

EOC refers to the tendency of decision-makers to allocate additional resources, either tangible (e.g. money) or intangible (e.g. time or effort), to a course of action in pursuit of goals anchored in their initial decisions or anticipated future success (Brockner, 1992; Staw, 1997). EOC theory explains why individuals persist with prior courses of action even when alternatives appear more favorable (Brockner, 1992). In practice, decision-makers frequently escalate commitment to avoid admitting that earlier investments of psychological, emotional, and physical resources were misallocated (Devigne et al., 2016). At its core, the theory highlights mechanisms such as sunk cost sensitivity, self-justification, ego protection, and identity entrapment (Sleesman et al., 2012), leading decision-makers to continue investing in suboptimal or ambiguous projects.

Contemporary research recognizes that escalation is shaped not only by cognitive mechanisms (Brockner, 1992) but also by interpersonal influences (Sleesman et al., 2018). What may appear as an intrapersonal bias can be socially reinforced through social validation, impression management, and relational commitment (Wong et al., 2008). Individuals may persist (i.e. continue in a venture) not only to justify prior decisions but also to maintain legitimacy and trust within their social environment (Drummond, 2014). These insights highlight the need to specify boundary conditions under which escalation occurs (Sleesman et al., 2018). This is particularly relevant in angel investing, where reinvestment decisions are made under uncertainty and within ongoing relationships. How to manage the relationship and deal with the conflicts that arise in it is thus becoming crucial.

Conflict Management Styles

Conflict generally refers to “perceived incompatibilities or discrepant views among the parties involved” (Jehn & Bendersky, 2003, p. 189). Scholars show that despite investors’ efforts, between 35% and 55% of investor-backed firms still fail. One of the key factors of such failures is personal friction between entrepreneurs and investors (Zacharakis & Meyer, 2000), which can trigger investors’ exit intention (Collewaert, 2012), weaken investor–investee relationships (Collewaert & Sapienza, 2016), and affect venture performance (Higashide & Birley, 2002). It may also impede reinvestment intentions (Tetteh et al., 2024). Importantly, conflict is not inherently detrimental (Higashide & Birley, 2002); it can be functional (Tetteh et al., 2024) or dysfunctional (De Dreu, 2006; Tetteh et al., 2024), depending on how it is managed (Tetteh et al., 2024).

We conceptualize entrepreneurs’ CMSs as the behavioral approaches used to handle disagreements with investors. Investors often base decisions on observable indicators linked to venture prospects (Mason & Harrison, 1996; Mitteness et al., 2012), but post-investment conflict can hinder venture development when poorly managed (Higashide & Birley, 2002). We therefore expect that angels are likely to consider how entrepreneurs handle disagreements when evaluating reinvestment decisions. Effective conflict management can enhance coordination, creativity, and decision quality (Todorova et al., 2020), whereas ineffective handling may reduce angels’ confidence and undermine continued support (Lee et al., 2022).

Following Tjosvold (1998), we classify entrepreneurs’ CMSs into three dimensions: cooperation, competition, and avoidance. Cooperative styles emphasize open communication, collaboration, and mutual goals (Tjosvold et al., 2014; Yin et al., 2020). Competitive styles prioritize self-interest and adopt a win–lose orientation (Chen et al., 2005; Tjosvold et al., 2014). Avoidant styles involve evasion and reluctance to confront disagreements (Chen et al., 2005; Tjosvold, 1998). These styles are distinct rather than sitting on a continuum. For instance, low cooperation does not imply high competitiveness (Tjosvold et al., 2006; Yin et al., 2020).

Prominent Role of CMSs in the Study Context

In China, where our data are drawn from, these dynamics are shaped by guanxi—a culturally embedded system of social relationships and reciprocal obligations that underpins business exchange (Batjargal et al., 2019; Batjargal & Liu, 2004; Chen et al., 2013). Within this context, conflict management carries relational meaning beyond instrumental disagreement: it signals social competence, respect, and commitment to relationship maintenance (Tjosvold et al., 2014; Yin et al., 2020). Therefore, Chinese angels are motivated not only by financial returns but also by non-financial rewards, including personal fulfillment, support for nascent ventures, and the cultivation of enduring relationships with entrepreneurs (Li et al., 2014). Consequently, entrepreneurs’ CMSs serve as an interpretive lens through which angels evaluate whether prior commitments are psychologically reaffirmed or relationally questioned.

Management research in China consistently emphasizes the importance of CMSs in influencing organizational and entrepreneurial outcomes. Studies show that CMSs play a key role in shaping team effectiveness, leadership coordination, and organizational innovation (Chen et al., 2005; Zhang et al., 2011). At the team level, CMSs shape team perceptions, relational dynamics, and overall effectiveness, influencing how teams handle both task and relationship conflicts (Tetteh et al., 2024; Tjosvold et al., 2006). Additionally, effective conflict management supports knowledge sharing, trust building, and stronger partnerships in Chinese organizations (Chen et al., 2005; A. Wong et al., 2005). This literature demonstrates the central role of CMSs in managing inevitable workplace disagreements in our study context.

Integration of CMSs and EOC in Angel Investment

As discussed earlier, EOC does not operate in isolation. In angel investing, persistence unfolds within ongoing interactions characterized by shared uncertainty and interdependence (De Clercq & Sapienza, 2006; Wiltbank et al., 2009). Therefore, reinvestment decisions are influenced not only by an internal desire to justify prior investments but also by relational cues signaling whether continued collaboration remains viable.

Prior research suggests that angel investment decisions reflect both psychological and relational factors (Ferrati & Muffatto, 2021; Lefebvre et al., 2022). Our systematic literature review shows similar patterns. While we found only 13 papers addressing angels’ post-investment behavior (see Supplemental Appendix A), 2 patterns emerged. First, studies directly examining angels’ reinvestment decisions remain scarce. In particular, the psychological reasons for reinvesting in originally funded ventures remain inadequately understood. Second, although some work has emphasized relational dynamics (e.g. trust, involvement), it provides a limited empirical and theoretical explanation of how such dynamics go beyond venture performance to aid or hinder consequential follow-on investment (Lefebvre et al., 2022). Together, this evidence suggests that given the same economic potential of a new venture, a reinvestment decision cannot be fully explained by psychological factors or relational forces alone but likely reflects their joint influence.

We propose that entrepreneurs’ CMSs provide a critical relational mechanism linking these domains (Afzalur Rahim, 2002; Chen et al., 2005). Because conflicts are inevitable during venture development, how entrepreneurs handle disagreement signals the quality and sustainability of the relationship (Collewaert, 2012). These signals shape how angels interpret their prior investment commitments and determine whether escalation tendencies are reinforced or attenuated. Specifically, some CMSs reinforce the translation of commitment into reinvestment by validating both economic and relational logic, whereas others disrupt this process by introducing relational strains. Accordingly, we conceptualize entrepreneurs’ CMSs as relational boundary conditions that shape how escalation unfolds: escalation is not solely an intrapsychic bias but a socially embedded process contingent on conflict management within the investor–entrepreneur dyad.

Hypothesis Development

Angels and EOC

As major providers of early-stage risk capital (Wiltbank et al., 2009), angels often adopt a “hands-on” posture, contributing experience, knowledge, and contacts while maintaining advisory engagement and exercising ex post control rights (Avdeitchikova et al., 2008; Paul et al., 2007). Such sustained involvement can foster psychological attachment and ownership, increasing the likelihood of prior commitments shaping follow-on decisions (Hogrebe & Lutz, 2024). Angels make both monetary (i.e. money invested) and non-monetary (e.g. time and effort) commitments (Lin et al., 2022). Once invested, these resources become sunk costs that can trigger escalation tendencies (Sleesman et al., 2018). Monetary commitments may motivate reinvestment to protect self-image and avoid reputational loss associated with being perceived as an ineffective investor (Sleesman et al., 2012). Non-monetary commitments can deepen psychological ownership by generating firm- and market-specific information and increasing perceived fit and control (Wiltbank et al., 2009). Together, these mechanisms increase the psychological cost of exit and make persistence more attractive under uncertainty.

In early-stage settings, where performance signals are often noisy, delayed, or ambiguous, and decision-making relies heavily on interpretive cues (Wiltbank et al., 2009), angels’ current commitment (i.e. time, energy, and money invested) becomes a powerful psychological anchor. These dynamics may be particularly salient in relationally embedded contexts such as China, where guanxi norms emphasize reciprocity, continuity, and the maintenance of “face” (Batjargal & Liu, 2004; Xiao & Anderson, 2022). Because investment relationships carry both financial and relational meaning in such environments, disengaging from a venture may signal not only economic withdrawal but also relational distancing (or even dissolution). Consequently, angels may be more inclined to persist with ventures they have previously supported, regardless of whether objective performance clearly merits it (Devigne et al., 2016; Hogrebe & Lutz, 2024). Therefore, we propose the following baseline hypothesis:

Moderating Effect of Cooperative CMS

The cooperative style is characterized by open communication, collaboration, and mutual-goal orientation (Tjosvold et al., 2006, 2014; Yin et al., 2020). In investor–entrepreneur relationships, cooperative conflict handling signals responsiveness, respect, and a willingness to engage in joint problem solving, thereby reinforcing relational trust and psychological safety (De Clercq & Sapienza, 2006). From an escalation perspective, the cooperative style provides validating social feedback that supports self-justification. When entrepreneurs handle disagreements constructively, angels are more likely to interpret their prior commitment as both economically reasonable and relationally sound. This relational validation strengthens the translation of commitment into persistence (Brockner, 1992; Sleesman et al., 2012).

This effect should be particularly strong in a relationally embedded environment such as China, where business exchange is structured by guanxi norms (Batjargal & Liu, 2004; Chen et al., 2013; Li et al., 2014). In this context, an entrepreneur’s cooperative style is more than an interpersonal preference; it is a relational signal of competence in sustaining long-term exchange through tactful and respectful engagement during disagreement (Farh et al., 1998; Yin et al., 2020). Consistent with EOC, individuals persist in prior investments due to self-justification and identity-consistency motives (Brockner, 1992; Sleesman et al., 2012). However, in guanxi-oriented systems, these psychological mechanisms are intertwined with relational considerations, where continued involvement signals relational credibility and adherence to norms of reciprocity (Batjargal & Liu, 2004; Chen et al., 2013).

When entrepreneurs manage conflict cooperatively, they affirm both the economic rationale of investors’ initial commitment and its relational appropriateness. Cooperative conflict management can transform disagreements into evidence of relational strength rather than relational strain. By preserving harmony, demonstrating responsiveness, and maintaining face, entrepreneurs sustain investor trust and emotional attachment (Luo, 1997; Chen et al., 2013). This relational reassurance supports the cognitive reinforcement underlying escalation, allowing angels to justify persistence without experiencing relational dissonance. By contrast, when cooperative cues are absent, relational affirmation weakens, making it more difficult for prior commitment to translate into continued engagement. Accordingly, we propose the following hypothesis:

Moderating Effect of Competitive CMS

The competitive style reflects an assertive and self-oriented approach in which individuals prioritize their own goals and frame disagreements as win–lose contests (Tjosvold et al., 2006; Yin et al., 2020). In investor–entrepreneur relationships, persistent competitive behavior, such as dominating discussions, resisting feedback, and publicly challenging investors, signals relational tension and reduces psychological safety (Zhang et al., 2011). It may also signal low emotional intelligence, rigidity, and power imbalance, thereby weakening investor confidence and undermining perceptions of the entrepreneur as a reliable long-term partner (Zou et al., 2016).

In guanxi-oriented contexts such as China (Chen et al., 2013; Luo, 1997), competitive CMS carries implications beyond strategic disagreement. Behaviors that challenge authority or disrupt norms of relational deference and face are therefore interpreted as relational disrespect rather than constructive assertiveness, as argued in Western settings (Chen et al., 2013; Farh et al., 1998; Hwang, 1987; Luo, 1997). This disruption weakens the relational foundation underlying continued collaboration. Thus, the psychological mechanisms sustaining escalation, particularly self-justification, become harder to maintain, as prior commitment can no longer be easily framed as consistent and appropriate (Brockner, 1992).

Moreover, because guanxi relationships are embedded in broader social networks, conflict behaviors may carry reputational risks beyond the focal dyad (Chen et al., 2005; Luo, 1997; Tjosvold et al., 2006). These relational and network-level concerns increase the perceived costs of involvement (Li et al., 2014; Wang et al., 2016), attenuating the cognitive and affective forces that sustain escalation. Consequently, competitive conflict management introduces relational dissonance, making it harder for angels to frame their earlier investment as sound. Instead of reinforcing commitment, it may prompt reassessment by signaling a potential relational misjudgment (e.g. “I trusted someone who does not respect harmony”). Therefore, we test the following hypothesis:

Moderating Effect of Avoidant CMS

The avoidant style reflects a tendency to withdraw from or deflect disagreement rather than address it directly (Yin et al., 2020; Zou et al., 2016). Entrepreneurs adopting this style may delay discussion, sidestep contentious issues, or maintain surface-level harmony without resolving underlying tensions (Chen et al., 2005). Although such behavior can appear to preserve relational peace, it often generates relational ambiguity by leaving disagreements unarticulated and communication opaque. This ambiguity limits the relational cues investors rely on to assess responsiveness, accountability, and collaborative intent (Lefebvre et al., 2022).

In guanxi-oriented systems, avoidance carries relational implications beyond simple conflict preferences. Because these relationships depend on ongoing reciprocity, emotional exchange, and sustained relational attentiveness (Chen et al., 2013), withdrawal during disagreement may signal reduced commitment to maintaining mutual obligations (Chen et al., 2013; Farh et al., 1998). Thus, avoidance is not interpreted as neutrality but as relational distancing, signaling a reduced willingness to invest relationally in the partnership (Batjargal & Liu, 2004; Li et al., 2014).

This interpretation undermines escalation by removing the relational reinforcement needed to justify continued commitment. In guanxi-oriented investment contexts, ongoing engagement and responsiveness provide reassurance that prior commitment remains relationally legitimate (Batjargal & Liu, 2004; Chen et al., 2013). When entrepreneurs avoid addressing tensions, angels lose the relational visibility needed to interpret continued involvement as reciprocated and respected. The absence of open dialogue increases ambiguity about the entrepreneurs’ intentions and reliability (Chen et al., 2005), weakening the cognitive basis for persistence. Consequently, angels become more cautious and less inclined to rely on escalation-based reasoning (Wong et al., 2008). Therefore, the avoidant style does not directly contradict prior commitment; rather, it removes the relational scaffolding that makes continued investment psychologically and socially defensible. Accordingly, we propose the following hypothesis:

To examine our baseline and three hypotheses, we conduct three complementary studies: archival data investigation (preliminary study), a conjoint experiment (Study 1), and a field study (Study 2). The preliminary study informs the baseline assumption and guides the design of subsequent studies, while Studies 1 and 2 test the conditions outlined in Hypotheses 1 to 3, providing both internal and external validity of empirical findings. This multi-method approach enables the triangulation of empirical findings and assessment of their robustness.

Preliminary Study

Method

We begin with a preliminary study using data from the AIPP (Wiltbank & Boeker, 2007a; see Supplemental Appendix B) to assess whether EOC applies to angel reinvestment decisions. Given the limitations of archival data, particularly the absence of direct measures for some constructs, this analysis is exploratory but informs the design of subsequent hypothesis testing studies.

Dataset and Sample

The AIPP data include 1,137 exits and closures from 3,097 investments made by 539 accredited angels. It reports angels’ pre- and post-investment strategies, deal-level variables, and angel-level characteristics (Wiltbank & Boeker, 2007b), as well as non-monetary engagement indicators such as due diligence hours and interaction frequency. After excluding observations with missing focal variables, the final sample comprises 661 reinvestment decisions. Angels in the sample are predominantly later-career individuals (mean age = 56 years, range: 30–81), typically hold a master’s degree, and possess substantial entrepreneurial experience (on average, 3 ventures and 14 years). They have, on average, 11 years of investment experience and 16 angel deals, allocating approximately 13% of their wealth to angel investing; 22% of deals have received follow-on funding. Consistent with prior research, angels are actively involved: 26% interacted daily or weekly, and 48% on a monthly or quarterly basis (Mason & Harrison, 2002).

Measures

The dependent variable captures the angels’ reinvestment, measured as a binary indicator of whether an angel reinvested in the same firm. Independent variables capture monetary and non-monetary commitment. Monetary commitment is measured by the initial investment amount, while non-monetary commitment is proxied by interaction frequency, coded as follows: 1 = rare (annual or less), 2 = moderate (monthly/quarterly), 3 = frequent (daily/weekly). Following prior research (Sleesman et al., 2012), we control for angel age, the share of personal wealth allocated to angel investments, and venture performance proxied by revenue at the time of initial investment. CMS data are unavailable.

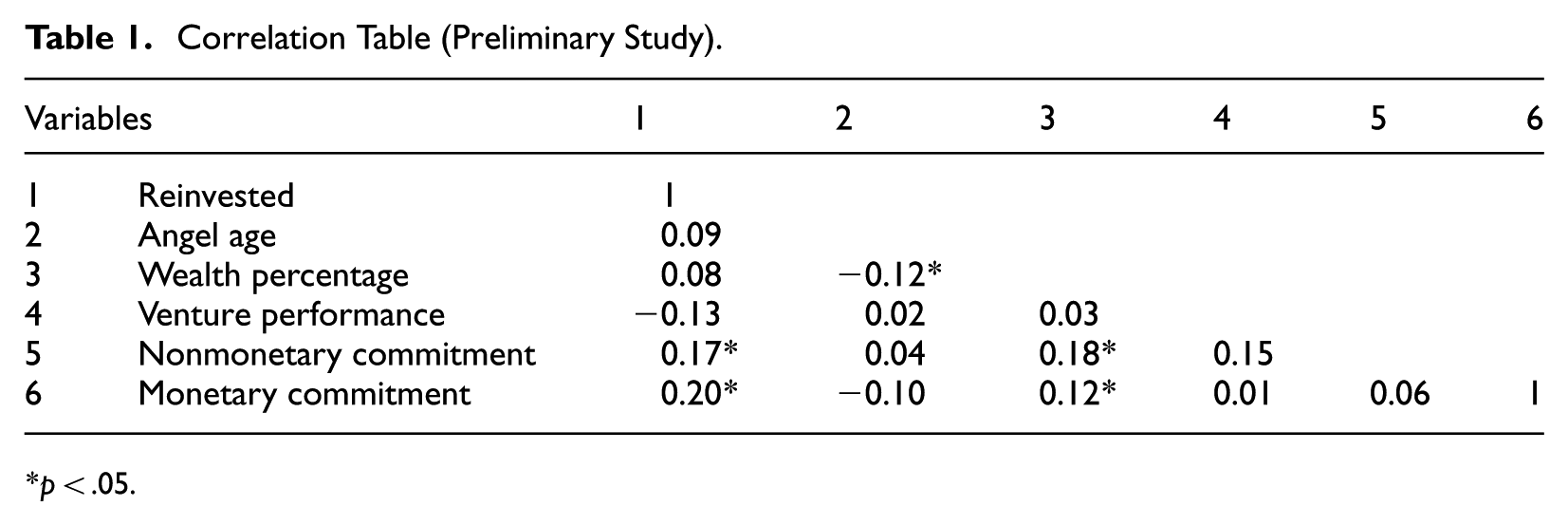

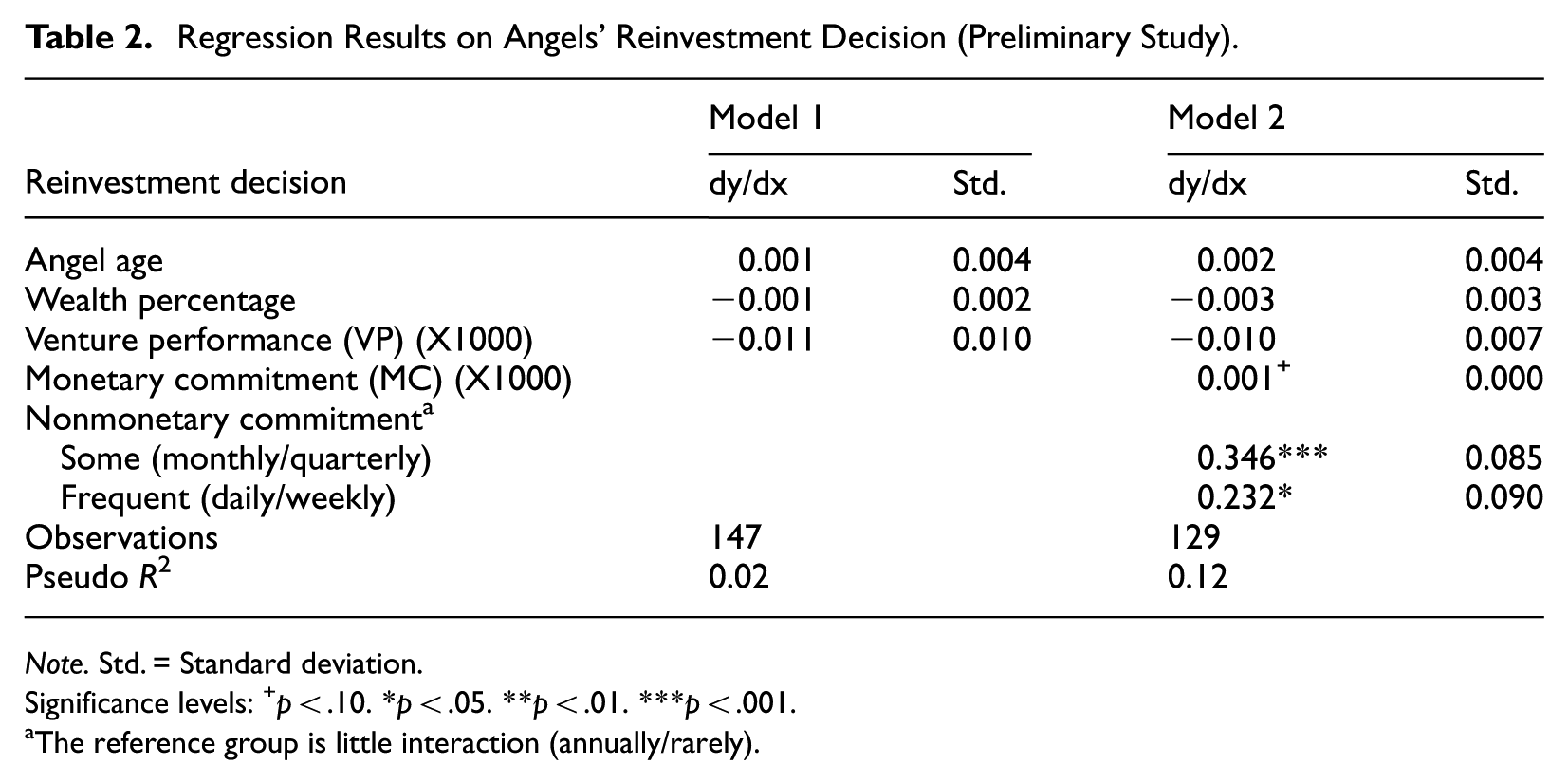

Analysis and Results

We employ binary logistic regression and report average marginal effects for interpretability (Ganter & Hecker, 2013). Table 1 shows that correlations are below 0.5, indicating no multicollinearity concerns. As seen in Table 2, monetary investment shows a marginal effect on reinvestment (p < .10), whereas non-monetary commitment strongly predicts reinvestment. Frequent interaction strongly predicts reinvestment: monthly/quarterly (dy/dx = 0.346, p < .001) and daily/weekly (dy/dx = 0.232, p < .05) relative to rare interaction. Overall, the results support the premise that prior financial and time commitments drive escalation, with non-monetary commitment exerting the strongest effect.

Correlation Table (Preliminary Study).

p < .05.

Regression Results on Angels’ Reinvestment Decision (Preliminary Study).

Note. Std. = Standard deviation.

Significance levels: +p < .10. *p < .05. **p < .01. ***p < .001.

The reference group is little interaction (annually/rarely).

Study 1: Conjoint Experiment

Method

Building on the preliminary study, which provides initial evidence of escalation in reinvestment decisions, Study 1 employs a conjoint experiment to identify the boundary conditions of EOC, focusing on the entrepreneurs’ CMSs. The experiment design isolates decision attributes and minimizes contextual confounds, allowing us to examine angels’ underlying decision-making processes. Conducting the study in China also extends and reveals other escalation mechanisms beyond the Western institutional context.

Background of the Angel Investment Industry in China

Although angel investing emerged relatively late in China, it has expanded rapidly since the 2000s, supported by policy incentives, digital platforms, and entrepreneurial networks (Wang et al., 2016). Activitiy was negligible in the late 1990s—for instance, major firms such as Tencent and Alibaba had to raise seed capital abroad, as no domestic early-stage investors would support them (Chen, 2022; Clark, 2016). Institutionalization began around 2009, with the number of active angels in the Zhongguancun Demonstration Zone growing by more than 60%, reaching approximately 200 and with 33 angel funds established there by 2012 (Liu et al., 2015). With formal recognition under the “Mass Entrepreneurship and Innovation” initiative launched in 2014, the market entered a period of explosive growth. China angel institutions completed 766 disclosed deals in 2014, a 353% year-on-year (YoY) increase, with disclosed investment exceeding US$526 million. In the same year, 39 new professional angel funds were launched, raising US$1.07 billion, doubling the 2013 total (Zero2ipo Research, 2015). By 2015, the aggregated Chinese risk capital pool reached CNY15 trillion (including a CNY2.2 trillion government-backed pool), and the number of risk capital firms actively investing in new and young firms reached 10,000, overtaking the United States and making China the world’s largest private-equity market (Xiao & Anderson, 2022; Zero2ipo Research, 2020). This trajectory from negligible activity to a multi-billion dollar market with thousands of annual deals underscores the central role of angel investing in China’s entrepreneurial finance system (Wang et al., 2016).

Despite this expansion, the market remains cyclical and sensitive to institutional and macroeconomic conditions. Annual angel investment peaked and crossed the RMB10 billion threshold in 2015 to 2016 (Zero2ipo Research, 2016), followed by contractions across several dimensions. ITJuzi (2024) data show that the number of newly established Chinese angel institutions has declined every year since 2017, falling to single digits in 2022 and 2023. Angel-round financing volume fell by 17.3% YoY in 2022 (Zero2ipo Research, 2024). In the first half of 2023, combined seed- and angel-round deal counts dropped to 724 (−24% YoY), whereas their share of all equity deals rose to 19%, which reflect a deliberate “invest early, invest small” pivot by Chinese liability partners (LPs) and general partners (GPs) (KPMG China, 2023). Even under these tightened conditions, the market continues to generate approximately 3,000 to 3,300 angel/seed deals per year (Li & Ban, 2026), particularly following policy support in the early 2010s (Anh et al., 2023). Supplemental Appendix C provides further information on Chinese angel investment deal characteristics.

Angel investment activity also exhibits strong regional concentration. From 2008 to 2013, approximately 79% of angel-backed ventures were located in just five provinces—namely, Beijing, Shanghai, Guangzhou, Zhejiang, and Jiangsu—which together absorbed 87% of the total value of angel investment (Liu et al., 2015). Sectorally, investments are heavily concentrated in technology, media, and telecommunications, alongside growing activity in healthcare and advanced manufacturing (Cumming & Zhang, 2019; Wang et al., 2016). From 2008 to 2013, internet, telecommunications, and information technology (IT) together absorbed 72% of angel investment value (Liu et al., 2015). Since 2020, capital has rotated sharply toward “hard tech” such as semiconductors, artificial intelligence, new energy, advanced manufacturing, and biotech, with semiconductors alone capturing 67% of IT-sector private equity (PE)/venture capital (VC) investment in H1 2023 (KPMG China, 2023). Supplemental Appendix C provides the detailed statistics.

A key distinction from the Western context is the prominence of guanxi, which shapes deal sourcing, monitoring, and post-investment involvement (Batjargal & Liu, 2004; Chen et al., 2013; Li et al., 2014). Therefore, investment decisions carry strong relational meaning (Li et al., 2014), making the management of interactions and disagreements (e.g. CMS) particularly consequential. At the same time, conflicts remain prevalent (Tetteh et al., 2024; Xiao & Anderson, 2022), making China a suitable context to examine how CMS shapes the translation of prior commitment into reinvestment decisions.

Sample and Data Collection

We recruited participants through a platform company in Hangzhou, Zhejiang Province, that connects entrepreneurs and investors. The platform has ties to investors involved in unicorn ventures such as Alibaba Cloud, Cainiao Network, and Caocao. To ensure appropriate sampling, angels were defined as external individual investors who invest some of their personal wealth in unlisted companies in exchange for shares and remain actively involved after investment (Collewaert, 2012). Similar to other entrepreneurship studies (Fu & Tietz, 2019), participants were contacted via WeChat, a commonly used platform for business communication in China.

We reached out to 575 participants and received 148 valid responses (response rate = 25.7%). Each participant completed 16 decisions, yielding 2,368 (16 × 148) observations for final analysis. The number of observations is comparable to or exceeds other conjoint experiments on angels’ decision-making (Svetek, 2023; Warnick et al., 2018).

Our respondents included 35 female and 113 male experienced investors (mean age = 44.65 years; range: 33–61). All respondents held at least a bachelor’s degree and possessed entrepreneurial experience. All participants indicated that they had completed at least one portfolio investment. Furthermore, the respondents’ investment experience ranged from 5 to 26 years (mean = 14.06), and all respondents had made at least one investment in the past 12 months. Finally, the minimum investment per deal exceeded US $10,000. These characteristics are consistent with prior research (Hsu et al., 2014), supporting sample validity. The experimental instrument was initially written in English; thus, we followed the commonly used back-translation procedure (Brislin, 1980; Fu & Tietz, 2019) to ensure accuracy when translating it into Chinese.

Conjoint Experiment

The conjoint experiment approach is vital for investigating investors’ investment decisions (Svetek, 2023; Warnick et al., 2018). Prior studies show that such an approach “can predict the real behavior of real individuals in real situations” (Louviere, 1988, p. 114). Additional benefits of the conjoint experiment include its potential to clarify trade-offs among decision factors (Monsen et al., 2010) and its ability to avoid retrospective and outcome biases in real-time decision-making (Mathias & Williams, 2017).

Experimental Instrument

Before data collection, we interviewed 13 angels to validate attribute definitions and ensure face validity and clarity. Based on their feedback, we refined the survey item language and instrument flow.

We followed established studies (Svetek, 2023; Warnick et al., 2018) to design a baseline investment condition constant across all experimental scenarios (Supplemental Appendix D). Participants were asked to evaluate several hypothetical profiles and were given definitions of the “low” and “high” conditions for the attribute associated with each profile (Supplemental Appendix E). To reduce respondent fatigue (Reibstein et al., 1988), we employed a fractional factorial design (Simarasl et al., 2020; Warnick et al., 2018), resulting in 16 profiles while preserving orthogonality and enabling interaction tests.

Participants also completed one practice profile (excluded from analyses) and three repeated profiles to assess test–retest reliability (Drover et al., 2014). Profile and attribute order were randomized to minimize order effects (Chrzan, 1994). Each profile was presented on a separate screen, and responses could not be revised. Attribute definitions were accessible via mouse-over functions (Warnick et al., 2018). Sample profiles are presented in Supplemental Appendix F.

Measures

Dependent Variable

The dependent variable is “reinvestment likelihood.” Similar to other conjoint studies (Warnick et al., 2018), after each profile, the participants were asked to indicate their likelihood of reinvesting on a seven-point Likert scale (1: Least likely to 7: Most likely).

Conjoint Attributes

Each reinvestment scenario includes five attributes—four focal attributes and one control: (a) current commitment, (b) cooperative style, (c) competitive style, (d) avoidant style, and (e) venture performance (control). These variables were manipulated at two levels (high vs. low) each. Following prior work (Warnick et al., 2018), we effect-coded all attributes as −0.5 (low) and 0.5 (high), yielding zero-mean predictors.

Post-Experiment Control Variables

Prior research indicates that investors’ experience is crucial when evaluating investment deals (Murnieks et al., 2016; Warnick et al., 2018). Thus, our post-experiment questionnaire captured angels’ experience-related information. Specifically, participants’ years of investing experience in ventures and their entrepreneurial experience (i.e. the number of ventures founded) were captured. We also controlled for demographic variables, such as participants’ age, gender, and education level, which potentially influence investment decisions (Svetek, 2023).

Analysis and Results

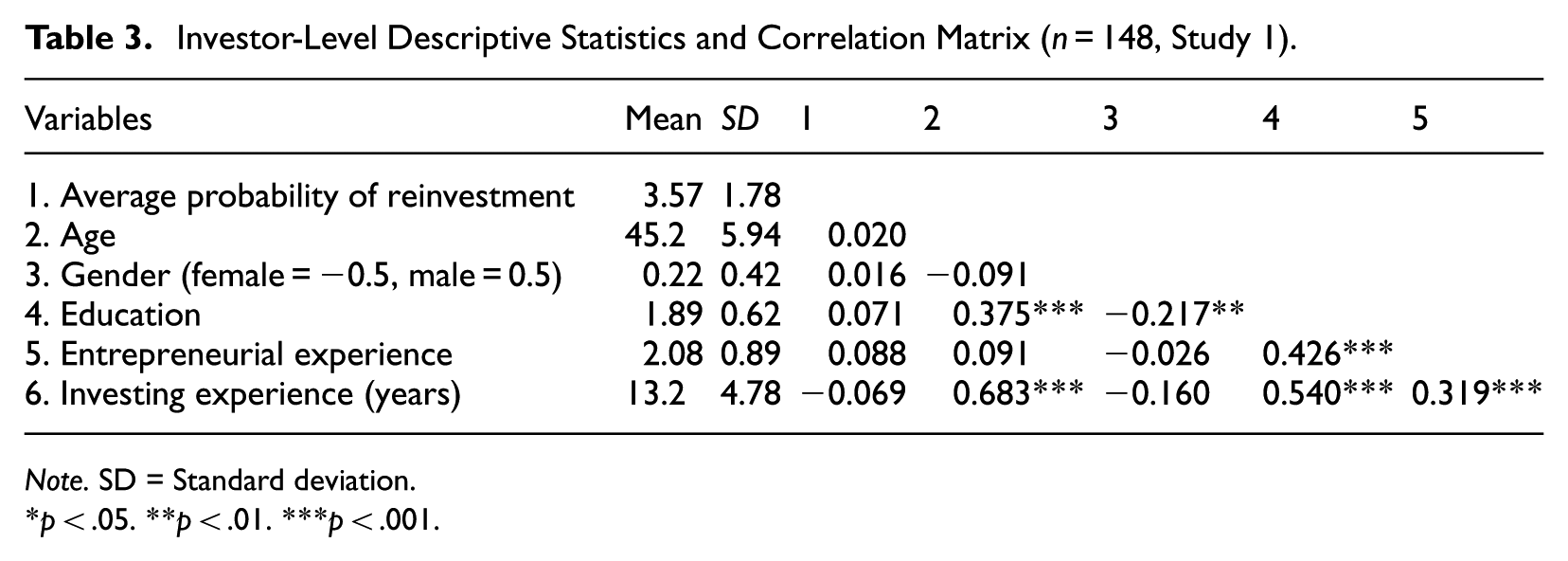

Table 3 outlines the descriptive statistics for the demographic variables. We checked the response reliability prior to data analysis. Each respondent’s decisions had good test–retest reliability, with a mean test–retest correlation of 0.94 and no significant differences between original and repeated conjoint profiles.

Investor-Level Descriptive Statistics and Correlation Matrix (n = 148, Study 1).

Note. SD = Standard deviation.

p < .05. **p < .01. ***p < .001.

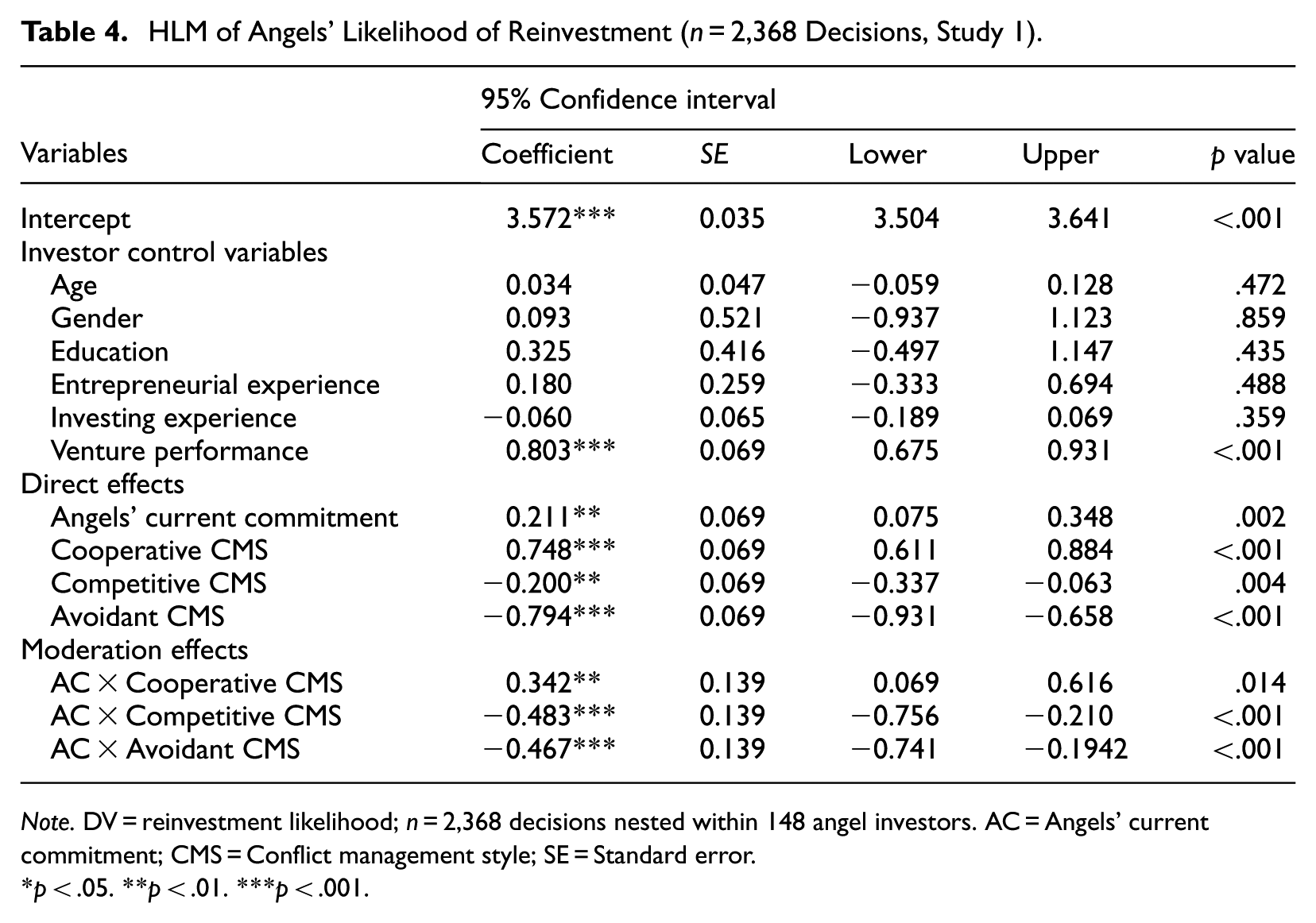

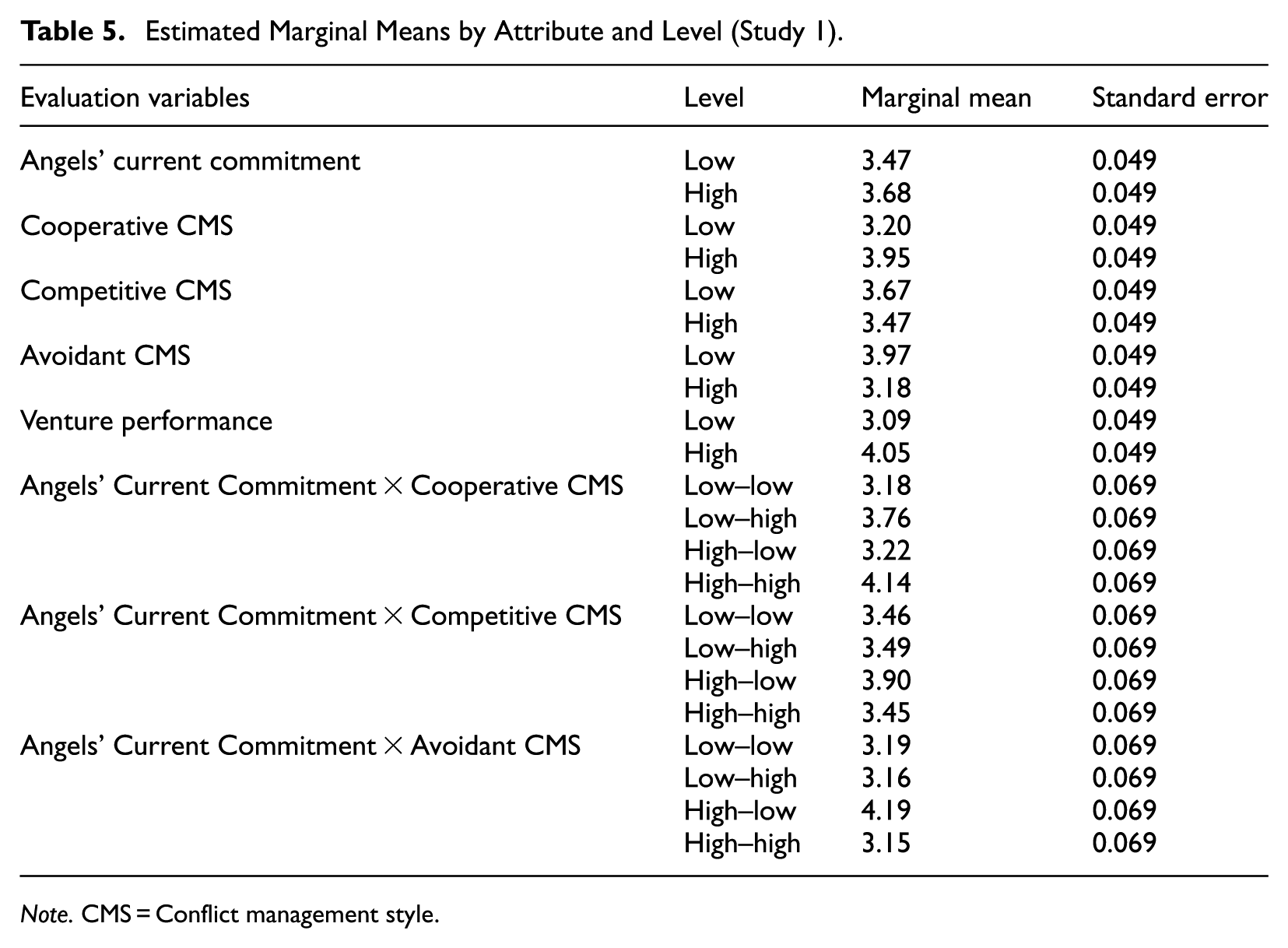

Hypotheses are tested using hierarchical linear modeling (Hofmann et al., 2000). Table 4 shows that angels’ current commitment, such as time, effort, and money, positively impacts their reinvestment likelihood (β = .211, p < .01). This supports our baseline hypothesis.

HLM of Angels’ Likelihood of Reinvestment (n = 2,368 Decisions, Study 1).

Note. DV = reinvestment likelihood; n = 2,368 decisions nested within 148 angel investors. AC = Angels’ current commitment; CMS = Conflict management style; SE = Standard error.

p < .05. **p < .01. ***p < .001.

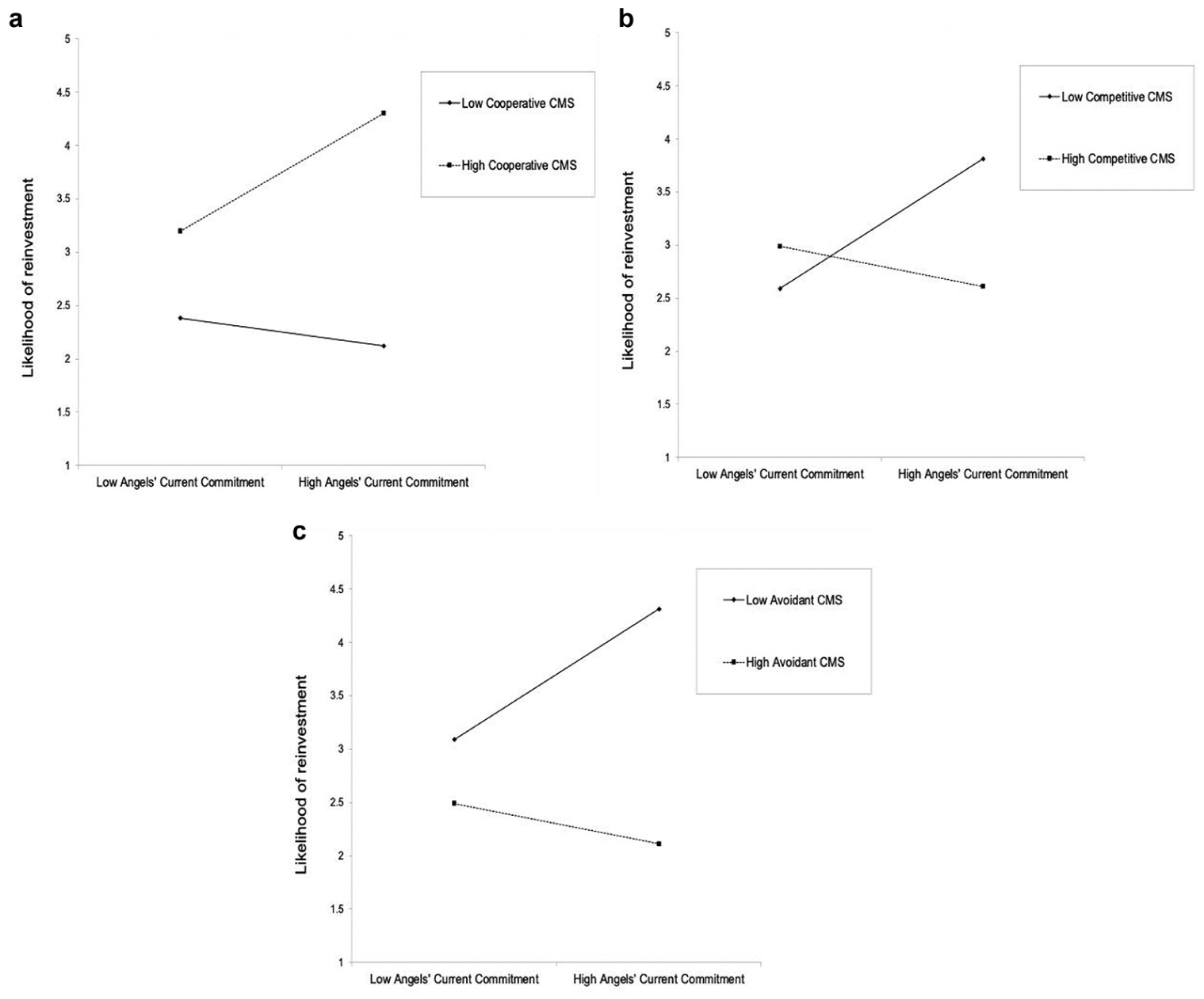

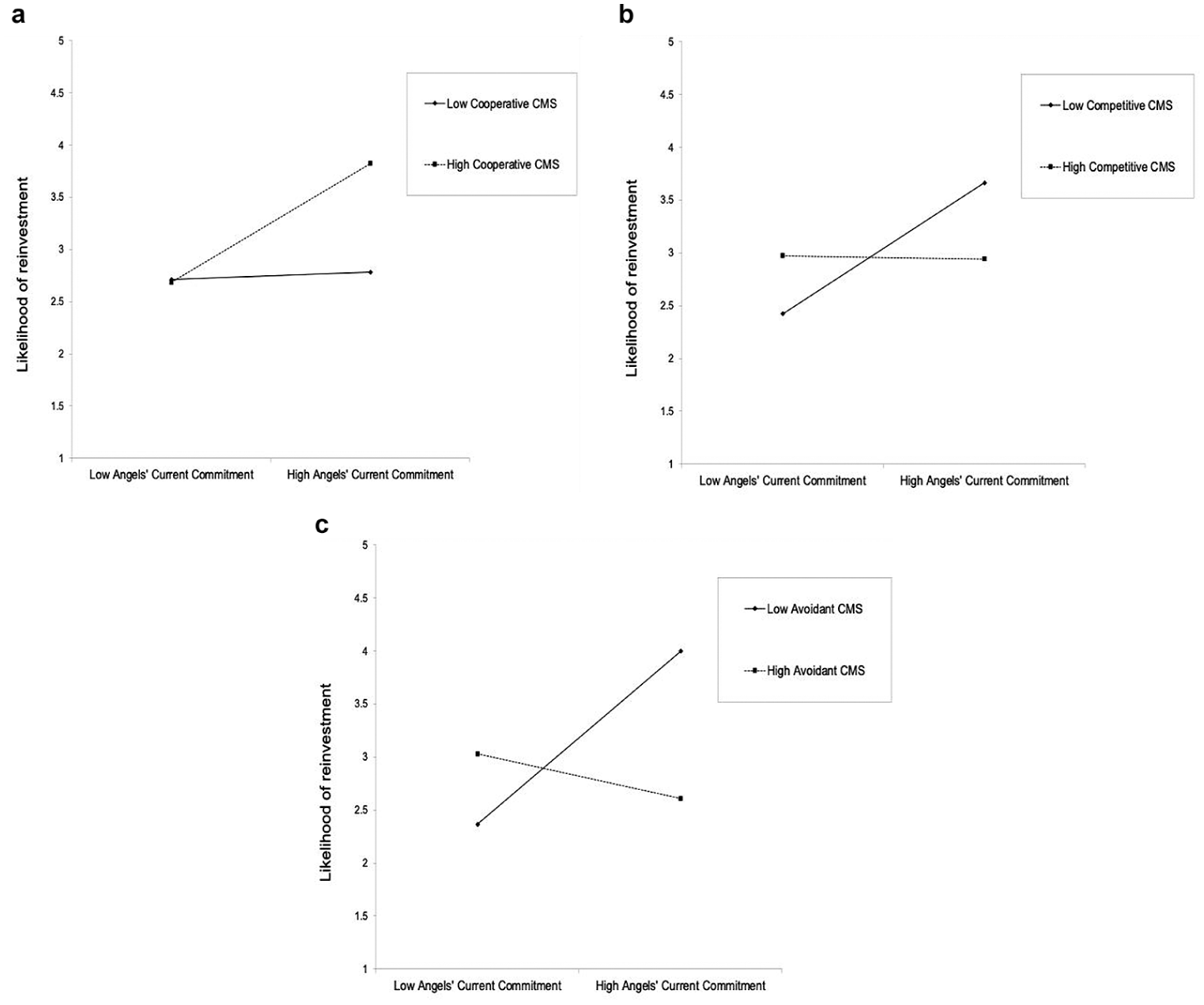

Hypothesis 1 suggests that angels’ EOC is contingent on their perception of entrepreneurs’ cooperative style. Table 4 shows that the interaction between the angel’s current commitment and the entrepreneur’s cooperative style is statistically significant and positive (β = .342, p < .01). Simple slope analysis (Figure 1a) shows that angels’ EOC on reinvestment likelihood increases at high (+1 Standard deviation [SD]; β = .382, p < .001) than at low (−1 SD; β = .040, p = .685) levels of entrepreneurs’ cooperative style. Marginal means (M) in Table 5 further support this hypothesis. Angels’ EOC to reinvest is higher when they perceive their current commitment to the firm as high and the entrepreneurs’ cooperative style as high (M = 4.14). However, angels’ EOC to reinvest is lower when they perceive their current commitment as high but the entrepreneurs’ cooperative style as low (M = 3.22). These findings provide strong support for Hypothesis 1.

Interaction between angels’ current commitment and entrepreneurs’ CMSs (study 1): (a) between angels’ current commitment and entrepreneurs’ cooperative CMS, (b) between angels’ current commitment and entrepreneurs’ competitive CMS, and (c) between angels’ current commitment and entrepreneurs’ avoidant CMS.

Estimated Marginal Means by Attribute and Level (Study 1).

Note. CMS = Conflict management style.

Hypothesis 2 suggests that angels’ EOC to reinvest in firms they initially funded is weaker when the entrepreneurs’ competitive style is high. Table 4 shows that the interaction effect between angels’ current commitment and entrepreneurs’ competitive style is negative and significant (β = −.483, p < .001). Simple slope analysis (Figure 1b) shows that angels’ EOC on reinvestment likelihood decreases at high (+1 SD; β = −.030, p = .758) than at low (−1 SD; β = .453, p < .001) levels of entrepreneurs’ competitive style. The estimated marginal mean (M) in Table 5 further confirms that angels report high reinvestment likelihood when they perceive their current commitment as high and the entrepreneurs’ competitive style as low (M = 3.90), compared with when both angels’ commitment and the entrepreneurs’ competitive style are perceived to be high (M = 3.45). These findings support Hypothesis 2. Interestingly, Table 5 also shows that when angels’ commitment is low, angels report high reinvestment likelihood when entrepreneurs’ competitive style is high (M = 3.49) compared with when it is low (M = 3.46).

Finally, Hypothesis 3 suggests that angels’ EOC to reinvest will be weaker when the entrepreneurs’ avoidant style is high. Table 4 shows that the interaction effect between angels’ current commitment and entrepreneurs’ avoidant style is negative and statistically significant (β = −.467, p < .001). Simple slope analysis (Figure 1c) shows that angels’ EOC on reinvestment likelihood decreases under conditions of high (+1 SD) levels of entrepreneurs’ avoidant CMS (β = −.023, p = .819) than low (−1 SD) levels of avoidance (β = .445, p < .001). The estimated marginal means in Table 5 further support this hypothesis. Angels’ EOC to reinvest is lower when they perceive their current commitment to the firm as high and the entrepreneur’s avoidant style as high (M = 3.15). However, they are more likely to escalate commitment to reinvest when they perceive their current commitment to the firm as high and the entrepreneur’s avoidant style as low (M = 4.19). These findings provide strong support for Hypothesis 3.

Study 2: Field Study

Method

As conjoint experiments rely on hypothetical scenarios, concerns may arise regarding their external validity—a general concern for all conjoint experiments (Lohrke et al., 2010). To address this limitation and strengthen confidence in our findings, in Study 2, we conducted a field study. This design enabled direct measurement of angels’ actual monetary and non-monetary prior commitments, their perceptions of entrepreneurs’ CMS, and their effects on reinvestment likelihood. By integrating archival, experimental, and field evidence, we provide a more comprehensive and externally valid account of reinvestment decision-making (Davis et al., 2011).

Sample and Data Collection

We collected data from angels in the cities of Hefei (Anhui Province) and Ningbo (Zhejiang Province), where two authors have established connections with local angel groups. One author also regularly hosts investment-focused podcasts involving these investors. As in Study 1, the survey was developed in English and translated into Chinese using a standard back-translation procedure (Brislin, 1980; Fu & Tietz, 2019). Participants were recruited via WeChat. Given the well-documented difficulty of accessing early-stage investors (Block et al., 2019; Mason & Harrison, 2002), we also used referral sampling, consistent with prior research (Svetek, 2023).

Because angels often hold multiple investments, we allowed each participant to rate up to three ventures to increase the number of observations. After completing one evaluation, participants were asked whether they had additional current investments and, if so, whether they were willing to rate another, up to a maximum of three ventures. Each venture was evaluated independently on separate screens, and responses could not be revisited.

We invited 417 angels and received 115 responses. After excluding 3 incomplete cases, the final sample included 112 angels (response rate: 26.8%). Among them, 33 evaluated 3 ventures, 36 evaluated two, and 43 evaluated one, yielding 214 venture-level observations. This sample size is comparable to that in field studies of angels (Collewaert, 2012; Collewaert & Sapienza, 2016).

The final sample included 23 female and 89 male respondents, aged from 34 to 57 years (M = 47.6). All held at least a bachelor’s degree and confirmed active angel investment status. On average, they had 11.04 years of investment experience and had been involved with the focal ventures for at least 3 years. All reported being financially capable of providing follow-on funding.

Measures

Dependent Variable

The dependent variable is the angels’ reinvestment likelihood. Following prior studies (Murnieks et al., 2016; Warnick et al., 2018), we measured reinvestment likelihood using two items: 1) the participants were asked to indicate “how likely it is that they would reinvest” (1 = least likely, 7 = most likely); and 2) participants were asked to indicate “the amount they would likely reinvest” (1 = lowest possible amount, 7 = highest possible amount). The items were averaged to form a composite measure of the likelihood to reinvest (α = .904).

Independent Variable

Angels’ current commitment—monetary and non-monetary—was measured using four items adapted from the AIPP data and Study 1. Sample items include, “How much money have you invested in this venture?” (1 = very little, 5 = a great deal) and “How frequently do you interact/communicate with the venture?” (1 = rarely, 5 = weekly or daily). We included both subjective and objective items to reduce confounding. The four items were averaged into a composite measure (α = .87).

Moderators

Cooperative, competitive, and avoidant CMS items were adapted from Chen et al. (2005) and measured on a 7-point scale. Participants were instructed to respond with the focal entrepreneur in mind. Cooperative style assessment included five items (e.g. “Seeks a solution that will be good for all of us”), competitive style four items (e.g. “Treats conflict as a win–lose contest”), and avoidant style six items (e.g. “Smooths over differences by trying to avoid them”). Item scores were averaged to create overall CMS measures. All scales demonstrated strong reliabilities (α = .96, .94, and .92, respectively). Full items are reported in Supplemental Appendix G.

Control Variables

We controlled for factors previously shown to affect angel investment decisions. To account for financial motivations (Mason, 2006), we controlled for venture performance: relative performance to competitors (Collewaert, 2012), profitability, and revenue growth (Block et al., 2019). We also controlled for venture characteristics, including management team track record, presence of current investors, firm size, and firm age (Block et al., 2019). Additional controls captured conflict frequency between investors and entrepreneurs, industry type, investment stage, and whether the venture had previously received follow-on financing. Consistent with prior studies (Murnieks et al., 2011; Warnick et al., 2018), we controlled for investor demographics: age, gender, education, entrepreneurial experience (ventures founded), and years of investment experience. Further details are provided in Supplemental Appendix H.

Analysis and Results

Analytical Approach

Hypotheses were tested using structural equation modeling using M-plus 8.4 (Muthén et al., 2017), which allows for modeling nested data (i.e. multiple venture ratings nested within individual investors). We performed confirmatory factor analysis for the full model. Our hypothesized five-factor measurement model (i.e. reinvestment likelihood; current commitment; and cooperative, competitive, and avoidant CMS) included a set of distinct factors and could correlate freely. The results indicate that the hypothesized measurement model provides a good fit to the data: χ2 (142) = 435, p<.001, comparative fit index = .94, Tucker–Lewis index = 0.92, standardized root mean square residual = 0.05, and root mean square error of approximation = 0.07, with all paths loading significantly onto their respective factors.

Furthermore, we checked for multicollinearity by calculating the variance inflation factors (VIFs) for each regression model. All VIFs are below the acceptable upper limit of 5 (O’brien, 2007), with the highest mean VIF at 1.14. These values suggest that multicollinearity does not influence the model results. Harman’s single-factor test suggests that common method bias is unlikely because the first factor accounted for only 28.5% of the total variance (Podsakoff et al., 2003). Finally, we assessed the degree of nonindependence in the data by calculating the intra-class correlation coefficient (ICC) for the dependent variable. The ICC was 0.173, indicating that 17.3% of the variance in reinvestment likelihood was attributable to differences between investors. This nontrivial level of clustering justifies the use of multilevel modeling (Bliese, 2000).

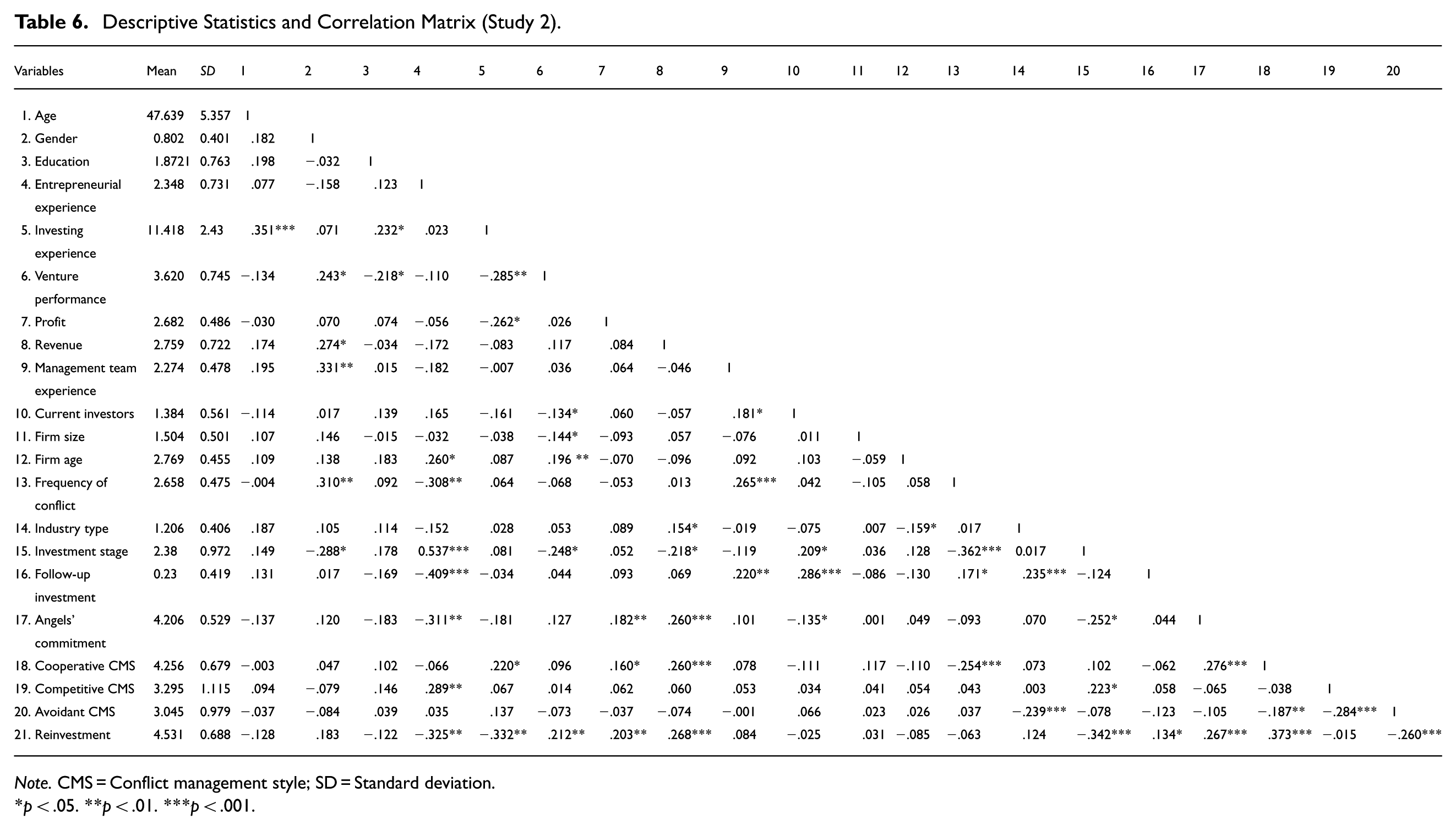

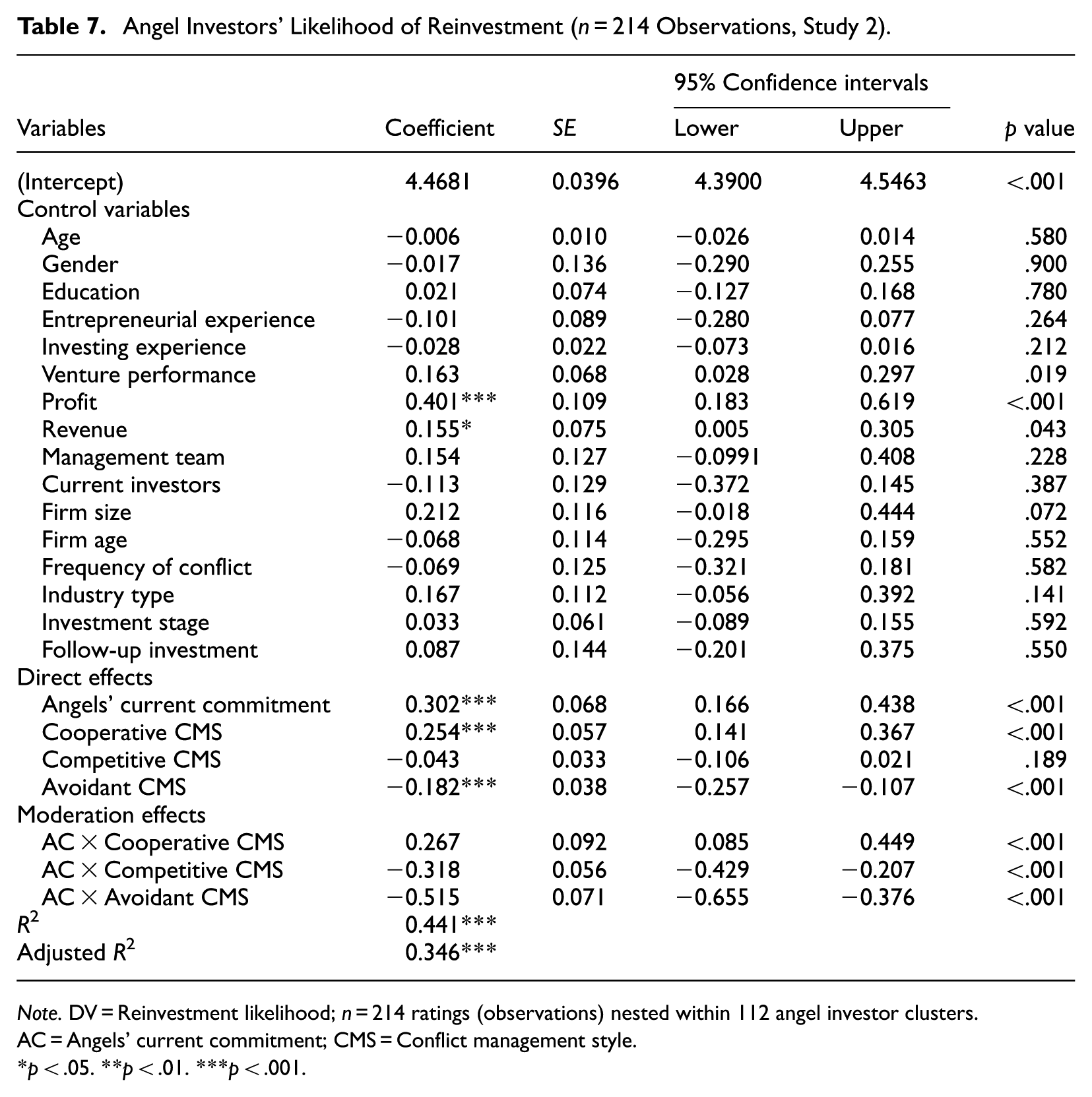

Before conducting the regression analysis, we mean-centered all variables (Aiken et al., 1991). Table 6 presents the descriptive statistics for and correlations between the variables. Table 7 presents the regression results, which show that angels’ current commitment positively influences their EOC to reinvest (β = .302, p < .001), once again supporting the baseline hypothesis.

Descriptive Statistics and Correlation Matrix (Study 2).

Note. CMS = Conflict management style; SD = Standard deviation.

p < .05. **p < .01. ***p < .001.

Angel Investors’ Likelihood of Reinvestment (n = 214 Observations, Study 2).

Note. DV = Reinvestment likelihood; n = 214 ratings (observations) nested within 112 angel investor clusters. AC = Angels’ current commitment; CMS = Conflict management style.

p < .05. **p < .01. ***p < .001.

The interaction between angels’ current commitment and entrepreneurs’ cooperative style is positive and statistically significant (β = .267, p < .001). As shown in Figure 2a, simple slope analysis indicates that the effect of angels’ EOC to reinvest is stronger at high (+1 SD; β = .484, p < .001) than low (−1 SD; β = .121, p = .179) levels of entrepreneurs’ cooperative style, supporting Hypothesis 1.

Interaction between angels’ current commitment and entrepreneurs’ CMSs (study 2): (a) between angels’ current commitment and entrepreneurs’ cooperative CMS, (b) between angels’ current commitment and entrepreneurs’ competitive CMS, and (c) between angels’ current commitment and entrepreneurs’ avoidant CMS.

Further, the interaction between angels’ current commitment and entrepreneurs’ competitive style is negative and statistically significant (β = −.3178, p < .001). Simple slope analysis in Figure 2b shows that the effect of angels’ current commitment on the escalation tendency to reinvest decreases under high (+1 SD) levels of entrepreneurs’ competitive CMS (β = −.052, p = .580) but increases under low (−1 SD) levels of entrepreneurs’ competitive CMS (β = .656, p < .001), supporting Hypothesis 2.

Finally, the interaction between angels’ current commitment and entrepreneurs’ avoidant CMS is negative and statistically significant (β = −.515, p < .001). Simple slope analysis in Figure 2c shows that the effect of angels’ EOC to reinvest is weaker under high (+1 SD; β = −.202, p < .05) than low (−1 SD; β = .807, p < .001) levels of entrepreneurs’ avoidant CMS, supporting Hypothesis 3.

Robustness Analysis

Similar to the preliminary study, we separate angels’ current commitment into monetary and non-monetary types to assess how each influences angels’ likelihood of reinvestment. The results show that non-monetary commitment (time, energy, and effort invested in the venture) has a stronger effect on reinvestment likelihood (β = .281, p < .001) than monetary commitment (β = .163, p < .05), consistent with preliminary findings. To evaluate the robustness of our findings, we further excluded all the control variables from the analysis. This does not alter the pattern of the findings: interaction effects remain significant for entrepreneurs’ cooperative (β = .414, p < .01), competitive (β = −.214, p < .01), and avoidant styles (β = −.501, p < .01).

Discussion

This study examines a central yet understudied question in entrepreneurial finance: When and under what conditions does prior commitment lead angels to reinvest in ventures they have already backed? By addressing this question, we extend research on angel investment decisions (Svetek, 2023; Warnick et al., 2018) by differentiating between initial investment and post-investment (i.e. reinvestment) decision processes. Drawing on EOC theory (Brockner, 1992; Staw, 1997) and the CMS perspective, we demonstrate how investors’ prior commitment interacts with entrepreneurs’ CMS to shape reinvestment decisions beyond venture performance.

Across three complementary studies—involving archival data analysis, a conjoint experiment, and a field study—we report three main findings. First, consistent with EOC theory, prior commitment increases angels’ likelihood of reinvestment, suggesting that sunk cost drives continued investment even under uncertainty (Devigne et al., 2016; Hogrebe & Lutz, 2024). Second, this relationship is conditional on entrepreneurs’ CMS. Specifically, a cooperative CMS strengthens the positive relationship between prior commitment and reinvestment, whereas competitive and avoidant styles attenuate it. This finding indicates that escalation is not purely a cognitive bias but is shaped by relational interaction cues during post-investment engagement. The finding also aligns with evidence suggesting that post-investment evaluation processes become more deliberate and reflective (Fisher & Neubert, 2023), reinforcing recent angel research highlighting the salience of relational quality and ongoing interaction in follow-on investment decisions (Lefebvre et al., 2022; Tetteh et al., 2024). Third, our conjoint results (Study 1) offer a more nuanced interpretation of competitive and avoidant CMS in angel–entrepreneur relationships. Competitive CMS may be tolerated when angels’ prior commitment is low, but becomes detrimental when their commitment is high. Conversely, avoidant CMS consistently weakens reinvestment likelihood, regardless of the angels’ level of prior commitment. These observations are interesting as we ascertain when competitive CMS may be perceived as functional or dysfunctional (Tjosvold, 1998) in investor–entrepreneur interactions, and our results also confirm the detrimental outcomes of avoidant CMS (Chen et al., 2005). Together, these findings highlight that reinvestment decisions emerge from the interplay between psychological commitment and relational dynamics rather than from either in isolation.

Theoretical Implications

First, we advance EOC theory by demonstrating that escalation is not solely an intrapsychic bias but a relationally embedded process. Prior research has emphasized internal mechanisms such as self-justification and sunk costs (Brockner, 1992; Sleesman et al., 2018; Staw, 1997). Our findings extend this perspective by identifying entrepreneurs’ CMS as a critical boundary condition that shapes whether prior commitment translates into continued investment. This perspective reframes escalation decisions as contingent on interaction dynamics: investors do not simply persist because of prior commitment, but because ongoing relational cues allow that commitment to remain justifiable. In doing so, we shift EOC theory from a static cognitive bias to a context-sensitive decision process embedded in ongoing relationships. For scholars, the current findings underscore the need to consider relational factors when theorizing EOC.

Second, we extend conflict management literature by repositioning CMS from predictors of relational outcomes to moderators of decision processes. Prior research has primarily examined how different CMSs affect trust, negotiation outcomes, or team effectiveness (Chen et al., 2005; Tjosvold, 1998). Our findings show that CMSs also shape how decision-makers interpret and act on prior commitments under uncertainty. In this sense, CMS functions as a relational filter through which escalation unfolds, determining whether commitment is reinforced or reconsidered. By positioning CMSs as moderators of the escalation process, this study broadens the theoretical scope of conflict management research and opens an avenue for researchers to consider CMS factors that may influence other established relationships.

Third, we contribute empirically to the angel investment literature by shifting attention from initial investment decisions to reinvestment decisions. Prior research has largely examined the attributes angels consider when evaluating new investment opportunities (Murnieks et al., 2016; Warnick et al., 2018), often isolating economic or relational factors. Our findings complement this literature by showing that reinvestment decisions reflect the joint influence of psychological commitment and relational interaction. This suggests that the determinants of continued investment differ fundamentally from those of initial investment, as they unfold within an established relationship rather than under conditions of first-time evaluation. By integrating these perspectives, we provide a more complete account of how early-stage investments evolve over time.

Practical Implications

This study offers actionable insights for entrepreneurs, investors, and support organizations. First, entrepreneurs should recognize that reinvestment is not solely performance-driven. The way they manage disagreement plays a critical role in sustaining investor support. Demonstrating openness, responsiveness, and collaborative problem-solving can reinforce investor confidence and increase the likelihood of follow-on funding. Second, investors often emphasize venture performance, founder experience, and market potential when deciding to reinvest; yet, our findings indicate that investors may benefit from incorporating relational assessments into their due diligence and post-investment monitoring processes. While financial performance remains important, evaluating how entrepreneurs handle conflict can provide additional insights into the viability of continued collaboration. Finally, accelerators and entrepreneurial educators should emphasize conflict management, emotional intelligence, and relational skills in training programs. These capabilities are not only interpersonal competencies but also influence long-term financing outcomes. More broadly, these insights suggest that governance mechanisms in early-stage investing should account for both cognitive and relational dimensions of decision-making.

Limitations and Future Research

This study has some limitations that suggest avenues for future research. First, while escalation research typically focuses on individuals (Staw, 1981) and CMS research at the dyadic level (Tjosvold et al., 2006; Zhang et al., 2011), future research could adopt a cross-level perspective by examining how individual angels’ commitment interacts with group-level conflict norms in syndicates or investment committees. This would respond to calls to contextualize escalation processes (Sleesman et al., 2018) and may yield more generalizable theoretical insights. Moreover, a longitudinal design could track how CMS perceptions and commitment evolve and shape continued investor engagement. Second, entrepreneurs’ psychological capital (e.g. resilience, optimism, and hope) may influence CMSs (Zou et al., 2016) and could change investors’ perception of entrepreneurs’ CMSs. Future studies could incorporate these factors to ascertain if their presence shifts angels’ perception when evaluating entrepreneurs’ CMS and its subsequent effect on their EOC. Third, beyond CMS, other relational and individual factors—such as trust or investor personality—may further condition reinvestment behavior, meriting investigation in future studies. Fourth, while we conceptualize angels’ commitment as financial and non-financial, future research may benefit from distinguishing between different forms of commitment (e.g. emotional vs. financial) and how these levels of commitment influence their evaluation of entrepreneurs’ CMS in investment decisions. Last, given the relational embeddedness of context, comparative studies across institutional settings could examine how different cultural environments shape the role of CMS in reinvestment decisions.

Conclusion

This study shows that angels do not make reinvestment decisions solely based on economic factors, nor are they influenced by psychological or social considerations alone. Instead, they consider these factors holistically to make informed reinvestment decisions. Prior commitment creates a tendency toward persistence, but whether this tendency translates into reinvestment depends on how entrepreneurs manage ongoing relationships. By integrating EOC theory and CMS, we demonstrate that escalation is a socially embedded process shaped by relational dynamics. In doing so, we explain not only why angels persist in ventures but also when they withdraw and how entrepreneurs’ interaction styles shape the trajectory of early-stage investment.

Supplemental Material

sj-pdf-1-etp-10.1177_10422587261453867 – Supplemental material for Angel Investors’ Reinvestment Decisions: Escalating Commitments and Conflict Management Beyond Venture Performance

Supplemental material, sj-pdf-1-etp-10.1177_10422587261453867 for Angel Investors’ Reinvestment Decisions: Escalating Commitments and Conflict Management Beyond Venture Performance by Alexander Narh Tetteh, Haibo Zhou, Dan K. Hsu and Qingxiong (Derek) Weng in Entrepreneurship Theory and Practice

Footnotes

Acknowledgements

The authors are grateful to the editor Dr. Bat Batjargal and two anonymous reviewers for their very constructive and helpful comments during the review process. This Project is supported by Ningbo FinTech Governance and Innovation Mechanisms Key Laboratory. We would also like to thank Editage (![]() ) for English language editing.

) for English language editing.

Ethical Considerations

All participants of studies involving primary data collection have given their consent to be part of this study. They were well-informed about the purpose and objectives of both studies. The Research Ethics Committee of the School of Management of the University of Science and Technology of China reviewed and approved this study and data collection procedures. The study was also conducted in accordance with the ethical standards of the Declaration of Helsinki guidelines.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Qingxiong (Derek) Weng acknowledges funding support by the National Natural Science Foundation of China, with grant/award number: 72472146.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting this study are available upon reasonable request.*

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.