Abstract

India's education sector is one of the largest in the world, with over 260 million students enrolled in more than a million schools and universities. The country's education system is facing several challenges, including low levels of learning outcomes, inadequate infrastructure, and a shortage of skilled teachers. In recent years, the EdTech industry has emerged as a potential solution to these challenges, providing students with access to quality education and personalized learning experiences. This case study explores the revolutionary growth and challenges faced by the EdTech industry in India.

Introduction

India has been experiencing a surge in the adoption of educational technology (EdTech) in recent years. India has the biggest K–12 student population in the world, with an estimated enrollment rate (2017–2018) of 250 million students in 1.5 million institutions nationwide. Therefore, improving the educational system to take advantage of EdTech and ICT-driven learning will undoubtedly help in the overall development of human capital and consequent increase in productivity, as well as technological advancements in India that result in higher economic growth. This motivation has encouraged the Indian education sector to develop into a breeding ground for emerging EdTech companies in recent years. Initiatives from both the private and public sectors have been observed to be expanding in order to mainstream and integrate EdTech into the Indian educational system.

The launch of the EDUSAT satellite serves as a stepping stone for the Indian EdTech community. The Indian Space Research Organization (ISRO) undertook a project worth INR 5.5 billion in September 2004 to deploy this satellite, which was made specifically to meet the needs of the nation's educational system. In order to provide education through visualization made possible by video programmes broadcast by the satellite, the satellite was specifically used to establish virtual classrooms in remote regions of India.

E-learning platforms like Extramarks and Khan Academy gained popularity in India in 2008 as private companies entered the market. As a result, startups in India's market with a large user base eventually began receiving successful business models from EdTech. In 2015–2016, this steady increase peaked and became an EdTech boom. Nearly 1000 EdTech startups applied to join the EdTech venture in India in 2015 alone, according to reports in The Economic Times and estimates made by NASSCOM, with an expected funding of $125 million. In parallel, Indian students began participating in other globally renowned platforms. More than 1.5 million students enrolled in online classes on the MyStory platform in 2015, according to the report.

The Indian education sector has developed into a breeding ground for many flourishing and booming EdTech companies, which is in line with the huge potential of the Indian market. In India, there are currently about 4530 EdTech companies, of which more than 400 were established after 2019 (Fazzin, 2022). Recent investments in Indian EdTech startups have totaled almost $4 billion over the last 2 years, of which $2.2 billion was made in 2020 alone, immediately following the country's countrywide lockdown that paralyzed the education sector. The list of global EdTech unicorns (companies valued at more than $1000 million billion) has grown by three more Indian names thanks to an extra $1.9 billion investment made in 2021.

Government policies are also focusing on EdTech in privately pursued EdTech ventures in India, like EDUSAT. In order to achieve Sustainable Development Goal (SDG) 4 (to provide quality education for its citizens), the National Education Policy (NEP) 2020 embodies the very concept of EdTech in the day-to-day operations of schools. NEP also proposes to deliver educational content to the general public through standardized multimedia platforms, such as radio and television. Students will be able to access courses according to their needs and preferences from 30 May 2020, as the top one hundred universities across the country are allowed to offer online courses from that date itself. Relocating and worrying about geographic barriers, to bridge the gap between facilities and academic resources, the country's educational system needs technological projects.

The Big Role of Technology in Indian Education

Education technology is the concept of teaching and learning through the well-organized medium of technology. The highlights of National Educational Policy 2020 show that technology should be properly integrated into all levels of Indian schooling with the goal of improving instructional methods and fostering teacher professional growth. Improved educational opportunities for those with limited resources, especially children with special needs, will also be a part of this. Future educational planning, administration, and management in Indian schools and universities will also be streamlined through the use of technology. In addition to incorporating technology, the new policy has done away with the 10+2 framework of the school curriculum in favor of a 5+3+3+4 structure. Basically, the length of time it takes to graduate is now 3 years.

The Government of India has declared the lock down and shutdown of educational institutions as a sensible measure to impose social distance within communities (Irfan and Singh, 2021; Yikici et al., 2022). To confirm their choice for students to take advantage of and continue their education during lockdown, the Ministry of Human Resource Development shared a number of free digital e-learning platforms with them in a press release on March 21, 2020, including the National Programme on Technology Enhanced Learning (NPTEL), Study Web for Active Young Expiring Minds (SWAYAM), e-Pathshala, DIKSHA portal, SWAYAM Prabha, National Repository of Open Educational, etc. The ministry also urged HEIs to keep teaching online and asked instructors to conduct their classes from home. With the introduction of new, innovative educational approaches to teachers and students through COVID-19, the old teaching model was replaced with EdTech methodologies (Anand Shankar Raja and Kallarakal, 2021; Watson et al., 2013).

Revolution of EdTech

The EdTech industry in India is witnessing a significant shift in the ways education is imparted and accessed. The industry today is focusing on providing customized and personalized learning experiences to its customers. With its increased adoption, the industry in India has seen tremendous growth in investment and funding in the last few years. From offline to online education, from traditional to innovative teaching methods, EdTech in India has come a long way. It has developed diverse learning models like gamification, adaptive learning, and Artificial Intelligence (AI) that have transformed the education industry in India.

The accessibility of mobile technologies is another element fueling the growth of online learning. Because of the widespread use of smartphones and tablets, students can now access educational materials at any time and from any location (Domingo and Garganté, 2016). The demand for mobile-friendly information has increased as a result, which has led to the development of learning platforms that can be accessed via mobile devices. Additionally, because it avoids expenses related to actual classrooms, such as rent, utilities, and maintenance, online education is more affordable than traditional forms of education. This opens up online education to a wider spectrum of students, including those who might not have otherwise had access to it (Ruiz-Iniesta et al., 2018).

Students are also able to select from a greater variety of courses and faculties because online education is expanding and is no longer restricted by geography. As a result, students can access education from organizations all over the world from the convenience of their own homes. The emergence of EdTech platforms has the potential to completely transform the education sector.

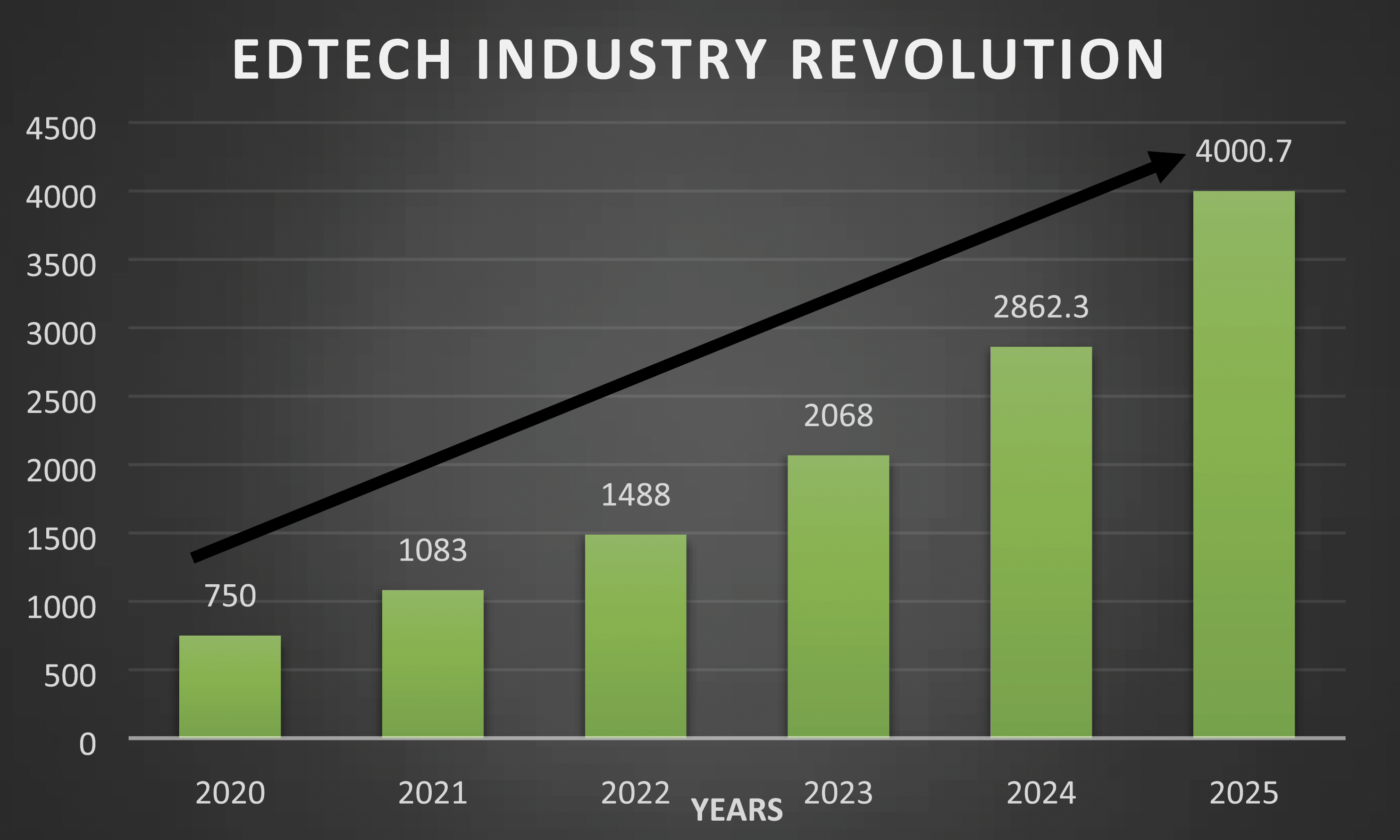

According to Figure 1 chat results, the EdTech industry has been growing rapidly over the past few years. In 2020, the industry revolution was at 750 billion, which increased to 1083 billion in 2021. In 2022, the industry revolution reached 1488 billion, and it is expected to continue growing in the coming years. In 2023, the industry revolution is expected to reach 2068 billion, and in 2024, it is expected to reach 2862.3 billion. By 2025, the industry revolution is expected to reach 4000.7 billion. This growth can be attributed to the increasing demand for digital tools in classrooms, especially during the global lockdowns that disrupted traditional face-to-face ways of teaching and learning. Finally, EdTech in India is growing rapidly and is expected to reach $10.4 billion by 2025 with 37 million paying users. Revolutionary Growth of EdTech Industry. Source-India brand equity foundation (IBEF)

After COVID-19, when the education sector was adversely affected, there has been a noticeable increase in this sector. More businesses joining this market with better services is a result of the demand for technological advancement in the currently used traditional educational system. According to a survey by PGA Laboratories and IVCA, India's education sector is anticipated to increase from $117 billion in 2020 to $225 billion by 2025.

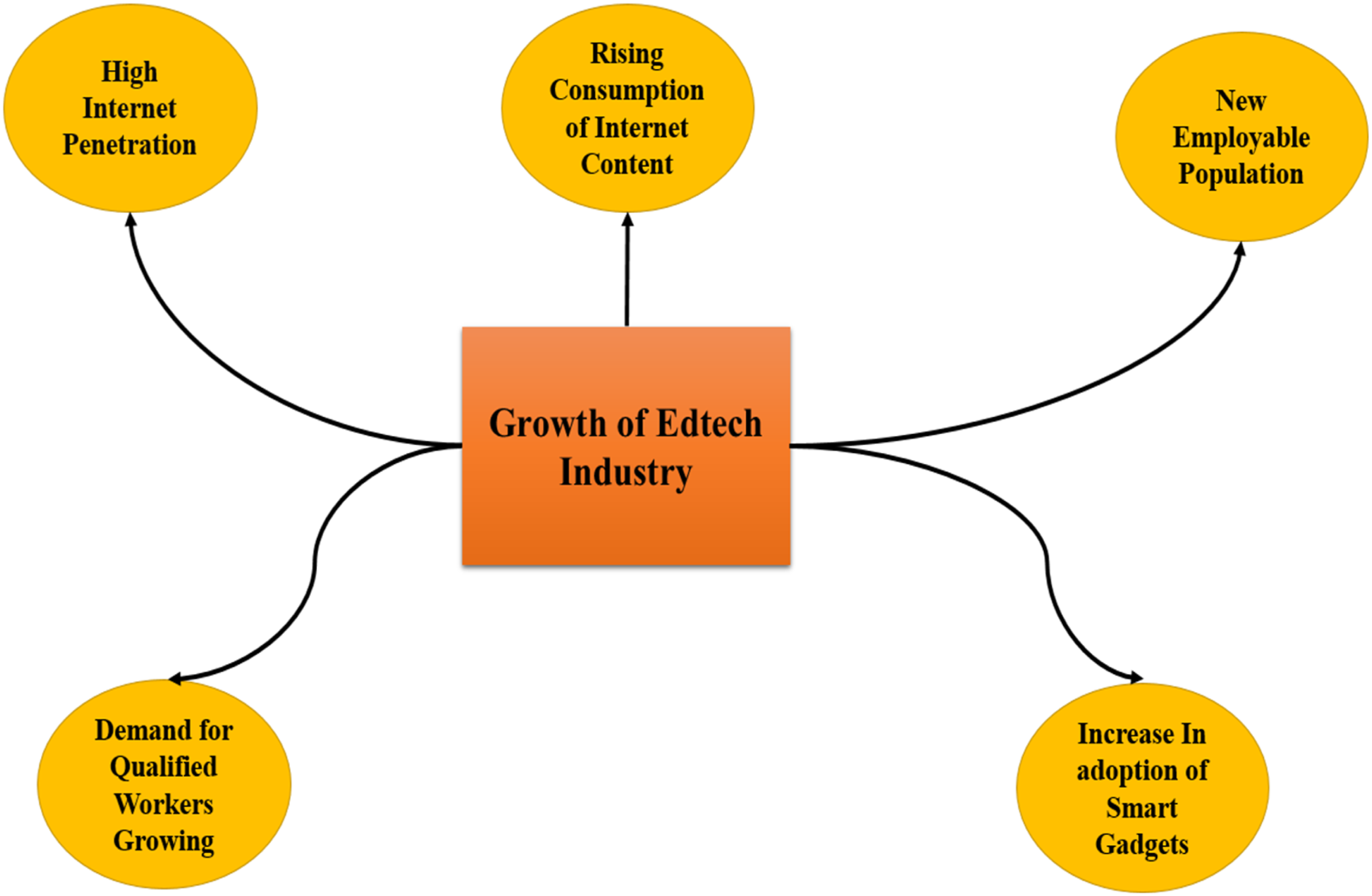

Major Drivers of EdTech Industry Growth

The following are few major drivers to the growth of EdTech industry in India (Figure 2). Growth of EdTech industry in India

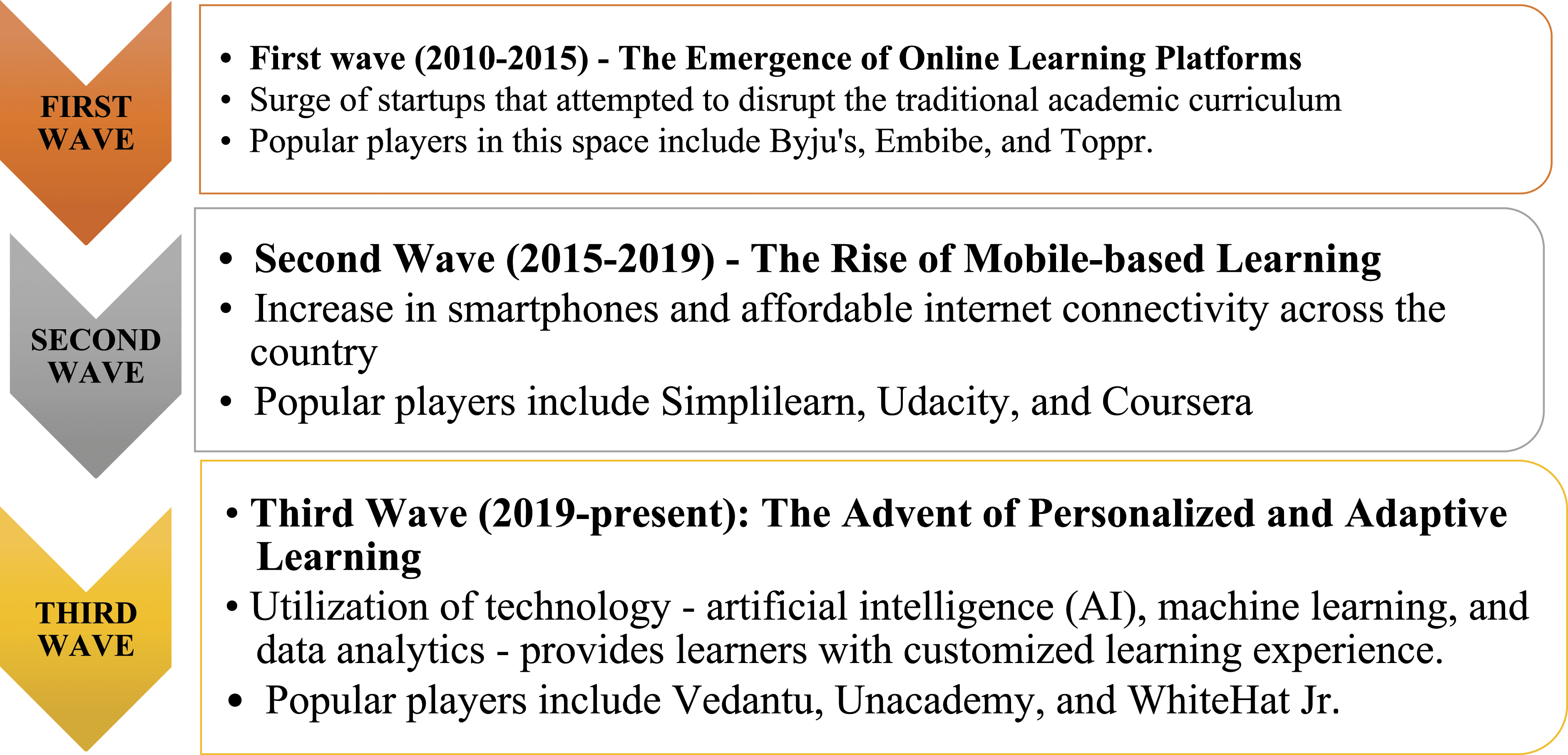

India has seen three major waves of EdTech platforms in recent years. These waves are categorized by technology and business model (shown in Figure 3). EdTech Startup Landscape in India

First Wave of EdTech in India (2010-2015): The Emergence of Online Learning Platforms

The first wave of EdTech in India saw a rise in online learning platforms that enhanced traditional classroom teaching through customized content and effective student progress monitoring. It also saw startups disrupting the academic curriculum by offering skills training and vocational courses. Initially focused on video-based content and test preparation, these platforms monetized through subscription models. Byju's, Embibe, and Toppr were notable players. This wave marked a significant shift towards digital education, fostering an evolving industry driven by new technologies.

Second Wave of EdTech in India (2015-2019): The Rise of Mobile-based Learning

The second wave of EdTech in India is characterized by a shift towards mobile-based learning, facilitated by widespread smartphone availability and affordable internet access. Mobile learning provides flexibility and accessibility, allowing learners to access educational resources at their convenience. It has been particularly beneficial in improving education quality in remote areas. This wave has spurred the development of innovative educational apps and platforms catering to diverse learning needs. It has also led to the emergence of marketplaces and learning management systems (LMS) that offer various courses and content from multiple providers. Notable players in this space include Simplilearn, Udacity, and Coursera.

Third Wave of EdTech in India (2019-Present): The Advent of Personalised and Adaptive Learning

The third wave of EdTech in India introduces personalized and adaptive learning, utilizing AI, machine learning, and data analytics to tailor educational experiences to individual needs. Adaptive learning platforms analyze student performance data to identify areas for improvement and recommend personalized learning paths. This approach benefits students who struggle with traditional teaching methods or have diverse learning needs. Online tutoring and learning platforms are prominent in this wave, offering personalized and adaptive learning experiences through AI algorithms and live tutoring sessions. Popular players include Vedantu, Unacademy, and WhiteHat Jr. However, successful implementation requires investment, infrastructure, and teacher training.

Overall, the EdTech industry in India has seen significant growth in recent years, driven by factors such as increasing internet penetration, the availability of affordable smartphones, and a growing demand for upskilling and reskilling opportunities.

Indian EdTech Industry Categories

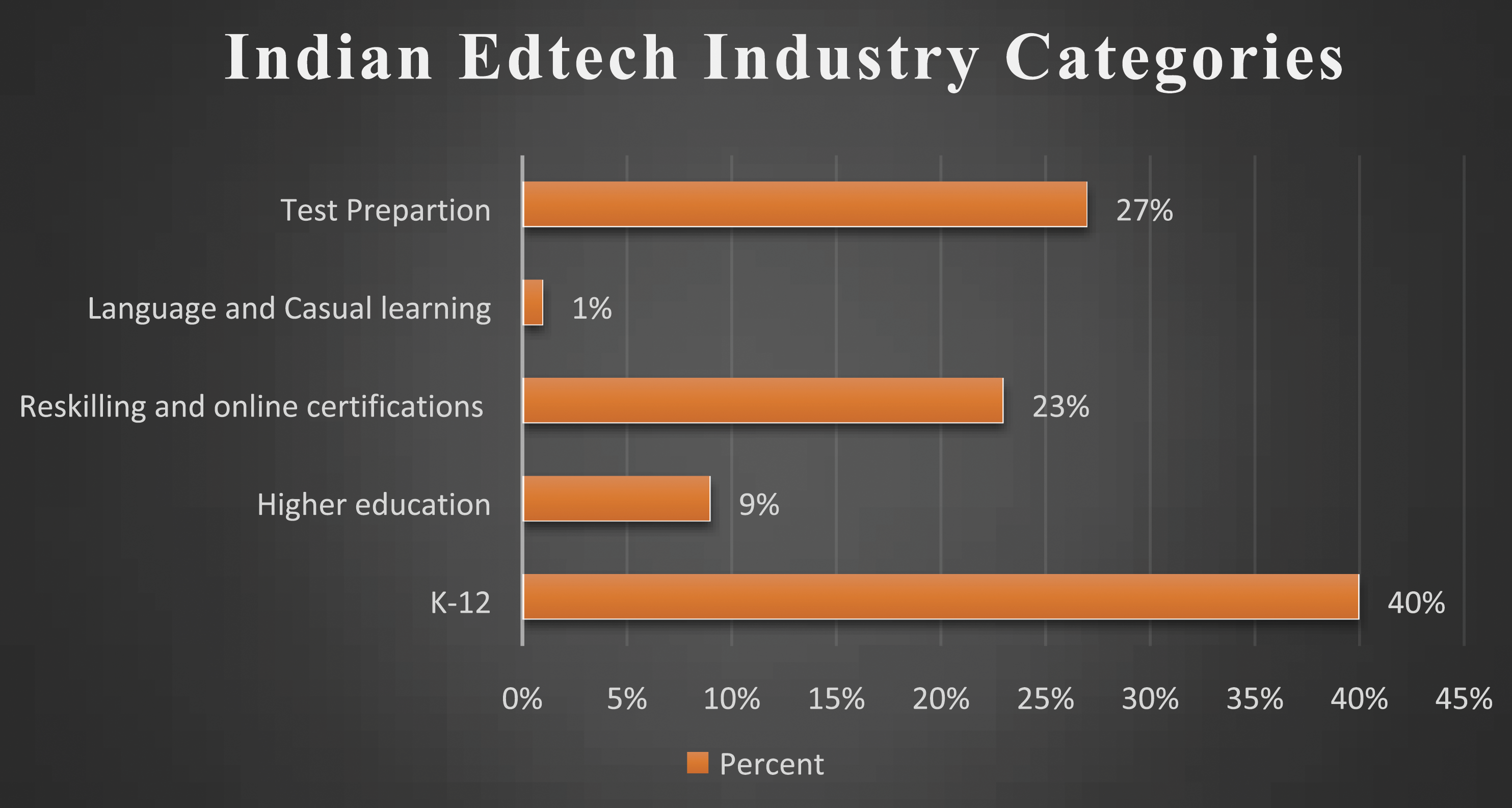

Figure 4 illustrates a breakdown of the Indian EdTech industry by category and percentage. The market share of K-12 (Kindergarten through 12th grade) education is 40%. The products and services of educational technology that are aimed at elementary and secondary school pupils are referred to here. 9% of the market is occupied by higher education. The products and services in this category are geared towards college and university students and are related to education technology. Retraining and online certificates account for a significant 23% of the industry. This category includes educational technology goods and services that have a focus towards reskilling and upskilling the workforce through online training and certification courses. Indian EdTech Industry Categories

Language and casual learning account for 1% of the market. Language learning and general interest themes are covered in this category of educational technology products and services.

Test preparation commands a sizable market share of 27%. This category includes educational technology goods and services that assist students in preparing for a variety of competitive exams, such as college admission exams, government job exams, and professional certification exams.

Indian Government Initiatives in EdTech

Indian government wants to see a rise in digital dominance and intensity. The appropriate government agencies have implemented a number of steps to support online learning and skill development in the entire country. Here is a brief outline of a few government programmes.

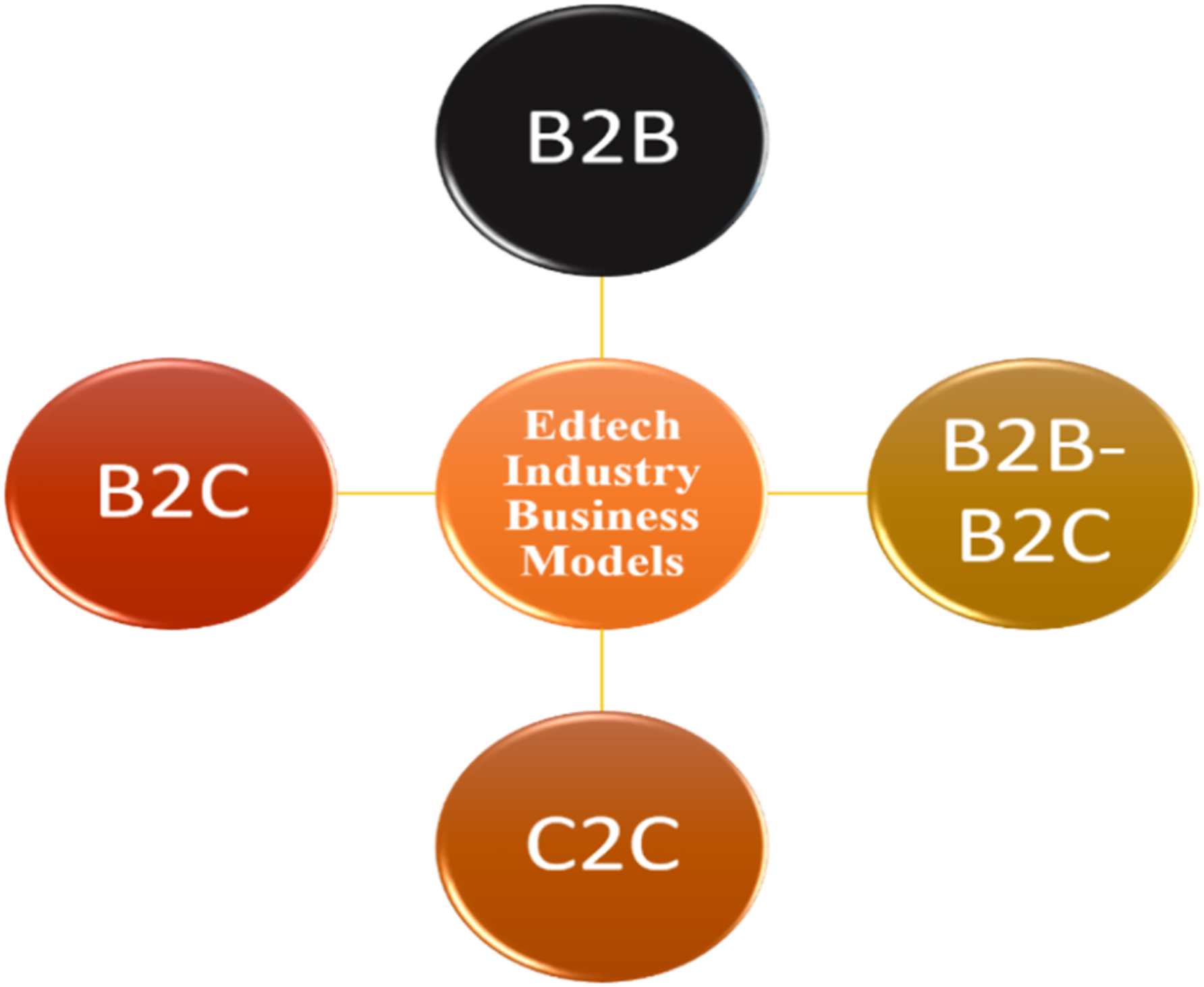

EdTech Industry Business Models

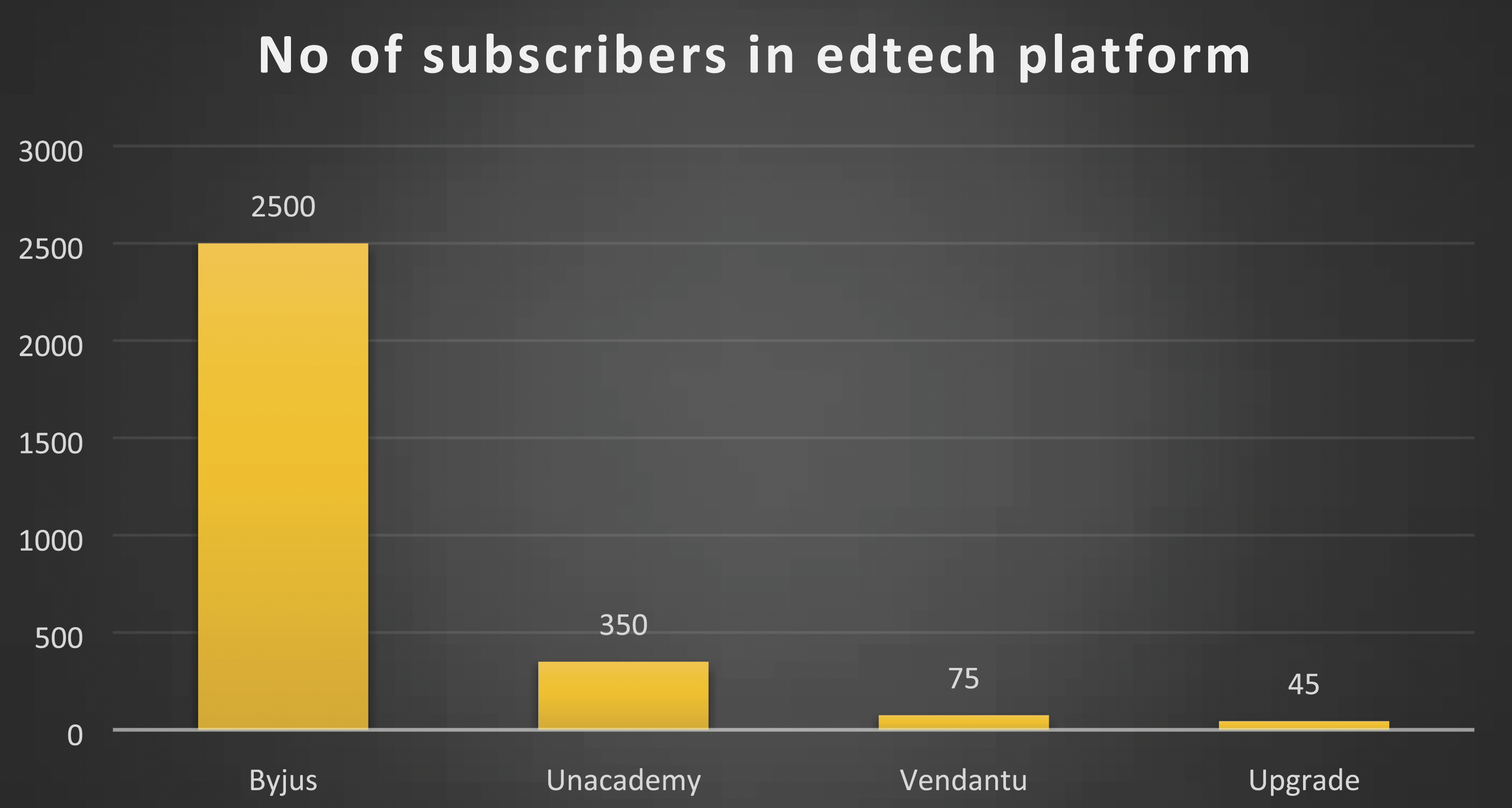

Top EdTech Platforms in India

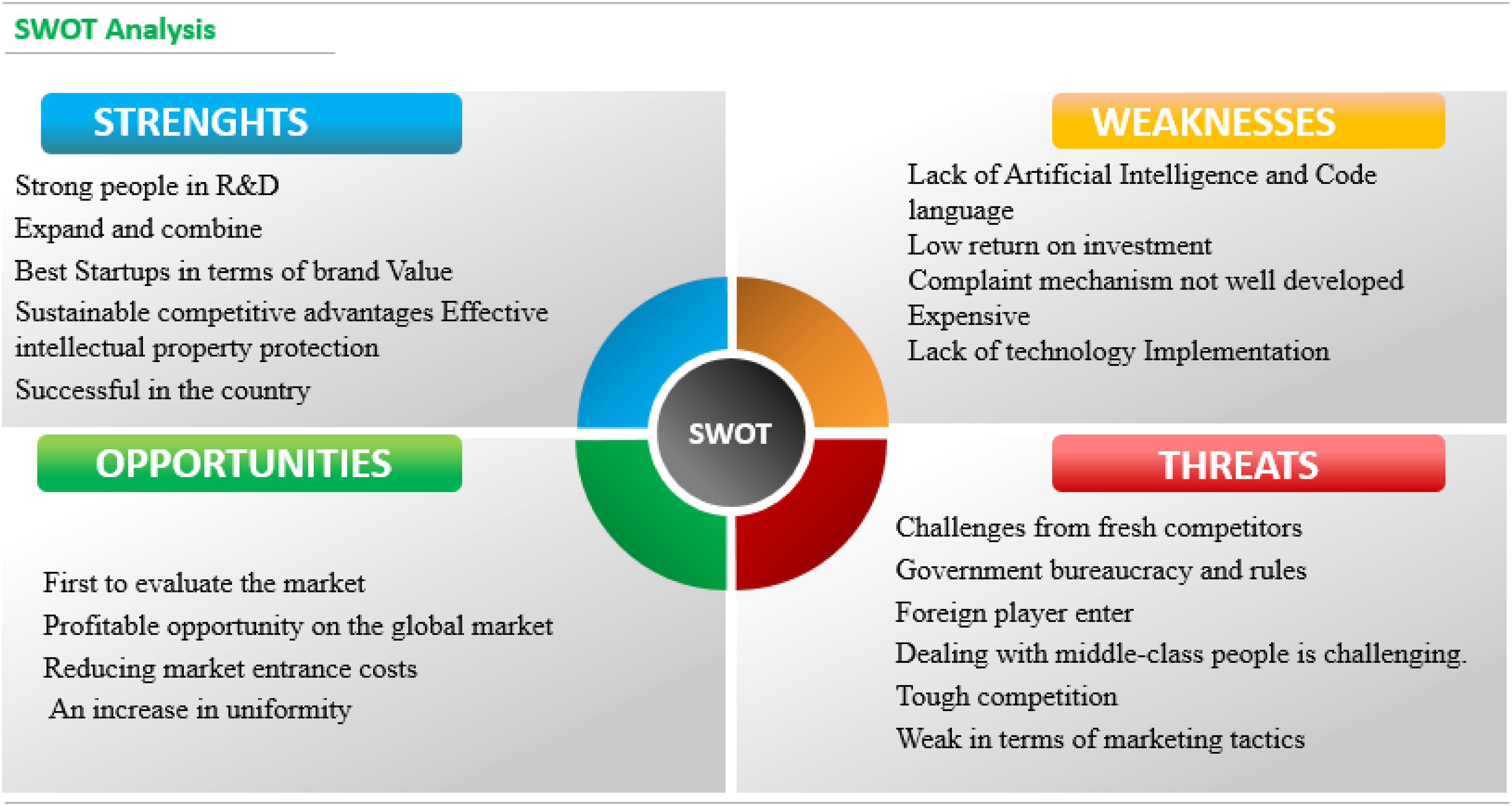

SWOT Analysis of EdTech Industry in India

After identifying the weaknesses of the company, finding solutions to overcome these weaknesses with better plans to compete with the competitors in the market, then identifying and exploiting market opportunities and reaching the first position in exploiting opportunities, finally knowing the threats to the company in the market to reduce future losses in the business and developing strategies to beat the competitors in the market, Byju's App adopts and implements the SWOT analysis.

EdTech provides a way to efficiently deliver education, and as a result, it can lead to increased labor productivity, technological innovation, and implementation of newer technology. This is why countries with EdTech implementations see a social and economic interest in implementing it. EdTech platforms offer numerous benefits to the learners’ community. Especially during the COVID-19 pandemic, the industry supported the teaching-learning process without interruption. • Brings the classroom to the learners’ home virtually which helped them to continue learning without the need for a physical location. When it comes to skill-based learning, more work is needed, and it is possible to use simulations and software to clarify the concepts. • Encourage peer connection among students by holding breakout sessions. The learning experience is validated by features such as doubt clearing with a user-friendly interface and easy support from teachers. Online pedagogies such as termbase learning, discussion forums, and open education resources are available. • Gamification makes the learning app more interactive, helps users be more proactive, and makes it more fun. Online learning is not as engaging for kids in particular; hence, gamification needs to be added. • Making use of collaborative tools like Google Docs, Google Drive, Google Hangouts, MS Teams, SlideShare, Minecraft, Kahoot, Mural, Voice Thread, Edmodo, and others to enable learners to discuss, listen to others, reflect, and evaluate peers and colleagues will help create structured evaluations and create an immersive learning environment. • Conducting a poll or feedback survey after each live session helps to troubleshoot any issues that may have arisen. In case of connectivity problems, record all live sessions so students can view them.

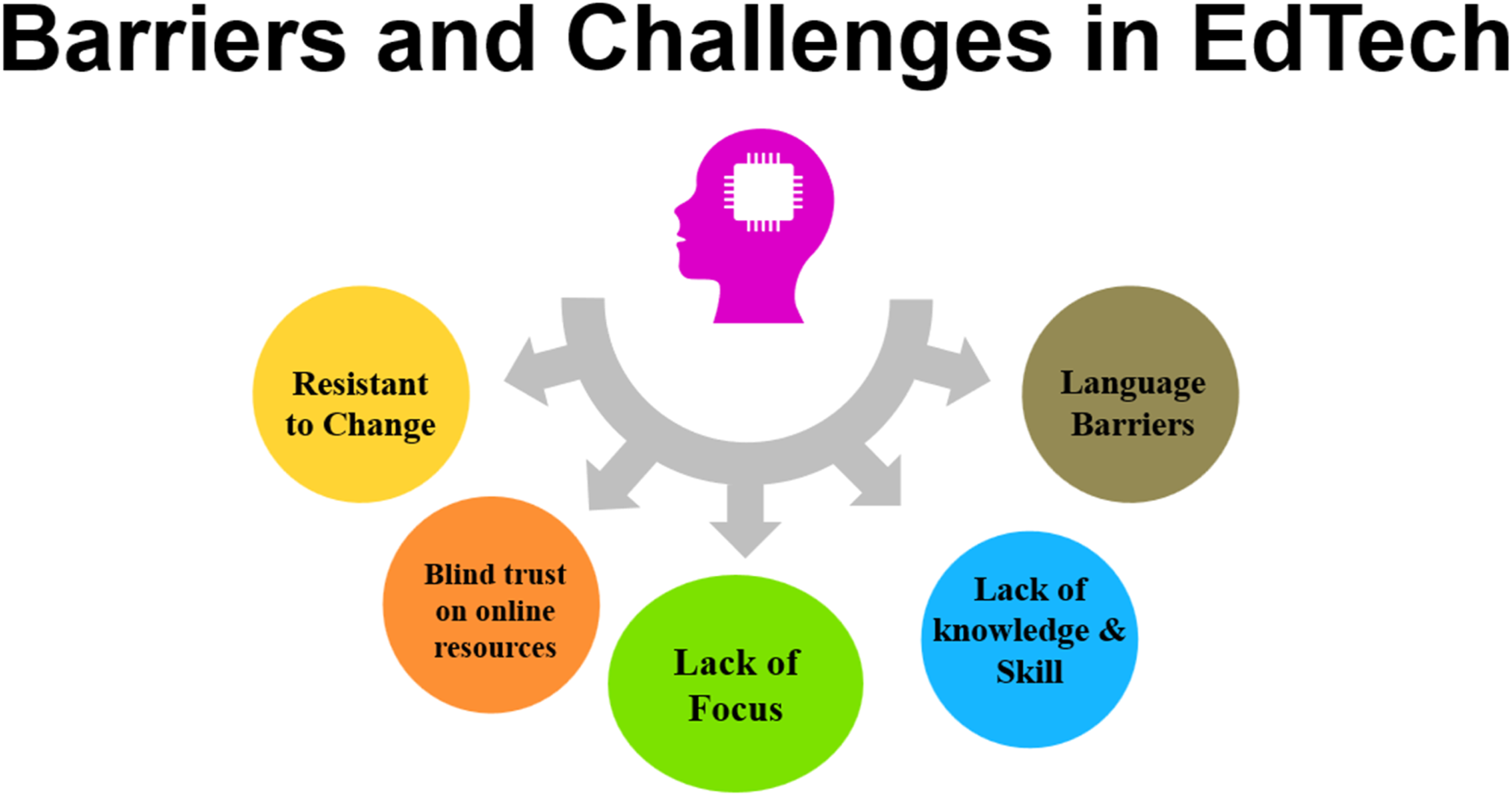

Barriers and Challenges in EdTech

Figure 8 shows the barriers and challenges in EdTech. Barriers and Challenges in EdTech

The EdTech industry has also faced several challenges, including low digital literacy levels, inadequate infrastructure, and the need for regulatory clarity. Additionally, the COVID-19 pandemic has highlighted the digital divide in Indian education, with millions of students lacking access to online learning platforms.

Conclusion

The EdTech industry in India has witnessed significant growth in recent years, driven by factors such as increasing internet penetration, rising smartphone usage, and a growing middle-class population. The industry has also received significant investment, with over $2 billion invested in Indian EdTech startups between 2014 and 2020. In the Indian industry, a number of EdTech businesses have become market leaders, providing a variety of services like online learning platforms, test preparation, language learning, and upskilling programmes. To meet the varying demands of Indian students, these businesses have used a variety of business models, including subscription-based, freemium, and premium courses.

The EdTech industry in India has the potential to transform the country's education landscape, providing students with access to quality education and personalized learning experiences. However, the industry must overcome several challenges, including low digital literacy levels, inadequate infrastructure, and regulatory uncertainty. The government, educators, and EdTech companies must work together to address these challenges and ensure that all students have access to quality education. Learning spaces will become less physical and more digital in the future. By improving the institutions' offerings, EdTech will help meet the needs of young learners who are hungry for education.

Discussion Questions of teaching cases in classroom

1. What are some of the major challenges facing the EdTech industry in India and how can they be addressed? 2. What initiatives has the Indian government taken to promote the use of educational technology (EdTech) in schools and universities across the country? 3. Will this use of technology align with government priorities and lead to the strengthening of national education systems? 4. Describe the EdTech platform in India. 5. Discuss the role of education technology development of India. 6. If you had to predict how the EdTech sector would change in the next 5 years, what do you think would happen? 7. What are the future prospects of the EdTech industry in India? 8. What decision would you make with regard to improvements and awareness of EdTech Platforms?

Footnotes

Acknowledgments

The authors would like to thank SRM Institute of Science and Technology, Kattankulathur Campus, for supplying the required research infrastructure.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

All data were used in the article.