Abstract

The federal Child and Dependent Care Credit (CDCC) subsidizes child care costs for working families. Before 2021, the CDCC was nonrefundable, so only families with positive tax liability after other deductions benefited. I estimate how CDCC eligibility, benefits, and marginal tax rates would change if the credit were made permanently refundable. Under refundability, some 5 percent of single parents gain eligibility and receive on average over $1,000 annually. Eligibility increases are largest among Black and Hispanic households. Increases in marginal tax rates among moderate-income taxpayers are small.

Introduction

Child care in the United States is expensive. In recent years, the average household in the bottom quartile of the income distribution spent nearly 20 percent of their income on child care (Herbst 2018). As researchers show that child care costs keep parents out of the labor market, 1 many policymakers have recommended active labor market policies to decrease the cost of care. The Child and Dependent Care Credit (CDCC), a tax credit based on income and child care expenses, is one such policy. Specifically, the credit subsidizes child care costs for working families and is available to households with children younger than 13 in which all parents have positive annual earnings. While many families meet these criteria, from its introduction in 1976 through 2020, the CDCC was nonrefundable, so only families with positive tax liability after other deductions benefited. As low-income households tend to spend a higher proportion of their income on child care (Herbst 2018) and researchers show that the CDCC promotes work participation, 2 many policymakers advocated making the credit refundable. In response to the COVID-19 pandemic, the American Rescue Plan Act of 2021 made the CDCC refundable and increased its generosity during tax year 2021 only. In this paper, I estimate how CDCC eligibility, benefits, and marginal tax rates would change for different groups if the credit were made permanently refundable. I describe changes in outcomes and incentives that arise solely from changes in tax policy, relative to CDCC parameters as of 2020. The results are the first step in understanding the effects of a permanently refundable CDCC.

Earlier work on the distributional impacts of the nonrefundable CDCC, in which authors use data from the 1970s through the 1990s, suggests that the nonrefundable credit does not reach the bottom decile of the income distribution (Altshuler and Schwartz 1996; Dunbar and Nordhauser 1991; Gentry and Hagy 1996). I expand upon this work by estimating eligibility rates across different income and demographic groups and accounting for changes in CDCC parameters and the distribution of taxpayers over time. Additionally, I consider distributional impacts on marginal tax rates and discuss how the CDCC differentially affects work incentives across the income distribution. Finally, I estimate how such distributional impacts would change if the credit were made permanently refundable.

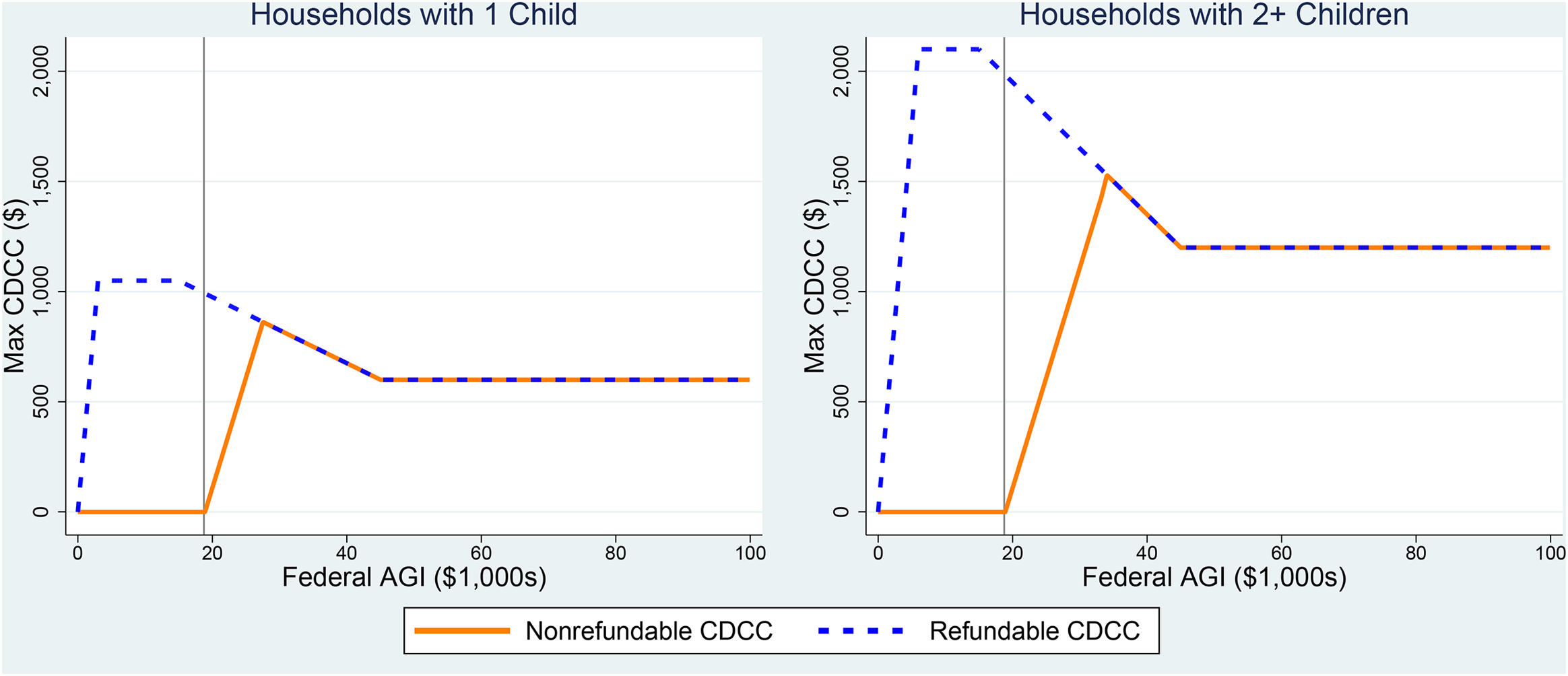

In the paper, I first examine the maximum federal CDCC benefits that households may receive across the income distribution. Under the nonrefundable CDCC, the maximum benefit for households with two or more qualifying dependents is about $1,500 per year, and households with adjusted gross income (AGI) below $18,650 are ineligible for benefits because they do not have any tax liability. If the CDCC were made permanently refundable, low-income households could gain eligibility and receive up to 35 percent of AGI, to a maximum of $2,100 per year, in benefits.

While making the CDCC permanently refundable would encourage child care spending and labor force participation, it would generate complex intensive margin labor supply incentives. Because refundability would alter the AGI thresholds at which benefits increase, decrease, or remain constant as income increases, marginal tax rates would change in different directions and by different amounts across the income distribution. I therefore simulate marginal tax rates as a consequence of federal individual income taxes and tax benefits targeted at families with children, including the CDCC, using tax code provisions and the National Bureau of Economic Research’s (NBER) TAXSIM program. I find that making the CDCC permanently refundable would decrease marginal tax rates substantially for very-low-income families. Refundability, however, would increase marginal tax rates for taxpayers with $25,000 to $33,000 in AGI increase by over 10 percentage points.

Given different effects of refundability across the income distribution, I also study the extent to which actual taxpayers would benefit from a permanently refundable CDCC using data from the 2018 Survey of Income and Program Participation (SIPP). Simulation results show that, all else equal, making the CDCC permanently refundable would lead to relatively large increases in eligibility among single-parent, Black, and Hispanic households, which are all less likely to qualify for the nonrefundable credit. Specifically, some 3 percent of Black households, 2 percent of Hispanic households, and 1 percent of white households would gain eligibility, all else equal. Another 14 percent of Black households, 8 percent of Hispanic households, and 7 percent of white households have incomes too low to qualify for the nonrefundable CDCC but would become eligible if refundablility led them to pay for child care. About 5 percent of single parents would gain eligibility and would receive on average over $1,000 in benefits annually. This increase is substantial, constituting 18 percent of existing child care spending and 10 percent of AGI. As expected, marginal tax rates with respect to income would increase for some moderate-income taxpayers, all else equal. Nevertheless, increases in marginal tax rates with respect to income are small relative to decreases in marginal tax rates with respect to child care expenditures, which could mitigate intensive margin labor supply disincentives.

In the following section, I provide institutional details and document CDCC eligibility and benefits with and without refundability. In section “How Would Permanent Refundability Affect Incentives?,” I characterize how making the CDCC permanently refundable would affect average and marginal tax rates. In section “Effects across the Distribution of Taxpayers,” I use data from the 2018 SIPP to show how refundability would affect CDCC eligibility, potential benefits, and marginal tax rates across income and demographic groups. In section “State CDCC Benefits,” I discuss implications of refundability on state child care credit programs. In section “Conclusion and Discussion,” I conclude.

Institutional Details and CDCC Generosity

Congress implemented the federal CDCC in 1976 and expanded it in 1981 and 2001. The latter expansion took effect in 2003, and between 2003 and 2020, households were able to claim up to $3,000 worth of child care expenses per year for each of up to two children younger than 13. Such households could receive a tax credit worth up to 35 percent of those expenses, or $1,050 per child. Beginning at $15,000 in AGI, the benefit rate decreased by 1 percentage point for each additional $2,000 until it remained at 20 percent for those with $43,000 or more in AGI, who could receive up to $600 per child in benefits. The CDCC, however, was nonrefundable, so taxpayers without positive tax liability were ineligible. The credit is not indexed to inflation.

Moreover, CDCC claimants must work to qualify for benefits, including both spouses among married taxpayers filing jointly. Additionally, if either spouse’s earnings are less than child care expenditures, then the CDCC is calculated as a percent of the lesser of the two taxpayers’ earnings. Almost any child care expenditures are eligible for the credit, except care provided by a noncustodial parent. To claim the credit, taxpayers must list their earnings, child care expenditures, and child care providers’ tax identification or Social Security numbers on federal Form 2441. Benefits decrease taxes due at tax filing time.

Nonrefundability generates a difference between statutory and effective, or actual, benefits received. I therefore use the tax filing thresholds, AGI levels at which taxpayers begin to have positive tax liability, to document maximum effective CDCC benefit schedules with and without refundability in Figure 1. Specifically, the figure displays benefits for single parents with one (left panel) or two or more (right panel) eligible dependents and the maximum qualifying child care expenditures as of 2020. 3 The figure shows that taxpayers’ incomes must exceed the tax filing threshold of $18,650 to be eligible for nonrefundable benefits. For taxpayers with incomes above this threshold, nonrefundable benefits (orange solid lines) increase with income before reaching peaks of about $860 at $27,600 in AGI for households with one eligible dependent and $1,530 at $34,100 in AGI for households with two or more eligible dependents. Benefits then decrease until they plateau at $600 per child for taxpayers with $43,000 or more in income.

Maximum Federal CDCC Benefits by Federal AGI. Notes: Left panel: Maximum federal CDCC benefits for households with one eligible dependent with and without refundability as of 2020. Right panel: Maximum federal CDCC benefits for households with two or more eligible dependents with and without refundability as of 2020. Source: Author’s calculations using federal tax forms.

Figure 1 shows that if the CDCC were made permanently refundable (blue dashed lines), low-income taxpayers would receive larger benefits. For very-low-income taxpayers, refundable benefits increase as income increases and then hold steady at $1,050 per child at incomes up to $15,000. For taxpayers with AGI above $15,000, refundable benefits steadily fall as income increases until they converge with nonrefundable benefits. Hence, Figure 1 shows that making the CDCC permanently refundable would increase generosity among low-income taxpayers without affecting benefits for those with higher incomes.

Interactions with other elements of the tax code also affect CDCC generosity. 4 For instance, for some taxpayers, nonrefundable CDCC benefits directly offset benefits from the CTC, a partially refundable tax credit for families based on number of children. (Similar to the CDCC, the CTC was temporarily expanded during tax year 2021 only. In my analyzes, I consider CTC parameters as of 2020, which are set to be restored in 2022.) Households are able to receive up to $2,000 in CTC benefits per child younger than 17. 5 If the credit value exceeds the amount of tax a household owes, the household can receive refundable benefits through the Additional Child Tax Credit (ACTC). The ACTC is worth 15 percent of earnings over $2,500, up to a maximum of $1,400 per child. CTC benefits decrease with income for single taxpayers with more than $200,000 and for married taxpayers with more than $400,000.

Before calculating CTC benefits, taxpayers’ tax liability is reduced by several nonrefundable tax credits, including the nonrefundable CDCC. Therefore, taxpayers with positive tax liability before claiming the CDCC but without positive tax liability after claiming the CDCC become ineligible for the nonrefundable portion of the CTC but remain eligible for the ACTC. Because the ACTC is limited to a percent of AGI over $2,500, however, nonrefundable CDCC benefits decrease total CTC benefits for some taxpayers. If the CDCC were made permanently refundable, these taxpayers’ CTC benefits could increase: refundable tax credits come after nonrefundable tax credits on federal Form 1040, so CDCC benefits no longer would affect tax liability used to calculate the CTC.

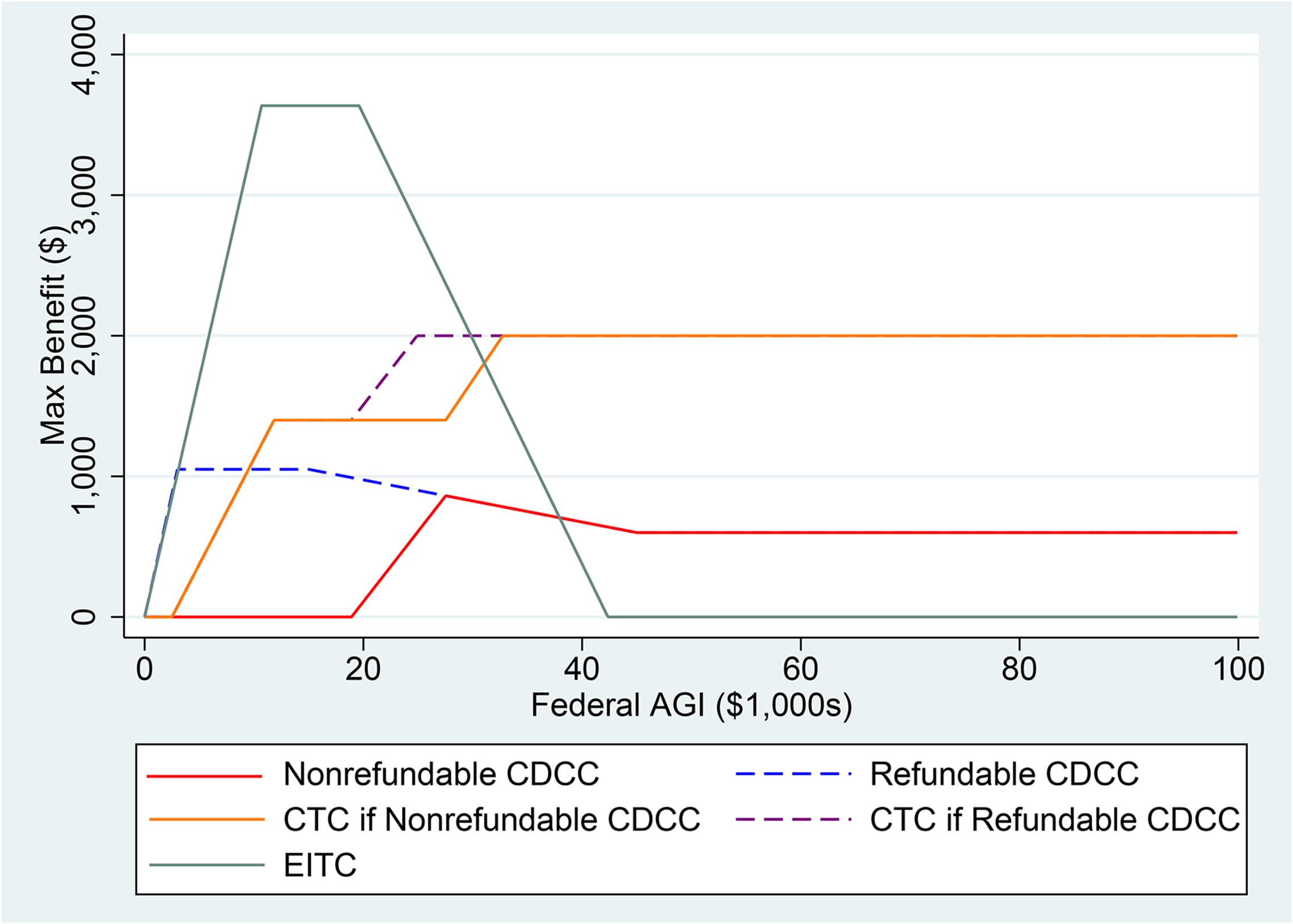

Figure 2 illustrates the interactions between CDCC and total CTC benefits—which include both the refundable and nonrefundable portions of the credit—across the income distribution. In particular, the figure documents benefits for tax-minimizing single taxpayers with one eligible dependent, no additional children, the maximum qualifying child care expenditures as of 2020, and only earned income. Nonrefundable (solid red line) and refundable (dashed blue line) CDCC benefits are identical to those shown in Figure 1. Under a nonrefundable CDCC, CTC benefits (solid orange line) increase with income for taxpayers with less than about $12,000 in AGI, who receive the refundable portion of the CTC. Benefits then hold steady at $1,400 until AGI reaches about $28,000, where taxpayers begin to benefit from both the refundable and nonrefundable portions of the credit. Benefits then increase until they peak and remain constant at $2,000 for taxpayers with $33,000 or more in AGI. As expected, if the CDCC were made permanently refundable, total CTC benefits (dashed purple line) would increase for some taxpayers. In particular, CTC benefits would increase by up to $600 among taxpayers with around $19,000 to $33,000 in AGI.

Maximum Federal CDCC, CTC, and EITC Benefits by Federal AGI. Notes: Federal CDCC, CTC, and EITC benefits for single households with one eligible dependent, no additional dependents, and the maximum qualifying child care expenditures with and without CDCC refundability as of 2020. Results shown for tax-minimizing households with income that comes solely from earnings. Source: Author’s calculations using federal tax forms.

The CDCC also may interact indirectly with the EITC. Although CDCC benefits do not affect EITC benefits directly, both tax programs promote work and redistribute income toward working families with children. The EITC is a refundable tax credit targeted at low- to moderate-income families. As shown in Figure 2, EITC benefits increase with household earnings until they reach a maximum benefit level, $3,584 for families with one child as of 2020. Benefits then remain constant until household earnings reach another level, $19,330 for families with children as of 2020, at which point benefits begin to phase out toward zero. 6

Furthermore, twenty four states and the District of Columbia supplement the federal CDCC with their own refundable or nonrefundable state child care credits. Statutory maximum benefits vary considerably across states, from $394 to $2,310 for families with two eligible dependents as of 2020. Unlike the federal CDCC, however, some states offer refundable credits, limit benefits to taxpayers with incomes below a certain threshold, or provide larger benefits to low-income households. States generally calculate their benefits as a percent of the federal CDCC received or the federal CDCC that the taxpayer would have received if the federal credit were refundable. I consider how state supplements to the federal CDCC would affect changes in benefits and marginal tax rates under permanent refundability in section “State CDCC Benefits.”

How Would Permanent Refundability Affect Incentives?

As a subsidy for child care, CDCC benefits encourage child care spending and effectively increase wages net of child care costs. Since all parents must work to receive benefits, increases in benefits promote labor force participation. However, the CDCC generates complex intensive margin labor supply incentives. And as shown in Figure 1, making the credit permanently refundable would create different phase-in, plateau, and phase-out regions of the credit. Each of these credit region shifts would generate changes in marginal tax rates, and their size and direction of would vary across the income distribution.

In this section, I examine the effects of making the CDCC permanently refundable on extensive and intensive margin labor supply incentives by comparing average and marginal tax rates with respect to income with and without refundability. More specifically, I simulate average and marginal tax rates as a consequence of federal individual income taxes and the CDCC, CTC, and EITC—hereafter, family tax benefits—with and without refundability. Accounting not only for the CDCC but also for other tax programs that affect families with children allows interactions between the CDCC and other tax benefits to affect tax rates. This is particularly important when studying the effects of refundability on incentives, as evidence documented in section “Institutional Details and CDCC Generosity” shows that making the CDCC permanently refundable would increase CTC benefits for some taxpayers. 7

Throughout the analyzes, I document average and marginal tax rates separately across single and married taxpayers, who receive different tax treatment. For instance, married parents receive larger standard deductions and face lower individual income tax rates. Additionally, at low income levels, CDCC benefits are a function of the lesser earner’s earnings. To estimate marginal tax rates, I use tax code provisions and NBER’s TAXSIM program, which calculates individuals’ tax liabilities and tax credits, including their family tax benefits under 2020 tax law. In doing so, I assume households tax-minimize, single parents file as head-of-household, and married parents file jointly. I also assume all income comes from earnings. For married parents, I document marginal tax rates for spouses with equal earnings but find similar results for married parents with unequal earnings in the Online Appendix. 8

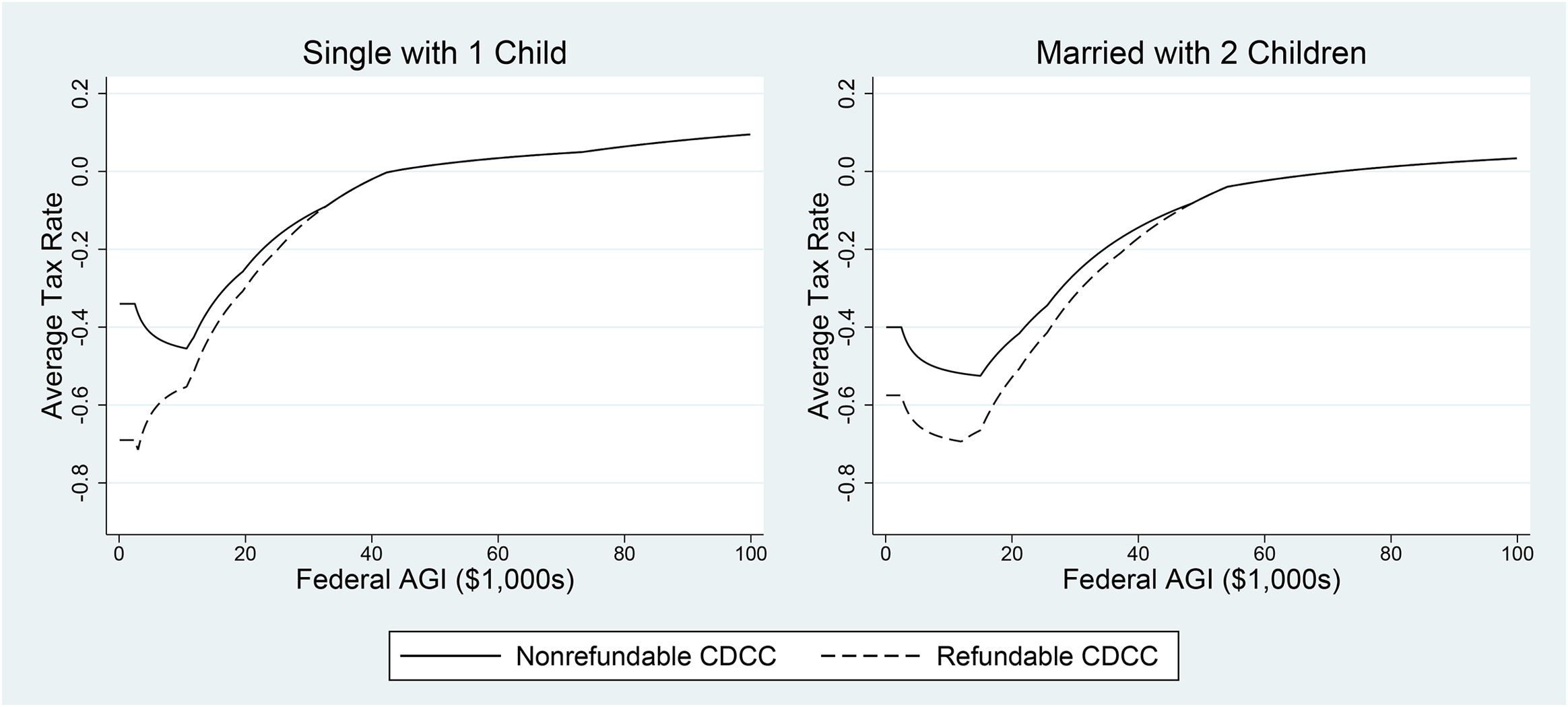

The left panel of Figure 3 displays the average tax rates for single parents with one eligible dependent, no older children, and the maximum qualifying child care expenditures.

9

The black line depicts average tax rates as a consequence of federal individual income taxes and family tax benefits under 2020 tax law. Average tax rates tend to decrease as income increases at low income levels until they bottom out at

Average Tax Rates due to Federal CDCC, CTC, EITC, and Individual Income Taxes. Notes: Left panel: Average tax rates with respect to earnings due to federal CDCC, CTC, and EITC benefits and federal individual income taxes among single parents with one eligible dependent and no older children with and without refundability as of 2020. Right panel: Average tax rates with respect to the lesser earner’s earnings due to the federal CDCC, CTC, EITC, and individual income taxes among married parents with two eligible dependents, no older children, and equal earnings with and without refundability as of 2020. Source: Author’s calculations using TAXSIM and federal tax forms.

Similarly, the right panel of Figure 4 depicts average tax rates for married parents with two eligible dependents, no older children, and the maximum qualifying child care expenditures. Though married taxpayers tend to face lower average tax rates, the pattern of results is largely similar to that for single taxpayers. Taken together, results from Figure 3 confirm that making the federal CDCC permanently refundable would encourage labor force participation, particularly among low-income households, who would experience the largest increases in benefits and decreases in average tax rates. Results imply that under the assumption that all parents pay for child care while working and an extensive margin labor supply elasticity of 0.4 (Kleven and Kreiner 2006), employment among single taxpayers with one eligible dependent and $15,000 in AGI would increase by 8.3 percent if the CDCC were made permanently refundable. This is an upper bound on the extensive margin labor supply response under refundability, as parents may be able to enter the labor force without paying for child care.

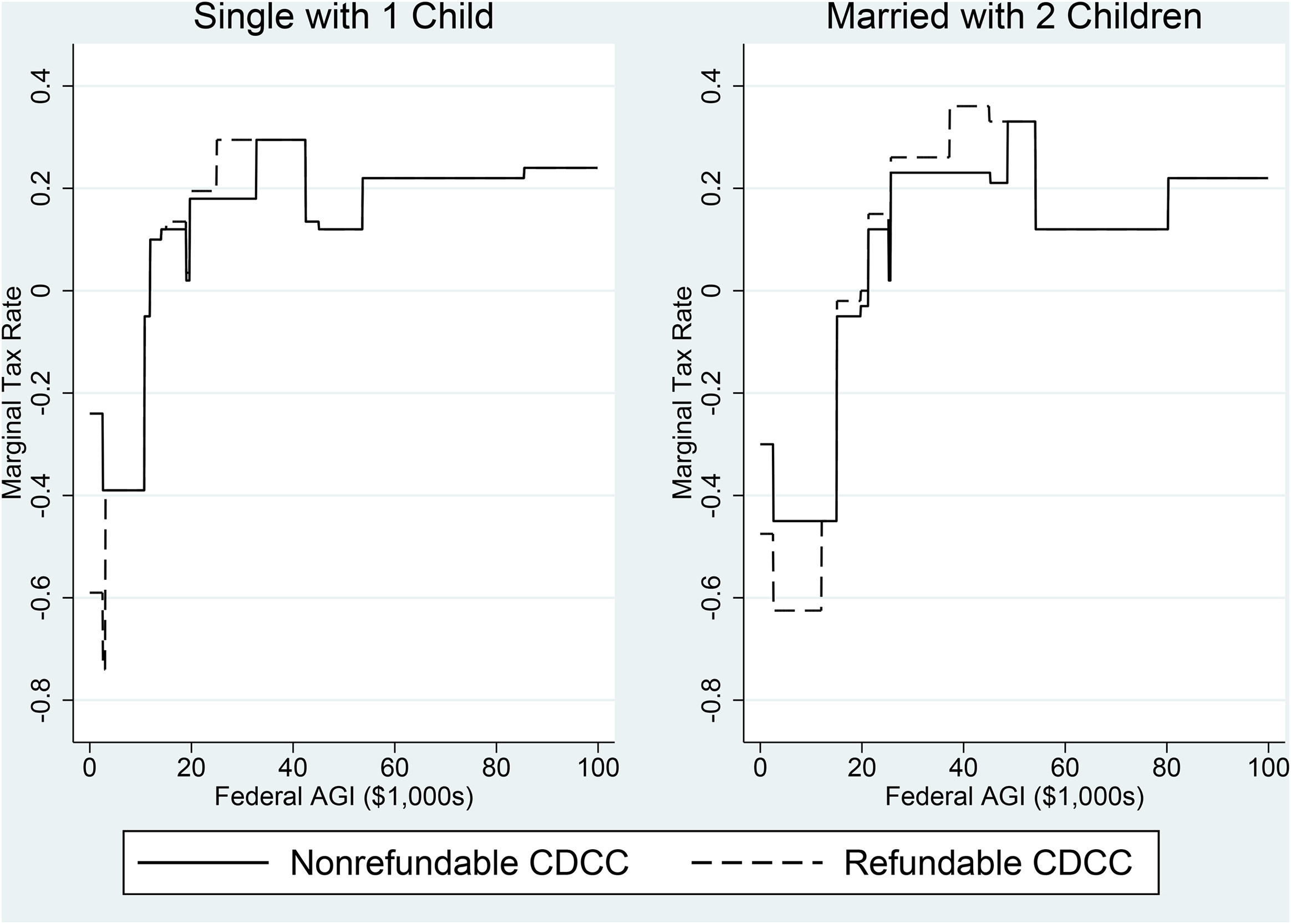

Marginal Tax Rates due to Federal CDCC, CTC, EITC, and Individual Income Taxes. Notes: Left panel: Marginal tax rates with respect to earnings due to federal CDCC, CTC, and EITC benefits and federal individual income taxes among single parents with one eligible dependent and no older children with and without refundability as of 2020. Right panel: Marginal tax rates with respect to the lesser earner’s earnings due to the federal CDCC, CTC, EITC, and individual income taxes among married parents with two eligible dependents, no older children, and equal earnings with and without refundability as of 2020. Source: Author’s calculations using TAXSIM and federal tax forms.

Next, to study intensive margin labor supply incentives, Figure 4 shows the estimated effects of refundability on marginal tax rates. The left panel, which, similar to that in Figure 3, shows the marginal tax rates for single parents with one eligible dependent, indicates that making the CDCC permanently refundable would decrease marginal tax rates by 35 percentage points for those with less than $3,000 in AGI. Refundability would not affect marginal tax rates for single parents between incomes of $3,000 and $15,000, but it would increase rates by 1.5 percentage points between incomes of $15,000 and $25,000 and by 11.5 percentage points between incomes of $25,000 and $33,000.

Marginal tax rates for otherwise similar married parents with two eligible dependents exhibit a similar pattern. Thus, intensive margin labor supply incentives of making the CDCC permanently refundable depend on the region of the credit in which taxpayers fall. Because a refundable CDCC would subsidize earnings for single taxpayers with less than $3,000 in AGI and married taxpayers with less than $6,000 in AGI, very-low-income households experience a positive substitution effect that encourages work hours and a negative income effect that discourages work hours. Weakly positive income and substitution effects among taxpayers on the phase-out region of the refundable CDCC discourage intensive margin labor supply.

Effects across the Distribution of Taxpayers

Given different effects of refundability across the income distribution shown in sections “Institutional Details and CDCC Generosity” and “How Would Permanent Refundability Affect Incentives?,” I now study the extent to which actual taxpayers would benefit from a permanently refundable CDCC. To do so, I account for taxpayer characteristics and child care spending using data from Wave 1 of the 2018 SIPP. The data allow me to estimate CDCC eligibility rates by family structure and race and to simulate how permanent refundability would affect CDCC benefits and marginal tax rates across households that face different child care and labor supply incentives.

The SIPP is a nationally representative survey of about 45,000 households. Wave 1 of the 2018 SIPP was administered during 2018 and documents individuals’ demographics and economic outcomes, including their child care expenses and income from various sources, as of 2017. Specifically, I observe monthly individual earnings, as well as annual household income from rent, alimony, retirement, Social Security, and a number of assets. I also observe household child care expenses as of December 2017. When I study CDCC outcomes, I assume that child care expenses remain constant throughout the year. This likely yields an underestimate of annual child care expenses, as parents are more likely to rely on child care during the summer (Capizzano, Adelman, and Stagner 2002). In this case, I underestimate households’ potential CDCC benefits and any changes in benefits that would occur if the credit were made permanently refundable.

To isolate the population most affected by the CDCC, I limit the sample to households with children younger than 13. There are about 5,500 households in the sample. I use information on income, demographics, and child care expenses to estimate households’ potential nonrefundable federal CDCC benefits—the benefits that they would receive if they claimed the credit—using TAXSIM. 10 In doing so, I estimate CDCC benefits that respondents would have received using 2020 tax parameters, but estimates using 2017 tax parameters are nearly identical. 11

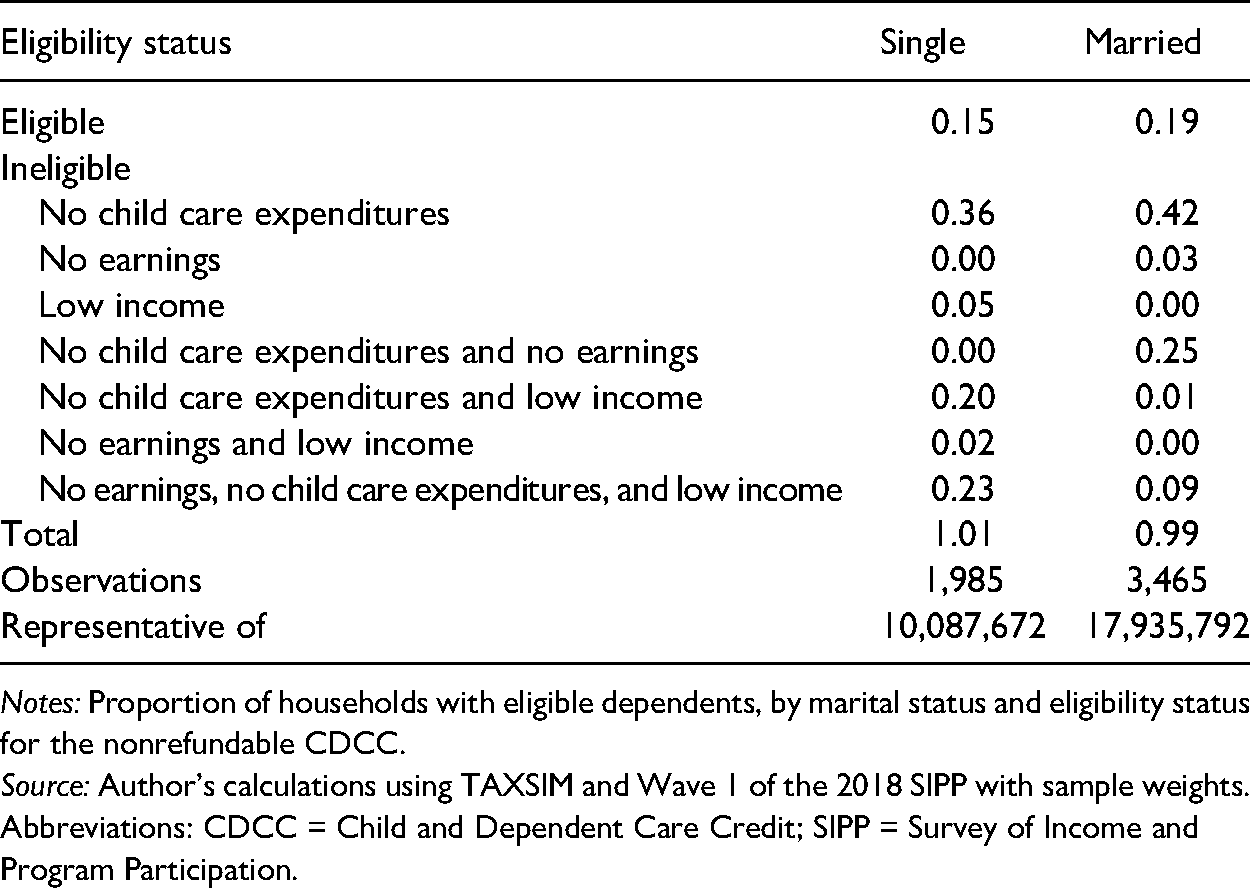

Table 1 documents the proportion of single and married parents by eligibility status under the nonrefundable CDCC using sample weights. The table shows that 15 percent of single parents and 19 percent of married parents are eligible for nonrefundable CDCC benefits. About 5 percent of single parents have incomes too low to qualify for the nonrefundable CDCC but would become eligible if the credit were made permanently refundable. Another 56 percent of single parents would gain eligibility if refundability led them to pay for child care. The remaining 25 percent of single parents do not work and have incomes too low to qualify for the nonrefundable CDCC. Among married parents, 10 percent have incomes too low to qualify for the nonrefundable CDCC, but virtually none of these households pay for child care and, therefore, would remain ineligible under a refundable credit. Most married parents are ineligible for the CDCC because they do not pay for child care or one of the parents does not work.

Proportion of Households by Marital Status and Eligibility Status.

Notes: Proportion of households with eligible dependents, by marital status and eligibility status for the nonrefundable CDCC.

Source: Author’s calculations using TAXSIM and Wave 1 of the 2018 SIPP with sample weights. Abbreviations: CDCC = Child and Dependent Care Credit; SIPP = Survey of Income and Program Participation.

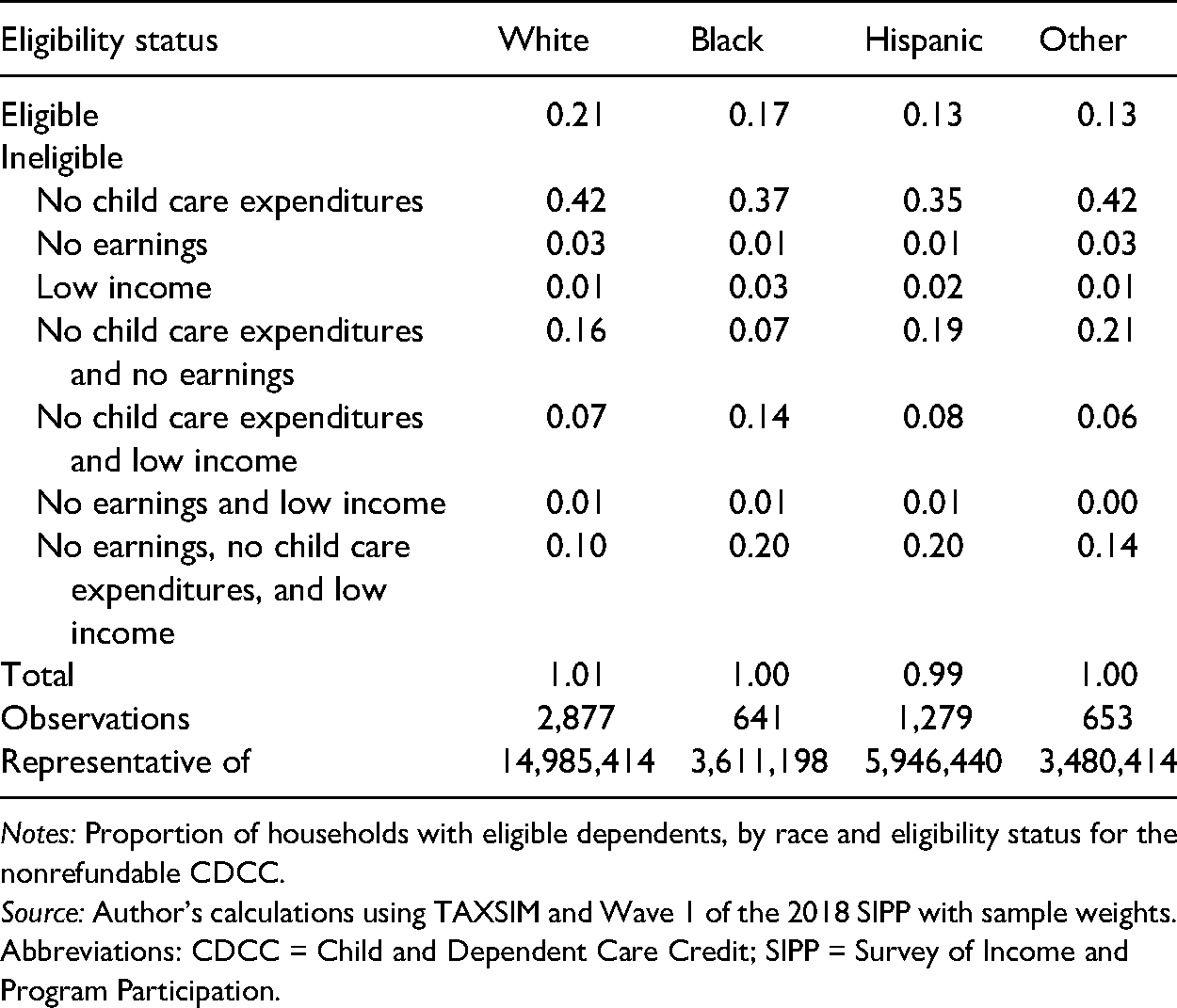

Similarly, Table 2 documents the CDCC eligibility rates by the race of the mother or single father. 12 The table shows that Black and Hispanic households, which tend to have lower incomes, are less likely than white households to be eligible for the nonrefundable CDCC. Whereas 21 percent of white households are eligible, only 17 percent of Black households and 13 percent of Hispanic households are eligible. Making the CDCC permanently refundable would increase eligibility by about 3 percentage points among Black households, by about 2 percentage points among Hispanic households, and by about 1 percentage point among white households. Another 14 percent of Black households, 8 percent of Hispanic households, and 7 percent of white households have incomes too low to qualify for the nonrefundable CDCC but would become eligible if refundability led them to pay for child care. There may be more scope for such behavioral responses among Hispanic households in particular, who are less likely to pay for child care and meet the CDCC’s work requirements. Specifically, all parents have earnings in about 70 percent of both white and Black households, but all parents work in only 59 percent of Hispanic households. Consistent with differences in labor supply across Hispanic and non-Hispanic households, 25 percent of white and 22 percent of Black households pay for child care while only 18 percent of Hispanic households pay for care. In general, Table 2 suggests the permanent CDCC refundability would decrease eligibility gaps between whites and underrepresented groups, especially if increases in benefits induce more Hispanic households to work and pay for child care. 13

Proportion of Households by Race and Eligibility Status.

Notes: Proportion of households with eligible dependents, by race and eligibility status for the nonrefundable CDCC.

Source: Author’s calculations using TAXSIM and Wave 1 of the 2018 SIPP with sample weights.

Abbreviations: CDCC = Child and Dependent Care Credit; SIPP = Survey of Income and Program Participation.

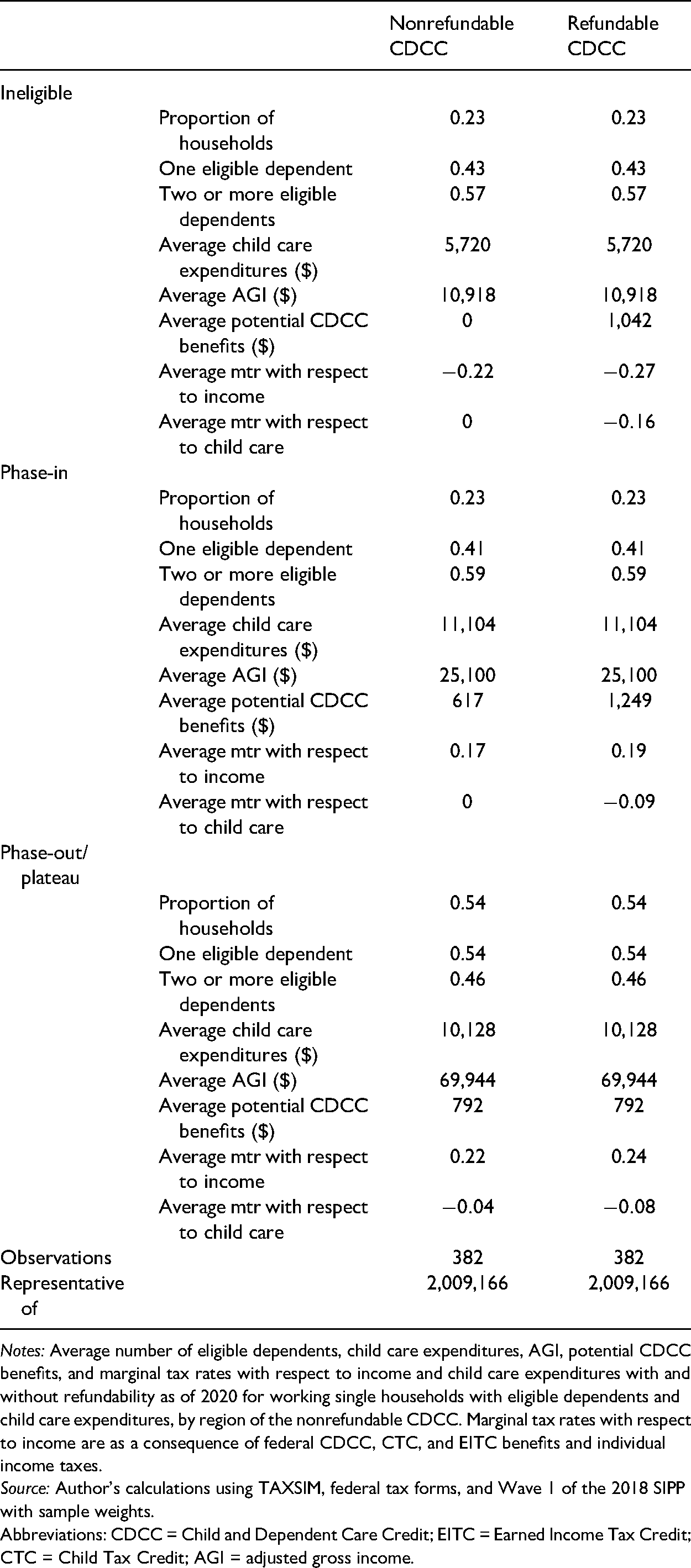

Next, I study how potential CDCC benefits and marginal tax rates would change if the CDCC were made permanently refundable among parents who currently work and pay for child care, all else equal. To study outcomes separately across working households who face different incentives due to the CDCC, I assign households to the ineligible, phase-in, or phase-out/plateau regions of the nonrefundable credit. As in section “How Would Permanent Refundability Affect Incentives?,” I simulate marginal tax rates with respect to income as a consequence of family tax benefits and individual income taxes using 2020 tax code provisions and TAXSIM. I also use 2020 tax code provisions and TAXSIM to simulate marginal tax rates with respect to child care expenditures as a consequence of the CDCC. 14

Table 3 displays the average number of eligible dependents, child care expenditures, AGI, potential CDCC benefits, and marginal tax rates with respect to income and child care expenditures among working single parents with child care expenses using sample weights. The table yields several key findings. First, nearly half of the parents fall in the ineligible or phase-in regions of the nonrefundable CDCC. Specifically, some 23 percent fall in the ineligible region, another 23 percent fall in the phase-in region, and the remaining 54 percent fall in the phase-out/plateau region. About 60 percent of households in the ineligible and phase-in regions and about 45 percent of households in the phase-out/plateau region have two or more eligible dependents. Second, despite having low income levels, households in the ineligible and phase-in regions spend a considerable amount on child care—about $6,000 and $11,000 per year, respectively. 15 While households on the phase-out/plateau region have similar average child care expenditures as households on the phase-in region, their average income, nearly $70,000, is quite high compared to average incomes in the other credit regions.

Distribution of Working Single Households with Eligible Dependents and Child Care Expenditures.

Notes: Average number of eligible dependents, child care expenditures, AGI, potential CDCC benefits, and marginal tax rates with respect to income and child care expenditures with and without refundability as of 2020 for working single households with eligible dependents and child care expenditures, by region of the nonrefundable CDCC. Marginal tax rates with respect to income are as a consequence of federal CDCC, CTC, and EITC benefits and individual income taxes.

Source: Author’s calculations using TAXSIM, federal tax forms, and Wave 1 of the 2018 SIPP with sample weights.

Abbreviations: CDCC = Child and Dependent Care Credit; EITC = Earned Income Tax Credit; CTC = Child Tax Credit; AGI = adjusted gross income.

Third, Table 3 shows that permanent refundability would generate substantial increases in average annual potential CDCC benefits among households in the ineligible and phase-in regions. In particular, average annual potential CDCC benefits would increase from $0 to $1,042 in the ineligible region and from $617 to $1,249 in the phase-in region, all else equal. In the ineligible region, the increase constitutes 18 percent of existing child care spending and 10 percent of AGI. In the phase-in region, it constitutes 6 percent of child care spending and 3 percent of AGI. As expected, benefits would not increase in the phase-out/plateau region of the credit.

Finally, consistent with evidence from section “How Would Permanent Refundability Affect Incentives?,” benefit increases affect marginal tax rates as a consequence of family tax benefits and individual income tax, all else equal. In the ineligible region, the average marginal tax rate with respect to income decreases from

Among married parents, approximately 1 percent fall in the ineligible region of the nonrefundable CDCC, and about 4 percent fall in the phase-in region. In the online appendix, I show that making the CDCC permanently refundable would increase average potential CDCC benefits by $160 per year among married parents in the phase-in region, all else equal.

State CDCC Benefits

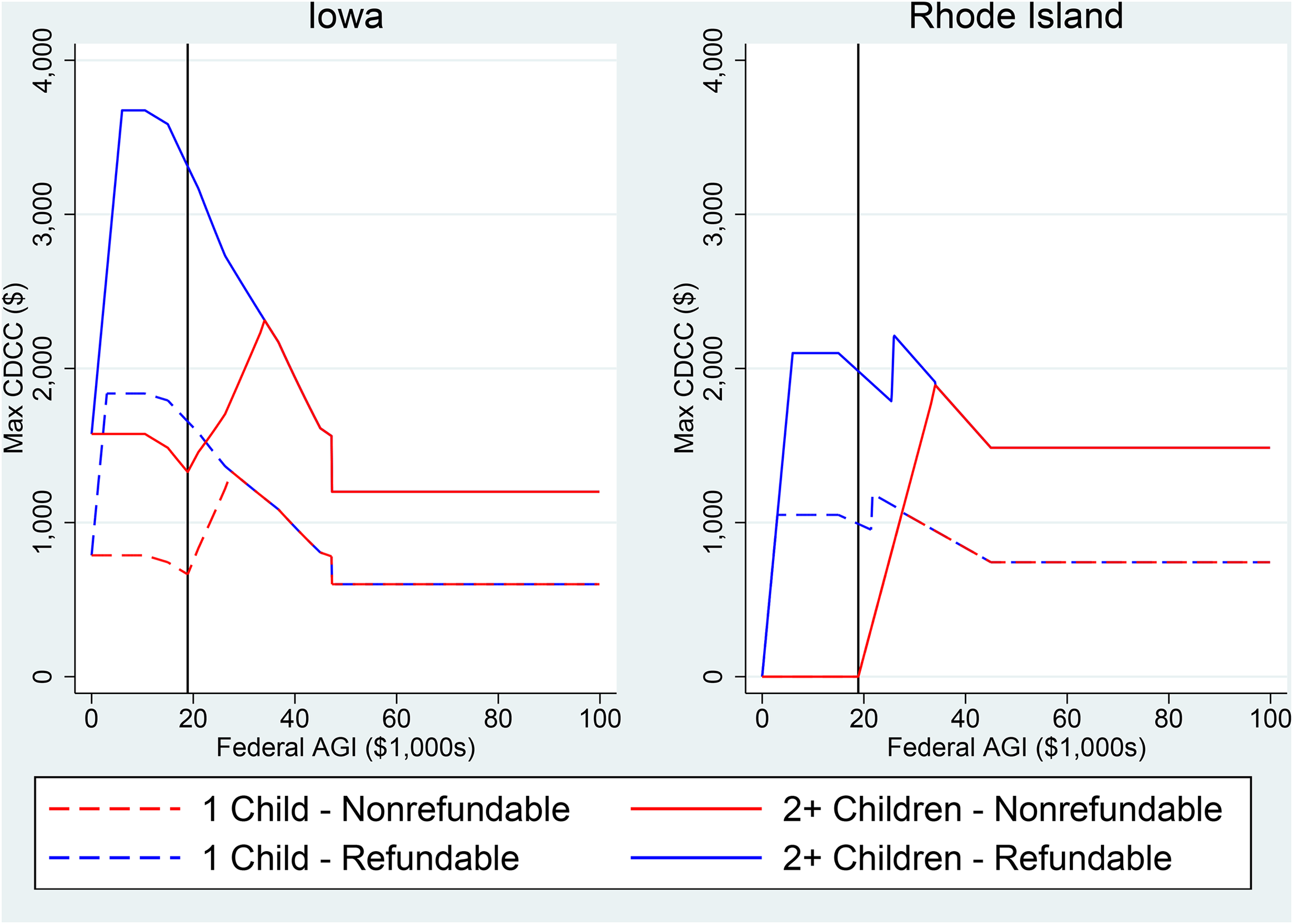

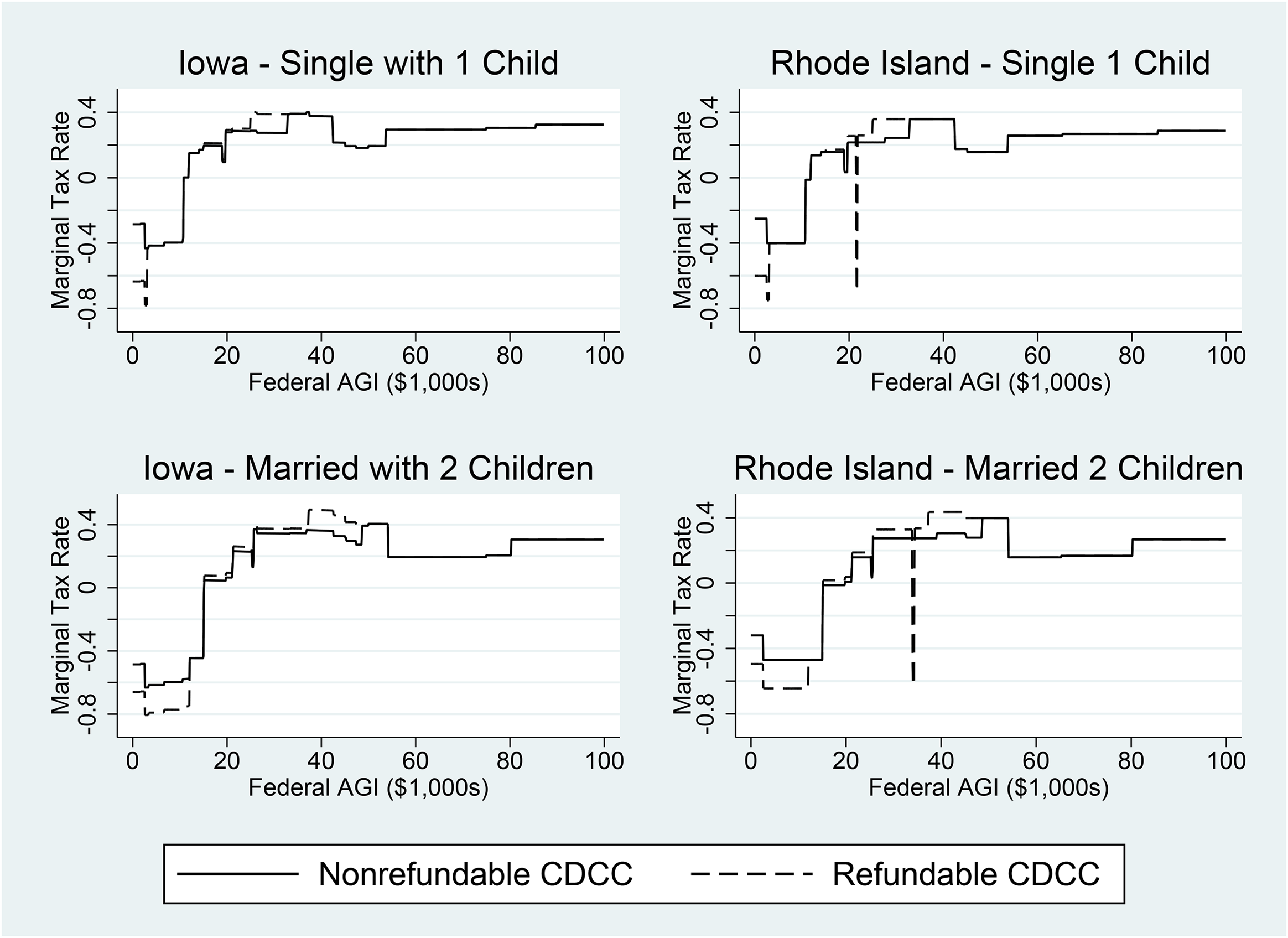

Because states with CDCC programs generally calculate their benefits as a percent of the federal credit or the child care expenses used to calculate it, making the federal CDCC permanently refundable may yield different effects on benefits and marginal tax rates across states. I therefore study effects of refundability on benefits and marginal tax rates as a consequence of both state and federal CDCCs in two states with typical state CDCC programs—Iowa, which offers a refundable credit, and Rhode Island, which offers a nonrefundable credit. 17 Specifically, Iowa’s refundable CDCC is available to taxpayers with less than $45,000 in AGI. Those with less than $10,000 in AGI receive 75 percent of the federal CDCC that they would receive if it were refundable. Benefits decrease with income for taxpayers with more than $10,000 in AGI so that those with $40,000 to $45,000 receive 30 percent of the “allowable” federal CDCC. Rhode Island’s nonrefundable CDCC is available to taxpayers regardless of income and is worth 25 percent of the federal CDCC received after accounting for nonrefundability. Given the different CDCC calculations across these two states, we would expect that making the federal CDCC refundable would not affect state benefits in Iowa but would increase state benefits for some taxpayers in Rhode Island.

The left panel of Figure 5 documents the maximum total state and federal CDCC benefit schedules for taxpayers with and without refundability in Iowa as of 2020. The figure shows that Iowa taxpayers with two or more eligible dependents and incomes too low to qualify for the nonrefundable federal credit (solid red line) still may receive over $1,500 in refundable state CDCC benefits. As expected, total CDCC benefits begin to decrease with income at $10,000 in AGI but increase once income reaches the tax filing threshold and taxpayers become eligible for the federal CDCC. Maximum total benefits peak at about $2,300 for taxpayers with $34,000 in AGI; benefits then decrease with income. In particular, benefits decrease substantially at $45,000 in AGI, where taxpayers are no longer eligible for the state CDCC.

Maximum State and Federal CDCC Benefits by Federal AGI. Notes: Left panel: Maximum state and federal CDCC benefits for households with one or two or more eligible dependents in Iowa with and without refundability as of 2020. Right panel: Maximum state and federal CDCC benefits for households with one or two or more eligible dependents in Rhode Island with and without refundability as of 2020. Source: Author’s calculations using state and federal tax forms.

If the federal CDCC were made permanently refundable, total CDCC benefits for Iowa taxpayers with two or more eligible dependents (solid blue line) would increase. As expected, the difference between the blue and red lines is completely explained by the increase in federal CDCC benefits under refundability shown in Figure 1. The panel also shows that if the federal CDCC were made permanently refundable, low-income taxpayers in Iowa could receive over $3,600 per year in total CDCC benefits. Total CDCC benefits for Iowa taxpayers with one eligible dependent are less generous, but the pattern of results is otherwise similar.

Turning to Rhode Island, the right panel of Figure 5 shows that, unsurprisingly, taxpayers without federal tax liability receive neither state nor federal CDCC benefits under the nonrefundable federal CDCC. Taxpayers with higher incomes, however, benefit from both the state and federal CDCC; total benefits for taxpayers with two or more eligible dependents peak at about $1,900 for taxpayers with $34,100 in AGI. If the federal CDCC were made permanently refundable, taxpayers with two or more eligible dependents and less than $25,500 in AGI would receive federal but not state CDCC benefits, as they do not have positive state tax liability. Total CDCC benefits then increase sharply as state tax liability increases. Rhode Island taxpayers with two or more eligible dependents and $25,700 to $34,000 in AGI experience increases in both state and federal CDCC benefits under refundability, which increases the maximum total benefit to about $2,200 at $26,000 in AGI. The pattern of results for Rhode Island taxpayers with one eligible dependent is similar.

Because increases in CDCC generosity generate complex changes in intensive margin labor supply incentives, as in section “How Would Permanent Refundability Affect Incentives?,” I examine how permanent refundability would affect marginal tax rates among taxpayers in Iowa and Rhode Island. Specifically, I simulate marginal tax rates as a consequence of state and federal individual income taxes and state and federal family tax benefits with and without refundability as of 2020 in Figure 6. The top and bottom left panels of the figure document marginal tax rates in Iowa for single parents with one eligible dependent and for married parents with two eligible dependents, respectively. The left panels show that accounting for state individual income taxes and family tax benefits yields lower marginal tax rates among very-low-income taxpayers but higher marginal tax rates among moderate-income taxpayers, relative to those shown in Figure 4. For instance, refundability increases marginal tax rates among Iowa single taxpayers with one eligible dependent and $15,000 in AGI from 0.197 (solid lines) to 0.212 (dashed lines). Similar taxpayers with about $33,000 to $42,000 face marginal tax rates around 0.40, regardless of refundability. Because a permanently refundable federal CDCC would not affect state CDCC benefits in Iowa, changes in marginal tax rates due to federal CDCC refundability are equivalent to those shown in Figure 4 for both single and married taxpayers.

Marginal Tax Rates due to State and Federal CDCC, CTC, EITC, and Individual Income Taxes. Notes: Top left panel: Marginal tax rates with respect to earnings due to state and federal CDCC, CTC, and EITC benefits and state and federal individual income taxes among single parents with one eligible dependent and no older children in Iowa with and without refundability as of 2020. Bottom left panel: Marginal tax rates with respect to the lesser earner’s earnings due to state and federal CDCC, CTC, and EITC benefits and state and federal individual income taxes among married parents with two eligible dependents and no older children in Iowa with and without refundability as of 2020. Top right panel: Marginal tax rates with respect to earnings due to state and federal CDCC, CTC, and EITC benefits and state and federal individual income taxes among single parents with one eligible dependent and no older children in Rhode Island with and without refundability as of 2020. Bottom right panel: Marginal tax rates with respect to the lesser earner’s earnings due to state and federal CDCC, CTC, and EITC benefits and state and federal individual income taxes among married parents with two eligible dependents and no older children in Rhode Island with and without refundability as of 2020. Source: Author’s calculations using TAXSIM and state and federal tax forms.

Similarly, the top and bottom right panels of Figure 6 characterize marginal tax rates for single taxpayers with one eligible dependent and married taxpayers with two eligible dependents in Rhode Island. The right panels show that at low income levels, accounting for state individual income taxes and family tax benefits largely does not affect marginal tax rates. Given that low-income taxpayers do not benefit from Rhode Island’s CDCC, it is unsurprising that, among taxpayers with less than about $20,000, changes in marginal tax rates under a refundable federal CDCC are equivalent to those depicted in Figure 4. The sharp increase in state CDCC benefits as Rhode Island taxpayers begin to have positive state tax liability and to receive state CDCC benefits shown in Figure 4, however, generates a substantial decrease in marginal tax rates for taxpayers within a small income bin. Specifically, the marginal tax rate among single taxpayers with one eligible dependent and about $21,500 in AGI decreases from 0.22 to

Figures 5 and 6 imply that in states with refundable CDCCs, making the federal CDCC permanently refundable is unlikely to change state CDCC benefits or to differentially affect incentives. In states with nonrefunable CDCCs, making the federal CDCC permanently refundable may lead to small increases in state CDCC benefits. Discontinuities in the total CDCC benefit schedule under federal CDCC refundability also could generate sharp decreases in marginal tax rates for some taxpayers. For most taxpayers, however, changes in marginal tax rates are likely to remain similar when accounting for state individual income taxes and family tax benefits.

Conclusion and Discussion

In this paper, I show that making the CDCC permanently refundable would increase eligibility and benefits among low-income taxpayers. Refundability would lead to particularly large increases in eligibility among Black and Hispanic households, which are relatively unlikely to qualify for the nonrefundable CDCC. Turning to intensive margin labor supply incentives, refundability would decrease marginal tax rates with respect to income among very-low-income taxpayers. Moderate-income taxpayers would experience small increases in marginal tax rates with respect to income but decreases in marginal tax rates with respect to child care expenditures.

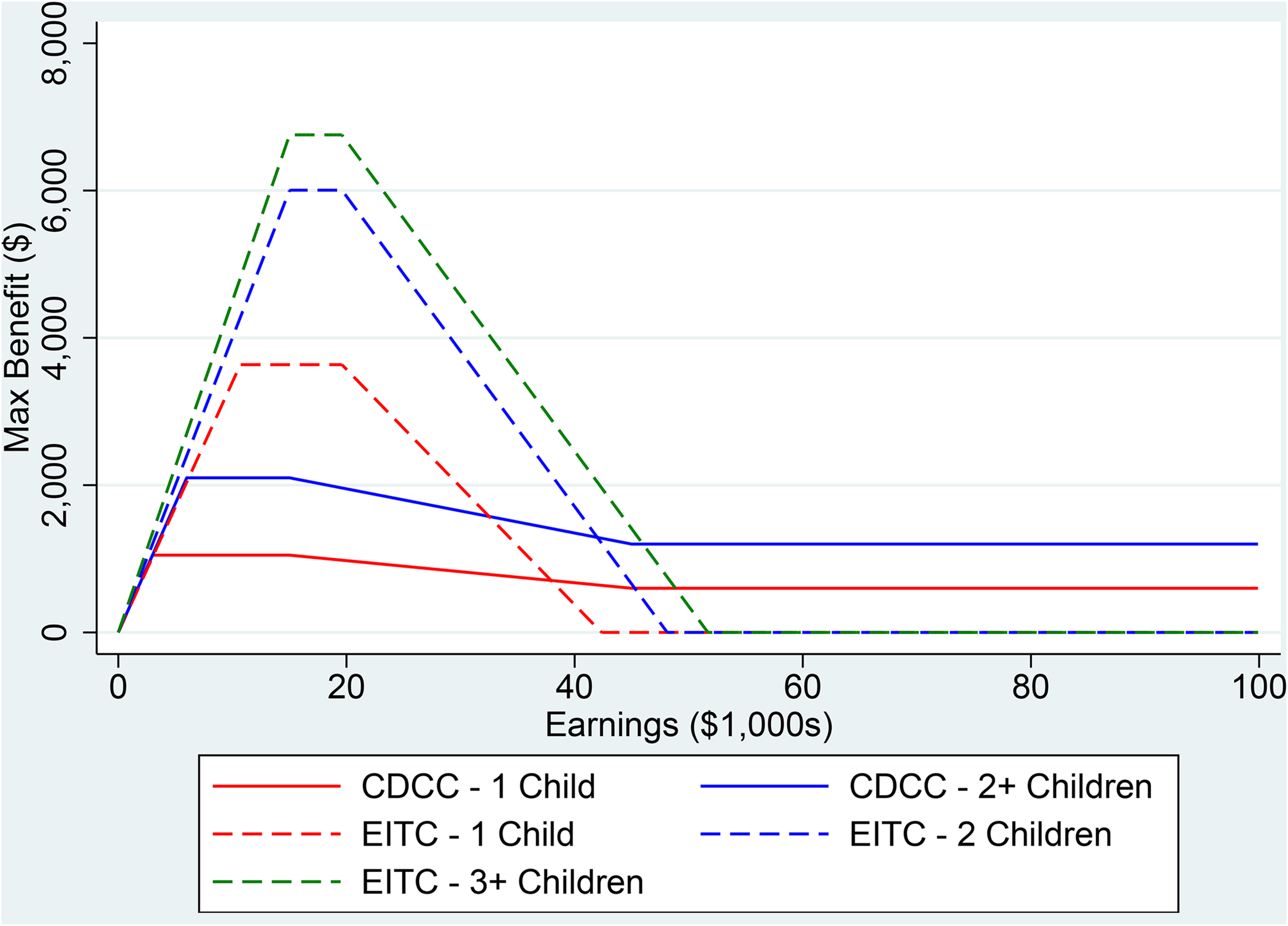

Making the CDCC permanently refundable would make the credit more similar to the EITC by transferring income toward low-income working families, though unlike the EITC, the CDCC would promote paid child care spending. Figure 7 compares the maximum refundable CDCC and EITC benefit schedules as of 2020 for households with one, two, and three or more children by AGI. While EITC benefits are more generous, refundable CDCC and EITC benefits phase in at similar rates for low-income households. The refundable CDCC phases out at a much lower rate relative to the EITC (and never phases out completely), though the CDCC’s maximum plateau and phase-out regions begin at lower income levels. More specifically, for households with two or more children, the EITC phase-out rate (0.21) is considerably higher than both the refundable CDCC phase-out rate (0.03) and the average marginal tax rate increase among households currently on the phase-in and phase-out/plateau regions of the nonrefundable CDCC (0.02).

Maximum Refundable Federal CDCC and EITC Benefits by Earnings. Notes: Maximum refundable federal CDCC and EITC benefits for households with one, two, and three or more children as of 2020. Source: Author’s calculations using federal tax forms.

Despite relatively high marginal tax rates in the phase-out region of the EITC, researchers show that EITC benefits increase work participation among single mothers (Eissa and Liebman 1996; Hoynes and Patel 2018; Keane and Moffitt 1998; Meyer and Rosenbaum 2001; Michelmore and Pilkauskas 2021) and that decreases in labor supply among taxpayers on the phase-out region are relatively small (Chetty, Friedman, and Saez 2013). Hence, evidence from research on the EITC, along with the relatively small increases in marginal tax rates due to refundability shown in Table 3, suggests that making the CDCC permanently refundable would increase work among low-income parents who are willing to pay for child care. 18 Evidence that increases in CDCC generosity increase paid child care use (Miller and Mumford 2015; Pepin 2020) corroborates the idea that a permanenty refundable CDCC likely would increase both work and child care spending among low-income parents.

In addition to affecting taxpayers, CDCC benefit increases under refundability would increase tax expenditures. Results from Table 3 suggest that if all households with benefit increases were to claim the CDCC, making it permanently refundable would increase tax expenditures annually by about $800 million, all else equal. 19 This constitutes a 22 percent increase in CDCC spending compared to that during the late 2010s. Although an $800 million increase in spending is considerable relative to recent years, it would restore real tax expenditure levels that have decreased over time, as the CDCC is not indexed to inflation (Internal Revenue Service 2021). Of course, under budget neutrality, policymakers must consider whether the benefits of making the CDCC permanent refundable outweigh budget cuts to other programs.

One limitation of the current study is that it does not take into account effects of increases in CDCC benefits on child care prices. Existing research demonstrates that a substantial proportion of CDCC benefits are passed through in the form of higher child care prices (Rodgers 2018, 2021). In particular, Rodgers (2021) uses changes in the refundability of California’s CDCC to estimate that child care prices capture about half of households’ increased benefits. Any such increases in prices would effectively diminish additional benefits that low-income households receive under refundability.

As I describe changes in outcomes that arise solely from changes in tax policy, additional research is needed to understand how increases in eligibility and benefits would affect taxpayers’ labor supply and paid child care use. Future research also may examine how CDCC benefits lead parents to substitute across various types of child care arrangements, such as parental care, informal unpaid care, informal paid care, and paid formal care. Because decreases in the cost of formal care tend to benefit the human capital development of children from disadvantaged households only (Baker, Gruber, and Milligan 2008; Havnes and Mogstad 2011; Kottelenberg and Lehrer 2017), permanent refundability may promote the child development of low-income children without deterring that of their higher-income counterparts. Characterizing the extent to which increases in CDCC generosity among low-income taxpayers induce parents to pay for child care and to enter the labor force, as well as how those actions affect children’s outcomes, will allow policymakers to better understand the costs and benefits of permanent refundability.

Footnotes

Acknowledgements

I thank Jing Cai for excellent research assistance and Stacy Dickert-Conlin, William Gentry, Priscillia Hunt, Nathalie Mathieu-Bolh, Katherine Michelmore, Barra Roantree, Bryce VanderBerg, David Vitt, Luke Watson, and seminar participants at Georgetown University, the W.E. Upjohn Institute for Employment Research, the EEA Annual Conference, the NTA Annual Conference, the WEAI Annual Conference, and the WEAI International Conference for helpful comments and suggestions.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.