Abstract

Financial innovations are bringing about significant changes in the design and delivery of banking services in both developed and developing countries. Despite the fact that studies have looked at the connection between innovation and bank performance, no known empirical study has attempted to investigate this relationship using micro-level data in Ghana. Using dataset obtained from 31 banks from 2011 to 2017 and the generalized method of moments regression technique, we find that: first, banking innovations positively impact their profit levels. Second, the effect of innovation is consistent in the long run but much larger than in the short run. Third, being innovative improves firm profits just as improvements in profitability enhance banks’ innovativeness, albeit this conclusion may vary depending on the measure of innovation used. We recommend that banks in the country deploy sufficient resources to develop innovative products that will make banking more affordable and convenient, in that the profit benefits will be enjoyed in the short to the long run. We further suggest that policies should speed up digitization efforts and lay the appropriate information technology infrastructure base required by the banks to develop various innovations that will spur the country’s financial inclusion agenda.

Introduction

Innovations in finance are fast changing the range of banking products available and their delivery globally (Frame & White, 2004; Jahangir & Parvez, 2012; Tufano, 2003). Indeed, financial innovations have and continue to alter the structure and competitiveness of the global banking industry (Cruz-García et al., 2021; Hasan et al., 2020; Lee et al., 2021). According to Yusheng and Ibrahim (2019), banks are adopting innovations for two key reasons namely: first, to deal with competition, and second, to enhance service delivery. The consequence of competition has been rising customer acquisition costs, increasing customer expectations, as well as a high rate of customer defection (Yusheng & Ibrahim, 2019). To reduce operational costs, build stronger bank–customer relationships, and promote customer loyalty, it becomes necessary for banks to innovate (Yusheng & Ibrahim, 2019). As aptly observed by Chipeta and Muthinja (2018), innovation is one of the surest means to achieving enhanced financial performance; hence, the importance of innovations cannot be overlooked.

Firms seek to be unique in their product design and delivery via both product and process innovations. By becoming innovative and unique, firms are expected to gain a competitive advantage over their rivals. The competitive advantage enjoyed by innovative firms could create value for shareholders through enhanced performance. In line with this argument, Jahangir and Parvez (2012) observe that many banks are now relying on information technology (IT) to remain relevant and competitive. An efficient and profitable banking system is important in the promotion of economic prosperity via the financial intermediation function. The innovativeness of the entire financial sector is critical in promoting economic growth (Beck et al., 2015). Ledhem and Mekidiche (2020) thus argue that economic growth is influenced by banking sector performance because of its impact on investment and capital stock. Consequently, there have been several studies into the determinants of bank performance, especially in Africa (Addai et al., 2022; Isayas, 2022; Kyei et al., 2022; Yahaya et al., 2022). These studies have often focused on areas including corporate governance, bank risk, income diversification, micro- and macroeconomic factors, and how these factors affect the performance of banks. Financial innovation, an important driver of bank performance, appears to have been neglected in the discourse within the context of sub-Saharan Africa (SSA) and Ghana in particular.

Financial innovations-related studies are not entirely new in Africa. While some of these studies have focused on the innovation–performance nexus among small and medium-sized enterprises (SMEs) (Makanyeza & Dzvuke, 2015), others have investigated the determinants of bank innovativeness (Hussen & Çokgezen, 2020; Muthinja & Chipeta, 2018). In Ghana, there appear to be three categories of studies on this subject matter. First are studies that assess the effect of innovations on savings and economic growth (Ansong et al., 2011; Nsor-Ambala & Amewu, 2023); the second strand of studies examines the perception of banking clients, adoption behavior, and the level of satisfaction with financial innovations (Domeher et al., 2014; YuSheng & Ibrahim, 2019). Finally, Agyapong (2021) focused on the implications of digitization on the efficiency of financial markets. Unfortunately, however, studies focusing on financial innovations and how they impact bank financial performance in Ghana are quite rare.

The very few studies that have attempted to investigate this relationship (Baba, 2012; YuSheng & Ibrahim, 2020) appear quite problematic. For instance, Baba (2012) attempted to investigate the effect of innovation on market share. However, the work was purely a perception-based study, where the author focused on the perception of managers from only one of the several banks in Ghana. This, the author himself acknowledged, is a major weakness that makes generalization difficult and the findings very subjective. Furthermore, YuSheng and Ibrahim (2020) attempted an investigation of the innovation–bank performance relationship. Here too, the study was based on the perception of 100 employees of banks located in just one city (Kumasi) in Ghana. While these perception-based studies may have provided some baseline studies on the subject, it is important to note that perceptions could deviate significantly from reality and we may end up with policy recommendations that are unable to address the real issues in the banking industry. There is, therefore, the need for a study that will investigate the relationship based on real industry or firm-level data that goes beyond perceptions and broadens the scope beyond a study of individual banks in isolation. This will improve the validity and applicability of the findings and lead to more relevant policy solutions.

Furthermore, it is argued that some innovations (technological) are highly imitable. Therefore, even though they lead to enhanced efficiency and improved product quality, the profitability benefits for the firm may not last long (Scott et al., 2017). The opposing view to this is that, it takes a long time for firms to adopt innovations and completely incorporate them into a firm’s processes (Greve, 2009). This alternative view explains why the profit effect of innovation may persist in the long run. Thus, the innovation–performance nexus also needs to be empirically tested in the long run. Unfortunately, there is no known study in Ghana that has attempted to do this. In addition, even though the theoretical literature points to the possibility of reverse causality between innovation and performance, none of the existing studies have attempted to investigate the direction of causality between the two variables. Financial innovations do not come free but at a cost. It will take only financially resourceful banks to undertake innovative activities. From the resource-based view (RBV) theory, it can be deduced that banks with superior financial performance are more capable of paying for the initial cost of investment in innovative activities. Investigating the direction of causality would thus provide relevant policy implications for stakeholders.

The study aims to assess the innovation–performance nexus in the banking sector within the setting of a developing economy (Ghana). The country has seen large investments in technological innovations and has become the information and communications technology (ICT) destination in West Africa (International Telecommunication Union, 2018). Despite these developments, there are no known studies in Ghana that attempt to investigate the impact these investments are making, especially in the banking sector. This article thus seeks to contribute to the innovation-bank performance literature by being probably the first to provide evidence from the entire banking industry in Ghana based on real firm-level secondary data. This makes the results more generalizable in Ghana and provides more reliable policy implications, which could be insightful for the stakeholders in the sub-region of SSA. In addition, we contribute to theory by attempting to test the applicability of the RBV which argues that it is rather financial performance that leads to innovations by banks by testing for the direction of causality. We contribute further to the literature by testing for the long-run elasticity to determine whether the effects vary in the long run. The other sections of the study are structured as follows: the next section offers a thorough analysis of the pertinent literature related to the subject. The study’s methodology is described in the section after that. The findings are then presented and discussed in the subsequent section. The study is concluded in the last section, which presents policy suggestions based on the major results of the investigation.

Literature Review

Financial Innovation

Financial innovation is the term used to describe the creation of unique financial products and the processes that allow financial institutions to deliver better quality products at lower costs to meet the ever-changing needs of their clients. According to Tufano (2003), it involves a heavy reliance on technology and the development of new instruments within unique financial markets. Financial innovations can be classified into product innovations and process innovations. With the former, institutions seek to differentiate themselves from others in the industry by designing new products that meet peculiar needs that are not satisfied by existing products. The latter, however, is fueled by new technologies which permit the banks to deliver their services more efficiently and conveniently. Lerner and Tufano (2011) aptly define them as follows: Product innovation comes with the creation of new products, while the development of new methods for distributing, transacting, or pricing financial products constitutes process innovation. Both product and process innovation work together to produce the optimal outcome of enhancing bank performance (Damanpour & Gopalakrishnan, 2001).

Transaction Cost Theory of Innovation

The theory that is probably most applicable in explaining the innovation–performance nexus is the transaction cost theory of innovation. According to Hicks and Niehans (1983), innovations via technological advancements are essential for lowering transaction costs for firms and boosting service delivery effectiveness. The theory holds that lowering transaction costs can help financial institutions achieve their primary goal of profit maximization. They also argue that when the relevant transaction cost is lower, firms tend to innovate more, leading to further enhancement in financial services. With innovations, organizations become more cost-effective and efficient (Hsieh et al., 2016). It can be deduced from this theory that financial innovation works toward reducing costs for both the banks on the one hand and the clients on the other. Innovations may influence bank performance in two main ways. First, through process innovations, banks can deliver their services more efficiently. A lot of waste is cut off with the help of technology, and this could reduce the cost to the bank in its service delivery activities. All things being equal, this could lead to an improvement in profits. The reduction in the banks’ cost of operation could also lead to a lower cost of services for clients. This, coupled with the convenience that comes with the innovation, is expected to give innovating banks some competitive advantage. This works to enhance client loyalty, retention, and bank performance. This study makes use of the aforementioned theory as a framework to explain how innovation affects bank performance.

RBV Theory

According to the RBV, possessing strategic resources, such as IT, can give an organization a competitive advantage over its rivals, resulting in higher profits (Shaw et al, 2013). To gain this advantage, firms must align their resources, knowledge, and skills with their core competencies. Core competencies refer to the operations that a company can perform better than its competitors (Hanson et al, 2016). The RBV contends that a company’s unique resources and capabilities (rather than the underlying structural characteristics of the industry it serves) have a greater impact on its long-term profitability. When a company has access to resources that are uncommon, difficult to duplicate, or incomparable, it can establish a competitive edge and generate superior profits. Therefore, by examining the key components of the RBV, it is possible to identify resources that can provide a company with a competitive advantage that can be sustained over time (Donnellan & Rutledge, 2019). In this study, the RBV theory helps us explain our expectation that reverse causality may exist in the innovation–performance relationship such that the effect may not be unidirectional flowing from innovation to performance but could also flow from performance to innovation. That is to say, the performance of banks is what rather determines their investment in financial innovation.

Empirical Literature: The Innovation and Bank Performance Relationship

Generally, the empirics support the theory. Studies conducted in different countries in Africa and elsewhere appear to mostly support a positive impact of innovations on performance. For instance, in Kenya, Sirengo (2022) investigated innovations in electronic funds transfer among other things, and established a positive impact on bank profits. Similar studies in Kenya that have also focused on e-banking and mobile banking (see Chipeta & Muthinja, 2018; Kithaka, 2014; Mabwai, 2016; Mutiso & Senelwa, 2017; Nduta & Wanjira, 2019; Odhiambo & Ngaba, 2019) have all concluded that these innovations were having a positive effect on profitability. Unlike the majority of the studies, Mugane (2015) discovered a negative effect of product innovations on Kenyan banks’ profits. In Nigeria, studies on digital innovations and mobile banking services established that they impact positively on bank profit levels (Arilesere et al., 2021; Bagudu et al., 2017). In Ghana, studies on this topic are also quite rare. One of the few studies in this area is the work by YuSheng and Ibrahim (2019) who attempted to assess the relationship between innovation adoption and bank performance. The study identified four dimensions of innovation, including organizational, product, process, and marketing innovations, and found a direct and favorable relationship.

In the Middle East, similar results have been reported. Several kinds of banking innovations have been studied, namely: internet banking, mobile banking, ATMs, computer software investments, debit and credit cards, point of sale terminals (PST), and electronic funds transfer, and have all been found to have a positive effect on the performance of Lebanese banks (El-Chaarani & El-Abiad, 2018; Sujud & Hashem, 2017). Chalabi (2020) investigated the effects of innovation on the performance of 17 Lebanese banks from 2009 to 2015 and found that investments in computer software have a significant positive impact on bank performance, while mobile banking was reported to have a negative impact. Additionally, a study on publicly listed banks in Amman established a direct link between ATM usage and online banking and bank profits (Hamdan et al., 2021). A few studies can also be found in Asia on the innovation bank performance relationship. For instance, in Indonesia, Khalifaturofi’ah (2023), using data from 2009 to 2018, found that the innovation–profitability relationship is positive. This is confirmed by Hu and Xie (2016) who used data from China and also discovered that financial innovations affect bank profitability positively.

In the Americas and Europe, the available studies on this subject appear to mainly confirm the findings reported in Africa, Asia, and the Middle East. Focusing on small banks in the USA, DeYoung et al. (2007) found that a considerable increase in bank profitability was related to the use of online banking. They conclude that “on average, click-and-mortar banks became more profitable relative to their brick-and-mortar rivals between 1999 and 2001.” In the Single Euro Payments Area (SEPA), Hasan et al. (2012) provide strong proof that innovative retail payment systems significantly increase both interest and non-interest income. The study comes to the conclusion that innovative retail payment services are essential in helping banks generate predictable revenue while also lowering their risk. Gündoğdu and Taskin (2017) also found that credit card usage increased profitability for banks in Turkey. Akhisar et al. (2015), in a study involving 23 developed and developing countries, noted that some innovations (card and ATM usage) positively affect performance while the impact of others (PST and internet banking) on performance was reported to be negative. Beccalli (2007) studied 737 European banks and found innovations as measured by the acquisition of computer hardware and software negatively impacted bank performance. This negative relationship is possible, where the investment in IT and other innovations fail to yield proportionate benefits. In that case, the expected positive effects of innovation may be missed. This is what is referred to as the IT–profitability paradox. Scott et al. (2017) found a long-run effect of financial innovation for both smaller and large banks.

The empirical literature across the globe generally appears to converge on a direct effect of innovation on profits. This positive relation is generally explained with the help of the transaction cost theory discussed earlier. Innovations help improve the efficiency of banking operations and also reduce costs for both clients and banks alike. The improved efficiency gives the banks some competitive edge, which then translates into enhanced financial performance. There are, however, a few studies that established that innovation impacts negatively on bank performance (see empirical review above). This negative relationship may also be explained by the fact that the cost of investing in innovation-related activities could outweigh the benefits derived from the innovations developed. The literature thus points to some level of variations in the findings on the innovation–bank performance nexus albeit, these variations do not appear very widespread. These variations, where they exist, appear to be based on the type of innovation used and the approach adopted in the study. Based on the theoretical and empirical literature reviewed above, we hypothesize as follows:

H1: Financial innovations have a significantly positive impact on bank financial performance. H2: The innovation-bank performance effect is stable from the short to the long run. H3: There is a bidirectional causality in the innovation–performance nexus.

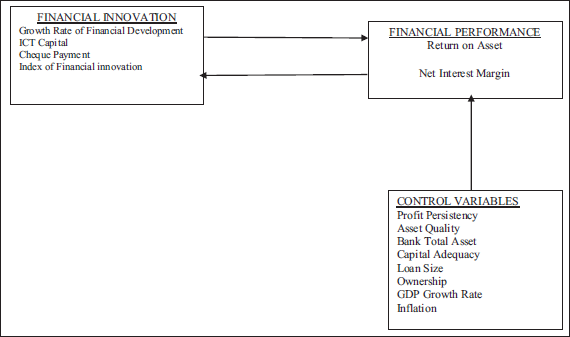

The conceptual model based on the literature reviewed is presented in Figure 1.

A Conceptual Framework of the Innovation–Financial Performance Nexus for Banks.

Methodology

Data and Data Sources

In this study, we use bank-level archival data from the Bank of Ghana and the World Development Indicators (WDI) databases. The data on our adopted measures of innovation were obtained via a request made to our contacts at the central bank because this information is not publicly available. The data on the country-specific controls were gathered from the WDI, while that on the bank-specific controls were obtained from the central bank’s website. Our data involved 31 banks with 193 bank-year observations. It was an unbalanced dataset spanning from 2011 to 2017.

Variable Definitions and Measures

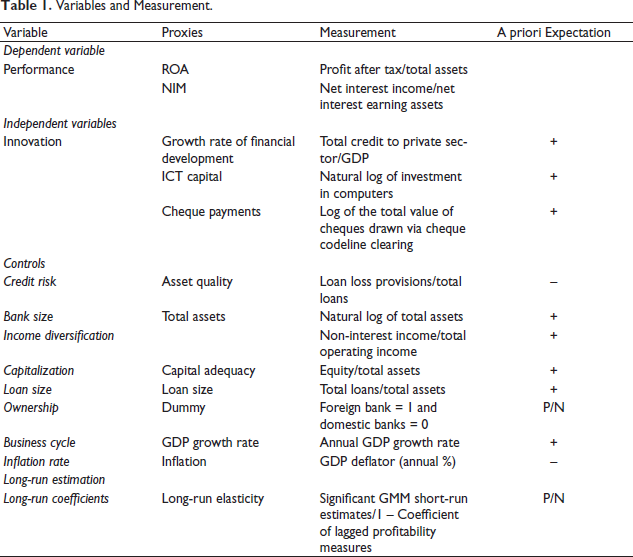

We outline in Table 1 the key variables used in the study. Financial performance is the dependent variable, while financial innovation is the independent variable. The research takes into account a variety of distinct bank-level features as well as macroeconomic variables that are known to affect banks’ performance. The variables and their measurements, as well as a priori expectations, are indicated in Table 1.

Variables and Measurement.

Estimation Techniques

A dynamic panel data estimation technique (specifically, the two-step system generalized method of moments (GMM)) is used in this study. Due to its ability to accurately capture the persistence of profits over time, this approach is frequently utilized when examining business performance. This estimation technique, according to Roodman (2009), is particularly appropriate when: the dependent variables are endogenous and their current values are impacted by their previous values; and the panel data consists of a relatively small T (time periods) and a larger N (number of entities or banks). This is consistent with the features of our dataset (T = 7 and N = 31). Three measures of financial innovation (cheque payment innovation, the growth rate of financial development (GRFD), and IT capital) are captured by our model in the initial analysis while controlling for some specific bank and macroeconomic determinants of profitability. Subsequently, we isolate only the significant variables to test for their long-run elasticities. The study uses the “pvargranger” command as recommended by Abrigo and Love (2016) to examine the probable direction of causation between financial innovations and financial performance. Several preliminary tests are carried out to assess the validity and reliability of the study before the Granger causality tests were performed. First, the Fisher unit root test (augmented Dickey–Fuller), which is deemed most appropriate for unbalanced panel datasets, is used to determine if the variables under examination are stationary. Furthermore, the tests for stability condition and appropriate lag selection are carried out. These tests ensure that the chosen model is stable and reliable while also assisting in determining the ideal lag time for the study.

Model Specification

In this section, we outline the generic and specific models used to investigate the link between financial innovation and the financial performance of banks. The generic model is shown below in Equation (1).

where:

Yit is bank i’s performance over time t;

Xit is bank i’s financial innovation indicators over time t;

Zit represents the set of control variables as detailed in Table 1;

c is a constant term;

εit is the disturbance term as defined in Equation (2) above;

νi is the unobserved bank-specific effect;

uit represents the idiosyncratic error;

α and β are the coefficients of the independent and control variables.

We adopt the strategy employed by Sarpong-Kumankoma et al. (2018) and incorporate a lag of the dependent variable among the independent variables to account for the impact of previous earnings on current profits as reflected by Equation (3) below. Equation (3) is generated by transforming Equation (1) as shown below:

where

where,

ROA = Return on asset;

NIM = Net interest margin;

GRFD = Growth rate of financial development;

ICTCPT = capital;

CPMT = Cheque codeline clearing system;

IDIV = Income diversification;

AQ = Asset quality;

TA = Bank total asset;

CA = Capital adequacy;

LSZ = Loan size;

OWN = Ownership;

GDP = Gross domestic product growth rate;

INF = Inflation.

To test for the direction of causality, we use the Granger causality Wald test based on the pvargranger command in Stata. This is done just after the panel vector autoregressive regression (PVAR) model is estimated. The command in Stata allows for the estimation of PVAR and accounts for individual bank heterogeneity within the stated dynamic model, which is represented by Equations (6) and (7) below. In the Granger causality test, we used three measures of innovation namely: FINDEX, CPMT, and GRFD against the two measures of financial performance namely: ROA and NIM.

where,

Xit represents financial innovation;

Yit represents financial performance.

Supplementary Analysis

The main results in this article were based on a balanced panel dataset spanning from 2011 to 2017. The unavailability of current data, especially on our innovation measures, did not permit us to update this. To overcome this weakness, we use an unbalanced panel dataset from 2011 to 2022. The pooled ordinary least squares (OLS) and random effect model estimation techniques were applied to the data. Since the result reported inTable 7 was generated from an unbalanced panel, it is not our preferred output. Our preferred results are the outputs from the balanced panel reported in Tables 4, 5, and 6. However, the results of the unbalanced panel have been reported (see Appendix Table 7) to provide readers with supplementary information.

Results and Discussions

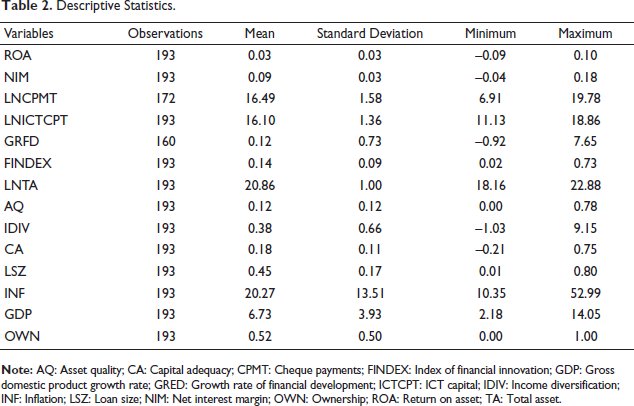

Descriptive Statistics

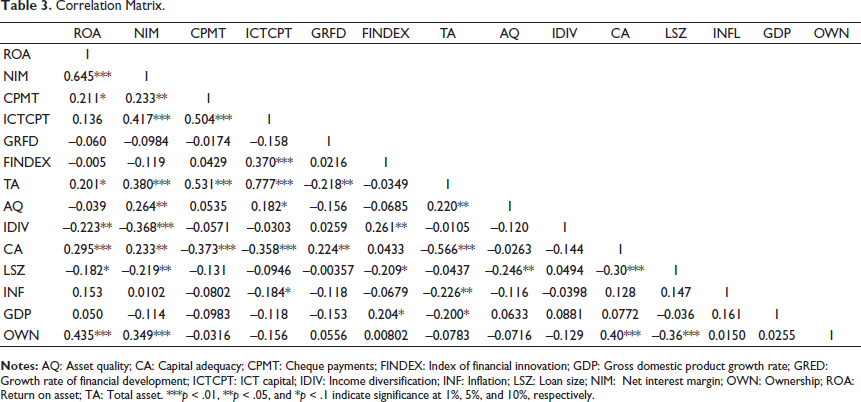

The descriptive statistics for the study variables are presented in Table 2. The results show that return on assets (ROA), a key indicator of financial success, has an average value of 3% and a maximum value of 10% in the dataset. The average net interest margin, which measures the profitability of assets that pay interest, is 9%, with a highest value of 18% recorded during the research period. In Ghana, non-interest income accounts for 38% of the total revenue earned by universal banks. Additionally, loan portfolios account for about 45% of bank’s total assets, with some institutions holding as much as 80% of their total assets in loans. A correlation matrix showing the connections between the study’s variables is shown in Table 3. Since all reported correlation coefficients are below 0.8, there is no convincing evidence of multicollinearity problems.

Descriptive Statistics.

Correlation Matrix.

Estimation Results: Financial Innovation and Bank Performance

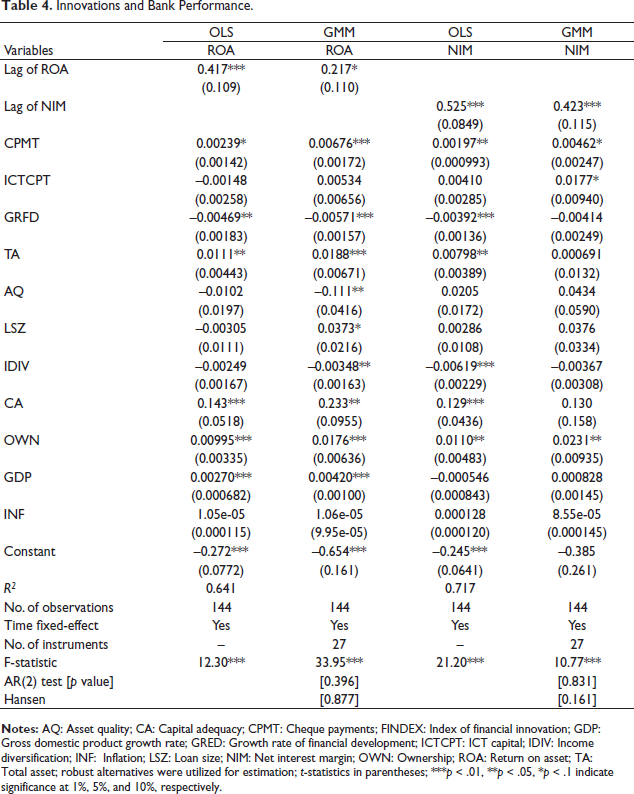

In Table 4, we present model estimations of the effects of financial innovations on the financial performance of banks. Regardless of the performance indicator used, the results show that Ghanaian banks exhibit profit persistence. The lags of ROA and NIM revealed positive and significant coefficients in both the OLS and GMM models (for instance, in the GMM model, the current values of NIM and ROA are positively related to their previous year’s values (0.423; p < .01 and 0.217; p < .1, respectively)). This is also true in the OLS models. The results show the coefficients of the second lag of the performance variables are insignificant. This suggests that the competitiveness among banks causes short-term profit to rapidly erode. The profit persistence thus does not go beyond the first lag. Though profit persistence has been observed, it is short-lived and on average is limited to just 1 year. In order to maintain their profit levels beyond the first lag, we argue that Ghanaian banks must remain innovative to stay one step ahead of their rivals. The reliability of the models is demonstrated by the diagnostic tests performed, which are all within acceptable limits. The results of these tests, which include the F-test to determine the overall goodness of fit, the AR(2) test to determine whether serial autocorrelation of the second order exists, and the Hansen J statistic to validate the applicability of the overriding limitations, are presented in Table 4. The robustness of the models utilized in the study is enhanced by these tests.

Innovations and Bank Performance.

Generally, our results from Table 4 also show that innovation enhances banks’ profitability levels irrespective of the measure of profitability (ROA and NIM) used. At a 99% confidence level, the results reveal that cheque payment innovation enhances bank profit levels. A unit increase in the cheque payment-related innovation enhances bank performance by 0.00676 (p < .01) in the ROA-GMM model and 0.00239 (p < .1) in the ROA-OLS model. A similar trend is also reflected by the NIM models. This positive effect is corroborated by Sirengo and Muturi (2022) that innovations in non-cash payments have a significant positive effect on commercial bank performance in Kenya. We explain this by the fact that the adoption of cheques and other non-cash payment innovations in general have the potential to increase fee income derived by banks, and this could spur growth in profits.

According to Hasan et al. (2012), by offering convenient payment options, default risk is reduced as borrowers tend to look for stress-free payment channels for meeting their repayment commitments. This, we argue is partly the reason why cheque payment innovation is enhancing the two indicators of performance used in this study. However, Mugane (2015) discovered contrary to our findings that product innovation affects profits negatively.

The findings in Table 4 also generally endorse a positive effect of innovation (measured by ICT capital) on bank profits. The observed effect though significant is quite marginal in the NIM-GMM model (0.0177; p < .1). A dollar increase in banks’ investment in ICT enhances their performance by 0.0177. This positive relationship established here is in tandem with the findings of Hamdan et al. (2021) and Chalabi (2020) who explored the impact of investment in IT and computer software on the profitability of banks. The relationship is, however, negative but insignificant (–0.0148) in the ROA-OLS model. The results here, however, generally depart from the literature on the existence of an “IT - Profitability paradox,” which according to Beccalli (2007) explains the situation where more investments in IT do not lead to a significant improvement in bank profit levels. Our finding is, however, justified in that, in an environment where ICT adoption is not very advanced, banks that are first to adopt can gain a competitive advantage and enjoy enhanced performance as a result. Furthermore, this could also be an indication that the cost reduction benefits that banks enjoy far outweigh their initial investment in ICT. Ghana’s banking industry is still in the early stages of automation, and customers commonly complain about long waiting times to access their money due to network issues or manual processes carried out by bank employees. In order to improve client experiences both inside and outside of banking halls, more investments in IT that can eliminate these impediments and boost the efficiency of banking services are required. According to YuSheng and Ibrahim (2019), this would thereafter be expected to increase customer loyalty, strengthen bank brand awareness, and eventually lead to enhanced financial performance.

We also found that our third measure of financial innovation, the GRFD, has a negative influence on performance in all the models with the exception of the NIM-GMM model. Specifically, the results show that a 1% increase in the GRFD dampens bank performance by –0.00469 (p < .05), –0.00571 (p < .01), or –0.00392 (p < .01), respectively, for the ROA-OLS, ROA-GMM, and NIM-OLS models. The negative relation observed here possibly points to the ineffectiveness of the innovations used in the loan approval process; if these innovations fail to help in discriminating bad borrowers from good borrowers then we may observe a rise in bad loans across the banking industry in Ghana (PWC, 2017). We explain our results here by the argument that without the appropriate innovations to facilitate the screening of borrowers, a rise in credit advances could dampen bank profits (Sarpong-Kumankoma et al., 2018) through rising non-performing loans.

For the control variables, we found that bank size positively affects financial performance in all the models. For instance, in the GMM model, a 1% increase or decrease in bank size leads to a 0.0188 (p < .01) decrease or increase in bank’s ROA. This is in tandem with the work of Anggari and Dana (2020) who also found a positive association between size and bank performance in Indonesia. All the models in our study show a significant relationship except the NIM-GMM model, which is positive but insignificant. The results thus largely support the RBV theory, which generally posits that firms with a large asset base are more likely to record higher profitability. The availability of resources to firms with large asset bases makes them more capable of investing in innovations that can stimulate profitability.

Credit risk was also found to have a negative and statistically significant influence on financial performance in the ROA-GMM model (–0.111; p < .05), which is consistent with the existing theory. Higher risks potentially lead to higher defaults in the bank’s loan portfolios, which in turn will dampen profit levels significantly. The NIM model, on the other hand, predicts a positive albeit insignificant impact on bank financial performance. Our finding here contradicts that of Dao and Nguyen (2020) who established that in Vietnam, a positive and significant relationship exists between credit risk and bank performance. In almost all our models, bank capitalization and performance are positively related (0.143, p < .01; 0.233, p < .05; 0.129, p < .01). This is in line with Sarpong-Kumankoma et al. (2018) and Ikpesu and Oke (2022) for Ghana and Nigeria, respectively. Well-capitalized banks have the ability to increase profit by making use of their access to a greater pool of capital. Instead of significantly depending on debt, these banks may rely on their own capital, which lowers the cost of funding their financial intermediation operations and ultimately boosts profitability.

Evidence from three of our models in Table 4 shows that the profitability of banks is positively affected by bank loan size albeit the effect is statistically significant only in one model, the ROA-GMM model (0.0373, p < .1). This implies that when banks allocate more of their assets to loans, the possible rise in interest income can enhance their financial performance. Alternatively, we argue that the high loan premiums charged by banks in Ghana enhance their profit positions even in the midst of significant loan loss provisioning when a very large proportion of their assets is made up of loans. The results on loan size and profitability are generally consistent with the studies of Ghosh (2016) and Yildirim (2022).

On bank ownership structure and performance, we found a positive relationship (see Table 4). This is in line with Ghosh (2016) who also observed that in countries where more than 50% of the banks are foreign-owned, ownership structure exerts a positive effect on performance. A similar study in Tunisia also concludes that the relationship between ownership structure and bank performance is positive (Daadaa, 2021). We thus conclude from our results that banks with foreign ownership are generally more profitable than those locally owned.

In Table 4, we observe a negative effect of diversification on performance from both the ROA-GMM model and the NIM-OLS models (0.00348, p < .05 and –0.00619, p < .01, respectively). The link is still negative in the other models though statistically insignificant. This negative relationship is confirmed by prior studies, including Calmès and Théoret (2010) and Githaiga (2021). Calmès and Théoret (2010) argue that though the margin on non-interest income may be high, income diversification could still lead to a negative impact on profitability due to the high volatility often associated with non-interest income. Our results here, however, differ from that of Luu et al. (2020) who found a positive effect in Vietnam. Our finding thus points to a diversification discount for Ghanaian banks possibly also because the cost of diversification outweighs the benefits. The business cycle also showed a positive and significant effect on bank performance as shown in the ROA models (0.00270, p < .01; and 0.00420, p < .01), and this confirms the study by Dao and Nguyen (2020).

We explain this by arguing that during periods of strong economic growth, corporate demand for loans rises and debtors’ capacity to repay loans grows, which could ultimately result in higher profitability.

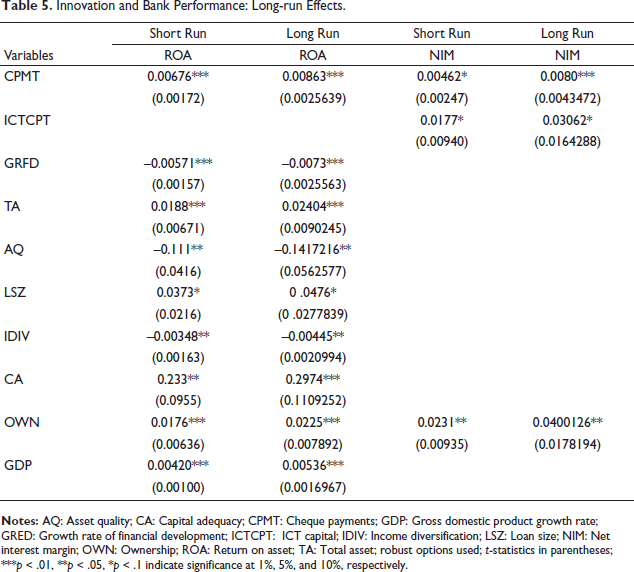

Innovation and Performance: Long-run Elasticity

In this study, we further sought to estimate the long-run effects of innovation on performance. The GMM approach estimates short-run coefficients from which long-run coefficients are estimated using only those variables that were significant in the short-run system GMM estimates. The findings shown in Table 5 reveal an inelastic long-term association between innovations and bank performance. This is true with all our measures of innovation except one (GRFD), which has an elastic long-run effect.

Innovation and Bank Performance: Long-run Effects.

Table 5 reports the short- and long-run relationships based on the GMM estimation technique. We observe that in the ROA model, the short- and long-run relationships between innovation (measured by cheque payment) and performance are positive and significant (0.00676, p < .01; 0.00863, p < .01, respectively). This is confirmed by the NIM model, which further enforced the positive and significant relation in both the short and long run (0.00462, p < .1; 0.0080, p < .01, respectively). The results also show higher coefficients in the long run, an indication that the positive impact of this kind of innovation (cheque payment innovation) is bigger in the long run. The relationship established here is also confirmed when the second measure of innovation (ICT capital) is used. We observe a stable positive and significant relationship from the short to the long run. Furthermore, the impact is bigger in the long run (0.03062, p < .1) than in the short run (0.0177, p < .1). This confirms the observation by Greve (2009) that the economic rents from innovation adoption persist since it takes a long time before other firms can imitate it. The only deviation in the above results is observed with our third measure of innovation (GRFD) where the effect on performance is negative and significant in both the short run (–0.00571, p < .01) and long run (0.0073, p < .01).

We further observe that irrespective of the nature of the innovation–performance relationship, the impact tends to be bigger in the long run. We observe this consistency also with our control variables. Hence, all positively and negatively significant relationships reported in the short run remain the same in the long run with only variations in the size of the coefficients and significance level. This reflects the robustness of our findings. The implication is that bank managers can effectively forecast the profitability rewards of their financial innovation strategies. Any investments in innovation will generate profit benefits from the short to the long run. Our results here largely confirm that of Scott et al. (2017) who also established that digital innovations have a large and significantly positive long-term effect on bank performance in Europe and the Americas. It further confirms the observation by Ngugi and Karina (2013) that innovations that radically change a firm’s products are required for its long-term performance in terms of growth.

Direction of Causality: Panel Granger Causality Tests

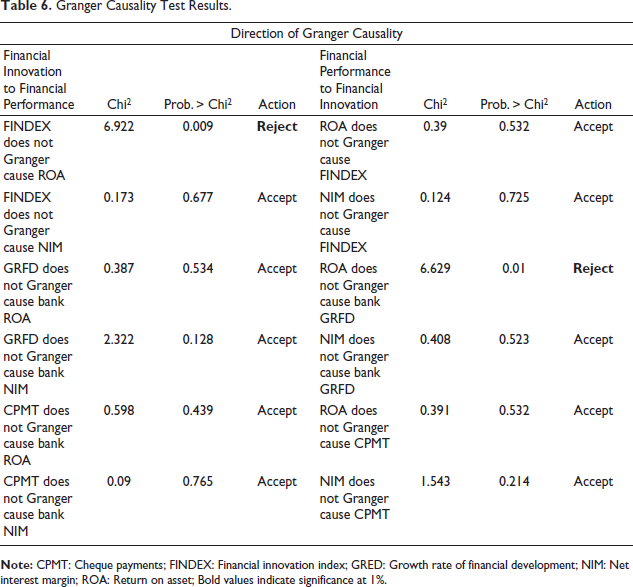

In this section, we used the Abrigo and Love (2016) causality analysis method to investigate the relationship between bank financial performance and innovations. We first ran the augmented Dickey–Fuller unit root tests. The finding of which led us to reject the null hypothesis that “all panels contain unit roots” in favor of the alternative hypothesis that “at least one panel is stationary.” We then proceeded to perform the Granger causality test. The first lag was consistently preferred by the MBIC, MAIC, and MQIC criteria as the optimal lag length for the panel VAR model across all variable pairs.

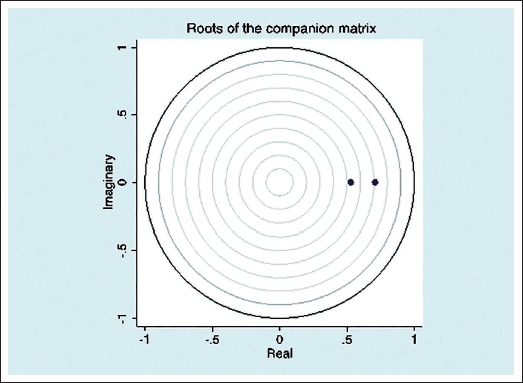

From Table 6, we observe that between innovation (the composite measure) and performance (ROA), there is a significant unidirectional causal relationship. This means that banks looking to increase their profitability could focus on enhancing the individual components of the composite innovation measure. A unidirectional causal association was also observed from bank ROA to financial innovation (as assessed by the GRFD). This conclusion is consistent with the RBV theory, since successful banks with large capital base and other resources are better equipped to steadily increase the amount of credit they extend to domestic companies. Based on this, we generally conclude that a two-way causal relationship exists between innovation and profitability of banks in Ghana. One should, however, be cautious with this generalization taking into consideration the measures of innovation involved. We test for the stability of the Granger causality model based on the recommendation by Girma (2017). This test guarantees the stability and accuracy of the PVAR models used for causality analysis. All eigenvalues must be contained inside the unit circle in order for the stability criteria to be satisfied (Girma, 2017) as can be visualized from Figures 2 to 4.

Granger Causality Test Results.

Stability Condition Cheques.

Stability Condition Growth Rate of Financial Development (GRFD).

Stability Condition Financial Innovation (FI) Index.

Conclusions and Policy Implications

Despite the seemingly growing interest in technology and other relevant innovations by banks, there is no publicly available study that investigates the relationship between innovations and performance in Ghana using firm-level secondary data. This article thus aims to fill in this gap using secondary data from the banking sector in Ghana. We further sought to determine if the effects observed remain stable in the long run. Finally, we examined the causality in the innovation–performance relationship based on the theoretical literature, which gives the impression that a two-way causal effect could exist between innovation and performance.

Our findings reported above give a clear indication of profit persistence in the Ghanaian banking sector even though it is usually short-lived, not extending beyond the first lag. We also observe that the innovation–performance relationship is positive. With the exception of only one of the measures of innovation (growth rate of financial development), the other indicators (ICT capital, cheque payments) exhibited a positive effect at least on either ROA or NIM. As a result, banks that proactively invest in ICT and non-cash payment mechanisms can expect enhanced financial performance (Sirengo, 2022). Bank efficiency improves significantly with investment in ICT. According to YuSheng and Ibrahim (2019), this has the potential to promote customer loyalty, bank brand recognition, and ultimately high performance. We observe that the innovation–performance nexus of Ghanaian banks is generally positive in the short run and remains stable in the long run where the impact tends to be bigger. Banks thus stand to gain bigger performance-enhancing benefits from their investments in relevant innovations in the long run. Given this, bank owners and management should take advantage of the technological revolution to develop and integrate ICT and non-cash payment innovations as part of their product/service portfolios. Even though resources may be scarce, such a move will likely ensure sustainability in profit creation in the long run (Yusheng & Ibrahim, 2019). Furthermore, while financial innovations affect bank performance, we found that the performance of banks also affects their innovativeness. The relationship is thus generally bidirectional. This is, however, only true for certain indicators of innovation and performance. We thus have some evidence that generally supports a two-way effect between innovation and bank performance. This provides management with more evidence to justify investment decisions in relation to innovative activities knowing that such innovations could spur profits. The higher profit in turn spurs further investments in more innovations. This can go back and forth creating value for shareholders from the short to the long run.

We make significant contributions to the innovation–performance literature within the Ghanaian banking industry in that no empirical research on this exists even though the adoption of innovations appears to be rising steadily over the past few years. First, our study has provided empirical evidence on this topic using real firm-level secondary data from the entire banking sector (probably the first study to do so in Ghana). We thus provide more robust and reliable findings, which build on the existing individual bank-level and perception-based studies. Second, we also contribute by providing useful evidence on not only the short-run but also the long-run dynamics in the innovation bank performance relationship. Third, we contribute to the literature by providing evidence to support a bidirectional relationship in the innovation-bank performance argument which though important for strategic decision-making, has previously been neglected in prior research. Fourth, our finding that financial performance drives innovation contributes to the theory as it also provides evidence in support of the RBV theory. Fifth, we make a practical contribution as our results may influence bank-level policy decisions on investment in various innovations. Bank managers in an environment of high resource limitations can justify their decisions to allocate scarce resources to various innovative activities based on our findings here. The outcomes also provide the government strong justification to speed up its digitization initiatives and build a solid ICT infrastructure that will facilitate cutting-edge banking services, resulting in greater financial inclusion and overall economic growth.

The main limitation of our study has to do with the limited availability of secondary data on the key financial innovation indicators. We use firm-level microdata that spans from 2011 to 2017 to estimate the innovation-bank performance nexus in Ghana. The data on the micro-level innovation variables are not publicly available. The only innovation data that is made publicly available by the regulator are aggregated and also span from 2015 to 2019. We have tried to go through the public sources hoping to get some data all to no avail. In a developing country like the one in our case, this is usually one of the challenges that researchers face. In the past, many researchers in Ghana have shied away from this kind of study because of this data limitation. This explains why the very few studies in existence have often focused on the use of surveys to study only individual banks based on managers’ perceptions. Even though our data may be a bit old, it nonetheless makes a very significant contribution by being one of the first to investigate the phenomenon using real secondary data. Our findings are relevant as they provide insights not previously known in the Ghanaian banking industry. As an additional precautionary measure, we attempt to extend the data period beyond 2017 up to the year 2022. This resulted in an unbalanced panel and the supplementary results reported do not deviate very significantly from our main findings.

Furthermore, our study provides a more objective, robust, and reliable set of findings on the subject with critical policy implications. This can serve as an important baseline study that will inform future research in this area as more data become publicly available. We recommend that future research should extend our study as more data become available to cover the period after 2017, and also focus on how the banking sector clean-up between 2017 and 2020 may have affected the innovation–performance relationship. Further studies can also directly test the transaction cost theory to determine the effect of innovation on bank efficiency and the drivers of innovation in the Ghanaian banking industry, which were not examined in our study.

Footnotes

Appendix

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.