Abstract

The front end of projects is strategically important; yet, how project concepts are identified, evaluated, and selected at the pre-project stage is poorly understood. This article reports on an inductive multiple-case study of how executives made such decisions in major upstream oil and gas projects. The findings show that in such a high-risk context, often an experienced executive makes these decisions alone and he creates value by facilitating growth. We identified three value-creating decision processes that varied by the executives’ risk approach and decision context. These processes depart from the formal project management prescriptions and the strategic decision-making literature.

Keywords

Introduction

The dominant focus of project management research has been the evaluation of potential projects and the management of the project portfolio (Williams et al., 2019). Such a focus is justified, as companies implement their strategies and create financial value through projects (Serra & Kunc, 2015). This research has yielded well-defined normative project management principles and best practices, recommended across different types of projects and contexts (Williams et al., 2019).

With the focus on formally evaluating and selecting projects and managing the existing portfolio, the literature has said little about how new project concepts (opportunities) are identified at the front end, before formal evaluation and selection. A common assumption is that staff scout for opportunities, screen them through formal project management processes, and present those selected to the executive decision makers, who typically are not involved in generating project ideas (Heising, 2012). The executives then choose projects for the company’s portfolio (Artto et al., 2011; Florén et al., 2018; Koen et al., 2014; Young et al., 2012). Besides being the final decision makers for the portfolio selection (Beringer et al., 2013), executives also make project termination decisions (Dilts & Pence, 2006; Lechler & Thomas, 2015) and provide functional expertise (such as finance or operations; Geng et al., 2018). Despite this literature, a knowledge gap remains about the executives’ role in the pre-project front end.

This assumption about new project selection processes may hold well in the context of the public sector and industries where outcomes are highly certain. However, recent literature reviews suggest that the assumption is not valid across all types of projects and contexts (Williams et al., 2019). For example, in contexts where exploration of the unknown and highly uncertain (March, 1991) is required to identify high-risk, high-reward project opportunities, the processes of opportunity identification and evaluation may look quite different from the normative project management guidelines. Research on managing risk in projects (to facilitate value creation and protect the value created) also agrees (Browning, 2019; Sanchez-Cazorla et al., 2016).

In high-risk, high-reward contexts, executive decision makers are not the project approvers at the end of the search process but play a central role as the opportunity identifiers and evaluators much earlier in the pre-project front end. Research on the role of executives at the front end is scant (Eling & Herstatt, 2017; Sergi, 2012; Takey & Carvalho, 2016; Williams et al., 2019); yet, their role at this stage is recognized as central because the project opportunities they identify and evaluate have such a significant value-creating impact (Morris, 2009; Samset & Volden, 2016).

To address these gaps in the project management literature—the lack of knowledge about decisions at projects’ front end and the lack of attention to different industry contexts—we formulated our research question: How do executives make front-end project selection decisions in the upstream oil and gas industry?

Our comparative case study of 16 decisions on major project opportunities at 14 companies in the high-risk, high-reward context of the upstream oil and gas industry sheds light on the front end of projects, addressing the research question. In contrast to the existing literature, our findings suggest a much more central role of executive decision makers at the front end of projects in a high-risk, high-reward context, before the application of formal project management processes.

We identify three decision processes by executives at this stage and show how the processes vary, depending on the type of project, differences in their context, and the risk approach of the decision makers. Our findings help explain how front-end decisions affect the projects’ value creation in a high-risk, high-reward context and what is required of the decision makers. Our findings also lead to questions about the universal applicability of formal project processes to all types of projects in different contexts, such as those provided by the Project Management Institute (Garel, 2013).

The remainder of this article is structured as follows. The theoretical background that guided us to study executive decision-making at the front end of projects is reviewed first. We discuss the research on strategic decision-making, front-end project activities, and executives’ roles in managing project risks and value creation. Research methods are described next, followed by the findings about three types of front-end decision processes. Finally, the study’s contributions to project management theory and practice and its limitations are discussed.

Theoretical Background

Strategic Decision-Making and Project Management

Companies’ strategies and projects are inextricably linked, as the former are implemented through the latter, such as product development, technology adoption, construction, and acquisition projects. Yet, the research on strategic management and project management remains mostly separate and discussed in different journals. This is notwithstanding a recent increase in research on projects’ impact on companies’ long-term financial performance (Artto et al., 2016; Patanakul & Shenhar, 2012), the primary dependent variable in strategic management research. Some project management studies report many projects failing to have a positive impact on company performance (Serra & Kunc, 2015). Others have attributed project failures to insufficient integration of project ideas with company strategy at the front end (Kock et al., 2016; Morris, 2009; Samset & Volden, 2016).

The strategic management literature, focused on strategic decision-making, points to the importance of understanding executives’ decision processes, which also include identifying, evaluating, and selecting project ideas. The project management literature calls this stage “the fuzzy front end,” as it is poorly understood (Takey & Carvalho, 2016). A comprehensive review of this stage (Williams et al., 2019) identified a theoretical gap of what the front end includes. Further, the authors of that review were unable to find research on evaluating different types of projects, such as new product development, construction, or software development.

Project management researchers have called for better understanding of the fuzzy front end: how firms and individuals search and select project concepts (Salter et al., 2015; Savino et al., 2017; van den Ende et al., 2015). Yet, the literature is clear that a project concept must include the technical solution, the business case, and the various intraorganizational and interorganizational relationships involved, before it is ready for selection (Williams et al., 2019). In other words, the “fuzziness” must be cleared before the project concept decision is made. Understanding what happens at the front end is crucial, since establishing concept feasibility early on can reduce costs and risks as the project progresses and ultimately creates objectively measurable financial value or value perceived by some key stakeholders (Thanasopon et al., 2016; Willumsen et al., 2019). The literature on these front-end processes is reviewed in its own section further below.

The strategic decision-making literature suggests the role of executives in project concept generation and selection is worth studying. For example, the “upper echelons perspective” (Hambrick & Mason, 1984) emphasizes the role of executives in shaping firms’ strategies and performance through their decisions. While Hambrick and Mason’s (1984) early work focused on the impact of demographic factors on executives’ decision-making, rather than their decision-making processes, much of the subsequent research on strategic decision-making has employed a cognitive or behavioral perspective (Schwenk, 1995). For example, the behavioral theory of strategy is based on the assumption that the strategic leaders’ superior ability to manage their mental processes (e.g., associative reasoning) contributes to their firms’ above-average profitability (Gavetti, 2012). Similarly, the microfoundations perspective on strategy explains companies’ superior financial performance through the cognitive processes of their executives (Felin et al., 2015; Helfat & Peteraf, 2015). Some research on managerial cognition also contributes to understanding strategic decision-making in that it focuses on the interaction of intuition and rational analysis in decision processes (Dane et al., 2012; Hodgkinson & Sadler-Smith, 2018; Woiceshyn, 2009).

In contrast, the project management literature has mainly focused on executives’ decision-making as prescribed by the formal project management processes (Eling & Herstatt, 2017; Sergi, 2012; Takey & Carvalho, 2016). These processes, described by project life cycle models, were developed to manage each project phase (Pinto & Prescott, 1988). The models vary slightly but they all depict a sequence where a project is formally evaluated after the idea has been conceived. If the evaluation is successful, the project proceeds to planning and execution (Munns & Bjeirmi, 1996; Pinto & Prescott, 1988). The most frequently cited formal decision-making and assessment models for post-project idea conception (Rodrigues Pereira et al., 2017) are Cooper’s Stage-Gate model (Cooper, 1993, 2008), the three-phase front-end model (Khurana & Rosenthal, 1998), and the new concept development model (Koen et al., 2002). The project portfolio model is the most common. Supported by research, this model prescribes well-developed processes to evaluate the feasibility of project concepts after they have been identified (DeFillippi & Sydow, 2016).

It should be noted that research on project decision-making from the behavioral perspective is increasing, although it has not focused on the executives’ role at the front end (Stingl & Geraldi, 2017). This suggests project management literature is starting to be informed by strategic decision-making concepts, which also inspired the focus of our study.

The Front-End Project Ideation Process

Where do project ideas come from? Specifically, what is their source in dynamic contexts where the outcome—a desired return on the investment—is highly uncertain, in other words, highly risky? Who conceives project ideas and how? A literature review of projects’ front end (Takey & Carvalho, 2016) found only two studies (out of 59) with the individual decision maker as the unit of analysis. The majority had a company (28) or a project/portfolio (25) as the unit of analysis. Some research suggests it is unclear who is best suited to conceive a project idea (Poskela & Martinsuo, 2009; Williams et al., 2019).

Heising (2012) found that senior leaders were not typically involved in project conception. The project management literature depicts the roles of senior leaders, post project conception, as broad and varied (Christiansen & Gasparin, 2016). For example, senior leaders have been shown to improve the overall quality of the project idea (Salter et al., 2015), to align projects with the organization’s strategy and goals (Florén et al., 2018; Williams & Samset, 2010), and to ensure more efficient use of a firm’s resources for revenue generation (Mannor et al., 2016).

Early on, strategic decision-making researchers (e.g., Mintzberg et al., 1976) modeled the executives’ decision process to include three phases: opportunity/problem identification, solution development, and selection. In the selection phase, the decision maker(s) evaluate the alternative solutions and choose one that provides the best fit with the company’s strategic goals (Schwenk, 1995). This model weighs the opportunity identification phase equally with the subsequent two phases, whereas the project management literature focuses on the latter phases. For example, Heising (2012) defines project ideation as a three-stage process: identifying and generating ideas; evaluating and selecting them; and condensing, clustering, and bundling the ideas into proposals for new projects or for changes in existing projects. The literature recognizes the importance of a continuous inflow of good project ideas so that they can be compared with others in the portfolio (van den Ende et al., 2015).

Because senior leaders have a “big-picture” vantage point across divisions and down the hierarchical levels of their organization, they have a more integrated perspective (than, e.g., middle managers) from which to evaluate project concepts and ensure strategic alignment (Poskela & Martinsuo, 2009; Salter et al., 2015). Project management research has recently started to focus on “exploratory” projects that require management tools and applications different from what traditional project management models offer (Lenfle, 2016).

Front-End Decision-Making for Managing Project Risk and Value Creation

All projects pose risks that threaten their potential value creation. It has been argued that uncertainty is greatest at the front end of projects and therefore the opportunity to mitigate risks at that stage is the most significant (Williams et al., 2019). Another reason to study the front end of projects, particularly in high-risk contexts, is to understand how risks can be reduced and value creation enhanced.

Assessing the value created by a project across industries has traditionally been based on the operational criteria of the “iron triangle:” time, budget, and quality (i.e., consistently meeting client expectations; Pollack et al., 2018). The value created is often considered a stakeholder’s social construct from perceived project deliverables (both immediate and later outcomes) and the client’s willingness to pay for them (Green & Sergeeva, 2019; Martinsuo et al., 2019) and not objectively defined (Willumsen et al., 2019). Research has not established a linear relationship between formalized project management processes and a project’s success, and key success factors at the front end remain ill-defined (Florén et al., 2018).

Research on projects’ contribution to companies’ long-term financial value creation is evolving, but few studies have examined how that value is created (Laursen & Svejvig, 2016; Willumsen et al., 2019). Yet some researchers note it should start early, at the front end (Artto et al., 2016).

Project management risk, including at the front end, has been well researched, but there is no consensus on how to best manage that risk (Sanchez-Cazorla et al., 2016; Williams et al., 2019). Project management entails risk management (Browning & Eppinger, 2002), and although an estimated 38 risk tools and processes are in use (Raz & Michael, 2001), they may still be inadequate to manage project concepts at the front end (Browning, 2019).

Different risk management tools are used in different project phases (e.g., design phase risks) and industries. However, only three of 85 studies have focused on the early concept stage, one of them in the oil and gas industry. Moreover, the impact of risk management decisions made in the early stages of megaprojects has not been studied in the later stages of these projects (Sanchez-Cazorla et al., 2016). Some have argued that lowering the expectations of a project’s goals can decrease project risk; however, this might also lower the overall commercial value of the project (Browning, 2019).

A study on complex projects found senior managers rated the impact of project risks 20% lower on average than the project managers assessing the same risks. The researchers suggested the reason might be that senior managers are further removed from those project issues (Williams, 2017). Also, experienced decision makers may consider projects less risky than those who don’t have the same level of experience (Slovic, 1987).

Research Methods

We studied front-end decisions in the high-risk, high-reward context of the upstream oil and gas industry. We chose this industry, first, because it is a prime example of a dynamic, high-risk context, where payback periods on project investments are long and the front-end activities are emphasized (Williams et al., 2019). Also, the upstream oil and gas industry is, and continues to be, the major source of the world’s energy (over 50% in 2015) that powers most other industries (Matsumura & Zakia, 2019). Finally, we had excellent access through personal networks to CEOs and other high-level executives who identify and evaluate major upstream oil and gas projects.

Our study examined how the executives identified, evaluated, and selected project ideas; what factors they considered; who they included in the decision; what they regarded as risky; as well as the specific contexts of their companies. To ensure qualitative rigor with an inductive research approach, we employed the “Gioia methodology” (Gioia et al., 2012), which entails developing a data structure from first-order concepts to second-order themes and to abstract (theoretical) dimensions in order to explain the phenomenon of interest. In mapping out executives’ decision-making processes for major capital projects retrospectively—to understand how they constructed meaning out of their “daily realities” and their interpretations of those realities—we also utilized Corbin and Strauss (1990) version of the grounded theory methodology (Suddaby, 2006).

While the literature guided us to pay attention to executives’ decision-making, we started the data analysis inductively, circling back to the literature to compare our findings to existing literature and see what we could add to previous research. We also used insights from strategic decision-making literature to analyze and interpret our study’s findings.

Data Collection and Analysis

The executives in our study made decisions about major project ideas, which were either acquisitions (of existing operating assets) or greenfield developments (e.g., buying undeveloped land). At a few companies, the executives considered both types of projects. Some of these projects were domestic, whereas others involved a large-scale global expansion.

We used specific criteria to choose the companies where the front-end project decisions were made. First, each company considered a strategically important major project that required senior level/CEO approval and significant capital investment relative to their firm’s size, which increased its financial risk (Eisenhardt, 1989). Second, these companies were publicly traded, with financial information and documentation available about the projects. The project costs ranged from CA$3 million (US$2.3 million) for a small exploration company to over CA$1 billion (US$750 million), with most projects costing between CA$200 and CA$500 million. Some were megaprojects, with significant interdependencies, interfaces, complexities, and risks and were managed at a level above the project team (Jergeas, 2008).

To prepare for the interviews and to confirm interview information, additional data about the projects of interest and the company context for the project decision were also collected. The data set were rich and provided a comprehensive contextual understanding of each project decision case (Yin, 2009). These data included company documents: internal analyses, press releases, several years of annual reports, quarterly reports and management circulars, investor presentations, information on the leadership team members and the board of directors, governance policies, specific project information, and company strategy and vision. Additional data were also collected from public sources, such as newspapers, market and investor information, and historical stock prices.

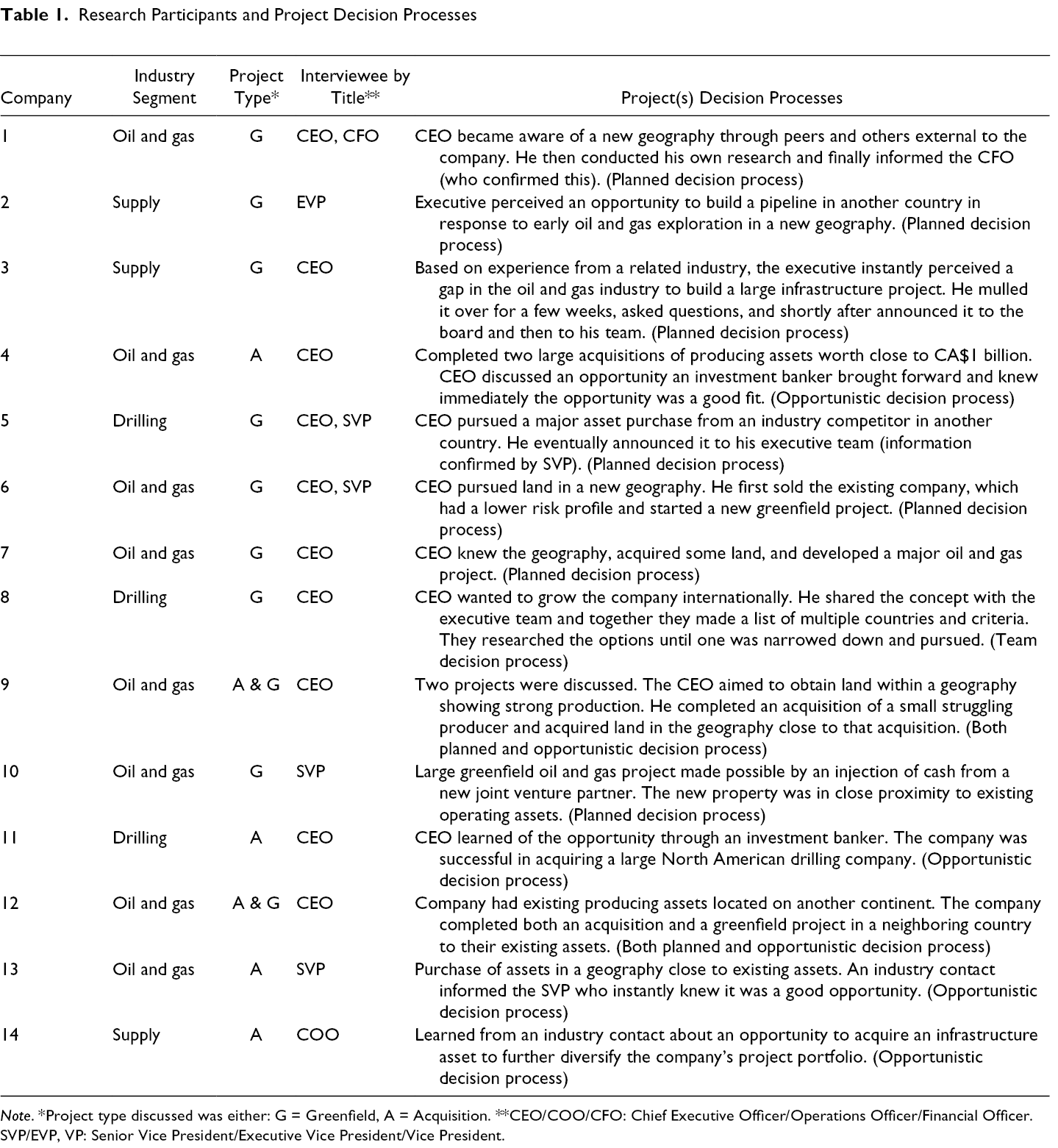

A semistructured interview guide was designed to answer the research question and to understand the project and its company context. Interviews were conducted with the primary front-end project decision makers, which, in each case, turned out to be the CEO or a senior leader with the appropriate decision authority. While these were the primary sources of data, they were supplemented by interviews of additional executives at three of the companies and by the interviewer’s direct observations. As per the grounded theory methodology, theoretical sampling was employed for the purpose of extending theory rather than making generalizations outside of the sample population (Pickard, 2007). We collected and analyzed data about 16 project decisions at 14 oil companies (as summarized in Table 1). Table 1 also indicates the decision process types, which are discussed in the Findings section of this article.

Research Participants and Project Decision Processes

Note. *Project type discussed was either: G = Greenfield, A = Acquisition. **CEO/COO/CFO: Chief Executive Officer/Operations Officer/Financial Officer. SVP/EVP, VP: Senior Vice President/Executive Vice President/Vice President.

All but one interview were recorded and transcribed into NVivo. The transcripts totaled 255 typed pages as well as noted pauses, emotion, intonation, and anything else that stood out during transcription. Handwritten notes (one half to six pages) were made about the interviewer’s contextual observations and reflections.

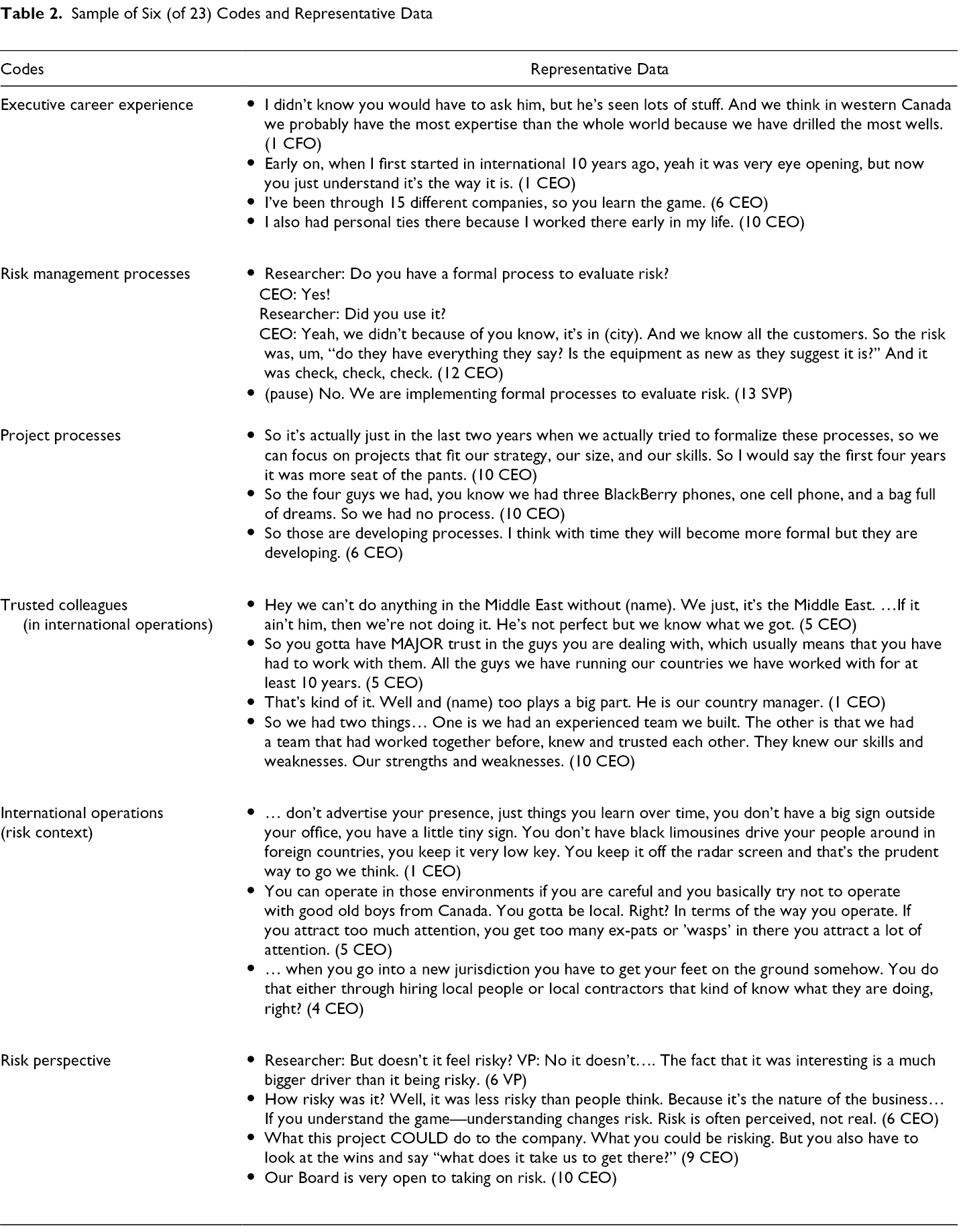

Developing first-order concepts (Gioia et al., 2012) followed multiple steps. First, the interview data were categorized (using Excel) into 23 coded columns. Each sentence, or a cluster of sentences, for each transcript was assigned a descriptive code that reflected the essence of the sentence content. For example, many executives would initiate a discussion about how to conduct business in other countries; this was captured under a code “international operations” (Table 2). As the number of interviews increased, slight adjustments were made to the interview guide and codes based on patterns induced from the data (Gioia et al., 2012).

Sample of Six (of 23) Codes and Representative Data

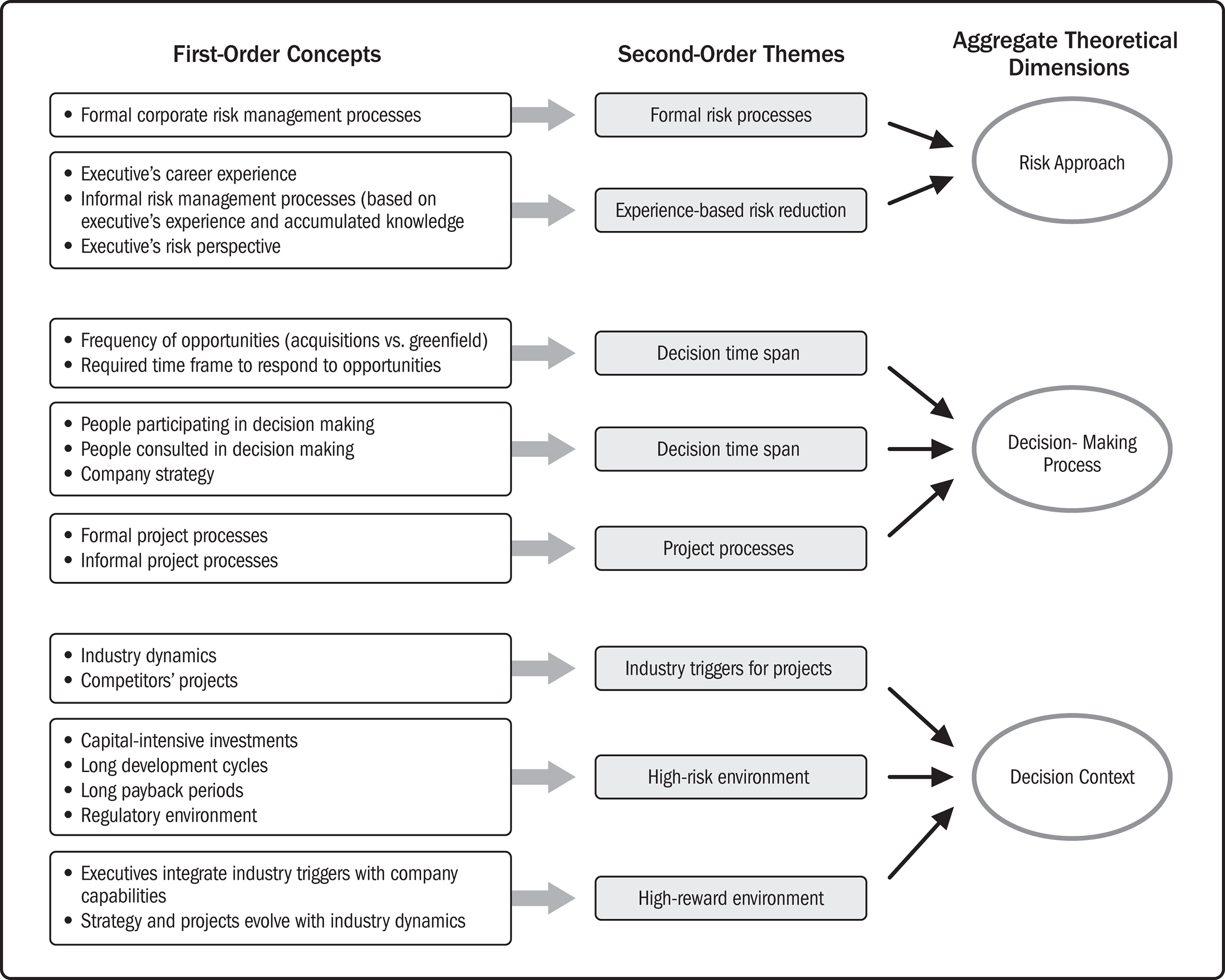

Next, information within each of the 23 coded columns was analyzed, summarized, and recorded on 23 individual index cards. To induce first-order concepts (Gioia et al., 2012), we looked for patterns, sequences, or commonalities by placing the cards side-by-side and into small groups. For example, there were six cards with codes focused on contextual factors in the operating environment (e.g., environmental and regulatory issues, influential people or companies [e.g., investment brokers]). This process resulted in eight first-order concepts. To abstract to second-order themes, the first-order concepts were grouped by similarity and a theme was assigned based on this similarity.

At this stage, grounded theory method (Glaser & Strauss, 1967) would suggest theoretical saturation had occurred. However, the analytical process continued further by working with the second-order themes until they were abstracted into three aggregate theoretical dimensions (Gioia et al., 2012): risk approach, decision-making process, and decision context (Figure 1). These dimensions helped explain how an executive made their project decision, as discussed in the Findings section.

Data structure.

The later and final interviews were not adding new information or insights. Steps were taken throughout the data collection and analysis to ensure validity and reliability of the findings. First, consistent data collection procedures were followed. Second, interview data were verified with other data sources. These sources served to test alignment between the executive’s recollection of events versus what public sources indicated (e.g., investment analyst). Third, memos to track the researcher’s thoughts about the data and analysis (Yin, 2009) were used. As a means of validation, findings were communicated back to those executives who were interested. Finally, we interviewed four executives at engineering, procurement, construction (EPC) companies. They provided perspective on the relationships between their EPC companies and the executives from oil and gas companies with regard to risk, time, and urgency for project design and construction.

Findings

The study’s purpose was to understand how front-end project decisions—identifying, evaluating, and selecting project concepts—were made in upstream oil and gas companies. Before discussing what we discovered about the decision processes, we substantiate why the upstream oil and gas industry is a specific high-risk and high-return context that requires a different approach to front-end project decisions versus what the normative project management guidelines would suggest.

Upstream Oil and Gas as a Specific Context: Risk Management and Value Creation

Project management entails risk management to facilitate value creation through projects (Williams et al., 2019). In the upstream oil and gas industry, value for shareholders is created primarily through growth (as opposed to profits and dividends), by accumulating oil and gas-producing assets. As one interviewee told us: “The assets themselves create value, the execution of projects to exploit the asset is really making sure you don’t destroy value in the process” (6 VP). Companies need to acquire or develop productive assets in order to increase their share price and keep growing, competing for both assets and capital, in continual cycles. This makes the industry highly dynamic and the management of risk very important to ongoing value creation:

We did another private raise. Because we needed to move the share price in order to keep going… what’s our share price comprised of? It’s comprised of NPV x the number of risk factors. Financial risk. Technical risk. And then you add up what’s the actual share price. NPV x risk 1 x risk 2 gives you the actual share price. (6 VP)

These oil and gas executives had learned to manage risks through their accumulated understanding of their industry, such as the geological properties of oil and gas reservoirs, the technologies available to assess and produce from them, and the expertise of various industry players:

We (will) operate it, which is very important to us corporately… It’s not particularly deep drill depths so it’s extremely manageable for a small company. It’s close to significant light oil production, which is important to us from a risk standpoint. And it’s also something that is attractive to investors. Really coming back to risk we see it as a lower risk; it’s still exploration but it’s not rank wild cat new basin type of exploration type stuff. Relatively low risk from an exploration standpoint… It would NOT be that significant to (x company) but for a little company like us and… That will have an undiscounted PV number of about CA$300 to CA$350 million dollars. Very significant. A significant game changer… And it’s a project that we can manage, we can afford—by afford meaning, we can raise funds, bring in partners… (1 CEO)

Front-End Project Decision Processes

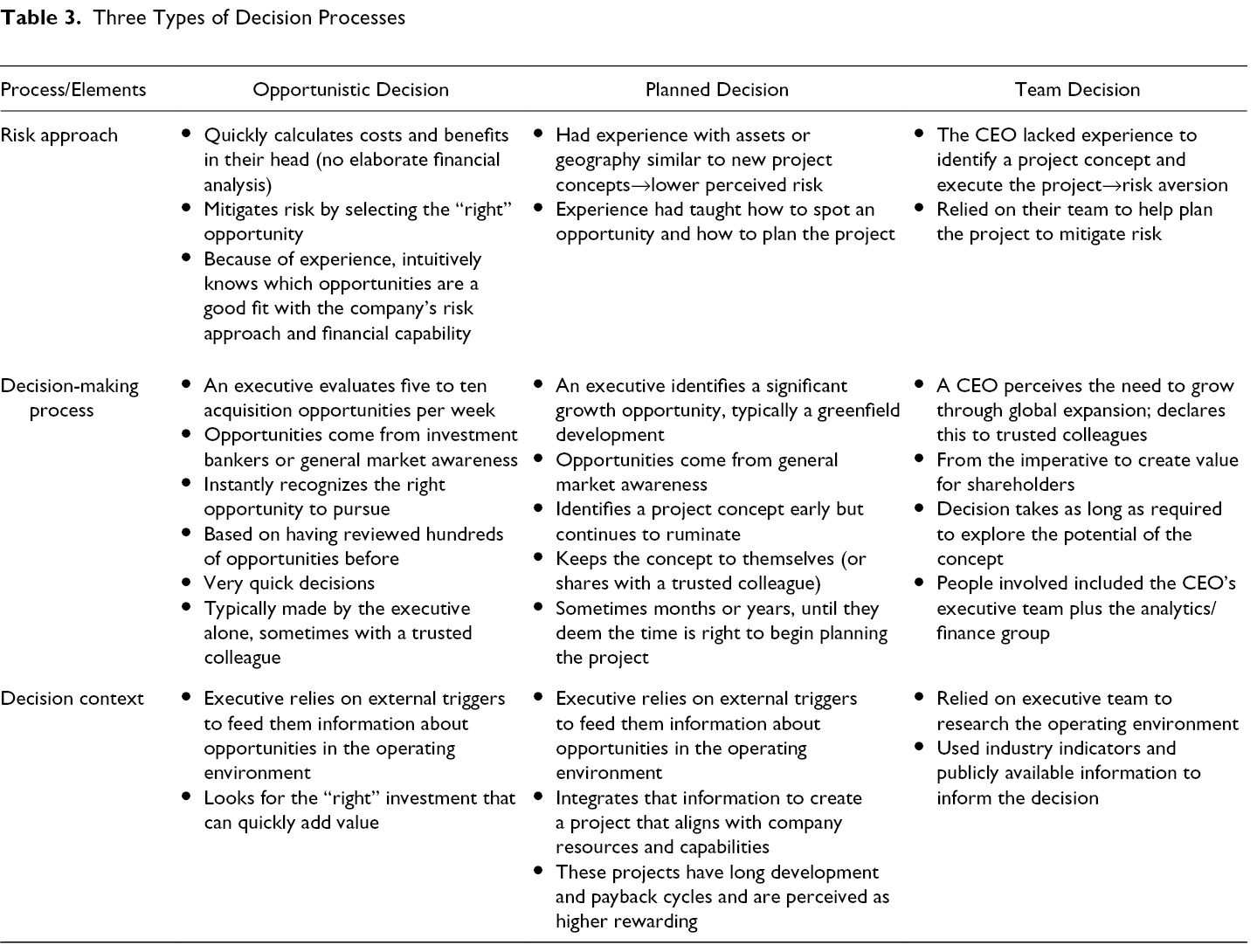

From our data, we identified three types of processes the executives used to make value-driven major project decisions. Two of these were similar and more common: Opportunistic and Planned, whereas the third, labeled as a Team Decision Process, was different and used by only one CEO. These decision processes varied by the aggregate theoretical dimensions depicted in Figure 1 in the Method section. The Team Decision Process began in a similar fashion as the Planned Process, but as the project concept progressed, it developed along a significantly different path. The three processes are summarized in Table 3.

Three Types of Decision Processes

Opportunistic Process

This project decision process was typically applied to acquisition projects. Executives, typically CEOs, encountered hundreds of acquisition opportunities per year. Each interviewed executive told us how he had learned about the “right” opportunity from weekly reviews of potential acquisitions. All commented on how opportunities to acquire oil and gas assets constantly circulate in the marketplace. The information about these opportunities came from external sources (e.g., investment bankers or the executive’s network or other industry contacts) as opposed to employees or the executive team members.

The Opportunistic Process had an extremely short time span—almost instantaneous—to make a decision, facilitated by three factors. First, these executives were very aware of the market for oil and gas assets. For example, during the interview they commented on their peers’ oil and gas projects. Second, they were exposed to five opportunities per week on average, which accumulated their industry knowledge. Third, the executives perceived the risk as reduced because of their experience with similar past opportunities. Once they made the decision to proceed (taking minutes to hours), the next step was to seek additional information to validate the decision. As time progressed, additional information was gathered and risks identified, and a bid on the project was or was not made.

The final step in this process was to determine when to share the project concept with others in the organization. Although the decision maker had already finalized the decision, transferring his vision and concept to others could take time (or may not occur at all if they did not proceed past this point). The person(s) with whom the decision maker shared the decision varied but generally included either a board member or a member of the executive team.

The information the CEOs had about the opportunity to make the decision would be considered insufficient by most people. However, these experienced executives viewed it as ample. Many had trouble articulating why this was such a good fit, because their decision to proceed was as obvious to them as proceeding through an intersection when the light turns green. In the words of one executive:

…it was a combination of things. On any one day we are looking at maybe 10 different opportunities. Maybe I’ll say five corporate opportunities on any day of the week. And then, usually they are too expensive, and usually they, there’s issues… Um, or maybe not quite the right strategic fit or whatever. So all the stars lined up vertically on this one. Where it was a strategic fit. Where it was an extremely good valuation… And, of course, the financial ability to do it and the financial ability to execute on the lands once we had done the acquisition. (10 CEO)

Although the executives were exposed to hundreds of acquisition opportunities per year, they identified only a handful of projects as worth pursuing, distributed randomly throughout the year. In addition, each opportunity had a short window. Therefore, when a value-creating project idea presented itself, it had to be acted upon immediately. The constant inflow of opportunities added to the executive’s already deep knowledge. This contrasts with a portfolio management process, where the reviewer has time to make a systematically considered decision, often involving multiple decision makers (Heising, 2012).

Planned Process

In a Planned Process, the decision maker perceived an untapped opportunity (often a greenfield development) in the market and believed he could develop it into a value-creating project. In the words of one CEO: “and it has to be all in kind of analysis. What this project COULD do to the company. What you could be risking. But you also have to look at the wins and say ‘what does it take us to get there?’” (9 CEO).

The decision period is longer and potentially riskier than in the Opportunistic Process, because the decision maker was gathering information about his concept and building the business case. Once the decision maker believed he had a well-formed concept (e.g., information about a country or specific location and proximity to other successful oil and gas production projects), he began to include additional individuals in the process. Until then, the decision maker kept the project concept confidential. One CEO shared the concept with his leadership team only just prior to announcing it publicly:

Researcher: When did you first consider [opportunity]? My guess is…

Interviewee: Oh, way before we even started. (stated very matter of factly)

Researcher: I was going to say that! How long before June? I mean (researcher is cut off)

Interviewee: Oh, years. (5 CEO)

Another CEO had identified a unique opportunity, but with a much higher risk profile than acceptable to the shareholders of the current company. This CEO first disclosed the project concept to a few key board members. Each of them then sold their position and together formed a new company and raised capital for a higher-risk venture to develop the new project concept. The process took almost two years from concept to launch. The shareholders had signed up for a higher-risk stock:

Having had the opportunity to work through a number of projects … the capital understood what we did and do.… And so that knowledge allowed us to … to take on what might be more perceived risk for a greater return. So by going earlier into a play, you take on more risk but the return is high…To also have an understanding in investors’ minds that we weren’t just simply “wild-ass” I have to use that word. We were quite rational…And so we used the words ‘the road less traveled’ or opportunities less commonly exploited, not because they shouldn’t be, but because they hadn’t been. And so that creates the opportunity for us and that was the reason we went after it… (6 CEO)

Team Decision Process

This process contrasts with the other two. Only one CEO in the study had taken a methodical, well-documented team-decision approach. This CEO’s intent was to create value for shareholders through growth by pursing a geographical diversification strategy. Once the CEO had made the decision to expand into a new country, his approach was to include the executive team in the concept development and have the team choose the country for expansion. The team created a list, researched each country, and then narrowed it down to seven options. Each was evaluated according to the team’s criteria: political stability, economic opportunity, ease of signing contracts, and other factors. Unlike the other interviewees, this CEO appeared to not favor any one opportunity; all options seemed to have merit in the early stages.

Importantly, the decision to establish an international presence was made by the CEO alone, similar to the other two processes. However, the key difference was that additional people were brought in earlier and had input into the project concept, whereas in the other processes, others joined the project planning and execution phases after the project was conceived.

The CEO using the Team Decision Process differed from the other executive decision makers and had transitioned to oil and gas late in his career from an unrelated industry. His educational background was associated with risk management and his risk tolerance was much lower than that of the other interviewed executives. This CEO also characterized his decision as a team process. For example, he mentioned involving the team and used the word “we” much more than the other CEOs interviewed; he also shared more information with his team during project concept decision-making.

Executives’ Major Project Decision Processes Compared

All three decision processes can be visualized as a funnel. In the Team Decision Process, the funnel mouth starts wide, rich with opportunities to enter several countries and plentiful information. Over time, the mouth narrows until a final decision is made. All options were systematically considered, based on decision criteria and gradually eliminated, until the eventual project took shape and was finalized through the management team’s joint decision-making. This resembles the normative guidelines for a project portfolio process (Heising, 2012).

For the other two processes, the reverse was true: the decision was made quickly, starting at the narrow stem or neck of the funnel. As more information became known to the decision makers, and as more people were brought in on the project, the funnel widened and each new piece of information confirmed what the decision maker had suspected in his original decision.

The difference between the Team Decision Process and the Opportunistic and the Planned decision processes is how the Aggregate Theoretical Dimensions (Figure 1) manifested in the executives’ decision. Despite how the opportunities may have presented themselves and how or why a project conceived varied (in line with the Aggregate Theoretical Dimensions), we identified elements common to the Opportunistic and Planned project decision-making processes.

First, the executives were mostly the sole decision makers at the front end of projects. They emphatically believed their key contribution was being the major project decision maker. They perceived their strength and responsibility to create long-term value for shareholders. They believed they made value-creating decisions that aligned with market and shareholder expectations and had absolute confidence in their decisions. Most told us they failed to see where another person could contribute. The decision maker owned the responsibility: “Not to denigrate anybody’s contribution at Board level but its management stuff. It drives the truck…. here is how we think we should move the company ahead.” (7 CEO)

Given the confidence in his own abilities and the need to be discreet about project ideas to protect their value-creation potential, the executive kept the opportunity to himself for a period of time or only shared it with a select few. Until the decision maker believed the timing was right, he saw no need to share the idea. An additional reason for this was that the high number of opportunities that landed on a CEO’s desk regularly made it impossible to review each systematically with the full executive team, particularly if the decision needed to be made quickly, as in the case of an acquisition.

Second, the executives had deep industry experience, which was highly relevant to their ability to choose value-creating projects and manage risks. For example, they had typically worked in the geographies they were considering for projects, often still had strong networks there, knew how to conduct themselves in the region, or knew how to seek out information. All of this helped reduce risk (e.g., knowledge of regulatory processes) or manage the safety of those involved (e.g., hire local contractors or keep a low profile in international jurisdictions):

…when we evaluate risk we evaluate business risk…there is security risk… fiscal risk…regulatory… environmental… liability…. Aboriginal… government…. social… community… All these risks we see every day here. Of all of these risks there is only one there that a company can actually manage and that’s security. You can hire, or we can build fences. Or we can put in place travel policies and procedures… But all those other risks we can’t manage… So you look at [country] and everyone thinks “oh guerrillas, and drugs and people getting shot.” In reality, we can manage that. The cost, it’s an operating cost. (10 CEO)

Third, the executives were often able to make the front-end project decisions quickly with minimal analysis, based on substantial experience relevant to their major project concept. They did not need to build spreadsheets or perform a formal analysis. They could easily and quickly complete a long-term cost/benefit analysis in their head and determine a rough estimate and whether they could raise capital and bring the project to fruition.

Finally, for many of the CEOs, being able to decide on these major project opportunities was a major motivator. They thrived on the challenges, managing risks, and being able to create value through projects:

… the international game is a lot more unique from the domestic game than most domestic E&P guys appreciate. In fact, I would wager a lot…a lot different than those guys think… Having said that, it’s also WAY more fun… And to be honest, quite simple. You go overseas where there are NO templates, NO processes for anything. There are NO data… (1 CEO)

Well, I would be bored as hell excuse the expression. Personally, I think that the challenge is why I do it. … That’s why I’m doing it…I like new ideas…For me, the repetition is not what I am looking for. It’s the enhancement or testing or trial and then the dynamic and the speed. That part is a huge amount of fun. So, I am doing that to scratch that. (6 CEO)

Discussion

For too long, the ideation process at the front end of a project has remained elusive to researchers (Sergi, 2012; Takey & Carvalho, 2016). Research on long-term value creation is evolving and subjective; few studies address how that value is created (Laursen & Svejvig, 2016; Willumsen et al., 2019). By understanding how projects are conceived in different types of contexts, we can determine whether and which project processes help create long-term value, or destroy it.

We offer three contributions to the literature about the front end of projects. First, our findings show that in high-risk, high-reward contexts such as the upstream oil and gas industry, pre-project, front-end decision-making significantly affected value creation from projects (through growth), and formal project management processes play a lesser (or no) role. Second, an experienced executive with integrated knowledge is often the sole decision maker identifying, evaluating, and selecting project concepts, even for major projects. Last, we identified three processes for such decisions in this high-risk, high-reward context; they all yielded value-creating projects but varied by the decision maker’s risk approach and particular decision context. Each of these is discussed as follows.

First, the executives in our study used knowledge integrated from past experiences to create value for their organizations. The executives chose projects that utilized and incorporated their prior experience, such as having worked in a similar geography (e.g., the same hydrocarbon basin or country). They also maintained close working relationships with colleagues from prior projects. All of these factors reduced uncertainty and risk. The direct application of their previous experience allowed them to navigate the complexity within their environment and create value from what most would deem to be a highly ambiguous situation (Eling et al., 2014; Matinheikki et al., 2016).

This is supported by the strategic decision-making literature. Some researchers attribute this to the decision makers’ superior cognitive capability, which they consider the microfoundation of firms’ sustainable competitive advantage (or above-average profitability; Felin et al., 2015; Helfat & Peteraf, 2015). For example, Gavetti (2012) attributes executive decision makers’ superior cognitive capability to their experience-based associative reasoning, through which executives draw analogies to past experiences and, therefore, can recognize more distant opportunities than those with less experience.

Researchers who have studied the role of intuition in decision-making often attribute the ability to make fast, effective decisions to the ability to harness intuition (understood as a sudden, subconscious insight), based on, again, previous experiences (Dane et al., 2012; Hodgkinson & Sadler-Smith, 2018). The relationship between intuition and rational analysis in decision-making is not as well understood. However, some research indicates that it is the decision makers’ ability (which can be learned, regardless of experience) to integrate the intuition (subconscious cognitive processing) with conscious, rational analysis (identification and application of principles), which enables rapid, efficacious decision-making (Woiceshyn, 2011).

Second, our findings substantiate a unique role for executives within the project ideation phase as the sole project concept initiator for major projects. Only two prior studies examined an individual as the unit of analysis, with no prior study considering an executive as the project initiator (Page & Schirr, 2008). In addition, our findings provide a basis for arguing who might be best suited (Eling & Herstatt, 2017; Poskela & Martinsuo, 2009; Salter et al., 2015) to create long-term value for the firm (Mannor et al., 2016) in high-risk, high-reward contexts. In such contexts, the executive decision makers are not the project approvers at the end of the search process, but play a central role as the opportunity identifiers and evaluators, much earlier at the front end of the project decision-making process.

Experience can reduce the perception of risk, which invites more exploration of opportunities. The role of the project initiator came naturally to the executives in our study, as they held deep experience from years in their industry with similar projects. Therefore, they perceived their operating environment as unambiguous and straightforward. In addition, they saw options for growing their organization but exhibited patience for what they deemed to be the right opportunity, which included value for both the organization and other stakeholders (Martinsuo, 2019; Smyth et al., 2018). They were not trying to make perfect decisions but decisions that they deemed value-creating, based on their experience. Executives reside in an ideal position, given their responsibility to ensure projects align to the strategic direction and their vantage point of looking across divisions of their organization (Poskela & Martinsuo, 2009; Salter et al., 2015).

Finally, our study identified and described three decision-making processes (Opportunistic, Planned, and Team Decision) used by the executives at projects’ front end. They bypassed a formal project management front-end evaluation process. Instead, the executives relied on their deep industry experience and used long-term value creation as the main decision criterion for concept selection. These findings raise questions about the applicability of front-end project concept evaluation processes. Traditionally, a rational lens has been used to assess projects, but recent research suggests projects viewed as “fuzzy” are actually carefully managed but adhere to a different logic and therefore require different assessment processes (Lenfle, 2016).

Both exploration of new opportunities and exploiting existing resources (March, 1991) are required for long-term value creation (measured as return on shareholders’ investment). Because exploration projects carry more risk, are less certain, and take longer to develop than exploitation projects, we argue that they require different evaluation processes. Had the executives’ project concepts been evaluated through formal project processes, they would have been likely classified as high-risk and subjected to longer and more elaborate scrutiny (Lenfle et al., 2019; Samset & Volden, 2016), potentially leading to missing valuable opportunities. Exploitation projects are less risky (often with a smaller relative return), easier to predict and, therefore, well suited to being evaluated with traditional project management processes.

According to Williams et al. (2019), “the strategic role of the ‘front-end’ is in defining what the project is to achieve, establishing its feasibility, and shaping project ‘success’” (pp. 3–4). The executives in our study used the “iron triangle” criteria of time, budget, and quality as their guide to creating value (Pollack et al., 2018). These decisions were made because the executives’ experience taught them to spot value-creating opportunities among the many ideas that presented themselves. They showed discipline by proceeding with the project only when they believed it would have the highest probability of success. “The front-end …. [sits] within an environment and context which defines the need and context for the project.” (Williams et al., 2019, p. 4).

Relating existing front-end project processes to the three types of project decision-making processes may help decisions on timing (e.g., how fully developed the concept should be prior to applying project processes), on choosing a front-end decision model (based on project type or size), and on who should use front-end processes (e.g., level of experience required). Based on the three decision processes examined in our study, we suggest a high need for fit for context flexible processes and tools that can fit the unique requirements of each project and therefore create and preserve value at this early stage of project conception.

There are two important boundary conditions to our findings. First, the executives in our study were all industry veterans, which gave them the ability to integrate that deep experience into effective, value-creating project concepts. Those with little or no industry experience likely could not have made decisions as rapidly and efficaciously (which the Team Decision Process also suggests). The level of experience of the executive decision makers is a key theoretical implication of our finds and helps explain why rigid project processes at the project conception stage might hamper, rather than enhance, value creation. The practical implications of our findings reflect this also: The executives kept the project concept to themselves until they deemed it ready for further planning (not evaluation).

Second, the executives had deemed the projects they discussed to have achieved success. The process the executives used (aside from Team Decision) required no company resources (besides the executives’ time), making the project ideation both cost effective and efficient. Analysis of the Opportunistic Process the executives used for acquisition decisions indicated that formal project processes were not responsive enough within the short decision-making time frame. In addition, due to the frequency with which the executives reviewed acquisition opportunities, applying judgment is the easiest way to decide (Pitz & Sachs, 1984). Although the project concept was initiated by the executives, by sharing it, they transferred responsibility for further planning to others in the organization. Only at that point did the project require additional resources. Researching projects deemed to have failed may yield very different findings.

Limitations of the Study and Future Research

While our research sheds light on the “who” and the “how” at the front end of projects, it is one study in one industry context of mostly very experienced decision makers. More research in different industries and on different projects will help determine which project decision-making processes are best suited for what types of projects.

This research focused on the decision-making process of a sole executive and did not follow the process of transitioning into formal corporate processes for further planning. More could be learned about the transitional period of moving a concept into formal processes, which could be a stumbling point in the overall success of a project. A longitudinal study, drawing from some of the strategic decision-making literature we have cited, would allow following the internal decision-making process of an executive as it is occurring, including the transition into formal corporate project processes and, finally, into closure and operationalization.

As Suddaby (2006) noted, the purpose of qualitative research is not to make truth statements about reality but to provide fresh understandings of relationships between social actors. Therefore, the findings from this study cannot be used as a generalization of how all executives make major capital project decisions or decisions outside of their domain of experience (e.g., IT projects). This study does, however, increase our understanding of the decision-making process in the high-risk context of natural resource exploration with major oil and gas projects.

Future research could identify additional decision-making processes and types of decision makers. For example, do decision processes vary with the type of project, industry, or level of authority within the organization? All the projects and organizations studied were in the oil and gas sector. Oil and gas projects face evolving and stringent environmental regulations, require a substantial capital investment, and often have a long-time horizon. Each of these factors increases the level of risk. Other industries may have different project drivers (e.g., innovation) and place these further up or down the list of priorities.

While our study adds to the small portion of qualitative studies (25) about the front end of projects, more could be learned from a similar approach (Savino et al., 2017). For example, decision makers in different industries or the same industry in different geographic locations and experience levels may view opportunities, risk, and projects very differently. Research examining the experience level of a project concept initiator and what they deemed as risky might give us insight into when corporate governance should be applied in the early project processes.

Conclusion

Based on their position in the organization, senior executives are often the only individuals who can look across the organization and into each of the levels within their organization. By doing so, they can evaluate existing strategic opportunities and use their extensive experience to conceive new projects, without involving others. Using one of the three decision-making processes identified in this study and their experience can help executives to manage risk and conceive value-creating projects. We suggest that in dynamic, high-risk contexts and with exploratory projects, the formal project assessment processes may hamper value creation and should not be applied to project concepts initiated by experienced executives. Instead, such processes should be used with exploitation projects or in subsequent project stages where they have proved useful: in transitioning well-developed concepts to project teams for detailed planning and execution.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Author Biographies