Abstract

The increasing complexity of global financial crimes, driven by the rise of virtual currencies and evolving fraudulent techniques, has posed significant challenges for Taiwan’s anti-money laundering and fraud-prevention mechanisms. The research highlights challenges such as insufficient public awareness, inefficiencies in the Know Your Customer process, and the inability to address emerging fraud schemes that involve virtual currencies.

This study examines these issues by reviewing the current anti-money laundering framework, identifying operational deficiencies, and proposing solutions through a literature review and in-depth interviews with financial professionals. Findings reveal that effective anti-money laundering measures require enhanced public education, advanced technological applications such as artificial intelligence and blockchain, and improved personnel training to identify suspicious activities. Furthermore, the study underscores the importance of cross-border cooperation and international coordination in combating transnational financial crimes. The practical recommendations aim to strengthen the robustness, security, and compliance of Taiwan’s financial system while offering insights for the Asia-Pacific region. Theoretically, the research clarifies how anti-money laundering strategies intersect with virtual currencies and offers a framework to guide future studies.

Keywords

Introduction

The acceleration of globalization and the integration of financial markets have enabled unprecedented capital flows while also increasing opportunities for cross-border money laundering and financial fraud. Perpetrators exploit the complexity of the global financial system, using multilayered transfers, digital platforms, and virtual assets to conceal illicit proceeds. International research has documented how globalization and regulatory fragmentation can obscure transnational laundering and complicate enforcement and compliance coordination (Arnone and Borlini, 2010; Haigner et al., 2012). Consistent with these trends, the United Nations Office on Drugs and Crime (UNODC) estimates that money laundering may amount to approximately 2%–5% of global GDP annually, underscoring the scale and traceability challenges faced by enforcement and compliance systems (UNODC, 2011). These developments help explain why contemporary fraud and laundering increasingly converge in digitally mediated financial environments, exposing the limitations of conventional monitoring tools (Abukari, 2026). Recent studies further highlight the growing convergence of cybercrime, fraud, and money laundering within digitally mediated financial environments (bin Azero et al., 2024).

In this context, anti-money laundering (AML) governance is no longer solely a compliance architecture; it increasingly functions as a cross-level coordination problem that links macro-regulatory coherence, meso-institutional implementation capacity, and microbehavioral/typological adaptation by offenders.

Internationally, fraud has grown in both complexity and scale. Recent cross-national evidence underscores persistent exposure and repeat victimization across diverse jurisdictions. The Fraudscape Briefing (Hyde and Gibson, 2024), based on a representative survey of adults in 15 countries, reported that just over 21% of respondents experienced at least one incident of fraud between 2021 and 2023, with approximately 40% reporting repeat victimization and one in six experiencing three or more incidents. The study further estimated roughly 228 million unique victims and more than 331 million incidents across the surveyed countries during the same period, with authorized “push payment” fraud reported as the most common type and substantial perceived gaps in governmental prioritization of anti-fraud measures (Hyde and Gibson, 2024).

Taken together, these patterns suggest that fraud is increasingly routinized in everyday financial life and that the prevention of illicit financial flows requires not only legal rules but also operational mechanisms capable of responding to fast-evolving typologies.

Executive Yuan, Republic of China (Taiwan), 2024. Taiwan, as a major economy in the Asia-Pacific region, is increasingly facing these evolving threats. Official anti-fraud reporting and monitoring mechanisms indicate sustained fraud activity and substantial associated losses, reinforcing the need for rapid reporting, coordinated response, and risk communication across stakeholders (National Police Agency, Ministry of the Interior, Republic of China [Taiwan], 2024). Against this backdrop, Taiwan has institutionalized multiple reporting and response channels, including the 165 Anti-Fraud Hotline for reporting and consultation and the 110 emergency hotline for urgent police assistance (Executive Yuan, Republic of China (Taiwan), 2024; National Police Agency, Ministry of the Interior, Republic of China [Taiwan], 2024). At the policy level, the Executive Yuan’s New-generation Anti-Fraud Strategy Action Program (Version 2.0) further reflects efforts to coordinate cross-agency governance, strengthen legal and technical measures, and reinforce public–private cooperation in daily fraud prevention (Executive Yuan, Republic of China (Taiwan), 2024).

These institutional developments make Taiwan an empirically informative setting for examining how AML and anti-fraud policies translate into on-the-ground implementation routines and where translation gaps persist under digital-finance conditions.

Technological change and the diversification of fraud methods—particularly those involving virtual-asset infrastructures—have also made illicit funds increasingly difficult to trace and have intensified compliance and investigative burdens. Rather than relying on a single dominant method, contemporary fraud–laundering pathways often evolve through rapid typology mutation and cross-border transferability, creating jurisdictional complexity and reinforcing the need for adaptive monitoring, inter-agency coordination, and risk-based regulatory responses (Abukari, 2026). If these problems are not resolved in a timely and effective manner, the consequences can be severe. From an economic perspective, persistent fraud can generate substantial losses, raise transaction and compliance costs, and weaken investor confidence. For banks and financial institutions, ongoing fraud entails regulatory exposure, increased compliance burdens, and reputational risk. Moreover, law enforcement and compliance officers face mounting challenges in tracing increasingly complex cross-border financial flows, leading to inefficient resource allocation and reduced capacity to combat financial crime (Ahmed, 2025; Lo, 2022; Mathias and Wardzynski, 2023).

Accordingly, the central analytical challenge is not merely whether AML rules exist, but whether the combined system of detection, reporting, enforcement, and inter-organizational coordination can remain effective when offenders adapt faster than institutional routines and supervisory responses.

In light of these challenges, this study aims to provide an in-depth analysis of Taiwan’s current AML mechanisms and to examine the operating models adopted by fraud syndicates, particularly those that leverage virtual assets for cross-border fund transfers. By synthesizing international practices and Taiwan’s policy and statistical context, and by drawing on expert interviews and a comprehensive literature review, this research identifies critical implementation gaps and proposes actionable improvement strategies. Prior studies have predominantly emphasized regulatory design and provided a limited understanding of how virtual-asset-enabled laundering operates in practice; this study builds upon prior research conducted in Taiwan on fraud and AML practices (Li and Kao, 2024) while extending the analysis through a multi-level analytical framework. This study addresses that gap and offers practice-informed implications for financial regulators, compliance functions, and law enforcement agencies seeking to enhance fraud prevention in Taiwan’s rapidly evolving digital-finance environment. Ultimately, addressing these challenges is critical not only for Taiwan’s economic stability but also for reinforcing the integrity of the global financial system in an increasingly interconnected digital economy.

Accordingly, this study pursues three interrelated objectives:

To map the most salient fraud typologies encountered in Taiwan’s financial sector and clarify how fraud proceeds are laundered through both conventional channels (e.g. mule/dummy accounts) and virtual-currency pathways.

To diagnose implementation bottlenecks that constrain AML and anti-fraud effectiveness across macro–meso–micro levels, including regulatory/judicial frictions, institutional compliance capacity (e.g. Know Your Customer (KYC)/suspicious-transaction reporting (STR) routines), and technology-enabled laundering practices.

To develop a practice-informed, integrated framework and actionable improvement strategies for regulators, financial institutions, and law enforcement agencies to strengthen Taiwan’s prevention and detection of illicit financial flows involving virtual currencies.

Literature review

An overview of money laundering prevention

Money laundering prevention is a global policy priority. With technological advancements and financial liberalization, money laundering techniques have become increasingly complex, posing threats to the international community and the global financial system. Sultan and Mohamed (2024) define money laundering as the process of converting illicit proceeds into ostensibly legitimate fund

The Financial Action Task Force (FATF) has issued 40 recommendations and 9 special recommendations to provide guidance on global money laundering prevention. These recommendations require countries to strengthen financial regulation and ensure the implementation of STR mechanisms (Costantino, 2024). Since the 2017 amendment of Taiwan’s Money Laundering Control Act (MLCA), the government has adopted multiple measures, including strengthening the KYC system and imposing stricter scrutiny on high-risk transactions. However, fraud syndicates continue to launder money through mule/dummy accounts and to transfer funds to accounts obtained via fake job postings or investment scams (Li, 2024).

As the digital economy thrives, virtual currencies have become prominent conduits for money laundering due to their pseudonymity and ease of cross-border transfer, which complicate the tracing of illicit funds (Subbagari, 2024). Haigner et al. (2012) further note that the complexity of cross-border transactions and regulatory divergences across jurisdictions are major obstacles to global money laundering prevention. Even if some countries pursue strict enforcement, overall effectiveness is undermined when other countries do not participate.

In short, money laundering poses a serious challenge to global financial stability, and effective prevention depends on robust international cooperation and rigorous legal oversight.

The current state of money laundering and financial fraud

Money laundering and financial fraud are increasingly intertwined, particularly due to the widespread use of dummy accounts and virtual currencies. This section provides an overview of the current state of these crimes in Taiwan and internationally, including their evolving methods and impact on regulatory systems.

Overview and trends

Virtual currencies can be broadly divided into two categories: convertible (open) and non-convertible (closed) virtual currencies (FATF, 2014). Convertible virtual currencies have equivalent value in fiat currency and can be exchanged in both directions for real money. In contrast, non-convertible virtual currencies are confined to specific platforms or ecosystems and cannot officially be exchanged for fiat currency. This study primarily focuses on convertible virtual currencies, which are commonly used in money laundering activities due to their pseudonymity and cross-border transferability.

According to Li (2024), Taiwanese scam syndicates often launder money through multilayered cash transfers. After defrauding individuals through investment or romance fraud, these syndicates transfer the stolen money to multiple dummy accounts. Leuprecht et al. (2023) observe that the pseudonymity of virtual currency facilitates money laundering, enabling criminals to swiftly integrate fraudulent gains into the legitimate financial system. Chang et al. (2017) and Zhu (2024) further emphasize the scale and damage of financial fraud in Taiwan, reporting over 35,000 cases in 2023 with losses exceeding NT$7.9 billion.

Common criminal schemes involving dummy accounts

The use of dummy accounts remains a primary tactic for laundering illicit funds. Common schemes include:

Fake job offers: Scam syndicates solicit personal bank account details from victims (Wang, 2026).

Loan fraud: Bogus loan services are used to facilitate fund transfers.

Romance fraud: Victims are manipulated into transferring funds to dummy accounts (Tiwari et al., 2025).

Advance payments via prepaid game cards: Criminals exploit lightly regulated prepayment methods (Akartuna et al., 2022).

Cryptocurrency conversion: Fraud proceeds are laundered via virtual-currency exchanges (Leuprecht et al., 2023).

International exchanges and cross-border remittances: Criminals leverage foreign exchanges to obscure fund flows (Li, 2024).

Challenges in monitoring illicit financial flows

Despite measures taken by governments and financial institutions to prevent money laundering, fraud groups continue to transfer funds through third-party payment platforms and virtual currencies (Subbagari, 2024). These criminal groups often hide funds through multilayered, cross-border transfers, which complicates financial monitoring. To address this challenge, the international community has proposed to strengthen KYC procedures and to implement an identity-based system for virtual-currency transactions (Haigner et al., 2012; Leuprecht et al., 2023).

In addition, the lack of harmonized regulatory frameworks across jurisdictions further complicates supervision. Differences in regulatory standards and definitions of suspicious activity hinder cross-border cooperation, thereby creating gaps that transnational criminal networks can exploit (Abukari, 2026; Arnone and Borlini, 2010).

Moreover, the rapid evolution of digital payment systems, combined with the inherent pseudonymity of virtual currencies, presents significant challenges to traditional monitoring mechanisms. Advances in encryption and decentralized blockchain networks often render conventional tracking methods ineffective, necessitating constant technological and procedural updates (Leuprecht et al., 2023; Subbagari, 2024).

Furthermore, third-party intermediaries and non-bank financial institutions are increasingly involved in the payments ecosystem, fragmenting transaction data across multiple channels. This fragmentation complicates effective data integration and the tracing of illicit financial flows, thereby reducing the effectiveness of current AML systems (Abukari, 2026; Haigner et al., 2012).

Finally, emerging strategies—such as the strategic use of virtual accounts and the ability to quickly switch between trading platforms—undermine conventional KYC and monitoring protocols. Addressing these issues requires the deployment of advanced analytics and real-time data monitoring, as well as a comprehensive modernization of AML frameworks (Leuprecht et al., 2023; Subbagari, 2024).

Typologies and mechanisms of money laundering and fraud

Integration of fraud and laundering mechanisms

Fraud schemes such as investment, romance, or impersonation fraud often serve as entry points for money laundering. Once funds are obtained, they are disbursed through dummy accounts, virtual currencies, or low-value, high-frequency transfers. Typical patterns include:

Investment fraud combined with layered transfers (Li, 2024).

Romance scams leading to cross-border fund movements (Tiwari et al., 2025).

Conversion of illicit gains into cryptocurrencies to enable rapid international transfers (Leuprecht et al., 2023).

Use of prepaid game cards to evade traditional AML controls (Akartuna et al., 2022).

Job-fraud recruitment of mule accounts for multistep laundering processes (Li, 2024).

Bulk-cash smuggling and structuring via multiple small-value transfers, which remain prevalent (Li, 2024).

Tax evasion within digital ecosystems, integrating illicit proceeds into legitimate businesses (Subbagari, 2024).

Regulatory and operational challenges

Tiwari et al. (2025) report that fraudsters employ trade-based money laundering (TBML) to conceal illicit gains, manipulating trade transactions to facilitate laundering. Taiwanese scam syndicates also transfer funds across borders through virtual currencies, further complicating regulatory supervision (Li, 2024).

In recent years, money laundering and fraud have become increasingly interconnected, necessitating more robust regulatory responses and coordinated international efforts (Li, 2024; Tiwari et al., 2025). Global regulators need to strengthen international cooperation, enhance client identity verification, and deploy artificial intelligence (AI)-based monitoring to improve supervisory effectiveness (Haigner et al., 2012; Leuprecht et al., 2023; Li, 2024). Implementing identity-based systems for virtual-currency transactions can further enhance regulatory efficiency (Leuprecht et al., 2023).

Although Taiwan has established an anti-fraud joint platform, the rapid development of virtual currencies and digital payment systems underscores the need for continuous legal, regulatory, and technological upgrades (Li, 2024). Going forward, advancements in technology and deeper international cooperation should be prioritized to more effectively counter transnational crime (Haigner et al., 2012; Li, 2024).

Definition and comparative analysis of predicate offenses

Concept of predicate offense

A predicate offense refers to any serious crime that generates illicit proceeds, which then become the target of money laundering activities. According to the FATF Recommendation 3 and its Glossary (FATF, 2012–2025), predicate offenses include but are not limited to fraud, smuggling, corruption, drug trafficking, terrorist financing, and tax crimes. A clear articulation of this concept is crucial to demonstrate how offenses like fraud or tax evasion can serve as the origin of funds that are later laundered to appear legitimat

Internationally, the scope of predicate offenses has expanded over time. FATF encourages jurisdictions to adopt a broad approach, covering all offenses punishable by at least 1 year of imprisonment or those deemed serious crimes under national law (Aljinović and Bartulović, 2023; FATF, 2012–2025). For instance, tax crimes have been recognized as primary sources of laundered proceeds, alongside drug trafficking and corruption (Pali and Mustafaj, 2025).

Furthermore, recent policy and regulatory assessments underscore the convergence of predicate crimes with complex financial mechanisms, such as the use of shell companies and trusts, which serve to obscure the origin of illicit proceeds (FATF, 2012-2025).

Comparative procedures across jurisdictions

Common law systems (e. g. the United States and Australia)

Conviction of the predicate offense is often required before prosecuting money laundering. For example, the US AML framework may mandate proof of the underlying crime before pursuing asset forfeiture (Pali and Mustafaj, 2025). Australia’s AML regime emphasizes the role of financial intelligence and the reporting obligations of institutions under the Anti-Money Laundering and Counter-Terrorism Financing Act (Moiseienko and King, 2025).

Civil law systems (e. g. European Union (EU) jurisdictions)

Some EU countries permit nonconviction-based confiscation, enabling authorities to freeze or confiscate suspicious assets without requiring a prior conviction of the predicate offense (Pavlidis, 2022).

Italy, for instance, acknowledges that foreign tax crimes can qualify as predicate offenses for money laundering within its territory (Pierini, 2020).

Asian jurisdictions

China has expanded its legal framework to include self-laundering—where offenders launder the proceeds of their own crimes—as part of its AML enforcement (He, 2024).

Taiwan’s operational mechanism

Taiwan’s MLCA defines “specified unlawful activity,” equivalent to predicate offenses, in Article 3. According to the Ministry of Justice (2024), this includes all crimes with a minimum penalty of 6 months’ imprisonment and enumerates specific offenses such as fraud, smuggling, and serious tax violations. Importantly, Article 4 of the MLCA stipulates that a conviction for the predicate offense is not required to determine that property constitutes criminal proceeds; authorities may investigate money laundering independently, freeze assets, and initiate prosecutions without waiting for a final judgment on the underlying offense (Ministry of Justice, 2024). This framework aligns with FATF’s risk-based approach (FATF, 2012–2025) and enables quicker intervention against illicit financial flows.

The Financial Supervisory Commission (FSC) and Investigation Bureau have strengthened enhanced due diligence (EDD), suspicious transaction reporting (STR), and continuous AML training for financial and non-financial sectors, including trust and company service providers (TCSPs), while Taiwan has reaffirmed its commitment to regional AML cooperation through participation in the Asia/Pacific Group on Money Laundering (APG) Annual Meeting (Anti-Money Laundering Office, Executive Yuan, 2024).

Strategies for combating and preventing fraud: Theory and practice

Fraud remains a pervasive threat that undermines economic stability and erodes public trust. A comprehensive approach to combating fraud requires both theoretical insights and practical measures. One of the most influential frameworks in this field is the Fraud Triangle theory (Cressey, 1953), which posits that fraud occurs when pressure, opportunity, and rationalization converge. This core model has been refined into the Fraud Diamond (Wolfe and Hermanson, 2004), introducing competence as a key factor, and later extended to incorporate elements such as collusion and arrogance (Bader et al., 2024).

Challenges in fraud prevention

Organizations encounter several obstacles in preventing fraud. First, inadequate internal controls and a weak organizational culture can create an environment that is highly susceptible to fraudulent activities. Maulidi and Ansell (2021) found that the internal control systems of many public-sector organizations are not strong enough to detect or deter fraud. Second, rapid advances in technology have equipped fraudsters with increasingly sophisticated tools to exploit vulnerabilities. Traditional fraud-detection methods are being outpaced by innovative schemes, especially those involving virtual currencies, which can obscure the source of funding and complicate tracking (Allimia et al., 2024; Mora et al., 2019). Third, gaps in regulation and enforcement further impede effective fraud prevention, as law enforcement agencies often lack the resources and cross-border coordination needed to combat fraud effectively (Lo, 2022; Mathias and Wardzynski, 2023).

Improvement strategies

Addressing these challenges requires a multilayered strategy that integrates theoretical insights with practical interventions.

Enhancing internal controls and organizational culture

Organizations must implement internal control systems tailored to their risk profiles. This includes rigorous risk management, ongoing monitoring, and actively fostering a culture of integrity. Moreover, establishing a strong whistleblowing mechanism and conducting regular training can empower employees to report suspicious activities, thereby reducing fraud risk (Maulidi and Ansell, 2021).

Leveraging advanced technologies

The integration of AI and machine learning with fraud-detection systems shows significant promise. These technologies enable the processing of large datasets in real time, the detection of anomalies, and adaptive responses to emerging fraud tactics. Research indicates that AI and machine learning improve the accuracy and speed of fraud detection, enabling organizations to move from reactive to proactive prevention strategies (Ijiga et al., 2024; Okonta and Nnamdi, 2025). With the proliferation of digital transactions, AI systems are becoming increasingly important for identifying subtle patterns that may be overlooked by traditional methods.

Strengthening regulatory frameworks and cross-border cooperation

Modern fraud often transcends national borders, so policymakers must modernize legal frameworks and strengthen international collaboration. Enhanced coordination among regulators, law enforcement bodies, and international institutions facilitates the sharing of intelligence and best practices to improve overall fraud-prevention efforts (Doig et al., 2025; Okolie and Egbon, 2025).

Building public awareness and communication

Low public awareness is an important cause of fraud victimization. Comprehensive public-awareness campaigns through multiple media channels are essential to educate citizens on the risks of fraud and prevention strategies. For example, campaigns promoting the use of hotlines and digital reporting tools have been shown to be effective in raising public vigilance (Setyawan et al., 2023).

An overall strategy to combat fraud must address these multifaceted challenges through strong internal controls, innovative technology solutions, strengthened regulatory measures, and effective public education. Theoretical models such as the Fraud Triangle and Fraud Diamond provide an important basis for understanding the drivers of fraud. By applying these insights, organizations and policymakers can design targeted interventions to reduce risk, protect assets, and restore public trust in financial systems.

The current situation of money laundering prevention in Taiwan

Building on the global trends discussed above, this section focuses on Taiwan’s current AML framework, with an emphasis on recent regulatory improvements and persistent challenges.

In terms of regulation and institutional mechanisms, Taiwan amended the MLCA in 2017, thereby strengthening financial institutions’ KYC procedures, suspicious-transaction reporting (STR) mechanisms, and overall money laundering detection capabilities (Hong, 2022). The Asia/Pacific Group on Money Laundering (APG) mutual evaluation has further encouraged Taiwan’s alignment with the international community and has contributed to the maturation of Taiwan’s AML system, improving its capacity to address the challenges posed by globalization.

With respect to virtual currencies and digital payments, their pseudonymity and cross-border functionality make them attractive tools for criminal syndicates. Leuprecht et al. (2023) argue that the decentralized architecture of virtual currency enhances the concealment of funds. Wu et al. (2024) contend that blockchain analytics can improve traceability and help mitigate anonymity risks. Akartuna et al. (2022) also note that prepaid instruments (e.g. game time cards) can facilitate money laundering schemes. In response, Taiwan’s regulators have intensified oversight to address these evolving methods. Regarding the interaction between financial fraud and money laundering, Hong (2022) observes that crime syndicates commonly use mule/dummy accounts and virtual currencies to execute multiple—including cross-border—transfers of illicit proceeds, thereby making the origins of funds difficult to trace. This dynamic has heightened supervisory burdens for financial institutions and law enforcement agencies.

In terms of blockchain technology and information sharing, Wu et al. (2024) emphasize that the transparency of distributed-ledger systems can enhance regulatory insight and facilitate cross-institutional information sharing, thereby strengthening the capability to trace suspicious transactions. In practice, Taiwanese financial institutions have begun deploying blockchain-based tools to improve supervisory efficiency and have reinforced cross-border cooperation mechanisms for financial information sharing to better combat money laundering.

The current study and research questions

Building on the foregoing review of global trends in money laundering and fraud, as well as Taiwan’s evolving AML regime, this section specifies the research questions (RQs) guiding the present study and explains the analytical rationale for selecting Taiwan as an empirically informative qualitative case. As highlighted in the Introduction, Taiwan has experienced a high volume of fraud cases and substantial financial losses, while virtual-currency-related laundering pathways have further complicated detection and enforcement.

Research questions

Guided by the study objectives outlined in the Introduction, the present research addresses the following RQs:

RQ1. What fraud typologies are most salient in Taiwan’s financial sector, and how are their proceeds operationally laundered through mule/dummy accounts and virtual-currency channels?

RQ2. What are the most critical barriers to effective AML and fraud prevention in Taiwan across governance levels (e.g. regulatory/judicial constraints, KYC/STR execution challenges, and technology-related limitations)?

RQ3. How do emerging technologies and virtual-asset infrastructures reshape both fraud methods and AML capabilities in Taiwan’s enforcement and compliance practices?

RQ4. What capability-building measures and inter-organizational/cross-border cooperation mechanisms are considered most feasible for improving Taiwan’s AML and anti-fraud system?

Analytical rationale for selecting Taiwan as a case

Design-wise, this research treats Taiwan as an information-rich qualitative case that illuminates the convergence of fraud and AML challenges in digitally mediated finance (Gerring, 2006; Yin, 2018). Taiwan is analytically suitable for at least four reasons.

First, Taiwan has experienced high exposure to fraud and substantial financial losses, making the problem empirically salient and policy-relevant.

Second, Taiwan’s fraud ecosystem is frequently characterized by mule/dummy account operations and rapidly evolving typologies, which are directly tied to laundering processes and place significant pressure on AML implementation.

Third, Taiwan’s AML governance has undergone major reforms (e.g. post-2017 legal and supervisory strengthening) and has been shaped by (APG) mutual evaluation dynamics, providing a meaningful compliance context for assessing implementation gaps.

Fourth, the growing involvement of virtual currencies in transnational laundering routes makes Taiwan a useful lens for understanding broader regional and global trends in regulatory adaptation and technology-enabled financial crime.

Accordingly, the study’s case-based insights are intended to contribute not only to Taiwan-focused policy debates but also to the wider literature on fraud–AML convergence, FATF-aligned regulatory adaptation, and the operational challenges of tracing illicit financial flows in the era of virtual assets (Gerring, 2006; Yin, 2018).

Research method

Conceptual framework

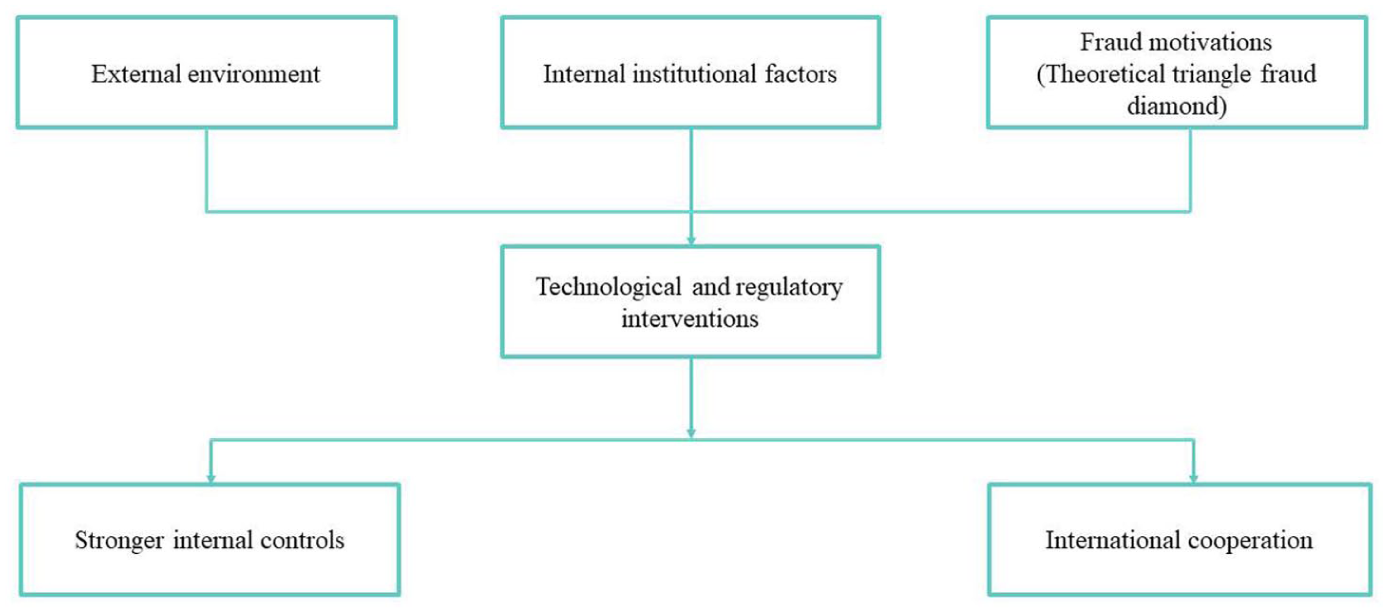

The conceptual framework for this study integrates macro-, meso-, and micro-level factors to illustrate the mechanisms underlying money laundering and financial fraud in Taiwan. As shown in Figure 1, the framework combines theoretical constructs and empirical observations, offering a multidimensional lens for analyzing the interplay between fraud schemes, laundering practices, and regulatory responses. At the macro level, the external environment captures economic and regulatory trends—such as financial liberalization, technological innovation, and cross-border capital flows—that create systemic opportunities for criminal exploitation (Aljinović and Bartulović, 2023; FATF, 2012–2025).

Conceptual framework.

At the meso level, internal institutional factors underscore organizational vulnerabilities, including gaps in compliance systems, insufficient KYC protocols, and weak staff training, all of which may facilitate the concealment of illicit proceeds (Lu, 2017). Meanwhile, fraud motivations are addressed at the micro level, drawing on behavioral theories such as the Fraud Triangle and Fraud Diamond, which emphasize the influence of pressure, opportunity, rationalization, and capability (Yahaya, 2026).

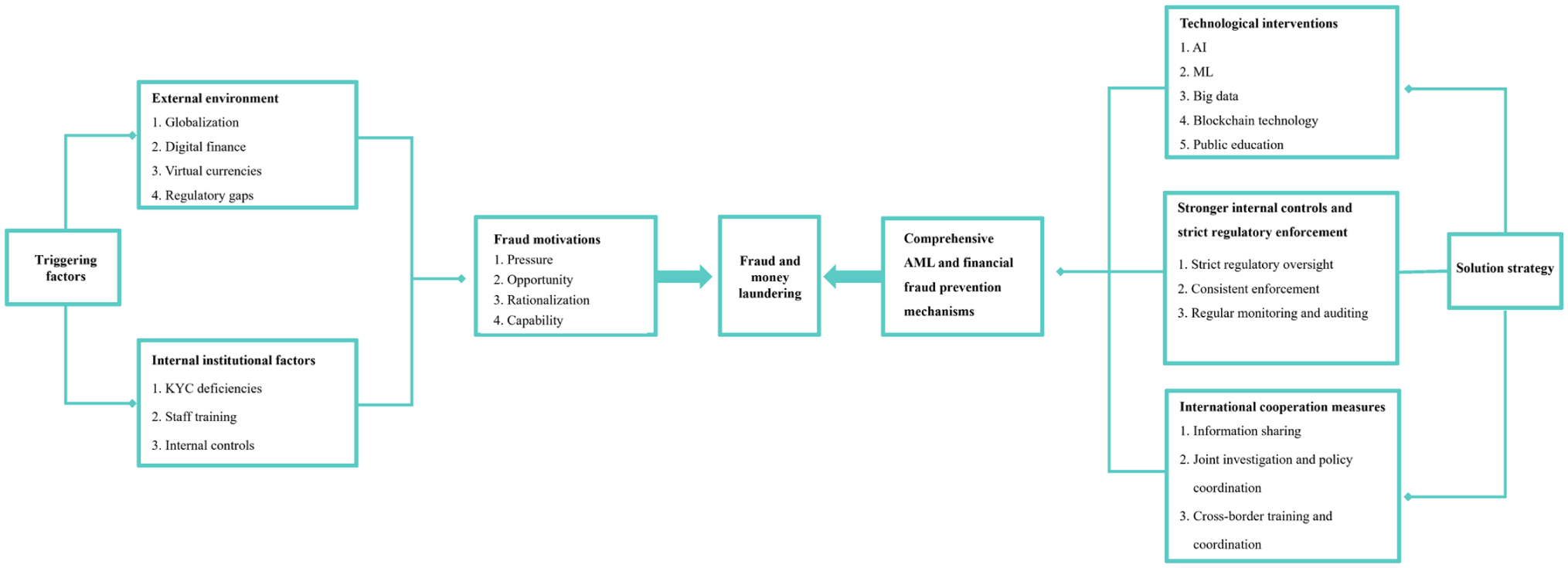

The framework further highlights the critical role of technological and regulatory interventions, particularly the application of AI, blockchain analytics, and advanced transaction monitoring to improve fraud detection and prevention (Leuprecht et al., 2023). These interventions, combined with stronger internal controls—such as EDD, regular audits, and stringent compliance practices—help close operational loopholes and strengthen institutional defenses (Ministry of Justice, 2024). Finally, recognizing that money laundering and financial fraud are transnational issues, the framework underscores the importance of international cooperation through coordinated regulation, data-sharing arrangements, and harmonized enforcement practices (Moiseienko and King, 2025; Pavlidis, 2022).

In sum, this framework not only synthesizes the theoretical foundations of money laundering and fraud but also provides the analytical basis for the study’s research design, interview protocol, and thematic analysis. By combining macro-, meso-, and micro-level perspectives, it offers a holistic understanding of how scamming and money laundering intersect, with particular attention to Taiwan’s legal and regulatory context. Building on these theoretical perspectives, Figure 2 presents an integrated AML and financial fraud prevention framework that underpins the analysis and discussion in this study. It links macro-level environmental challenges, meso-level institutional factors, and micro-level fraud motivations with technological and regulatory interventions, forming the foundation for the discussion that follows.

Comprehensive anti-money laundering and financial fraud prevention mechanisms.

Research approach and method

This study adopts a qualitative single-case study design focusing on Taiwan and draws on grounded theory procedures to inductively develop a practice-informed theoretical framework. The research proceeded through two complementary data streams: (1) a systematic review and documentary analysis of domestic and international academic literature, government reports, and professional documents to map the regulatory and typological context, refine the interview protocol, and provide contextual triangulation; (2) semi-structured interviews with financial professionals as the primary empirical source for theory building. Accordingly, the “Research results and analysis” reports interview-derived categories/themes as the main findings, while documentary materials are used to contextualize and corroborate relevant claims where appropriate (Yin, 2018).

Subjects and sampling methods

This study focuses on professionals responsible for AML in financial institutions, covering the following roles: (1) Compliance officers, responsible for KYC procedures and STR reporting and directly involved in the compliance-risk management of financial institutions; and (2) risk-management personnel, responsible for monitoring and analyzing suspicious transactions to ensure the safety of fund flows. Taking financial professionals as the research subjects offers three advantages: (1) their extensive experience in compliance and risk management provides insight into practical AML challenges; (2) as frontline observers of policy implementation, they can assess the effectiveness and limitations of AML policies in practice; and (3) they contribute applied perspectives on the use of blockchain and data-analytics technologies in AML.

This study employs purposive sampling to conduct in-depth, semi-structured interviews with professionals who possess AML experience within financial institutions. Data saturation was deemed achieved when interview responses became repetitive, and no novel insights emerged (Guest et al., 2006). The initial plan was to recruit five to seven participants; however, saturation was reached after five interviews.

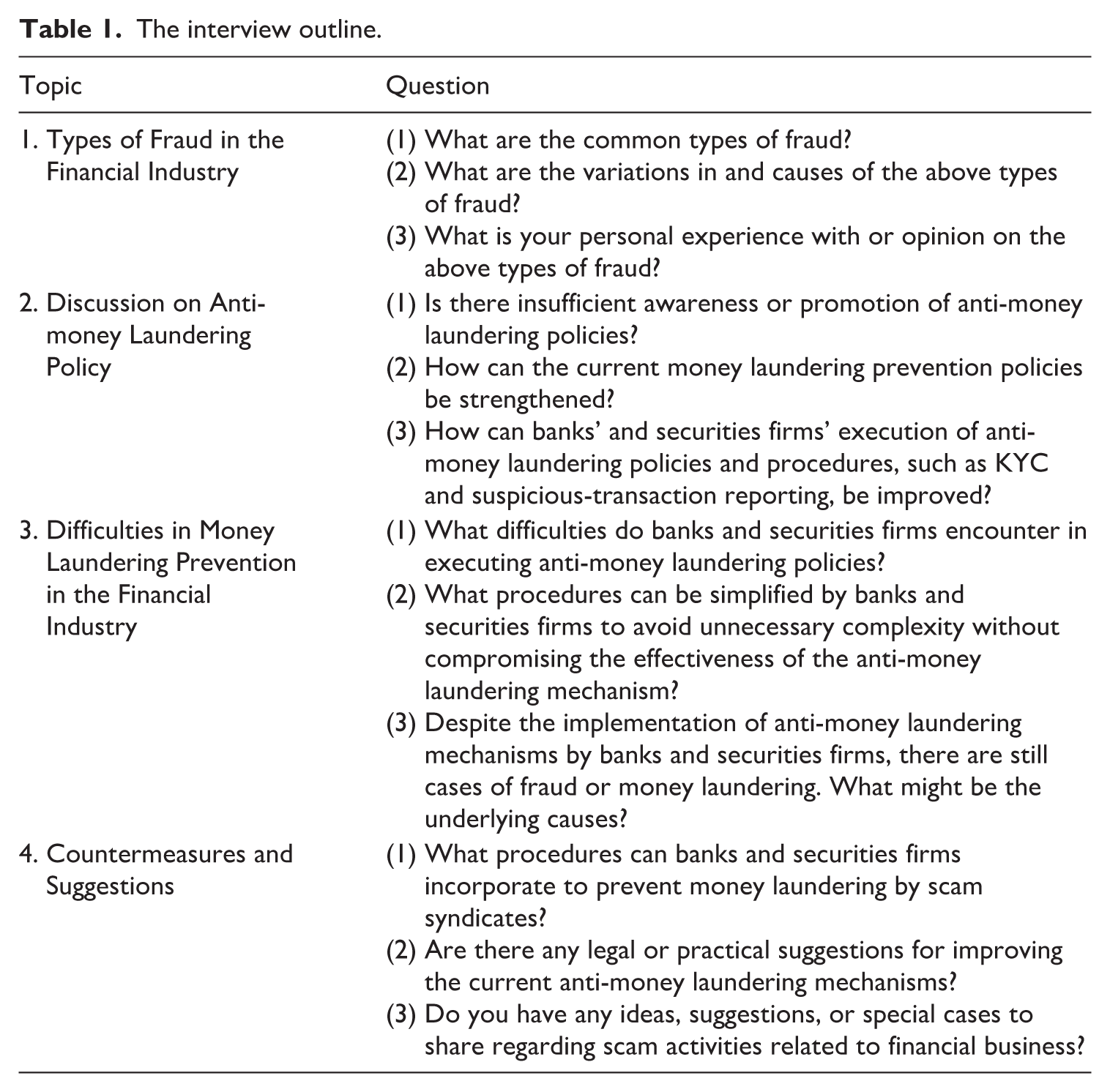

Interview outline

The design of the interview outline is informed by the following considerations:

In recent years, Taiwan has often been characterized in media discourse as the “Kingdom of Fraud,” reflecting the prevalence of fraudulent activities, including the widespread use of mule/dummy accounts by scam syndicates and high-profile cases in which victims have been wrongfully detained—sometimes referred to as the “Taiwanese version of KK Park.” The illicit proceeds derived from these schemes are frequently channeled into money laundering, with constantly evolving typologies that pose challenges for the effectiveness of AML policies. Although Taiwan has enacted the MLCA and related regulations and issues regular public advisories regarding ATM and digital-banking fraud, scam cases remain prevalent, underscoring persistent implementation challenges and gaps in policy effectiveness. Consequently, there is an urgent need to fortify AML measures.

The focus of the in-depth interviews covers four themes:

Common fraud types—investment fraud, job-recruitment fraud, and impersonation scams. With ongoing technological advancement, modus operandi continue to evolve, complicating victim identification and early detection.

Promotion and implementation of AML policies—public-facing outreach remains insufficient, limiting awareness and compliance. In addition, the complexity of financial institutions’ KYC processes and suspicious-transaction reporting (STR) procedures can affect client satisfaction; these workflows require optimization for efficiency without compromising risk controls.

Practical implementation difficulties—banks and securities firms report client dissatisfaction and technical constraints when implementing preventive measures. Moreover, the covert and complex methods of money laundering hinder timely detection, thereby constraining the effectiveness of existing mechanisms.

Countermeasures and capability building—prioritized investments in analytics, periodic control testing, and scenario-based training; improved inter-agency coordination and data-sharing protocols; and adaptive playbooks for emerging typologies.

Accordingly, this study recommends that financial institutions strengthen technical controls, enhance internal supervision, and dynamically update their prevention mechanisms to improve AML effectiveness. Incorporating insights from case studies and near-miss analyses can further bolster responsiveness to emerging threats.

The interview outline, therefore, covers four major areas: (1) common fraud types in the financial industry, (2) AML policy promotion and implementation, (3) implementation challenges, and (4) countermeasures and capacity enhancement. The interview questions are presented in Table 1.

The interview outline.

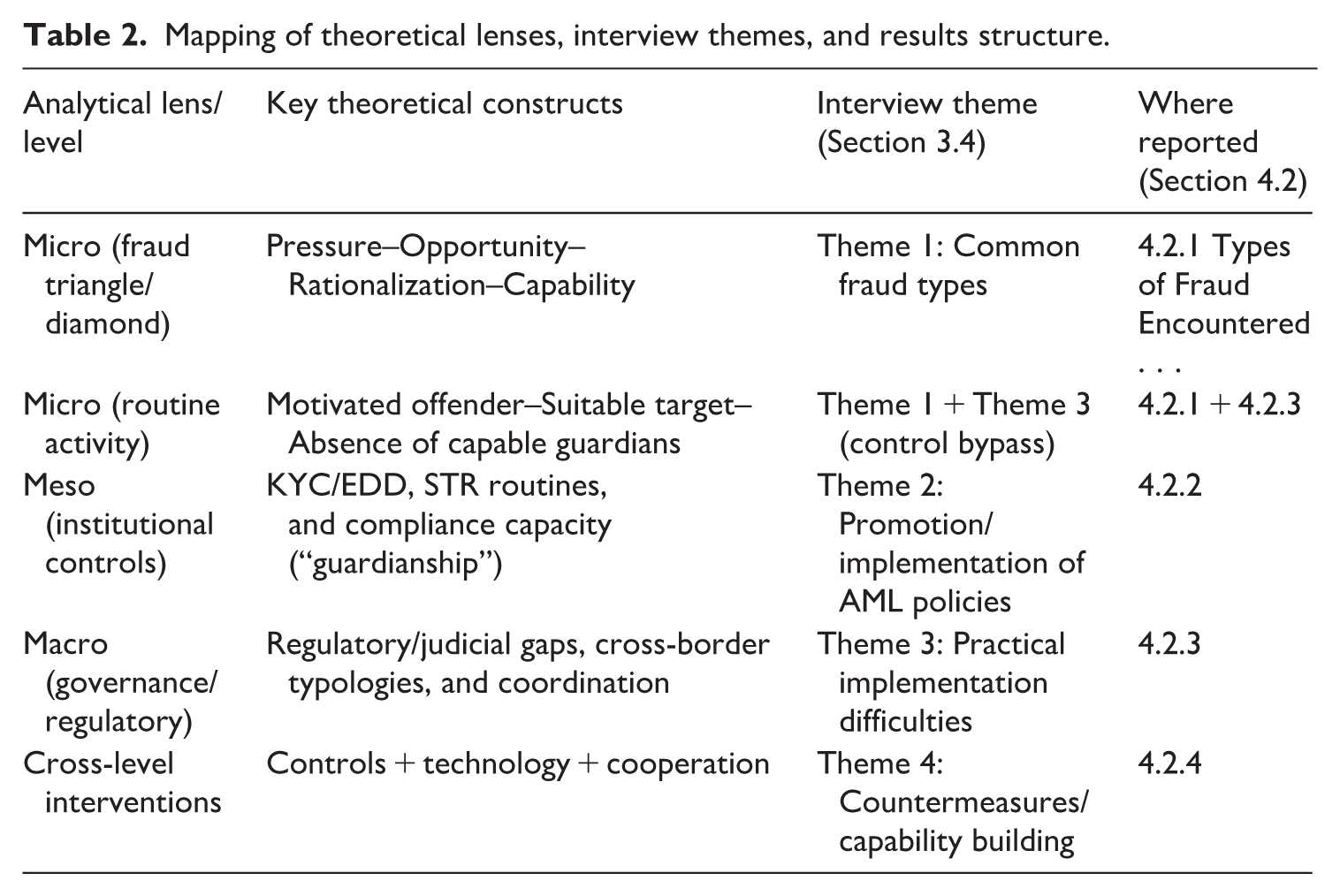

Linking the conceptual framework to the interview protocol and thematic results

Building on the integrated conceptual framework (Figure 2), this study explicitly connects micro-level fraud motivations with meso- and macro-level institutional and governance conditions to guide the interview protocol and subsequent thematic analysis. At the micro level, the Fraud Triangle and Fraud Diamond posit that fraud is enabled by the convergence of pressure (incentive), opportunity, and rationalization, with the Fraud Diamond further emphasizing capability as the fourth element that allows offenders to recognize and repeatedly exploit available “doorways” to fraud (Cressey, 1953; Wolfe and Hermanson, 2004). Consistent with opportunity-structure perspectives, routine activity theory also highlights that offending becomes more likely when motivated offenders converge in time and space with suitable targets in the absence of capable guardians, thereby providing a criminological rationale for examining how everyday financial routines and control “guardianship” may be bypassed (Cohen and Felson, 1979).

Guided by these theoretical lenses, the interview outline was structured around four interrelated themes that map onto the macro–meso–micro logic and directly inform the organization of the “Research results and analysis” (Section 4.2). Specifically, Theme 1 (Common fraud types) focuses on how evolving fraud typologies (including virtual-currency-enabled schemes) reflect offenders’ opportunity and capability to exploit digital channels and victims’ vulnerabilities. Theme 2 (Promotion and implementation of AML policies) examines meso-level compliance routines (e.g. KYC/STR workflows, risk-based implementation, and public outreach) that function as organizational “guardianship” to reduce opportunities for illicit flows. Theme 3 (Practical implementation difficulties) investigates how macro-level regulatory/judicial constraints and meso-level resource/technology limitations jointly create enforcement and compliance bottlenecks that sustain opportunity structures for laundering. Theme 4 (Countermeasures and capability building) captures cross-level interventions—strengthening internal controls and training, deploying analytics and virtual-asset tracing tools, and enhancing inter-agency and cross-border cooperation—to shrink fraud opportunity, disrupt offender capability, and improve system-wide AML effectiveness. Accordingly, Section 4.2 reports interview findings using the same four-theme structure to ensure coherence between the conceptual framework, interview protocol, and empirical results.

To make the logic of the research design transparent, Table 2 summarizes how the conceptual lenses (micro-level fraud mechanisms and macro–meso governance conditions) informed the interview themes and how those themes are carried forward into the results structure reported in Section 4.2.

Mapping of theoretical lenses, interview themes, and results structure.

Data analytics, reliability, and validity analysis

This study utilizes grounded theory (Strauss and Corbin, 1998) for data analysis, which is well suited to examining complex issues such as money laundering and fraud, especially when existing theories do not fully capture the dynamics of Taiwan’s financial environment. The process comprised data collection, analysis, and the application of reliability and validity checks.

Data collection

The data in this study were collected through semi-structured interviews with financial professionals working in AML, including compliance officers, risk managers, and KYC specialists. Participants were selected through purposive sampling to include individuals with direct experience of AML processes and fraud prevention. A total of five professionals were interviewed; after the fifth interview, data saturation was reached, as no new insights emerged. Part of the empirical material has been analyzed in prior Chinese-language publications; however, the present study reinterprets the data through a different theoretical lens. The interviews were audio-recorded and transcribed verbatim and analyzed using grounded theory to identify emerging themes and categories.

All interviews were conducted in Mandarin Chinese. Transcripts were first produced in Mandarin, and the initial coding and theme development were conducted using the original-language transcripts to preserve contextual nuance. For reporting purposes, illustrative quotations were translated into English by a bilingual researcher with domain familiarity in AML practices. To minimize potential meaning loss in cross-language qualitative reporting, the translated quotations were then checked against the original Mandarin transcripts by a second bilingual reviewer (via side-by-side comparison), and any discrepancies were resolved through discussion with reference back to the source-language wording. Consistent with methodological guidance on cross-language qualitative research, we retained the source language as long as possible during analysis and explicitly documented the translation procedure to enhance transparency and validity (Van Nes et al., 2010).

Data analysis

Following grounded theory procedures, the analysis proceeded through three iterative phases—open, axial, and selective coding—to build the final theoretical framework from the interview data (Charmaz, 2014; Strauss and Corbin, 1998). To enhance analytic rigor, the coding process was conducted by two members of the research team using an iteratively refined codebook. Prior to full coding, both coders independently coded a subset of the transcripts (approximately 25%, selected to reflect variation in professional roles) to calibrate code definitions and refine category boundaries. Discrepancies were discussed to reach consensus, and when disagreement persisted, a third senior researcher reviewed the evidence and served as an adjudicator. An audit trail was maintained to document codebook revisions, analytic memos, and decision rules throughout the iterative analysis (Miles et al., 2014).

1.

Open coding involved close, line-by-line examination of the verbatim transcripts to identify meaningful units related to fraud typologies, laundering pathways, and AML implementation experiences. Initial codes were recorded in a structured codebook (code label, definition, inclusion/exclusion criteria, and illustrative excerpts). Recurrent phrases and concepts were captured as preliminary codes and iteratively refined through constant comparison across interviews. In parallel, analytic memos were produced to record emerging interpretations and to document coding decisions and revisions (Charmaz, 2014; Strauss and Corbin, 1998).

2.

Following open coding, axial coding was used to specify relationships among categories by grouping related codes into higher-order categories and clarifying conditions, mechanisms, and consequences. Categories were organized into a category tree and aligned with the study’s four major reporting themes (see Section 3.5.4; Results Section 4.2): 1. Types of fraud in the financial industry, 2. AML policy discussions (promotion and implementation), 3. Challenges in preventing money laundering (practical implementation difficulties), and 4. Countermeasures and recommendations (capability building).

This step ensured that the thematic structure used to report findings was grounded in systematic category development rather than post hoc organization (Strauss and Corbin, 1998).

3.

In the final phase, selective coding integrated the major categories into a cohesive explanatory storyline and refined the core relationships underlying Taiwan’s AML and fraud-prevention mechanisms. Specifically, selective coding consolidated (a) macro-level regulatory and cross-border conditions, (b) meso-level institutional execution (e.g. KYC/EDD/STR routines and internal controls), and (c) micro-level fraud opportunity/capability dynamics into the integrated framework presented in Figure 2. The final theoretical explanation thus accounts for evolving fraud methods, the growing role of virtual assets, and the practical interventions required to strengthen AML prevention and detection (Strauss and Corbin, 1998).

4.

To enhance transparency, one representative coding chain is provided. Interview statements describing “checkbox-style KYC,” “limited time for verification,” and “fragmented information across units” were first captured as open codes (e.g. perfunctory KYC execution, workload-constrained verification, information silos). These were then clustered during axial coding under Theme 3: Practical implementation difficulties (e.g. institutional bottlenecks in KYC/EDD execution). During selective coding, this category was integrated into the core explanatory logic—namely, that meso-level compliance capacity gaps sustain laundering opportunities and weaken detection—thereby informing the intervention priorities summarized under Theme 4: Countermeasures and capability building (Strauss and Corbin, 1998).

Reliability and validity

To ensure the reliability and validity of the findings, methodological triangulation was employed (Bans-Akutey and Tiimub, 2021). This involved comparing and cross-referencing insights from different interviewees to ensure consistency and resolve discrepancies. In addition, interviews were conducted with professionals in various sectors, such as banks and securities firms, to obtain a comprehensive understanding of these issues.

Inter-coder reliability was assessed on the double-coded subset. Specifically, we computed percent agreement and Cohen’s kappa to evaluate coding consistency beyond chance (Cohen, 1960). The agreement results were reviewed alongside qualitative resolution notes to ensure that reliability was supported not only by statistical indices but also by transparent consensus-building and documented coding decisions (Miles et al., 2014).

Member checking was conducted by asking respondents to review the findings and provide feedback on their accuracy and relevance to real-world situations. This process helped to ensure that the interpretations were based on actual practice and were not unduly influenced by the researcher’s biases. Moreover, the constant-comparative method was applied throughout the analysis to maintain data integrity, ensuring that emerging theories remained grounded in the data.

Type of analysis and analytic categories (themes)

Guided by grounded theory procedures (Strauss and Corbin, 1998), the study applied iterative coding and constant comparison to develop a set of four primary analytic categories (reported as themes for readability) that structure both the analysis and the presentation of results (Section 4.2). To ensure methodological coherence, these categories are intentionally aligned with the interview outline and are reported in the “Research results and analysis” as four corresponding themes (Sections 5.2.1–5.2.4).

Category/theme 1: Types of fraud encountered in the financial industry

This category captures how respondents characterized dominant and emerging fraud typologies and how these schemes are operationalized in practice. Key subthemes include:

(a) Impostor and investment fraud as recurrent, high-volume modalities;

(b) Romance and social engineering scams exploiting psychological vulnerabilities (e.g. trust and emotional dependency);

(c) Digital-channel-enabled fraud (e.g. smishing, identity theft, and boiler-room operations) facilitated by messaging apps and social media; and

(d) Virtual-asset/cryptocurrency-related fraud linked to rapid and opaque cross-border value transfers.

Category/theme 2: Discussion on AML policy

This category concerns how AML policies are communicated, interpreted, and received across institutions and the public, highlighting the gap between policy dissemination and behavioral uptake. Key subthemes include:

(a) Evaluation of policy promotion and dissemination (e.g. institutional announcements and government communication materials);

(b) Public awareness and engagement, including uneven comprehension and the “awareness–action” gap;

(c) Communication effectiveness as operational guardianship, shaping customer cooperation during KYC processes; and

(d) Perceived enforcement inconsistency, including concerns that judicial variability can weaken deterrence and policy credibility.

Category/theme 3: Difficulties in money laundering prevention in the financial industry

This category synthesizes barriers and bottlenecks that hinder effective AML implementation in practice, spanning institutional routines and system-level constraints. Key subthemes include:

(a) Client cooperation challenges and skepticism during KYC and due diligence interactions;

(b) Rapid typology evolution that outpaces institutional updating and monitoring cycles;

(c) Perfunctory or inconsistent internal execution (e.g. “check-box” compliance and training gaps); and

(d) Regulatory and judicial ambiguities that complicate enforcement expectations and weaken compliance incentives.

Category/theme 4: Countermeasures and recommendations

This category consolidates respondents’ proposed improvement strategies, emphasizing multi-level capability building rather than single-point fixes. Key subthemes include:

(a) Strengthening KYC and internal controls, including risk segmentation and routine review mechanisms;

(b) Capability development through training and organizational learning, such as case-sharing and continuous professional development;

(c) Technology-enabled monitoring and analytics, including AI/ML tools and virtual-asset tracing capabilities; and

(d) Governance coordination, including interdepartmental collaboration and cross-border information sharing.

Taken together, these aligned categories/themes provide the analytic backbone for the interview-based findings in Section 4.2 and ensure that the methodological description (Section 3.5) and empirical presentation (Section 4.2) follow a single, consistent narrative logic (Strauss and Corbin, 1998).

Research results and analysis

Because interviews constitute the primary data for theory development in this qualitative case study, the results below focus on interview-based findings, with documentary sources referenced selectively for contextualization and triangulation (Yin, 2018).

Basic information about interviewees

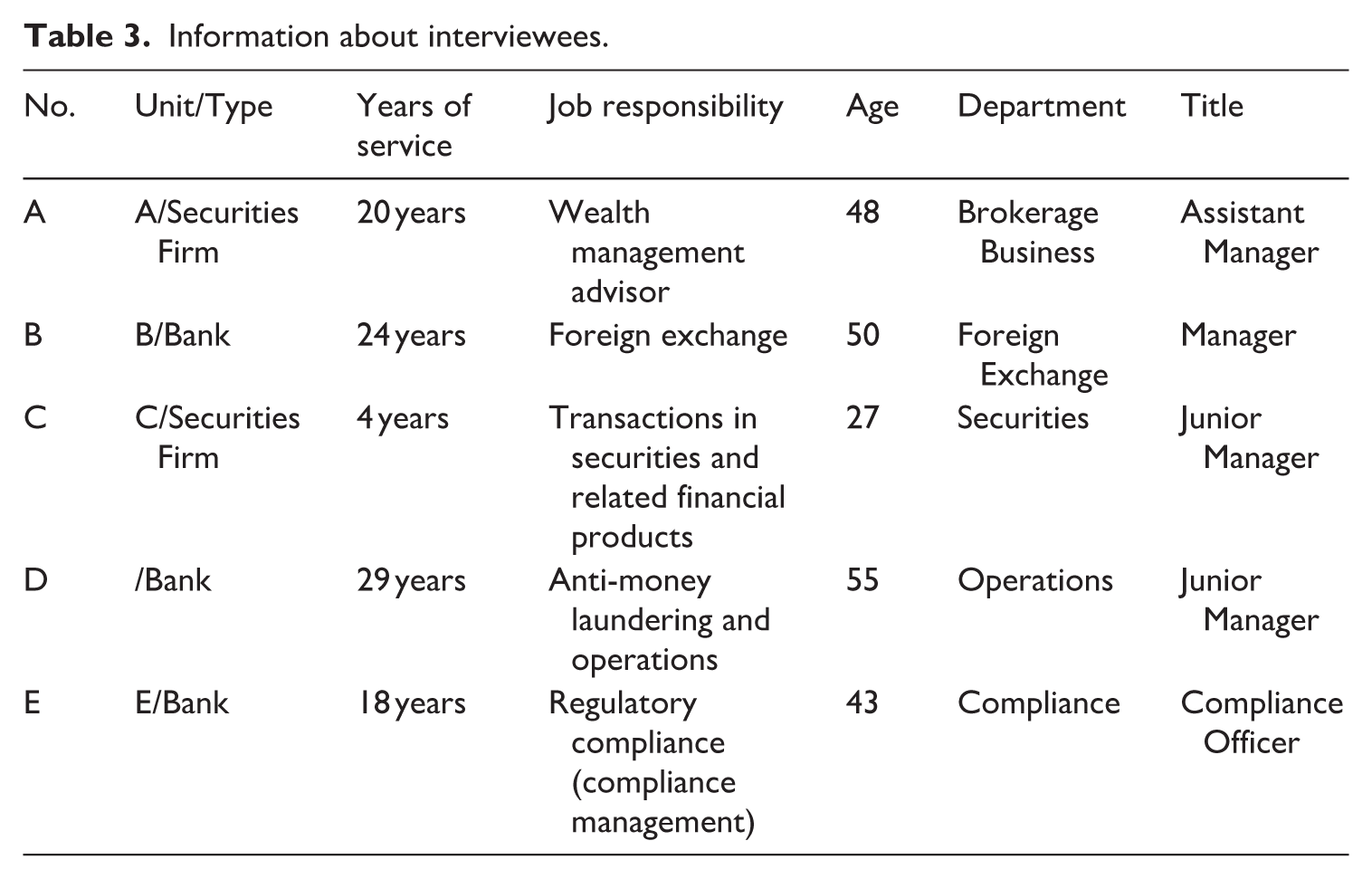

To understand the implementation of AML in the financial industry, this study collected financial professionals’ experiences, opinions, and suggestions through in-depth interviews with five securities specialists and bank staff, including compliance officers, risk-management supervisors, and staff. These professionals have extensive experience in AML, and their expertise is highly relevant to the execution of AML measures within their respective institutions. The interviewees are identified by letters “A” through “E,” with details shown in Table 3.

Information about interviewees.

Interview-based analysis of AML challenges and policy responses in Taiwan

The following analysis examines the interview data according to the research objectives and the established interview outline, focusing on four major themes: types of fraud in the financial industry, AML policy discussions, challenges in preventing money laundering, and proposed countermeasures and recommendations. This analysis not only addresses our RQ1–RQ4 (see Section 2.7) but also integrates empirical insights with theoretical frameworks to provide a comprehensive understanding of the challenges and potential solutions in Taiwan’s AML efforts.

Types of fraud encountered in the financial industry

This theme defines the dominant fraud typologies and their operational features as micro-level manifestations of fraud motivation and execution—highlighting how pressure, opportunity, rationalization, and perpetrator capability jointly shape laundering-adjacent scams in Taiwan (Cressey, 1953; Wolfe and Hermanson, 2004).

According to financial industry respondents, the most common types of fraud include impostor fraud, investment fraud, romance fraud, smishing, identity theft, boiler-room fraud, and cryptocurrency fraud. These schemes leverage modern communication tools and exploit victims’ psychological vulnerabilities, such as greed and trust.

1. Impostor and Investment Fraud

According to several interviewees, the most prevalent forms of fraud are impostor fraud and investment fraud. “The most common methods we see today are impersonation and investment fraud. Scammers often pose as legitimate securities firms or financial institutions to lure victims into joining online groups via SMS and messaging apps like LINE,” one respondent explained (A-1-1). In these schemes, fraudsters initially offer small returns to build trust and subsequently induce larger investments, which result in substantial losses. Investment fraud is typically characterized by promises of high and rapid returns. Fraudsters use persuasive language and, at times, invoke the reputations of so-called “financial gurus” to convince victims to invest significant sums. One interviewee noted, “Scammers will offer an attractive initial return (e.g. 10% or so) to earn your trust, but once you’re fully committed to investing, they’ll scam you out of more money” (C-1-1).

2. Romance and Other Fraud Schemes

Romance fraud involves scammers exploiting victims’ emotional vulnerabilities, cultivating fake relationships, and ultimately defrauding them of money. In addition, other fraud schemes such as smishing (SMS phishing), identity theft, and boiler-room fraud also play significant roles. Some interviewees highlighted emerging trends such as pump-and-dump schemes and fake high-yield investment programs, in which perpetrators disseminate false information to inflate stock prices and then liquidate their holdings for profit. A distinct example provided by one respondent described the use of social media: “We have seen cases where fraudsters create ‘skyrocketing stock’ groups on Facebook. They lure victims into these groups through fake advertisements and text messages. Once inside, the scammers provide stop-loss and day-trading advice that gives an illusion of professional expertise, leading victims to invest money, only for the scammers to suddenly dump the stocks and lock the accounts, leaving the victims unable to retrieve their funds” (E-1-1).

3. Cryptocurrency Fraud

As digital currencies grow in popularity, fraudsters have found new ways to launder money and deceive victims. Cryptocurrency fraud typically involves the use of virtual currencies to conceal the origin of funds and to facilitate cross-border transfers. Interviewees highlighted that these schemes benefit from the pseudonymity and speed of virtual-currency transactions, making detection and tracing extremely challenging (Subbagari, 2024).

Overall, the interviews reveal that fraud in the financial industry takes many forms, with impostor and investment fraud being the most common. However, the continuous evolution of scam techniques means that fraudsters continuously develop new ways to exploit vulnerabilities in technology and human psychology.

Discussion on AML policy

This theme focuses on meso-level “guardianship” and institutional signaling—how AML policies are communicated, interpreted, and internalized by the public and financial actors, thereby shaping compliance behaviors and the preventive reach of AML governance.

Taiwan’s current AML policy is widely disseminated through websites, media, government notices, and institutional announcements. While many interviewees consider these promotional measures relatively mature, there remain problems regarding public comprehension and engagement.

1. Evaluation of Promotional Efforts

Interviewees noted that the government’s promotional efforts are strong, particularly pamphlets and videos produced by the Executive Yuan and the Taiwan Stock Exchange. “The promotional efforts are comprehensive and have reached many financial institutions, including well-produced brochures and videos,” one respondent stated (B-2-1). This suggests that the policy has been implemented effectively at the operational level. However, a key concern is whether the public truly understands and accepts AML policies. One interviewee remarked, “While the government has been pursuing these policies, the real question is whether the public pays attention to and truly understands the information provided” (C-2-1), particularly among those with limited access to digital resources, such as the elderly or individuals who rarely engage in financial transactions.

2. Public Awareness and Engagement

Public education remains a critical gap in the current AML strategy. Although promotional campaigns are in place, interviewees consistently stressed that knowledge alone does not translate into proactive behavior. “People continue to fall victim to scams despite being exposed to promotional materials, which implies that awareness has not yet fully transformed into vigilance,” observed one participant (D-2-1). Therefore, the challenge lies not in the volume of information but in its effective delivery and the behavioral change it produces. Some respondents emphasized the importance of interactive, community-based education. “If AML promotion begins in schools and communities, it could significantly improve the public’s understanding of fraud risks,” suggested an interviewee (D-2-2). In addition, leveraging social-media influencers to reach younger demographics was recommended. “Collaborating with influencers on platforms such as YouTube can help spread AML awareness more effectively among tech-savvy populations,” noted another interviewee (E-2-2).

3. Gaps in Policy Impact

Despite the relative maturity of promotional measures, the policy’s impact is weakened by limited public engagement and understanding. Some interviewees pointed out that, despite active communication between financial institutions and regulators, the messages do not always resonate with the public. “The problem is not that the publicity is insufficient, but that the message fails to effectively engage the audience,” explained one respondent (C-2-1). This disconnect can lead to a situation where—despite high reported awareness—actual preventive behavior remains suboptimal. Moreover, inconsistencies in judicial interpretation further undermine the effectiveness of AML policies. The deterrent effect is weakened by discrepancies in penalties and determinations in cases of fraud involving mule/dummy accounts or account providers. One interviewee stated, “The court’s sometimes conflicting standards for punishing account providers create opportunities for fraudsters” (D-3-1), emphasizing the need for greater consistency in enforcement.

Difficulties in money laundering prevention in the financial industry

This theme identifies the practical bottlenecks that erode AML effectiveness at the meso level (institutional operations) and at the macro interface (regulatory and judicial frictions), where implementation gaps widen opportunities for laundering and fraud to persist.

The implementation of Taiwan’s AML policies faces multiple challenges that hinder the effective prevention of financial fraud and money laundering. These challenges can be grouped into issues related to client cooperation, rapidly evolving fraud methods, internal operational deficiencies, and regulatory ambiguities.

1. Client Cooperation and Awareness

One of the most significant challenges is the lack of client cooperation. Many individuals are either unaware of AML policies or skeptical about their purpose. This reluctance undermines the KYC process, a cornerstone of effective AML controls. As one interviewee explained, “Clients are defensive and often worry about being scammed by securities specialists. When asked to provide basic personal information during KYC, some refuse, resulting in their accounts being flagged or even frozen” (B-3-1), which not only impedes data collection but also diminishes the overall effectiveness of AML monitoring systems. In addition, clients’ speculative tendencies also play a significant role. Despite being aware of the risks, some continue to engage in high-risk investments, driven by greed and overconfidence. “I have a client who kept investing in Hong Kong stocks despite recognizing the risks; initial gains fueled overconfidence—much like a pyramid scheme—but eventually he incurred substantial losses,” stated one respondent (B-3-3).

2. Rapidly Evolving Scam Methods

Fraudsters are constantly updating their tactics, and existing AML systems struggle to keep pace. Scammers integrate advanced technology and continuously devise new ways to bypass traditional surveillance systems. One interviewee commented, “The methods used by fraudsters are evolving so quickly that our preventive measures often become obsolete before we can even update them” (C-3-1), illustrating the dynamic and rapidly changing nature of these schemes. This rapid evolution includes the use of virtual accounts, multi-tier fund transfers, and sophisticated digital platforms that mask the source of illicit funds. The problem is further exacerbated by virtual currencies, whose pseudonymity and ease of cross-border transfer make it exceptionally challenging for regulators to trace and monitor illicit financial flows (Subbagari, 2024).

3. Inadequate Internal Execution

Operational deficiencies within financial institutions also pose a significant barrier to effective AML implementation. Several interviewees highlighted that while policies and procedures exist, on-the-ground execution can be perfunctory. “Although our policies require detailed verification during the KYC process, in practice some employees simply tick the boxes and submit the results without verifying details with clients” (E-2-3). This lack of diligence enables exploitation of procedural loopholes and elevates money laundering and fraud risk. In addition, these issues are compounded by inadequate on-the-job training, as employees may lack the necessary up-to-date knowledge to identify and respond to new scam methods. “Regular training is crucial, but many of our employees still lack the necessary updates to keep up with evolving fraud tactics,” stated another interviewee (D-2-3).

4. Regulatory and Judicial Challenges

Regulatory ambiguity further undermines AML efforts. Despite the maturity of the legal framework, inconsistencies in enforcement and judicial interpretation create gaps that offenders can exploit. Some interviewees expressed concerns about the variable treatment of individuals who provide mule/dummy accounts. “There is a wide variation in the way the courts handle cases related to false or rented accounts, which makes it difficult to establish a strong deterrent against money laundering,” remarked one respondent (D-3-1). Such a lack of uniformity may discourage strict institutional enforcement, given uncertainty about judicial follow-through. Consequently, even well-designed AML policies may fail to achieve the desired results if they are not enforced consistently.

Countermeasures and suggestions

This theme consolidates capability-building responses across governance levels—linking micro-level fraud dynamics, meso-level control enhancements (e.g. KYC/STR execution), and macro-level coordination (regulatory alignment and cross-border cooperation) into actionable institutional reforms.

Based on the challenges identified, interviewees proposed a range of countermeasures to enhance the effectiveness of AML and fraud-prevention efforts in the financial industry. The suggestions fall into four primary areas: improving internal processes and KYC procedures, leveraging technological innovations, enhancing public education and awareness, and strengthening regulation and interdepartmental cooperation.

Synthesis and future directions

Integrating the above findings and countermeasures, the interview evidence points to a multicomponent prevention approach that simultaneously addresses technical, organizational, and behavioral vulnerabilities. In line with the Fraud Triangle and Fraud Diamond, the persistence of fraud and laundering is not driven solely by external technological change but also by opportunity structures created through uneven execution of internal controls, limited public engagement, and enforcement frictions (Cressey, 1953; Wolfe and Hermanson, 2004). Accordingly, the proposed response package emphasizes (a) strengthened KYC/EDD routines and internal controls, (b) continuous training and case-based learning for frontline staff, (c) targeted and behavior-oriented public education, and (d) coordinated regulatory, judicial, and cross-departmental collaboration—supplemented where feasible by technology-enabled monitoring such as AI/ML and virtual-asset analytics. Together, these elements form an adaptive framework capable of responding to evolving fraud typologies and laundering pathways in Taiwan’s financial sector.

Future research should evaluate the long-term effectiveness of these interventions, particularly under rapid advances in AI, blockchain analytics, and digital financial services, and assess how implementation outcomes vary across institutional types and population groups. Additional work is also needed to clarify how regulatory and judicial consistency conditions the deterrent effect for mule/dummy account facilitation and laundering-related offenses and how cross-border information sharing can be operationalized despite jurisdictional constraints. As one interviewee summarized, “Our fight against fraud is not only about catching criminals, but about building a system that protects trust, and every stakeholder—from individual clients to large institutions—plays a role in maintaining financial integrity” (E-4-1).

In summary, the fight against fraud and money laundering in Taiwan’s financial industry requires an integrated approach that combines theoretical insights with practical strategies. By understanding fraud through the Fraud Triangle and Fraud Diamond frameworks, we can identify key weaknesses such as insufficient internal controls, rapidly evolving fraud methods, and inadequate public awareness. The interview data provide empirical support for these challenges and yield actionable recommendations, including strengthening KYC procedures, leveraging advanced technologies, enhancing public education, and promoting robust interdepartmental and international cooperation. Addressing these multifaceted challenges is essential to maintain financial stability and protect vulnerable populations. Going forward, sustained policy and technological innovation—coupled with concerted efforts to educate and engage the public—will be critical to reducing the incidence of fraud and money laundering. Only by adopting a holistic and adaptive approach can the financial community in Taiwan and beyond effectively mitigate fraud risks and help ensure a safer economic environment for all.

Conclusions and recommendations

In an ever-changing global financial environment, money laundering and fraud in Taiwan have become increasingly complex. Through interviews and a review of the literature, this study identifies the challenges in implementing existing AML policies and offers suggestions for improvement. The following sections present the discussions and key findings of this study:

Discussion

To strengthen coherence between the literature review, the interview-based results (Section 4.2), and the proposed framework (Figure 2), this discussion is organized around the same four themes reported in the results. This structure enables a transparent analytic dialogue in which each theme is first summarized as an empirical finding, then interpreted through relevant theoretical and empirical scholarship, and finally articulated as a specific contribution to AML research and practice in Taiwan’s rapidly evolving fraud and virtual-asset environment. Importantly, to avoid repetition with the synthesis provided in Section 4.2.5, the discussion below emphasizes interpretation, explanatory mechanisms, and theoretical/practical contributions rather than re-listing policy recommendations.

Theme 1: Fraud typologies as evolving micro-level mechanisms

Core finding

The interviews indicate that fraud in Taiwan’s financial ecosystem is no longer dominated by a single scheme type; rather, it is characterized by a portfolio of hybrid, technology-enabled scams (e.g. impostor and investment fraud, romance fraud, smishing, and cryptocurrency-related fraud). These schemes exploit both technological channels (messaging apps, social media, and virtual-asset rails) and predictable psychological vulnerabilities (e.g. trust, greed, and emotional dependency), thereby increasing the speed and scale at which illicit funds can be mobilized and layered across accounts and platforms.

Link to theory and literature

Interpreted through the Fraud Triangle and Fraud Diamond, these findings suggest that contemporary fraud–laundering linkages are best understood as a dynamic combination of (a) pressures and inducements faced by victims and perpetrators, (b) rapidly expanding opportunities enabled by digital platforms and cross-border transferability, (c) rationalization processes facilitated by social engineering narratives, and (d) perpetrator capability strengthened by technological literacy and organizational coordination (Cressey, 1953; Wolfe and Hermanson, 2004). The results also align with the literature emphasizing that digital financial integration and virtual currencies have lowered frictions for cross-border movement of illicit funds, thereby exposing the limitations of conventional monitoring systems (Abukari, 2026; Subbagari, 2024).

Contribution and gap addressed

The study contributes by showing how “fraud typology mutation” operates as a micro-level driver that continually outpaces static AML controls. Rather than treating fraud types as descriptive background, the interviews demonstrate that typologies constitute an empirical entry point into understanding how laundering pathways are constructed and adapted in practice—particularly when perpetrators leverage virtual assets to increase speed, obfuscation, and jurisdictional complexity.

Theme 2: Policy communication and public engagement as meso-level guardianship

Core finding

Interviewees generally regarded Taiwan’s AML policy dissemination as institutionally mature in form (e.g. government websites, media, notices, and institutional announcements) yet limited in effect due to uneven public comprehension, weak behavioral uptake, and persistent “awareness–action” gaps. Respondents highlighted that exposure to AML messaging does not reliably translate into vigilance or compliant cooperation during KYC interactions, particularly among groups with limited digital access or low perceived relevance.

Link to theory and literature

This pattern is consistent with the broader literature suggesting that AML effectiveness relies not only on rule design but also on social uptake and compliance behavior in everyday financial interactions. In practice, policy communication functions as a meso-level guardianship mechanism: it shapes whether customers interpret KYC requests as legitimate controls or as intrusive, burdensome, or even suspicious demands. The interviews further suggest that when communication fails to generate behavioral change, policy implementation becomes vulnerable to displacement effects—fraudsters can continue exploiting routine cooperation gaps even when formal AML messaging appears extensive.

Contribution and gap addressed

The study advances existing discussions by specifying how “communication effectiveness” becomes an operational constraint in AML governance. It identifies public engagement not as a peripheral educational issue but as a direct determinant of KYC feasibility, customer cooperation, and the downstream quality of monitoring signals that institutions depend on for risk identification.

Theme 3: Implementation bottlenecks and the meso–macro friction of AML practice

Core finding

Beyond external threats, interviewees emphasized internal and system-level constraints that weaken AML performance: inconsistent KYC execution, insufficient training, perfunctory “check-box” compliance, and difficulties keeping pace with rapidly evolving scams. These operational deficiencies were compounded by regulatory ambiguities and judicial inconsistencies, which were perceived to undermine deterrence and create enforcement uncertainty—particularly in cases involving mule/dummy accounts and account providers.

Link to theory and literature

These findings reinforce the argument that AML capacity is jointly determined by institutional routines and the broader regulatory–judicial environment. Even when formal KYC systems have improved, operational integrity depends on consistent staff capability, updated typology awareness, and internal control discipline—conditions that may lag behind the speed of fraud innovation (Hong, 2022; Li, 2024; Sambrow and Iqbal, 2022; Viritha et al., 2015). The interviews further imply that macro-level inconsistency (e.g. interpretive variance in judicial outcomes) can weaken meso-level compliance incentives, thereby eroding the credibility and expected payoff of rigorous AML execution.

Contribution and gap addressed

The study contributes by empirically characterizing AML governance as a multi-level coordination problem rather than a purely technical compliance task. It clarifies how the meso–macro interface—where institutional routines meet regulatory and judicial practice—can become a persistent “friction point” that expands opportunity structures for laundering and fraud, even when institutions nominally possess AML policies and tools.

Theme 4: Capability building as a multi-level reform package

Core finding

Rather than pointing to a single “silver bullet,” interviewees converged on a capability-building logic in which technological tools, organizational routines, and governance coordination must function as a coupled system. In this sense, “capability building” is best interpreted as an alignment problem: detection capacity (data/analytics), execution capacity (KYC/STR discipline and training), and governance capacity (regulatory and cross-unit coordination) must reinforce one another to remain effective under fast-changing fraud typologies.

Link to theory and literature

The findings resonate with scholarship emphasizing that AML modernization requires both technological and organizational readiness. While AI/ML tools can increase anomaly detection and shift monitoring toward more proactive risk identification, their effectiveness depends on data quality, execution discipline, and governance coordination that can translate detection into timely intervention (Ijiga et al., 2024; Okonta and Nnamdi, 2025; Yi, 2024). Moreover, the transnational nature of laundering underscores the need for harmonized standards and cross-border cooperation to reduce jurisdictional arbitrage (Arnone and Borlini, 2010).

Contribution and gap addressed