Abstract

This article presents an interdisciplinary assessment of the need to transform our single-planet civilization into a multi-planetary species through the lens of space resource extraction. In light of the annually increasing volumes of resource mining driven by ever-growing demand, the issue of replenishing the mineral and raw materials base required to sustain and further advance technological progress remains highly relevant. Accordingly, this article evaluates the prospects for the development of space resource mining, emphasizing its interconnection with the energy development of civilization as outlined by N.S. Kardashev, and provides a brief overview of the sources of these resources along with existing strategies for their utilization.

Keywords

INTRODUCTION

Life on Earth has a long history, estimated by various geological and radiometric methods to span over 4.5 billion years. 1 However, the first reliable evidence of human civilization (in the form of systematic writing) appears only about 5 thousand years ago, which constitutes less than one-millionth of the total time our planet has existed. Up to that point, evolution proceeded extremely slowly—from the simplest unicellular organisms to multicellular life, and eventually to the emergence of higher forms with advanced cognitive abilities. 2 Yet even in this brief historical period, humanity has journeyed a long way from primitive agrarian communities to a developed technological civilization, launching spacecraft beyond the boundaries of the solar system.

Throughout history, however, our evolution has been accompanied by a series of risks capable of either slowing down our development (as has partially occurred) or completely annihilating it (potential risks with a prospect spanning tens to hundreds of millions of years):3,4

Large-scale military conflicts result in hundreds of thousands of deaths and cause colossal economic damage. Moreover, the existence of nuclear weapons—and the possibility of their use during escalated conflicts—remains an acute concern. This factor significantly undermines the capacity of civilization to adapt to both external and internal threats, thereby increasing the risk of global collapse. Earth’s geological history demonstrates that the planet has repeatedly endured catastrophic impacts. For example, the impact of a large asteroid about 66 million years ago led to the extinction of the dinosaurs. Such events serve as a reminder that external, extraterrestrial factors can radically alter the conditions for life on our planet. According to various scientific estimates, within the next 1–2 billion years, the Sun’s luminosity will increase sufficiently to cause significant heating of the Earth. This, in turn, could trigger the so-called “runaway greenhouse effect”, ultimately transforming our planet into an excessively hot, arid, and uninhabitable environment.

In the context of discussing the so-called “Great Filter”, a key question arises: can humanity leave its planet before facing an irreversible catastrophe?

Modern research in the fields of geosciences, space engineering, robotics, and other related disciplines emphasizes the need to rethink the strategy for the long-term survival of our human civilization. A comprehensive analysis of Earth’s evolution, cosmic risks, and the potential for mining mineral resources on various celestial bodies leads to the formulation of the hypothesis that transitioning to a multi-planetary expansion is a crucial step for the survival of humanity as a biological species.

Limited Earth Resources as a Stimulus for the Exploration of Celestial Bodies

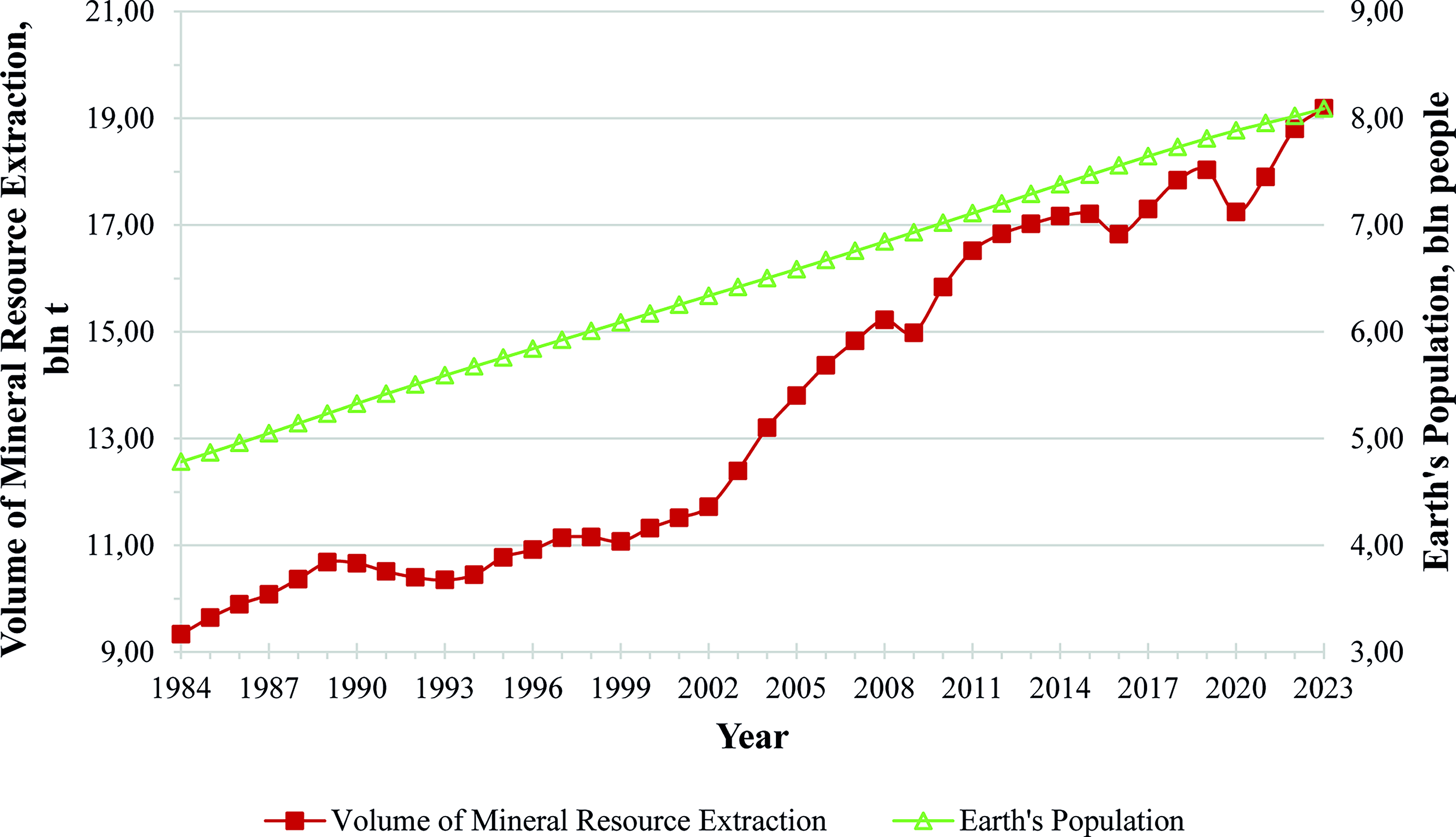

As the population of our planet grows and the economy develops, the extraction of mineral resources becomes increasingly large-scale and intensive (see Fig. 1 ). The evolution of modern civilization is accompanied by a constant rise in the demand for resources needed to sustain economic activity, drive technological progress, and support infrastructural development.

Dynamics of mineral resource extraction volumes and Earth’s population growth from 1984 to 2023.

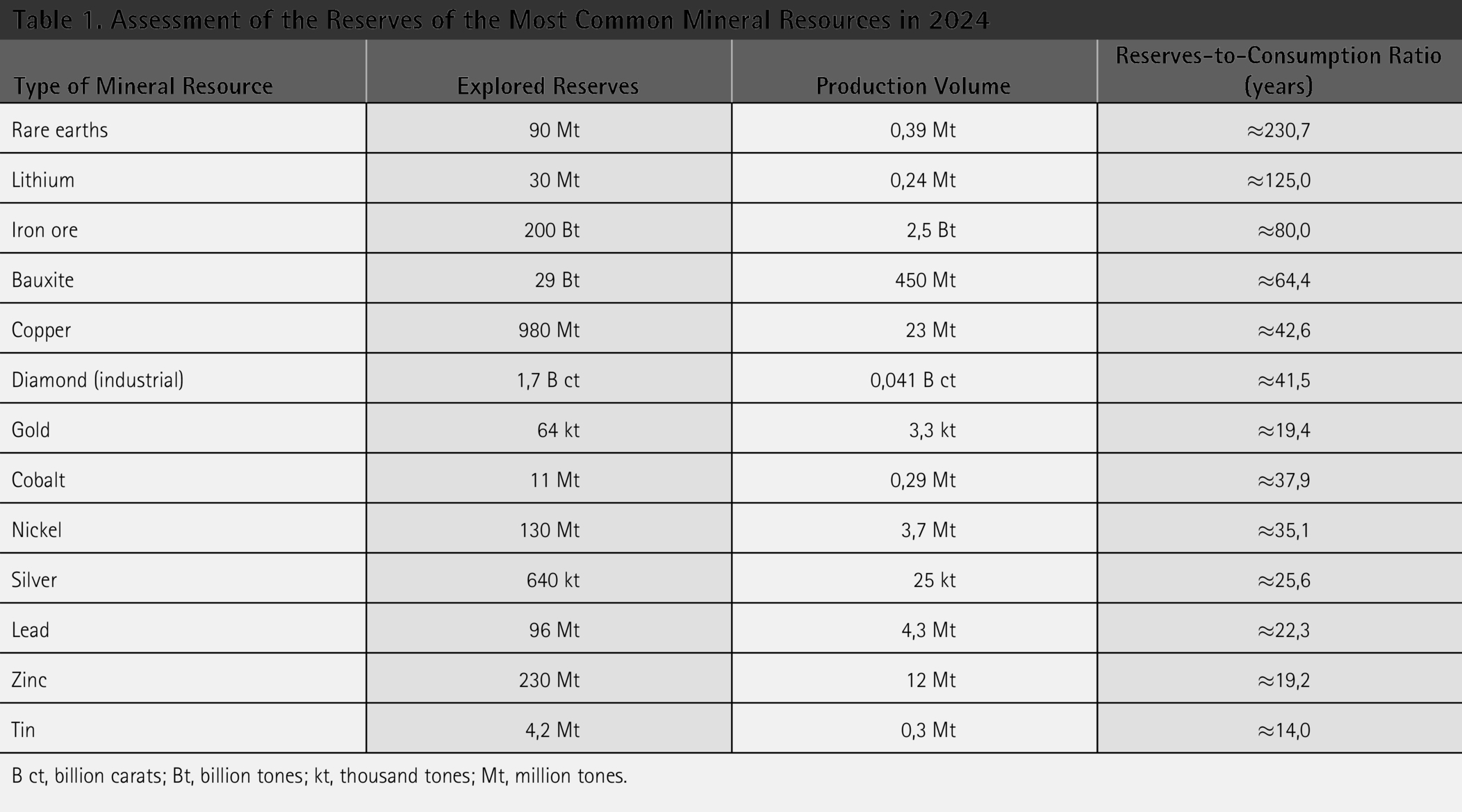

However, Earth’s existing reserves of mineral resources are gradually depleting, and their extraction is becoming increasingly costly and associated with environmental risks. Table 1 presents the up-to-date (2024) information on the explored reserves of some mineral resources, extraction volumes, and the ratio of reserves to consumption (according to data from the US Geological Survey). It should be noted that the data in the table do not include identified resources—the total amount of known raw material that is not always economically feasible to extract under current economic conditions. For example, the identified resources of zinc amount to 1.9 billion tones, copper to 1.5 billion tones, nickel to 350 million tones, and iron ore to 800 billion tones.

Assessment of the Reserves of the Most Common Mineral Resources in 2024

B ct, billion carats; Bt, billion tones; kt, thousand tones; Mt, million tones.

Moreover, it is important to understand that these data are dynamic and are continuously updated. This is due to further exploration of existing deposits and the discovery of new ones. A prime example is the case of gold: in 2000, the explored reserves amounted to 48 thousand tones, and by now they have increased to 64 thousand tones, which corresponds to a 33% growth. A similar increase was observed in the annual production volumes of this metal—from 2445 tones in 2000 to 3300 tones at present (a 35% growth). Thus, if the explored gold reserves and production volumes from 2000 had remained unchanged, all the reserves would have been completely exhausted by now. However, this has not occurred, and we are witnessing an increase in these indicators due to further exploration and the commissioning of new major deposits (Sukhoy Log, Russia; Kerr-Sulphurets-Mitchell, Canada; Norte Abierto, Chile; Donlin Creek, USA; La Colosa, Colombia, etc.), advancements in mining and ore processing technologies, as well as economic factors (the rise in gold prices has rendered the extraction of low-grade ores economically viable).

At the global level, the extraction of major mineral resources (such as iron ore, copper, nickel, rare earth elements, hydrocarbons, etc.) represents a complex industrial system. The continuously increasing volumes of extraction for all types of mineral resources (see Fig. 1 ) indicate strong demand from industrial sectors and underscore the need for ongoing expansion of production capacities to meet growing requirements.

An inevitable outcome of such resource consumption will be the depletion of onshore mineral reserves and, consequently, a reduction in production volumes—a trend already observed in some regions of the world. In addition to the economic aspects, intensive mining leads to negative environmental impacts, such as land degradation, water pollution, and the loss of biodiversity. One of the responses to the challenges posed by the depletion of continental resources is the gradual development of deep-sea mining, which represents a promising direction for establishing an additional resource base.5,6

Despite the promise of developing new technologies for exploiting continental deposits with low concentrations of useful components, and the prospects for deep-sea mining in the coming years, the finite nature of Earth’s resources predetermines their inevitable depletion. Consequently, our species will face a critical choice: either to confront resource shortages, which could lead to the collapse of global production and economic systems, or to make the strategic decision to explore space for alternative sources of raw materials. 7

This becomes a prerequisite for transitioning toward the development of multi-planetary infrastructure as an essential condition for the long-term survival of humanity.

The Energy Paradigm of Transitioning to Extraterrestrial Resource Extraction

The transition to space resource exploitation is closely tied to the concept of the energy development of civilization, as reflected in the scale developed by the Soviet scientist N.S. Kardashev. According to this scale, a civilization capable of fully harnessing all the energy available on its home planet (Type I) must possess advanced technologies not only for the efficient distribution of resources but also for their replenishment from external sources. In the long term, expanding the resource extraction base beyond Earth is a necessary condition for transitioning to a higher type of civilization. 8

At present, humanity has not yet fully exploited the potential of our planet (i.e., achieving Type I on the Kardashev scale), but the transition to a higher type entails the increasingly significant involvement of resources, including those from extraterrestrial sources. This is why mining mineral resources on the Moon, asteroids, and Mars is considered both a strategic and evolutionary step, contributing to:

Alleviating resource constraints for high-tech industries. Establishing an extensive infrastructure beyond Earth. Progressing toward a Type I civilization as defined by Kardashev, and eventually even higher types in the more distant future.

Expanding the mining base beyond Earth not only compensates for the finite nature of terrestrial resources but also lays the foundation for a substantial increase in the energy potential of civilization.

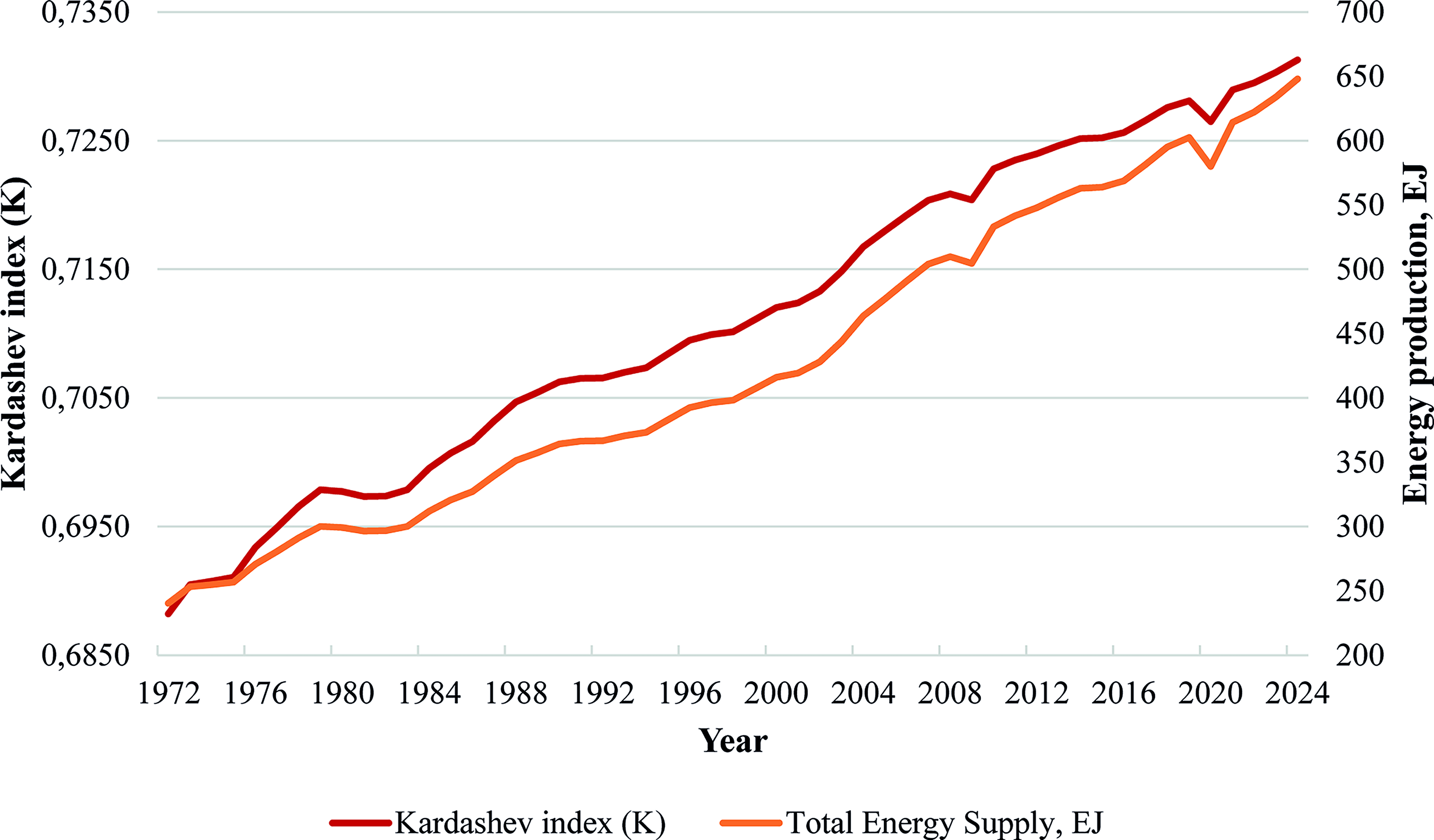

Despite a 2.5-fold increase in global energy production over the past half-century (from 244 EJ in 1972 to 648 EJ in 2024 9 ), humanity remains far from fully realizing the planet’s energy potential. According to calculations, in 1972, the level of human civilization corresponded to K ≈ 0.6882 on the Kardashev scale, while by 2024, it had reached only K ≈ 0.7313. This indicates that progress over 50 years has been quite limited: the increase amounts to only 0.0431, underscoring the inertia of energy evolution under planetary constraints.

Figure 2

illustrates the changes in civilization’s energy level based on global energy production data. The graph clearly delineates phases of stagnation (1979–1984), acceleration (2002–2014), and temporary decline (2019–2020), reflecting the influence of global economic and technological factors.

Change in the Kardashev index (K) with key phases of global energy development (1972–2024).

According to a recent study by Zhang et al., 10 which projects the development level of our civilization through 2060, humanity is expected to experience extremely slow growth if current energy strategies persist—reaching only K ≈ 0.7449, despite a projected rise in total global energy consumption to approximately 887 EJ.

Moreover, scenario analyses accounting for the potential deployment of nuclear fusion energy suggest a possible increase to K ≈ 0.7719 by 2100. These projections provide a compelling rationale for viewing space-based solar power, helium-3 extraction, and extraterrestrial mining of other resources as critical directions for accelerating the evolution of global energy capacity.

Multi-planetary expansion (the colonization of the Moon or Mars, the construction of space infrastructure, etc.) is intrinsically linked to understanding how humanity can transition from an energy-constrained planetary system to a more expansive space economy:

In the short term (the coming decades), mining mineral resources on the Moon and asteroids will help reduce the costs of space logistics and lessen dependence on launching cargo from Earth. In the medium term (several decades until the end of the 21st century), a phase will be reached in which the construction of large stations and potentially powerful space-based power plants will catalyze the utilization of the Sun’s resources (a partial transition to Type II). In the long term (the coming centuries and millennia), humanity may embark on interstellar journeys and the search for habitable exoplanets, serving as a precursor to civilizations of even higher types on the Kardashev scale.

Thus, it follows that the Kardashev Scale not only provides a futuristic assessment of the distant future but also serves as a motivational model for understanding how the exploitation of space resources becomes a step in the transition from a limited planetary community to a fully-fledged spacefaring species.

Current Status and Market Dynamics of Extraterrestrial Resource Extraction

Market volume and development forecasts

According to Morgan Stanley, the global space economy is valued at over $550 billion (as of 2025) and is projected to reach $1 trillion by 2030. At present, only a small fraction of this total is attributed directly to extraterrestrial resource extraction. Accurately assessing the current market value of space mining remains challenging, as the sector is still in its early developmental stages, and estimates vary significantly depending on the methodologies employed by different agencies.

Nevertheless, analytical reports indicate a general consensus placing the current value of the space mining market at approximately $2 billion. This reflects growing interest in the extraction of high-value resources from asteroids, the Moon, and other celestial bodies. Although the market is still nascent, and most governmental and private-sector efforts are currently focused on scientific research and the development of prototype robotic systems, substantial expansion is expected in the coming years.

According to projections by various research firms (including Stratview Research, Mordor Intelligence, Allied Market Research, and The Brainy Insights), the global space mining market could grow to between $3.5 billion and $5 billion by 2030. This growth will be driven by advancements in relevant technologies, increased public and private investment, and the emergence of viable commercial space missions.

The role of governments in shaping the regulatory and technological environment

In recent years, there has been a surge of interest from governmental agencies in the development of extraterrestrial resource utilization. Notable examples include National Aeronautics and Space Administration’s (NASA) Asteroid Redirect Mission 11 (later cancelled and replaced by the Double Asteroid Redirection Test mission, which conducted the first-ever asteroid deflection experiment 12 ); the Luxembourg Space Agency, which actively promotes the commercial space mining sector; 13 and the Japan Aerospace Exploration Agency (JAXA), which has demonstrated a sustained interest in asteroid resource extraction. 14

A closer look at the approaches of leading spacefaring nations to space resource development reveals the following:

United States—The undisputed leader in terms of the number of projects and the scale of private sector engagement. The United States was also among the first countries to adopt national legislation addressing space resource extraction. The “U.S. Commercial Space Launch Competitiveness Act” (H.R.2262), enacted in 2015, 15 granted U.S. companies the legal right to own resources extracted from asteroids and other celestial bodies.

Another significant milestone in the institutional shift toward extraterrestrial resource exploitation was the issuance of Space Policy Directive 1, signed by President Donald Trump in December 2017. The directive emphasized the priority of returning American astronauts to the Moon as a cornerstone of national space policy and specifically highlighted the importance of establishing a “sustainable presence” on the lunar surface. In official strategies, this concept entails not only regular human presence on the Moon but also the gradual development of an in situ resource base to support long-duration missions. Thus, the directive signals a transition from short-term exploratory expeditions to infrastructure-based and resource-driven lunar development.

In alignment with this policy, NASA is coordinating the Artemis program, whose strategic objective extends beyond the mere return of humans to the Moon. The program aims to establish the prerequisites for sustained operations of crewed habitats, autonomous logistics systems, and a scientific-industrial infrastructure on the lunar surface. A key focus area is the development and utilization of lunar resources—primarily water ice located in the polar regions—which may serve both life support needs and as a source for producing rocket propellant.

As of June 2025, the Artemis Accords have been signed by 55 countries. This document outlines a framework for international cooperation in the exploration and utilization of the Moon and other celestial bodies. It includes provisions on transparency, the peaceful nature of activities, and most notably, the principle of establishing “safety zones” to protect areas of active resource extraction or deployed equipment from potential conflicts between nations or organizations. While the accords themselves do not constitute a binding international treaty, they are shaping a de facto regulatory foundation for future extraterrestrial resource operations.

In April 2020, the US Geological Survey released the Unified Geologic Map of the Moon, 16 which provides comprehensive geological coverage of the lunar surface. This map enables researchers to plan future space missions and mineral exploration activities on the Moon with greater precision (see Fig. 3 ).

Fragment of the Unified Geologic Map of the Moon.

This represented a significant step toward the systematization of knowledge about the Moon’s natural resources and the transition from theoretical models to the practical implementation of mining projects. As a result, the United States is already forming a comprehensive architecture of legal, scientific, and technological foundations that renders the scenario of initiating industrial-scale lunar development within the coming decades increasingly feasible.

The People’s Republic of China has adopted a distinctly different approach to extraterrestrial resource utilization, characterized by a high degree of centralized governance, long-term strategic planning, and interagency coordination. Although there is currently no specific law in China regulating the legal regime of space resource extraction, this domain has been officially included in the list of national scientific and technological priorities since 2017. Space mining is considered a strategic objective within the broader framework of high-tech development.

China’s space program is predominantly state-funded, ensuring coherence and stability throughout all stages of implementation. In 2020, the Chang’e-5 mission successfully returned samples of lunar regolith to Earth, laying the groundwork for further research in in situ resource utilization (ISRU). Subsequently, China deployed its Tiangong orbital space station, which serves as a platform for long-duration crewed missions and the testing of equipment under microgravity conditions—an essential phase in the preparation for extraterrestrial mining operations.

In parallel, missions targeting small bodies of the solar system are under development. A sample return mission from asteroid Kamoʻoalewa is scheduled for 2027, which will enable the testing of drilling, capture, and return technologies for extraterrestrial materials.

Of particular note is the structure of China’s strategic planning: principles traditionally applied in terrestrial mining have been fully transferred to the domain of space resource utilization. As outlined in the 14th Five-Year Plan (2021–2025), which emphasizes reducing raw material imports, enhancing geological exploration, and promoting ecological modernization, 17 China’s space strategy similarly incorporates target indicators, state-industry integration, and a focus on scalable technological solutions. Thus, space is perceived as a natural extension of China’s broader resource policy aimed at ensuring technological sovereignty.

In partnership with Russia, China is also advancing the establishment of the International Lunar Research Station by 2035.18,19 This ambitious initiative envisions both scientific exploration and the validation of technologies for in situ resource extraction and utilization.

Beyond governmental efforts, China is actively fostering a commercial space industry. Companies such as Origin Space and CAS Space, supported by state investment funds, are conducting satellite tests for asteroid detection and developing techniques for the capture of small celestial bodies.

Thus, China is implementing a comprehensive model that combines centralized strategic planning, technological advancement, and the integration of heavy industry into the domain of extraterrestrial resource activities. If the current trajectory is maintained, the People’s Republic of China is well positioned to become one of the first nations to achieve practical implementation of space resource extraction within the coming decades.

In contrast, the European Union has adopted a more decentralized approach to the development of extraterrestrial resource utilization, with an emphasis on intergovernmental cooperation and scientific-technological collaboration. Although there is currently no unified European legal framework governing the exploitation of space resources, several member states, as well as the European Space Agency (ESA), have initiated efforts aimed at developing critical components of the infrastructure required for space mining.

A particularly proactive stance has been taken by the Grand Duchy of Luxembourg, where in 2017 a national law was enacted recognizing the right of private companies to own resources extracted in outer space. This legislation provided legal certainty for commercial actors and positioned Luxembourg as a major hub for space technologies and investment. Numerous international enterprises and startups have already taken advantage of this legal environment, selecting Luxembourg as a base for their operations.

Japan is pursuing a gradual and technology-oriented strategy in the domain of extraterrestrial resource utilization, combining advanced scientific missions, the development of a regulatory framework, and active engagement of the private sector. In contrast to countries such as the United States and Luxembourg—whose efforts have focused primarily on establishing legal mechanisms for ownership of space resources—Japan places particular emphasis on the engineering validation of critical technologies and the creation of conditions for their commercial application. A prime example is the Hayabusa2 mission, which successfully returned samples from asteroid Ryugu.20,21

At the national policy level, space resource development is embedded within Japan’s long-term strategic framework—the Space Basic Plan, adopted by the government and codified in the Act on the Promotion of Business Activities for Exploring and Developing Space Resources. 22 This document underscores the importance of integrating Japanese companies into global technology value chains and promoting international cooperation, particularly with the United States, through joint participation in NASA and Artemis programs.

Despite the relatively recent establishment of its national space program, the United Arab Emirates (UAE) has demonstrated a deliberate and strategically sound policy toward the development of extraterrestrial resource utilization.

In 2019, the UAE enacted a national space law, 23 granting legal entities registered in the country the right to own and manage resources extracted from celestial bodies. The legislation is designed to align with international legal frameworks, including the provisions of the 1967 Outer Space Treaty, and positions the UAE as a jurisdiction favorable for registering space-related enterprises.

In this context, the UAE government launched the Dubai Future Foundation, a dedicated fund aimed at supporting high-tech initiatives, including the development and deployment of solutions for extraterrestrial mining.

A central aspect of the UAE’s strategy in this domain is its participation in international missions and cooperative projects. A notable example is the Emirates Lunar Mission, through which the Mohammed Bin Rashid Space Center developed the Rashid-1 rover. In December 2022, the rover was launched aboard the Hakuto-R M1 lander developed by the Japanese company iSpace. The mission’s primary objectives included analyzing the physical properties of lunar regolith (grain size and structure), surface texture, and environmental conditions.

After successfully entering lunar orbit, the lander attempted a soft landing on the Moon’s surface on April 25, 2023. However, the landing was unsuccessful: a hard impact led to the destruction of both the M1 lander and the Rashid-1 rover.24,25

Despite the failure to achieve a soft landing, the Emirates Lunar Mission represented a significant technological milestone for the UAE. It demonstrated the country’s growing capacity to participate in high-technology international projects and to develop indigenous components of planetary exploration systems. Given the UAE’s strong financial resources, sustained government support, and commitment to technological diversification of the national economy, the country is poised to continue expanding its presence in the space sector.

Structure of the In-Space economy

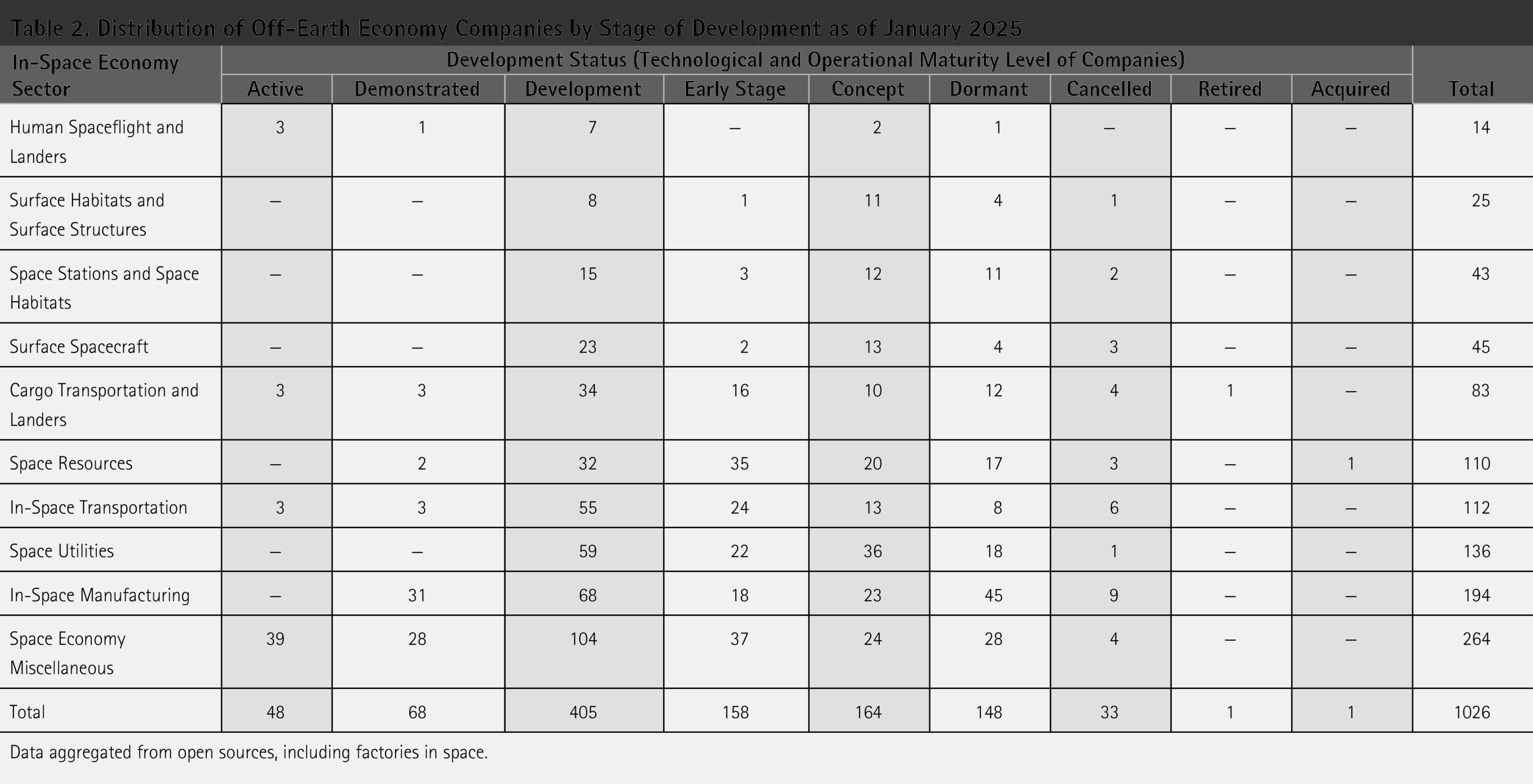

According to data from the specialized online platform Factories in Space, 26 as of January 2025, its database includes over 1,000 companies engaged in the development of various sectors of the in-space economy—a domain encompassing commercial activities carried out using resources, infrastructure, and manufacturing capabilities located beyond Earth.

To gain a more detailed understanding of the current state of the in-space economy, all companies (n = 1,026) were classified based on their stage of technological development. Table 2 presents the distribution of market participants by activity status within each of the ten identified sectors.

Distribution of Off-Earth Economy Companies by Stage of Development as of January 2025

Data aggregated from open sources, including factories in space.

An analysis of Table 2 reveals that nearly 40% of all projects are currently in the development stage, indicating a high level of engineering activity. The dominance of this stage also suggests that, despite the growing interest from both governmental and private sectors, the space industry remains in the process of maturing technological solutions that are suitable for practical deployment in extraterrestrial environments.

When the Early Stage (15.4%) and Concept (16.0%) categories are taken into account, it becomes evident that nearly 71% of all companies at the time of analysis had not yet reached the phase of initial technology demonstration. This is typical of industries characterized by high scientific and technical complexity and extended development cycles, where the transition from a conceptual idea to a fully engineered solution demands substantial resources, time, and infrastructure.

In the case of the in-space economy, this dependence is particularly pronounced due to the need for systems that ensure reliability, autonomy, and adaptability to the extreme conditions of the extraterrestrial environment—including microgravity, radiation exposure, and wide temperature fluctuations.

At the same time, the number of companies classified as being in the Active and Demonstrated stages comprises only about 11.3% of the total. Notably, 39 out of the 48 active-stage companies belong to auxiliary and service-oriented sectors, such as educational, analytical, legal, marketing, logistics, and IT infrastructure services. This underscores the limited number of mature technological solutions and their practical implementation. It reflects the immaturity of the sector, which has not yet transitioned into a phase of scalable and commercially reproducible operations. Many projects remain either pilot systems or demonstration missions intended to validate the viability of fundamental technological components.

Special attention should be paid to the number of projects classified as dormant and cancelled, which together account for 17.6% of all registered companies. This points to significant structural risks within the sector. Among the main contributing factors are financial instability, high technical risk, regulatory uncertainty, and insufficient coordination among stakeholders in the domain of international space governance.

The fact that only one company has been recorded in the acquired and retired categories highlights the very low level of consolidation and lifecycle completion within the sector. The near-total absence of mergers and acquisitions may be attributed not only to the technological immaturity of the market but also to the fact that most companies remain focused on fundamental research and engineering development. They have not yet reached a stage of sustainable market differentiation, where strategic acquisitions or consolidations typically occur.

Private sector and key companies

Amid increasing governmental activity in major spacefaring nations, the private sector is playing an increasingly prominent role. It views extraterrestrial resource development not only as a technological challenge but also as a promising avenue for commercialization.27–29 The previously discussed initiatives aimed at developing national legal frameworks, along with the creation of technological prototypes and growing interest from the scientific community, are fostering favorable conditions for the influx of venture capital, corporate investment, and the formation of startup ecosystems.

Against this backdrop, particular attention should be given to the Space Resources sector, which includes companies engaged in the exploration, extraction, and processing of natural materials on the Moon, asteroids, and other celestial bodies within the Solar System. As of early 2025, this sector comprises 110 registered companies, displaying a high degree of diversity in terms of development stages. This makes the group a representative sample for evaluating the sector’s maturity and its potential for transition toward a multi-planetary industrial economy.

The following section will present selected examples of private initiatives operating in this domain.

The first attempts to commercialize extraterrestrial resource extraction were undertaken by Planetary Resources and Deep Space Industries (DSI), both founded in the early 2010s. Planetary Resources focused on the development of small satellites for asteroid prospecting. However, in 2018, the company was unable to secure additional funding and was subsequently acquired by the blockchain firm ConsenSys later that year, which resulted in a shift in its core business focus. DSI, meanwhile, was acquired by Bradford Space in 2019.

Contemporary space mining companies demonstrate a diverse range of approaches and technologies:

– AstroForge: a U.S.-based startup founded in 2021, specializing in the extraction of platinum-group metals (PGMs) from asteroids. According to Seedtable, a platform aggregating data on technology startups and investments, AstroForge raised $13 million in seed funding in 2022 and secured an additional $40 million in Series A financing in 2024 (the second stage of venture capital funding). The company’s stated goal is to become the first commercial entity to mine PGMs from asteroids, utilizing proprietary technologies.

To date, AstroForge has conducted two launches:

Brokkr-1 Mission (April 2023)—the company’s first demonstration satellite, launched aboard a SpaceX Falcon 9 rocket. The mission aimed to test asteroid material processing technologies under microgravity conditions. However, it encountered technical difficulties, including communication failures and issues with solar panel deployment, which prevented the mission from achieving its primary objectives. Odin Mission (February 2025)—targeted the asteroid 2022 OB5. The goal was to obtain spectroscopic imagery of the asteroid to support planning for future extraction activities. Nevertheless, contact with the spacecraft was lost within less than 24 h after launch due to communication problems, leading to the mission being declared unsuccessful.

The company’s upcoming third mission, Vestri, scheduled for 2026, aims to land on a metallic asteroid and demonstrate in situ metal extraction and processing technologies. This will mark the first attempt by a commercial entity to perform resource extraction directly on an asteroid.

– TransAstra is developing an “optical mining” technology that utilizes concentrated sunlight to heat and vaporize volatiles from asteroids and lunar regolith. The company has received funding from NASA under the NIAC (NASA Innovative Advanced Concepts) program and is currently preparing a technology demonstration. TransAstra actively collaborates with NASA, the United States Space Force, and other governmental and private entities. The company has secured investment from Y Combinator, Helium-3 Ventures, and other investors, and has won multiple grants, including Small Business Innovation Research and Small Business Technology Transfer awards. TransAstra’s developments include the Worker Bee space tug, the Sutter telescope system, and the Mini Bee debris capture system.

– OffWorld is developing and deploying autonomous robotic systems with artificial intelligence for mining operations in extreme, unstructured environments, both on Earth and in space. In collaboration with the ESA and the Luxembourg Space Agency, the company is designing systems for the extraction and storage of oxygen and hydrogen from lunar regolith, with a demonstration mission planned for 2027.

OffWorld has developed a suite of autonomous robotic platforms, including the Surveyor, Excavator, Collector, Hauler, Dozer, and Micro Fractor, each designed to perform specific functions—ranging from mapping and exploration to material transport and processing.

– Moon Express is a private American aerospace company founded in 2010 and headquartered at Cape Canaveral, Florida. The company views the Moon as Earth’s “eighth continent” rich in valuable resources such as water, helium-3, platinum, and others. Its mission is to harness these resources to support life on Earth and enable future space missions. Moon Express has announced three key missions:

Lunar Scout—the first commercial mission to the Moon, carrying a diverse set of payloads, including the International Lunar Observatory; Lunar Outpost—the establishment of the first commercial research station at the Moon’s south pole aimed at prospecting for water and mineral resources; Harvest Moon—the first commercial sample return mission to bring lunar material back to Earth for scientific and commercial purposes.

– ispace is a Japanese company with offices in Tokyo, Luxembourg, and Denver, specializing in the development of robotic lunar landers and rovers for commercial lunar missions. The company has set an ambitious goal: to establish a lunar settlement with a population of approximately 1,000 people by 2040, and to support up to 10,000 annual visitors. ispace views the Moon as a critical component in the advancement of the space economy and the long-term sustainability of humanity.

– Asteroid Mining Corporation (AMC) is a UK-based company founded in 2016, focused on developing technologies for asteroid resource extraction. The company’s objective is to become the first profitable enterprise in the space resource sector by commercializing robotics for both terrestrial and space applications.

AMC’s flagship projects include:

Space Capable Asteroid Robotic-Explorer—a six-legged robotic platform designed for exploration of asteroids and the lunar surface, capable of navigating complex and irregular terrain; Asteroid Prospecting Satellite One—a planned satellite mission for spectral analysis of near-Earth asteroids aimed at identifying potentially valuable targets for resource extraction.

According to Space Capital, the total investment in space startups reached $12.5 billion in 2023, of which less than 5% was allocated to infrastructure segments, including resource extraction. The primary deterrents for investors remain the extended return-on-investment timelines and significant technological risks. Expert assessments suggest that commercial space mining operations may not reach break-even before 15–20 years after project initiation.

Primary Sources of Space Resources and Existing Strategies for Their Utilization

The development of interplanetary infrastructure largely depends on the ability to utilize resources located beyond Earth. Currently, the main accessible sources of space resources are considered to be asteroids, comets, and the Moon.30,31

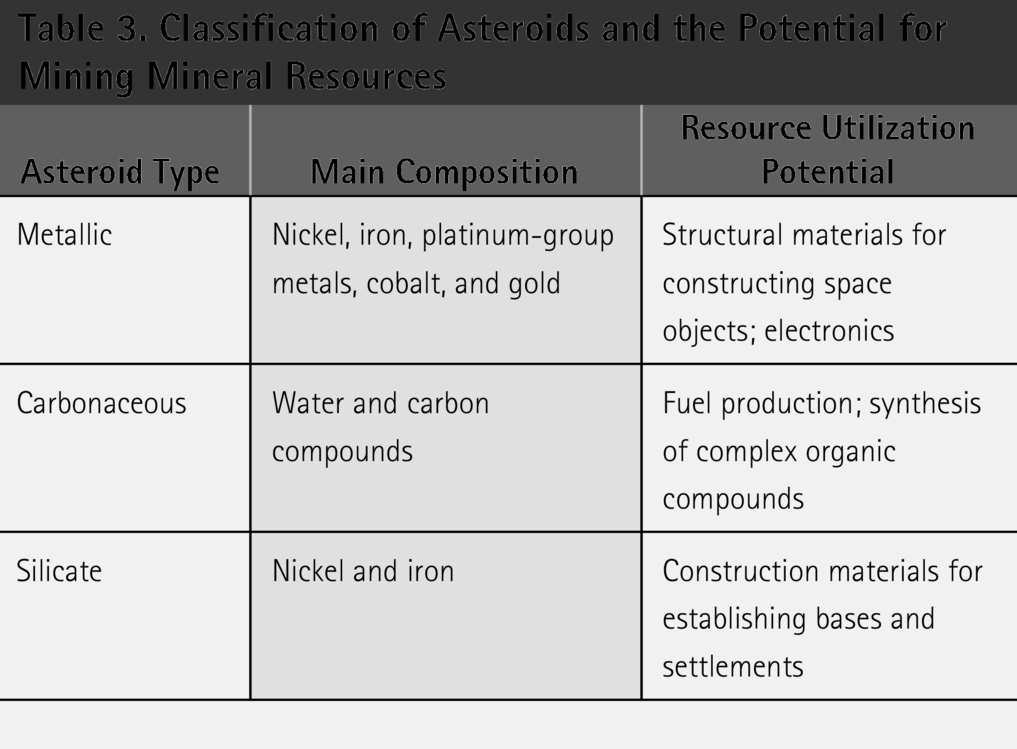

Asteroids represent one of the most promising targets for mining mineral resources. They are classified by composition into metallic, carbonaceous, and silicate types:32,33

Metallic Asteroids (M-type): Rich in iron and nickel, as well as containing PGMs. These materials can be used for constructing structures in the space environment and for subsequent processing at orbital or planetary facilities. Carbonaceous Asteroids (C-type): Contain organic compounds and water in the form of hydrates. Water is a key resource for producing rocket fuel via electrolysis and for supporting the life systems of future space settlements. Silicate Asteroids (S-type): Composed mainly of rocky materials (e.g., olivine, pyroxene) along with nickel–iron metals.

Potential utilization of resources from these asteroids is presented in Table 3 .

Classification of Asteroids and the Potential for Mining Mineral Resources

The Moon possesses significant potential for resource extraction, particularly in its polar regions, where deposits of water ice have been discovered in permanently shadowed craters. Its surface is covered with regolith, which also contains various metals and oxides suitable for further processing to create construction materials for lunar bases and orbital structures.

Of the listed sources, comets currently present the least interest for resource extraction. Due to the high eccentricity of their orbits, reaching them requires higher velocities compared to missions to asteroids. The continuous outgassing of gas and dust on comets poses threats to spacecraft systems and complicates navigation. However, despite these challenges, comets also serve as a source of water and other important resources, making them potentially valuable and viable for future space missions and research.

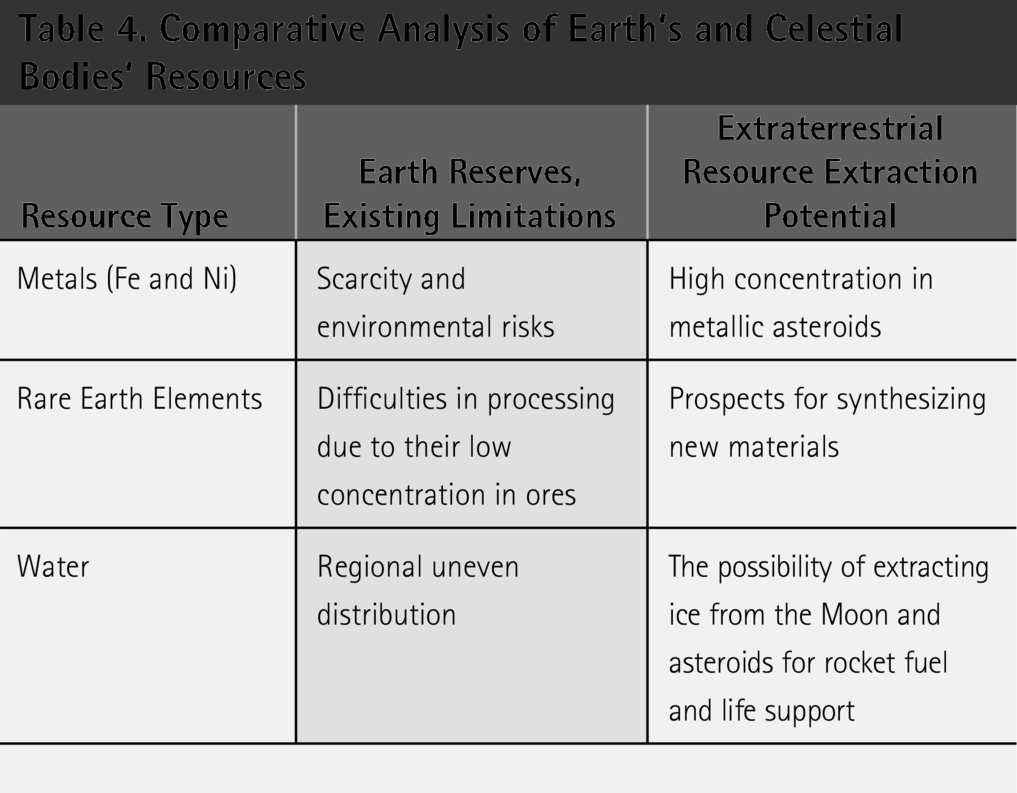

Table 4 presents the main limitations of resource extraction on our planet compared to the extraction potential available on celestial bodies.

Comparative Analysis of Earth’s and Celestial Bodies’ Resources

Given the above, it can be concluded that the potential for resource extraction from celestial bodies is quite vast, though it is important to note our current (human) technological limitations. Overcoming these limitations in the coming decades will allow us to confidently develop this new direction—industrial space mining.

In the scientific literature, two main approaches to the utilization of resources mined in the space environment are identified: ISRU, in which resources is used directly to create and maintain space infrastructure, and the transportation of resources to Earth, where the mined materials are delivered to our planet and processed using traditional methods. Each of these strategies has its own advantages as well as specific technological and logistical requirements.

The concept of on-site resource utilization (directly in space) involves the immediate application of extracted materials for the construction and maintenance of space objects, such as orbital stations, lunar bases, asteroid settlements, or infrastructure for interplanetary travel. The advantages of this approach include:

Reduction in transportation costs: Since resources remain at the extraction site, there is no need for costly launches and the subsequent return of materials to Earth. Sustainability of space infrastructure: Utilizing resources directly in the space environment contributes to the development of self-sustaining systems. For example, lunar regolith can be processed into construction blocks using 3D-printing technologies, and water extracted from asteroids or lunar ice can be used to produce rocket fuel via electrolysis.

The second approach involves transporting the extracted resources back to Earth to replenish resource shortages or for use in high-tech industries. The key aspects of this strategy include economic benefits (e.g., the high value of certain PGMs may justify the transportation costs), diversification of the resource base (to create a strategic reserve as Earth’s continental and submarine resources are depleted), and the stimulation of new sectors and technologies.

The choice between ISRU and transporting resources back to Earth depends on numerous factors, including economic viability, technical feasibility, environmental risks, and the ultimate purpose of these resources. In the long term, integrating both strategies may prove to be the most optimal solution. In the initial stages, while ISRU technologies are still under development, the transportation of high-value resource components will serve as an incentive for investment in space mining and further optimization of logistical processes. Once space technologies have sufficiently advanced, the ISRU concept will enable the creation of self-sustaining bases capable of supporting interplanetary missions and reducing reliance on resource and equipment supplies from Earth.

DISCUSSION

As we approach the 2030s, a qualitatively new phase in the development of the extraterrestrial resource extraction industry is taking shape. While previous decades were dominated by theoretical studies and experimental initiatives, the coming years are expected to mark a transition toward the first practical operations capable of demonstrating the applied value and technical feasibility of space resource utilization. A critical prerequisite for this transition is the successful implementation of technology demonstration missions aimed at validating key components of the future production chain—from resource prospecting to in situ extraction and initial processing.

In the coming years, a number of missions are planned that have the potential to establish the technical and resource foundations for subsequent commercial initiatives. In the coming years, a number of missions are planned that have the potential to establish the technical and resource foundations for subsequent commercial initiatives. One of the upcoming projects implemented within the framework of NASA’s programs is the Draper APEX (Artemis Payload and Experiment) 1.0 mission, scheduled for 2027. Operations in the Schrödinger Basin crater are expected to yield the first seismic and geophysical data from the far side of the Moon, laying the groundwork—including for future resource prospecting and extraction.

It is also worth noting the VIPER (Volatiles Investigating Polar Exploration Rover) mission, intended for the study of lunar polar ice (canceled by NASA in July 2024 before reaching the stage of implementation 34 ), and the PRIME-1 (Polar Resources Ice Mining Experiment-1) mission (which envisaged drilling regolith and extracting lunar water ice, but ended without obtaining samples due to the lander’s overturn)—as examples of early technological solutions that played an important role in shaping engineering approaches, testing landing platforms, and in the establishment of the regulatory and organizational framework for future operations.

In parallel with lunar initiatives, efforts are also underway to return samples from small bodies of the Solar System: NASA’s OSIRIS-REx (Origins, Spectral Interpretation, Resource Identification, Security, Regolith Explorer) and JAXA’s Hayabusa2 have successfully returned asteroid samples to Earth, providing invaluable data on the composition of extraterrestrial materials and offering critical insights into the nature and accessibility of off-world resources.

By the end of the decade, prototype production facilities are expected to be deployed on the lunar surface. As part of China’s Chang’e-8 mission and the international Artemis Base Camp project, demonstrations are planned for technologies enabling oxygen extraction from regolith and, potentially, pilot-scale harvesting and processing of water ice. These activities aim not only to advance ISRU concepts and infrastructure but also to strengthen investor confidence by showcasing tangible progress.

One of the indicators of the sector’s maturity will be the signing of the first commercial contracts for the supply of extraterrestrial resources. It is anticipated that by 2035, the first transaction may be concluded not within the framework of a demonstration mission, but for practical purposes.

Nevertheless, the continued advancement of the industry will depend on the establishment of a robust international legal framework. By 2030, the number of countries adhering to agreements analogous to the Artemis Accords is expected to increase, alongside parallel efforts—potentially under the auspices of the United Nations—to develop universal legal norms. These may include mechanisms for the registration of off-world operations or systems for the equitable distribution of resource rents. As noted in the preceding section, such developments are foundational for the long-term stability of the extraterrestrial economy, helping to mitigate legal uncertainties that currently constrain large-scale investment.

Against the backdrop of rapid technological advancement, international competition in the field of extraterrestrial resource development is expected to intensify. The United States will likely strive to maintain its technological leadership in this domain. However, China—rapidly advancing its lunar program and aiming to construct a lunar base by 2035—is emerging as a formidable competitor and an alternative hub for innovation in space resource utilization. The formation of technological alliances is likely to lead private companies to align themselves with national or multilateral initiatives within such blocs.

At the same time, other nations are actively developing their own extraterrestrial mining strategies. India has expressed interest in the potential use of helium-3 for energy production and is exploring participation in lunar exploration programs. Australia, with its well-developed mining industry, is working together with NASA (within the framework of the Commercial Lunar Payload Services program) to develop the semi-autonomous rover Roo-ver, which is intended to collect lunar soil samples.

Given these developments, the emergence of the first commercial operations will inevitably require a range of auxiliary services—from mission insurance to legal frameworks for ownership rights over extracted resources. In the foreseeable future, legal precedents may arise from disputes between governmental and private entities, contributing to the evolution of jurisprudence in this emerging industry. Concurrently, specialized infrastructures will likely develop to support risk insurance and legal facilitation of transnational transactions involving space resources.

In the coming decades, the foundational elements of a fully developed extraterrestrial mining industry are expected to emerge. The reduction in launch costs—primarily due to the proliferation of reusable rocket systems—combined with the growing momentum of lunar missions, will significantly enhance the logistical accessibility of the Moon and nearby asteroids. It is anticipated that by that time, at least one experimental extraction unit will be operational either on the lunar surface or on an asteroid, with small quantities of resources such as water, oxygen, and regolith being utilized directly in space.

Despite the still limited volumes and relatively modest financial scale (estimated at $2–4 billion), humanity faces a critical qualitative shift: from exploratory missions to the formation of an emerging commercial ecosystem. According to various agency projections, if demonstration missions prove successful, the total value of the space economy could reach $1.0–2.7 trillion by the 2040s, with a substantial portion linked to the use of off-Earth resources—for supporting lunar bases, orbital logistics, and space-based energy generation.

Therefore, in the short term, the key indicators of success will not be purely financial, but rather the achievement of technological milestones, the establishment of commercial precedents, and the expansion of international participation. The presence of private entities on the lunar surface by 2028–2030 would mark a pivotal moment, signaling the birth of a new industry capable of transforming not only the space economy but also global industrial supply chains on Earth.

CONCLUSION

In summary, the exploration of space resources in the foreseeable future not only addresses the practical challenges of today associated with the depletion of Earth’s subsurface resources but also lays the foundation for a further evolutionary leap, the emergence of humanity as a multi-planetary species.

An analysis of Earth’s evolutionary processes, cosmic risks, and the great filter hypothesis leads to the conclusion that multi-planetary expansion is critically necessary for the long-term survival of our civilization. The implementation of this strategy requires not only the exploration of space but also the establishment of a resource base through the mining of celestial bodies.

As demonstrated in the sections on the Kardashev scale and energy strategy, extraterrestrial resource extraction is not merely a technological domain, but a cornerstone in the transition toward a multi-planetary civilization. The utilization of resources from the Moon, asteroids, and other celestial bodies provides the foundation for establishing autonomous infrastructure beyond Earth. This, in turn, breaks the critical dependency on planetary supply chains, reduces operational costs, and enhances the resilience of missions to Mars, asteroids, and beyond.

ISRU systems, which employ locally sourced materials to produce fuel, water, oxygen, and construction components, are essential for enabling long-duration human presence off Earth. These systems form a critical part of the logistical architecture for future interplanetary expeditions. Without extraterrestrial mining, the very concept of multi-planetary expansion becomes economically and technically unsustainable.

However, it is important to emphasize that this path demands not only technological progress but also a profound reevaluation of the worldview of modern society. Courage in embracing new challenges and the ability to adapt to changing conditions are key to our survival and long-term prosperity. This is why the strategic exploration of space becomes an integral part of the global agenda, uniting scientific, economic, and cultural interests in a shared pursuit of a sustainable future.

Thus, the development of new methods or the integration of traditional mining techniques with space technologies represents a promising direction capable of ensuring the continued growth of our civilization and its transition to a new level of development. In this context, multi-planetary expansion emerges not only as a technical challenge but also as an essential condition for the further evolutionary advancement of humanity, ensuring the long-term survival of our species.

AUTHOR’S CONTRIBUTIONS

A.K.K. is the sole author and contributor. He performed all data curation, formal analysis, conceptualization, investigation, and project administration.

Footnotes

AUTHOR DISCLOSURE STATEMENT

The author has declared that no competing interests exist, and all relevant data are within the article. The author declares that they are primarily involved in education and academic research and are not directly supported by the government.

FUNDING INFORMATION

No funding was received for this article.