Abstract

This systematic review examines pedagogical approaches in global youth financial education. Eligibility followed five criteria: population (youth in formal education), intervention (explicit pedagogical methods or teaching activities), design (empirical research or case studies), language (French/English), and source (peer-reviewed articles, proceedings, or reports). Data were sourced from Web of Science, Scopus, and ERIC (last consulted in August 2025). Quality was assessed by two reviewers, with thematic synthesis presented in a summary table. Cohen's Kappa Coefficient (0.71) was applied to ensure inter-rater reliability. The selection process, illustrated in a PRISMA flowchart, yielded 44 studies. Each is characterized by author(s), year, country, population (kindergarten through university), sample size, program name, and intervention duration (15 min–3 years). Experiential learning appears to be the most common pedagogical approach. A key limitation is insufficient reporting of pedagogies, often requiring deduction from activity descriptions and limiting effectiveness analysis. This review calls for embedding metacognitive strategies and creative collaboration into financial education,and for future research to operationalize and assess creative competencies within specific pedagogical frameworks.

Background

As the classic adage goes, “money is a good servant but a bad master.” Financial education precisely aims to reverse this dynamic of subordination by equipping each individual with the necessary capabilities to become an enlightened strategist of their own resources. According to its definition (World Bank Group, 2014, P1), financial education seeks to improve the understanding of financial concepts and products, develop the skills and confidence needed to identify risks and opportunities, and foster the adoption of informed decisions to enhance financial well-being.

Financial literacy can thus be defined as the mastery of a set of fundamental competencies covering the key domains of economic life: generating income, managing expenses, using credit, saving, and investing(Manz, 2011).This mastery rests on four interdependent pillars: (1) conceptual and institutional knowledge of the financial system; (2) numerical and mathematical skills applied to financial calculations; (3) the capacity for self-regulation and discipline in decision-making; and (4) a form of practical intuition or judgment in the face of financial situations (Manz, 2011).

This intuitive judgment assumes heightened significance within a global landscape characterized by

Consequently, the adoption of creative and innovative cognitive and strategic approaches emerges as an indispensable imperative for navigating this inherently unpredictable and uncertain reality.

Conceptually, creativity is defined as “the production of a response, product, or solution that is novel and appropriate to an open-ended task over time…It must be valuable, correct, feasible, or somehow fitting to a particular goal”(Amabile, 2013). It constitutes a meta-skill, encompassing the capacity for persistent critical inquiry and the application of novel frameworks to confront challenges, thereby generating innovative solutions across diverse fields of application(Saliceti, 2015). Within the domain of personal finance, this capability is operationalized as the strategic navigation of constraints imposed by adverse economic climates. This may involve identifying and pioneering novel, salutary pathways—for instance, through the adaptive reconfiguration of savings mechanisms or investment strategies. Cultivating such a creative financial mindset facilitates the exploration of new horizons, promotes divergent thinking, and, fundamentally, contributes to the development of a resilient personal temperament equipped to engage in calibrated and reasoned risk-taking (Gardner, 2007).

The imperative for targeted financial education is especially pronounced among youth, a demographic characterized by heightened vulnerability to financial risks. Over-indebtedness constitutes a significant threat to both individual welfare and broader societal stability (Amagir et al., 2018). Empirical evidence, such as that from the EOS Study (EOS Solutions, 2023), indicates a tangible manifestation of this risk, with 20% of individuals aged 18 to 34 reporting recent debt accumulation. As a substantial and influential consumer segment, young people possess a need for financial guidance commensurate with that of adult populations (Romagnoli and Trifilidis, 2013). This rationale supports the OECD's policy recommendation (World Bank Group, 2014) for the early introduction of financial literacy instruction, ideally preceding active financial agency (Lusardi et al., 2009). The formal education system serves as the optimal conduit for this intervention, capitalizing on a developmental stage of maximal cognitive receptivity (Romagnoli and Trifilidis, 2013).

Consequently, the integration of financial education into national school curricula has become a widespread policy initiative. Empirical studies demonstrate that such programs effectively enhance financial literacy among young learners (e.g., (Amagir et al., 2018); Bruhn et al., 2013; Mancone et al., 2024; Peng et al., 2007).

Recent scholarly reviews have undertaken global examinations of these programs’ content and pedagogical delivery. Amagir et al.'s (2018) systematic review concluded that most interventions yielded significant short-term improvements in students’ financial knowledge and attitudes, notably self-efficacy (

The present systematic review examines youth financial education programs across international contexts and explores the extent to which their pedagogical approaches may be considered creativity-oriented. The study is guided by the following research question: Which pedagogical approaches are most commonly employed in youth financial education worldwide?

Method

As this study constitutes a systematic review, the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) guidelines (Moher et al., 2009) were applied to the corpus to determine the final article selection.

Eligibility criteria

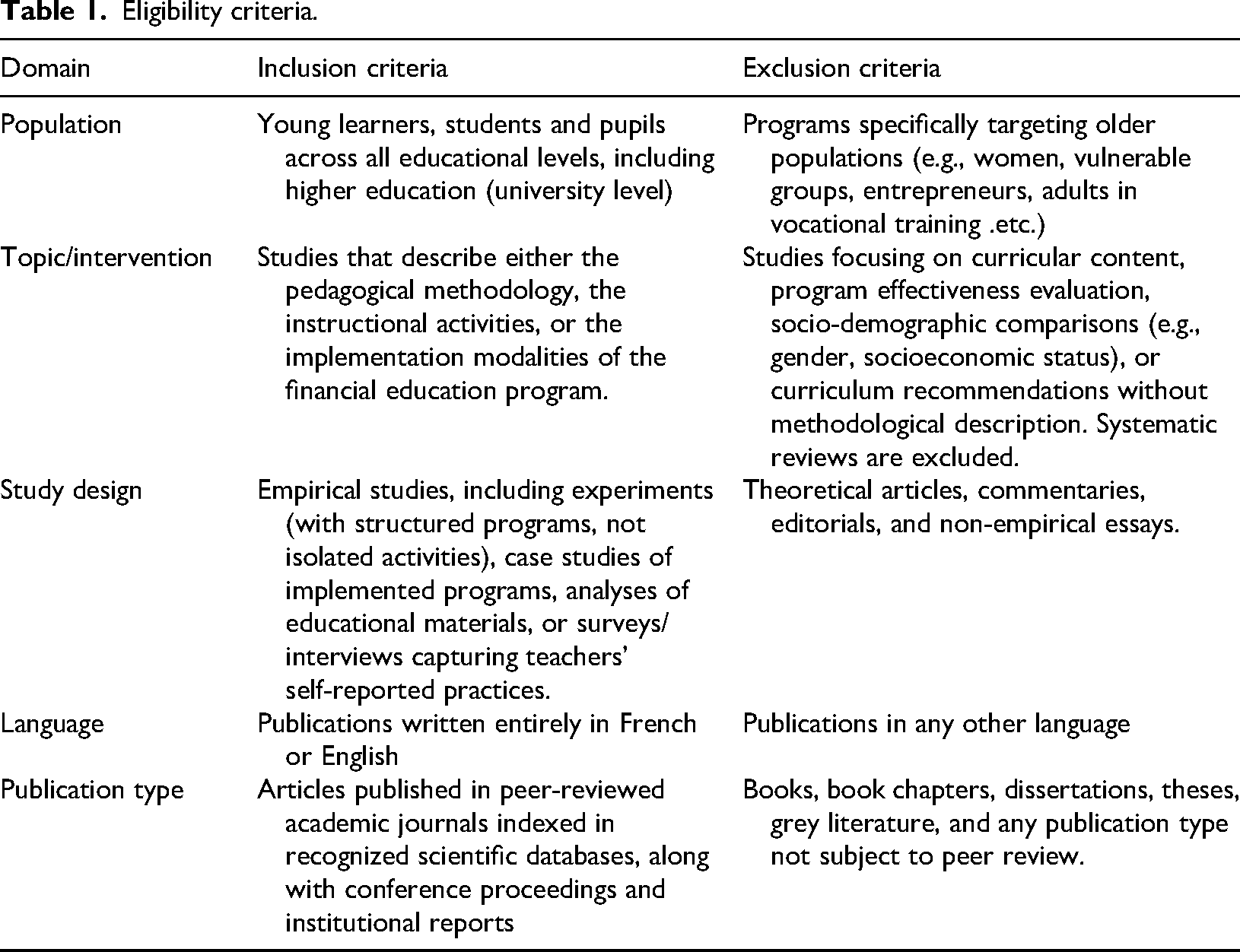

The assessment of study eligibility was based on a five-dimensional analytical framework. First, the population criterion delimited the corpus to young learners across all levels of formal education, including higher education, thereby excluding programs targeting other populations such as women, entrepreneurs, or adults in vocational training. Second, the thematic/intervention domain required that studies explicitly describe either the pedagogical methodology, teaching activities, or concrete modalities of implementing financial education programs, which excluded works limited to content analysis, impact evaluation, or curriculum recommendations without operational reference. Third, the study design prioritized empirical research, including structured experiments, case studies, analyses of pedagogical materials, and surveys or interviews capturing teachers’ self-reported practices, while excluding theoretical articles, editorials, and non-empirical essays. Fourth, the language criterion restricted the selection to publications written entirely in French or English. Finally, the publication type was limited to articles in peer-reviewed journals indexed in recognized scientific databases, as well as conference proceedings and institutional reports, excluding books, book chapters, theses, and grey literature. This set of criteria was designed to ensure a rigorous, reproducible selection aligned with the methodological standards of systematic reviews (Table 1).

Eligibility criteria.

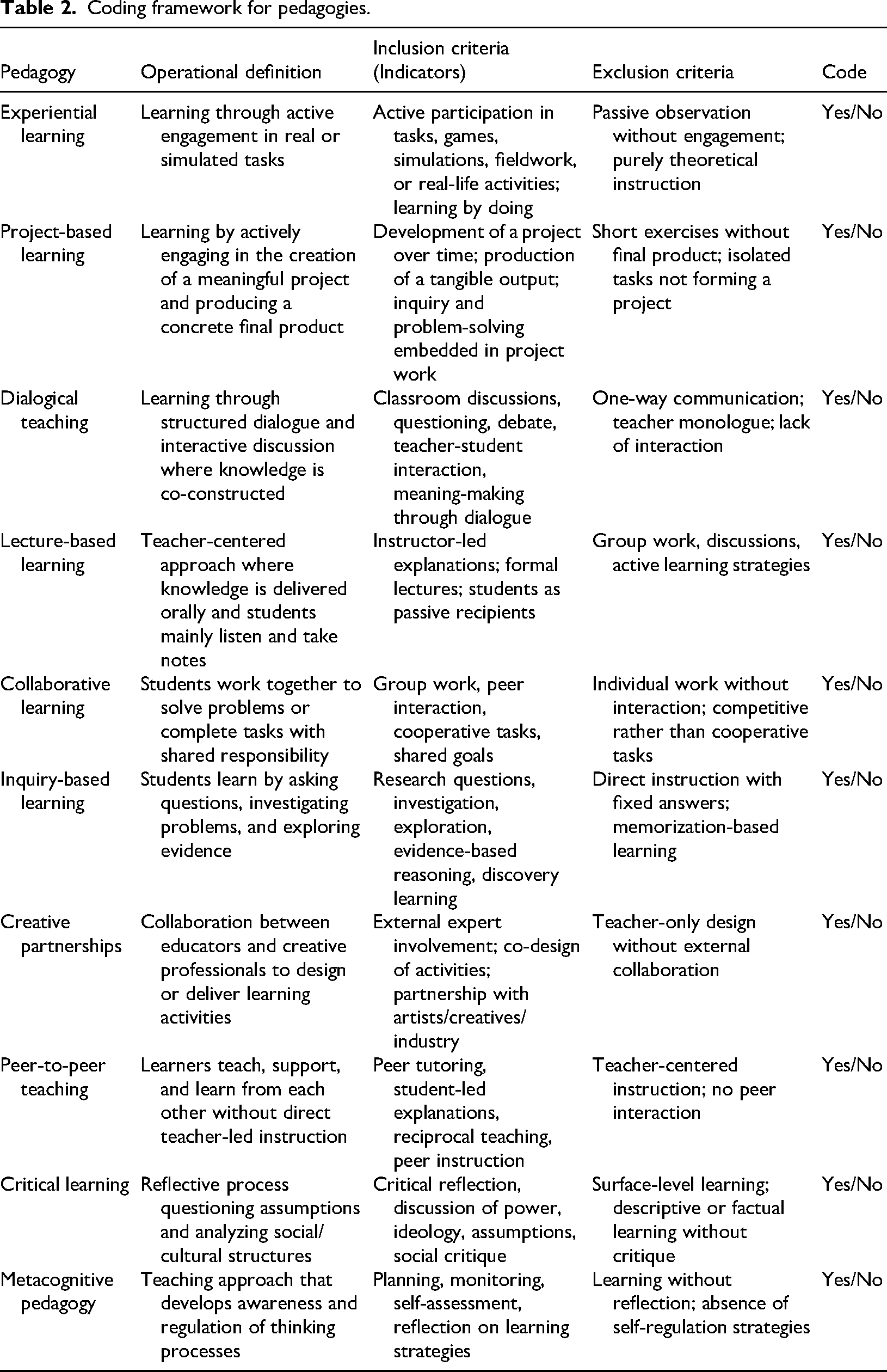

The study selection procedure was conducted in several stages. An initial screening was performed based on an analysis of titles and abstracts, followed by the classification of references according to their source database. The publications thus identified were then subjected to a thorough review, leading to their categorization into two distinct sets: included studies and excluded studies. Finally, the selected articles underwent a meticulous analytical reading to extract the relevant data. To this end, both reviewers used a coding framework (Table 2) that specified the decision's rules applied throughout the coding process.

Coding framework for pedagogies.

Information sources

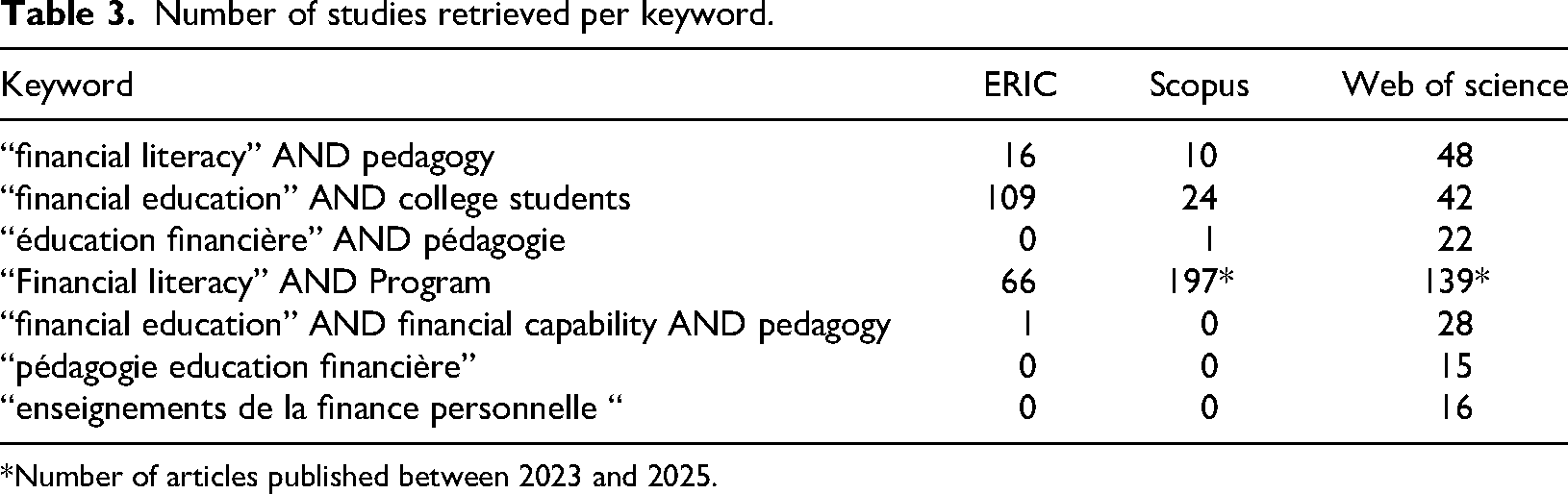

This process was applied to the literature identified through a systematic search conducted across three bibliographic databases: ERIC, Web of Science, and Scopus.

The search strategy employed seven keyword combinations, formulated in both English and French to capture relevant literature in both languages. The search terms were as follows: “financial literacy” AND pedagogy, “financial education” AND college students, “éducation financière” AND pédagogie, “financial literacy” AND program, and “financial education” AND financial capability AND pedagogy (Table 3).

Number of studies retrieved per keyword.

*Number of articles published between 2023 and 2025.

Cohen's Kappa coefficient per pedagogy.

To further enrich the study corpus, 17 articles cited in Amagir et al. (2018), which were deemed relevant, were also included before removing the duplicates from the corpus.

The identification and selection of relevant studies from the bibliographic databases were carried out between July and August 2025.

Search strategy

To ensure the accessibility and reproducibility of sources, the search was limited to documents indexed within these databases. The majority of identified references were available through open access. An exception was granted for the ERIC database solely because our institutional access at the time included its limited-access collection of Taylor & Francis articles, which was deemed a valuable addition to the research corpus.

No date restrictions were applied to the majority of search queries. However, for the search combining the terms “Financial Literacy” AND “Program” in the Web of Science and Scopus databases, the publication period was limited to the years 2023 to 2025. The differentiated application of the search criteria was intended to optimize the document selection process. The keyword combination “Financial Literacy” AND “Program” yielded a large number of references, many of which were not directly related to the research theme. A chronological filter was therefore applied to narrow the results to a more recent and relevant body of literature. In contrast, the other keyword combinations produced fewer and more focused publications, making additional temporal restrictions unnecessary.

Selection process

The study selection and eligibility screening were conducted by 2 reviewers. For each record, an initial screening of titles and abstracts was performed, followed by a full-text review of all potentially relevant articles. During the full-text assessment, the reviewers examined the methodology and results sections of each publication to identify either explicit pedagogical approaches, teaching activities, or program implementation details. If the required information was not sufficiently detailed in these sections, the introduction and discussion were consulted to locate relevant indicators. Articles that did not meet all pre-defined eligibility criteria or that corresponded to an exclusion criterion were subsequently removed from the corpus. Cohen's Kappa coefficient was calculated (0,74) to assess inter-rater reliability between the two reviewers, with separate Kappa values computed for each pedagogy and an overall score obtained by averaging these values across all pedagogies.(Table 4)

Data collection process

Data extraction was conducted following the same manual and unidirectional protocol as the study selection. For each included publication, an in-depth analysis of the full text was carried out to systematically extract relevant information, with a primary focus on the sections detailing methodology and results to identify pedagogical practices, learning activities, and program operational modalities. If these elements were not explicitly described, the introduction and discussion sections were examined to infer the missing indicators (Table 2). This process was independently carried out by two reviewers. In line with the overall methodology, this work was performed without the use of automation tools.

Data items

Data extraction focused on two predefined outcomes aligned with the research question. The first concerns pedagogical approaches, understood as teaching methods either explicitly identified by the authors or inferred from the learning activities described. The second dimension is related to pedagogical tools, encompassing digital, material, or documentary resources used as mediating instruments in the learning process.

The extraction process did not aim to catalogue every occurrence within each study. Instead, hierarchical selection principles were applied to retain information that was analytically salient and conceptually coherent. For pedagogical approaches, explicit labeling (e.g., project-based learning) constituted the primary data source; when absent, inferences were drawn from the nature of learner tasks, based on the assumption that instructional design reflects underlying pedagogical orientations. By contrast, the identification of tools required little interpretation, as these were generally clearly named and enumerated in the studies.

Data was extracted through a close analytical reading of the full texts rather than by means of a standardized extraction grid. The retained information was subsequently subjected to an interpretive qualitative synthesis. Extraction was intentionally limited to the two core variables of interest; contextual or descriptive study characteristics—such as participant profiles, intervention length, funding sources, or geographic setting—were not systematically collected, as they lay beyond the scope of the present methodological focus.

The methodological assessment employed a qualitative critical appraisal focused on clarity of objectives, specificity of pedagogical description, and soundness of analysis. Cohen's Kappa coefficient was employed to assess inter-rater reliability. As a qualitative review, no quantitative effect measures—such as effect sizes—are reported; instead, findings are synthesized thematically and presented in a summary table and narrative form. The synthesis integrated all eligible studies into a unified thematic analysis based on two predefined categories: pedagogical approaches and tools. Results are conveyed through a descriptive table, summary table, a frequency chart, and an interpretive narrative. Heterogeneity was examined qualitatively rather than statistically, with interpretations reinforced through predefined extraction criteria and iterative re-evaluation. Thematic saturation was achieved when additional studies no longer produced new substantive categories. Confidence in the evidence is supported by the exclusive use of peer-reviewed literature and the observed richness, coherence, and recurring patterns across the included studies, indicating a comprehensive and reliable mapping of pedagogical practices in financial education.

Results

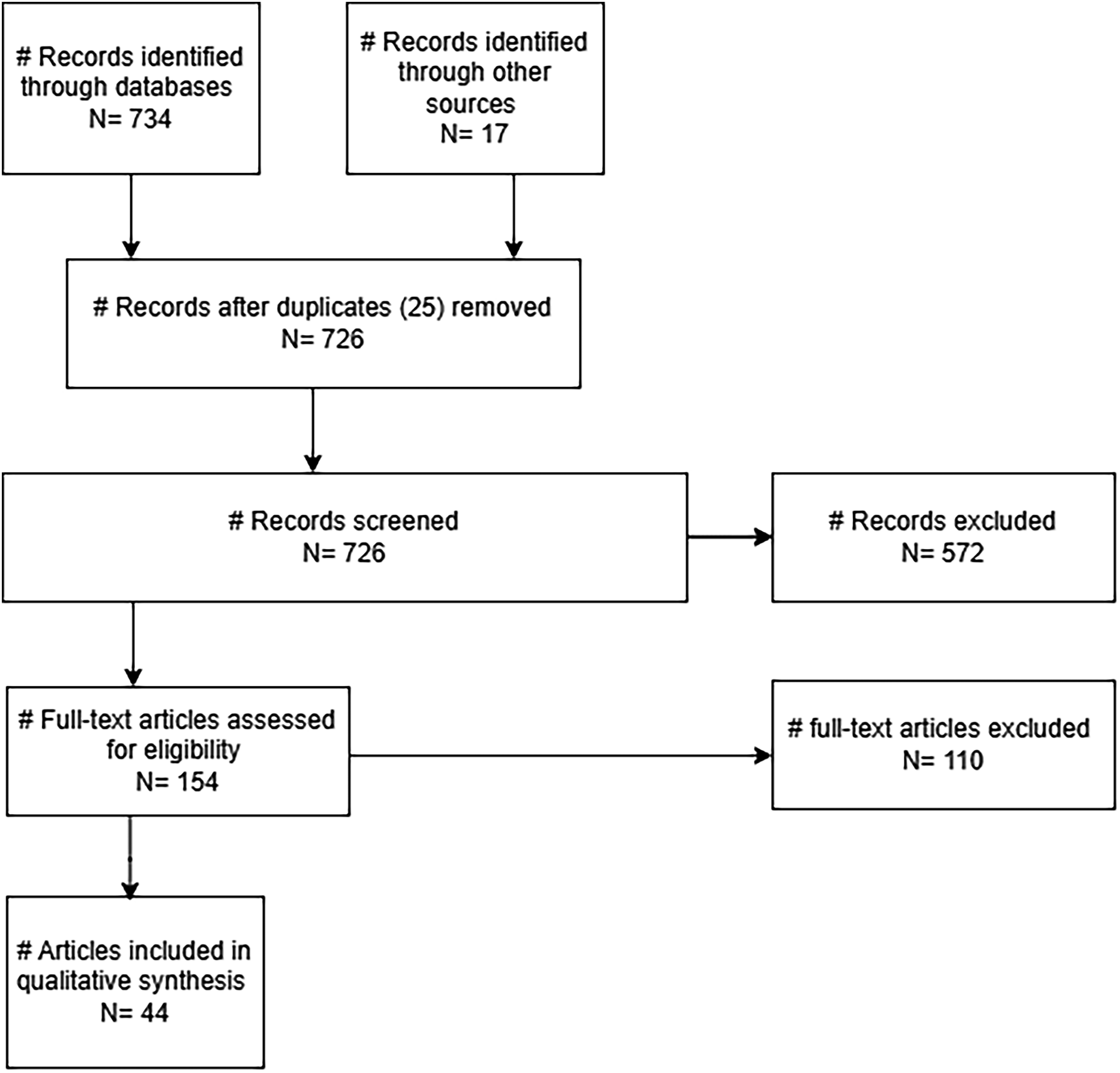

The literature search was conducted across three electronic databases. This initial search yielded a total of 734 records. In addition, 17 further records were identified through manual screening of the reference lists of a key article by Amagir et al. (2018). Overall, 751 records were identified for potential inclusion.

Following the removal of duplicates (25), the remaining records (709) were screened based on their titles and abstracts. Studies that did not meet the predefined inclusion criteria were excluded at this stage (see Table 1). Full-text screening was subsequently performed for the remaining articles to assess their eligibility. Articles were excluded when they did not provide any information on the study variables, despite appearing to be relevant to the scope of the review at first screening. As a result of this selection process, a total of 44 studies met the inclusion criteria and were retained for the qualitative synthesis. The study selection process is summarized in Figure 1 using a PRISMA flow chart.

Flow chart prisma.

Several studies initially appeared to meet the inclusion criteria based on their thematic focus on financial education or related programs but were ultimately excluded after full-text assessment due to misalignment with the analytical objectives of this review.

For instance, (Bužienė, 2024) was initially considered eligible because the study compared multiple financial education programs and employed a SWOT analysis, which suggested a potential focus on pedagogical approaches. However, a closer examination revealed that the analysis primarily addressed program effectiveness and structural characteristics, with only cursory and non-analytical references to teaching methods. As the study did not provide sufficient detail on pedagogical practices, it was excluded.

Similarly, (Sherraden et al., 2011) were excluded because their analysis focused predominantly on socio-economic and contextual determinants of financial education outcomes, without offering empirical indicators or descriptions of how instructional content was delivered or how learning activities were structured.

The study by Phillips and Kiracofe (2023) was also excluded, as data collection was limited to interviews with school representatives and did not examine specific educational programs or classroom practices. Consequently, it did not allow for the identification or analysis of pedagogical approaches or instructional tools.

Other studies, including Kamarudeen and Vijayalakshmi (2023), Marin and Notargiacomo (2021) Romagnoli and Trifilidis (2013), Lührmann et al. (2012), and Cavalcante (2025) were excluded for similar reasons. Although these studies addressed financial education or related interventions, they primarily evaluated outcomes, policy frameworks, or participant characteristics, rather than providing a sufficiently detailed account of pedagogical methods, creative processes, and instructional tools relevant to the objectives of the present review.

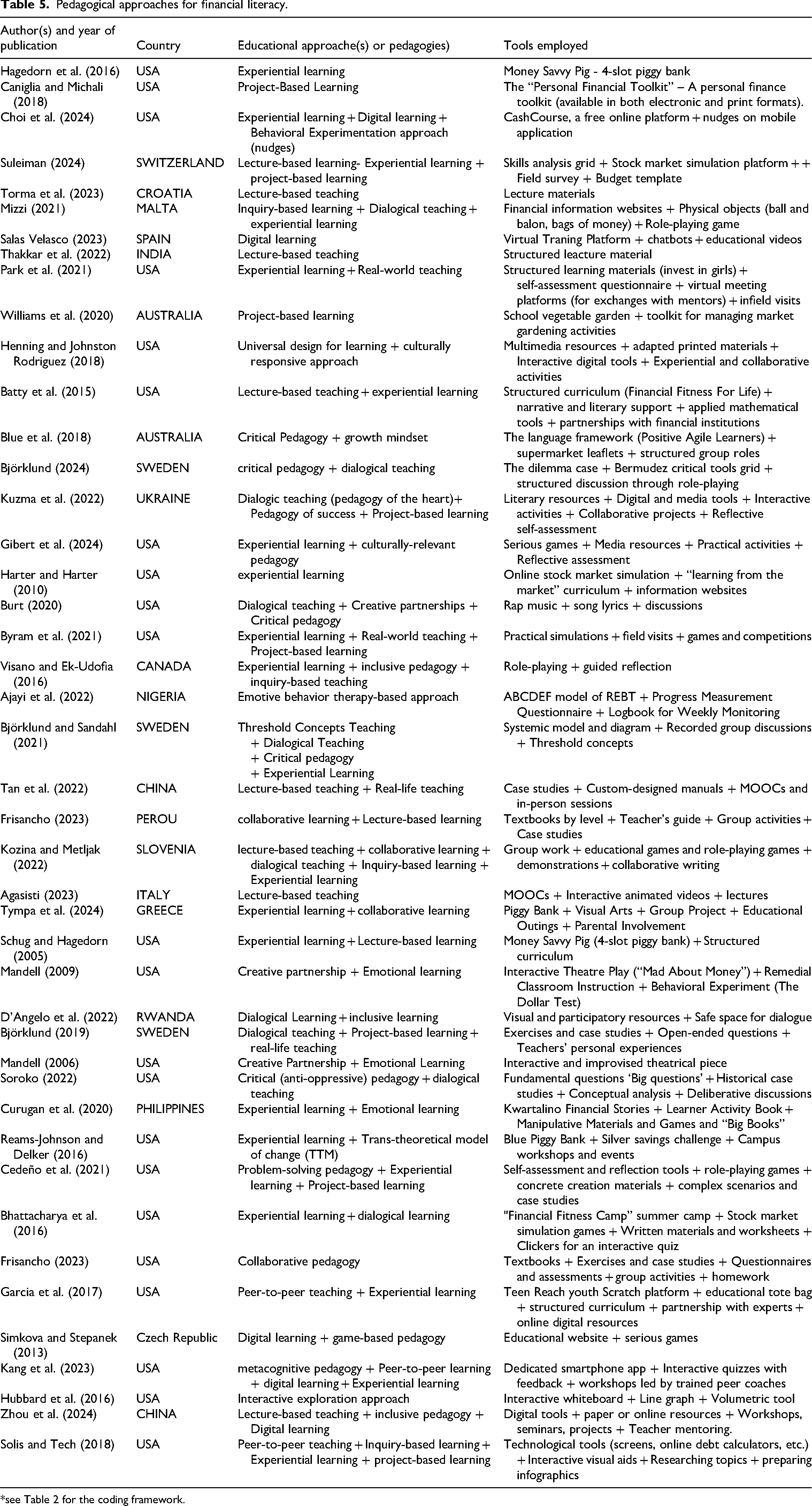

The included studies were described in terms of the pedagogical approach and tools in Table 5.

Pedagogical approaches for financial literacy.

*see Table 2 for the coding framework.

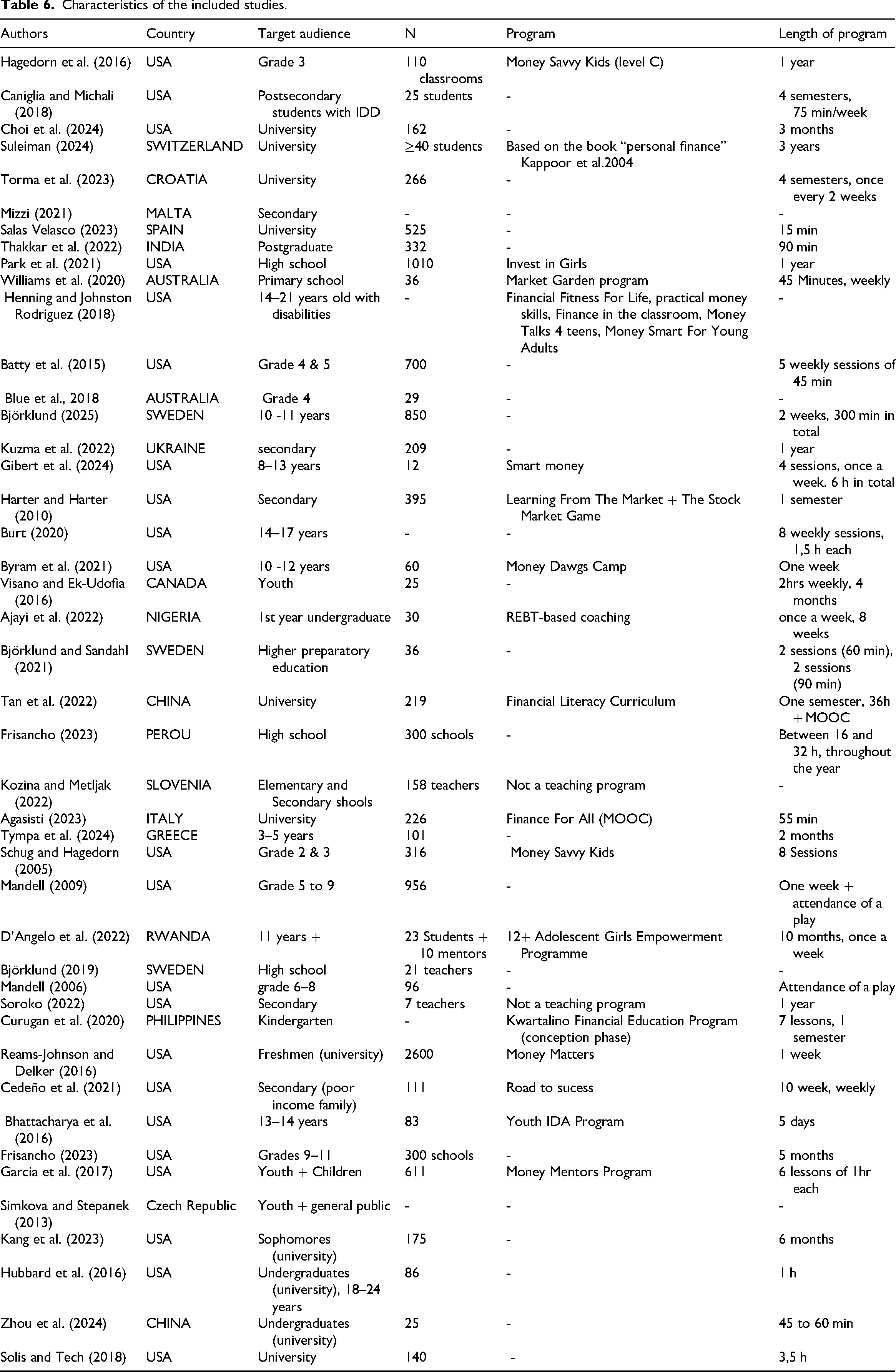

The main characteristics of the included studies are summarized in Table 6. Each study is cited and described in terms of its author(s), year of publication and country. The table provides, for each included study, the target population, participant count, program name (where applicable), and intervention duration.

Characteristics of the included studies.

Educational approaches and pedagogies employed in youth financial education programs

Prior to analysis, key definitions are required. Durkheim (2012) defines education as deliberate adult action on the young. Pedagogy is the academic study of this action. Didactics concerns content transmission; pedagogy manages the classroom, didactics the curriculum (Tasra, 2017) Etymologically, pedagogy means “to lead the child.” Mialaret (1991) defines it as a reflection on education's aims and conditions, a distinct subset of educational sciences.

Of the 44 studies reviewed, geographic distribution spanned 19 countries, with a strong U.S. predominance and a notable absence of MENA region states. This omission aligns with the latest PISA financial literacy survey, which included only two Arab countries (UAE and Saudi Arabia) out of 20 participants.(OECD, 2024) The absence may reflect either limited government interest in financial education or the prioritization of other policy areas.

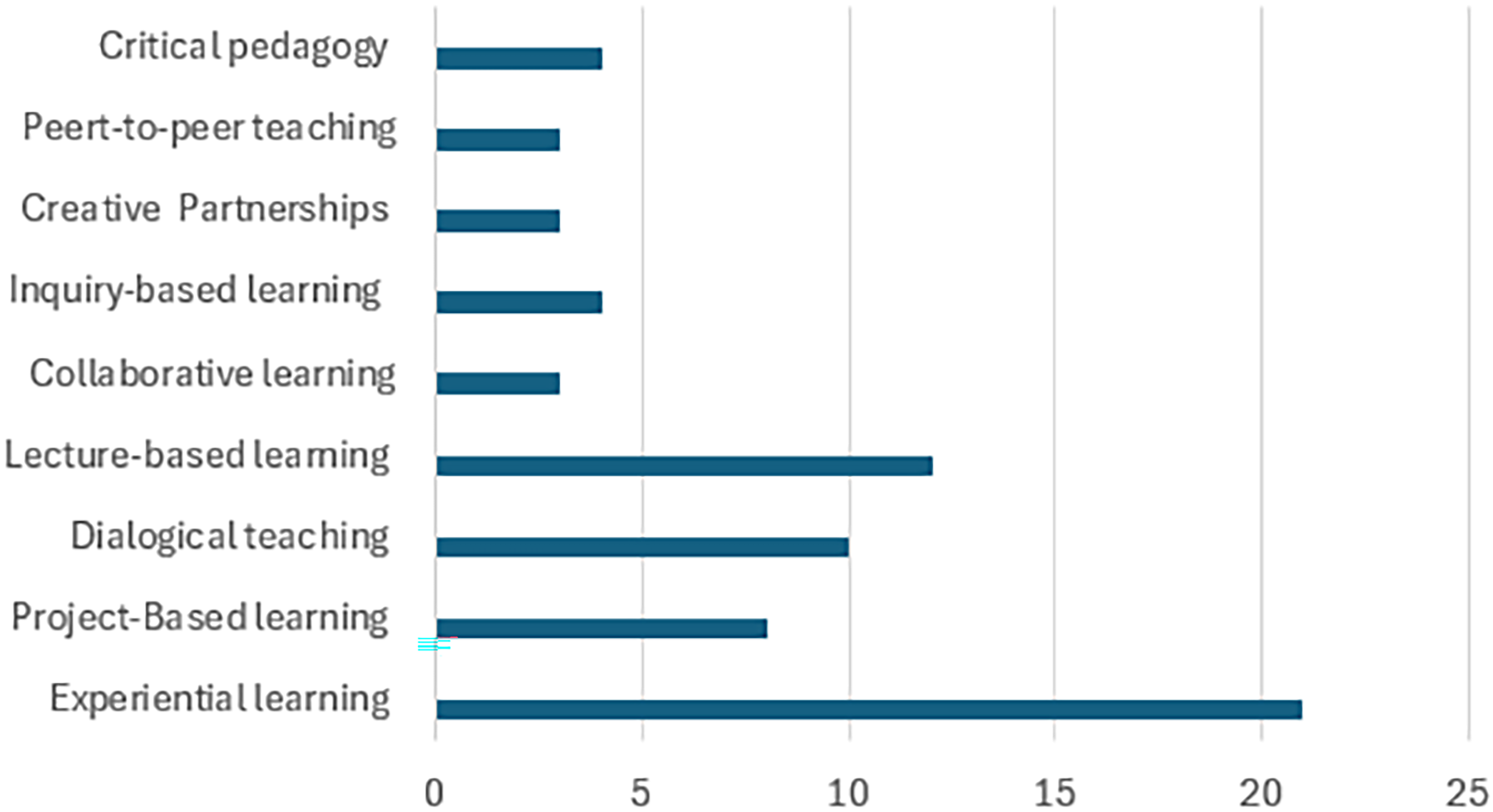

This study analyzes pedagogical approaches fostering learner creativity. From 44 studies, 34 distinct approaches were identified; eight received recurrent attention (≥3 studies). Four are “signature pedagogies for creativity”(Vincent-Lancrin et al., 2020), including inquiry-based learning, project-based learning, creative partnerships, and dialogic teaching. Analysis focuses on these. However, experiential learning—the most common approach in Financial Education—(Figure 2)is not inherently creativity-fostering (Vincent-Lancrin et al., 2020).

Frequency of use of different pedagogical approaches in financial literacy teaching.

Creative partnerships

The Creative Partnerships approach entails structured collaboration between cultural entities and educational institutions to embed external resources into pedagogy, positioning creativity at the core of learning (Vincent-Lancrin et al., 2020). It fosters social, cognitive, emotional, and creative competencies, promotes curiosity-driven inquiry, collaborative work, communication (Europeen Union, 2014), project management, and motivation—a key component of creative learning (Mc Lellan et al., 2012) while enhancing self-confidence and decision-making autonomy (Thomson et al., 2012).

Despite its theoretical relevance, this model appears in only three empirical studies within our corpus (Burt, 2020; Mandell, 2006, 2009). Its applications—such as rap-based interventions (Burt, 2020) and theater-based financial education programs (Mandell, 2006, 2009)—suggest positive effects on knowledge acquisition but limited or inconsistent behavioral impact. Overall, creative partnerships appear promising but empirically underdeveloped and highly context-dependent.

Project-based learning

Project-based learning is an active, learner-centered method based on learning by doing (Reverdy, 2013). Students, often in teams, solve problems by creating tangible products and developing disciplinary knowledge and project-management skills. Its core features include a driving question, clear objectives, inquiry, collaboration, technological tools, and an artifact(Markula and Aksela, 2022). It promotes interdisciplinarity by integrating diverse knowledge within realistic contexts (Zhang and Ma, 2023). A cross-study analysis of the corpus reveals that Project-based learning is primarily used as a mechanism for situating financial literacy within realistic and applied contexts. It supports the integration of interdisciplinary knowledge and promotes the transfer of learning to complex, real-world situations (Zhang and Ma, 2023). In this sense, this approach functions less as a narrowly defined instructional technique and more as an overarching pedagogical architecture that enables contextualized and applied learning.

Empirically, this approach appears seven times in the corpus (Björklund, 2019; Byram et al., 2021; Caniglia and Michali, 2018; Cedeño et al., 2021; Kuzma et al., 2022; Solis and Tech, 2018; Williams et al., 2020) with implementations ranging from financial portfolio construction tasks (Caniglia and Michali, 2018) to applied school-based projects such as managing a school garden economy (Williams et al., 2020). Despite this diversity of applications, a common pattern emerges: Project-based learning is consistently mobilized to connect abstract financial concepts to concrete, situated experiences, thereby enhancing learner engagement and applied understanding.

Dialogical teaching

Dialogic teaching uses language to foster reflection and understanding through iterative instructor-student discourse, promoting analytical reasoning, verbal expression, argumentation, active listening, and receptivity to divergent perspectives (Vincent-Lancrin et al., 2020). Learners engage in critical inquiry and co-construct knowledge through dialogic interaction with peers and educators (García-Carrión et al., 2020). Modalities such as group discussion and Socratic dialogue further develop capacities for autonomous analysis and evaluation (Hajhosseiny, 2012). Efficacy presupposes mutual willingness to engage with unfamiliar content; the instructor's role entails formulating generative questions and establishing a climate conducive to open discourse (Daniel et al., 2017).

This approach is represented in ten studies within the corpus (Bhattacharya et al., 2016; Björklund, 2019, 2024; Björklund and Sandahl, 2021; Burt, 2020; D’Angelo et al., 2022; Kozina and Metljak, 2022; Kuzma et al., 2022; Mizzi, 2021; Soroko, 2022). Across these studies, it is rarely used as a standalone method but is instead embedded within broader pedagogical approaches, particularly experiential and critical frameworks.

In financial education contexts, dialogic teaching mainly supports conceptual understanding through guided questioning, dialogue, and interactive activities such as role-play (Mizzi, 2021). Its effectiveness is consistently associated with respectful and empathetic classroom environments (Kuzma et al., 2022). The approach also shows strong alignment with critical pedagogy, particularly in culturally grounded interventions such as rap-based educational practices (Burt, 2020).

Inquiry-based teaching

Inquiry-based learning appears in four corpus studies on financial education (Kozina and Metljak, 2022; Mizzi, 2021; Solis and Tech, 2018; Visano and Ek-Udofia, 2016), and is consistently conceptualized as an active, learner-centred pedagogy in which students construct knowledge through processes of questioning, investigation, and hypothesis generation rather than through passive reception of information. Across the studies, the role of the teacher is similarly reconceptualized as that of a facilitator who guides inquiry processes rather than a transmitter of predefined content.

A cross-study pattern emerges in the adaptability of inquiry-based learning across diverse educational contexts. In formal settings, it is associated with structured investigative activities, including guided exploration of specialized financial education resources (Mizzi, 2021) and collaborative design and critical evaluation of financial education programs targeting marginalized youth (Visano and Ek-Udofia, 2016). In contrast, informal implementations emphasize peer-led and student-driven learning environments in which learners autonomously seek, share, and validate information (Solis and Tech, 2018). A further recurring pattern relates to conditions of adoption, with greater uptake observed among primary-level educators and among teachers who place stronger emphasis on financial literacy education (Kozina and Metljak, 2022).

Collectively, the studies converge on the view that inquiry-based learning fosters higher-order cognitive and metacognitive skills, particularly creativity and reflective thinking. By engaging learners in iterative cycles of questioning, information gathering, and problem-solving, the approach supports experiential and socially mediated knowledge construction, consistent with constructivist learning theory (Ismail et al., 2006).

Critical pedagogy

Critical pedagogy is consistently characterized in the literature as an approach that rejects educational neutrality and situates schooling within broader processes of political dialogue, critique, and resistance (Leroy, 2022; Rahimi and Sajed, 2014). Across studies, a central recurring principle is the emphasis on praxis, whereby critical reflection must be coupled with transformative action, as knowledge alone is considered insufficient to disrupt or counteract structures of domination (LeRoy, 2022) This orientation also entails a curricular imperative to integrate learners’ lived experiences and to position students as active participants in knowledge construction (Rahimi and Sajed, 2014; Sharif Uddin, 2019).

A second cross-study pattern concerns the translation of critical pedagogy into pedagogical frameworks that operationalize its principles in classroom practice. For instance, “Rap Therapy” (Burt, 2020) illustrates the use of cultural expression as a pedagogical entry point; however, Leroy (2022) cautions that such practices may inadvertently reproduce forms of alienation when cultural expression is not explicitly linked to political agency and action. Similarly, the Positive Agile Learners (PALs) framework is presented as a relational infrastructure for embedding social justice and ethical reflection within everyday classroom interactions (Blue et al., 2018).

A further consistent pattern is the use of conceptual and case-based scaffolds to support processes of conscientization. Threshold Concepts, for example, function as epistemic gateways that enable transformative shifts in understanding. In financial literacy education, Björklund and Sandahl (2021) demonstrate how concepts such as financial systems and political governance reorient analysis from individual financial behavior toward structural issues of power and inequality. In parallel, dilemma-based case studies operationalize critical inquiry by situating individual financial situations within broader socio-economic structures. Björklund (2024), for instance, reframes the case of “Brian” by interpreting debt not as an outcome of personal budgeting failure but as embedded within intersecting financial and political systems.

Collectively, these studies highlight a shared pedagogical pattern: critical pedagogy is enacted through tools that systematically shift analysis from individual responsibility toward multi-level structural understanding, thereby fostering critical economic citizenship.

Experiential learning

Experiential learning is the most frequently cited pedagogical approach in the corpus, appearing in 21 studies (Batty et al., 2015; Bhattacharya et al., 2016; Björklund and Sandahl, 2021; Byram et al., 2021; Cedeño et al., 2021; Choi et al., 2024; Curugan et al., 2020; Garcia et al., 2017; Gibert et al., 2024; Hagedorn et al., 2016; Harter and Harter, 2010; Kang et al., 2023; Kozina and Metljak, 2022; Mizzi, 2021; Park et al., 2021; Reams-Johnson and Delker, 2016; Schug and Hagedorn, 2005; Solis and Tech, 2018; Suleiman, 2024; Tympa et al., 2024; Visano and Ek-Udofia, 2016). This method engages learners holistically by integrating intellectual, emotional, and sensory dimensions. A recurring pattern across studies is its embodied and action-oriented nature, particularly evident in the use of role-playing activities (Cedeño et al., 2021; Mizzi, 2021; Visano and Ek-Udofia, 2016) and serious games (Byram et al., 2021; Gibert et al., 2024; Harter and Harter, 2010), which immerse learners in simulated environments requiring active decision-making and perceptual engagement (Andreson et al., 1995). Across these implementations, learning is framed as extending beyond cognitive acquisition toward affectively and experientially grounded understanding.

A second cross-study pattern concerns the use of structured experiential models to facilitate the internalization of financial concepts. The “four-slot piggy bank” model—allocating money across spending, saving, investing, and donating—appears in four studies (Hagedorn et al., 2016; Reams-Johnson and Delker, 2016; Schug and Hagedorn, 2005; Tympa et al., 2024) as a recurring pedagogical device that enables learners to operationalize abstract financial principles through concrete practice. Complementing this, several studies indicate a learner preference for experiential formats such as simulations, projects, and training activities over didactic instruction (Zhou et al., 2024), while field-based learning experiences, including field trips (Byram et al., 2021; Park et al., 2021) and partnerships with financial institutions (Batty et al., 2015), further reinforce the transfer of knowledge to real-world contexts.

A third pattern relates to the social and collaborative dimension of experiential learning, particularly through peer-to-peer mechanisms. Student-led workshops (Solis and Tech, 2018) exemplify informal experiential environments in which learning is co-constructed through active peer interaction. Similarly, programs such as “Teens Reaching Youth” and peer-coaching models demonstrate that the act of teaching others functions as an additional learning cycle, whereby knowledge transmission strengthens mentors’ own understanding through re-experience and consolidation(Garcia et al., 2017; Kang et al., 2023).

Collaborative learning

Collaborative learning refers to both a pedagogical philosophy and a teaching methodology in which small, interdependent groups of students work jointly to solve problems, accomplish tasks, or produce shared work. It is characterized by an emphasis on shared responsibility, mutual respect for contributions, and consensus-building through cooperative effort, positioning it in opposition to competitive or individualistic learning paradigms (Laal and Ghodsi, 2012). Research indicates that collaborative learning functions by strengthening social support among students. This enhanced peer support acts as a key mediator, directly contributing to a significant, positive increase in student engagement, as learners feel more connected, motivated, and accountable within a supportive peer network (Li, 2025).

In terms of implementation within financial education, only three studies in the corpus explicitly evidence its application (Frisancho, 2023; Kozina and Metljak, 2022; Tympa et al., 2024). The pedagogical tools employed predominantly consist of group-based activities, including collaborative projects, group assignments, and in-class collaborative tasks. Notably, this approach is frequently combined with or embedded within broader instructional frameworks, such as project-based learning or experiential learning, suggesting it is often utilized as a core collaborative component within these more extensive, hands-on educational methodologies.

Metacognitive pedagogy

Metacognition is defined as “thinking about thinking,” involving a reflective and distanced stance toward one's own mental processes. It encompasses both declarative knowledge about cognition—including an understanding of learning strategies, task characteristics, and one's own strengths and weaknesses—as well as procedural control skills, namely the ability to actively regulate these processes (Doly, 2006).

Implementing a metacognitive pedagogy entails equipping learners with mechanisms such as anticipation, planning, monitoring, and verifying results, which enhance their performance and allow for the adjustment of their strategies according to task demands (Frenkel and Deforge, 2014). This framework also fosters the emergence of creative thinking when confronting novel situations.

Metacognition is not only extremely underutilized, but it is also underexploited in the sole study where it appears (Kang et al., 2023). Far from occupying a central role within a pedagogy grounded in cognitive science and aimed at enhancing financial education, its use is limited to two questions in a post-test administered five months after the intervention. It is employed there solely to measure, in a declarative manner, the participants’ metacognitive confidence.

Creativity-supporting pedagogies in financial education

Across the financial education corpus, several pedagogical approaches are identified, among which metacognitive pedagogy, project-based learning, inquiry-based learning, dialogical teaching, and creative partnerships occupy a specific position in that they are the only ones that also correspond to the creativity-supporting pedagogies outlined in Lancrin's framework (Vincent-Lancrin et al., 2020). The following paragraphes therefore focuses on these overlapping pedagogies, while interpreting their potential—rather than empirically established—relationships with different forms of creativity in financial education.

Metacognitive pedagogy may be associated with reflective forms of financial creativity, insofar as it encourages learners to monitor, evaluate, and regulate their own thinking processes. In financial education contexts, this could support awareness of how financial decisions are made, including budgeting, saving, or risk assessment. Such reflective regulation may facilitate more flexible and adaptive reasoning, although its effects depend on pedagogical design and implementation.

Project-based learning (Frisancho, 2023; Kozina and Metljak, 2022; Tympa et al., 2024) may be linked to applied financial creativity. By engaging learners in sustained, goal-oriented tasks, it can lead to the production of concrete outputs such as financial plans, simulations, or problem solutions. Creativity in this case may be understood as iterative design and refinement within authentic or semi-authentic financial problems, where learners translate conceptual understanding into practical artefacts.

Inquiry-based learning (Kozina and Metljak, 2022; Mizzi, 2021; Solis and Tech, 2018; Visano and Ek-Udofia, 2016) may foster exploratory financial creativity by positioning learners as active investigators of financial issues. Through processes of questioning, information gathering, and hypothesis development, learners may generate multiple ways of interpreting financial phenomena. This can potentially encourage more divergent approaches to topics such as debt, saving behavior, or financial systems.

Dialogical teaching, often embedded in discussion and collaborative exchange (Frisancho, 2023; Solis and Tech, 2018)may support relational forms of creativity. In such settings, creativity may emerge through interaction, as learners negotiate meanings, confront differing perspectives, and co-construct understandings of financial concepts through dialogue.

Creative partnerships (Batty et al., 2015; Byram et al., 2021; Mandell, 2006; Mandell 2009) may extend financial education into situated contexts by involving external actors such as institutions or practitioners. These arrangements may provide opportunities for learners to engage with real-world financial practices and adapt their learning to authentic constraints, thereby potentially supporting context-sensitive and applied forms of creativity.

Overall, these five pedagogical approaches represent the intersection between the pedagogies identified in the financial education corpus and those included in Lancrin et al.'s framework. While the corpus includes additional pedagogical forms, these overlapping approaches may be interpreted as offering complementary pathways to creativity in financial education, ranging from reflective and exploratory processes to applied, relational, and context-situated forms of engagement, depending on how they are implemented.

Discussion

This systematic review identifies one principal finding: experiential learning constitutes the most widely used pedagogy in Financial Education. In line with this, accumulated evidence affirms that experiential learning has emerged as the predominant pedagogical approach in financial education, a promising paradigm that effectively transcends the limitations of traditional direct instruction(Amagir et al., 2018). Although the term “experiential learning” is not explicitly cited as a pedagogy that fosters creativity, it can be argued that it serves as an overarching framework which encompasses other creativity-enhancing pedagogies, such as project-based learning. This active, application-based model, which integrates simulations, can be particularly effective in enhancing both financial literacy and associated cognitive competencies, based on the experiential framework of Kolb's (2015) theory. This theory frames learning as a process where knowledge is created through the transformation of experience. Its foundational four-stage cycle, progressing from Concrete Experience through Reflective Observation and Abstract Conceptualization to Active Experimentation, is inherently a cycle of problem-solving and decision-making.

This decision-making capacity is not merely a supplementary benefit that reinforces financial education; rather, it constitutes an indispensable component of financial literacy itself (Manz, 2011). Employing creativity within the decision-making process is essential for optimally applying financial knowledge to real-world contexts.

Another approach that has the potential to foster creativity is metacognitive pedagogy(Jia et al., 2019; Lebuda and Benedek, 2023; Vincent-Lancrin et al., 2020). The benefits of metacognition are twofold: it is known to improve learning quality and is integral to effective problem-solving, which requires not just critical thinking but also awareness and cognitive as well as non-cognitive regulation (Rivas et al., 2022). Despite its potential, this pedagogy is scarcely employed in financial education curricula, with only a single documented instance (Kang et al., 2023). It is therefore recommended that educators and curriculum developers actively adopt this pedagogical strategy and integrate it more often.

Another underutilized pedagogical approach is creative partnerships which appears in only three relevant studies, despite its impact on creativity. (Barrett et al., 2021; Wilkins, 2018) This approach may be valuable for leveraging the impact of emotions on financial behavior. As a core dimension of financial literacy, financial behavior critically influences decision-making, among other outcomes.

A limitation of the studies included in this review is the frequent lack of clear information regarding the specific pedagogies employed. Consequently, it was necessary to deduce these elements from the textual descriptions and the possible activities of the interventions. Even when a pedagogical label is applied, a lack of descriptive detail concerning its enactment often precludes a meaningful analysis of its effectiveness or fidelity. Although pedagogical strategies can be theoretically associated with enhancing particular types of creativity, the studies provide no measurable indicators or assessment data to verify whether these outcomes were genuinely achieved.

Ultimately, this review affirms the importance of experiential learning while arguing for the integration of metacognitive pedagogy and creative partnerships into financial education. To advance the field, future studies should focus on operationalizing and measuring the specific creative competencies engendered by each pedagogical framework, a necessary step to close the existing evidence gap.

Other information

This review was not formally registered, and a systematic review protocol was not published in advance. The research received no financial or material support.

The author declares that there are no competing interests related to the content of this work.

All studies included in this review were sourced from and are accessible via the three databases specified in the methodology.

AI technology was utilized for linguistic refinement and structural suggestions. The authors oversaw the entire process, ensured factual and conceptual accuracy, and affirmed sole accountability for the scholarly content presented.

Footnotes

Acknowledgements

AI technology was utilized for linguistic refinement and structural suggestions. The author oversaw the entire process, ensured factual and conceptual accuracy, and affirms sole accountability for the scholarly content presented.

Ethical approval and informed consent statements

Not Applicable

Consent to participate

Not Applicable

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

All studies included in this review were sourced from and are accessible via the three databases specified in the methodology.